E-Compass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

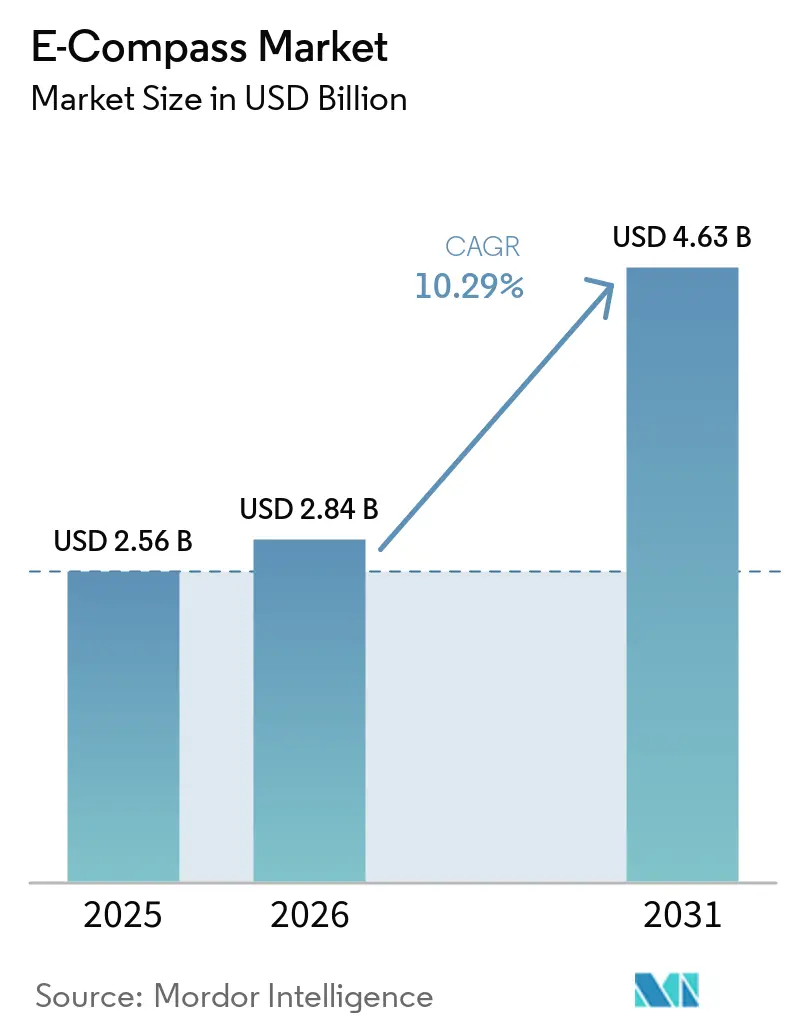

| Market Size (2026) | USD 2.84 Billion |

| Market Size (2031) | USD 4.63 Billion |

| Growth Rate (2026 - 2031) | 10.29% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

E-Compass Market Analysis by Mordor Intelligence

The E-Compass market size is projected to be USD 2.56 billion in 2025, USD 2.84 billion in 2026, and reach USD 4.63 billion by 2031, growing at a CAGR of 10.29% from 2026 to 2031. Rapid migration from Hall-effect to tunneling magneto-resistive (TMR) architectures in smartphones and vehicles, broader use of multi-sensor fusion in advanced driver-assistance systems, and early field trials of quantum compasses that maintain heading accuracy without magnetic calibration are shaping demand. Middle East sovereign electronics programs, Asia-Pacific’s depth in MEMS manufacturing, and North America’s aerospace and defense requirements continue to diversify regional revenue streams. Suppliers are blending hardware miniaturization with machine-learning calibration to offset urban interference, while pricing pressure in consumer tiers is driving a pivot toward automotive, industrial, and medical applications that support higher average selling prices.

Key Report Takeaways

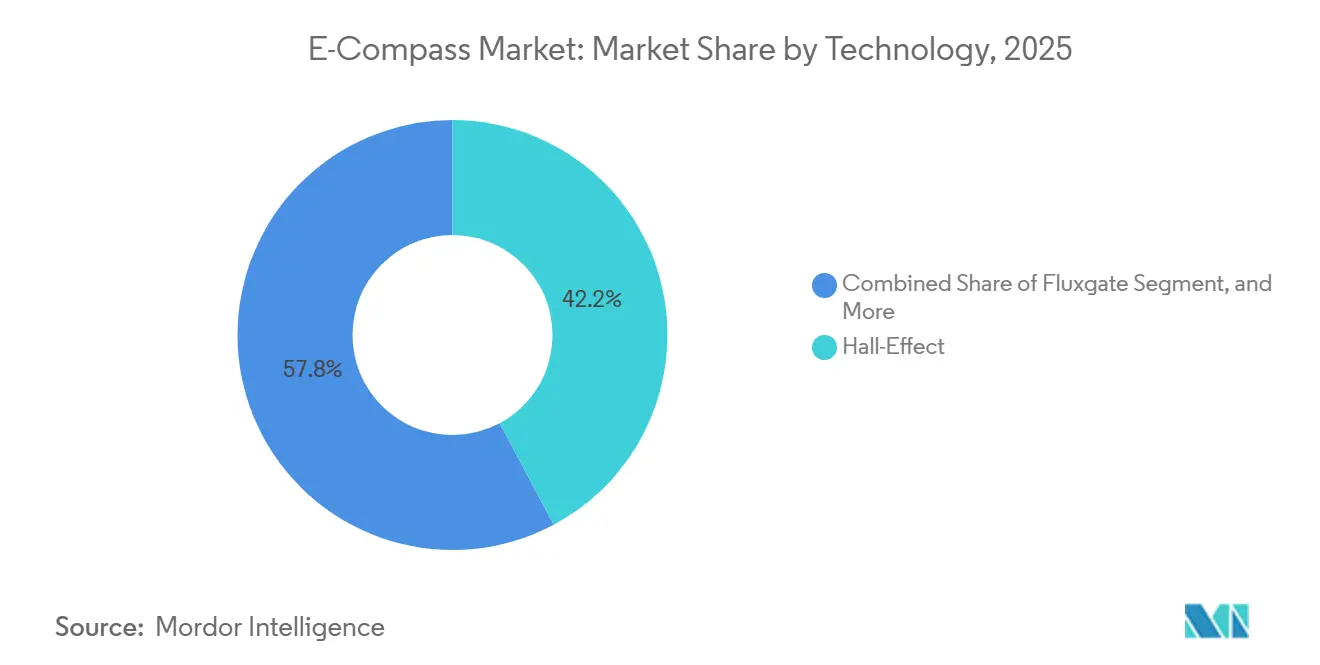

- By technology, tunneling magneto-resistive sensors led the E-compass market with 42.19% of 2025 revenue, while quantum compasses are projected to advance at a 10.99% CAGR through 2031.

- By axis orientation, 3-axis devices accounted for 61.18% of shipments in 2025, whereas 6-axis and 9-axis devices are forecast to grow at 10.57% over 2026-2031.

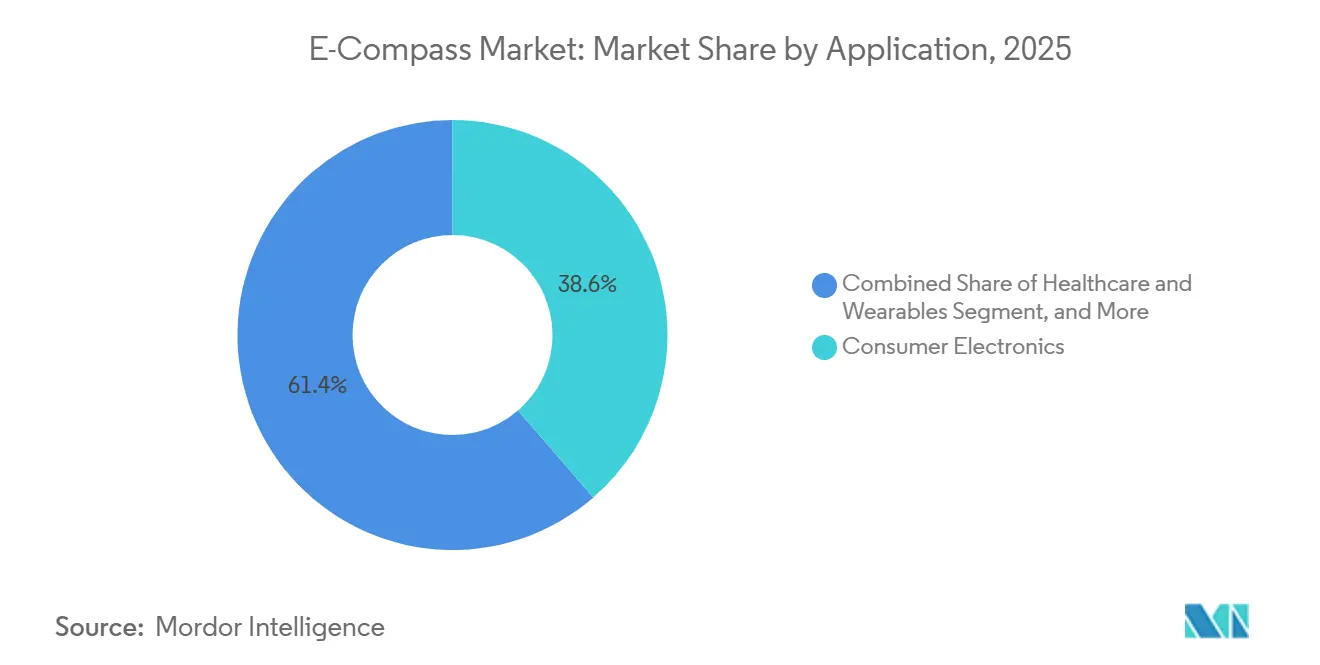

- By application, consumer electronics accounted for 38.63% of demand in 2025, yet healthcare wearables are the fastest-growing use case, with a 10.64% CAGR to 2031.

- By form factor, integrated sensor-combo modules captured 47.77% of 2025 revenue, and system-on-chip embedded compasses are expanding at 10.78% through 2031.

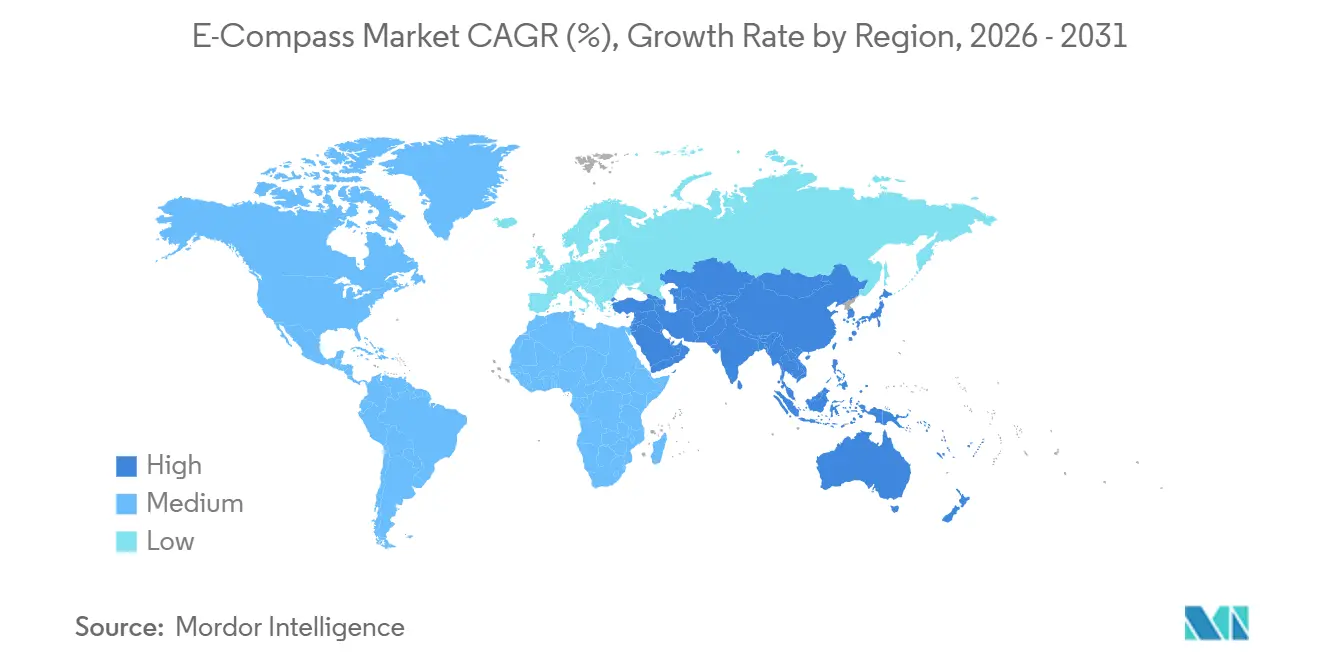

- By geography, in the E-compass market, Asia-Pacific retained 48.79% of the 2025 value, while the Middle East is expected to post a 19.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global E-Compass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Smartphones Integrating Navigation Sensors | +2.8% | Global, with concentration in Asia-Pacific manufacturing hubs (China, South Korea, Vietnam) | Short term (≤ 2 years) |

| Rising Adoption of ADAS in Passenger and Commercial Vehicles | +2.5% | North America, Europe, China (automotive production centers) | Medium term (2-4 years) |

| Miniaturization and Cost Reduction Through MEMS Processes | +1.9% | Global, led by Asia-Pacific foundries (Taiwan, Japan, South Korea) | Medium term (2-4 years) |

| Expansion of Wearable and XR Devices Demanding Ultrathin Compasses | +1.6% | North America and Europe (early adopters), Asia-Pacific (manufacturing) | Medium term (2-4 years) |

| Autonomous Maritime Drones Needing Tilt-Compensated Heading | +0.9% | North America, Europe, Middle East (defense and commercial maritime) | Long term (≥ 4 years) |

| Precision-Agriculture Robots Deploying Row-Guidance E-Compass Arrays | +0.6% | North America, Europe, Australia (large-scale commercial farming) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Smartphones Integrating Navigation Sensors

Smartphone subscriptions stood at 6.9 billion in 2025, and virtually every mid-tier or flagship handset embeds a 9-axis sensor hub that blends magnetometer, accelerometer, and gyroscope data for augmented-reality overlays and indoor navigation.[1]IEEE Xplore, “Multi-Sensor Fusion for Smartphone Indoor Navigation,” ieee.org Integrated combo modules trimmed bill-of-material cost by 25% and enabled sub-1 millimeter package heights suitable for foldable displays.[2]STMicroelectronics, “Sub-Millimeter Navigation Sensors for Foldables,” st.com Pedestrian dead-reckoning in subways and malls now depends on magnetometer-driven heading when GNSS is unavailable. Asahi Kasei’s AK09974C, released in October 2025, achieves 0.15 µT resolution in a wafer-level 1.2 × 1.2 mm package, showcasing aggressive miniaturization.[3]AK Mikrodevices, “AK09974C Ultra-Miniature 3-Axis Magnetic Sensor,” akm.com Because fewer than 40% of users perform manual figure-eight calibration, vendors are building auto-calibration based on machine-learning models harvested from millions of motion traces.

Rising Adoption of ADAS in Passenger and Commercial Vehicles

Advanced Driver Assistance Systems (ADAS) were shipped in 45% of new passenger vehicles in 2025, and each Level 2+ platform includes at least one 6-axis or 9-axis inertial measurement unit to meet ISO 26262 functional-safety requirements. Magnetometers within these IMUs correct gyroscope drift during prolonged highway driving, preventing cumulative heading error. TDK’s PositionSense, qualified to AEC-Q100 Grade 1 in 2024, now ships to European and Japanese OEMs, prepping 2027 model launches. Fleet operators add compass-equipped telematics boxes that shave 3-5% fuel through optimized routing, offsetting the USD 15-25 incremental sensor cost. Mandatory emergency braking and lane-keeping systems introduced in the European Union from 2024 onward continue to elevate accident rates.

Miniaturization and Cost Reduction Through MEMS Processes

Wafer-level packaging and through-silicon vias have reduced magneto-resistive die footprints by 60% since 2020. Taiwanese and Japanese foundries are moving analog front ends from 180 nm to 110 nm CMOS, cutting active current by 40% and die cost by 30%. Bosch Sensortec’s BMI423, shown at CES 2026, integrates a compass and 6-axis IMU in a 2.5 × 3.0 mm outline that draws 1.8 mA, half the power of prior discrete parts. Automated magnetic-field sweep testers now complete in under 2 seconds per die, lowering test costs from USD 0.08 to USD 0.03, savings passed on to entry-level phones. Asia-Pacific assembly plants enjoy labor and overhead below 15% of total cost, reinforcing regional supply dominance even amid tariff uncertainty.

Expansion of Wearable and XR Devices Demanding Ultrathin Compasses

Smartwatches, fitness trackers, and AR glasses shipped 320 million units in 2025, with 85% using 9-axis hubs for gesture detection, fall monitoring, and spatial audio. Power budgets in wrist-worn devices are limited to microampere levels, so magnetometer duty-cycle sampling is throttled to 10-25 Hz while accelerometers interpolate motion. XR headsets, including Meta Quest 3 and Apple Vision Pro, demand sub-degree accuracy for pinning virtual objects, driving custom fusion pipelines that blend magnetometer data, visual-inertial odometry, and depth cameras. Healthcare wearables add posture-aware sensing, lowering false cardiac-alert rates by 20% when body orientation is known. Suppliers are responding with 1 mm-thick chip-scale packages that fit beneath stacked batteries in next-generation wearables.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Susceptibility to Magnetic Interference and Calibration Drift | -1.4% | Global, acute in urban environments (North America, Europe, Asia-Pacific megacities) | Short term (≤ 2 years) |

| Commodity Pricing Pressure in Consumer-Grade Devices | -1.1% | Global, concentrated in Asia-Pacific consumer electronics supply chains | Medium term (2-4 years) |

| High Power Consumption in Fluxgate and Quantum Compass Designs | -0.7% | North America, Europe (aerospace, defense, research applications) | Long term (≥ 4 years) |

| Export-Control Limits on High-Sensitivity Fluxgate Modules | -0.5% | Middle East, Asia-Pacific (non-allied nations), South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Susceptibility to Magnetic Interference and Calibration Drift

Local ferrous objects and current loops create magnetic disturbances exceeding 500 µT, orders above Earth’s 25-65 µT field, causing heading errors beyond 30 degrees in phones, robots, and drones. Urban skyscrapers, subway rails, and factory motors exacerbate distortion. Only 60% of end users complete manual calibration, leaving a residual offset that degrades indoor navigation. Automotive systems mitigate drift by fusing GNSS and wheel-speed encoders, but stationary service robots must rely on lookup tables or periodically updated magnetic-anomaly maps. Asahi Kasei partnered with Aizip in December 2025 to crowd-source magnetic-field maps that shorten calibration cycles from days to hours.

Commodity Pricing Pressure in Consumer-Grade Devices

Average selling prices for 3-axis Hall and AMR compasses fell from USD 0.75 in 2023 to USD 0.48 in 2025 due to oversupply from Chinese MEMS foundries. Gross margins compressed to 25%, pushing vendors toward automotive and industrial tiers where margins remain above 30%. Smartphone OEMs increasingly demand single-vendor combo modules that drop board-level assembly expense by 15%, squeezing pure-play magnetometer suppliers. Smaller firms without automotive qualification face consolidation pressure; MEMSIC’s 2025 takeover of Crossbow Technology exemplified forced M&A for scale. New Southeast Asian entrants keep undercutting prices by 10-15%, perpetuating erosion and discouraging fundamental R&D.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: TMR Dominance Faces Quantum Disruption

Hall-effect, TMR sensors commanded 42.19% of 2025 revenue, anchored by sub-nanotesla sensitivity and thermal stability that meet AEC-Q100 and IEC 61508 norms for powertrain, avionics, and factory automation. The E-Compass market for TMR modules is set to grow at a steady, high-single-digit pace as carmakers and industrial integrators choose the architecture for long-life-cycle platforms. Hall-effect alternatives keep share in cost-constrained phones because their unit cost stays below USD 0.40, but their 10 µT noise floor caps accuracy at around 5 degrees, a ceiling that limits premium adoption. Fluxgate compasses deliver sub-degree precision for submarines and aircraft, but consume 50-200 mW, so they remain niche.

Quantum compasses using nitrogen-vacancy diamond or optically pumped alkali vapor cells are poised to grow at a 10.99% CAGR through 2031, the fastest in the E-Compass market, because they resist magnetic interference in defense and subsea environments where heading drift is unacceptable. A 2024 laboratory record showed 0.1-degree accuracy, and prototypes are undergoing trials on autonomous vehicles. Vendors such as Q-Nav are packaging diamond sensors with FPGA controllers that filter microwave drive noise, slimming form factors to 45 cm³. Governments fund pilot deployments despite 5-10× higher power draw, betting that unmanned underwater or space platforms will prioritize accuracy over battery life. Parallel R&D in chip-scale optically pumped vapor cells could shrink quantum modules to several cubic centimeters by 2030.

By Axis Orientation: Sensor Fusion Drives Multi-Axis Growth

Three-axis compasses still accounted for 61.18% of shipments in 2025 because they meet the cost ceilings for smartphones and drones and have well-understood legacy software stacks. E-Compass market share for single-axis and dual-axis units slipped to 12% as developers reject mechanical alignment constraints. Six-axis and nine-axis packages that integrate accelerometers and gyroscopes are forecast to rise 10.57% over 2026-2031, helped by automotive Tier-1 moves to single-system-in-package units that save 40% of board area and enable tightly coupled Kalman filters.

In the automotive domain, dual 9-axis setups provide redundancy to meet ISO 26262 compliance requirements, ensuring limp-home steering even if one sensor fails. Wearables exploit 9-axis hubs to recognize gestures and detect falls, as magnetometer data improves classifier accuracy by 15% when distinguishing rotation from translation. PNI Sensor’s RM3100-based NaviGuider bundles continuous hard-iron and soft-iron autocalibration, aimed at ocean gliders that cannot surface for manual routines. As downstream firmware unifies sensor-fusion libraries, manufacturers are transitioning from discrete compasses to integrated hubs that deliver quaternion vectors at 200 Hz directly to application processors, reducing development time.

By Application: Healthcare Wearables Outpace Consumer Electronics

Consumer electronics accounted for 38.63% of 2025 demand, driven by 1.3 billion smartphones and 320 million wearables shipped with navigation and gesture functions. Yet year-on-year growth has plateaued, pressing vendors to explore medical and industrial niches. Healthcare wearables are the fastest mover in the E-Compass market, expanding at a 10.64% CAGR thanks to continuous glucose monitors and arrhythmia patches that demand posture context to cut false alarms.

Automotive systems absorbed 28% of 2025 revenue as electronic stability control, lane-keeping, and automated parking proliferated. The E-Compass market in healthcare is gaining ground because FDA regulatory pathways for digital therapeutics now recognize inertial data as clinical evidence. In one 2025 clinical trial, posture-corrected glucose readings trimmed false hypoglycemia alerts by 22%, easily justifying a USD 2-3 sensor bill. Aerospace and defense relied on radiation-hardened fluxgate and emerging quantum modules for satellites, accounting for 18% of value, while industrial robotics and warehouse AGVs required tilt-compensated heading on sloped floors, accounting for about 12% of shipments. Marine customers insist on pressure-proof housings for 4,000-meter depths, a depth where Teledyne’s Compact Navigator couples a fiber-optic gyro and compass for 0.10-degree accuracy.

By Form Factor: SoC Integration Accelerates

Integrated sensor-combo modules accounted for 47.77% of 2025 form-factor revenue, as smartphone and wearable OEMs prefer single-vendor packs that cut board-level assembly labor by 15%. The E-Compass market size for system-on-chip embedded compasses is growing at 10.78% as mobile application processors absorb magnetometer front ends and sensor-fusion DSP blocks, enabling sub-6 mm z-height designs in foldable phones and tablets.

Discrete modules kept 32% share, favored by automotive and industrial engineers who value plug-and-play qualification cycles that decouple sensor upgrades from host redesigns. Development boards and custom ASICs accounted for 8% of revenue, serving research labs and defense primes that require radiation-hardening or bespoke performance envelopes. Asahi Kasei’s AK09974C in a 1.2 × 1.2 mm chip-scale package exemplifies miniaturization trajectories, allowing hearing aids and implantable pumps to integrate orientation sensing with negligible volume penalty. Tier-1 auto suppliers now request 3 × 3 mm multi-die modules that bundle a compass, accelerometer, gyroscope, and barometer, reducing the part count by 60% and simplifying ISO 26262 documentation.

Geography Analysis

Asia-Pacific accounted for 48.79% of the 2025 value, driven by China, Japan, and South Korea, which supply roughly 70% of the global Hall-effect and AMR dies. Despite the large E-Compass market share, regional players face margin compression because automotive qualification cycles stretch past 24 months and OEMs demand zero-defect supply. China absorbs 35% of local shipments through domestic phone and EV assembly, yet export restrictions on high-grade fluxgate and quantum sensors limit defense uptake, spurring indigenous firms like Bewis Sensing to fill the gap.

Japan and South Korea specialize in automotive-grade TMR and integrated IMU modules under long-term contracts with European and North American OEMs that guarantee volume until 2028. India is emerging as a leading electronics manufacturing hub, supported by electronics manufacturing incentives totaling USD 1.2 billion during 2024-2025, positioning the country as a low-cost alternative for consumer and industrial markets. The E-Compass market size in Asia-Pacific is expected to expand steadily but at slower margins than in Western regions.

The Middle East shows the fastest trajectory, slated for a 19.84% CAGR through 2031, as Saudi Vision 2030 drives local sensor production and defense programs procure ITAR-free navigation systems. Teledyne’s 2025 launch of its Dammam plant and KROHNE’s 2026 localization MoU underscore thee riseof regional supply chains. North America and Europe together accounted for 32% of 2025 revenue, driven by the aerospace, defense, and industrial robotics sectors, which demand radiation-hardened, tilt-compensated compasses. South America remained below 5%, but precision agriculture in Brazil and Argentina is prompting the adoption of GNSS-aided compass arrays for centimeter-level row guidance.

Competitive Landscape

The E-Compass market is moderately concentrated, with STMicroelectronics, Bosch Sensortec, TDK-InvenSense, Asahi Kasei, and Honeywell accounting for roughly 55% of 2025 revenue. Incumbents defend automotive and industrial positions with AEC-Q100 grade portfolios, 18-to-24-month validation pipelines, and multiyear supply contracts that smaller rivals struggle to match. STMicroelectronics’ February 2026 acquisition of NXP’s MEMS sensor assets for USD 950 million added accelerometers, gyroscopes, and magnetometers, making the firm the world’s second-largest MEMS vendor and reinforcing its bargaining power with Tier-1 customers.

Bosch Sensortec invests in on-chip sensor-fusion DSPs that output quaternions directly, stripping away host-processor overhead and shortening software integration for OEMs. TDK-InvenSense leverages its PositionSense TMR platform in tandem with AEC-Q100 Grade 1 IMUs to penetrate Level 2+ ADAS pipelines. Asahi Kasei differentiates through crowd-sourced magnetic-field mapping and sub-microminiature hearing aid packages. Honeywell and Analog Devices focus on high-reliability aerospace and industrial modules featuring radiation-tolerant design.

Start-ups such as VectorNav and PNI Sensor rely on edge-AI calibration co-processors that remove hard-iron and soft-iron offsets in real time. Chinese foundries receiving provincial subsidies undercut western peers by 10-15%, sparking price competition but also raising export-control concerns. Quantum-compass innovators backed by defense contracts are targeting sub-degree accuracy without magnetic calibration, a technology leap that could reset competitive hierarchies in the late 2020s. Standards bodies, including IEEE and IEC committees, are developing interference-immunity and calibration-drift test protocols, with STMicroelectronics and Infineon leading draft contributions.

E-Compass Industry Leaders

STMicroelectronics N.V.

Honeywell International Inc.

Robert Bosch GmbH (Bosch Sensortec GmbH)

Asahi Kasei Microdevices Corporation

NXP Semiconductors N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: STMicroelectronics completed the USD 950 million acquisition of NXP’s MEMS sensor business, unifying automotive-grade inertial and magnetic sensors under a single portfolio.

- February 2026: KROHNE signed a memorandum of understanding with Saudi Sensing to localize the supply of instrumentation for oil, gas, and petrochemicals, aligned with Vision 2030.

- January 2026: Bosch Sensortec launched the BMI5 IMU platform at CES, integrating a compass, a 6-axis IMU, and an on-chip fusion coprocessor with an active current of 1.8 mA.

- December 2025: Asahi Kasei partnered with Aizip to build a crowd-sourced magnetic-field map that cuts smartphone calibration intervals from days to hours.

Global E-Compass Market Report Scope

The E-Compass market refers to the global industry that designs, develops, manufactures, and commercializes electronic compass solutions that enable digital orientation, heading, and directional sensing across a wide range of electronic and industrial systems. E-compasses use magnetic sensing technologies to detect the Earth’s magnetic field and determine directional positioning, often integrated with accelerometers, gyroscopes, and sensor-fusion software to enhance navigation accuracy and motion tracking.

The E-Compass Market Report is Segmented by Technology (Hall-Effect, Anisotropic, Giant, Tunnel Magneto-Resistive, Fluxgate, Magneto-Inductive, and Quantum), Axis Orientation (1-2-Axis, 3-Axis, and 6- and 9-Axis Sensor-Fusion), Application (Consumer Electronics, Automotive, Aerospace and Defense, Industrial and Robotics, Marine and Sub-Sea, and Healthcare), Form Factor (Discrete Compass Modules, Integrated Sensor-Combo, SoC-Embedded E-Compass, and Dev-Boards and Custom ASICs), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Hall-Effect |

| Anisotropic, Giant, Tunnel Magneto-Resistive |

| Fluxgate |

| Magneto-Inductive |

| Quantum |

| 1-2-Axis |

| 3-Axis |

| 6- and 9-Axis Sensor-Fusion |

| Consumer Electronics |

| Automotive |

| Aerospace and Defense |

| Industrial and Robotics |

| Marine and Sub-Sea |

| Healthcare and Wearables |

| Discrete Compass Modules |

| Integrated Sensor-Combo |

| SoC-Embedded E-Compass |

| Dev-Boards and Custom ASICs |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Technology | Hall-Effect | ||

| Anisotropic, Giant, Tunnel Magneto-Resistive | |||

| Fluxgate | |||

| Magneto-Inductive | |||

| Quantum | |||

| By Axis Orientation | 1-2-Axis | ||

| 3-Axis | |||

| 6- and 9-Axis Sensor-Fusion | |||

| By Application | Consumer Electronics | ||

| Automotive | |||

| Aerospace and Defense | |||

| Industrial and Robotics | |||

| Marine and Sub-Sea | |||

| Healthcare and Wearables | |||

| By Form Factor | Discrete Compass Modules | ||

| Integrated Sensor-Combo | |||

| SoC-Embedded E-Compass | |||

| Dev-Boards and Custom ASICs | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large will the E-Compass market be by 2031?

The market is forecast to reach USD 4.63 billion by 2031, advancing at a 10.29% CAGR from 2026.

Which technology is gaining the fastest traction?

Quantum compasses based on nitrogen-vacancy diamond and optically pumped vapor cells are projected to grow at 10.99% through 2031.

Why is the Middle East growing faster than other regions?

Defense procurement independent of export controls and Vision 2030 localization plans drive a forecast 19.84% CAGR in the region.

What drives the shift toward multi-axis sensor fusion?

Automotive ISO 26262 redundancy needs and wearable gesture recognition favor 6-axis and 9-axis packages that integrate accelerometers and gyroscopes.

How are suppliers addressing magnetic interference in cities?

Vendors are embedding machine-learning auto-calibration that uses crowd-sourced magnetic-field maps to suppress drift without user intervention.

Is the market becoming more consolidated?

Yes, acquisitions such as STMicroelectronics’ 2026 purchase of NXP’s MEMS assets illustrate a trend toward scale, but over 45% of revenue still sits with smaller players.

Page last updated on: