Endoscope Reprocessing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3 Billion |

| Market Size (2031) | USD 4.45 Billion |

| Growth Rate (2026 - 2031) | 8.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Endoscope Reprocessing Market Analysis by Mordor Intelligence

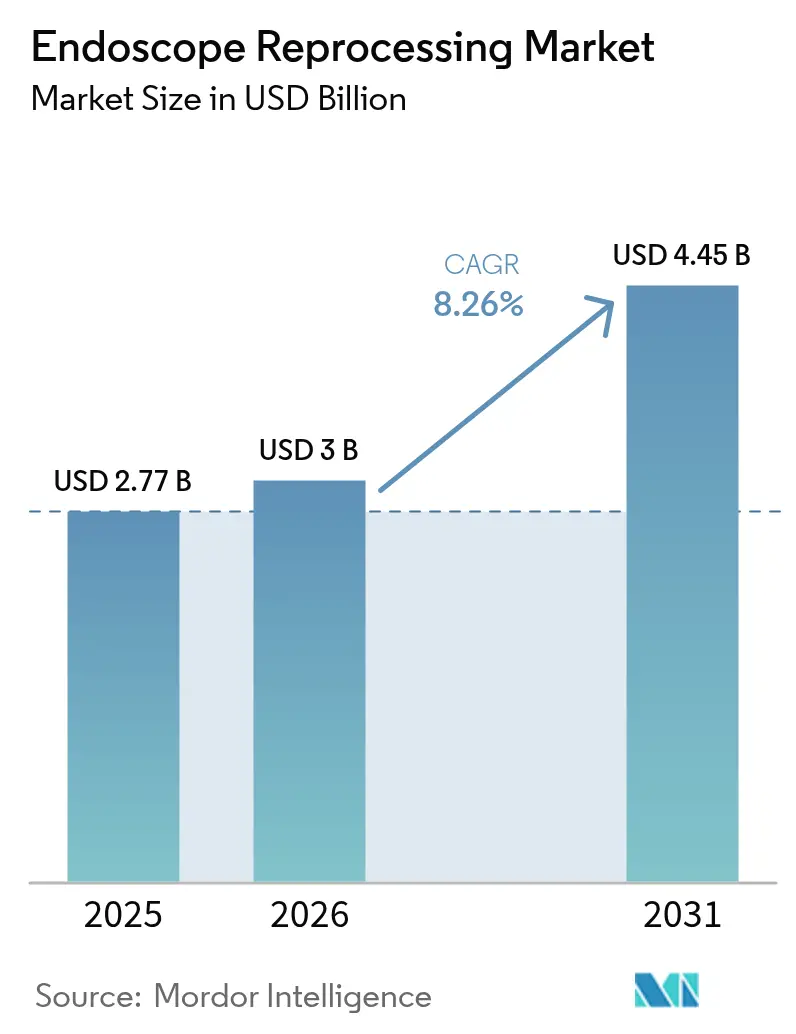

The Endoscope Reprocessing Market size is expected to grow from USD 2.77 billion in 2025 to USD 3.0 billion in 2026 and is forecast to reach USD 4.45 billion by 2031 at 8.26% CAGR over 2026-2031.

This expansion underscores the central role of the endoscope reprocessing market in curbing healthcare-associated infections through rigorous cleaning, disinfection, and sterilization of reusable scopes. Strong procedure growth, particularly in gastrointestinal (GI) and pulmonology suites, keeps demand elevated for consumables, automated reprocessors, and drying cabinets. Hospitals and ambulatory surgery centers (ASCs) are upgrading from high-level disinfection to sterilization following updated AAMI and ASGE guidance. At the same time, single-use scopes gain traction where reprocessing complexity remains high. Vendors respond with liquid chemical sterilization systems that shorten cycle times and with digitally enabled traceability platforms that log every stage of the cleaning workflow. Capital purchases are most pronounced in North America and Western Europe, whereas emerging Asia Pacific markets focus on high-volume, cost-efficient solutions.

Key Report Takeaways

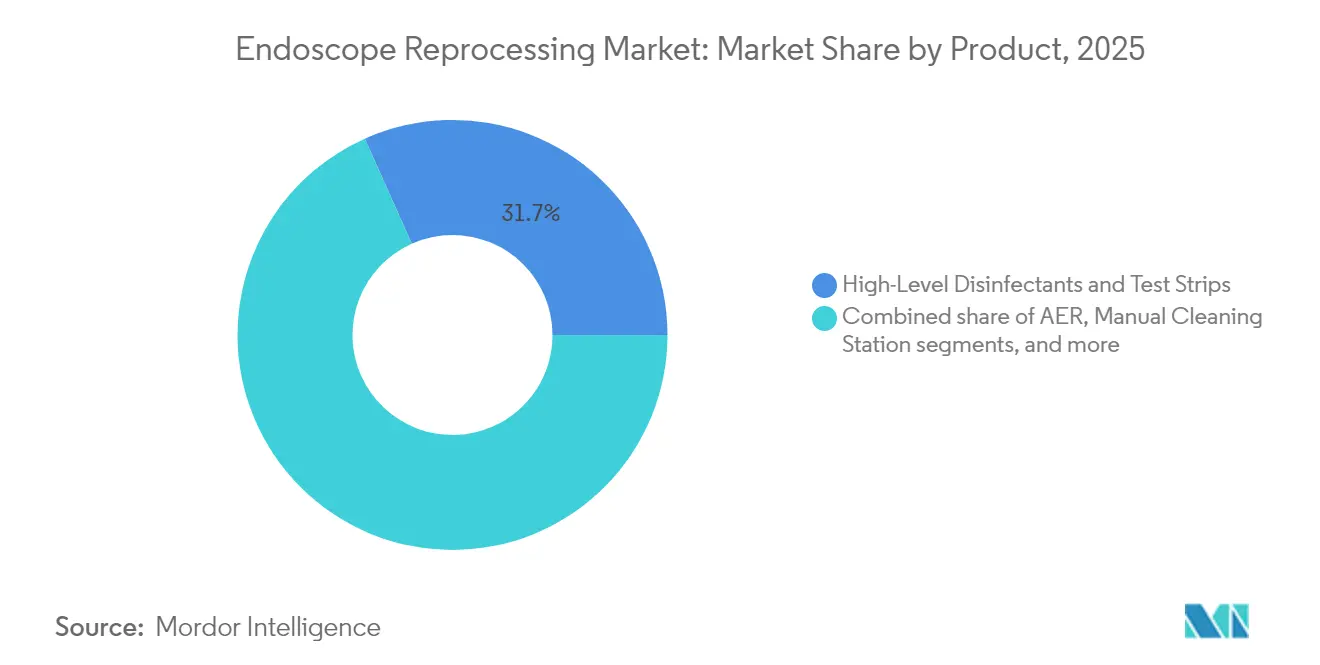

- By product, high-level disinfectants and test strips captured 31.68% of the endoscope reprocessing market share in 2025, while automated endoscope reprocessors are forecast to advance at a 10.31% CAGR through 2031.

- By endoscope modality, flexible endoscopes accounted for 71.10% share of the endoscope reprocessing market size in 2025; robot-assisted endoscopes are projected to grow at an 11.12% CAGR between 2026-2031.

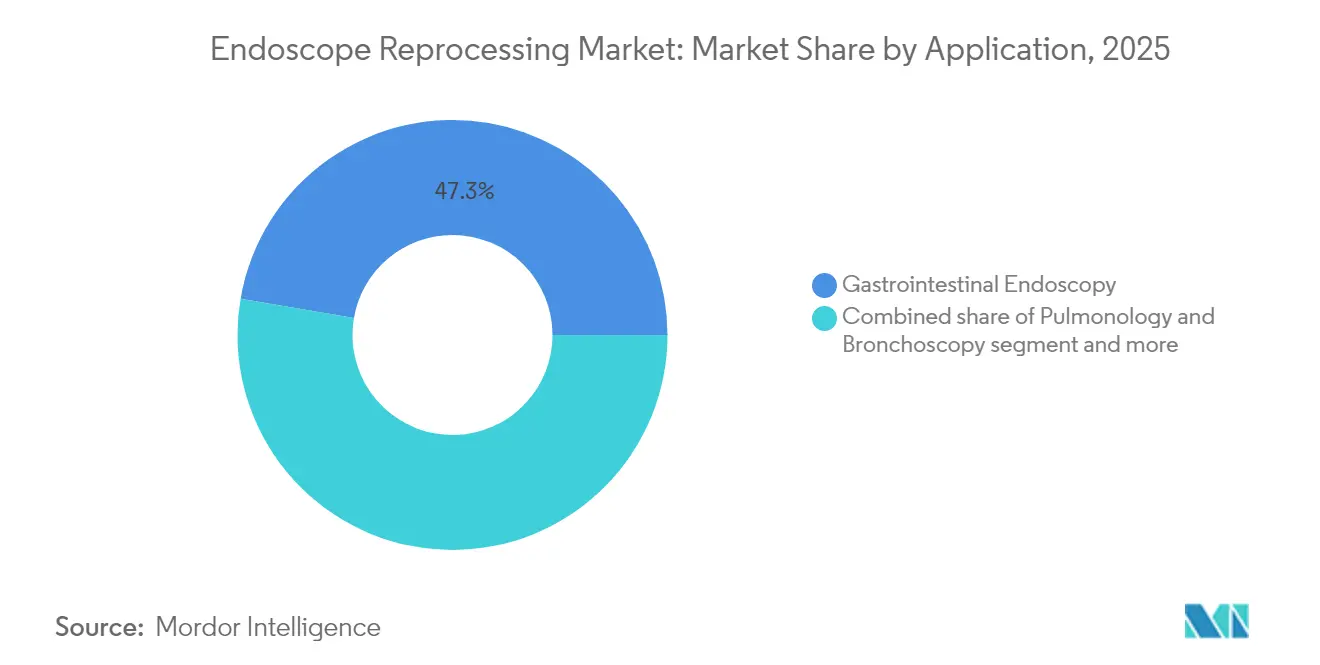

- By application, gastrointestinal endoscopy held a 47.30% share of the endoscope reprocessing market size in 2025; pulmonology and bronchoscopy are expected to register an 10.62% CAGR to 2031.

- By end-user, hospitals contributed 67.05% revenue in 2025, while ASCs are forecast to grow at a 9.88% CAGR through 2031.

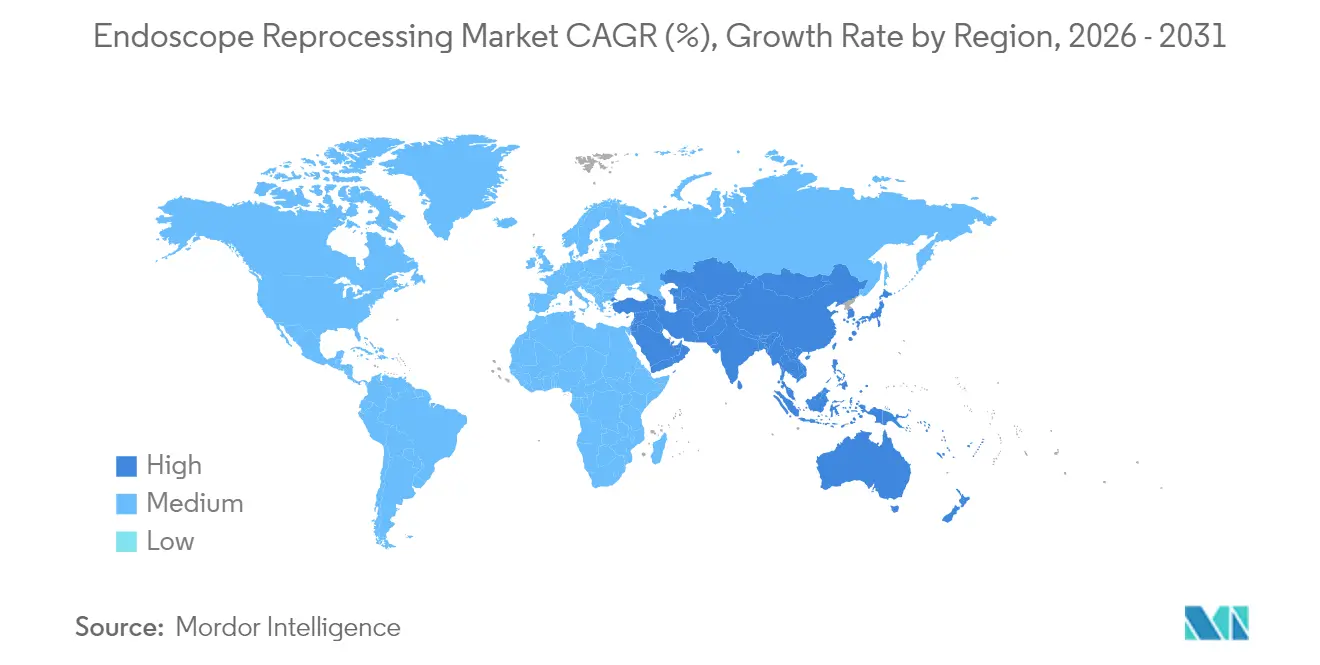

- By geography, North America led with 40.30% revenue share in 2025; Asia Pacific is projected to expand at a 10.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Endoscope Reprocessing Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising endoscopy procedures due to gastrointestinal disorders and cancers | +2.7% | Global, with higher impact in North America and Europe | Long term (≥ 4 years) |

| Increasing adoption of minimally invasive surgeries and daily scope turnover demands | +2.1% | Global, with significant impact in developed healthcare markets | Medium term (2-4 years) |

| Tightening infection-control and accreditation standards mandating validated reprocessing cycles | +1.8% | North America, Europe, and developed Asia-Pacific markets | Short term (≤ 2 years) |

| Advances in automated reprocessors that cut turnaround time and errors | +1.4% | Global, with early adoption in North America and Western Europe | Medium term (2-4 years) |

| Growing demand for single-use endoscopic accessories with compatible disinfectants | +1.1% | North America, Europe, and high-income Asia-Pacific countries | Medium term (2-4 years) |

| Expanding outpatient and ambulatory surgery center adoption of endoscopic procedures | +0.8% | North America and Europe, with emerging growth in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Endoscopy Procedures: Aging Demographics Fuel Demand

An expanding elderly population and broader cancer-screening guidelines are driving double-digit increases in GI and respiratory scope use, giving the endoscope reprocessing market sustained tailwinds. More than 20 million GI examinations are performed annually[1]Ruixue Hu et al., “Current Management Status of Cleaning and Disinfection for Gastrointestinal Endoscopy,” Scientific Reports, nature.com in the United States alone, according to a 2024 meta-analysis. Higher procedural throughput obliges facilities to invest in additional reprocessing capacity, rapid turnaround detergents and leak-testing tools that uphold sterility for every cycle.

Minimally Invasive Surgery: Scope Turnover Drives Reprocessing Innovation

Ambulatory surgery centers rely on tight scheduling and quick scope turnaround to remain profitable. A LEAN workflow pilot[2]Trilokesh Kidambi et al., “LEAN Methodology to Improve Endoscopy Unit Efficiency,” Cureus, cureus.com cut waiting-room time by 48.8% and reduced total facility time by 12%. These gains highlight why the endoscope reprocessing market increasingly favors fully automated washers, drying cabinets and real-time tracking software that shorten bottlenecks without compromising infection-control protocols.

Infection-Control Standards: Regulatory Pressure Transforms Practices

Guideline updates from AAMI and the American Society for Gastrointestinal Endoscopy now recommend sterilizing all flexible scopes to eliminate biofilm and multidrug-resistant organisms. Studies reveal that 5.4% of clinically used duodenoscopes remain contaminated even after standard cycles. In response, healthcare systems are recalibrating protocols to favor vaporized hydrogen peroxide, peracetic acid sterilizers and rigorous validation tests.

Automated Reprocessing: Technology Reduces Human Error

State-of-the-art automated endoscope reprocessors (AERs) integrate channel-specific flow control, leak testing and barcode-driven cycle selection, removing variability associated with manual processes. The FDA[3]U.S. Food and Drug Administration, “Information About Automated Endoscope Reprocessors,” fda.gov underscores their value in lowering infection risk from complex duodenoscopes. STERIS’s en spire 3000 delivers liquid chemical sterilization using peracetic acid in minutes, positioning automation as a principal growth vector in the endoscope reprocessing market.

Restraints Impact Analysis of Endoscope Reprocessing Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of certified endoscope reprocessing technicians and high turnover rates | -1.2% | Global, with severe impact in rural and underserved regions | Medium term (2-4 years) |

| High upfront and lifecycle costs for automated reprocessing systems and drying cabinets | -0.9% | Emerging markets in Asia-Pacific, Middle East & Africa, and South America | Short term (≤ 2 years) |

| Safety concerns with residual contamination in complex duodenoscopes | -0.7% | Global, with particular focus in North America and Europe | Short term (≤ 2 years) |

| Frequent audits and documentation cause high consumable costs and workflow disruptions | -0.5% | North America and Europe with strict regulatory oversight | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Workforce Challenges: Technician Shortages Impede Implementation

Effective cleaning demands specialized knowledge of scope architecture and channel brushing techniques. Yet many hospitals struggle to recruit and retain certified staff,[4]Cori L. Ofstead et al., “Endoscope Processing Effectiveness,” American Journal of Infection Control, ajicjournal.org with error-prone steps contributing to notable contamination events. Although automation offsets some manual tasks, qualified personnel remain indispensable for inspection, trouble-shooting and quality assurance across the endoscope reprocessing market.

Cost Barriers: Financial Constraints Limit Technology Adoption

Capital-intensive AERs, drying cabinets and tracking software strain budgets at small hospitals and clinics. Dual-basin reprocessors are preferred but command premium prices and recurring consumable costs. Facilities in emerging economies often extend the life of legacy washers or rely on manual methods, slowing modernization even as guideline expectations climb.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Endoscope Reprocessing Market Segment Analysis

By Product:

Disinfectants Remain Mainstay While Automation AcceleratesHigh-level disinfectants and indicator strips hold a 31.68% endoscope reprocessing market share in 2025, reflecting the historical reliance on chemical HLD for flexible scopes. Novel enzymatic detergents that eliminate rinse steps now save nearly 25 L of water and cut manual cleaning time by 15%. Yet outbreaks linked to residual biofilm are steering infection-control committees toward sterilants such as vaporized hydrogen peroxide and peracetic acid. This shift boosts demand for integrated washer-sterilizers that complete validated cycles without operator adjustment, a key performance criterion as accreditation audits intensify.

Automated endoscope reprocessors are the fastest-growing product group at a 10.31% CAGR, propelling the overall endoscope reprocessing market. Vendors emphasize closed-loop documentation, RFID tagging and cloud-based analytics that record every scope serial number, cycle parameters and leak-test result. Drying and storage cabinets also gain prominence; systems such as WASSENBURG DRY 320 preserve microbiological quality for 30 days under HEPA-filtered airflow. Together, these products help facilities demonstrate compliance and reduce costly re-processing failures.

By Endoscope Modality:

Flexible Scopes Face Robotic DisruptionFlexible endoscopes commanded 71.10% of 2025 revenue, underpinning the current endoscope reprocessing market size at the modality level. Owing to their reach and articulation, they remain indispensable across GI, respiratory, ENT, and urology suites. However, their complexity makes them vulnerable to channel debris. Structured borescope inspections and fluorescence markers are thus being adopted to affirm cleaning efficacy.

Robot-assisted endoscopes are projected to rise 11.12% annually through 2031, carving new opportunities in the endoscope reprocessing market. Two-armed robotic colonoscopes and multi-visceral surgical robots promise enhanced ergonomics and autonomy. Their adoption will demand dedicated washer racks, protocol modifications, and staff retraining. Rigid scopes retain a stable niche for arthroscopy and laparoscopy, benefiting from simpler lumens that sterilize reliably in steam autoclaves.

By Application:

GI Dominance Persists as Pulmonology SurgesGastrointestinal procedures generated 47.30% of revenue in 2025 and anchor the endoscope reprocessing market size for applications. Colonoscopy volumes expand as universal screening begins at age 45 in several countries, accelerating scope turnover. Subsequent high-profile incidents exposing patients to HIV and hepatitis due to lapses have driven hospitals to audit every cleaning phase. Facilities now incorporate automated channel flushing and real-time ATP bioluminescence tests to safeguard GI workflows.

Pulmonology and bronchoscopy represent the fastest-growing category with an 10.62% CAGR, reflecting heightened focus on chronic respiratory diseases and critical-care bronchoscopy. Visualization reviews underscore frequent contamination of reusable bronchoscopes when drying is incomplete. Single-use flexible bronchoscopes bypass the need for reprocessing and have recorded strong clinical acceptance in bronchoalveolar lavage studies. ENT, urology, and gynecology remain steady contributors, each confronting procedure-specific biofilm challenges that shape detergent selection and drying protocols.

By End-User:

Hospitals Dominate, ASCs Gain MomentumHospitals accounted for 67.05% of 2025 revenue, reflecting centralized capability, 24-hour staffing and the budget latitude to deploy multiple AERs per cleaning room. Meta-analysis indicates 76% of facilities maintain separate decontamination rooms yet just 30% utilize washer-disinfectors. Integrating electronic tracking dashboards helps infection-control teams reconcile scope usage logs with reprocessing data, reducing recall response times when contamination alerts arise.

ASCs are forecast to post a 9.88% CAGR, redirecting procedure mix away from inpatient settings and expanding the endoscope reprocessing market. Higher CMS reimbursement (+2.9% for 2025) encourages adoption of compact, dual-basin reprocessors tailored to outpatient footprints. Single-day throughput necessitates rapid drying cabinets and on-cart transport systems that preserve sterility until patient contact. Physician offices and specialty clinics, although smaller in absolute revenue, increasingly invest in tabletop washers and pre-filled sterilant cartridges that minimize staff burden.

Geography Analysis

North America Endoscope Reprocessing Market

North America held 40.30% of 2025 revenue, supported by high procedural volumes and rigorous oversight from the FDA, CDC and accreditation bodies. A spotlight on infection outbreaks at leading centers has intensified demand for traceable, automated workflows and for vaporized hydrogen peroxide cabinets capable of sterilizing duodenoscopes within 35 minutes. Regional growth is projected at an 7.92% CAGR through 2031, with spending tilted toward data-rich reprocessors, borescope inspection cameras, and disposable duodenoscopes for high-risk ERCP cases.

APAC, EMEA and South America Endoscope Reprocessing Market

Asia-Pacific is the fastest-expanding territory, anticipated to advance 10.35% annually. India’s medical-device roadmap seeks USD 50 billion in sector output by 2030, with endoscopy systems and ancillary reprocessing devices eligible for production incentives. China, Japan, and South Korea allocate capital to negative-pressure drying cabinets and channel-specific leak testers, while resource-limited Pacific Islands confront shortages of purified water and certified technicians. Europe commands roughly 29.30% of the endoscope reprocessing market, posting an 8.14% CAGR projection to 2031. EU surveillance attributes more than 3.5 million healthcare-associated infections to reusable devices each year. NHS contracts exceeding GBP 250,000 awarded in 2024 reflect hospital moves to validate decontamination equipment and ensure scope-level traceability. The Middle East & Africa and South America follow with moderate growth as tertiary centers modernize CSSD units and adopt AERs capable of handling mixed scope inventories without repeated chemical changes.

Regulatory Landscape

In the United States, automated endoscope washers, washer-disinfectors, and related reprocessing equipment are regulated as medical devices, with pathway expectations anchored in FDA 510(k) submissions and the requirement that healthcare facilities reprocess reusable devices strictly per the manufacturer instructions for use (IFU). Infection-control expectations are reinforced by CDC and HICPAC guidance for flexible endoscope reprocessing, which facilities align with accreditation and survey requirements emphasizing validated cycles, documentation, and staff training.

In Europe, the Medical Device Regulation (EU) 2017/745 (MDR) remains the governing framework as of January 1, 2026, shaping conformity assessment, post-market obligations, and the compliance burden around reprocessing workflows. Under MDR Article 17, reprocessing of single-use devices is permitted only where allowed by national law, and entities that reprocess single-use devices are treated as manufacturers under MDR, which elevates requirements for validation, risk management, and traceability and creates cross-country variability based on Member State rules.

Competitive Landscape

The endoscope reprocessing market features a medium concentration. STERIS, Olympus, Getinge and Advanced Sterilization Products lead through broad portfolios that bundle detergents, AERs, drying cabinets and SaaS compliance dashboards. STERIS markets the enspire 3000 liquid chemical sterilizer, enabling sterilization of complex scopes in 18 minutes, while Getinge’s Poladus 150 provides low-temperature options for heat-sensitive instruments. Olympus bolsters its presence with the OER-Elite AER coupled to its proprietary detergent line, streamlining post-market surveillance of scope condition.

Competitive dynamics intensify as Ambu, whose single-use scopes delivered 19.7% revenue growth and now represent 59% of corporate turnover, gains market share. The disposable model fundamentally displaces reprocessing for certain airway and GI indications, forcing incumbents to justify capital investments in automated systems through life-cycle cost analyses, downtime avoidance and environmental win-backs such as detergent recycling.

Emerging disruptors focus on workflow digitization. Nanosonics’ CORIS platform secured FDA De Novo clearance in March 2025 and automates channel brushing via micro-bristle technology, harvesting usage data for machine-learning algorithms that predict maintenance requirements. Start-ups delivering mobile leak-testers, ATP on-scope fluorescence sensors and AI-driven borescope analytics are expected to widen the supplier base and pressure pricing across the endoscope reprocessing market.

Endoscope Reprocessing Industry Leaders

Advanced Sterilization Products Services Inc

Ecolab Inc.

Getinge AB

Olympus Corporation

STERIS plc

- *Disclaimer: Major Players sorted in no particular order

Endoscope Reprocessing Market Companies Covered in this Report

- Advanced Sterilization Products Services Inc

- ARC Group of Companies Inc.

- Belimed

- BES Healthcare Ltd

- Creo Medical GmbH

- Ecolab

- Envista Holdings (Metrex Research)

- Getinge

- HOYA Corporation (Pentax Medical)

- Matachana Group

- Olympus

- Shinva Medical Instrument Co.

- Steelco

- STERIS

- UV Smart BV

- Wassenburg Medical B.V.

Market Opportunities and Future Outlook

Throughput-focused automation is increasingly pairing with auditable traceability as facilities respond to stricter reprocessing expectations while handling higher scope turnover in GI and pulmonology suites. Getinge's June 2026 launch of the Aquadis Endo 110 illustrates this direction, with faster standard cycles and embedded RFID-based program selection and traceability that support facilities tightening documentation and reducing manual steps that contribute to variability.

A second opportunity is the ongoing shift from high-level disinfection toward sterilization pathways for complex scopes, supported by platform-level cycle innovation and validated compatibility partnerships. In January 2026, Advanced Sterilization Products (ASP) received CE Mark for its ULTRA GI Cycle for duodenoscopes for use on the STERRAD 100NX Sterilizer in collaboration with FUJIFILM Healthcare Europe, reinforcing demand for validated, scope-specific cycles and complementary monitoring and compliance infrastructure inside sterile processing departments. Business models that reduce upfront capital friction, such as Ecolab's November 2025 Pay As You Go Endo Bundle combining Soluscope AERs, drying, and traceability software on a per-usage basis, also broaden addressability among ambulatory and mid-sized facilities that need standardized, reportable workflows while managing budget constraints.

Recent Industry Developments in Endoscope Reprocessing Market

- June 2026: Getinge launched the Aquadis Endo 110 automated endoscope reprocessor, highlighting a 20-minute standard cycle and integrated RFID for automated program selection and traceability. The launch underscores supplier focus on higher-throughput, lower-variability reprocessing to support rising procedure volumes and tighter documentation requirements.

- April 2026: Advanced Sterilization Products (ASP) announced a strategic partnership with ChemDAQ to integrate continuous hydrogen peroxide gas detection and monitoring into sterile processing environments. The partnership strengthens the safety and compliance layer around low-temperature sterilization workflows that use hydrogen peroxide-based processes.

- August 2024: Advanced Sterilization Products (ASP) announced FDA clearance for a sterilization cycle for duodenoscopes in partnership with PENTAX Medical. The clearance advances validated sterilization options for complex scopes where residual contamination concerns drive purchases of compatible sterilization systems and associated consumables.

Endoscope Reprocessing Market Report Scope and Research Methodology

Market Definition and Coverage

This market is defined as the revenue generated from products and solutions used to clean, high-level disinfect, dry, store, and safely handle reusable endoscopes between patient procedures in healthcare settings.

Scope exclusions: Single-use endoscopes and third-party endoscope repair or refurbishment services are excluded from this market sizing.

Segments Covered in This Report

- By Product

- High-Level Disinfectants & Test Strips

- Detergents & Enzymatic Wipes

- Automated Endoscope Reprocessors (AER)

- Single-basin

- Dual-basin

- Manual Cleaning Stations

- Endoscope Drying, Storage & Transport Cabinets

- Others

- By Endoscope Modality

- Flexible Endoscopes

- Rigid Endoscopes

- Robot-Assisted Endoscopes

- By Application

- Gastro-intestinal Endoscopy

- Pulmonology & Bronchoscopy

- Urology & Gynaecology

- ENT & Laparoscopy

- By End-User

- Hospitals

- Ambulatory Surgery Centres (ASC)

- Other End-Users

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the reprocessing workflow and to anchor the model using public signals that tend to be stable year to year. We reviewed sources such as US FDA safety communications and device guidance, US CDC infection prevention resources, Centers for Medicare and Medicaid Services procedure and facility context, and World Health Organization infection prevention and control materials. Where helpful, peer-reviewed papers on endoscope contamination risk and reprocessing compliance patterns were included to reduce reliance on a single narrative.

To translate those signals into a usable commercial view, we supplemented with company annual reports, investor presentations, and reputable press coverage of recalls and guideline changes. We also cross-checked with paid subscriptions for company financials and intelligence plus patent databases. Trade statistics and public procurement notices were referenced selectively when they helped validate equipment placement or replacement cycles. These desk sources are illustrative only, and many other public documents were used for data collection, validation, and clarification during the research.

Primary Interviews and Surveys

Primary work focused on confirming what is actually purchased and how often it is replaced across hospitals, ambulatory surgery centers, and specialty clinics, since practice varies by facility type and country. We spoke with a mix of infection prevention leaders, sterile processing teams, and procurement contacts, then rechecked assumptions with distributors and service partners that see ordering frequency in the field. Coverage was kept global so regional differences in guideline adoption and procedure growth could be reflected in the final market model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 19% | APAC: 46% |

| Mid tier: 43% | Functional/Unit leaders: 25% | EMEA: 35% |

| Smaller Players: 19% | Managers: 56% | Americas: 19% |

Market-Sizing & Forecasting

Market sizing starts with a top-down build where procedure volumes and installed endoscope fleets are used to reconstruct the demand pool for each reprocessing step, and then the spend is assigned across equipment and consumables. In practice, the model links demand to indicators such as endoscopy procedure growth, average reprocessing cycles per scope per day, AER and drying cabinet penetration, replacement and maintenance intervals, and high-level disinfectant consumption patterns. When the main clause is reached, the market value is obtained by applying realistic pricing bands and utilization levels to that demand pool.

Those totals are then checked using selective bottom-up approximations, such as roll-ups from sampled supplier revenue splits, channel feedback on unit shipments, and ASP times volume checks for AER placements and core consumable categories. Gaps that appear in smaller countries or outpatient settings are handled through proxy ratios built from comparable healthcare capacity metrics and then adjusted through interview feedback. For forecasting, we used scenario analysis supported by short-cycle drivers, which are then translated into year-by-year outcomes based on expert consensus on procedure growth, tightening reprocessing guidelines, and adoption of automated and drying solutions.

Data Validation & Update Cycle

Validation is done in layers so the final numbers are not driven by one data source or one assumption. We compare outputs against independent signals like procedure growth trends, equipment placement pace, and consumable run-rate logic, and then investigate any sharp jumps that do not match the operational reality described by respondents. When large variances show up by region or by product group, the assumptions are rechecked and, where needed, clarifying calls are triggered before the model is signed off.

Reports are refreshed annually, and interim updates are made when material events occur, such as major recalls, guideline changes, or step-changes in adoption of automated reprocessing and drying. Before delivery, the analysis is reviewed again so clients receive the latest updated view with consistent scope and currency handling.

Mordor Intelligence's Endoscope Reprocessing Market Sizing Compared With Other Published Estimates

Published market sizes for endoscope reprocessing can look far apart, even when the topic sounds the same, because each study draws its boundary around different products, end users, and pricing logic. Differences also come from the year used for sizing, how fast prices are assumed to move, and whether the estimate is refreshed after guideline changes or safety events.

By tracking AER placement signals, disinfectant consumption logic, and currency timing checks, Mordor Intelligence keeps the market total tied to reusable endoscope workflows while excluding single-use scopes and unrelated repair revenues, which is where many spreads start. Some estimates also mix factory-gate pricing with downstream markups or bundle adjacent probe disinfection categories, and these choices can shift the number up or down even before forecasting assumptions are applied.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.77 B (2025) | |

| Global Consultancy A | USD 1.80 B (2025) | Uses a narrower scope and a different base-year definition, which appears to undercount equipment and workflow-adjacent items like drying and storage solutions in some regions. |

| Industry Publisher B | USD 3.02 B (2025) | Leans on factory-gate values that may include related services and a broader equipment set, and the short historic growth rate can inflate the near-term number if applied uniformly across geographies. |

Across the table, the largest drivers are scope boundaries (what is counted as reprocessing), price level assumptions (manufacturer selling price versus broader revenue capture), and how recent operational changes are reflected. Our approach aims to keep the sizing steps traceable to procedure-linked demand, equipment penetration, and consumable run-rates, so the final value can be explained and rechecked with practical market signals.

Key Questions Answered in the Report

Why are healthcare providers adopting automated endoscope reprocessors (AERs) more quickly than manual methods?

Automated systems standardize every cleaning stage, integrate leak testing and digital documentation, and lower the risk of human error, which accreditation audits increasingly scrutinize.

How are updated infection-control guidelines influencing hospital purchasing decisions?

Guidelines that now prioritize sterilization for flexible scopes are prompting hospitals to invest in liquid-chemical sterilizers, low-temperature systems and drying cabinets rather than adding more chemical disinfectants.

What is driving the rise of single-use endoscopes in pulmonology and gastroenterology?

Concern over residual biofilm in complex channels, combined with pressure to shorten procedure turnover times, is pushing clinicians toward disposable scopes that bypass reprocessing altogether.

How are staffing shortages affecting endoscope reprocessing quality?

Limited availability of certified technicians leads to workflow bottlenecks and increases the likelihood of protocol deviations, encouraging facilities to automate tasks and deploy real-time tracking software for oversight.

Which digital technologies are improving traceability in endoscope reprocessing?

RFID tagging, cloud-based cycle logs, and AI-powered borescope inspection platforms are being integrated to create an end-to-end audit trail that simplifies compliance reporting.

What competitive strategies are established vendors using to respond to new market entrants?

Incumbents are bundling consumables, capital equipment and software into unified service contracts, while expanding training programs to help facilities transition from high-level disinfection to sterilization.

Page last updated on: