Magnetometer Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

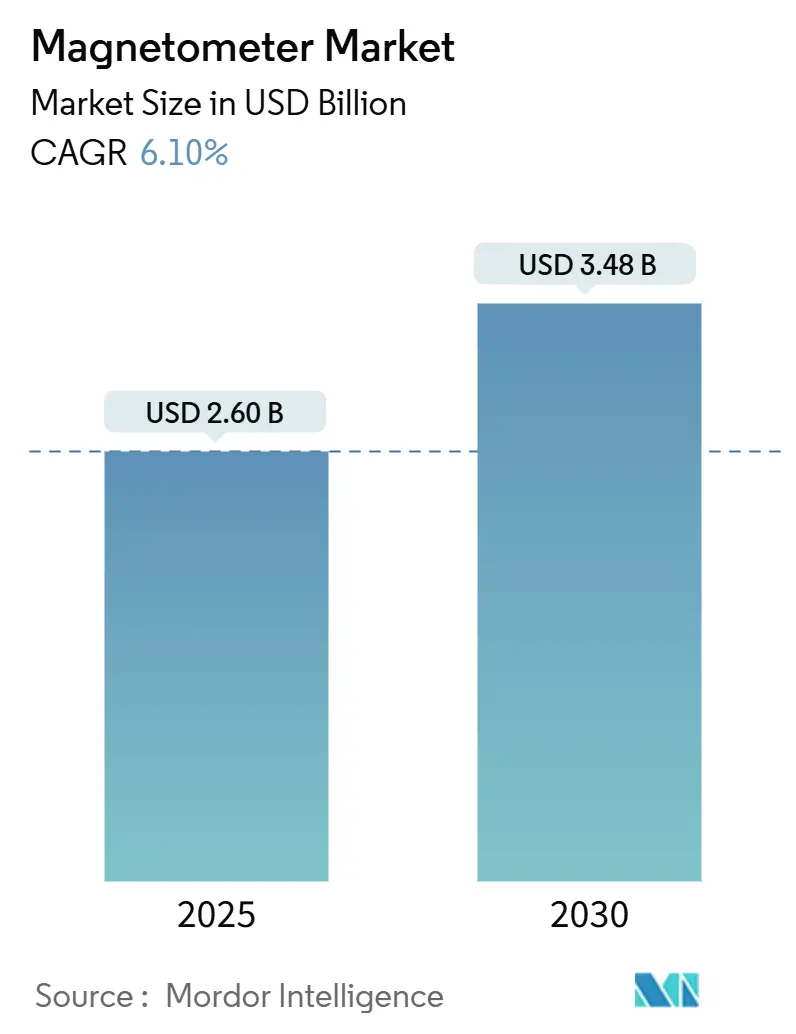

| Market Size (2025) | USD 2.60 Billion |

| Market Size (2030) | USD 3.48 Billion |

| Growth Rate (2025 - 2030) | 6.10% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Magnetometer Market Analysis by Mordor Intelligence

The global magnetometer market size reached USD 2.60 billion in 2025 and is forecast to attain USD 3.48 billion by 2030, reflecting a 6.1% CAGR over the period. Momentum stems from quantum-grade positioning systems that outperform conventional GPS backups, rapid adoption of 3-axis MEMS variants in consumer devices, and heightened demand for high-sensitivity sensors across autonomous navigation, mineral exploration, and subsea security programs. Vertical integration strategies, exemplified by Honeywell’s Civitanavi acquisition, are redefining competitive boundaries as suppliers race to secure rare-earth inputs and proprietary quantum sensing. Asia-Pacific currently anchors hardware production, yet North America is scaling fastest on the back of defense contracts that specify magnetic navigation redundancy. Meanwhile, optically pumped platforms are moving from laboratory prototypes to routine medical imaging, eliminating the cryogenics that once hindered clinical uptake.

Key Report Takeaways

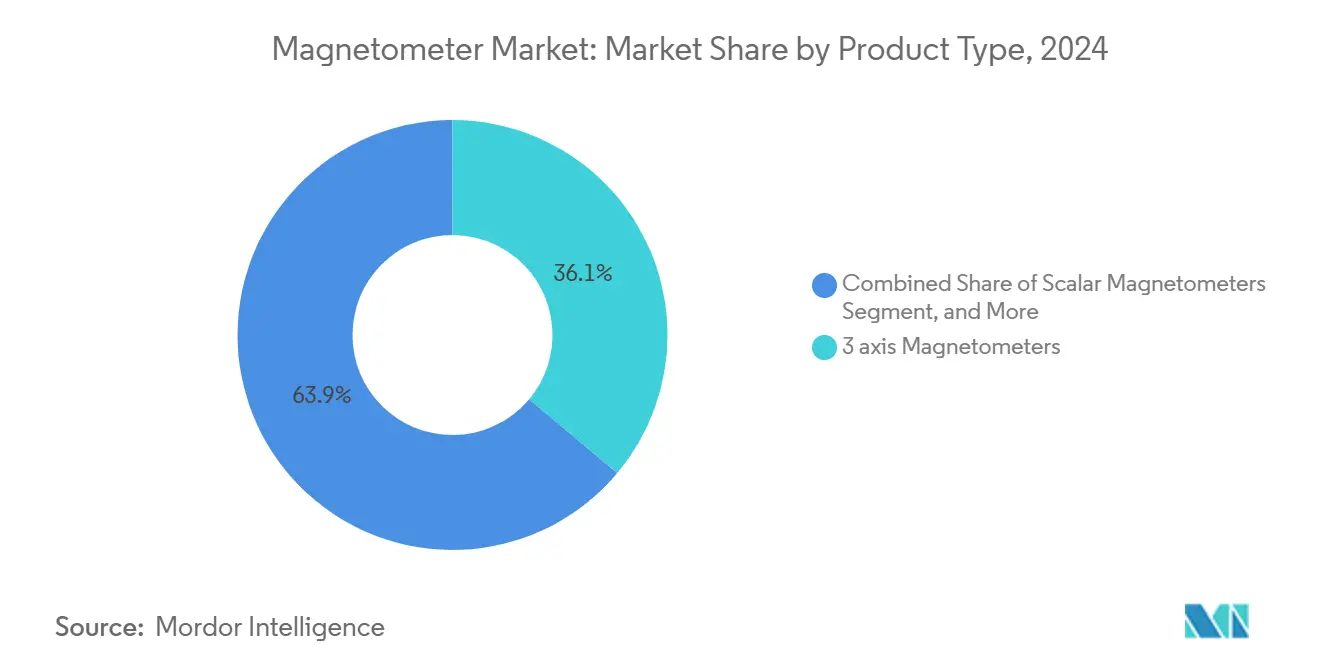

- By product type, 3-axis units held 36.1% of the magnetometer market share in 2024, while gradiometers are projected to expand at a 6.9% CAGR through 2030.

- By technology, Hall-effect devices led with 27.4% share in 2024; optically pumped systems are expected to advance at a 6.5% CAGR by 2030.

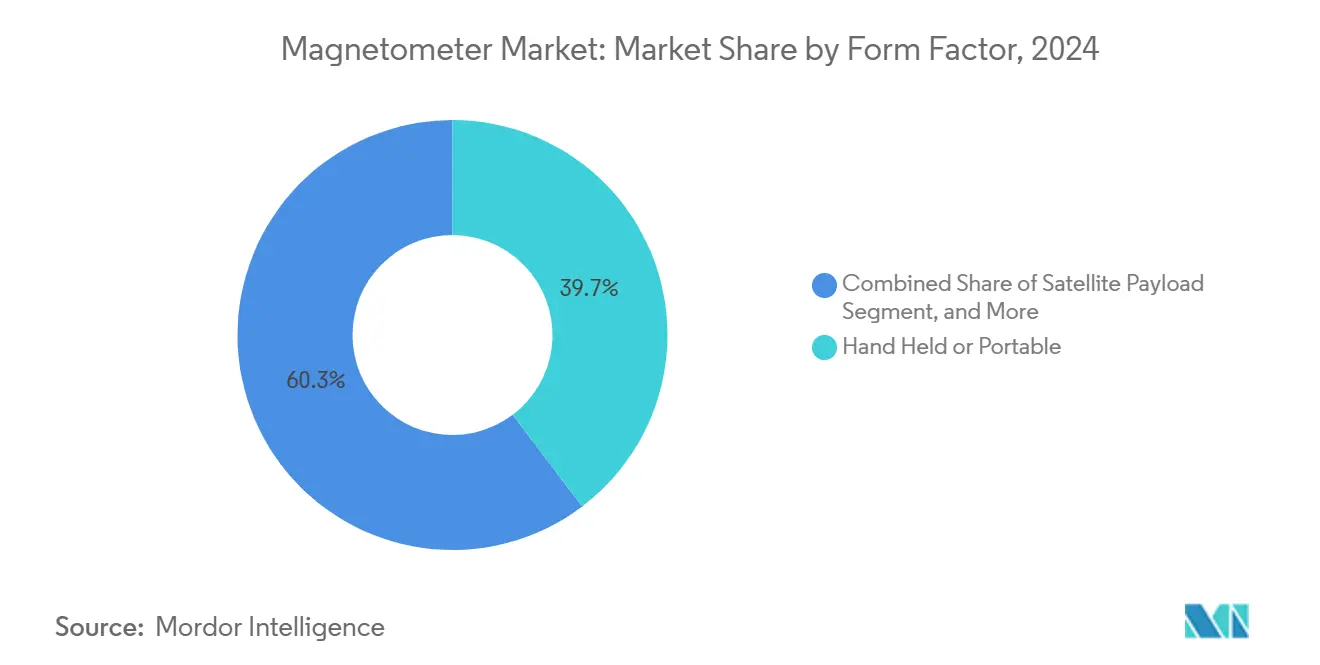

- By form factor, hand-held and portable versions accounted for 39.7% of the magnetometer market size in 2024, whereas satellite payload installations are rising at a 7.3% CAGR.

- By end-user industry, aerospace and defense captured 21.5% share of the magnetometer market size in 2024; automotive ADAS applications are pacing at a 6.8% CAGR to 2030.

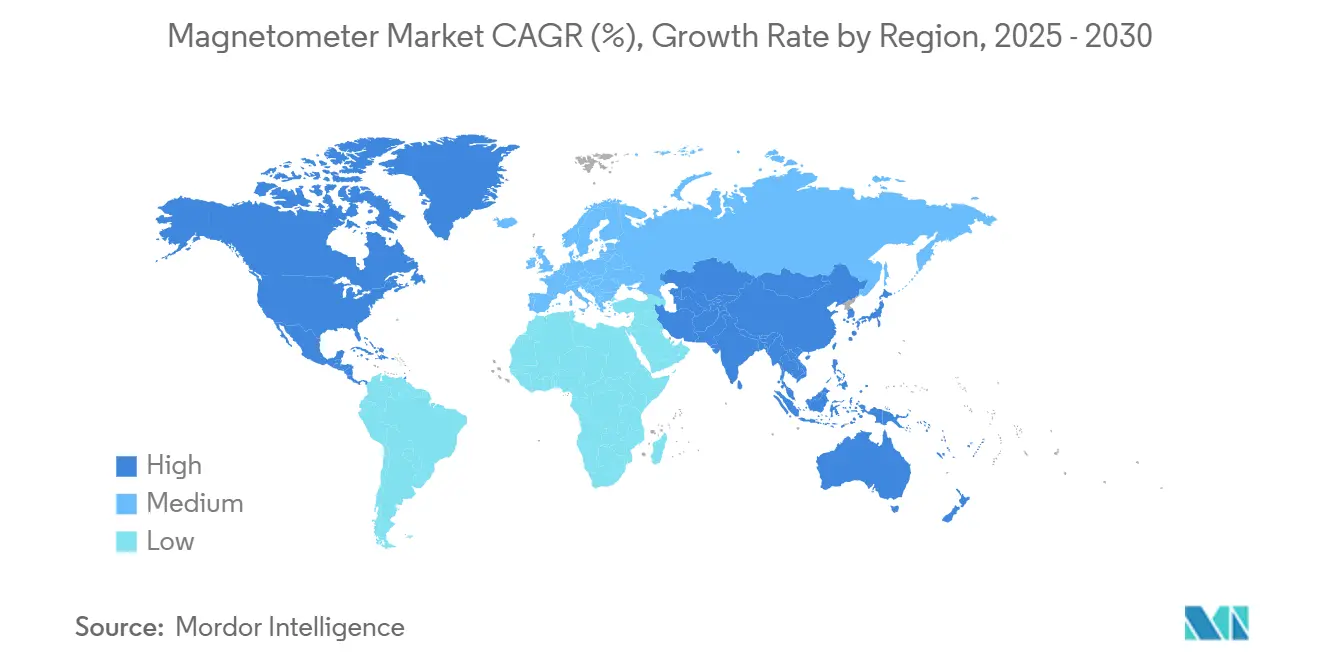

- By geography, Asia-Pacific commanded a 29.3% share of the magnetometer market in 2024, while North America records the highest regional CAGR at 7.9% through 2030.

Global Magnetometer Market Trends and Insights

Driver Imapct Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising adoption of 3-axis MEMS magnetometers in consumer electronics | +1.2% | Global with Asia-Pacific concentration | Short term (≤ 2 years) |

| Growing need for high-sensitivity magnetometers in autonomous navigation and ADAS | +1.5% | North America and EU extending to APAC | Medium term (2-4 years) |

| Expansion of geological mineral exploration activities for energy-transition metals | +0.8% | Australia, Canada, South America | Long term (≥ 4 years) |

| Under-sea magnetic anomaly detection for subsea infrastructure security | +0.6% | North Atlantic, Baltic, South China Sea | Medium term (2-4 years) |

| Integration of optically-pumped magnetometers with quantum-computing calibration | +0.9% | North America, Europe, select Asia-Pacific labs | Long term (≥ 4 years) |

| CubeSat demand for lightweight vector magnetometers for space-weather monitoring | +0.7% | North America and Europe space programs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of 3-Axis MEMS Magnetometers in Consumer Electronics

Smartphone and wearable designers now embed 3-axis MEMS units that achieve sub-degree compass accuracy after in-phone calibration, enabling seamless augmented-reality overlays. Sensor fusion of magnetometers, gyroscopes, and accelerometers has become a de facto feature in mid-tier devices, compressing board space and lowering power budgets. Manufacturing scale in Asia-Pacific has trimmed average selling prices, which accelerates the magnetometer market uptake across emerging economies. As tunnel magnetoresistance replaces legacy Hall-effect cores, designers obtain better temperature stability that supports all-weather navigation. Complementary firmware updates delivered over-the-air further fine-tune heading accuracy without hardware revisions, protecting OEM margins in a price-sensitive segment of the magnetometer market.

Growing Need for High-Sensitivity Magnetometers in Autonomous Navigation and ADAS

Quantum magnetometer arrays demonstrated positioning deviations under 22 m during 2025 flight tests, eclipsing traditional inertial systems as a fail-safe for GPS outages. U.S. defense contracts worth up to USD 106.2 million signal institutional confidence in magnetic-anomaly navigation, while ISO 26262 pushes automotive suppliers to adopt redundant magnetic paths within advanced driver assistance platforms. Urban canyon deployments benefit as magnetometers map baseline signatures that enable lane-level guidance when satellite visibility drops. AI engines resident in vehicle gateways now cross-check lidar and radar returns against magnetic patterns, cutting false-positive collision alerts. As regulatory deadlines for Level-3 automation near, Tier-1 suppliers view quantum-grade magnetometers as a route to differentiate reliability within the magnetometer market.

Expansion of Geological Mineral Exploration Activities for Energy-Transition Metals

Helicopter-borne magnetotelluric rigs cover 1,000 km² per day, allowing miners to fast-track lithium and copper scouting across remote basins.[1]Source: “New quantum-based navigation system 50 times more accurate than traditional GPS,” TechXplore, techxplore.comThe European Union underwrote a 26,700 km² Finnish critical-minerals survey in 2025, integrating airborne magnetometer data with machine learning to pinpoint subsurface anomalies.[2]Source: Nick Toscano, “EU-funded Deep-Rock Critical Minerals Hunt,” Sydney Morning Herald, smh.com.auBy reducing blind drilling, explorers cut environmental disturbance and capital costs, which expands budgets for high-density gradiometer grids. Diamond nitrogen-vacancy sensors now resolve nano-tesla anomalies at depth, enhancing the magnetometer market relevance in green-metal exploration. Financing packages increasingly specify quantum-ready magnetometer suites to future-proof survey capacity against deeper resource targets.

Under-Sea Magnetic Anomaly Detection for Subsea Infrastructure Security

NATO’s Baltic Sentry task force has deployed autonomous underwater vehicles that log continuous magnetic baselines around gas pipelines and telecom cables, achieving 2.5 s response times for anomaly alerts.[4]Source: NATO Naval Drone Fleet to Protect Undersea Infrastructure, Army Recognition, armyrecognition.com High-temperature superconducting magnetometers under a USD 18 million U.S. Navy contract detect mine casings at stand-off distances that traditional acoustic sonars miss. Signal-processing advances discriminate benign geologic signatures from man-made threats, which lowers false alarms and operational costs. Commercial operators now lease modular magnetometer pods for offshore wind-farm surveys, another growth node within the magnetometer market. Insurers increasingly require magnetic anomaly screening as a pre-condition for subsea asset coverage, formalizing demand.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Price erosion from commoditization of Hall-effect sensors | -0.8% | Global, especially Asia-Pacific | Short term (≤ 2 years) |

| Signal drift and calibration challenges in high-temperature environments | -0.5% | Heavy-industry clusters | Medium term (2-4 years) |

| Export-control restrictions on ultra-sensitive magnetometer technology | -0.7% | US-China corridors | Long term (≥ 4 years) |

| Rare-earth material supply constraints for fluxgate cores | -1.1% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Erosion from Commoditization of Hall-Effect Sensors

As 200 mm fabs optimize yield, entry-level Hall-effect dies sell for cents, compressing gross margins by up to 20% a year for legacy part numbers. Tier-one suppliers defend profitability by bundling on-chip DSP and ASIL-D diagnostics, yet copy-exact foundry clones in China challenge premiums. This deflation pressure pressures smaller players to pivot toward magneto-resistive or optically pumped niches with higher bill-of-materials value. Consumer OEMs welcome lower sensor prices, but ongoing price wars could slow innovation budgets across the broader magnetometer market.

Rare-Earth Material Supply Constraints for Fluxgate Cores

China’s April 2025 export license regime expanded lead times for dysprosium and neodymium alloys to 20–26 weeks, derailing European automotive production schedules. North American defense primes have invoked the Defense Production Act to prioritize local feedstock contracts, yet near-term capacity gaps persist. Research programs on iron-nitride composites show promise, though commercial volumes remain at least three years out. Meanwhile, magnetometer producers stockpile inventory, locking up working capital and adding volatility to the magnetometer market outlook.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Gradiometers Lead Precision Applications

The 3-axis category accounted for 36.1% of the magnetometer market share in 2024, favored for its ability to resolve complete field vectors in compact consumer and automotive modules. Magnetometer gradiometers booked the quickest revenue rise at a 6.9% CAGR, since they map differential field changes that unmask buried mineral seams and unexploded ordnance with superior clarity. Tensor configurations built with diamond quantum sensors now image nano-scale variations that scalar tools overlook, raising detection accuracy by 30% in nondestructive inspection trials.

Demand for vector and scalar instruments remains healthy in geophysics and scientific labs, though growth trails that of gradiometers. Single-axis devices still win cost-sensitive roles such as basic compass modules in smart locks. Integration of AI-driven pattern recognition with gradiometer arrays is shortening survey cycles and enabling automated anomaly classification, extending the addressable magnetometer market for turnkey geoscience services.

By Technology: Optically Pumped Systems Gain Medical Traction

Hall-effect stacks retained 27.4% revenue share in 2024, sustained by commodity pricing and deep design-in inertia among handset ODMs. However, optically pumped platforms are forecast to post a 6.5% CAGR through 2030 as cryogen-free magnetoencephalography reaches neurology clinics. Fluxgate architectures defend aerospace niches where thermal stability outweighs size, while SQUID arrays occupy ultra-low-noise laboratories despite their complexity.

Beijing’s nationwide rollout of SERF-based atomic scanners underscores commercial viability, with 20 hospital installations signed by 2024. Diamond quantum variants now register sub-10 pT sensitivity, positioning them for next-generation cardiac diagnostics. As automotive safety systems migrate from AMR to TMR stacks for better EMC margins, suppliers blend magnetoresistive dies with on-chip temperature graders. This diversification spreads risk and deepens the magnetometer market footprint across healthcare and transportation.

By Form Factor: Satellite Payloads Drive Miniaturization

Hand-held and portable units controlled 39.7% of the magnetometer market size in 2024, thanks to field geologists, security screeners, and plant-maintenance crews who value mobile diagnostics. CubeSat operators now spearhead growth: satellite payload installations are projected to log a 7.3% CAGR through 2030 as weather-monitoring constellations proliferate.

NASA’s TRACERS mission pioneered automated magnetic cleanliness screening on small spacecraft, a practice that cuts commissioning time by 25%. Down-hole tools for directional drilling capitalize on ruggedized fluxgate stacks that withstand 200 °C and 20,000 psi. Unmanned aerial, surface, and sub-surface vehicles mount vector arrays to automate corridors that humans find dangerous or expensive. Such versatility keeps the magnetometer market diversified across terrestrial and orbital platforms.

By End-User Industry: Automotive ADAS Accelerates Adoption

Aerospace and defense accounted for 21.5% of the magnetometer market size in 2024 as militaries validated quantum navigation for contested airspace. The automotive segment is slated to rise at a 6.8% CAGR as carmakers embed magnetometers into Level-3 perception stacks and battery-current monitors. Magna’s live trials on Sweden’s 5G corridor proved that fusing magnetic cues with V2X data sharpens lane-keeping in tunnels where GPS fails.

Geophysical and mining ventures remain steady buyers because net-zero transitions hinge on copper and lithium finds. Industrial automation adds incremental volume by pairing magnetometers with robotics for adaptive motor control. Healthcare joins the high-margin frontier through brain and heart diagnostics. Collectively, these sectors reinforce a balanced demand profile that supports long-term stability in the magnetometer market.

Geography Analysis

Asia-Pacific dominated with 29.3% share of the magnetometer market in 2024, leveraging dense electronics supply chains and privileged access to rare-earth inputs. China’s new export license rules may realign procurement, giving emerging hubs in India and Vietnam opportunities to capture assembly contracts. Japan and South Korea sustain leadership in miniaturized MEMS fabrication, while Australia positions itself as a field-testing ground through extensive mineral exploration programs.

North America posts the highest regional CAGR at 7.9% to 2030, supported by Department of Defense sponsorship of quantum navigation as well as Silicon Valley’s autonomous-vehicle pilots.[5]Source: “Honeywell Awarded Contracts for Quantum Navigation,” Honeywell Aerospace, honeywell.comCanada adds volume from airborne geophysics over untapped critical-metal belts, and Mexico’s auto clusters integrate magnetometers into electric-vehicle platforms under USMCA regional-content rules. Export-control regulations, however, complicate cross-border shipments of ultra-sensitive designs, nudging firms toward dual-sourcing strategies.

Europe records solid mid-single-digit expansion as NATO endorsements spur subsea surveillance rollouts across the Baltic and North Sea. Germany drives ADAS sensor demand, while Nordic research councils bankroll auroral-science magnetometer arrays. Middle East and Africa usage grows in pipeline integrity and smart-city pilots, albeit from a small base. South America benefits from lithium salt-flat surveys in Chile and copper corridor projects in Brazil, broadening revenue streams for the global magnetometer market.

Competitive Landscape

The magnetometer market features moderate concentration, with the top five suppliers controlling a significant share of 2024 revenue. Honeywell’s EUR 200 million (USD 232.15 million) purchase of Civitanavi reinforced vertical integration for inertial-magnetic hybrids that address both aerospace and industrial customers. SandboxAQ and Q-CTRL commercialized quantum navigation kits that claim fifty-fold accuracy gains relative to classic GPS backups, elevating performance benchmarks.

Established players differentiate on application depth: Bartington emphasizes marine and defense specifications, TDK exploits consumer scale, and QuSpin focuses on zero-field research niches. Patent filings in optically pumped and diamond quantum categories rose 18% year on year, indicating an arms race for IP that shields profitability. Supply chain risk management now influences buying decisions as customers scrutinize rare-earth sourcing and export-control compliance. This dynamic encourages multi-regional fabrication footprints and longer-term off-take contracts across the magnetometer market.

Magnetometer Industry Leaders

Honeywell International Inc.

Bartington Instruments Ltd.

GEM Systems Inc.

Geometrics Inc. (OYO Corp.)

Scintrex Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Honeywell secured U.S. defense contracts worth up to USD 106.2 million to produce quantum sensor navigation systems that integrate advanced magnetometers for GPS-denied missions.

- June 2025: China enacted rare-earth export licenses, extending fluxgate core material led times to as long as 26 weeks.

- April 2025: Q-CTRL flight trials showed quantum navigation achieving fifty-fold improvement over conventional backups, validated by magnetometer arrays.

- March 2025: TDK InvenSense released a 9-axis PositionSense suite that fuses magnetometers with inertial sensors for consumer electronics.

Global Magnetometer Market Report Scope

| Scalar Magnetometers |

| Vector Magnetometers |

| 1-Axis Magnetometers |

| 3-Axis Magnetometers |

| Magnetometer Gradiometers |

| Hall-Effect |

| Fluxgate |

| Magnetoresistive (AMR / GMR / TMR) |

| Optically-Pumped |

| SQUID |

| MEMS |

| Hand-Held / Portable |

| UAV / AUV / UGV-Mounted |

| Stationary / Laboratory |

| Down-hole / Borehole |

| Satellite Payload |

| Aerospace and Defense |

| Geophysical and Mineral Exploration |

| Industrial Automation and Robotics |

| Consumer Electronics and Wearables |

| Automotive (ADAS and EV) |

| Oil and Gas |

| Medical and Healthcare |

| Research and Academia |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Scalar Magnetometers | ||

| Vector Magnetometers | |||

| 1-Axis Magnetometers | |||

| 3-Axis Magnetometers | |||

| Magnetometer Gradiometers | |||

| By Technology | Hall-Effect | ||

| Fluxgate | |||

| Magnetoresistive (AMR / GMR / TMR) | |||

| Optically-Pumped | |||

| SQUID | |||

| MEMS | |||

| By Form Factor | Hand-Held / Portable | ||

| UAV / AUV / UGV-Mounted | |||

| Stationary / Laboratory | |||

| Down-hole / Borehole | |||

| Satellite Payload | |||

| By End-User Industry | Aerospace and Defense | ||

| Geophysical and Mineral Exploration | |||

| Industrial Automation and Robotics | |||

| Consumer Electronics and Wearables | |||

| Automotive (ADAS and EV) | |||

| Oil and Gas | |||

| Medical and Healthcare | |||

| Research and Academia | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the forecast size of the magnetometer market by 2030?

The magnetometer market is projected to reach USD 3.48 billion by 2030, reflecting a 6.1% CAGR.

Which product segment is expanding most rapidly?

Magnetometer gradiometers are expected to grow at a 6.9% CAGR through 2030 due to superior spatial-resolution benefits.

Why are optically pumped systems gaining traction in healthcare?

They eliminate the need for cryogenic cooling, making magnetoencephalography and cardiac imaging practical in routine clinical settings.

How will rare-earth supply controls affect sensor availability?

Export licenses from China lengthen fluxgate core lead times, prompting suppliers to diversify material sources and explore iron-nitride alternatives.

Page last updated on: