Permanent Magnet Motor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 57.94 Billion |

| Market Size (2031) | USD 89.47 Billion |

| Growth Rate (2026 - 2031) | 9.08% CAGR |

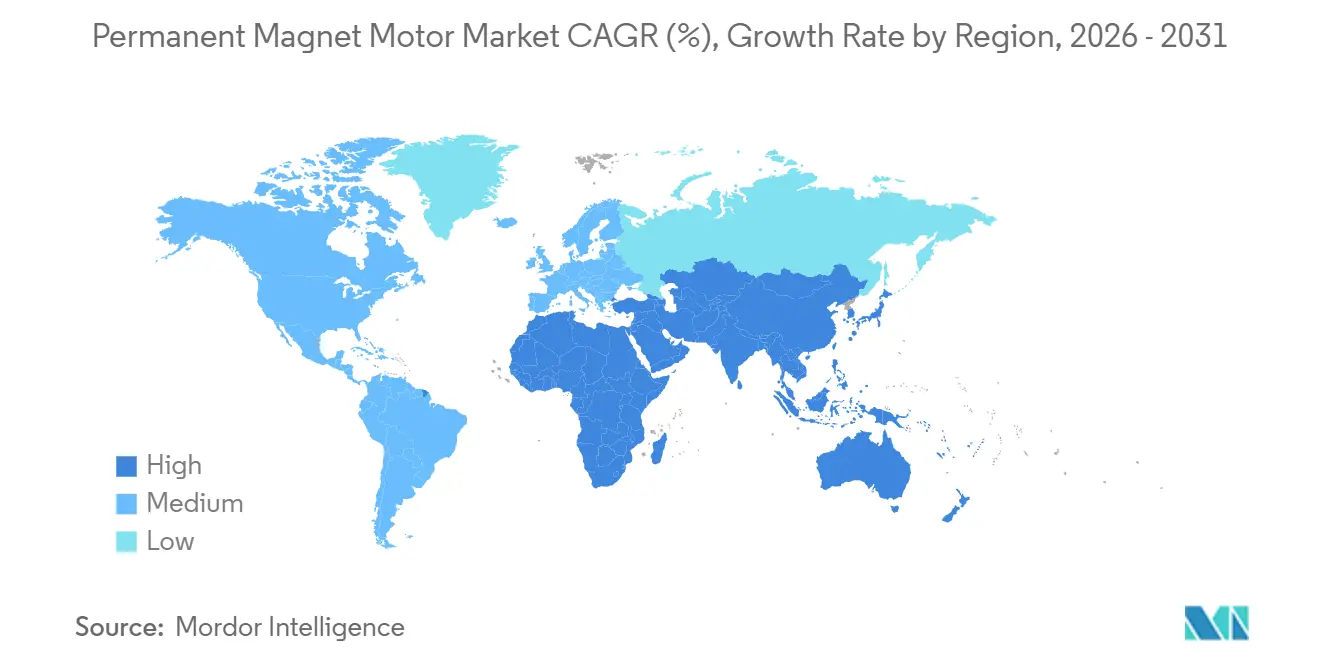

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Permanent Magnet Motor Market Analysis by Mordor Intelligence

The permanent magnet motor market stood at USD 57.94 billion in 2026 and is forecast to reach USD 89.47 billion by 2031, translating to a 9.08% CAGR over the period. Continued electrification of transport and industry, rapid tightening of motor-efficiency regulations, and the quest for resilient rare-earth supply underpin demand growth. Brushless DC topologies are moving ahead of legacy designs as automakers embed them in traction inverters and collaborative-robot builders specify them for fast torque response. Magnet innovators are pushing nanocomposite neodymium-iron-boron chemistries that curb heavy rare-earth content without eroding coercivity, an advance that eases geopolitical supply-chain risk while preserving torque density. Asia-Pacific dominates installed base thanks to China’s vertically integrated value chain, yet North American and European reshoring initiatives are reshaping procurement patterns as domestic magnet production scales up. Competitive tactics revolve around bolt-on acquisitions that secure magnet capacity and additive-manufacturing know-how, giving leading suppliers deeper control over cost and speed-to-market.

Key Report Takeaways

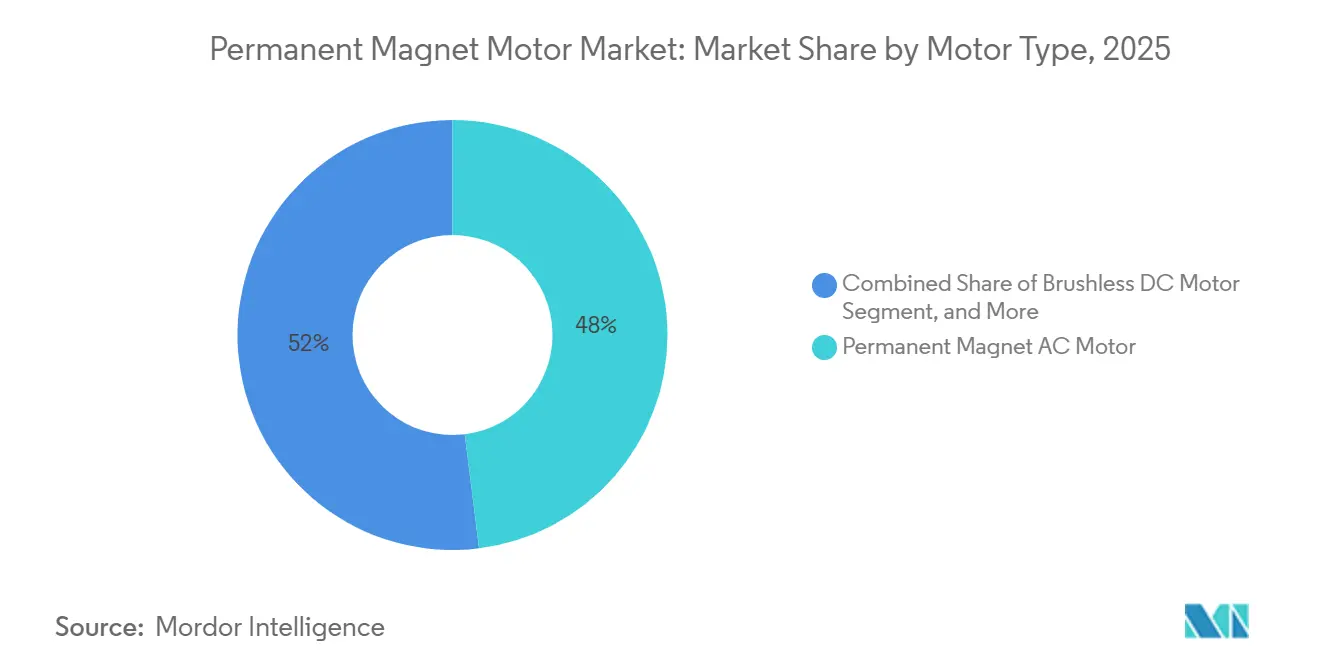

- By motor type, permanent magnet AC motors led with 48.03% revenue share in 2025, while brushless DC is projected to expand at a 10.86% CAGR through 2031.

- By power rating, the 4-22 kW class captured 41.37% revenue share in 2025, whereas the 75 kW-and-above bracket is forecast to advance at a 10.70% CAGR through 2031.

- By end-user industry, automotive accounted for 37.24% of permanent magnet motor market share in 2025, while the energy sector is set to record the fastest 9.90% CAGR to 2031.

- By geography, Asia-Pacific commanded 43.50% revenue share in 2025 and is expected to deliver the quickest 9.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Permanent Magnet Motor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increased Motor Efficiency Due to Permanent Magnets | +1.80% | Global, with strongest adoption in Europe and North America | Medium term (2-4 years) |

| Rising Demand for Electric Vehicles | +2.30% | Asia-Pacific core, expanding to Europe and North America | Short term (≤2 years) |

| Stringent Energy-Efficiency Regulations | +1.50% | Europe and North America, cascading to Asia-Pacific | Medium term (2-4 years) |

| Expansion of Renewable Energy Generation Using PM Generators | +1.20% | Global, with offshore wind concentrated in Europe and Asia-Pacific | Long term (≥4 years) |

| Advances in Additive Manufacturing of Custom PM Rotors | +0.90% | North America and Europe, pilot deployments in Asia-Pacific | Long term (≥4 years) |

| Regionalization of Rare-Earth Magnet Supply Chains | +1.10% | North America, Europe, and Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increased Motor Efficiency Due to Permanent Magnets

Permanent-magnet synchronous motors deliver 94-97% full-load efficiency in the 4-22 kW class, outpacing comparable induction designs by up to 5 percentage points, a delta that trims industrial payback periods below 18 months.[1]U.S. Department of Energy, “Industrial Technologies Program: Motor Systems,” energy.gov Variable-speed duty cycles amplify the savings because rotor copper losses disappear when magnet excitation replaces winding current, a fit with ISO 50001 programs that prize low part-load losses. The European Union’s Ecodesign Directive widened the scope of minimum efficiency rules in 2024, triggering retrofits in space-constrained refrigeration and ventilation equipment.[2]European Commission, “Ecodesign Regulation 2024,” ec.europa.eu Above 200 kW the cost-benefit narrows, yet niches such as regenerative cranes still justify magnet adoption where frequent cycling dominates lifecycle cost.

Rising Demand for Electric Vehicles

Global battery-electric output reached 14 million vehicles in 2025, and 78% used permanent-magnet traction motors for superior torque density and regeneration efficiency.[3]International Energy Agency, “Global EV Outlook 2025,” iea.org Chinese automakers now combine hairpin stators with segmented-magnet rotors to slash eddy losses, enabling continuous ratings above 150 kW without liquid cooling. Tesla’s reluctance-assisted design trimmed neodymium content by 20%, prompting rivals to accelerate dysprosium-free chemistries. Commercial fleets amplify demand: Daimler Truck and Volvo Group plan more than 50,000 electric heavy vehicles each year by 2027, absorbing over 1,200 metric tons of NdFeB magnets annually.

Stringent Energy-Efficiency Regulations

The U.S. Department of Energy finalized IE4-level motor requirements in March 2024 for 1-500 horsepower machines, effective January 2027, effectively pushing variable-torque designs above 50 hp toward permanent-magnet or synchronous-reluctance architectures. Manufacturers face USD 15-25 million retooling bills per plant, fuelling consolidation and creating openings for suppliers already scaled in magnet motors. Japan’s 2025 Top Runner update extended high-efficiency rules to hermetic compressors, a category that consumes 18% of residential electricity; permanent-magnet variants can cut household use by up to 280 kWh per year. Retrofit incentives in Germany and France accelerate uptake by allowing accelerated depreciation on qualifying motors.

Expansion of Renewable Energy Generation Using PM Generators

Offshore wind projects commissioned in 2025 favour direct-drive permanent-magnet generators rated 12-15 MW, eliminating gearboxes and pushing turbine availability above 97%. Vestas and GE Vernova locked in multi-year supply deals covering up to 4,000 metric tons of NdFeB per year through 2028. Hydropower upgrades that replace salient-pole alternators with permanent-magnet synchronous units add 4-6 percentage points of part-load efficiency, boosting generation by up to 20 GWh annually at 100 MW stations. Carbon-credit monetization of reduced curtailment further sweetens project economics in OECD power markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Diminishing Availability of Rare-Earth Metals | -1.40% | Global, acute in North America and Europe | Short term (≤2 years) |

| High Initial Cost of PM Motors | -1.00% | Emerging markets in South America, Middle East, and Africa | Medium term (2-4 years) |

| Demagnetization Risk at Elevated Operating Temperatures | -0.70% | Middle East, Africa, and tropical Asia-Pacific | Medium term (2-4 years) |

| Geopolitical Supply-Chain Concentration Risk | -0.90% | North America, Europe, and Japan | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Diminishing Availability of Rare-Earth Metals

Neodymium oxide supply totalled 38,000 metric tons in 2025 against demand poised to pass 45,000 metric tons in 2028, elevating spot prices from USD 68 /kg in early 2024 to USD 92 /kg by December 2025. Dysprosium remains tighter, with China controlling 94% of separation capacity and adjusting export quotas by up to 25% year-over-year. Manufacturers mitigate exposure through flux-concentrating rotors and grain-boundary diffusion that slash heavy rare-earth content by up to 40%, but the capital cost of new magnet lines ranges from USD 8-12 million. Recycling plants, while promising, still supply under 3% of global magnet demand.

High Initial Cost of PM Motors

List prices for 4-22 kW permanent-magnet units sit 35-50% above induction counterparts, stretching payback beyond 3 years in duty cycles under 4,000 hours per year. The gap is sharper in hermetic compressors, where magnet insertion and rotor balancing add USD 18-25 per unit, a 12-15% uplift that appliance makers struggle to pass on in price-sensitive markets. Financing hurdles in emerging economies limit access to green-loan programs common in OECD regions, though rising energy prices are nudging municipal utilities and mines to adopt total-cost-of-ownership models that favour efficient motors over time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Motor Type: Brushless Designs Extend Reach

Permanent magnet AC machines generated 48.03% of revenue in 2025, reflecting their entrenched role in factory automation and HVAC installations where three-phase grids and mature inverter ecosystems simplify deployment. The permanent magnet motor market is witnessing double-digit expansion of brushless DC alternatives that pair naturally with 48-volt subsystems in electric vehicles and collaborative robots. Manufacturers like Continental have demonstrated trapezoidal back-EMF profiles that reduce semiconductor switching losses by up to 12%, a performance gain that shortens controller cost recovery cycles. Legacy permanent magnet DC designs linger in small electronics, yet their share contracts as lithium-ion packs standardize around voltages that reward sensorless brushless topologies with longer lifespans. Hermetic motors sit at the intersection of the refrigeration boom and heat-pump retrofits, drawing interest because sealed stators eliminate refrigerant leakage paths during repeated thermal cycling.

Brushless architectures also reshape maintenance economics. Absence of brushes removes sparking and dust, extending overhaul intervals in food-grade conveyors and medical ventilators where cleanliness is paramount. The permanent magnet motor market size for brushless platforms in auxiliary vehicle systems is expected to maintain momentum because onboard electronics already support field-oriented control. Conversely, permanent magnet AC remains favoured in grid-tied equipment that demands smooth sinusoidal torque and accepts slightly larger frames to simplify compliance with electromagnetic compatibility norms. The net effect is parallel growth corridors rather than outright substitution, with design engineers selecting form factors according to duty cycle and inverter sophistication rather than magnet cost alone.

By Magnetic Material Type: Nanocomposites Gain Traction

Neodymium-iron-boron retained 52.40% share in 2025, thanks to energy products above 35 MGOe that let designers trim rotor diameters and still hit torque targets. Yet the permanent magnet motor market now tracks a rapid 10.04% CAGR for nanocomposite NdFeB, a chemistry that deposits terbium or dysprosium at grain boundaries, raising coercivity by up to 30% while cutting heavy rare-earth loadings nearly in half. These alloys shield OEMs from dysprosium price spikes that exceeded 60% in 2024-2025, and they allow operation beyond 180 °C in high-speed spindles without demagnetization. Aerospace and defense users still specify samarium-cobalt for thermal stability above 200 °C despite material costs roughly triple those of NdFeB. Ferrite, though lower in energy density, draws appliance and irrigation-pump producers that compete in regions where electricity tariffs sit under USD 0.08 /kWh, extending ROI thresholds beyond premium magnet economics.

Nanocomposite diffusion lines require tighter process controls and capital outlays upward of USD 10 million, but early movers lock in intellectual property barriers that deter fast-follower entry. The permanent magnet motor market share for ferrite will likely stabilize rather than collapse, helped by hybrid reluctance-assisted topologies that allow magnet mass reductions of 40-60%. Ultimately magnet mix bifurcates along performance and cost curves, matching technologically demanding automotive and industrial segments with nanocomposites, while volume-driven appliance makers optimize around ferrite.

By Power Rating: High-Power Adoption Accelerates

Motors in the 4-22 kW band contributed 41.37% of 2025 revenue, supported by widespread deployment in industrial pumps, fans, and conveyors where standardized frames ease drop-in swaps. However, the 75 kW and above class is the fastest mover, climbing at 10.70% CAGR as mining haul trucks, drilling mud pumps, and offshore compressors chase efficiency savings. The permanent magnet motor market size for high-power units grows because diesel replacement yields fuel cuts of up to 150 liters per 10-hour shift, and operators report maintenance interval extensions from 500 to 1,200 hours. Offshore platforms retrofit seawater injection systems with 150-300 kW permanent-magnet drives that shave 1.8 MWh per day per pump, translating to six-figure annual savings when crude prices remain above USD 80 per barrel.

In contrast, the up-to-4 kW segment caters to consumer electronics and medical devices where brushless DC dominates for low voltage and compact mass. The 22-75 kW range grows more slowly because plant managers often pair induction machines with variable-frequency drives to meet part-load flexibility at lower capital expense. When annual operating hours exceed 5,000 or regenerative service is essential, permanent magnets win the business case; otherwise, induction hardware holds ground.

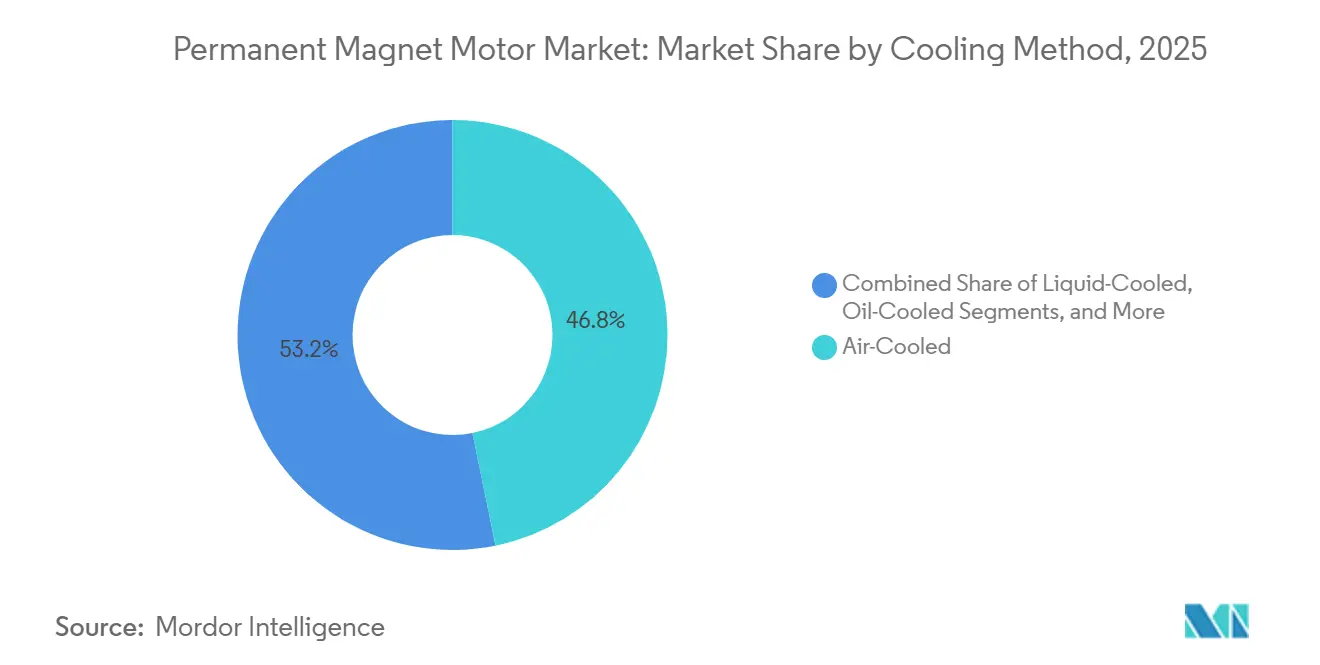

By Cooling Method: Liquid Systems Break Through

Air-cooled designs still represent 46.80% of installations, well-suited to continuous duty loads below 4 kW per liter. Yet liquid cooling gains a 9.67% CAGR as 800-volt vehicle platforms push current densities to 30 A/mm². The permanent magnet motor market, therefore, supports direct oil-jet or glycol-jacket stators that dissipate more than 150 W/cm² heat flux, unlocking 15-20% higher continuous power within unchanged envelopes. Oil-cooled variants penetrate high-speed machine-tool spindles, where speeds above 20,000 rpm would otherwise mandate bulky air coolers. Hybrid systems mix jackets and air channels to hold winding temperature within ±5 °C, stabilizing flux and encoder accuracy in precision servos.

Liquid cooling introduces new bill-of-materials items, such as thermal interface pads and manifolds, that add 8-12% to unit cost. Nevertheless, vehicle integrators absorb the premium because it delays derating and keeps performance consistent across broad ambient ranges. For stationary industrial settings, the trade-off depends on piping complexity and coolant maintenance protocols, yet demand rises in petrochemical plants where ambient temperatures exceed 50 °C and air cooling proves inadequate.

By End-User Industry: Energy Projects Surge

Automotive remained the largest user at 37.24% of 2025 demand, anchored by global light-vehicle electrification that hit 22% that year. Still, utilities are the fastest movers, with renewable-energy and hydro operators pursuing 9.90% CAGR as direct-drive generators eliminate gearboxes responsible for 15-20% of wind downtime. Industrial automation increasingly embeds servo motors with sub-millisecond torque response, empowering lights-out factories and human-robot collaboration. Mining, oil and gas follow, where energy savings of 4-7 percentage points per 100 kW motor justify premium capital amid high electricity or diesel costs.

Water and wastewater plants, aerospace and defense, consumer electronics, and healthcare round out the application landscape, with MRI-ready surgical robots and portable ventilators valuing low electromagnetic emissions and compact mass.

Geography Analysis

Asia-Pacific generated 43.50% of 2025 revenue and continues at a 9.58% CAGR as China’s vertically integrated chain shrinks lead times to under eight weeks. Japan leverages samarium-cobalt prowess for aerospace contracts insulated from Chinese competition, while South Korea channels KRW 1.8 trillion (USD 1.35 billion) into hairpin winding and segmented rotor capacity for Hyundai and LG projects. India, buoyed by production-linked incentives, speeds adoption of 1-5 kW brushless hub motors in two-wheelers and auto-rickshaws that meet cost targets by substituting ferrite magnets.

North America and Europe invest heavily in supply-chain regionalization. The U.S. Department of Defense awarded USD 285 million for domestic separation and magnet facilities aiming to cut import reliance below 50% by 2030. The European Union’s Critical Raw Materials Act requires 15% local rare-earth sourcing by 2028, spurring projects from Sweden’s Norra Kärr mine to German recycling plants. Inflation Reduction Act incentives push automakers toward U.S. magnet content despite a 12-18% procurement premium, since vehicles qualify for USD 7,500 consumer tax credits. Offshore wind ambitions of 60 GW by 2030 require vast permanent-magnet generator volumes, and long-term supply agreements already lock in price and availability.

Middle East and Africa plus South America show selective adoption. Gulf desalination plants retrofit high-pressure pumps with permanent magnet drives that cut energy use by up to 25%. Chilean and Peruvian copper mines trial conveyor and ventilation conversions that save over 1.2 GWh per site per year. Sub-Saharan markets remain price-sensitive but install solar-powered brushless DC irrigation pumps that avoid inverter costs, expanding crop yields where grid service is unreliable.

Competitive Landscape

The top five suppliers ABB, Siemens, Nidec, Rockwell Automation, and Mitsubishi Electric controlled roughly 40% of global revenue in 2025, yet none surpassed 12%, underscoring a moderately concentrated field. Leaders acquire magnet recyclers and additive-manufacturing firms to secure feedstock and deliver custom rotors within four-week windows. ABB’s September 2024 purchase of a European recycler covers 15-20% of its neodymium needs, while Nidec plans 4 million traction motors annually by 2028 through Chinese, Mexican, and Serbian expansions.

Patent filings in flux-weakening control and thermal materials climbed 32% year-over-year, with Siemens and Hitachi each lodging more than 40 applications in 2024-2025. Regional players such as Wolong Electric and WEG capture cost-sensitive pump and fan orders by undercutting multinational prices up to 30% yet still meeting IE3 norms.

White-space opportunities surface in ultra-high-speed motors above 30,000 rpm for electric aircraft and hydrogen compression. Only a handful of suppliers master soft-magnetic composites required to slash eddy losses at such speeds, positioning them for premium margins. The competitive map thus bifurcates between high-volume platforms that reward automation and niche segments that prize bespoke designs and rapid prototyping.

Permanent Magnet Motor Industry Leaders

ABB Limited

Rockwell Automation

Siemens AG

Franklin Electric Company Inc.

Allied Motion Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Siemens opened a 40,000-square-meter permanent-magnet motor plant in Nuremberg with 500,000-unit annual capacity focused on 15-75 kW ratings.

- November 2025: Nidec launched a Kyoto magnet-recycling joint venture able to reclaim 85% of rare-earth content from 1,200 metric tons of scrap motors yearly.

- October 2025: ABB acquired a Swiss additive-manufacturing specialist for USD 107 million, gaining rapid rotor-prototype capabilities.

- September 2025: Rockwell Automation released Allen-Bradley MP-Series liquid-cooled servo motors delivering 6.5 Nm/kg torque density.

Global Permanent Magnet Motor Market Report Scope

A permanent magnet motor is a type of brushless electric motor that uses permanent magnets rather than winding. Permanent magnet motors are more efficient than traditional induction motors or motors with field winding in high-efficiency applications like electric vehicles.

The Permanent Magnet Motor Market Report is Segmented by Motor Type (Permanent Magnet AC Motor, Permanent Magnet DC Motor, Brushless DC Motor, Hermetic Motor), Magnetic Material Type (Neodymium Iron Boron, Samarium Cobalt, Ferrite, Nanocomposite NdFeB), Power Rating (Up to 4 kW, 4-22 kW, 22-75 kW, 75 kW and Above), Cooling Method (Air-Cooled, Liquid-Cooled, Oil-Cooled, Hybrid Cooling), End-User Industry (Automotive, Industrial Automation, Energy, Water and Wastewater Management, Mining Oil and Gas, Aerospace and Defense, Consumer Electronics, Healthcare Equipment), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Permanent Magnet AC Motor |

| Permanent Magnet DC Motor |

| Brushless DC Motor |

| Hermetic Motor |

| Neodymium Iron Boron |

| Samarium Cobalt |

| Ferrite |

| Nanocomposite NdFeB |

| Up to 4 kW |

| 4-22 kW |

| 22-75 kW |

| 75 kW and Above |

| Air-Cooled |

| Liquid-Cooled |

| Oil-Cooled |

| Hybrid Cooling |

| Automotive |

| Industrial Automation |

| Energy (Wind and Hydro) |

| Water and Wastewater Management |

| Mining, Oil and Gas |

| Aerospace and Defense |

| Consumer Electronics |

| Healthcare Equipment |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Motor Type | Permanent Magnet AC Motor | |

| Permanent Magnet DC Motor | ||

| Brushless DC Motor | ||

| Hermetic Motor | ||

| By Magnetic Material Type | Neodymium Iron Boron | |

| Samarium Cobalt | ||

| Ferrite | ||

| Nanocomposite NdFeB | ||

| By Power Rating | Up to 4 kW | |

| 4-22 kW | ||

| 22-75 kW | ||

| 75 kW and Above | ||

| By Cooling Method | Air-Cooled | |

| Liquid-Cooled | ||

| Oil-Cooled | ||

| Hybrid Cooling | ||

| By End-User Industry | Automotive | |

| Industrial Automation | ||

| Energy (Wind and Hydro) | ||

| Water and Wastewater Management | ||

| Mining, Oil and Gas | ||

| Aerospace and Defense | ||

| Consumer Electronics | ||

| Healthcare Equipment | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the permanent magnet motor market today?

The market reached USD 57.94 billion in 2026 and is projected at USD 89.47 billion by 2031, reflecting a 9.08% CAGR.

Which end-user segment is expanding fastest?

Renewable-energy operators, notably offshore wind and modernized hydropower plants, are growing at 9.90% CAGR as they adopt direct-drive permanent-magnet generators.

Why are liquid-cooled motors gaining popularity?

800-volt electric-vehicle platforms and high-speed industrial spindles push current densities that air cooling cannot manage, so liquid jackets unlock 15-20% higher continuous power within the same footprint.

How are suppliers mitigating rare-earth price volatility?

Manufacturers pursue grain-boundary diffusion to cut heavy rare-earth usage and invest in recycling ventures that reclaim up to 85% of magnet material from end-of-life motors.

Which regions are investing in local rare-earth supply?

The United States and European Union are funding separation plants and recycling facilities aimed at reducing import dependence to below 50% and sourcing 15% locally, respectively.

What role do regulations play in adoption?

Upcoming IE4 and IE5 efficiency mandates in the United States, Europe, and Japan effectively steer new and replacement motors toward permanent-magnet or synchronous-reluctance designs that meet higher efficiency thresholds.

Page last updated on: