Global Stethoscope Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

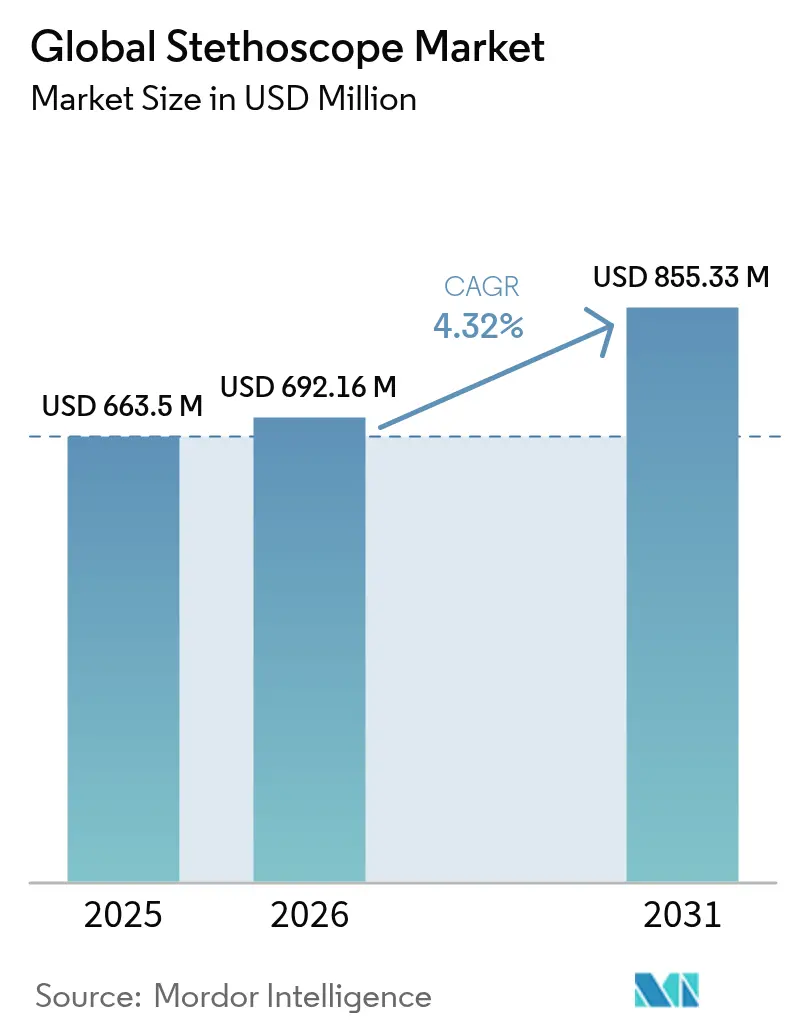

| Market Size (2026) | USD 692.16 Million |

| Market Size (2031) | USD 855.33 Million |

| Growth Rate (2026 - 2031) | 4.32% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

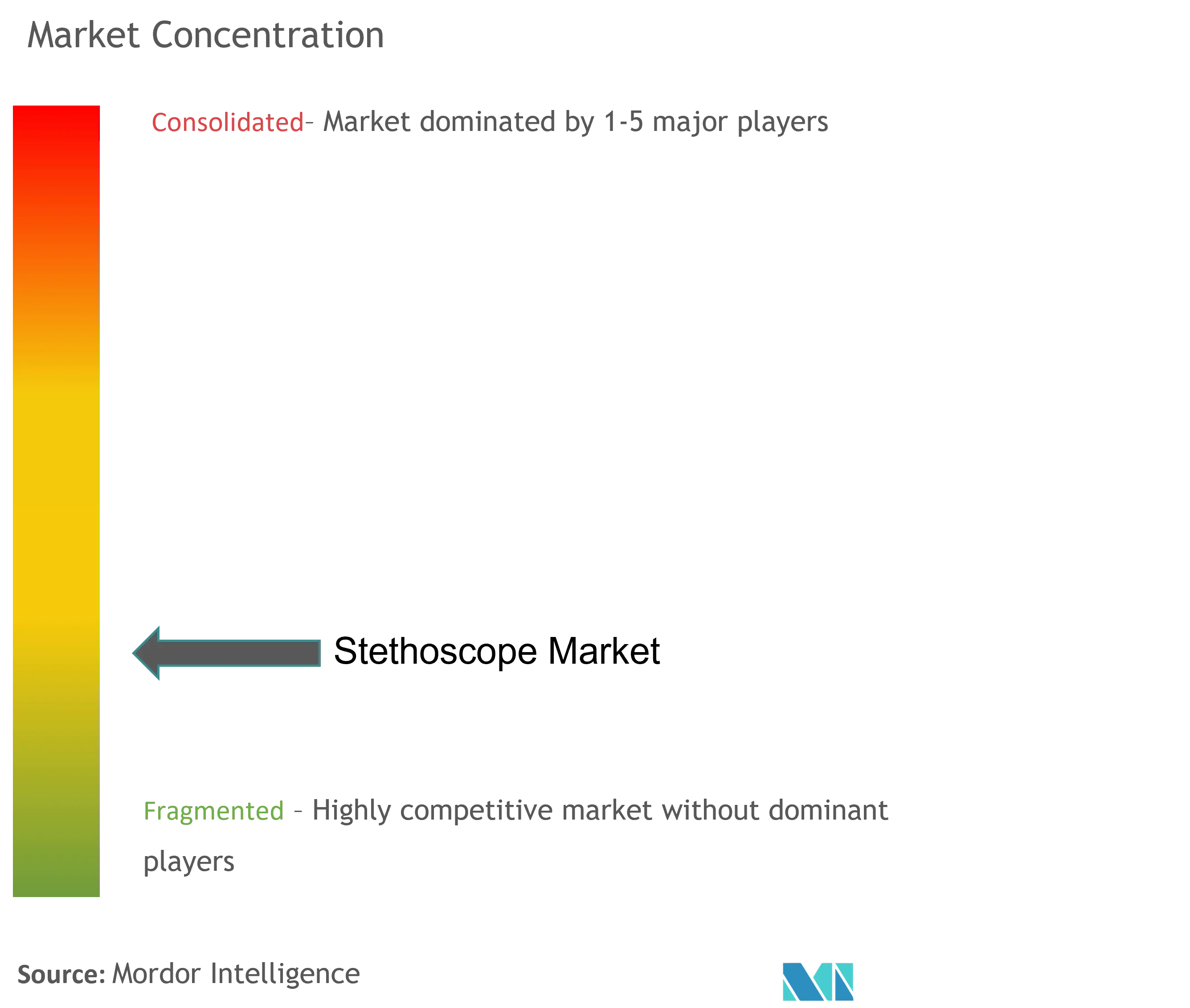

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Stethoscope Market Analysis by Mordor Intelligence

The Stethoscope Market size was valued at USD 663.50 million in 2025 and estimated to grow from USD 692.16 million in 2026 to reach USD 855.33 million by 2031, at a CAGR of 4.32% during the forecast period (2026-2031). Growth is shaped by the transition from purely acoustic devices to connected instruments that embed algorithms capable of flagging murmurs, low ejection fraction, and pulmonary crackles within seconds. Cardiovascular-disease prevalence, accounting for 80% of deaths in low- and middle-income nations, sustains baseline demand while telemedicine adoption opens new channels for point-of-care sales. FDA clearance of Eko Health’s low ejection-fraction algorithm has raised clinician confidence in smart auscultation and spurred venture funding toward handheld solutions that sync with electronic health-record platforms [1]Food and Drug Administration, “Eko Low Ejection Fraction Algorithm Decision Summary,” fda.gov. Parallel headwinds include handheld ultrasound substitution, component shortages, and incoming materials regulation, yet incumbent brands leverage scale to contain cost inflation and protect distribution footprints. Regional opportunities are most visible in Asia-Pacific, where public-sector spending on primary care and mobile clinics coincides with rising chronic-disease incidence, making the stethoscope market a focal point for med-tech localization programs.

Key Report Takeaways

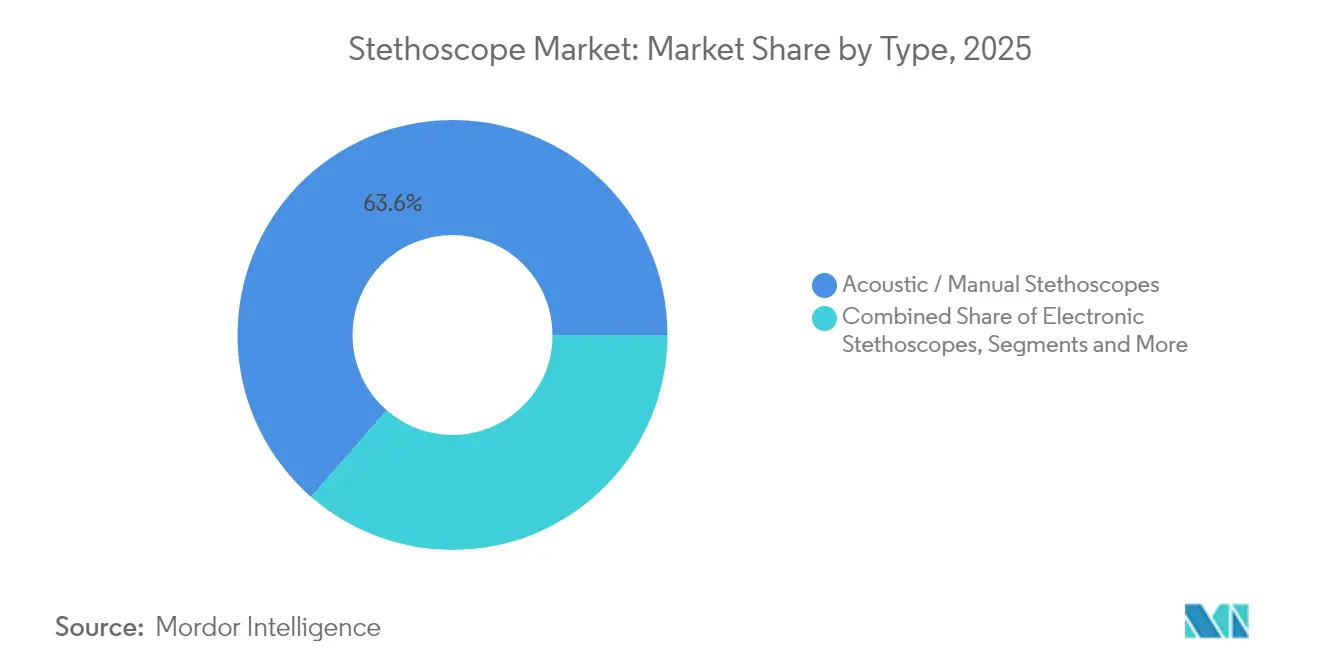

- By type, acoustic/manual units retained 63.58% of the stethoscope market share in 2025, while smart/AI-enabled models are on course for a 5.27% CAGR to 2031.

- By end user, hospitals held 59.22% revenue share of the stethoscope market size in 2025; home healthcare is poised to grow at 4.81% CAGR through 2031.

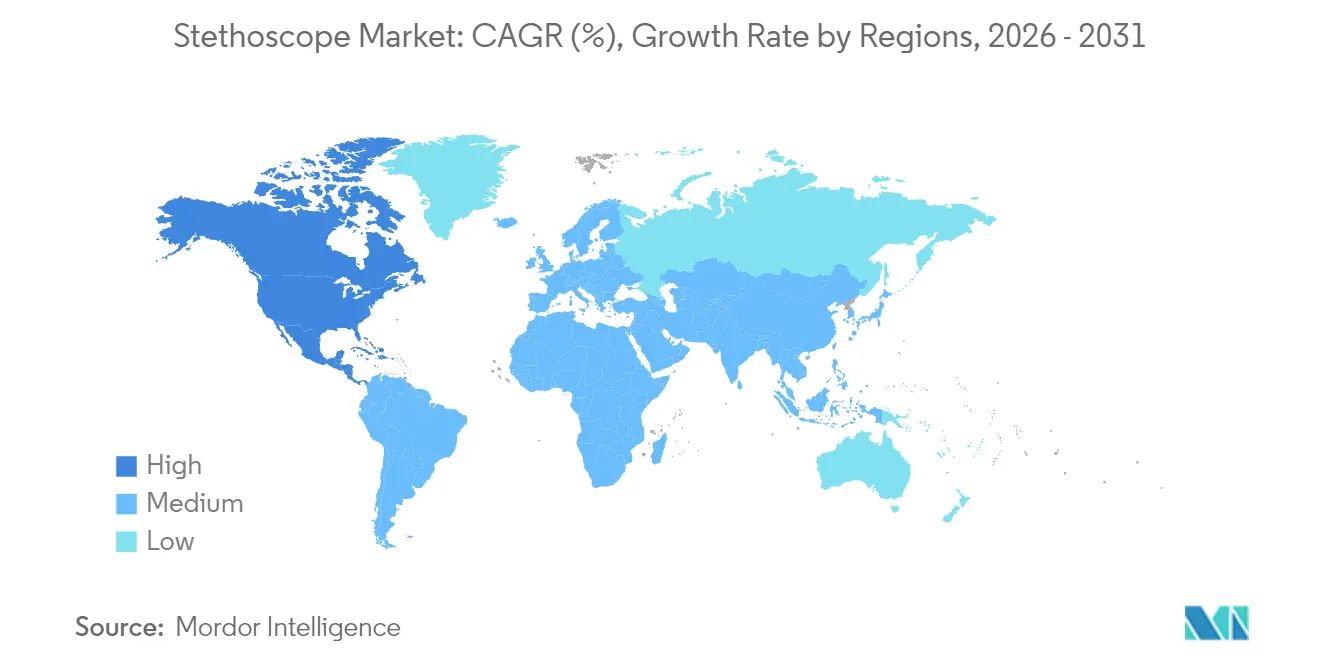

- By geography, North America led with 44.78% of the stethoscope market size in 2025, yet Asia-Pacific delivers the fastest 5.49% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Stethoscope Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of cardiovascular & pulmonary diseases | +2.1% | Global, strongest in Asia-Pacific and Middle East & Africa | Long term (≥ 4 years) |

| Increase in routine patient visits & physical exams | +1.8% | North America and Europe, extending into Asia-Pacific | Medium term (2-4 years) |

| Accelerating adoption of digital & AI-enabled stethoscopes | +2.3% | North America and Europe lead, Asia-Pacific follows | Medium term (2-4 years) |

| Expansion of home-care & remote monitoring models | +1.9% | United States, Canada, Germany, expanding globally | Short term (≤ 2 years) |

| Infection-control demand for disposable accessories | +0.8% | Global, most intense in hospital-dense nations | Short term (≤ 2 years) |

| Veterinary-care boom boosting specialty stethoscopes | +0.6% | North America & Europe, nascent in Asian metros | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Cardiovascular & Pulmonary Diseases

Ischemic heart disease maintained an age-standardized 108.8 deaths per 100,000 worldwide in 2023, and total CVD deaths climbed to 19.8 million in 2022. These data elevate continuous auscultation from episodic bedside practice into year-round monitoring in outpatient and community settings. A Mayo Clinic trial in Nigeria showed AI-ready scopes doubling peripartum cardiomyopathy detection versus legacy methods, underlining value in regions short on cardiologists. WHO non-communicable-disease strategies now encourage early-stage cardiopulmonary screening in primary care, further institutionalizing the stethoscope market within public-health budgets. In the United States, heart-failure management already drives more than USD 30 billion in annual spending, positioning algorithm-equipped devices as cost-avoidance tools for payers.

Accelerating Adoption of Digital & AI-Enabled Stethoscopes

FDA clearance in April 2024 for Eko Health’s low-ejection-fraction algorithm validated that 15-second heart-failure screening can fit into routine vitals collection. The ruling coincided with Eko’s USD 41 million Series D, expanding installed base to over 500,000 clinicians worldwide [2]Eko Health, “Series D Funding Announcement,” ekohealth.com. Machine-learning models trained on decades of heart-sound libraries now surface structural murmurs at primary-care level, narrowing referral delays. Device connectivity via Bluetooth and Wi-Fi funnels raw phonocardiograms to cloud dashboards, letting remote cardiologists verify findings asynchronously. Regulatory momentum, including updated FDA cybersecurity guidance, lowers adoption friction yet raises the bar on software maintenance—favoring suppliers with dedicated MLOps capacity.

Expansion of Home-Care & Remote Monitoring Models

Permanent telemedicine reimbursement in the United States permits stethoscope-assisted virtual visits, pushing devices into home-health kits marketed through payers and pharmacy chains. Caregiver-operated digital scopes achieved hospital-equivalent sound fidelity in pediatric tele-cardiology studies, proving layperson usability. Integration with HIPAA-compliant video platforms reduces rural travel burdens for chronic heart-failure and COPD cohorts. FDA-cleared USB scopes with screen-share features are now procured by assisted-living networks and school health programs, broadening end-user categories earlier absent from the stethoscope market.

Infection-Control Demand for Disposable Accessories

Post-pandemic infection-prevention protocols elevate stethoscope hygiene scrutiny. Clinical audits show surface contamination on 85% of inpatient scopes, prompting facilities to trial automated diaphragms and single-use covers [3]Aseptiscope, “Clinical Audit on Stethoscope Contamination,” aseptiscope.com. Disposable ear-tips and tubing liners add recurring revenue layers for OEMs and third-party suppliers. Hospitals’ quality-improvement teams increasingly allocate separate budgets for disposables that cut reprocessing labor and mitigate Medicare readmission penalties linked to hospital-acquired infections.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hand-held ultrasound reducing reliance on auscultation | -1.4% | North America & Europe early adoption, global expansion | Medium term (2-4 years) |

| Price pressure & commoditization of manual models | -0.9% | Global, particularly acute in price-sensitive markets | Short term (≤ 2 years) |

| PVC & elastomer shortages disrupting tubing supply | -1.1% | Global, with acute impact in Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Data-privacy concerns around cloud-linked devices | -0.7% | North America & Europe regulatory focus, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hand-Held Ultrasound Reducing Reliance on Auscultation

A study of 250 patients showed pocket ultrasound spotting 82% of cardiac abnormalities versus 47% for standard examination and trimming downstream testing spend from USD 707.44 to USD 644.43 per patient. Emergency departments adopt probe-based workflows that bypass auscultation, especially for dyspnea triage. Research groups at the University of Cambridge advanced flexible-patch sensors that record heart sounds through clothing, pairing ultrasound imaging and machine-learning analytics for valve screening. Although device costs and training requirements still block wholesale replacement, they compress the upgrade cycle for traditional scopes and challenge growth in high-acuity settings.

Price Pressure & Commoditization of Manual Models

Entry-level acoustic scopes face margin squeeze as contract manufacturers in Vietnam and India offer OEM batches below previous cost floors. Supply disruptions pushed logistics outlays to almost 20% of revenue for some vendors in 2024, magnifying sensitivity to nickel, copper, and medical-grade PVC price swings. Education segments remain price driven; teaching hospitals bulk-buy basic instruments for students each semester, favoring the lowest qualified bid. Without AI or telehealth hooks, mid-tier ranges risk erosion unless bundled with infection-control accessories or extended warranties.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Smart Variants Challenge Acoustic Dominance

In 2025 acoustic/manual devices controlled 63.58% of the stethoscope market, underscoring the category’s heritage and cost edge. The segment still anchors first-year medical curricula and dominates humanitarian‐aid kits, benefiting from batteries-free operation and repair simplicity. Electronic models supply amplified auscultation for ICU teams and pulmonologists who need clearer mid-frequency ranges. Niche teaching scopes integrate headsets that broadcast a single patient’s sounds to multiple trainees simultaneously. Veterinary editions ride the pet-health boom as owners allocate larger budgets for canine cardiology check-ups.

Smart scopes, although a smaller base, compound at 5.27% CAGR to 2031. The stethoscope market size for smart devices is forecast to climb in tandem with hospital digitization grants and insurer telemonitoring pilots. Products such as CORE 500™ layer ECG visualization onto auscultation, accelerating decision-making during chest-pain triage. Regulatory clarity on connected devices plus falling MEMS-microphone costs trim bill-of-materials, letting suppliers position AI features at price points digestible for primary-care clinics. Cloud dashboards add subscription revenue, turning one-time hardware sales into annualized software contracts.

By End User: Hospitals Dominate While Home Healthcare Accelerates

Hospitals captured 59.22% of the stethoscope market in 2025 thanks to centralized purchasing and round-the-clock patient turnover. Cardiology, emergency, and ward rounds collectively drive high utilization per instrument. Academic centers supplement demand with simulation labs that require extra teaching models for OSCE assessments. Outpatient ambulatory-surgery centers mirror hospital preferences but value antimicrobial tubing and auto-disinfection stations that minimize OR downtime.

Home-healthcare usage grows fastest at 4.81% CAGR. The stethoscope market size serving domiciliary nursing agencies will rise as payers reimburse remote auscultation during chronic-care management visits. Bluetooth-enabled scopes feed phonograms into clinician dashboards that trigger alerts when murmurs intensify or crackles emerge—avoiding unnecessary ER transports. Medicare’s telehealth parity rules, adopted permanently in 2024, cement revenue pathways for device makers tuned to at-home protocols. Pediatric asthma monitoring kits and heart-failure bundles shipped through retail pharmacies further widen consumer channels without cannibalizing institutional sales.

Geography Analysis

North America retained 44.78% of the stethoscope market in 2025 aided by robust reimbursement for digital health tools, a mature cardiology workforce, and FDA fast-track pathways that shorten time-to-market for AI algorithms. United States buyers absorb premium SKUs, while Canada’s provincial health systems standardize procurement through group purchasing organizations, keeping volume steady. Mexico’s public-hospital expansion under INSABI reforms nudges acoustic scope demand upward, albeit at lower price tiers. Regional challenges come from handheld ultrasound diffusion inside emergency consortiums where grant funding offsets acquisition costs.

Europe presents a steady but price-sensitive landscape. Demographic aging pushes cardiac-screening volumes, yet austerity measures in Southern nations cap device budgets. Germany and the United Kingdom pilot AI-scope rollouts in primary care to meet early-diagnosis targets, whereas France and Italy lean on hybrid acoustic-electronic formats that fit existing training protocols. The European Union’s postponed DEHP ban buys PVC-tube suppliers another five years but accelerates R&D in silicone-based alternatives Notified-body bottlenecks under MDR lengthen certification cycles, creating entry hurdles for smaller brands.

Asia-Pacific secures the fastest 5.49% CAGR through 2031, anchored by China, India, and Indonesia. Japan fosters early adoption through smart-hospital pilots that integrate auscultation data into nationwide EHRs, while South Korea couples local manufacturing capability with export subsidies, heightening competitive intensity. India’s Ayushman Bharat program steers funds toward primary-care diagnostics in rural blocks, though extreme price sensitivity favors hybrid electronic-acoustic units. Southeast Asian governments, led by Indonesia, channel pandemic-era health-budget increases toward telemedicine infrastructure that aligns with remote-ready stethoscopes.

Regulatory Landscape

In the United States, stethoscopes fall under FDA cardiovascular diagnostic device rules, with manual stethoscopes generally treated as Class I (often 510(k)-exempt) and electronic or digital stethoscopes as Class II devices that typically require 510(k) clearance under product code DQD (21 CFR 870.1875). Recent clearances reinforce the clinical-grade pathway for connected auscultation, including an FDA 510(k) clearance (K252915) in May 2026 for Ai Health Highway India Pvt., Ltd.s AiSteth dual-mode electronic stethoscope.

In Europe, classification commonly splits by intended use and functionality: manual stethoscopes are usually Class I under Regulation (EU) 2017/745, while electronic stethoscopes that monitor physiological parameters often fall under MDR Rule 10 and may be treated as Class IIa, bringing Notified Body involvement into the certification and surveillance cycle. In China, the YY/T 1035-2021 standard sets requirements for both manual and electronic stethoscopes under the National Medical Products Administration framework, shaping product testing and conformity documentation for suppliers selling into domestic and export-oriented channels.

Value Chain Analysis

The stethoscope value chain runs from commodity and specialty inputs into multi-step component production, final assembly, and regulated distribution. Key upstream materials include aluminum or stainless steel alloys for chest pieces, medical-grade polymers (PVC or silicone) for tubing, and smaller elastomeric parts for ear tips and seals. For electronic and smart models, suppliers also add MEMS microphones, PCBs, batteries, and Bluetooth or Wi-Fi modules. Manufacturing typically combines metal forming or die-casting and finishing, polymer extrusion and injection molding, and manual or semi-manual assembly (diaphragm fitment, tubing-to-binaural attachment, and acoustic checks), with quality control focused on sound transmission, durability, and biocompatibility.

Downstream, OEMs sell through hospital and clinic procurement channels, group purchasing organizations, e-commerce and retail distributors, and telehealth kit integrators that bundle devices with software access and accessories. The chain remains exposed to polymer and logistics volatility, with plastics cost shocks and availability constraints affecting tubing and accessory economics. For example, 2026 reporting around polypropylene price increases in India highlighted how geopolitics-linked resin inflation can disrupt medical-device plastic components. For smart stethoscopes, value capture increasingly shifts toward software validation, interoperability with EHR and telehealth platforms, cybersecurity maintenance, and recurring accessory sales (such as disposable covers and replacement parts) layered onto hardware distribution.

Competitive Landscape

The stethoscope market features a moderate concentration where 3M Littmann, Eko Health, Thinklabs, and a handful of regional OEMs collectively command an estimated upper-double-digit share. 3M defends its franchise through brand equity, dual-frequency diaphragm patents, and global dealer networks. Eko Health advances cloud-linked smart scopes bolstered by proprietary algorithms; its 2024 Series D injects capital for expanding embedded-software teams and enlarging service footprints in Europe and Asia. Thinklabs targets audiology-grade amplification niches valued by neurologists and ICU physicians.

Competitive tension heightens as handheld ultrasound manufacturers—Butterfly Network, GE Vscan—court the same frontline clinicians. Ultrasound portables offer visual affirmation of murmurs, positioning them as premium alternatives rather than outright substitutes due to higher cost and training complexity. Manufacturers respond by integrating ECG leads, broader frequency microphones, and infection-control accessories into next-generation stethoscopes, expanding functionality without significant workflow change.

Supply-chain resilience now determines fleet-replacement bids within large health systems. The FDA’s Office of Supply Chain Resilience flagged pediatric stethoscope shortages during 2024, prompting group purchasing organizations to seek multiregional component sources. Vendors with vertically integrated tubing, diaphragm, and PCB production absorb disruptions better, giving them leverage in three-year framework agreements. Cybersecurity mandates on connected devices add compliance costs that smaller entrants struggle to meet, nudging the market toward partnerships or acquisitions to pool resources.

Global Stethoscope Industry Leaders

3M

GF HEALTH PRODUCTS, INC

American Diagnostic Corporation

ICU Medical, Inc.

Baxter (Hill-Rom)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The clearest opportunity is clinically validated, AI-enabled auscultation that fits primary care workflows and supports earlier cardiopulmonary triage without changing the physical exam paradigm. Real-world evidence and regulatory activity have moved closer together: Eko Healths TRICORDER study published in The Lancet in January 2026 reported higher detection in primary care settings when AI-enabled stethoscopes were used, and multiple FDA 510(k) clearances in 2025-2026 (including Tyto Care for Tyto Stethoscope (G3), Ai Health Highway India Pvt., Ltd. for AiSteth, and Csd Labs for eMurmur Heart AI) indicate expanding scope for digital devices and associated software. A Predetermined Change Control Plan authorization for AI/SaMD updates (eMurmur Heart AI, December 2025) also creates operational room for suppliers to maintain and refine algorithms while staying aligned to FDA expectations for change management.

A second whitespace area is decentralized care packaging, where payers, home-health agencies, and telehealth providers procure connected stethoscopes as part of remote monitoring kits and virtual-visit workflows. The market is also making room for condition-focused algorithms (heart failure, atrial fibrillation, valvular disease), and for approaches that reduce adoption friction through noise reduction, training support, and simpler EHR connectivity. At the same time, competitive pressure from handheld ultrasound in high-acuity settings raises the bar for differentiated clinical use cases and total cost of ownership, favoring vendors that pair hardware reliability with compliant data handling, cybersecurity upkeep, and accessory ecosystems for infection control.

Recent Industry Developments

- May 2026: Ai Health Highway India Pvt., Ltd. received FDA 510(k) clearance (K252915) for the AiSteth dual-mode electronic stethoscope. The clearance expands the pool of regulated digital auscultation options for hospitals, primary care, and telehealth workflows and increases competitive pressure on incumbent smart and electronic stethoscope suppliers.

- December 2025: Csd Labs received FDA 510(k) clearance (K252284) for eMurmur Heart AI, including authorization for a Predetermined Change Control Plan to manage certain AI software updates. This supports a more structured pathway for iterative SaMD improvements in auscultation products, strengthening the case for vendors investing in ongoing model maintenance and clinical performance management.

- April 2024: The US FDA cleared Eko Healths low ejection fraction algorithm, validating a regulated approach to AI-assisted screening during routine vitals collection. The decision elevated clinician confidence in smart auscultation and reinforced outcomes-driven differentiation beyond hardware acoustics alone.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from stethoscopes used for clinical auscultation and routine patient assessment across healthcare settings. It includes acoustic models and electronic or smart variants sold through formal medical channels, measured in current USD at the manufacturer and distributor level.

Scope exclusions: We exclude toy or novelty items, unrelated standalone sensors that are not sold as stethoscopes, and used or refurbished device resale values.

Segmentation Overview

- By Type

- Acoustic / Manual Stethoscopes

- Electronic Stethoscopes

- Smart / AI-Enabled Stethoscopes

- Teaching & Training Stethoscopes

- Veterinary Stethoscopes

- By End User

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Home Healthcare

- Tele-health Providers

- Veterinary Practices

- Academic & Training Institutions

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- GCC

- South Africa

- Rest of Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by grounding the demand pool in healthcare delivery and clinical practice patterns, then linking those patterns to device replacement cycles and procurement behavior. We used public sources such as the World Health Organization, World Bank, OECD health statistics, and US CDC health indicators to understand provider density, care utilization, and disease burden that typically drives auscultation volumes.

On the supply and trade side, we reviewed materials from regulators and standards bodies such as the US FDA device databases and ISO publications, along with customs and trade statistics where relevant. Company annual reports, investor decks, and trusted press coverage were used to map product launches and channel mix shifts. Select paid subscriptions for company financials and patent databases helped cross-check active portfolios and the timing of product refreshes. These examples are not exhaustive, and we also referenced other public sources for data collection, validation, and clarification during the analysis.

Primary Interviews and Surveys

Primary work was used to validate what a typical purchase looks like, how often devices are replaced, and how pricing differs by acoustic versus electronic products. We spoke with a mix of manufacturers, distributors, hospital procurement teams, clinicians, and biomedical staff across major regions, so assumptions could be adjusted where practice patterns and budgets differ.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 14% | APAC: 50% |

| Mid tier: 54% | Functional/Unit leaders: 39% | EMEA: 31% |

| Smaller Players: 17% | Managers: 47% | Americas: 19% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where healthcare staffing and visit volumes are converted into an addressable user base, and then reconciled with typical device ownership and replacement behavior. In practice, we start with indicators such as the number of physicians and nurses, hospital and clinic counts, outpatient visits, and procedure volumes that commonly require cardiovascular and respiratory checks. These are then paired with stethoscope-to-clinician ratios, replacement cycles, and the mix of acoustic versus electronic purchases, which yields the main demand estimate.

After that structure is in place, results are corroborated with selective bottom-up approximations based on supplier and channel checks, along with sampled price points by product type and region. Where direct volumes are hard to observe, gaps are handled through conservative proxy rules, like using procurement cycle norms for public hospitals and applying smaller ownership assumptions in lower resource settings. For forecasting, scenario analysis was used to reflect different adoption paths for electronic models, and the short-term trajectory was cross-checked with exponential smoothing on historical healthcare spending and staffing series discussed in interviews.

Data Validation & Update Cycle

Validation is done by checking the model outputs against independent signals, such as healthcare workforce growth, hospital expansion activity, and observed pricing bands across channels. When a region shows a sharp change, the underlying drivers are re-checked, and outliers are reviewed in a separate analyst pass before internal sign-off.

The study is refreshed annually, and interim updates are triggered when material events occur, such as major regulatory shifts, supply disruptions, or meaningful pricing changes. Before delivery, we run a final update sweep so the numbers reflect the latest public data releases and any fresh interview feedback.

Mordor Intelligence's Stethoscope Market Size Compared Against Other Published Estimates

Published market sizes for stethoscopes can differ even when they look close, because the scope line is not always drawn in the same place and the pricing logic can be handled differently. Differences also come from the year chosen as the starting point, how inflation and currency conversion are treated, and how quickly assumptions are refreshed.

By tracking replacement-cycle inputs and channel-level price bands, Mordor Intelligence keeps the stethoscope market model tied to clinician ownership needs and separates device revenue from adjacent monitoring hardware that is sometimes bundled into broader estimates. A second driver is time framing, where some sources anchor their sizing in 2024 and project faster electronic adoption, while our baseline year and product mix assumptions follow the report scope and are re-checked with current procurement behavior.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 692.16 M (2026) | |

| Global Consultancy A | USD 671.08 M (2024) | Uses a different base year and a faster implied mix shift toward digital models, which can lift near-term revenue when pricing is averaged at a higher share of electronic units. |

| Industry Publisher B | USD 673.20 M (2024) | Anchors the market in 2024 and extends a longer forecast window, which can amplify growth assumptions around smart stethoscope adoption and pricing progression by channel. |

Overall, the spread is explained less by arithmetic and more by what is counted, when it is counted, and how product mix and pricing are advanced year to year. Our approach stays traceable to clear demand indicators, practical replacement behavior, and simple checks that can be repeated as new public data and interview inputs become available.

Key Questions Answered in the Report

What is the current Global Stethoscope Market size?

The stethoscope market stands at USD 692.16 million in 2026 and is projected to reach USD 855.33 million by 2031 at a 4.32% CAGR

Who are the key players in Global Stethoscope Market?

3M, GF HEALTH PRODUCTS, INC, American Diagnostic Corporation, ICU Medical, Inc. and Baxter (Hill-Rom) are the major companies operating in the Global Stethoscope Market.

Which is the fastest growing region in Global Stethoscope Market?

Asia-Pacific delivers the fastest 5.49% CAGR as China, India, and Indonesia expand primary-care capacity and adopt telehealth policies that favor connected diagnostic tools.

How does handheld ultrasound affect stethoscope demand?

Handheld ultrasound captures a share of diagnostic workflows—particularly in emergency care—yet higher cost, training needs, and battery dependence prevent complete substitution.

How does handheld ultrasound affect stethoscope demand?

Handheld ultrasound captures a share of diagnostic workflows—particularly in emergency care—yet higher cost, training needs, and battery dependence prevent complete substitution.

Page last updated on: