Endoscopic Retrograde Cholangiopancreatography (ERCP) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

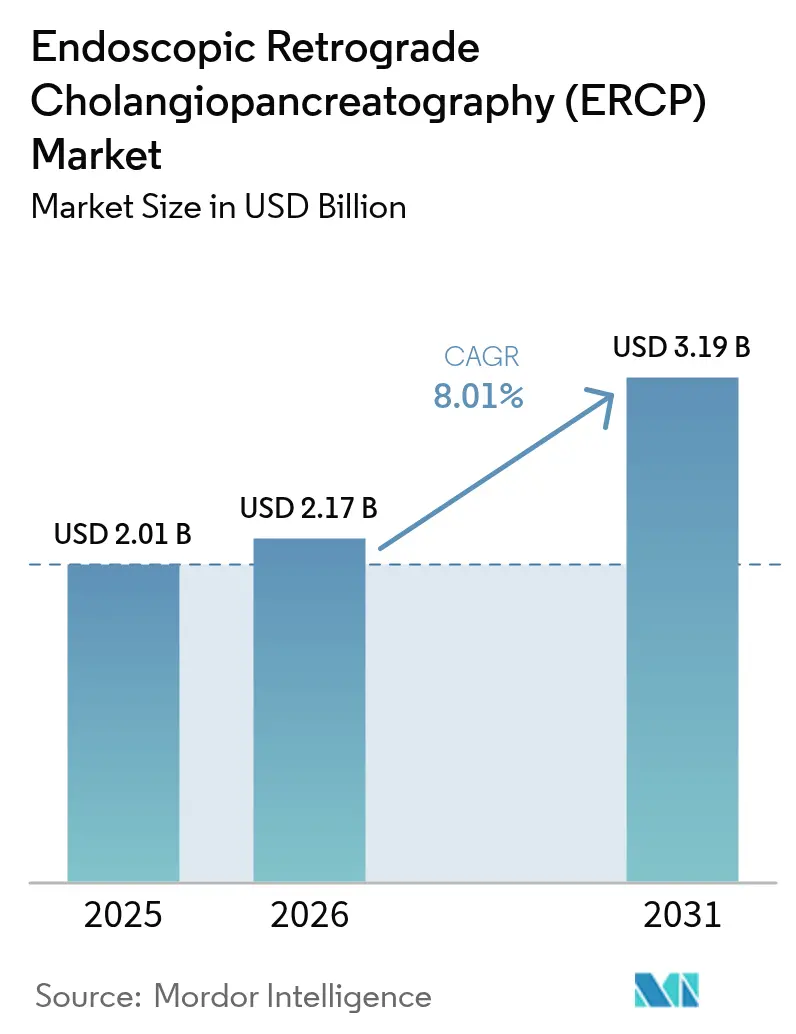

| Market Size (2026) | USD 2.17 Billion |

| Market Size (2031) | USD 3.19 Billion |

| Growth Rate (2026 - 2031) | 8.01% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

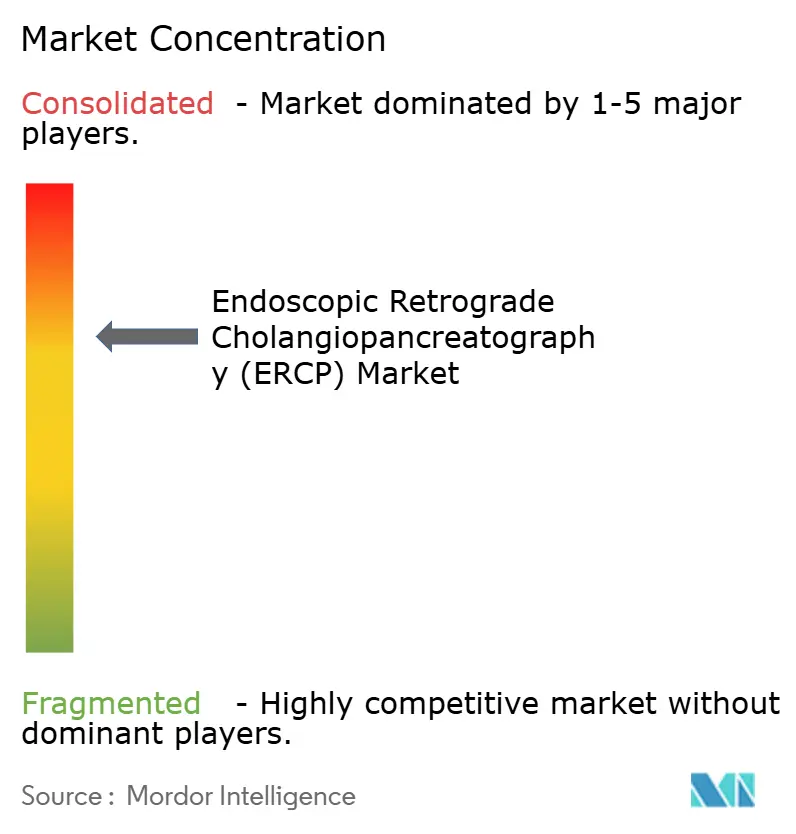

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Endoscopic Retrograde Cholangiopancreatography (ERCP) Market Analysis by Mordor Intelligence

The Endoscopic Retrograde Cholangiopancreatography market size was valued at USD 2.01 billion in 2025 and estimated to grow from USD 2.17 billion in 2026 to reach USD 3.19 billion by 2031, at a CAGR of 8.01% during the forecast period (2026-2031). Rising pancreatic and biliary disease burdens, rapid uptake of single-use duodenoscopes, and broader outpatient reimbursement drive this expansion. Infection-control concerns following contamination events intensify the shift from reusable to disposable devices, while AI-enabled imaging raises cannulation success and reduces procedure times. Outpatient ERCP adoption grows as health systems seek lower costs and higher patient satisfaction, and emerging economies add new endoscopy capacity, widening global access to advanced therapeutics.

Key Report Takeaways

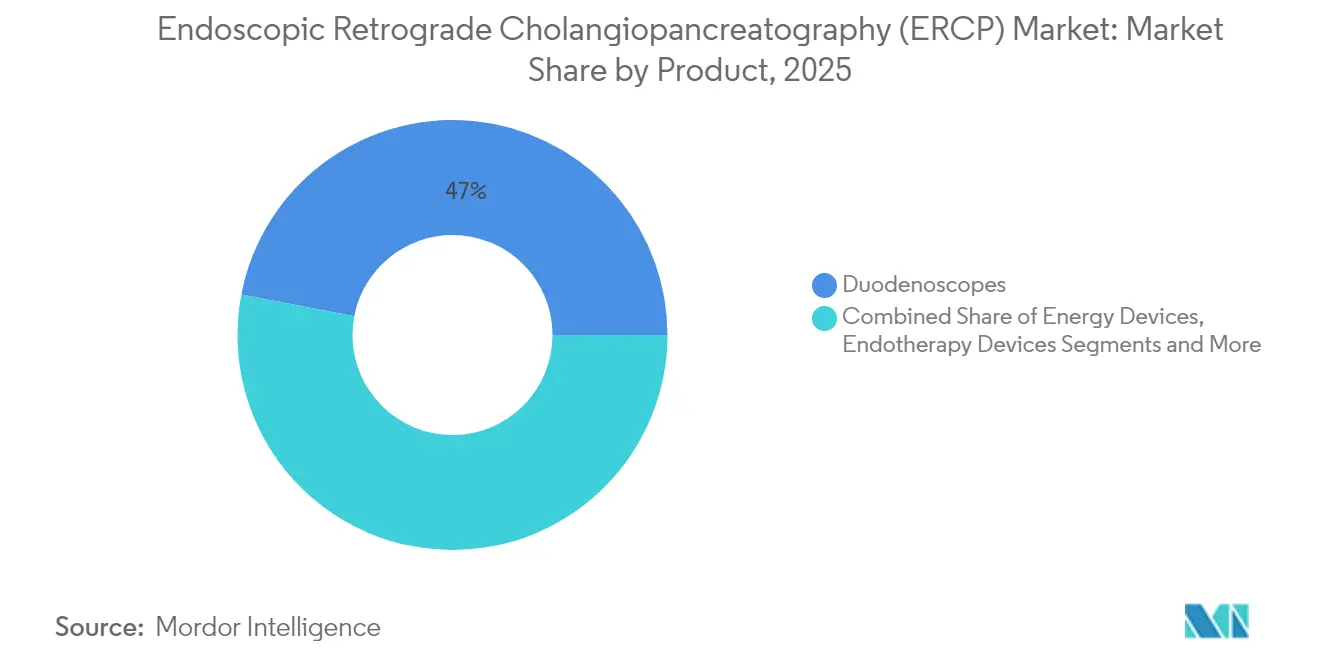

- By product category, duodenoscopes led with 46.98% of Endoscopic Retrograde Cholangiopancreatography market share in 2025, and the segment is projected to expand at an 11.62% CAGR through 2031.

- By procedure, biliary sphincterotomy held 26.35% share of the Endoscopic Retrograde Cholangiopancreatography market size in 2025, while pancreatic duct stenting is set to grow at a 12.25% CAGR to 2031.

- By end user, hospitals accounted for 58.81% revenue share in 2025, yet ambulatory surgery centers post the fastest growth at 10.54% through 2031.

- By technology, reusable systems retained 68.05% share in 2025, whereas fully single-use platforms record the highest forecast CAGR of 11.21%.

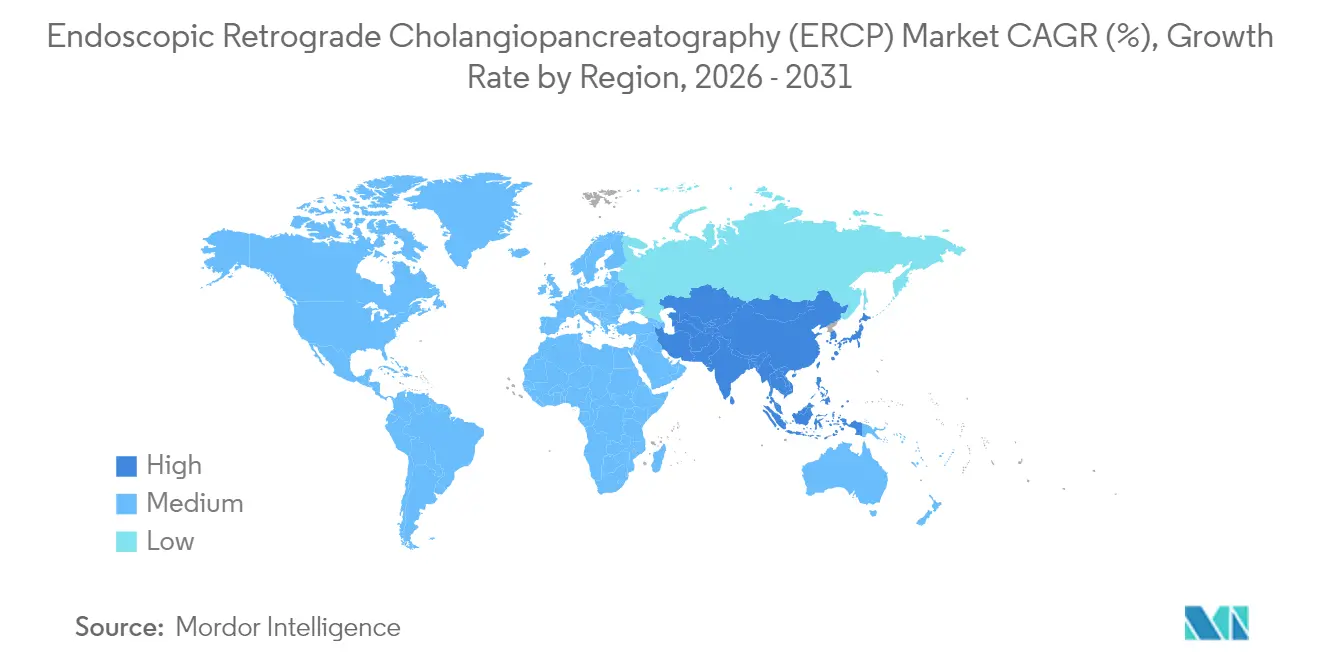

- By geography, North America captured 39.12% of Endoscopic Retrograde Cholangiopancreatography market share in 2025; Asia-Pacific displays the strongest growth momentum with a 9.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Endoscopic Retrograde Cholangiopancreatography (ERCP) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of pancreatic & biliary cancers | +1.8% | Global, higher in high-income regions | Long term (≥ 4 years) |

| Growing preference for single-use duodenoscopes to curb cross-infection | +2.1% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| AI-enabled imaging & navigation boosts cannulation success | +1.2% | North America, EU, select APAC markets | Medium term (2-4 years) |

| Reimbursement expansion for outpatient ERCP in OECD markets | +1.4% | OECD, mainly North America & EU | Short term (≤ 2 years) |

| Endotherapy device miniaturisation enabling pediatric ERCP | +0.6% | Global, early in developed markets | Long term (≥ 4 years) |

| ESG-driven hospital decarbonisation favouring low-water-use scopes | +0.9% | EU, North America, APAC sustainability leaders | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising incidence of pancreatic & biliary cancers

Gallbladder cancer prevalence has climbed to 20.3% among at-risk groups, notably individuals with gallstones, creating a large pool of patients who require endoscopic intervention.[1]Ali Afzal, “Epidemiology of gall bladder cancer and its prevalence worldwide: a meta-analysis,” Orphanet Journal of Rare Diseases, ojrd.biomedcentral.com Early-onset pancreatic cancer cases add clinical complexity, demanding specialised diagnostic and therapeutic protocols tailored to younger populations. These epidemiological shifts lift procedure volumes beyond normal demographic growth, especially in high-income nations with established reimbursement systems. Post-ERCP pancreatitis affects up to 15% of patients and adds more than USD 200 million in annual U.S. costs, intensifying the search for safer technologies.[2]Patrick Smith, “Preventing Pancreatitis After ERCP,” Johns Hopkins Medicine, hopkinsmedicine.orgAgeing societies and lifestyle risk factors combine to keep long-term demand for ERCP solutions strong.

Growing preference for single-use duodenoscopes to curb cross-infection

Hospitals increasingly choose single-use duodenoscopes, driven by safety, operational efficiency, and new reimbursement pathways. Boston Scientific’s EXALT Model D shows performance parity with reusable devices across seven peer-reviewed studies while removing cross-infection risks. The U.S. Centers for Medicare & Medicaid Services has granted an add-on payment for Ambu’s aScope Duodeno, alleviating cost concerns for administrators. These policy incentives, coupled with lower legal liability, accelerate broader adoption beyond high-risk cases.

AI-enabled imaging & navigation boosts cannulation success

Artificial-intelligence software raises selective cannulation success and diagnostic accuracy. Meta-analysis data reveal 93% sensitivity and 90% specificity for pancreatic cancer detection with AI-enhanced EUS, achieving an area under the curve of 0.95.[3]Hua Yin, “The Value of Artificial Intelligence Techniques in Predicting Pancreatic Ductal Adenocarcinoma with EUS Images,” Endoscopic Ultrasound, journals.lww.com Deep-learning models show 97% accuracy in spotting bile-duct dilatation on MRCP scans. Olympus plans to commercialise an AI endoscopy ecosystem in 2025, embedding cloud-based analytics to support real-time decision-making.

Reimbursement expansion for outpatient ERCP in OECD markets

Thirty new U.S. gastrointestinal endoscopy centres opened in 2023, mirroring expanded insurer coverage that equalises payment for outpatient and inpatient ERCP procedures. Ambulatory settings lower hospital infection risks, shorten recovery, and improve patient satisfaction while cutting facility costs. These benefits align with payer shifts to value-based purchasing, spurring health systems to invest in ambulatory ERCP capability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & per-procedure cost of disposable scopes | -1.6% | Global, stronger in cost-sensitive markets | Short term (≤ 2 years) |

| Shortage of ERCP-skilled endoscopists in emerging markets | -1.1% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Risk of post-ERCP pancreatitis & related litigation | -0.8% | North America, EU | Medium term (2-4 years) |

| Slow regulatory clearance for AI-guided cannulation software | -0.5% | Worldwide, variable by region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High capital & per-procedure cost of disposable scopes

Although infection risk falls to near zero, single-use devices still cost more per case than reusables, straining budgets in systems with tight reimbursement. Hospitals saved USD 451 million through device reprocessing programs in 2024, illustrating pressure to contain spending. As economies of scale improve and payment models evolve, the cost differential is expected to narrow.

Shortage of ERCP-skilled endoscopists in emerging markets

Advanced ERCP requires extensive training. Olympus has partnered with Rizal Medical Center in the Philippines to build a regional training hub, yet the pipeline cannot meet rising demand quickly. Until more clinicians acquire these skills, procedure volumes may lag equipment availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Duodenoscopes Drive Innovation While Endotherapy Expands

Duodenoscopes held 46.98% of Endoscopic Retrograde Cholangiopancreatography market share in 2025 and remain on track to grow at an 11.62% CAGR through 2031. Hospital infection-control policies and supportive reimbursement drive brisk conversion to single-use models, while hybrid scopes with disposable tips help institutions with tight budgets transition gradually. Olympus, Boston Scientific, and Ambu compete closely, each offering ergonomics, imaging clarity, and sterile packaging that answer clinician demands. As institutions retire ageing reusable fleets, procurement cycles increasingly favour newer single-use or hybrid options that lower reprocessing load and litigation exposure.

Endotherapy devices form the second-largest revenue block and cover sphincterotomes, guidewires, lithotripters, and stents. Growing case complexity, particularly in pancreatic interventions, sustains multi-device demand per procedure. Radiofrequency ablation catheters such as Habib EndoHPB broaden therapeutic scope and extend stent patency. Accessories and consumables enjoy steady volume growth, reflecting the overall expansion of procedures rather than large price swings.

By Procedure: Biliary Dominance Shifts Toward Pancreatic Complexity

Biliary sphincterotomy accounted for 26.35% of Endoscopic Retrograde Cholangiopancreatography market size in 2025, confirming its role as the traditional workhorse procedure. Pancreatic duct stenting, however, posts the quickest rise at a 12.25% CAGR as clinicians manage pancreatitis complications and malignant strictures with endoscopic techniques that once required surgery. Advances in imaging and wire technology improve cannulation precision, allowing safe navigation of complex duct anatomy. As procedural confidence grows, hospitals adopt expanded indications, driving a mix shift toward higher-value pancreatic work.

Pancreatic duct dilatation and combined EUS-ERCP techniques continue to gain ground. Technical success rates up to 92% in EUS-guided drainage highlight the expanding therapeutic envelope. Device firms market mini-sphincterotomes for difficult cannulations, reinforcing procedure adoption in less experienced hands. This broadening toolkit accelerates the transition from purely diagnostic ERCP toward comprehensive endoscopic therapy.

By End User: Hospitals Maintain Leadership While ASCs Accelerate

Hospitals captured 58.81% revenue share in 2025 by handling complex cases that demand anaesthesia support, imaging infrastructure, and intensive post-procedure monitoring. Many tertiary centres also act as regional referral hubs, ensuring high patient throughput. Yet ambulatory surgery centres are forecast to record a 10.54% CAGR as payers reward lower facility fees and faster discharge. Purpose-built outpatient suites slash turnover times and free inpatient capacity for more acute care. Health systems respond by spinning up hospital-owned ASCs, blending capital efficiency with clinical oversight.

Specialty and GI clinics fill a complementary role for routine diagnostic ERCP, patient follow-up, and minor therapeutic updates. As device makers refine smaller-footprint imaging systems, these clinics gain increased capability to perform straightforward cases, easing backlog at large hospitals. Collectively, the end-user mix reflects the healthcare sector’s broader shift to decentralised, cost-effective service delivery.

By Technology: Reusable Systems Face Single-Use Disruption

Reusable duodenoscope platforms controlled 68.05% market share in 2025, supported by existing reprocessing suites and sunk capital. Fully single-use systems, however, register an 11.21% CAGR as infection-control priorities gain urgency. Administrators weigh the financial trade-off between upfront capital avoidance and higher per-case consumable expense. Hybrid approaches—reusable main bodies with disposable tips—provide a stepping-stone for budget-conscious providers who still seek lower contamination risk.

Environmental sustainability also enters procurement criteria. Low-water detergents and energy-efficient washers improve the lifecycle profile of reusable fleets, while manufacturers investigate recyclable polymers for single-use models. These parallel innovations keep all technology categories in active contention, ensuring diverse supplier strategies in the medium term.

By Application: Biliary Disorders Lead While Pancreatic Gains Momentum

Biliary disorders represented 61.02% Endoscopic Retrograde Cholangiopancreatography market share in 2025, anchored in well-defined protocols for stone removal and stricture management. Pancreatic disorders, supported by emerging radiofrequency ablation evidence and EUS-guided access, are set to climb at a 9.28% CAGR. Improved survival rates in pancreatic cancer patients augment follow-on endoscopic needs for stent exchange and drainage procedures. For high-risk surgical candidates, endoscopic therapy provides a less invasive alternative with shorter recovery windows.

This application shift is mirrored in academic training curricula, which now dedicate more rotation time to complex pancreatic interventions. Device suppliers bundle biliary and pancreatic toolkits, simplifying inventory and driving cross-application utilisation. The net effect keeps overall procedure counts rising, and pushes average selling prices upward as advanced disposables replace generic accessories.

Geography Analysis

North America maintained 39.12% of Endoscopic Retrograde Cholangiopancreatography market share in 2025 due to robust reimbursement, mature training networks, and early roll-out of single-use scopes. U.S. ambulatory centre growth signals confidence in outpatient ERCP safety profiles, while Canadian provinces adopt similar policies to relieve inpatient pressures. Market players use the region to launch premium technologies, assuming rapid payer uptake and clinician buy-in.

Europe ranks second, driven by stringent infection-control mandates and environmental goals that elevate demand for hybrid and single-use options. The new EU Medical Device Regulation imposes uniform safety standards, smoothing cross-border distribution and encouraging pan-European procurement contracts. Hospitals in Germany and France lead adoption of AI-supported imaging, citing evidence of improved cannulation and reduced fluoroscopy exposure.

Asia-Pacific posts the fastest expansion at 9.92% CAGR. Investments in endoscopy training centres, as seen in the Philippines, bring advanced ERCP to previously under-served populations. China and India stand out with rising pancreatic cancer incidence, translating to higher procedure volumes. Government health-insurance schemes widen access, yet specialist shortages still cap throughput in rural areas. Regional private providers respond by offering executive health packages that include ERCP screening for high-risk demographics.

The Middle East & Africa and South America show smaller absolute numbers but strong relative growth. Sustained oil revenues support capital spending in Gulf Cooperation Council countries, while Brazilian teaching hospitals establish ERCP fellowships to retain talent. These regions rely on simplified scope platforms and tele-mentoring programs to overcome limited local expertise.

Competitive Landscape

The Endoscopic Retrograde Cholangiopancreatography market is moderately fragmented. Olympus, Boston Scientific, and Fujifilm combine broad product portfolios, global sales footprints, and long R&D track records. Olympus emphasises AI-ready ecosystems and hybrid scope designs. Boston Scientific doubles down on single-use innovation and therapeutic accessories such as the SpyGlass DS system, which improves direct visualization in intraductal procedures. Fujifilm leverages imaging depth and processor compatibility in multi-modality suites.

Challenger firms pursue niche tactics. Ambu focuses purely on single-use technology, banking on infection risk aversion to overcome cost objections. Medtronic’s planned distribution of Dragonfly Endoscopy’s pancreaticobiliary system illustrates cross-portfolio expansion that leverages existing channels. Start-ups develop AI software to guide wire placement and lesion classification, often partnering with scope makers to speed regulatory approvals.

Regulatory classification under FDA 510(k) pathways favours incumbents that possess legacy clearances and documentation. Smaller entrants counter with faster iteration cycles, targeting unmet needs such as paediatric instruments or ultra-thin cannulation wires. Strategic alliances, licensing deals, and regional manufacturing agreements continue to reshape competitive boundaries as the market gravitates toward integrated diagnostic-therapeutic platforms.

Endoscopic Retrograde Cholangiopancreatography (ERCP) Industry Leaders

CONMED Corporation

STERIS PLC

Cook Medical

Fujifilm Holdings Corporation

Olympus Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Olympus Corporation received FDA clearance for its EZ1500 endoscopes with Extended Depth of Field imaging, enhancing lesion detection during ERCP.

- April 2025: Medtronic agreed to distribute Dragonfly Endoscopy’s pancreaticobiliary system in the United States, broadening its endoscopic therapy offerings.

- October 2024: Olympus obtained CE approval for three cloud-based AI devices—CADDIE, CADU, and SMARTIBD—and confirmed a Q1 2025 launch of an Intelligent Endoscopy Ecosystem.

Global Endoscopic Retrograde Cholangiopancreatography (ERCP) Market Report Scope

As per the scope of the report, endoscopic retrograde cholangiopancreatography is a procedure that combines endoscopy and fluoroscopy to identify and treat biliary and pancreatic ductal system disorders.

The Endoscopic Retrograde Cholangiopancreatography (ERCP) Market is Segmented by Product (Endoscopes, Endotherapy Devices (Sphincterotomes, Lithotripter, Stents, and Other Endotherapy Devices), Visualization Systems, Energy Devices, and Other Products), Procedures (Biliary Sphincterotomy, Biliary Stenting, Biliary Dilatation, Pancreatic Sphincterotomy, Pancreatic Duct Stenting, and Pancreatic Duct Dilatation), End User (Hospitals, Ambulatory Surgery Centre's and Clinics, Other End Users), Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the market size in value terms in USD for all the abovementioned segments.

| Duodenoscopes | |

| Endotherapy Devices | Sphincterotomes |

| Guidewires & Cannulation Devices | |

| Lithotripters | |

| Stents | |

| Other Endotherapy | |

| Visualization & Imaging Systems | |

| Energy Devices | |

| Accessories & Consumables |

| Biliary Sphincterotomy |

| Biliary Stenting |

| Biliary Dilatation |

| Pancreatic Sphincterotomy |

| Pancreatic Duct Stenting |

| Pancreatic Duct Dilatation |

| Hospitals |

| Ambulatory Surgery Centers |

| Specialty & GI Clinics |

| Reusable |

| Hybrid (Reusable with Disposable Distal Cap) |

| Fully Single-Use |

| Biliary Disorders |

| Pancreatic Disorders |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Duodenoscopes | |

| Endotherapy Devices | Sphincterotomes | |

| Guidewires & Cannulation Devices | ||

| Lithotripters | ||

| Stents | ||

| Other Endotherapy | ||

| Visualization & Imaging Systems | ||

| Energy Devices | ||

| Accessories & Consumables | ||

| By Procedure | Biliary Sphincterotomy | |

| Biliary Stenting | ||

| Biliary Dilatation | ||

| Pancreatic Sphincterotomy | ||

| Pancreatic Duct Stenting | ||

| Pancreatic Duct Dilatation | ||

| By End User | Hospitals | |

| Ambulatory Surgery Centers | ||

| Specialty & GI Clinics | ||

| By Technology | Reusable | |

| Hybrid (Reusable with Disposable Distal Cap) | ||

| Fully Single-Use | ||

| By Application | Biliary Disorders | |

| Pancreatic Disorders | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current Endoscopic Retrograde Cholangiopancreatography market size?

The Endoscopic Retrograde Cholangiopancreatography market is valued at USD 2.17 billion in 2026.

How fast is the Endoscopic Retrograde Cholangiopancreatography market expected to grow?

It is projected to expand at an 8.01% CAGR, reaching USD 3.19 billion by 2031 during 2026-2031.

Which product segment holds the largest Endoscopic Retrograde Cholangiopancreatography market share?

Duodenoscopes lead with 46.98% revenue share in 2025 and continue to grow swiftly.

Why are single-use duodenoscopes gaining traction?

They remove cross-infection risk and now benefit from supportive reimbursement, making them attractive despite higher per-case costs.

Which region shows the highest growth potential through 2031?

Asia-Pacific is forecast to grow at a 9.92% CAGR, driven by expanding healthcare infrastructure and rising disease burden.

Page last updated on: