E-House Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.8 Billion |

| Market Size (2031) | USD 2.40 Billion |

| Growth Rate (2026 - 2031) | 5.86% CAGR |

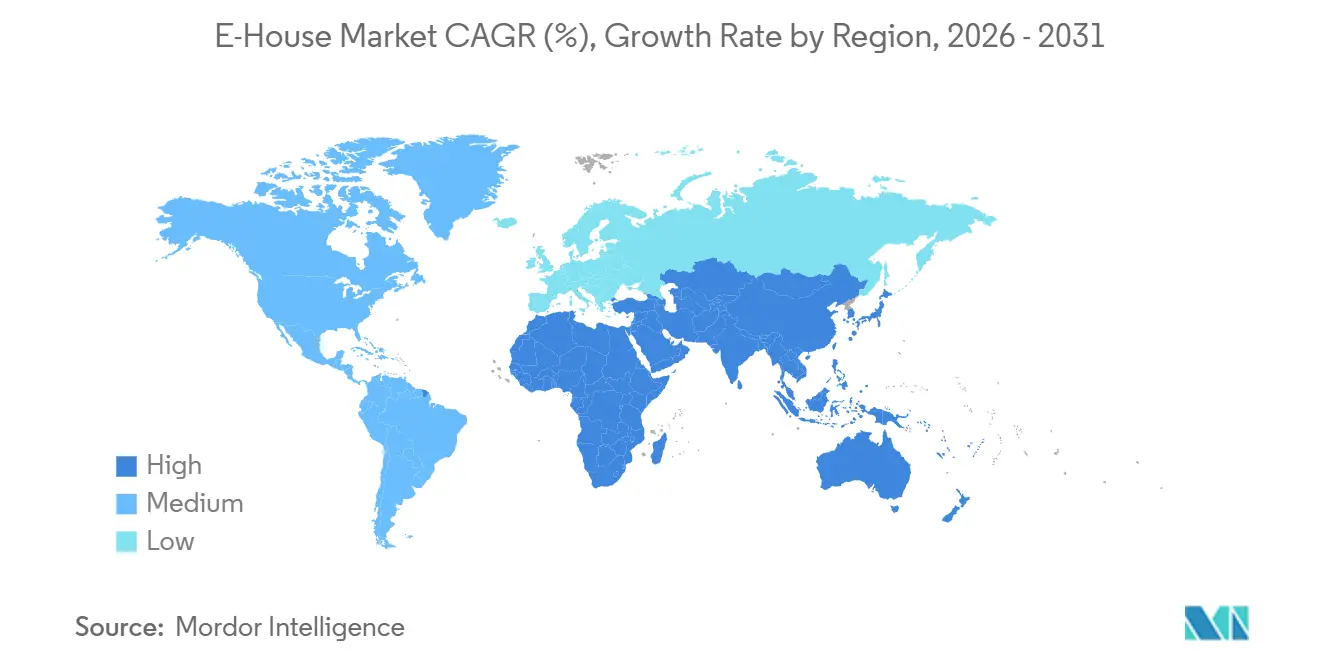

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

E-House Market Analysis by Mordor Intelligence

The E-House market size is projected to be USD 1.70 billion in 2025, USD 1.80 billion in 2026, and reach USD 2.40 billion by 2031, growing at a CAGR of 5.86% from 2026 to 2031. Surging demand for plug-and-play electrical infrastructure is altering procurement patterns, because factory-assembled modules shorten on-site work from months to weeks and lower construction risk. Utilities are embracing the approach to accelerate grid upgrades, while data-center developers value the ability to pre-commission power blocks that mirror the pacing of server deployments. Adoption is also buoyed by stricter environment, health, and safety rules that favor controlled manufacturing over field fabrication. Competitive pressure from price-aggressive regional players is pushing global suppliers toward flexible product tiers that balance cost and functionality, and the pending sulfur-hexafluoride phase-out is catalyzing a wider shift toward digital, SF₆-free switchgear.

Key Report Takeaways

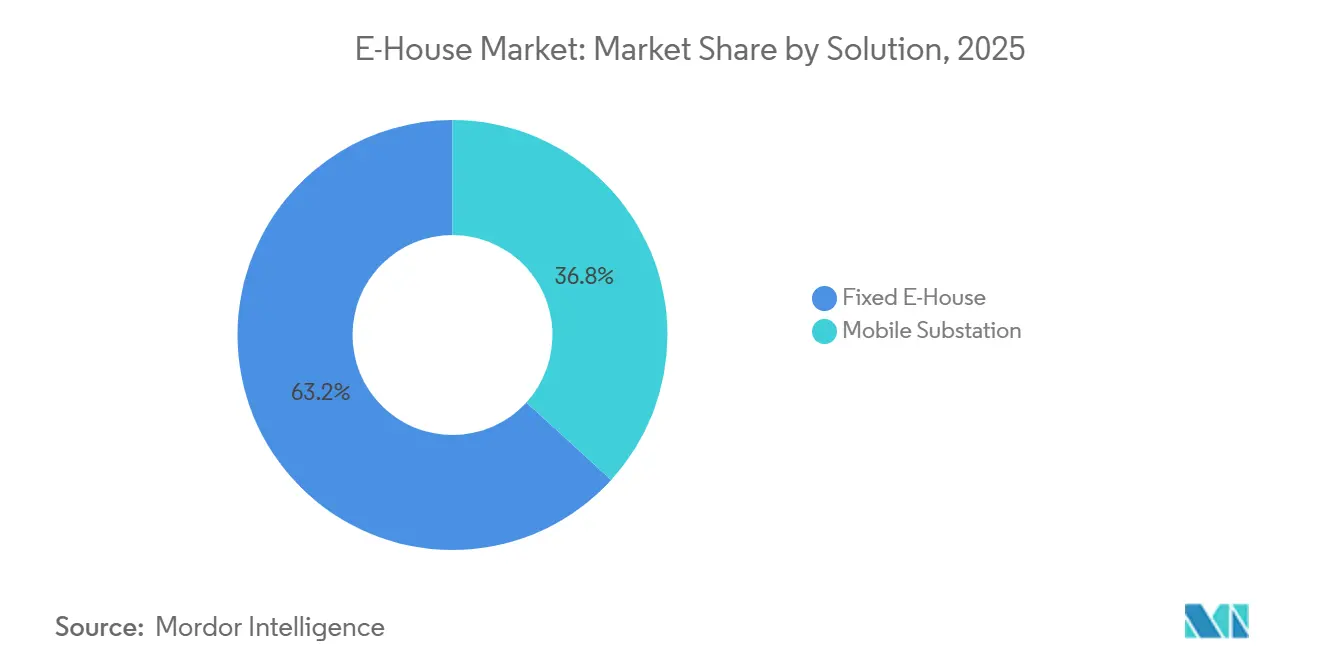

- By solution, fixed units captured 63.23% of 2025 revenue, whereas mobile substations are advancing at a 6.10% CAGR to 2031.

- By voltage rating, medium-voltage configurations held 55.81% of 2025 share, while high-voltage units are on track for a 7.60% CAGR through 2031.

- By application, utilities commanded 49.31% of 2025 revenue, yet data-center deployments are expanding fastest at an 8.14% CAGR to 2031.

- By component, switchgear led with 42.62% of 2025 revenue, and protection and control systems represent the fastest element, growing at an 8.31% CAGR.

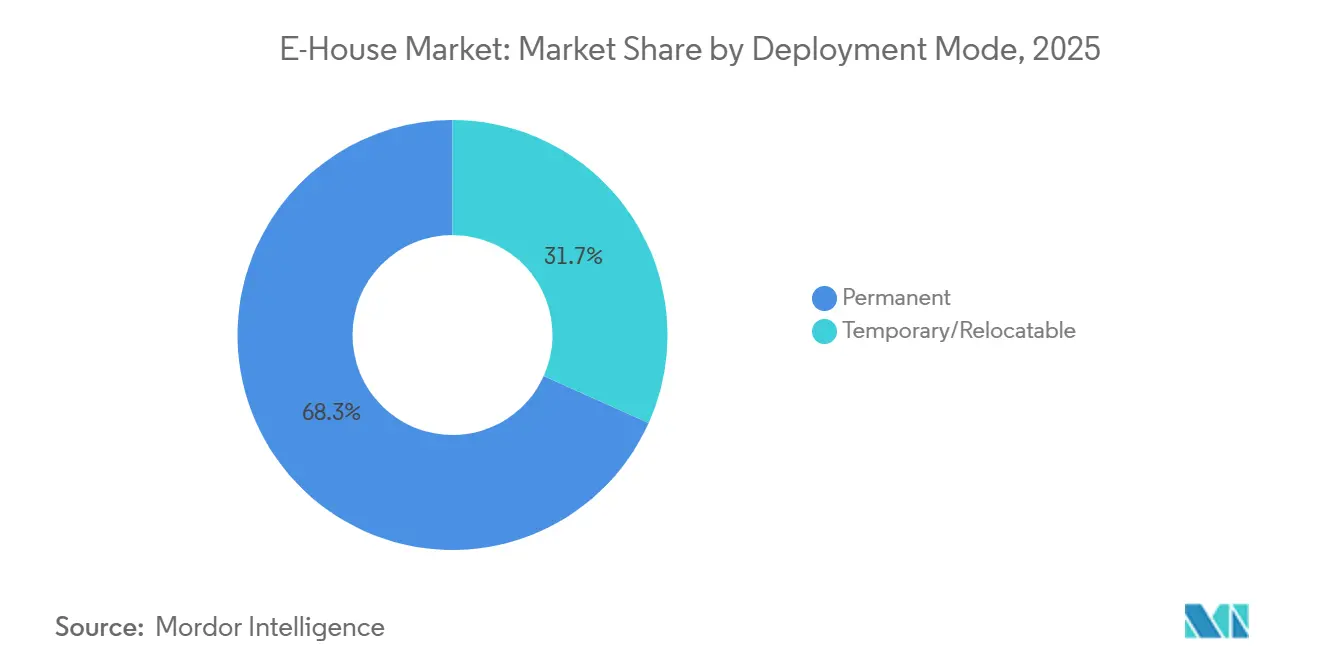

- By deployment mode, permanent installations accounted for 68.29% of 2025 revenue, but temporary and relocatable units are set to register a 5.99% CAGR to 2031.

- By geography, Asia-Pacific contributed 32.53% of global 2025 revenue, whereas the Middle East is forecast to post the highest regional CAGR of 9.42% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global E-House Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of renewable-energy projects requiring modular substations | +1.8% | Global, with concentration in APAC, Middle East, and South America | Long term (≥ 4 years) |

| Electrification of remote industrial and mining sites | +1.2% | APAC core, spill-over to Middle East and Africa, South America mining corridors | Medium term (2-4 years) |

| Replacement of SF₆ with eco-friendly GIS technologies | +0.9% | Global, EU and North America leading regulatory adoption | Short to Medium term (≤ 4 years) |

| Digitalization and remote monitoring for predictive maintenance | +0.8% | Global, with early gains in North America, Europe, and developed APAC markets | Medium term (2-4 years) |

| Demand for fast-deployable power for edge data-centers and 5G nodes | +0.7% | North America and APAC, urban and peri-urban clusters | Short term (≤ 2 years) |

| Resilience spending on modular grid assets for climate and cyber threats | +0.6% | Global, with priority in coastal and storm-prone regions | Medium to Long term (2-4+ years) |

| Source: Mordor Intelligence | |||

Rapid Expansion Of Renewable-Energy Projects Requiring Modular Substations

Utility-scale solar and wind installations are being completed 12–18 months faster than traditional substations, creating a timing gap that factory-built E-Houses bridge by reducing on-site commissioning to roughly one month.[1]Source: Hitachi Energy, “Grid-eXpand Modular Substation Solutions,” hitachienergy.com Saudi Arabia earmarked USD 7 billion in 2025 for grid links that incorporate standardized modules, and 22% of associated contracts already specify E-House designs. Similar policy moves in India, where 15 gigawatts of solar capacity tendered in 2025 carried mandatory modular substation clauses, demonstrate how procurement rules are institutionalizing the concept. Strong demand for 220 kilovolt and 400 kilovolt step-up units is feeding a 7.60% CAGR in the high-voltage segment through 2031. Developers now place E-House orders 9–12 months ahead of site preparation to secure factory slots, reflecting extended transformer lead times that reached 52 weeks in 2025.

Electrification Of Remote Industrial And Mining Sites

Operators in Australia, Chile, and sub-Saharan Africa are swapping diesel gensets for grid-connected E-House substations to curb fuel bills by roughly 45% and satisfy Scope 2 emission targets. Rio Tinto’s Pilbara mines introduced six mobile units in 2025, cutting diesel use by 180 million liters and avoiding 480,000 metric tons of CO₂-equivalent emissions.[2]Source: Rio Tinto, “Pilbara Electrification Program Reduces Diesel Use,” riotinto.com Temporary mobile designs, which represented 31.71% of 2025 revenue, suit exploration phases and are forecast to climb at 5.99% through 2031. Oil and gas producers in the Permian Basin report 25% lower completion costs after adopting electric-fracturing fleets powered by E-Houses. Schneider Electric’s microgrid integration, rolled out in 2025, enables demand-response income streams, proving that modular substations can double as active grid resources.

Replacement Of SF₆ With Eco-Friendly GIS Technologies

The European Union ban on sulfur hexafluoride in medium-voltage switchgear effective January 2026 has accelerated the transition to vacuum and dry-air solutions.[3]Source: European Commission, “Regulation on Fluorinated Greenhouse Gases,” ec.europa.eu ABB’s g³ portfolio attracted 340 orders in 2025, equal to 12% of the firm’s medium-voltage revenue. Siemens’ clean-air switchgear met IEC type-testing in 2025, and GE Vernova launched an SF₆-free E-House platform that captured 68 orders within nine months. Although compliance adds 8–12% to bill-of-materials cost, scale efficiencies are expected to bring parity with legacy designs by 2028. Utilities are therefore opting to replace whole modules rather than upgrade field-installed equipment, which minimizes outage windows.

Digitalization And Remote Monitoring For Predictive Maintenance

Grid operators are embedding IEC 61850-compliant relays and sensors that predict failures well before they occur. Schneider Electric’s Asset Advisor prevented unplanned outages by up to 40% across 1,200 substations as of end-2025. Eaton’s Brightlayer, integrated during the same period, streams busbar temperature and breaker-wear data to cloud dashboards. Regulatory mandates in North America now require critical fault data to reach control rooms within two seconds, a standard that analog relays cannot satisfy. Duke Energy’s deployment of 85 digitally enabled E-House units in 2025 produced a 22% cut in mean-time-to-repair. Suppliers offering integrated hardware-software packages earn 15–20% price premiums because utilities value the reduced operational risk.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX and limited financing in developing nations | -1.5% | Emerging markets in Africa, South Asia, and Southeast Asia | Medium to Long term (2-4+ years) |

| Availability of low-cost containerised switchgear packages | -0.8% | Global, with a concentration in price-sensitive markets | Short to Medium term (≤ 4 years) |

| Logistical constraints in relocating large E-House modules | -0.5% | Global, acute in regions with underdeveloped transport infrastructure | Medium term (2-4 years) |

| Utility interconnection approval delays for mobile substations | -0.4% | North America, EU, and developed APAC markets with complex regulatory frameworks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX And Limited Financing In Developing Nations

Turnkey E-House substations cost 25–35% more than containerized assemblies, straining budgets where concessional capital is scarce. Nigeria’s transmission utility secured only 40% of its USD 1.2 billion modernization plan in 2025 because lenders hesitated to finance movable assets. Developers in Indonesia shifted 18 planned purchases to locally fabricated containers costing USD 800,000 each, compared with USD 1.3 million for European turnkey solutions. Because many jurisdictions refuse to treat mobile units as real estate, sponsors cannot pledge them as collateral, which pushes weighted-average funding costs up by 2–3 percentage points. Although the African Development Bank offered a USD 500 million guarantee facility in 2025, only 12 projects qualified due to protracted approval cycles.

Availability Of Low-Cost Containerised Switchgear Packages

Manufacturers such as TGOOD and LS Electric sell medium-voltage switchgear housed in shipping containers for USD 600,000–900,000, roughly 30% below full E-House solutions, and have taken 42% of India’s collector-substation awards in 2025. Even after factoring transformer and HVAC add-ons, total installed cost stays 15–20% lower. In response, Tier-1 players are releasing stripped-down variants that omit redundancy features but threaten to cannibalize premium lines. Utilities in Brazil and Mexico specify container packages for rural projects where ambient temperatures seldom exceed 35 °C, eliminating the need for climate control and saving USD 80,000–120,000 per site. The price gap is therefore sharpest in low-voltage settings below 1 kilovolt, where technical complexity is limited.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Mobile Units Gain Traction In Disaster-Recovery Fleets

Fixed designs dominated revenue at 63.23% in 2025, underscoring their role in long-life utility and industrial assets that justify deep foundations and 25-year HVAC systems. The E-House market share advantage reflects confidence in structures that support seismic loads and corrosive environments. Meanwhile, the mobile substation slice is projected to clock a 6.10% CAGR through 2031, propelled by utilities seeking rapid storm recovery and miners wanting relocatable power blocks.

Duke Energy enlarged its hurricane fleet to 42 trailer units in 2025, restoring service to 180,000 customers within 72 hours of Hurricane Helene. Leasing models priced at USD 35,000–50,000 per month from specialist rental firms further reduce capital strain for short-cycle users. Fixed platforms are also evolving: Siemens’ 2025 release allows operators to bolt on extra switchgear without downtime, preserving the fixed segment’s lead while offering modular flexibility.

By Voltage Rating: High-Voltage Segment Accelerates With Transmission Upgrades

Medium-voltage equipment between 1 kilovolt and 35 kilovolts held 55.81% of 2025 revenue, because most distribution substations fall within this band. The E-House market size for the medium bracket remains anchored by standardized IEEE and IEC designs that streamline procurement. High-voltage modules above 35 kilovolts, however, are expanding at a 7.60% CAGR as nations connect offshore wind and hydropower to distant load centers.

National Grid’s eight high-voltage units for the Dogger Bank project cut site work by 14 months. Low-voltage solutions serve specialist roles in data centers and hospitals, where arc-flash-rated switchgear such as ABB’s 2025 MNS iS delivers enhanced safety. Overall, harmonized seismic and electromagnetic rules published in 2024 make cross-border sourcing easier, accelerating growth at both ends of the voltage spectrum.

By Application: Data Centers Provide The Fastest Lift

Utilities remained the anchor at 49.31% of 2025 revenue, reflecting ongoing replacement of aging grid infrastructure. Yet hyperscale cloud providers are driving the highest growth, with data-center use cases on an 8.14% CAGR trajectory through 2031 as artificial-intelligence inference clusters demand sub-10-millisecond latency. Microsoft added 14 edge sites in 2025, each powered by dual-feed, 20 MVA E-House blocks.

Renewable developers are the next largest adopters, with Siemens delivering 92 collector units in Spain and Portugal during 2025. Oil and gas fleets, miners, and chemicals plants round out demand with niche requirements such as ATEX-certified enclosures. Together these diverse end-users underscore the broad functional reach of modular substations beyond the traditional utility sphere.

By Component: Protection Systems Outpace The Core Switchgear

Switchgear commanded 42.62% of 2025 revenue, anchoring the E-House market share for first-line protection elements. Nevertheless, digital relay packages are forecast to expand at an 8.31% CAGR because operators prioritize condition-based maintenance and two-second fault reporting. Transformers equipped with amorphous-metal cores, commercialized by Hitachi Energy in 2025, further reduce losses by close to 65%.

Busbar systems are shifting toward aluminum alloys that deliver 30% weight savings, trimming transport costs. HVAC and auxiliary modules are adopting variable-speed chillers and free-cooling economizers that cut energy use nearly in half. Uninterruptible power units now operate at 99% efficiency at mid-load, enabling designers to downsize cooling equipment and lower lifetime operating expense.

By Deployment Mode: Permanent Installations Retain A Wide Lead

Permanent projects delivered 68.29% of 2025 revenue, showing that most operators still favor assets with 25-year depreciation schedules. Foundations engineered for seismic resistance, anti-corrosion paint systems, and integrated fire suppression all reinforce this dominance. The E-House market size for temporary and relocatable designs, however, is slated to widen at a 5.99% CAGR, reflecting event power rentals and mining feasibility studies.

Aggreko grew its fleet to 180 mobile units in 2025, serving Western Australia mines, Middle East construction ventures, and post-disaster relief in Southeast Asia. Quick-disconnect couplings let crews dismantle and truck entire substations within 72 hours, suiting phased rollouts. Yet bridge weight limits and narrow roads restrict adoption in dense cities and mountain corridors, meaning fixed installations will continue to dominate heavy-load geographies.

By Component: Advanced Systems Drive Market Evolution

Switchgear still holds leadership at 38%, yet the rapid uptake of digital protection is redrawing the component value chain. Digital-twin diagnostics delivering 97% fault-detection accuracy validate the investment thesis for smart control packages. Transformers, buswork, and HVAC systems now integrate IoT sensors to feed condition-based maintenance dashboards.

Edge computing embedded in the relay rack allows sub-cycle decision-making independent of central SCADA, a critical feature for islanded microgrids. Cable routings are being redesigned as plug-in modules, facilitating factory-acceptance tests that cut on-site commissioning days by 50%. These shifts suggest the E-House market will reward vendors capable of bundling hardware, firmware, and cloud analytics as a unified offer.

Geography Analysis

Asia-Pacific generated 32.53% of global E-House market revenue in 2025, underpinned by China’s USD 45 billion grid-reinforcement outlay and India’s hydrogen-linked renewables drive. State Grid of China installed 340 modular substations during the year to support cross-country power corridors. India’s Solar Energy Corporation incorporated E-House specifications in all 15 gigawatts of solar tenders launched in 2025, cutting execution risk and compressing schedules. Japan’s utility sector positioned 62 mobile units across earthquake zones, confirming that resilience planning is now a mainstream procurement criterion.

The Middle East is forecast to post a 9.42% CAGR through 2031, sustained by Saudi Arabia’s Vision 2030 backbone and the United Arab Emirates’ 75% clean-energy target. NEOM alone ordered 12 high-voltage modules for its 4 gigawatt hydrogen cluster in 2025. Qatar used modular substations to power cooling and desalination assets built for the FIFA World Cup. Africa’s uptake centers on South Africa, Nigeria, and Kenya, where Eskom contracted 14 units for renewable zones in 2025.

Europe and North America together held 45% of 2025 revenue, but regulatory momentum in the European Union, specifically the January 2026 SF₆ ban, positions the region as a technology bellwether. Germany’s Federal Network Agency cleared 28 offshore modules in 2025, each compliant with clean-air GIS rules. In North America, Duke Energy, National Grid, and Pacific Gas and Electric completed large-scale rollouts of IEC 61850 relays that slashed fault-reporting times. South America’s growth pivots on Brazilian and Chilean solar-plus-storage projects that now specify relocatable E-Houses to match incremental buildouts.

Competitive Landscape

Global concentration remains moderate: the top five suppliers, ABB, Siemens, Schneider Electric, Eaton, and GE Vernova, controlled roughly half of 2025 revenue. Their edge lies in vertically integrated transformer and gas-insulated switchgear manufacturing, which safeguards margins in capital-intensive high-voltage orders. Regional assemblers, particularly in China, erode pricing at the medium-voltage level by bundling containerized packages that come in 25–35% cheaper, pushing incumbents to offer value-strip variants.

Technology differentiation now hinges on digital overlays and SF₆-free designs. Schneider Electric’s EcoStruxure suite and Eaton’s Brightlayer platform deliver cloud analytics that foresee transformer failures six to nine months in advance, allowing suppliers to charge 15–20% premiums. ABB’s 2025 patent for temperature-sensing busbars exemplifies incremental hardware innovation. GE Vernova’s g³-ready line found rapid market uptake because utilities face statutory phase-out clocks.

Business models are broadening. Aggreko and United Rentals popularized 12-month leasing at USD 35,000–50,000 per month for 15 MVA trailers, drawing miners and event organizers who balk at outright purchase. Joint ventures such as Siemens and Bechtel’s 2025 partnership illustrate how engineering, procurement, and construction firms blend with OEMs to capture single-source contracts from data-center hyperscalers. White-space potential persists in sub-Saharan Africa and Southeast Asia, where slow grid extensions create a niche for relocatable assets that stand in until permanent infrastructure arrives.

E-House Industry Leaders

ABB Ltd.

Siemens AG

Eaton Corporation Inc.

Schneider Electric SE

Electroinnova S.L.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: ABB won a USD 180 million order for 42 high-voltage modules at NEOM’s hydrogen complex, coupled with a 10-year predictive-maintenance deal.

- December 2025: Siemens Energy and Larsen and Toubro formed an Indian manufacturing joint venture targeting 120 units per year by Q3 2026.

- November 2025: Schneider Electric launched an SF₆-free modular platform in Europe and secured 85 utility orders within six weeks.

- October 2025: Eaton acquired 60% of Zest WEG’s South African unit for USD 240 million, gaining access to mining clients across the region.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

We track factory-built E-Houses that carry medium or high-voltage switchgear, transformers, and control gear inside a mobile, climate-controlled shell. Units leave the factory tested for utilities, renewables, mines, and heavy plants. According to Mordor Intelligence, the market earned USD 1.70 billion in 2025.

Scope exclusion: Rental fleets, battery-only containers, and permanent concrete substations lie outside scope.

Segmentation Overview

- By Solution

- Fixed E-House

- Mobile Substation

- By Voltage Rating

- Low Voltage (≤1 kV)

- Medium Voltage (1–35 kV)

- High Voltage (>35 kV)

- By Application

- Utilities

- Industrial

- Oil and Gas

- Mining and Minerals

- Chemicals

- Data Centres

- Renewables (Solar/Wind)

- Other Industrial Applications

- By Component

- Switchgear

- Transformer

- Busbar and Cables

- Protection and Control Systems

- HVAC and Auxiliary Systems

- Others

- By Deployment Mode

- Permanent

- Temporary/Relocatable

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Argentina

- Mexico

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with switchgear integrators, EPC engineers, and grid planners across North America, Europe, the Gulf, and ASEAN. Their views on prices, build times, and adoption triggers filled gaps that desk work could not.

Desk Research

We merged IEA renewable tables, World Bank grid dashboards, UN Comtrade HS 8537 flows, and ICMM mining lists to gauge demand, then scanned utility tenders, patent files, and 10-K filings for deal values. Paid snapshots from D&B Hoovers and Dow Jones Factiva verified supplier scale. The examples above are illustrative; many further sources shaped validation.

Market-Sizing & Forecasting

We opened with a top-down model that links enclosure penetration to renewable MW adds, grid spend, and mining pipelines, then balanced outputs with sampled bottom-up ASP × volume rolls from supplier talks. Inputs, including renewables growth, mix shifts, ASP trends, metal costs, and regional grid outlays, feed a multivariate regression to 2030. Calibrated penetration ratios plug small regional holes.

Data Validation & Update Cycle

Results clear variance screens, peer ratios, and two-tier analyst review. Models refresh yearly and reopen when large utility awards or raw material shocks shift assumptions.

Why Mordor's E-House Baseline Commands Confidence

Published figures differ because scope, price bases, and refresh timing vary.

Key gap drivers include counting low-voltage skids, inflation deflators on ex-factory prices, and whether relocatable units book as new sales.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.70 B (2025) | Mordor Intelligence | - |

| USD 1.84 B (2025) | Global Consultancy A | Omits HV units, uses turnkey pricing |

| USD 1.51 B (2023) | Industry Journal B | Uses older shipment data, omits renewables |

| USD 2.30 B (2024) | Regional Consultancy C | Counts rental fleets and service deals |

These contrasts show how our tight scope, normalized prices, and timely refresh give decision-makers a baseline they can repeat and stress-test with little effort.

Key Questions Answered in the Report

What is the projected size of the E-House space by 2031?

It is forecast to reach USD 2.40 billion in 2031, advancing at a 5.86% CAGR from 2026.

Which region is expected to post the fastest growth over the next five years?

The Middle East is on track for roughly a 9.42% CAGR through 2031, lifted by Vision 2030 transmission build-outs and large hydrogen projects.

Why are data-center operators turning to modular substations?

Factory-assembled power blocks synchronize with rapid server rollouts and support the sub-10-millisecond latency that artificial-intelligence workloads demand.

How is the European sulfur-hexafluoride ban reshaping equipment designs?

Vendors are shifting to vacuum and dry-air switchgear, which adds about 8–12% to materials cost yet removes SF₆ leakage risk and ensures regulatory compliance.

Page last updated on: