Dermatoscopes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

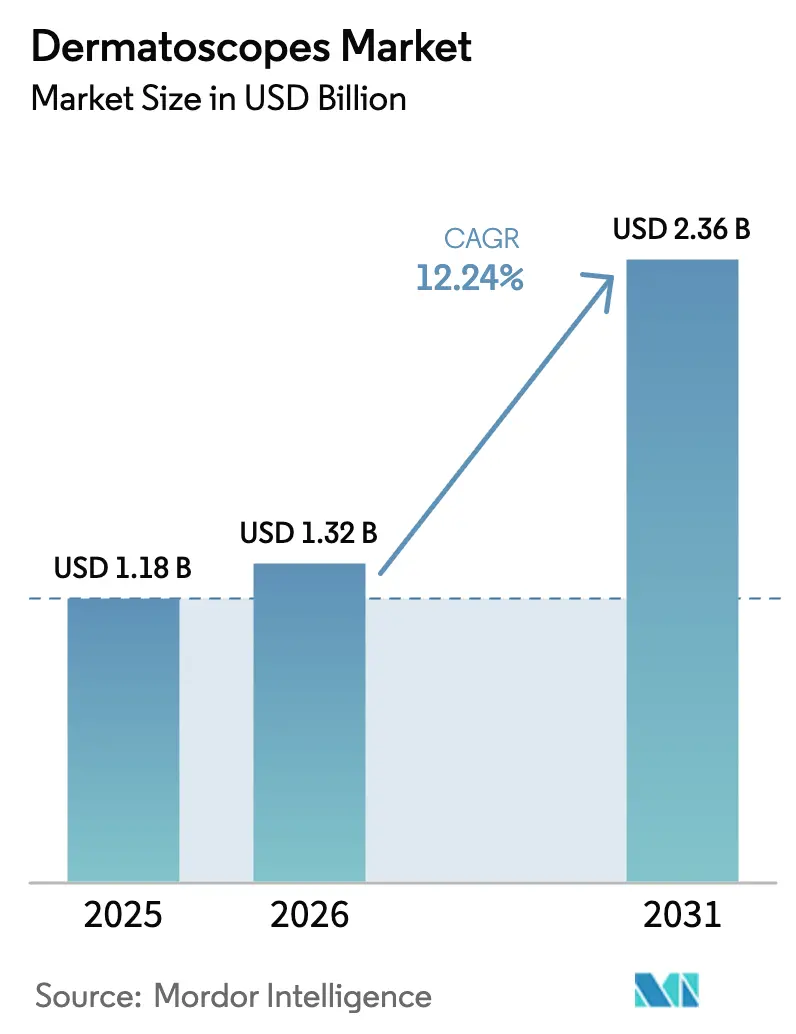

| Market Size (2026) | USD 1.32 Billion |

| Market Size (2031) | USD 2.36 Billion |

| Growth Rate (2026 - 2031) | 12.24% CAGR |

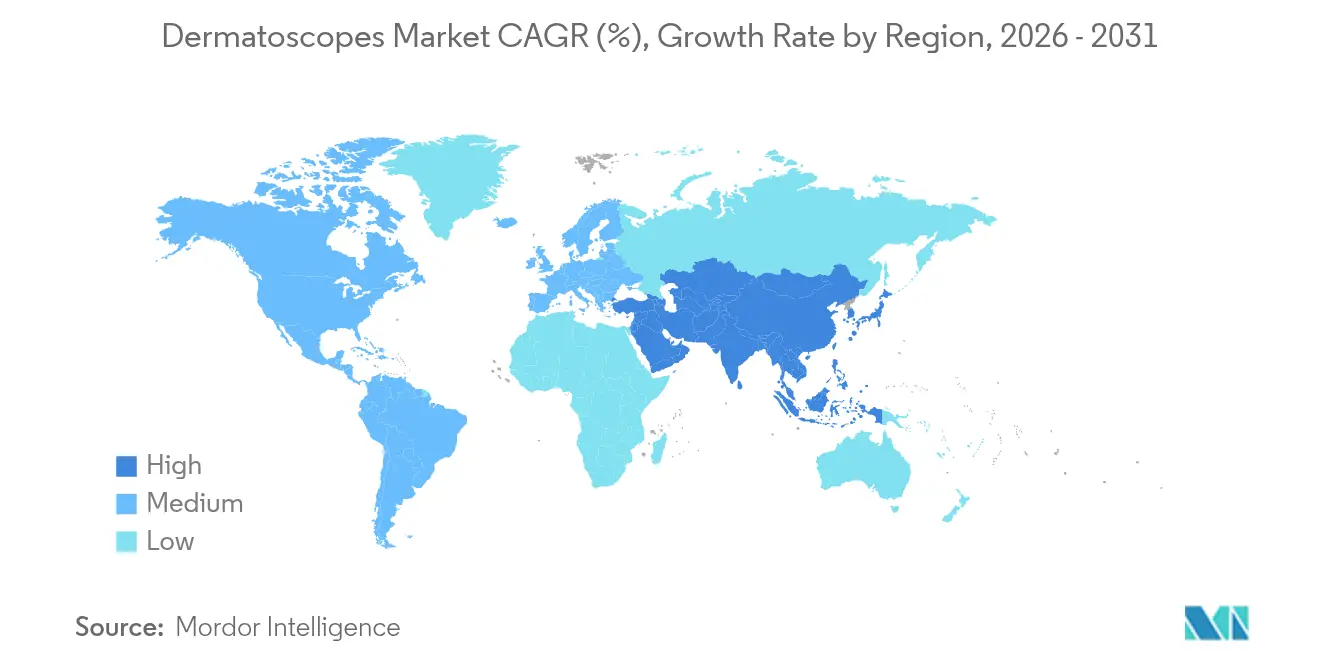

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dermatoscopes Market Analysis by Mordor Intelligence

The dermatoscope market size is expected to grow from USD 1.18 billion in 2025 to USD 1.32 billion in 2026 and is forecast to reach USD 2.36 billion by 2031 at 12.24% CAGR over 2026-2031. Rising skin-cancer incidence, rapid advances in AI-integrated optics, and broader teledermatology reimbursement are the chief forces steering revenue expansion. Government-backed digitization programs, notably in Asia-Pacific, accelerate device procurement, while the 2024 FDA clearance of DermaSensor validated spectroscopy-based diagnostics and spurred investor confidence. North America sustains volume leadership on the strength of robust insurance coverage, yet Asia-Pacific delivers the fastest incremental dollars as smartphone-attachable units enable remote triage in primary care. Product design is converging on AI-ready, cloud-connected platforms that shorten time-to-diagnosis, a strategic shift highlighted by FotoFinder’s 2024 purchase of DermLite to create an end-to-end imaging ecosystem. On the policy front, Medicare’s 2.83% dermatology fee cut in 2025 tempers U.S. margin outlook, but the FDA’s agency-wide AI initiative promises faster authorization lanes for novel devices, partially offsetting reimbursement pressure.

Key Report Takeaways

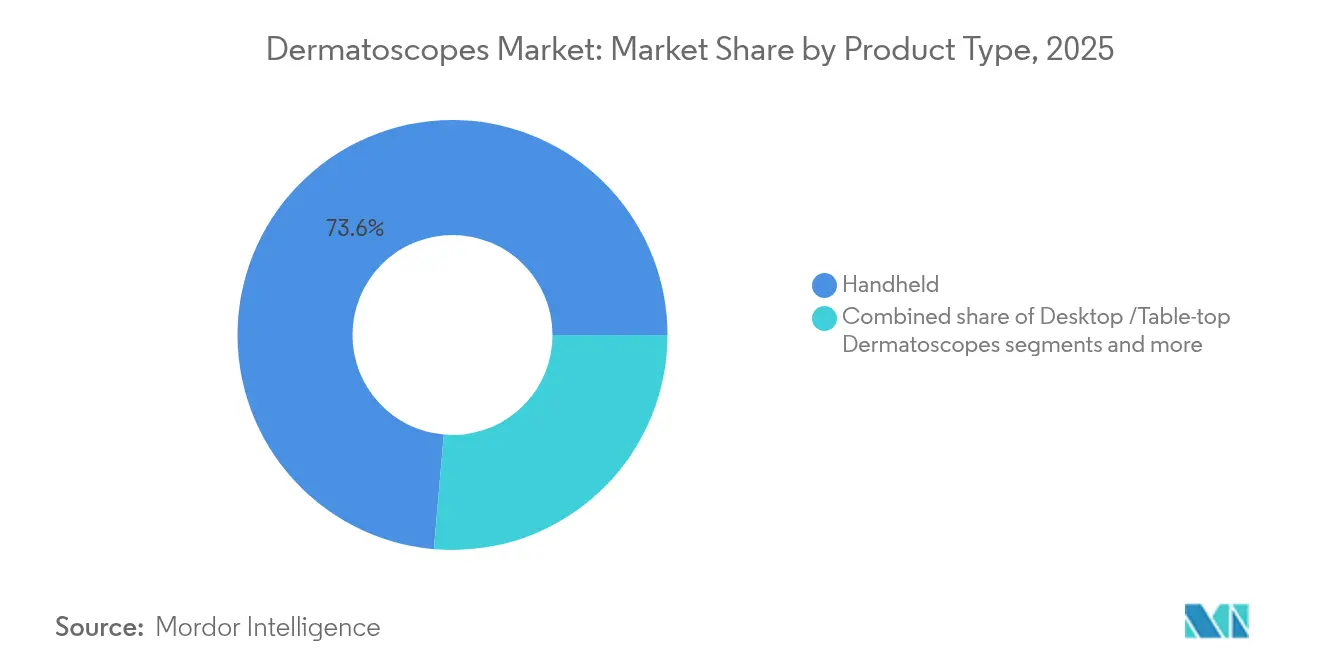

- By product type, handheld dermatoscopes accounted for 73.62% of the dermatoscope market share in 2025, while smartphone-attachable devices are advancing at a 12.85% CAGR through 2031.

- By technology, LED illumination led with 61.78% revenue share in 2025; ultraviolet imaging is projected to grow at 13.56% CAGR to 2031.

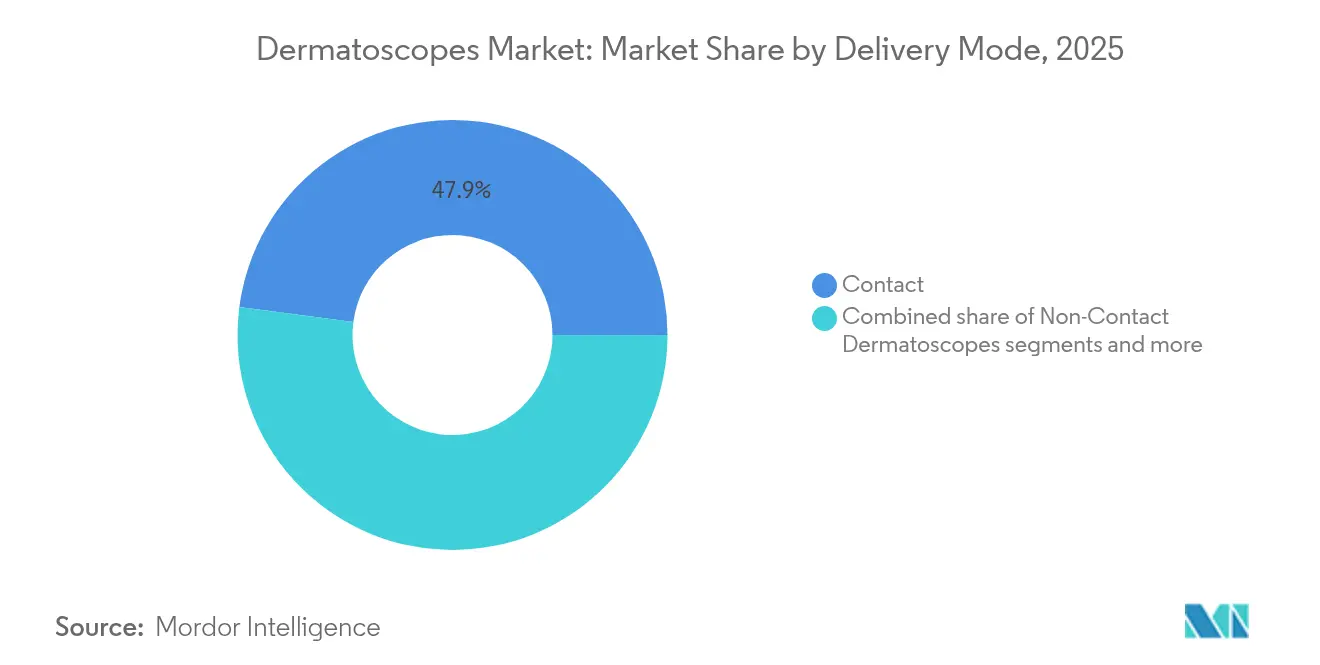

- By modality, contact units held 47.92% of the dermatoscope market size in 2025, and hybrid solutions are posting the highest 13.12% CAGR through 2031.

- By end user, dermatology clinics captured 46.35% share in 2025, whereas ambulatory centers are poised for 13.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dermatoscopes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of skin cancer requiring early non-invasive diagnostics | +2.8% | Global, with highest impact in North America & Australia | Long term (≥ 4 years) |

| Technological advances in digital & AI-integrated dermatoscopes | +3.2% | Global, led by North America & Europe | Medium term (2-4 years) |

| Growing adoption of teledermatology & remote monitoring | +2.1% | Global, accelerated in APAC & emerging markets | Short term (≤ 2 years) |

| Surge in dermatology training programs in emerging markets | +1.4% | APAC, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Bundled reimbursement codes for non-invasive skin imaging | +1.6% | North America & Europe, selective emerging markets | Medium term (2-4 years) |

| Variable-polarisation & multispectral imaging enabling rare-lesion detection | +1.1% | Global, concentrated in advanced healthcare systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Skin Cancer Requiring Early Non-Invasive Diagnostics

Over 5.5 million new skin-cancer cases were diagnosed in the United States during 2024, prompting payers to prioritize preventive screening pathways that rely on dermoscopy as a first-line tool. Treatment economics support early detection, as the cost of advanced melanoma care far exceeds that of stage-I intervention. Controlled studies show dermoscopy lifts diagnostic accuracy to 84% versus 75% for naked-eye exams, reinforcing clinical adoption. The University of Queensland’s 2025 3-D body-photography trial improved non-melanoma detection rates, yet unchanged melanoma sensitivity spotlights the continued need for complementary optical solutions. Collectively, epidemiological realities and cost containment imperatives underpin sustained device demand across surgical and primary-care settings.

Technological Advances in Digital & AI-Integrated Dermatoscopes

FDA-cleared AI platforms such as DermaSensor achieve 96% sensitivity across 200 histologies, converting subjective image review into quantitative risk scores that shorten decision cycles. FotoFinder’s Moleanalyzer pro overlays heat-map triage on captured lesions, a capability derived from deep-learning models trained on verified pathology. Spectroscopy plus machine learning enables real-time cellular analysis, while ZEISS’s 2025 research-data platform automates multicenter image ingestion and annotation, accelerating algorithm tuning. Next-generation full-body scanners under the iToBoS consortium promise six-minute whole-patient risk stratification, indicating a shift toward population-wide surveillance. As software intellectual property increasingly defines competitive advantage, partnerships between optics specialists and AI firms are intensifying.

Growing Adoption of Teledermatology & Remote Monitoring

Smartphone-ready attachments permit rural clinics to forward dermoscopic images to reference centers, closing care gaps without duplicative hardware spend. DermatologistOnCall’s nationwide network processes asynchronous consults within two business days, proving that virtual pathways can match in-office accuracy while slashing wait times. Studies confirm teledermatology’s diagnostic parity for non-melanoma skin cancer, catalyzing insurance recognition and codified billing routes. FotoFinder’s wireless “skeen” integrates cloud archiving and AI triage, demonstrating how ergonomic advances converge with virtual-care workflows. Lower-cost devices such as the USD 149.99 Sklip accessory broaden entry-level access and fund melanoma-research grants, underscoring telehealth’s virtuous cycle for innovation financing.

Surge in Dermatology Training Programs in Emerging Markets

Accredited courses like HealthCert’s Professional Diploma in Dermoscopy scale specialist skills across 50 countries and feed equipment procurement in secondary cities. The International Dermoscopy Society’s e-learning modules democratize best-practice imaging techniques formerly confined to academic centers. Thirty-six fellows from 26 nations attended the 2024 Open Medical Institute workshop, indicating pent-up demand for structured curriculum in low-resource regions. Government digital-health grants in India and Indonesia further subsidize dermatoscope rollout within primary-care digital hubs[1]Source: Baker McKenzie Research Team, “Healthcare and Life Sciences in Asia Pacific: 2024 sets to see rising investment and innovation,” bakermckenzie.com . Trained clinicians quickly adopt AI-ready devices, reinforcing a feedback loop between education and hardware sales.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timelin |

|---|---|---|---|

| High upfront cost & limited reimbursement in low-income nations | -1.8% | Emerging markets, rural healthcare systems | Medium term (2-4 years) |

| Shortage of validated AI datasets delaying regulatory approvals | -1.2% | Global, particularly affecting new market entrants | Short term (≤ 2 years) |

| Sterilisation & infection-control challenges for contact devices | -0.9% | Global, heightened in post-pandemic healthcare settings | Short term (≤ 2 years) |

| Fragmented SaMD regulatory requirements across regions | -1.3% | Global, most complex in multi-regional market entries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost & Limited Reimbursement in Low-Income Nations

Dermatoscope list prices and software subscriptions remain prohibitive where first-visit dermatology fees already range USD 150–300, with insurers often labeling dermoscopy “not medically necessary”. Medicare’s 2.83% payment cut compounds U.S. clinic strains, potentially delaying refresh cycles for optics hardware. DermaSensor’s USD 199–399 monthly SaaS model adds recurring overhead, a hurdle for resource-limited practices. Insufficient payer clarity chills capital budgeting even as inpatient dermatology costs top USD 5 billion annually, illustrating the price of late-stage intervention. Until coverage parity is achieved, unit shipment growth in low-income geographies will trail epidemiologic need.

Shortage of Validated AI Datasets Delaying Regulatory Approvals

The FDA now requires post-market performance audits on under-represented demographics, magnifying dataset demands for algorithm developers. Europe’s staggered MDR deadlines (December 2027–2028) impose overlapping verification layers that extend project timelines and cost structures. DermaSensor’s 20,000-scan evidence package illustrates the high bar for market entry, deterring smaller innovators. Explainable-AI mandates also force additional engineering layers to surface human-interpretable rationales, lengthening validation cycles. The cumulative effect is elongated time-to-revenue for software-centric newcomers, slowing overall innovation velocity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smartphone Integration Drives Innovation

Handheld units retained 73.62% share of the dermatoscope market size in 2025, mirroring entrenched clinician preference for familiar ergonomics. Desktop systems remain niche, addressing high-resolution research demands inside tertiary centers. In contrast, smartphone-attachable models are expanding at 12.85% CAGR, propelled by telehealth scale-up and minimal capital cost. The “skeen” wireless model bridges handheld convenience with AI cloud triage, signaling convergence toward multipurpose portable ecosystems. Casio’s DZ-D100 Dermocamera underscores non-traditional entrants leveraging optics pedigree to upend incumbent roadmaps.

Second-generation attachments benefit from smartphone ubiquity, removing the need for proprietary displays and enabling instant image upload into electronic-health-record flows. For providers, reduced hardware outlay de-risks fleet expansion across satellite clinics. As a result, smartphone units are expected to narrow the volume gap with traditional handpieces beyond 2027, especially within public-health teletriage initiatives across India and Brazil. The trend supports a more distributed screening model, crucial for regions where dermatologist density falls below one per 100,000 inhabitants.

By Technology: UV Imaging Gains Clinical Validation

LED platforms delivered 61.78% revenue in 2025, buoyed by long service life and stable luminance. Yet ultraviolet modalities lead growth at 13.56% CAGR, backed by studies confirming superior visualization of early vitiligo and subclinical basal-cell change. Polarized-digital systems integrating multilayer illumination and AI segmentation further diversify the technology mix, while xenon/halogen share continues to erode on energy-efficiency grounds. OBSERV’s 520x hybrid console, combining variable polarization with automated lesion mapping, typifies the migration toward multi-spectral, software-defined imaging.

Ultraviolet’s prospects rest on mounting evidence that cross-sectional fluorescence improves rare lesion detection and shortens biopsy queues. Cost headwinds persist, given additional sensor requirements, but scale manufacturing and modular upgrades are expected to compress price points by the decade’s close. Consequently, technology competition will likely center on bundled software analytics rather than illumination source alone.

By Modality: Hybrid Solutions Address Versatility Demands

Contact scopes controlled 47.92% of dermatoscope market share in 2025 as dermatoscope market practitioners valued direct skin interface to mitigate reflection artifacts. Yet infection-control protocols during the COVID-19 era spotlighted limitations, thus boosting non-contact alternatives in high-throughput clinics. Hybrid devices posting 13.12% CAGR harmonize both approaches, letting users switch seamlessly according to case complexity or sterility requirements. FotoFinder’s ATBM master exemplifies the all-in-one promise, combining full-body mapping with detachable contact heads in one workflow.

Demand for modality flexibility rises alongside teledermatology; images captured non-contact at primary-care sites can be revisited under contact mode when patients appear in-person. As payer policies increasingly favor bundled diagnostic episodes, hybrid units deliver economic advantages by eliminating redundant hardware purchases. By 2030, hybrids are forecast to eclipse stand-alone non-contact volumes in most OECD countries.

By End User: Ambulatory Centers Drive Access Expansion

Dermatology clinics account for 46.35% of global placements, retaining primacy owing to specialized staff and procedural throughput. Hospitals leverage dermatoscopy in emergency departments to triage suspicious lesions, but their share is diluted by competing capital priorities. Ambulatory surgical centers, however, are scaling fastest at 13.92% CAGR as payers steer low-risk excisions to outpatient venues for cost containment. Academic and research institutes influence device evolution through validation trials, though they represent a modest volume base.

AI-enabled diagnostics are broadening primary-care usage. DermaSensor’s regulatory win demonstrates that family physicians can deploy spectroscopy tools without dermatology subspecialty training, a model expected to diffuse across retail clinics and pharmacy chains. Continuous medical-education programs underpin this shift, ensuring confidence in device interpretation and integration into electronic referral pathways.

Geography Analysis

North America retained 37.85% share of the dermatoscope market in 2025 on the back of regulatory clarity, insurance adoption, and mature telehealth platforms. High skin-cancer prevalence sustains procedural demand, while the January 2024 DermaSensor clearance cemented the U.S. as launchpad for AI-integrated optics. Still, Medicare’s 2025 fee schedule cut dampens smaller-practice capital budgets; vendors are responding with leasing and per-scan pricing to preserve volume.

Asia-Pacific, expanding at 14.32% CAGR, benefits from government telemedicine grants and proliferating dermoscopy curricula. China’s Healthy China 2030 initiative allocates funding for AI diagnostics, while India’s Ayushman Bharat digital mission digitizes patient records, simplifying remote lesion review. The region’s smartphone penetration aligns with attachable-scope uptake, minimizing infrastructure hurdles in rural provinces.

Europe’s growth remains steady under the MDR regime, which, while stringent, levels the playing field through harmonized safety benchmarks. Germany’s design award for FotoFinder’s wireless scope exemplifies continental leadership in ergonomic engineering. Transitional compliance extensions through 2028 offer breathing room to mid-tier manufacturers, easing supply risk for distributors. In parallel, pan-European cancer-screening guidelines now endorse dermoscopy as part of multi-modality pathways, bolstering demand in public hospitals.

Latin America and the Middle East & Africa trail in absolute spend but show improving CAGR profiles as multilateral lenders support telehealth connectivity. Pilot programs in Brazil’s SUS system and South Africa’s public clinics have demonstrated cost savings via remote triage, supporting future procurement cycles. Currency volatility and customs tariffs still hamper pricing parity with mature markets, necessitating locally assembled units or differentiated payment models.

Competitive Landscape

Competitive intensity is moderate, with the top five players controlling roughly half of 2024 sales revenue. FotoFinder’s 2024 acquisition of DermLite created a vertically integrated line that spans handheld optics, total-body scanners, and AI analytics. ZEISS leverages ophthalmology AI talent to fast-track skin-imaging platforms, illustrated by its 2025 research-data platform launch[2]Source: ZEISS Media Relations, “ZEISS unveils AI-powered Research Data Platform,” zeiss.com . Consumer-electronics entrant Casio applies camera-sensor expertise to the DZ-D100, elevating image resolution benchmarks.

Strategic alliances between optics manufacturers and cloud-health start-ups aim to embed dermoscopy data directly into electronic-health-record systems, improving clinician workflow integration. Patent filings reveal growing attention to spectroscopy and hyperspectral modalities, fields where smaller firms such as DermaSensor and OncoRes pursue differentiation. Supply-chain disruptions highlighted in 2024 catalyzed dual-sourcing of light-emitting diodes and CMOS sensors, favoring firms with vertically integrated manufacturing. Meanwhile, price competition intensifies in entry-level smartphone accessories, where purchase decisions hinge on AI-software subscription structures rather than optics specs alone.

Continued consolidation is expected as midsize players seek scale for MDR compliance and AI-dataset acquisition. Venture capital inflows target algorithm-heavy start-ups, anticipating valuation premiums once regulatory approvals are secured. As reimbursement codes for AI triage crystallize, competitive advantage will increasingly align with clinical-outcome evidence and seamless telehealth interoperability rather than device hardware per se.

Dermatoscopes Industry Leaders

Caliber Imaging & Diagnostics

Firefly Global

ILLUCO Corporation Ltd.

Welch Allyn

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ZEISS unveiled an AI-powered Research Data Platform at ARVO 2025, automating clinical-image curation for retinal and dermatology studies

- March 2024: FotoFinder launched the wireless “skeen” dermatoscope featuring AI assistant AIMEE and secure cloud storage, winning the 2025 German Design Award

Global Dermatoscopes Market Report Scope

As per the scope of the report, dermatoscopes are the devices used to examine the skin surface. These devices are commonly used by dermatologists to detect the skin diseases such as skin cancer. The dermatoscopes market is segmented by Product (Contact Dermatoscopes, Noncontact Dermatoscopes, and Hybrid Dermatoscopes), Technology (LED, Xenon, Halogen, and Ultraviolet), Type (Handheld, Trolley Mounted, and Headband), Application (Skin Tumors, Scabies, Warts, Fungal Infections, and Other Applications), End User (Dermatology Clinics, Hospitals, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Handheld Dermatoscopes |

| Desktop /Table-top Dermatoscopes |

| Smartphone-attachable Dermatoscopes |

| LED Illumination |

| Xenon / Halogen |

| Ultraviolet |

| Polarised Digital Imaging |

| Contact Dermatoscopes |

| Non-Contact Dermatoscopes |

| Hybrid Dermatoscopes |

| Dermatology Clinics |

| Hospitals |

| Ambulatory Surgical Centres |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type (Value) | Handheld Dermatoscopes | |

| Desktop /Table-top Dermatoscopes | ||

| Smartphone-attachable Dermatoscopes | ||

| By Technology (Value) | LED Illumination | |

| Xenon / Halogen | ||

| Ultraviolet | ||

| Polarised Digital Imaging | ||

| By Modality (Value) | Contact Dermatoscopes | |

| Non-Contact Dermatoscopes | ||

| Hybrid Dermatoscopes | ||

| By End User (Value) | Dermatology Clinics | |

| Hospitals | ||

| Ambulatory Surgical Centres | ||

| Academic & Research Institutes | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global value of the dermatoscope market?

The dermatoscope market size stands at USD 1.32 billion in 2026.

How fast is demand for dermatoscopes projected to grow?

Revenue is forecast to rise at a 12.24% CAGR through 2031.

Which region is expanding sales the quickest?

Asia-Pacific shows the fastest growth, recording a 14.32% CAGR.

Which product format is gaining momentum over handheld units?

Smartphone-attachable scopes are growing at 12.85% CAGR, the top rate among product classes.

How are AI capabilities influencing purchasing decisions?

FDA-cleared AI scopes like DermaSensor validate diagnostic accuracy, raising provider confidence and accelerating adoption.

Page last updated on: