Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 18.85 Billion |

| Market Size (2031) | USD 23.6 Billion |

| Growth Rate (2026 - 2031) | 4.60% CAGR |

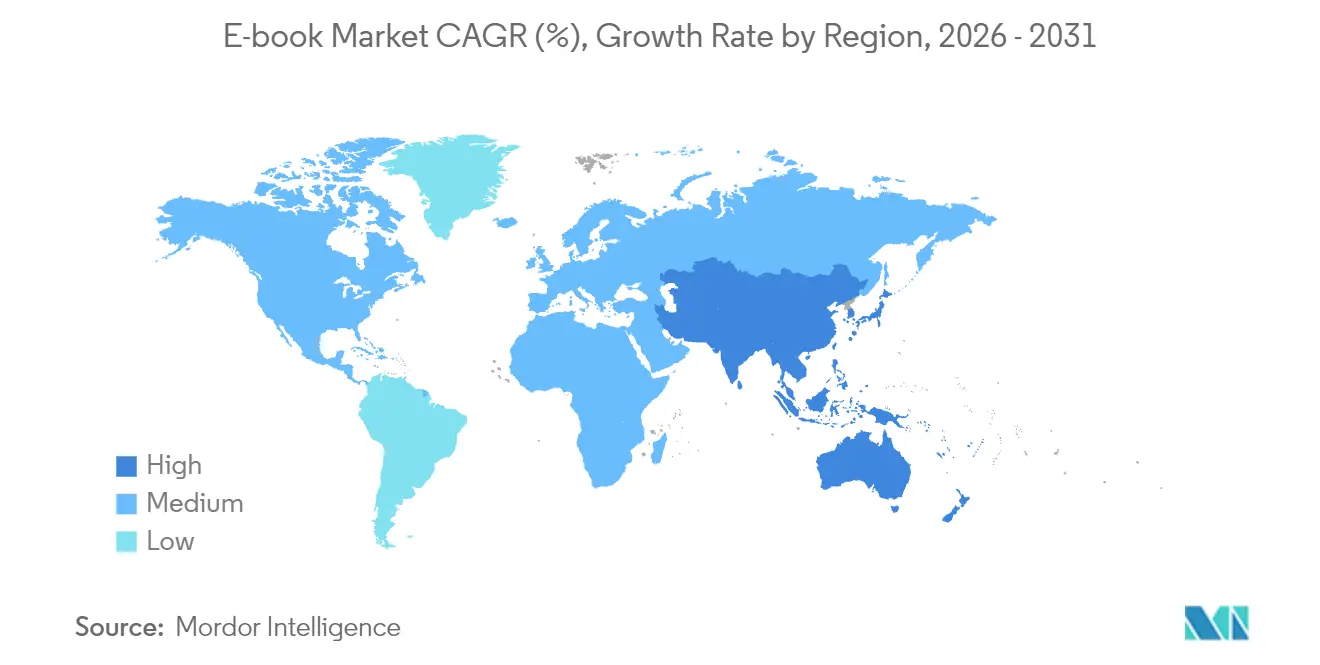

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

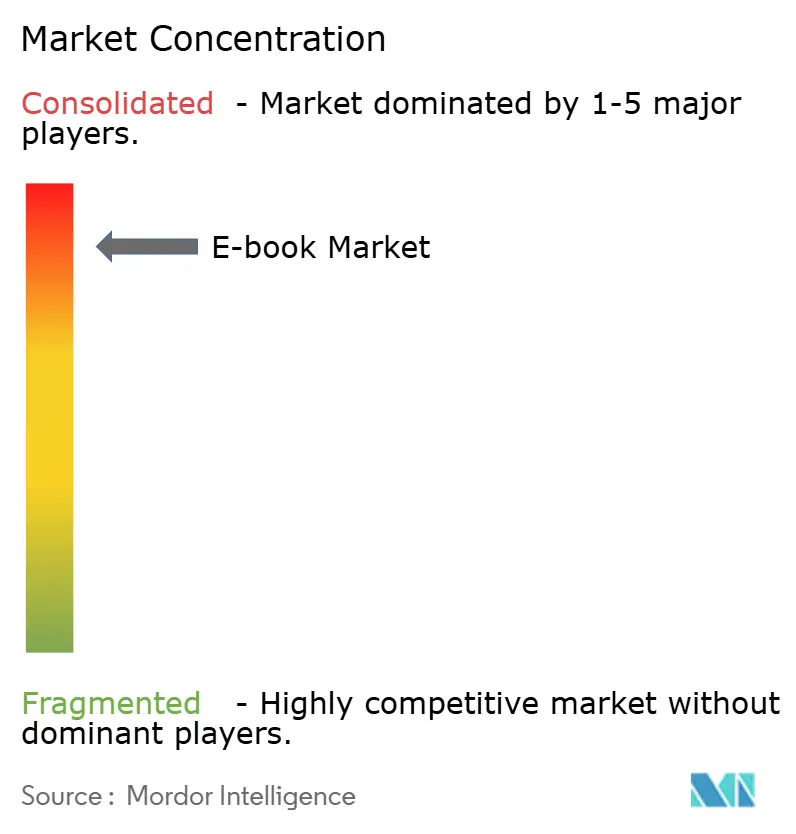

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

E-book Market Analysis by Mordor Intelligence

The e-book market size is expected to grow from USD 18.02 billion in 2025 to USD 18.85 billion in 2026 and is forecast to reach USD 23.6 billion by 2031 at 4.6% CAGR over 2026-2031. Subscription-led business models, institutional licensing momentum, and mobile-first reading habits are the three most powerful forces shaping the e-book market. Revenue predictability underpins publisher investment in platform-native experiences such as interactive textbooks and webtoon serialization. Smartphone ubiquity drives microtransaction experimentation and social discovery features that deepen reader engagement. Meanwhile, blockchain-enabled rights management is beginning to streamline author compensation, mitigating long-running disputes over digital royalties. Competitive intensity is moderate: Amazon’s Kindle ecosystem remains the anchor platform, but regional disruptors from Asia Pacific and library-centric vendors are eroding any path toward monopoly dominance.

Key Report Takeaways

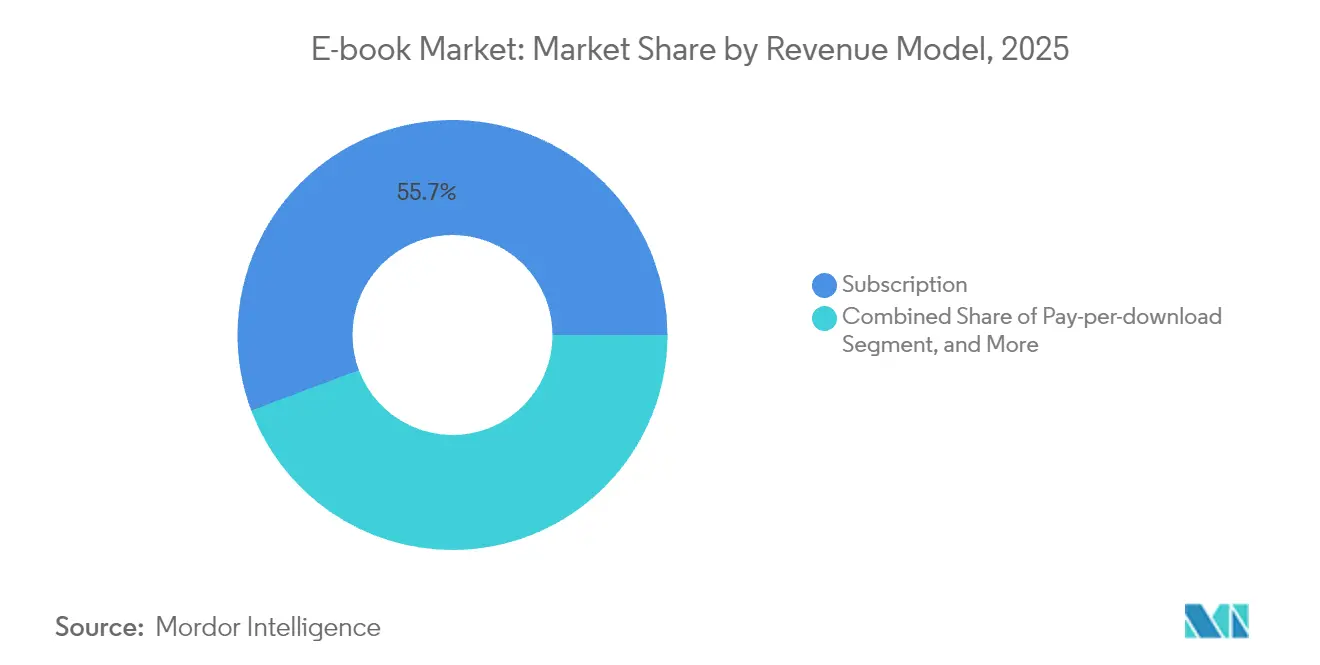

- By revenue model, subscription platforms captured 55.72% of the e-book market share in 2025; institutional licensing revenue is advancing at a 5.05% CAGR through 2031.

- By genre, fiction led with 44.02% share of the e-book market in 2025, while comics and graphic novels are expanding fastest at a 4.88% CAGR to 2031.

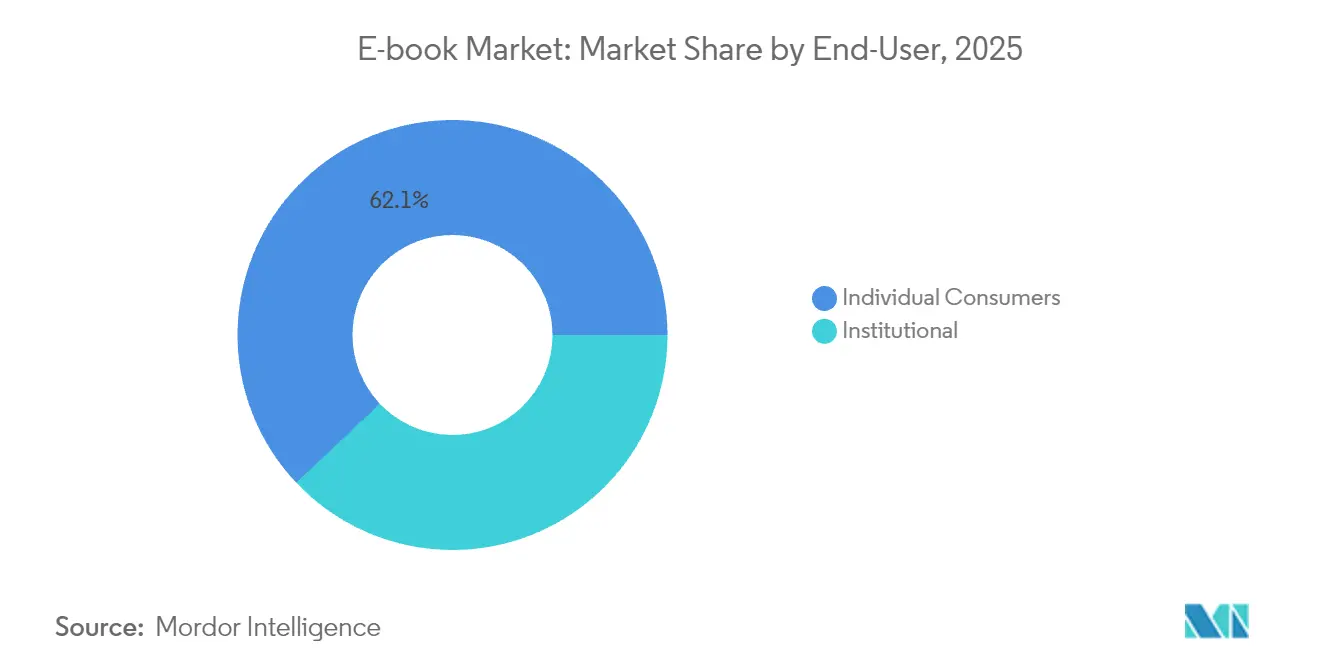

- By end-user, individual consumers accounted for 62.05% of the e-book market size in 2025; public library demand is rising at a 5.32% CAGR through 2031.

- By geography, North America commanded 39.45% of the e-book market share in 2025, whereas Asia Pacific is on track for the highest regional growth at a 4.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global E-book Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing penetration of mobile devices | +1.2% | Global, with strongest impact in Asia Pacific | Medium term (2-4 years) |

| Expanding global internet connectivity | +0.8% | Global, with emphasis on emerging markets | Long term (≥ 4 years) |

| Growth of digital education and e-learning | +1.1% | North America and Europe core, expanding to APAC | Short term (≤ 2 years) |

| Rising adoption of subscription-based reading platforms | +1.3% | Global, led by North America and Europe | Medium term (2-4 years) |

| Blockchain-enabled rights management and micropayments | +0.6% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Publisher D2C storefront integration with CRM data | +0.4% | North America and Europe primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Penetration of Mobile Devices

Smartphone saturation has shifted the center of gravity for digital reading away from dedicated e-readers and toward always-connected handsets. Publishers capitalize on this reality by releasing bite-sized content episodes, optimizing for vertical scrolling, and layering in gamified achievements that reinforce daily reading streaks. Display manufacturers are refining glare-free OLED screens and adaptive refresh rates that reduce eye strain during extended reading sessions. The rise of AI-driven recommendation engines further personalizes in-app discovery, boosting completion rates and average reading time per session. In Asia Pacific, where handset upgrades occur on rapid cycles, premium devices now ship with pre-installed reading apps that create a default pathway into the e-book market.[1]WEBTOON Entertainment Inc., “Q1 2025 Financial Results,” webtoon.com

Expanding Global Internet Connectivity

Next-generation broadband rollouts and 5G backhaul investments expand addressable audiences in markets historically constrained by bandwidth cost. GSMA’s Digital Nations framework shows 18 Asia Pacific governments prioritizing ubiquitous coverage as a pillar of economic competitiveness.[2]GSMA Intelligence, “Digital Nations in Asia Pacific,” gsma.com Faster, cheaper connections enable publishers to embed high-resolution artwork, audio snippets, and short-form video without incurring intolerable load times. Dynamic pricing tied to regional bandwidth quality is also gaining traction: readers on slower networks can opt for lower-bitrate packages at reduced prices, preserving accessibility while respecting infrastructure realities. Enhanced connectivity likewise removes frictions for cloud synchronization, ensuring seamless progress tracking across multiple devices.

Growth of Digital Education and E-learning

Educational institutions now bake e-book integration directly into learning management systems instead of treating it as a supplemental format. U.S. university procurement budgets increasingly earmark multiyear digital content contracts that guarantee perpetual updates, avoiding obsolete print inventories. Adaptive assessment modules embedded within interactive textbooks measure student comprehension in real time, signaling where faculty should intervene. Corporate training departments mirror academia by curating skill-based libraries that employees can access on demand, shortening time-to-competency. These institutional commitments reduce seasonality, making academic publishing revenue less volatile and enhancing the defensive qualities of the e-book market size. Observationally, textbook publishers report double-digit declines in print sell-through even as overall pedagogical content consumption rises.

Rising Adoption of Subscription-Based Reading Platforms

Publisher economics are migrating from one-time purchase toward recurring revenue, enabling richer lifetime value calculations and more aggressive customer-acquisition spend. PublishDrive’s Everand service illustrates the model’s promise, having crossed USD 125 million in annualized revenue while still expanding geographic coverage. Yet balancing reader affordability with equitable author payouts remains contentious; algorithmic allocation of subscription pools can depress earnings for niche titles. In response, hybrid platforms now offer “add-on unlocks” that grant early access to bestselling chapters for micro-fees atop the core subscription. This tiered approach dampens churn risk while generating incremental revenue that would have been absent in a strict all-you-can-read model.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy and copyright issues among e-sellers and authors | -0.7% | Global, with strongest impact in Europe due to GDPR | Short term (≤ 2 years) |

| Persistent preference for print books in emerging markets | -0.9% | Emerging markets in Africa, Latin America, and parts of Asia | Long term (≥ 4 years) |

| Interoperability limitations across e-reader ecosystems | -0.5% | Global, with particular impact in North America and Europe | Medium term (2-4 years) |

| Digital fatigue driving screen-time reduction initiatives | -0.4% | Developed markets, primarily North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Privacy and Copyright Issues Among E-sellers and Authors

Complexities around digital rights management and data usage threaten to fragment distribution ecosystems. European regulators enforce GDPR penalties that can absorb more than 10% of annual digital revenue for small presses struggling to maintain compliant infrastructure. Controlled digital lending lawsuits underscore lingering ambiguity over fair-use boundaries, delaying institutional purchasing decisions and depressing near-term e-book market growth in library channels. Authors increasingly question whether AI companies scrape full texts without consent, prompting early adopters like Johns Hopkins University Press to craft explicit AI licensing frameworks that guarantee compensation for model training. Forward-looking publishers explore blockchain timestamping of content transactions to record when, where, and how each copy is accessed, enhancing transparency and auditability.

Persistent Preference for Print Books in Emerging Markets

Cultural attachment to tangible reading experiences, intermittent electricity, and foreign-currency subscription charges converge to sustain physical formats in developing regions. Print remains resilient; five consecutive years of global unit growth testify that screens have not fully eclipsed paper. Local retail networks and school procurement policies still budget heavily for hardcopy textbooks because digital infrastructure is unreliable or absent. In rural Latin America, for instance, shared device ratios exceed three students per tablet, compromising personal study time. Inflationary swings also undermine household willingness to commit to recurring digital fees denominated in USD. Consequently, publishers deploy dual-format strategies, shipping low-cost paperbacks alongside lightweight e-pub files to hedge demand uncertainty.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Revenue Model: Subscription Strength and Institutional Upside

Subscription services commanded 55.72% of 2025 revenue and remain the engine behind the e-book market expansion. Their data-rich environments inform algorithmic commissioning of new series, ensuring that titles debut with pre-qualified audiences. Institutional licensing, chiefly libraries and corporate training portals, shows the sharpest momentum, growing at 5.05% CAGR on a base of high per-user spending. That uptrend contributes meaningfully to the e-book market size even though its user count trails consumer subscriptions. Pay-per-download persists for academic monographs and professional references where perpetual access is mandatory, while freemium models gain traction in cost-sensitive territories by monetizing advertising inventory or unlocking chapters after social sharing actions.

Publishers are engineering workflows around “content-as-a-service,” refreshing digital backlists with real-time errata fixes and multimedia add-ons. This lifecycle extension smooths revenue recognition and strengthens catalog durability. For platforms, subscription churn management has become a science: predictive analytics flag disengaging readers so that curated push notifications or loyalty rewards arrive before cancellation risk peaks. Integrated payment rails simplify tier upgrades, nudging heavy readers toward premium plans that bundle audiobooks or graphic content. These measures reinforce a virtuous loop wherein higher engagement elevates the e-book market share of subscription formats year over year.

By Genre: Fiction Dominance Meets Comics Acceleration

Fiction preserved its leadership at 44.02% of genre revenue in 2025, fueled by cross-platform franchises and rapid inclusion of day-and-date digital releases. High-budget marketing still revolves around novel-to-screen pipelines, with streaming platforms acting as accelerators for digital readership. Despite fiction’s scale, comics and graphic novels clock a quicker 4.88% CAGR, powered by webtoon platforms that convert mobile scrolling into effortless narrative flow. Serialized drop schedules keep fans returning weekly, markedly lifting active-user metrics that underpin platform valuations and, in turn, extend the e-book market size.

Educational publishers amplify nonfiction relevance by embedding assessments, while professional and technical manuals adopt modular chapter sales to serve time-pressed experts. Biography and memoir titles now include interactive timelines and primary-source documents, differentiating them from competing podcasts. Meanwhile, children’s and young-adult categories demonstrate brisk uptakes in gamified storytelling and voice-assisted read-aloud modes, broadening family purchasing baskets. This genre diversification mitigates revenue concentration risks and cushions the e-book industry against cyclical swings in any single content vertical.

By End-User: Consumer Volume Versus Institutional Velocity

Individual readers continue to buy or stream the majority of titles, giving them 62.05% of 2025 spending. Nevertheless, libraries, universities, and businesses are expanding budgets faster, adding 5.32% CAGR to their combined outlays. Each institutional license can cost three to five times more than a consumer edition, directly augmenting the e-book market. Public library consortiums negotiate metered-access terms that balance patron demand against budget ceilings, using data dashboards to optimize hold ratios. Corporate training divisions embed certification quizzes in purchased texts, verifying employee completion and skills transfer.

On the consumer side, segmentation deepens: value-driven readers gravitate toward all-inclusive subscriptions, while collectors pay premiums for deluxe digital editions featuring author annotations. Children’s household usage spikes during school holidays, encouraging publishers to release seasonal activity bundles that integrate reading comprehension exercises. Young-adult audiences prefer community overlays such as live author chats and fan-art contests, which subscription platforms leverage to extend session length. These micro-segment strategies collectively expand the e-book market size by unlocking overlooked pockets of demand.

Geography Analysis

North America retained its 39.45% share in 2025 owing to entrenched e-reader habits, high broadband penetration, and a dense ecosystem of library and academic buyers. Leading platforms invest in AI-generated reading companions that summarize chapters and translate passages on the fly, raising engagement among time-pressed professionals. Regulatory inquiries into platform exclusivity have not yet produced structural remedies, but they do temper acquisition strategies, pushing incumbents to focus on customer-centric feature upgrades rather than aggressive content hoarding.

Asia Pacific charts the fastest regional expansion at a 4.72% CAGR through 2031, propelled by smartphone ubiquity and flexible mobile payment systems. Japanese digital manga revenue has doubled since 2020, while Korean webtoons add recurring IP value thanks to drama and gaming adaptations that rebound consumers back into source titles. GSMA notes that Singapore, South Korea, and Australia achieve near-total 5G coverage, creating fertile ground for bandwidth-heavy interactive books. South-East Asian start-ups experiment with sachet-pricing, selling single chapters for cents, thereby broadening affordability and bolstering the e-book market.

Europe grows steadily on the back of institutional digitization mandates and cross-border content regulation. GDPR compliance engenders consumer trust, elevating subscription conversion rates though it imposes costly data-handling safeguards. Multilingual requirements spur publishers to invest in AI-translation pipelines that reduce localization timelines. Blockchain pilots in Germany and the Netherlands test transparent royalty disbursement, aiming to shorten payment cycles from months to days. In parallel, the UK navigates post-Brexit licensing complexities, leveraging its robust independent press scene to experiment with direct-to-reader bundles that integrate print-on-demand add-ons.

Competitive Landscape

Market concentration is moderate: Amazon wields unmatched scale across device, storefront, and cloud infrastructure, yet regional challengers dilute its influence. WEBTOON leverages creator-first revenue splits and purpose-built mobile user interfaces to dominate serialized comics, expanding English-language reach after its high-profile Disney partnership. Rakuten Kobo focuses on open-ecosystem strategies, collaborating with NetGalley to streamline advance digital copies for reviewer communities.[3]Rakuten Kobo, “Instapaper Integration Announcement,” kobo.com Apple and Google monetize reading time by embedding content inside larger app and media bundles, enriching their broader platform stickiness.

Publishers counterbalance platform leverage through consortium negotiations and direct-sales microsites that preserve first-party consumer data. AI-generated audiobooks and chapter summaries reduce production timelines, enabling backlist monetization at scale. Emerging blockchain utilities promise immutable royalty tracking, although transaction fees remain a hurdle for mass adoption. Regional subscription start-ups deploy hyper-local discovery engines, curating vernacular language catalogs that global giants historically overlook, thereby capturing incremental e-book market share. Overall, competitive dynamics favor hybrid approaches combining traditional ownership perks with subscription convenience, making platform differentiation contingent on personalization algorithms and cross-media interoperability.

E-book Industry Leaders

Amazon.com, Inc.

Rakuten Kobo Inc.

Apple Inc.

Barnes and Noble, LLC

Smashwords, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: WEBTOON and Disney agreed to adapt 100 Marvel and Star Wars titles into vertical-scroll webcomics, underscoring mainstream validation of the format.

- July 2025: Johns Hopkins University Press signed the industry’s first AI model-training license for its catalog, formalizing compensation for large-language model usage.

- April 2025: NetGalley enabled direct “Send to Kobo” wireless delivery for advance review copies, strengthening publisher-to-reviewer workflows.

- April 2025: Amazon launched AI-generated “Recaps” within Kindle, supplying condensed story arcs for complex series to re-engage lapsed readers.

Global E-book Market Report Scope

An ebook is a book written in a digital format or converted to one for use on a computer or a mobile device.

The scope of the study focuses on the market analysis segmented by geography (North America (United States and Canada), Europe (Spain, the United Kingdom, Germany, France, Italy, and Rest of Europe), Asia-Pacific (China, India, Japan, and Rest of Asia-Pacific), Latin America, and the Middle East and Africa).

The market sizes and forecasts are provided in value terms (USD) for all the above segments.

By Revenue Model

| Subscription (all-you-can-read) |

| Pay-per-download |

| Freemium / Ad-supported |

| Institutional licensing |

By Genre

| Fiction |

| Non-fiction |

| Education and Academic |

| Comics and Graphic Novels |

| Professional and Technical |

By End-user

| Individual Consumers | Adults |

| Children and Young Adults | |

| Institutional | K-12 Schools |

| Higher Education | |

| Corporate / Professional Training | |

| Public Libraries |

By Geography

| North America | United States | |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Indonesia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Revenue Model | Subscription (all-you-can-read) | ||

| Pay-per-download | |||

| Freemium / Ad-supported | |||

| Institutional licensing | |||

| By Genre | Fiction | ||

| Non-fiction | |||

| Education and Academic | |||

| Comics and Graphic Novels | |||

| Professional and Technical | |||

| By End-user | Individual Consumers | Adults | |

| Children and Young Adults | |||

| Institutional | K-12 Schools | ||

| Higher Education | |||

| Corporate / Professional Training | |||

| Public Libraries | |||

| By Geography | North America | United States | |

| Canada | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Indonesia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the e-book market in 2026?

The e-book market size is USD 18.85 billion in 2026.

What is the expected growth rate for e-books through 2031?

The market is forecast to expand at a 4.6% CAGR, reaching USD 23.6 billion by 2031.

Which revenue model is most profitable for publishers today?

Subscription services hold 55.72% market share and generate reliable recurring revenue, making them the most lucrative model.

Where is e-book adoption growing fastest regionally?

Asia Pacific leads with a projected 4.72% CAGR as mobile-first reading habits proliferate.

What genre is expanding more rapidly than traditional fiction?

Comics and graphic novels top the growth charts at 4.88% CAGR thanks to webtoon serialization.

Why are libraries important to future market growth?

Public libraries are increasing digital budgets at a 5.32% CAGR, purchasing multi-user licenses that boost institutional revenue streams.

Page last updated on: