Smart Pole Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

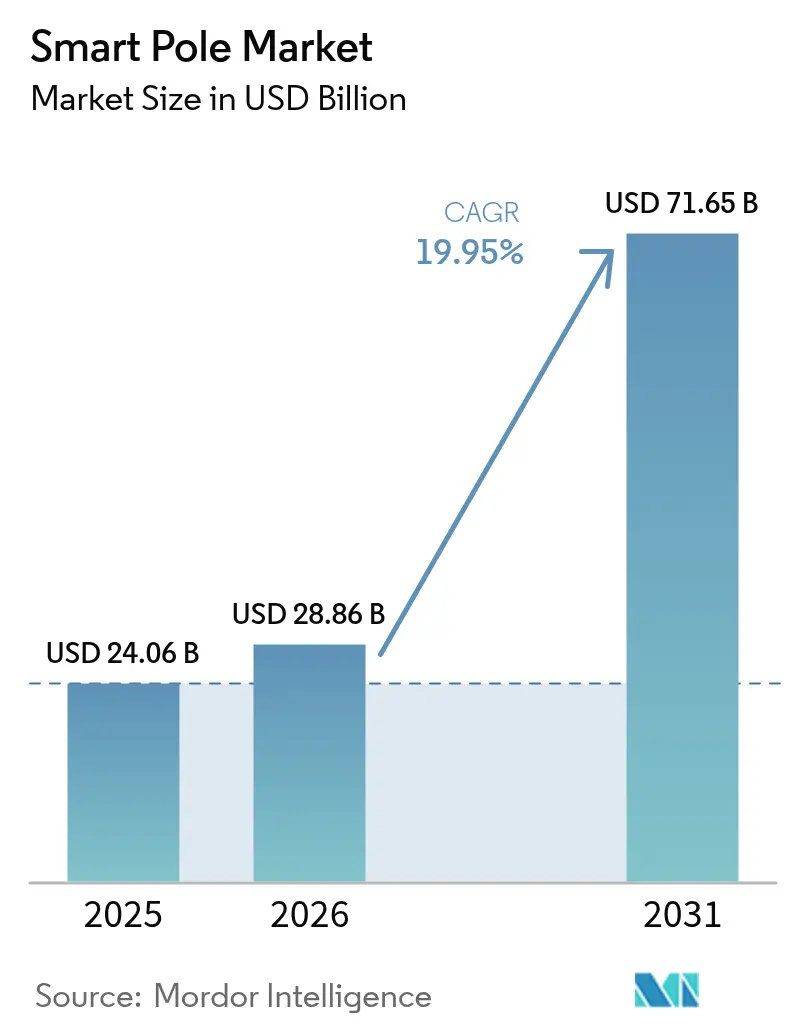

| Market Size (2026) | USD 28.86 Billion |

| Market Size (2031) | USD 71.65 Billion |

| Growth Rate (2026 - 2031) | 19.95% CAGR |

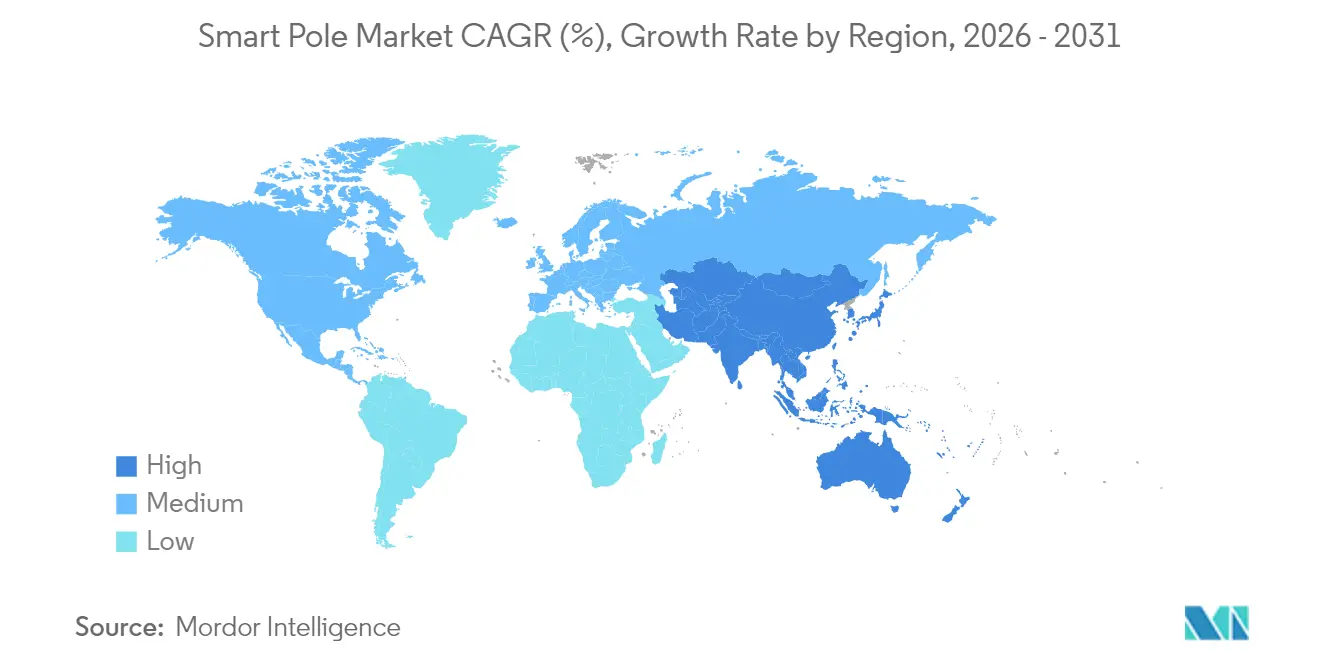

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Pole Market Analysis by Mordor Intelligence

The Smart Pole market size is expected to grow from USD 24.06 billion in 2025 to USD 28.86 billion in 2026 and is forecast to reach USD 71.65 billion by 2031 at 19.95% CAGR over 2026-2031.

This sustained rise reflects how 5G densification requirements, LED-retrofit mandates, and nationwide smart-city programmes have turned connected street furniture into essential digital infrastructure. Cities now view smart poles as revenue-positive assets. San Diego’s 500 smart streetlights aided 229 criminal cases and 166 arrests in 2024, underscoring clear socio-economic returns. Backed by policy pressure, China’s housing ministry issued 2024 rules that compel interoperable pole deployments, while the EU and India channel dedicated capital through Horizon 2020 and the Smart Cities Mission to speed adoption. Cellular co-location drives 46% of deployments because operators can mount 5G small cells on existing poles, trimming both time and zoning hurdles. Hardware remains the largest spending line, yet software platforms are rapidly scaling as municipalities monetise pole-generated data.

Key Report Takeaways

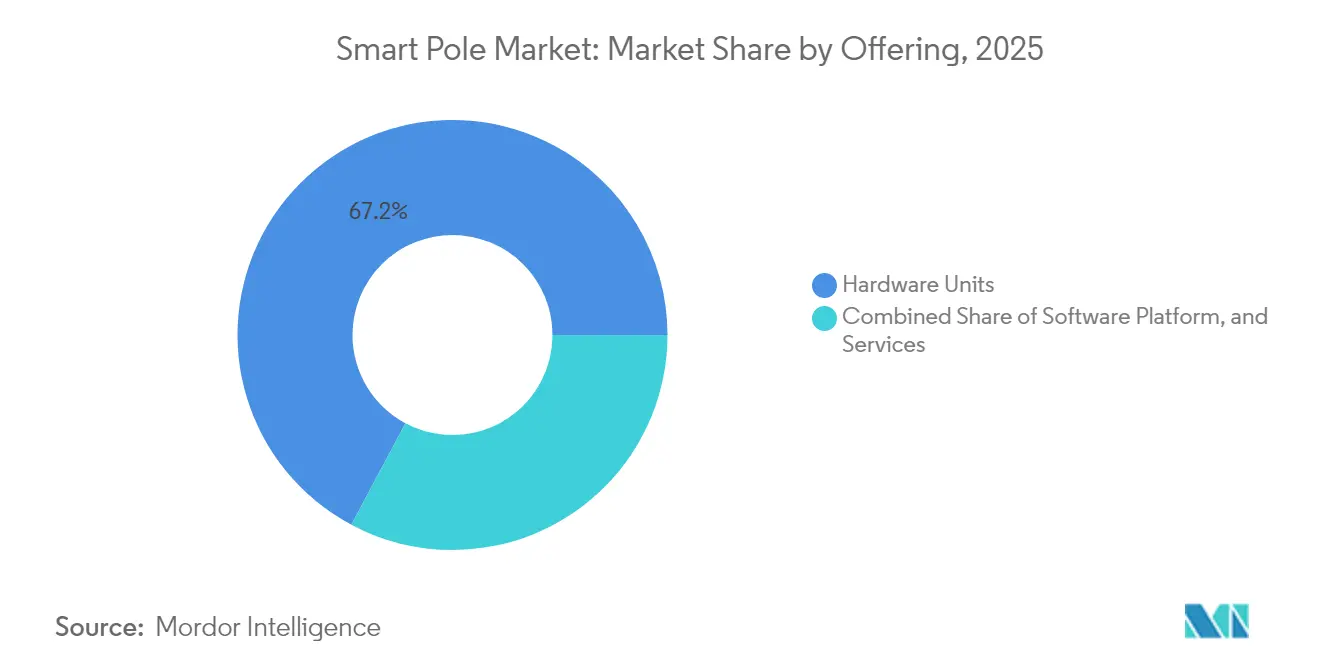

- By offering, hardware held 67.20% of the smart pole market share in 2025, while software is projected to register a 21.8% CAGR to 2031.

- By installation type, new deployments dominated with 56.30% revenue in 2025; retrofit installs are poised for a 20.1% CAGR through 2031.

- By connectivity technology, cellular networks accounted for 45.60% of the smart pole market size in 2025 and are set to expand at a 23.4% CAGR.

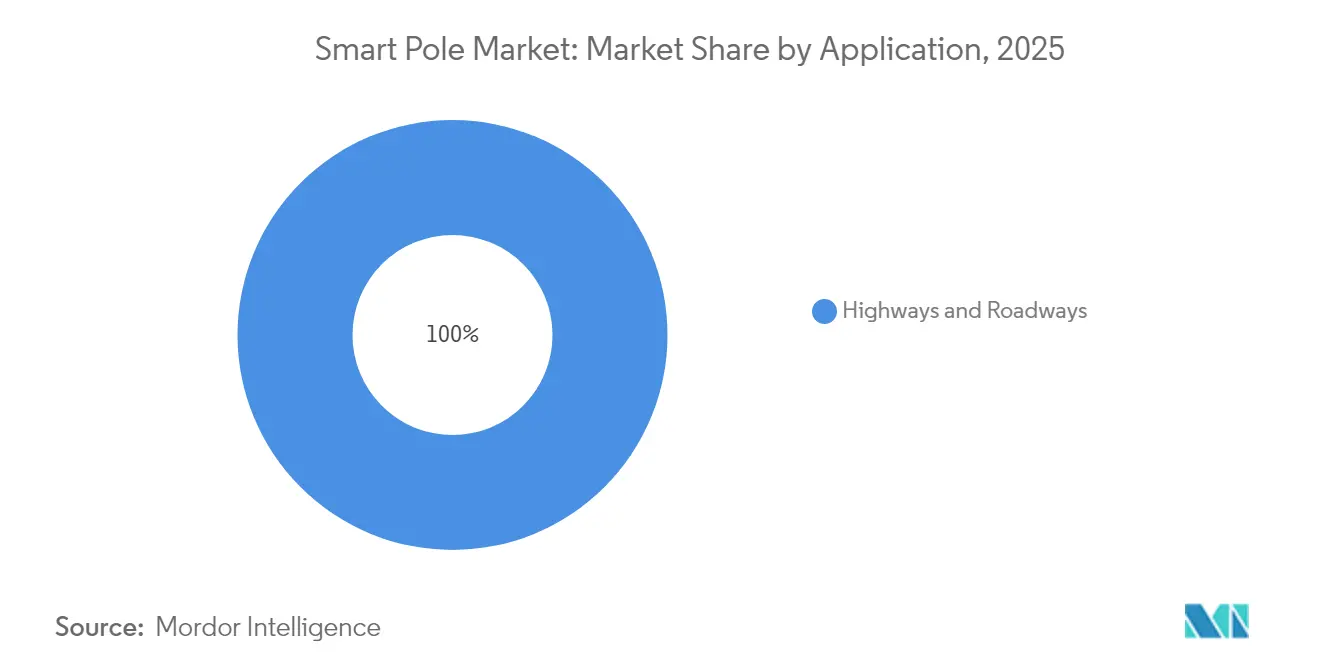

- By application, highways and roadways captured 51.30% of the smart pole market size in 2025; parking lots and campuses represent the fastest-growing niche at a 22.7% CAGR.

- By material, steel and aluminium structures led with 48.60% revenue in 2025, whereas composite poles are on course for a 20.6% CAGR thanks to lightweight corrosion-resistant designs.

- By geography, North America commanded 35.10% of the smart pole market in 2025; Asia Pacific is advancing at a 23.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Pole Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government smart-city mandates | +6.2% | Global, with concentration in China, EU, India | Medium term (2-4 years) |

| LED-retrofit energy-savings push | +4.8% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| 5G / small-cell co-location demand | +5.1% | Global, led by developed markets | Medium term (2-4 years) |

| Falling IoT-sensor costs | +2.9% | Global | Short term (≤ 2 years) |

| Ad-revenue and data-monetisation PPPs | +1.8% | North America, EU pilot markets | Long term (≥ 4 years) |

| ESG-linked muni-bond funding | +2.3% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Smart-City Mandates

Nation-level programmes anchor the smart pole market because municipalities must modernise lighting grids to meet climate neutrality, safety, and data-governance targets. The European Commission’s Cities Mission calls for 100 climate-neutral cities by 2030 and prescribes integrated digital infrastructure, including multi-service poles. In China, May 2024 guidance from the National Development and Reform Commission obliges city planners to fold smart poles into unified data platforms, accelerating standardised procurement. Chicago’s smart-lighting programme reports USD 10 million annual energy savings while enhancing crime monitoring through pole-mounted sensors. Such directives foster predictable procurement cycles that permit volume manufacturing and lower per-unit costs.

LED-Retrofit Energy-Savings Push

LED retrofits deliver 50-60% energy savings compared with high-pressure sodium lamps, giving cities an immediate fiscal incentive to adopt smart poles. Parramatta’s USD 5.55 million LED rollout swapped 4,500 luminaires, cutting energy bills and adding adaptive dimming. The U.S. Department of Energy notes that utility financing and energy-service contracts can cover upfront costs, unlocking adoption by budget-strapped towns. Incremental retrofits also avoid wholesale street works, allowing phased integration of sensors and connectivity modules across existing assets. As jurisdictions publicise cost-avoidance metrics, they create peer pressure that keeps the smart pole market on a rapid adoption curve.

5G Small-Cell Co-Location Demand

Mobile operators need dense, low-height sites to meet 5G coverage and capacity targets, and smart poles offer power, backhaul, and approved right-of-way in one bundle. Virgin Media O2’s UK tests showed that poles with integrated 4G/5G small cells can be installed without extra planning permission, halving deployment time[1]Virgin Media O2, “Smart Poles Boost Mobile Coverage,” virginmediao2.com. Cornerstone’s alliance with Signify extends the model nationwide, enabling multi-operator neutral hosts that lighten capital burdens for individual carriers. This revenue-sharing opportunity turns street lighting from a municipal cost into an income stream, accelerating private investment and fuelling the smart pole market.

Falling IoT-Sensor Costs

With cellular IoT modules tracking a 16% CAGR through 2027, environmental, traffic, and security sensors drop into double-digit dollar pricing. Platforms like Interact City harness real-time data to trim lighting energy use by up to 80% via adaptive algorithms. Edge processors embedded in poles perform analytics locally, slashing backhaul and cloud costs while improving emergency response latency. As the bill-of-materials shrinks, even mid-sized municipalities find comprehensive sensor suites financially tenable, broadening the addressable smart pole market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex and ROI risk | -3.4% | Global, acute in developing markets | Short term (≤ 2 years) |

| Interoperability gaps in protocols | -2.1% | Global | Medium term (2-4 years) |

| Urban-aesthetic zoning limits | -1.6% | Developed markets, historic districts | Long term (≥ 4 years) |

| Cyber-physical insurance premiums | -1.9% | Global, concentrated in critical infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex and ROI Risk

Municipal budgets rarely stretch to multi-million-dollar lighting upgrades without clear payback. In upstate New York, utilities require USD 5 million liability cover for smart streetlight pilots, inflating overall project cost[2]GovTech, “Utility Liability Requirements for Smart Lighting,” govtech.com. Wal-Mart’s car-park case study shows a 7.5-year payback when replacing 1,000 W metal halide fittings with LEDs, far longer than most city budget cycles. Public-private partnerships such as value-capture funding, showcased by Vijayawada’s Golden Mile, redistribute risk to concessionaires, yet smaller cities often lack the legal capacity to structure similar deals, muting near-term demand.

Interoperability Gaps in Protocols

Smart poles straddle lighting, telecom, transport, and public-safety systems, yet vendor protocols remain siloed. IEEE standards like P2413 and 2030.5 outline common architectures, but adoption is patchy, forcing integrators to support multiple stacks. The open OCPP model in EV charging illustrates a workable path to unification, but replicating it for smart poles requires coordinated municipal procurement and vendor commitment. Small suppliers struggle to maintain multi-standard firmware, raising integration bills and elongating project schedules, which slows smart pole market rollouts in the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Hardware Outlays Lead, Software Value Rises

Hardware purchases amounted to 67.20% of the smart pole market in 2025 as poles, luminaires, sensors, and communications gear demand significant upfront capital. Software, though presently a smaller line-item, is compounding at 21.8% annually, signalling a pivot from asset delivery to data services. Signify converts 93% of its EUR 6.1 billion lighting sales into LED units, demonstrating how economies of scale reduce capital costs for municipalities.

Firms now position cloud dashboards, API gateways, and AI-driven analytics as core value streams. Wide-area device management cuts truck rolls, while predictive maintenance extends asset life, improving total-life economics. Consequently, recurring licence and support fees are beginning to rival hardware margins, a progression that underpins long-run growth for the smart pole market.

By Installation Type: New Builds Dominate but Retrofits Accelerate

New installations comprised 56.30% of 2025 revenue because green-field smart-city districts favour custom-engineered poles with embedded radios, CCTV, and EV chargers. Retrofit programmes, however, should log a 20.1% CAGR through 2031, outpacing new builds, as cities swap sodium lamps for LED heads plus plug-in sensor modules. Chicago upgraded 270,000 lights to LED while adding remote-control nodes, cutting energy use, and enabling crime analytics.

Retrofits exploit existing power feeds and foundations, trimming civil works costs by as much as 30%. Payback windows can narrow to 4–5 years, suiting municipal budgeting cycles and supporting distributed rollouts. The pattern broadens geographic access, reinforcing demand diversity within the smart pole market.

By Connectivity Technology: Cellular Takes the Lead

Cellular links 4G, 5G, and NB-IoT, held 45.60% of 2025 revenue, expanding at a 23.4% CAGR as carriers push network densification without erecting new towers. American Tower’s 220,000-site global estate allows operators to piggyback on street poles in crowded urban cores. Robust licensed-spectrum reliability also suits safety-critical traffic-management and emergency-response apps.

Wi-Fi, Zigbee, and Bluetooth address localised, low-data tasks, while fibre or power-line links serve high-bandwidth video surveillance. Hybrid architectures are therefore normal, yet cellular remains the backbone, cementing its primary status in the smart pole market.

By Application: Highways Remain the Volume Anchor

Highways absorbed 51.30% of the smart pole market size in 2025 because kilometre-scale corridors need uniform illumination and traffic sensing. Wyoming’s I-80 saw 42% collision reductions after adding connected alerts, validating the safety dividend. Parking lots and campuses show the fastest growth at 22.7% CAGR as asset owners seek precise ROI; Walmart’s LED trial cut lighting energy by 63% while boosting perceived safety.

Public plazas, railheads, and harbours add incremental volume, particularly where smart poles double as signage, Wi-Fi hotspots, and charging points. Diversifying use cases fuels steady contribution from multiple sub-sectors, keeping demand resilient across cycles for the smart pole industry.

By Material: Steel Prevails, Composites Emerge

Steel and aluminium still account for 48.60% of 2025 shipments due to mature supply chains and favourable price-performance. Yet steel traded at USD 1.60 per pound in 2024, spurring interest in lighter composites that promise 42% cost savings over a 20-year life, owing to corrosion resistance. Covestro’s polycarbonate resins integrate cable-ducts and thermal channels, enabling slimmer profiles and easier 5G radio placement.

Composites are forecast to post a 20.6% CAGR as buyers prioritise life-cycle economics and simplified transport logistics. The resulting mix shift lowers pole weight, widens design freedom, and expands addressable sites, reinforcing long-run upside across the smart pole market.

Geography Analysis

North America commanded 35.10% of 2025 revenue, underpinned by large-scale LED retrofits and utility financing. The New York Power Authority’s plan to network 500,000 streetlights with Signify’s Interact platform highlights project scale and replicability. Robust municipal bond markets facilitate capital access, while broadband carriers harness smart poles to fill suburban 5G gaps, keeping order pipelines steady.

Asia Pacific is the quickest-growing arena, rising at 23.6% CAGR to 2031. China issued national guidelines urging “vehicle-road-cloud” integration, mandating sensorized roadside units that dovetail with multipurpose poles. India’s Smart Cities Mission budgeted INR 11.21 lakh crore (USD 1.35 billion) for 2025-26, of which 90% of 8,000 projects were completed by mid-2024, creating ready-made demand funnels.

Europe maintains consistent expansion owing to the EU’s Digital Europe and Horizon 2020 funds. The bloc allocated EUR 1.4 billion to smart-infrastructure pilots in 134 cities, providing de-risked capital pools. Cornerstone’s partnership with Signify to mount neutral-host 5G radios on street lighting demonstrates how infrastructure sharing cuts operator opex, keeping deal flow healthy despite macro headwinds.

Competitive Landscape

The vendor base is moderately fragmented; no single supplier holds a double-digit global revenue share. Lighting majors like Signify marry hardware, cloud software, and lifecycle services to offer turnkey propositions that simplify municipal procurement. The firm crossed 153 million connected light points in Q1 2025, up from 144 million the prior year, indicating strong platform stickiness.

Telecom-tower giants such as American Tower diversify into street-level assets, bundling real-estate expertise with small-cell integration support. Their developed-markets focus syncs with pole densification hotspots, reinforcing revenue resilience. Infrastructure specialists like Valmont supply engineered poles plus construction services; the company logged USD 3 billion infrastructure sales in 2024 and targets USD 4.2 billion in 2025[4]Valmont Industries, “FY 2024 Results,” valmont.com.

Value migration is shifting toward data analytics, drawing software-native entrants that license AI-driven optimisation modules across multi-vendor fleets. Open standards advocacy by IEEE and industry alliances aims to reduce lock-in, a trend likely to heighten competition on services rather than physical bill-of-materials economics. Consolidation through M&A and strategic alliances is expected as vendors race to deliver holistic solutions for the expanding smart pole market.

Smart Pole Industry Leaders

Iram Technologies Pvt. Ltd.

Signify Holding B.V.

Efftronics Systems Pvt. Ltd.

Shanghai Sansi Electronic Engineering Co., Ltd.

Lumca Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: China’s State Council rolled out a vehicle-road-cloud pilot requiring intelligent roadside assets built on smart pole frameworks.

- December 2024: Valmont unveiled rapid-install 5G poles in the UK using screw-pile foundations to minimise environmental impact.

- November 2024: China’s housing ministry published urban digital-infrastructure standards that require interoperable smart pole systems.

- March 2024: Virgin Media O2 completed fixed-network-powered smart pole trials, demonstrating zero-permit rollout of 4G/5G small cells.

Global Smart Pole Market Report Scope

Smart poles are connected light sources that can be remotely managed. The smart pole technology offers multi-utility functions and facilities for citizens, visitors, and businesses. Smart poles are used in applications, such as highways, roadways, and public places. Smart pole features technology to improve mobile network performance across the city and provide various benefits, such as internet connectivity, public announcement speakers, and charging points, to help citizens in public places.

The study tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The scope of the report encompasses market sizing and forecast for segmentation by geography. The market sizes and forecasts are provided in terms of value (USD) for the above segments. The study further analyzes the impact of COVID-19 on the ecosystem.

| Hardware Units |

| Software Platform |

| Services |

| New Installation |

| Retrofit |

| Wired (PLC, Fiber) |

| Wireless (Wi-Fi, BLE, Zigbee) |

| Cellular (4G/LTE, 5G, NB-IoT) |

| Highways and Roadways |

| Public Places and Plazas |

| Railways and Harbors |

| Parking Lots and Campuses |

| Steel/Aluminum |

| Composite and CFRP |

| Concrete |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Argentina |

| Brazil | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Offering | Hardware Units | |

| Software Platform | ||

| Services | ||

| By Installation Type | New Installation | |

| Retrofit | ||

| By Connectivity Technology | Wired (PLC, Fiber) | |

| Wireless (Wi-Fi, BLE, Zigbee) | ||

| Cellular (4G/LTE, 5G, NB-IoT) | ||

| By Application | Highways and Roadways | |

| Public Places and Plazas | ||

| Railways and Harbors | ||

| Parking Lots and Campuses | ||

| By Material | Steel/Aluminum | |

| Composite and CFRP | ||

| Concrete | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Argentina | |

| Brazil | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the smart pole market?

The smart pole market is valued at USD 28.86 billion in 2026 and is projected to reach USD 71.65 billion by 2031.

Which segment is growing the fastest?

Software platforms show the highest momentum with a 21.8% CAGR through 2031 as cities monetise data from connected poles.

Why are cellular networks central to smart pole adoption?

Cellular connectivity enables 5G small-cell co-location, providing carriers with rapid and cost-effective densification while offering municipalities an extra revenue stream.

Which region will expand the quickest by 2031?

Asia Pacific is forecast to post a 23.6% CAGR, propelled by China’s national digital-infrastructure mandates and India’s Smart Cities Mission.

What is the chief barrier to deployment?

High upfront capital expenditure and long payback periods deter budget-constrained municipalities, particularly in developing markets.

How do smart poles aid public safety?

Integrated cameras and sensors feed real-time data to law-enforcement systems, with San Diego reporting 229 criminal cases supported by its smart lighting network in 2024.

Page last updated on: