Duodenoscopes Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.61 Billion |

| Market Size (2030) | USD 2.20 Billion |

| Growth Rate (2025 - 2030) | 5.53% CAGR |

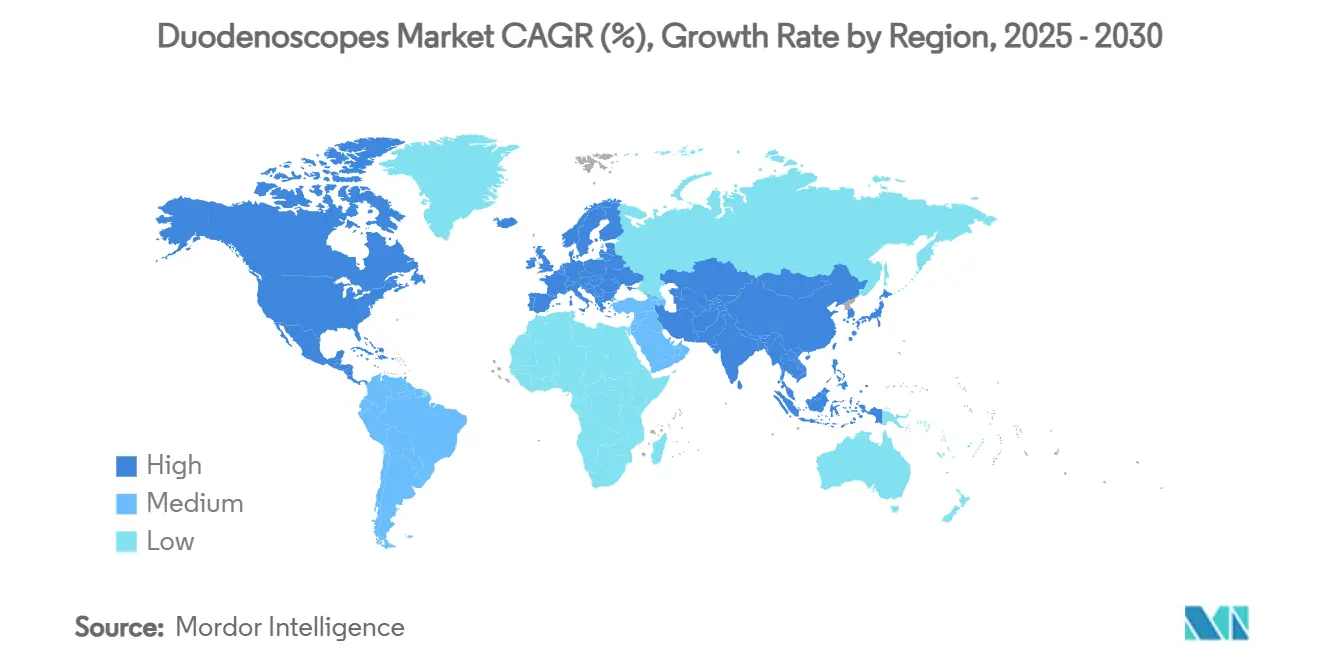

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

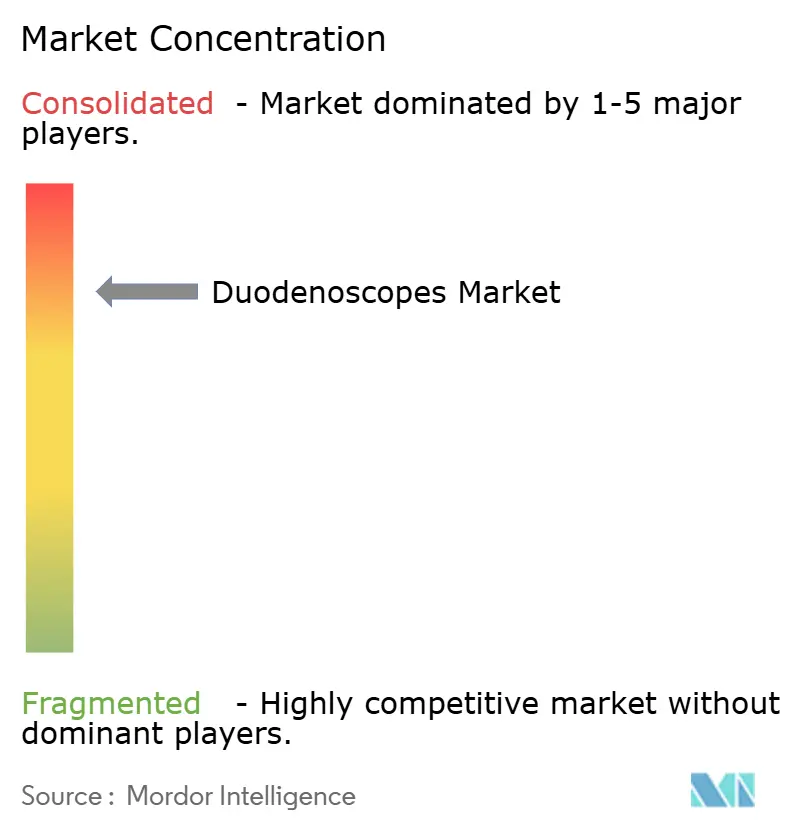

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Duodenoscopes Market Analysis by Mordor Intelligence

The Duodenoscopes Market size is estimated at USD 1.61 billion in 2025, and is expected to reach USD 2.20 billion by 2030, at a CAGR of 5.53% during the forecast period (2025-2030).

A steady climb in endoscopic retrograde cholangiopancreatography (ERCP) procedures, stricter infection-control mandates, and rapid technology upgrades underpin this expansion. Hospitals remain the largest buyers, yet the growing popularity of ambulatory surgery centers (ASCs) signals a gradual shift toward outpatient therapeutic care. Single-use scopes, though still a minority, continue to draw attention in high-volume Western facilities that can weigh infection liabilities against device cost. Meanwhile, Asia Pacific is adding procedure capacity at a brisk pace, encouraging global suppliers to localize production and distribution. Competition now hinges on balanced portfolios that pair reusable platforms with disposable options and advanced reprocessing systems.

Key Report Takeaways

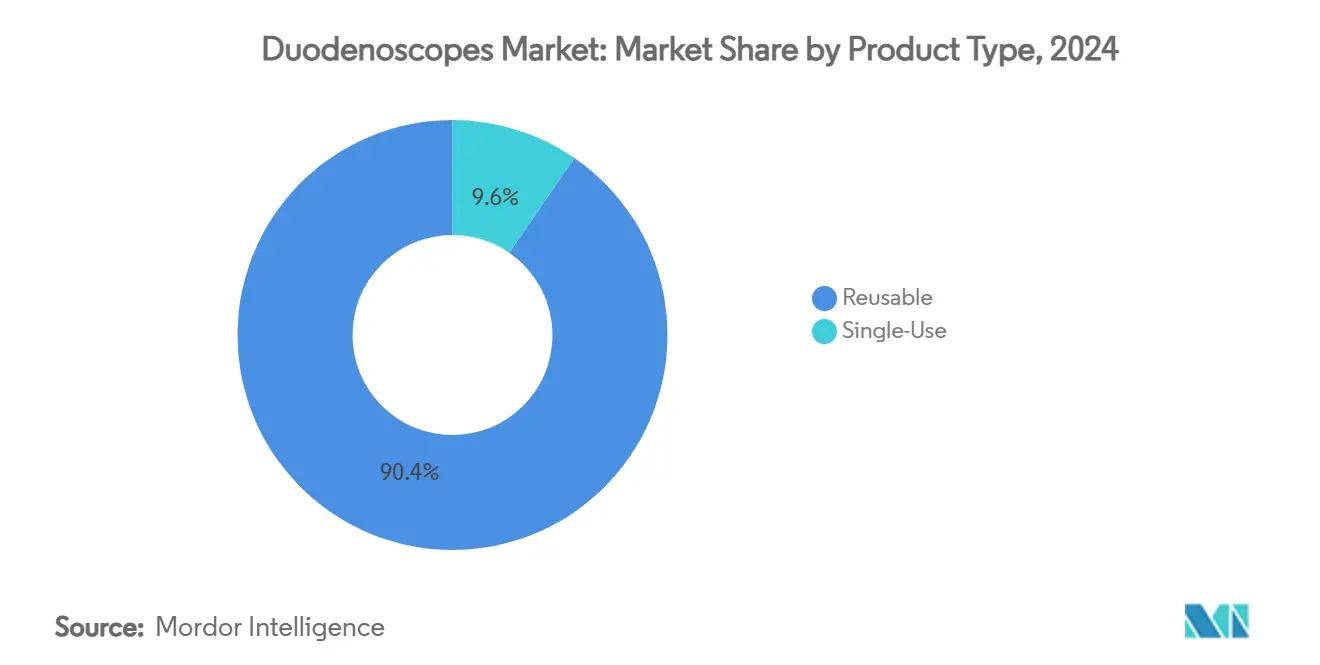

- By product type, reusable devices retained 90.4% of the duodenoscopes market share in 2024; single-use models are projected to post an 18.2% CAGR through 2030.

- By technology, video duodenoscopes accounted for 87.2% of the duodenoscopes market size in 2024 and are forecast to expand at 14.6% CAGR to 2030.

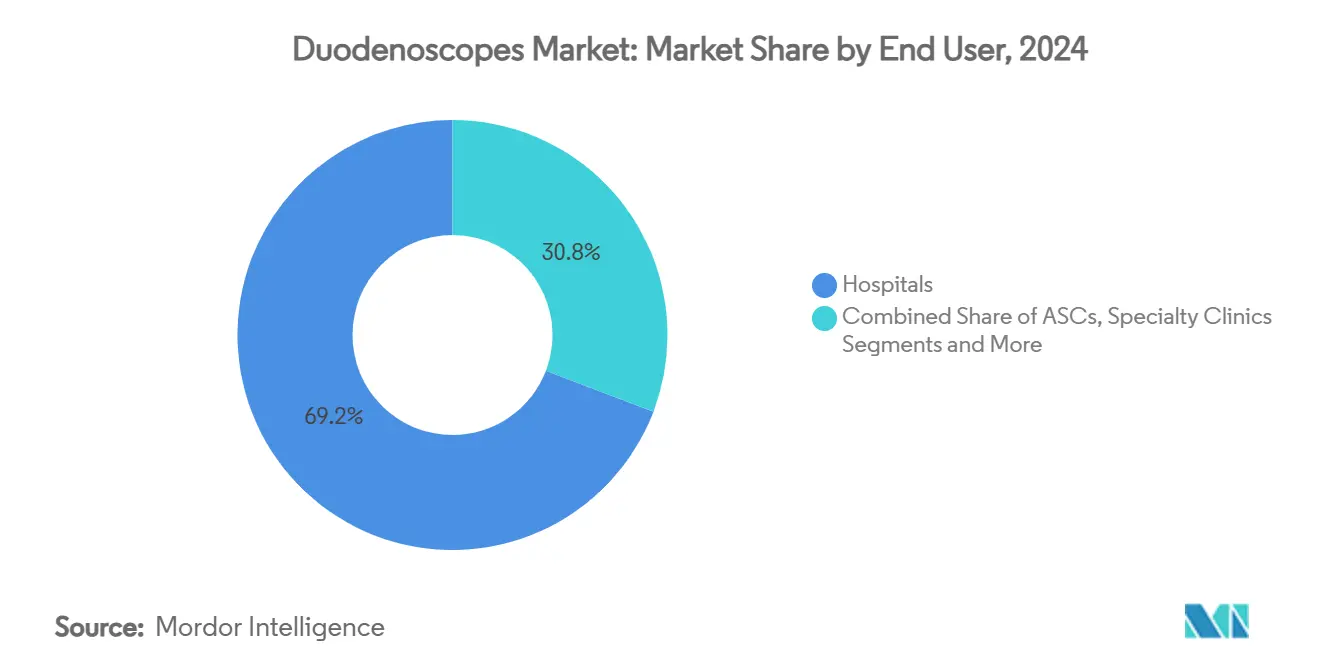

- By end user, hospitals led with 69.2% revenue share in 2024, while ASCs are expected to grow at 10.2% CAGR through 2030.

- By geography, North America commanded 39.9% of the duodenoscopes market in 2024, whereas Asia Pacific is set to grow at 8.8% CAGR over the forecast period.

Global Duodenoscopes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of pancreaticobiliary disorders | +1.80% | Global, higher in Asia Pacific and aging Western populations | Long term (≥ 4 years) |

| Increasing demand for minimally-invasive ERCP procedures | +1.20% | North America and EU lead; APAC following | Medium term (2-4 years) |

| Regulatory shift toward single-use duodenoscopes | +0.90% | North America and EU primary; selective uptake in APAC | Short term (≤ 2 years) |

| Continuous image-quality improvements (HD/4K, AI) | +0.70% | Global with premium adoption in developed markets | Medium term (2-4 years) |

| Cost pressure from ANSI/AAMI ST91-2021 rules | +0.60% | North America primary; EU secondary | Short term (≤ 2 years) |

| Variable-stiffness scopes for altered anatomy | +0.40% | Global, especially complex tertiary centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Pancreaticobiliary Disorders

Incidence of pancreatic cancer jumped from 24,480 cases in 1990 to 42,254 cases in 2021 as recorded by global burden studies, with absolute gallbladder and biliary disease cases climbing 60.1% in the same period.[1]Maolang He et al., “Gallbladder and Biliary Diseases Epidemiological Trends,” BMC Gastroenterology, bmcgastroenterology.biomedcentral.com Aging populations and lifestyle shifts in China, Korea, and other Asia Pacific nations accelerate demand for endoscopic retrograde cholangiopancreatography market, driving growth in the duodenoscopes market. Roughly 12% of the global population shows anatomical variants in the pancreaticobiliary duct junction, of which 29% are linked to malignancy.[2]Juan José Valenzuela-Fuenzalida et al., “Pancreaticobiliary Duct Junction Variants and Cancer,” MDPI, mdpi.com Such complexity calls for sophisticated imaging, boosting premium device uptake. Hospitals, therefore, budget for upgraded duodenoscopes even when capital funds are tight. The underlying disease burden is expected to keep procedure volumes on an upward trajectory well beyond the forecast window.

Increasing Demand for Minimally-Invasive ERCP Procedures

Healthcare systems now favor less‐invasive therapies that shorten stays and lower total costs, prompting steady expansion of ERCP capacity. In 2024, 30 new gastrointestinal endoscopy centers opened in the United States alone, underscoring sustained investment in outpatient infrastructure. Beyond stone extraction, ERCP now addresses complex situations such as endoscopic vacuum therapy, which reports success rates north of 80% in sealing transmural defects.[3]David Hoffman and Christina Cool, “Costs of New Endoscope Reprocessing Guidelines,” e-ce.org Such versatility strengthens the value proposition for advanced video scopes and further drives the duodenoscopes market. Standardized quality indicators in markets like South Korea further promote consistent adoption of high-performance instruments. As payers reimburse outpatient ERCP at favorable rates, ASCs gain momentum, pushing suppliers to tailor solutions for non-hospital settings.

Regulatory Shift Toward Single-Use Duodenoscopes

Following several high-profile outbreaks, the U.S. FDA cleared Boston Scientific’s EXALT Model D, the world’s first fully disposable duodenoscope, which has now treated more than 1,000 patients with results comparable to traditional devices. Per-procedure spending nevertheless swings from USD 297-818 for reusable scopes to USD 797-1,547 for disposable units in typical U.S. centers, once infection risk estimates are included. Olympus recalled an older accessory line in early 2025 after 120 injury reports and one fatality, highlighting regulator vigilance. Large institutions now weigh legal exposure against higher consumable costs and often split purchasing between reusable fleets and select single-use products for immunocompromised cases. These procurement shifts ripple across supplier roadmaps, spurring hybrid portfolios and influencing the broader duodenoscopes market.

Continuous Image-Quality Improvements (HD/4K, AI)

Technological upgrades continue to transform clinical practice and drive growth in the duodenoscopes market. Olympus secured FDA clearance in May 2025 for the EZ1500 series featuring Extended Depth of Field optics that compress near-to-far focus into a single frame, helping clinicians spot subtle lesions. Artificial intelligence tools add another laye r of precision; Medtronic’s GI Genius now runs in nearly 460 U.S. Veterans Affairs endoscopy rooms, cutting missed polyp rates by up to 50%. Variable-stiffness shafts also help navigate postsurgical anatomy, boosting cannulation success where fixed scopes fail. Collectively, these innovations nudge facilities toward premium video systems and complementary accessories that raise average selling prices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High per-procedure cost of disposable scopes | –1.4% | Global; most acute in emerging markets and low-volume centers | Medium term (2-4 years) |

| Infection-related recalls & heightened FDA scrutiny | –0.9% | North America primary; EU secondary with global spillover | Short term (≤ 2 years) |

| Environmental burden of single-use plastics | –0.8% | EU and other markets with strict sustainability mandates | Long term (≥ 4 years) |

| Shortage of certified reprocessing technicians | –0.6% | Global, with pockets of scarcity in rural and developing areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Per-Procedure Cost of Disposable Scopes

Economic headwinds continue to curb single-use adoption. Published cost models place the disposable device expense at USD 2,899 per case versus just USD 601 for conventional workflows when infection risk is fully priced in. Low-volume community hospitals see an even wider gap, sometimes approaching a five-fold premium. While Medicare offers pass-through reimbursement codes, these are temporary and subject to annual renewal. Budget-strained facilities therefore keep well-maintained reusable fleets and update reprocessors rather than switching outright. This bifurcation preserves a sizable installed base for traditional systems, slowing disposable penetration outside top-tier centers.

Infection-Related Recalls and Heightened FDA Scrutiny

Regulatory intervention remains a double-edged sword. Olympus issued a Class I recall of its MAJ-891 accessory in January 2025 due to contamination risk, which followed an FDA order targeting legacy reprocessors the previous year. Each notice prompts extensive internal audits, temporary device shortages, and heightened media attention that can shake clinician confidence. Suppliers must then allocate resources to field safety corrections rather than product development. Short-term revenue dips often accompany these episodes, particularly when elective cases are deferred. Over the medium run, however, safety alerts also accelerate demand for newer, easier-to-clean designs, adding complexity to forecasting and influencing trends in the duodenoscopes market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Reusable Dominance Meets Rising Single-Use Demand

Reusable duodenoscopes anchored 90.4% of the duodenoscopes market revenues in 2024, a reflection of entrenched capital investments and validated cleaning workflows. The market size of duodenoscopes for reusable systems is projected to remain larger through 2030, even as single-use offerings register an 18.2% CAGR. High-volume academic hospitals often deploy a hybrid strategy, reserving single-use scopes for immuno-compromised or critical ICU patients. ANSI/AAMI ST91-2021 added USD 52-67 per procedure and roughly 24 additional minutes to cleaning times, prompting administrators to revisit cost-benefit assumptions. EXALT Model D and Ambu aScope Duodeno now serve as flagship disposable devices in the United States and Europe, respectively, and broaden procurement options for facilities wrestling with infection liability.

Single-use scope suppliers are working on next-generation models that reuse electronics while replacing patient-contact parts, aiming to halve present cost differentials. Meanwhile, removable-cap reusable scopes seek to lessen contamination risk and reclaim flexibility for asset managers. Procurement teams now run detailed financial modeling, weighing litigation exposure against supply-chain sustainability. This dynamic drives incremental but consistent share gain for disposables, particularly in North America, where tort risk is front-and-center. In emerging regions, reusable dominance is likely to last through the decade, helped by lower labor costs and the absence of class-action pressure.

By Technology: Video Platforms Cement Market Leadership

Video scopes held 87.2% of the duodenoscopes market shipments in 2024 and are on track for 14.6% CAGR through 2030, supported by demand for crisp HD and 4K images during advanced therapeutic procedures. This technology segment commanded the highest market share among all categories of duodenoscopes. EDOF, Texture and Color Enhancement Imaging, and Narrow Band Imaging widen diagnostic windows, allowing physicians to pick up subtle mucosal patterns. Variable-stiffness shafts and integrated guide-wire locks further streamline cannulation in patients with altered anatomy. Fiber-optic scopes linger mainly as backup units in budget-sensitive facilities but face gradual phase-out.

Artificial intelligence overlays, particularly CADe and CADx modules, continue to raise physician expectations. Early adopters report procedure-time neutrality despite additional analytics, dispelling fears of workflow delays. Suppliers that can bundle imaging software upgrades into service contracts gain a stickiness edge with large hospital networks. Combining video with AI also opens data-sharing business models, positioning vendors for future predictive-analytics revenue. Smaller producers without software capabilities may struggle to compete on value and margin beyond the mid-decade, affecting competition within the duodenoscopes market..

By End User: Hospital Scale Meets Outpatient Momentum

Hospitals supplied 69.2% of global revenue in 2024 and will keep the largest wallet share, given their readiness to handle emergency ERCP and complicated anatomy. Nonetheless, ASCs are predicted to compound at 10.2% yearly as payers steer lower-risk patients toward sites with bundled procedure pricing. Clinical guidance now supports same-day discharge for straightforward cases, making ASCs attractive for patients and insurers. The market size of duodenoscopes reclaimed by hospitals still benefits from critical-care surcharges and more complex case mixes, while ASCs win in efficiency, contributing to overall growth in the duodenoscopes market.

Specialty digestive clinics are experimenting with subscription-style care plans that package diagnostic ERCP, follow-up ultrasound, and lifestyle coaching. Although market penetration is limited, such models could unlock latent demand in urban regions with rising middle-class cohorts. Vendors watch these pilot programs closely to refine channel strategies, including consignment or pay-per-use agreements. Each customer tier now expects tailored financing, technical training, and inventory support, pressuring manufacturers to deploy flexible account teams.

Geography Analysis

North America captured 39.9% of worldwide revenue in 2024, supported by robust reimbursement structures and aggressive infection-control policy enforcement. United States hospitals routinely integrate cost-of-harm calculations into procurement reviews, pushing duodenoscopes market adoption of single-use platforms despite added per-case outlays. Canada follows suit with centralized safety audits that favor video systems incorporating AI because of their documented error-reduction benefits. Device makers therefore prioritize early U.S. launches, banking on faster payback for R&D as higher average selling prices offset narrow margins elsewhere.

Europe exhibits a mature yet internally diverse profile. Germany and the United Kingdom allocate funds for 4K-ready endoscopy suites, whereas Spain and Southern Europe lean toward enhanced-reprocessing protocols to balance safety and cost. Environmental legislation in the EU introduces a new purchasing criterion that weights carbon footprint against infection risk, complicating business cases for single-use scopes. Suppliers must now present life-cycle assessments and recycling partnerships to pass hospital tenders, especially in Scandinavia and the Netherlands.

Asia Pacific records the fastest regional CAGR of 8.8% through 2030, underpinned by rising pancreaticobiliary disease incidence, rapid healthcare capacity build-outs, and broader insurance coverage. China alone accounts for a sizable uptick in ERCP rooms within tertiary centers as provincial governments place cancer detection under performance mandates. In Japan, Olympus, Fujifilm, and HOYA deploy home-market insights to refine imaging algorithms and elevator designs, reinforcing local brand loyalty. While India, Indonesia, and parts of Southeast Asia remain price sensitive, reusable fleets remain viable when combined with lower labor costs for reprocessing. Multinational suppliers often strike joint-venture or licensing agreements to ease regulatory clearance and import tariffs across the region, boosting growth in the duodenoscopes market..

Competitive Landscape

The sector stays moderately concentrated, with three global groups—Olympus, Boston Scientific, and HOYA—jointly steering technology direction and accumulating broad intellectual-property portfolios. Each firm couples flagship reusable lines with nascent single-use models and integrates reprocessing chemistry or sterilization to lock customers into platform ecosystems. Boston's more demanding Scientific's first-mover status in disposables earned premium early-adopter share, forcing rivals to accelerate comparable programs. Olympus responded with easier-to-clean removable-cap scopes and advanced imaging, underscoring that infection-risk mitigation can coexist with reusable economics, further shaping trends in the duodenoscopes market.

Niche entrants exploit white space in price-sensitive markets and AI-enabled imaging. Ambu's single-use approach appeals to European units wary of cross-contamination yet subject to environmental audits. Several start-ups focus exclusively on predictive analytics, planning to license software interfaces that overlay on existing video towers, thereby avoiding direct hardware battles. Partnerships also proliferate; the May 2025 tie-up between Olympus and Advanced Sterilization Products illustrates cross-domain collaboration to meet more demanding cleaning standards.

Strategic moves revolve around bundled service contracts that wrap capital equipment, accessories, software updates, and staff training into multi-year subscriptions. This alignment shifts income from one-off sales toward recurring revenue and stabilizes cash flow for both suppliers and hospitals. Firms quick to blend hardware, services, and data analytics now possess a competitive cushion that is difficult for latecomers to replicate at speed or scale.

Duodenoscopes Industry Leaders

Olympus Corporation

HOYA Corp. (Pentax Medical)

Fujifilm Holdings Corp.

Boston Scientific Corp.

Ambu A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Olympus Corporation secured FDA 510(k) clearance for the EZ1500 series, introducing Extended Depth of Field imaging for gastrointestinal procedures.

- May 2025: Advanced Sterilization Products gained FDA clearance for the ULTRA GI Cycle, developed with PENTAX Medical, which offers hydrogen-peroxide gas-plasma sterilization for duodenoscopes.

- August 2024: PENTAX Medical obtained FDA clearance for a duodenoscope equipped with an ASP-driven sterilization channel.

- April 2024: Ambu received FDA 510(k) clearance for its next-generation single-use duodenoscope, reinforcing the disposable trend.

Global Duodenoscopes Market Report Scope

| Reusable Duodenoscopes | Conventional Reusable |

| Removable-Cap Reusable | |

| Single-Use (Disposable) Duodenoscopes | EXALT Model D |

| aScope Duodeno | |

| Other Single-Use Models |

| Video Duodenoscopes |

| Fiber-optic Duodenoscopes |

| Hospitals |

| Ambulatory Surgery Centers |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Reusable Duodenoscopes | Conventional Reusable |

| Removable-Cap Reusable | ||

| Single-Use (Disposable) Duodenoscopes | EXALT Model D | |

| aScope Duodeno | ||

| Other Single-Use Models | ||

| By Technology | Video Duodenoscopes | |

| Fiber-optic Duodenoscopes | ||

| By End User | Hospitals | |

| Ambulatory Surgery Centers | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the duodenoscopes market?

The market was valued at USD 1.61 billion in 2024 and is projected to reach USD 2.20 billion by 2030, growing at a 5.53% CAGR.

Which region leads global revenue today?

North America holds the top position with 39.9% market share, propelled by stringent infection-control rules and early single-use adoption.

How fast are single-use duodenoscopes expanding compared with reusable models?

Single-use units are forecast to compound at 18.2% annually through 2030 while reusable systems remain dominant but slower-growing.

What are the main factors driving market growth?

Rising pancreaticobiliary disease incidence, higher ERCP procedure volumes, tighter FDA oversight, and continuous HD/4K and AI imaging upgrades all fuel adoption.

Why do many facilities still favor reusable devices?

Despite infection-control advantages, disposable scopes can cost roughly five times more per procedure, making reusable fleets more economical for low-volume or budget-limited centers.

Which end-user segment is growing fastest?

Ambulatory surgery centers lead in growth with a 10.2% CAGR as payers shift routine ERCP cases to outpatient settings for cost savings and patient convenience.

Page last updated on: