Disposable Endoscope Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

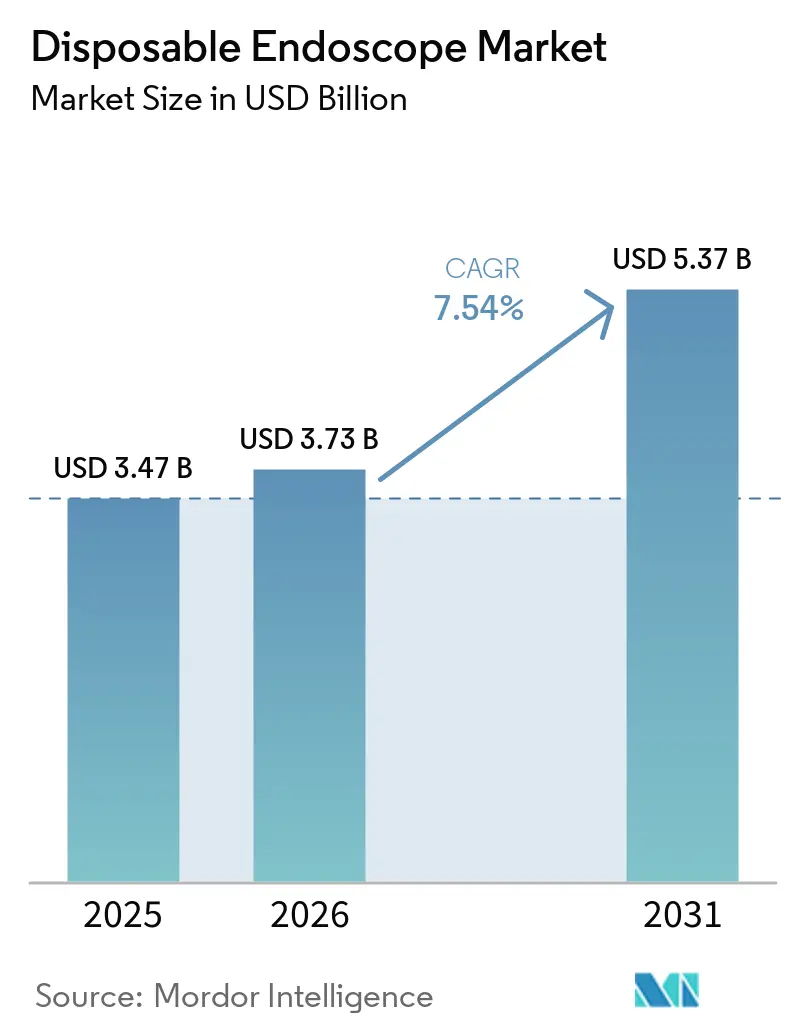

| Market Size (2026) | USD 3.73 Billion |

| Market Size (2031) | USD 5.37 Billion |

| Growth Rate (2026 - 2031) | 7.54% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Disposable Endoscope Market Analysis by Mordor Intelligence

The disposable endoscopes market size in 2026 is estimated at USD 3.73 billion, growing from 2025 value of USD 3.47 billion with 2031 projections showing USD 5.37 billion, growing at 7.54% CAGR over 2026-2031. Over the forecast horizon, declining CMOS sensor costs, clearer U.S. reimbursement codes, and rigorous reprocessing standards are tipping hospital purchasing teams toward single-use technology, positioning the disposable endoscopes market to outpace the broader flexible endoscopy field. Hospitals view disposables as a fast route to infection-risk mitigation, workflow simplification, and labor reallocation, while suppliers gain from scale-driven cost reductions that now outweigh plastic-resin volatility. Accelerated uptake in bronchoscopy, laryngoscopy, and ureteroscopy—especially inside intensive-care and ambulatory settings—underscores the transition of single-use scopes from niche infection-control solutions to mainstream workflow enablers. As duodenoscopes enter clinical practice because of ERCP cross-contamination concerns, the disposable endoscopes market is expected to experience an additional growth inflection, broadening revenue streams for manufacturers.

Key Report Takeaways

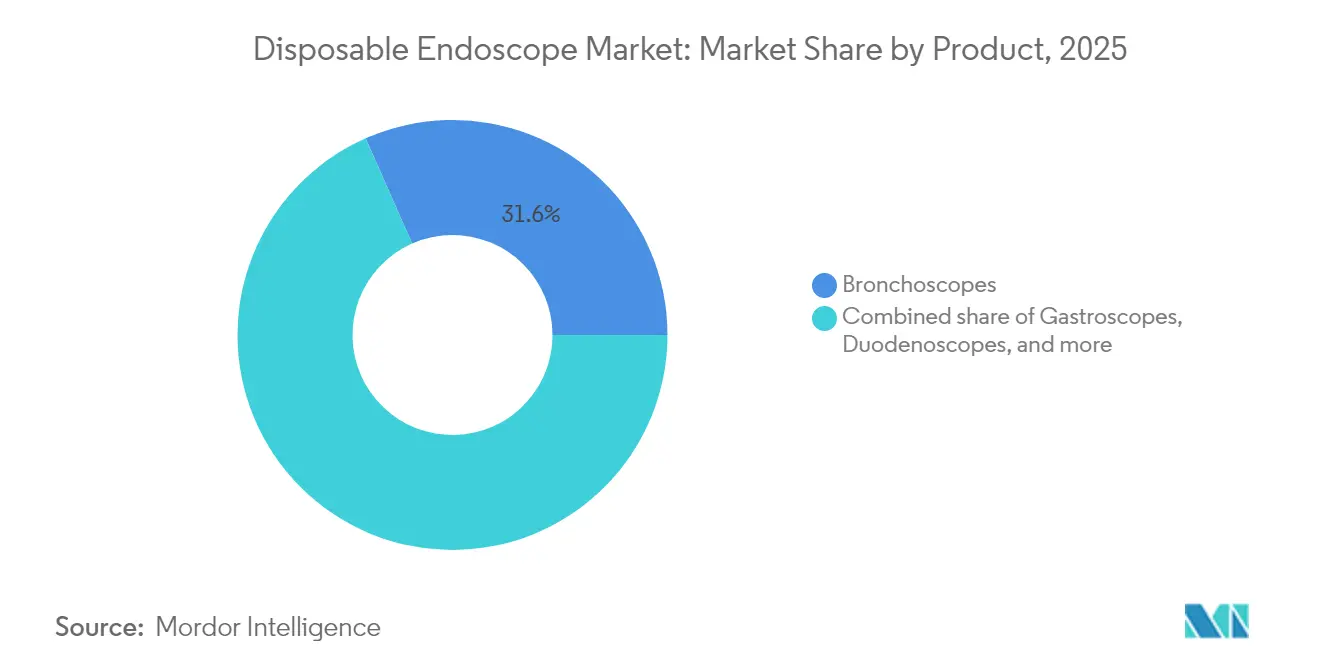

- By product, bronchoscopes led with 31.62% of the disposable endoscopes market share in 2025; duodenoscopes are forecast to advance at a 9.28% CAGR through 2031.

- By application, gastroenterology accounted for 39.85% of the disposable endoscopes market size in 2025, while pulmonology shows the highest projected CAGR of 8.95% to 2031.

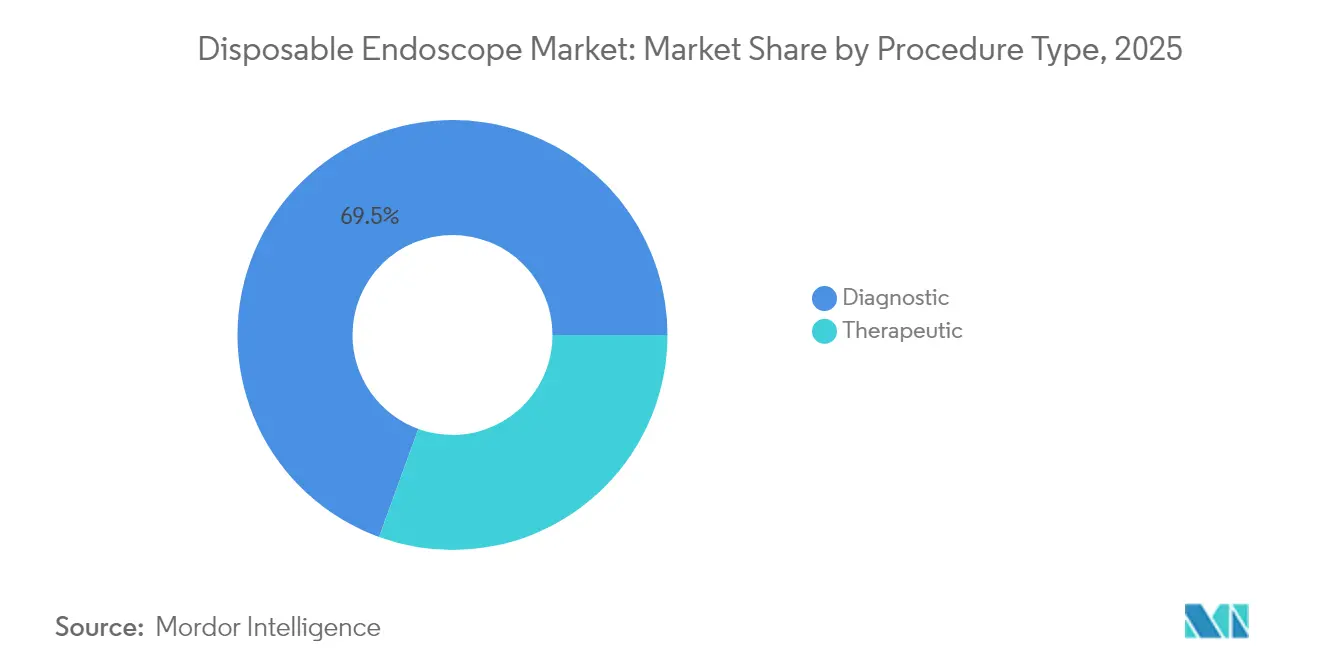

- By procedure, diagnostic work captured the largest volume and is on a 6.92% CAGR trajectory; therapeutic work is the fastest riser as channel-diameter solutions emerge.

- By end user, hospitals held 69.88% of the disposable endoscopes market in 2025, whereas ambulatory surgical centers post the strongest growth outlook of 9,82% on the back of Category III CPT code adoption.

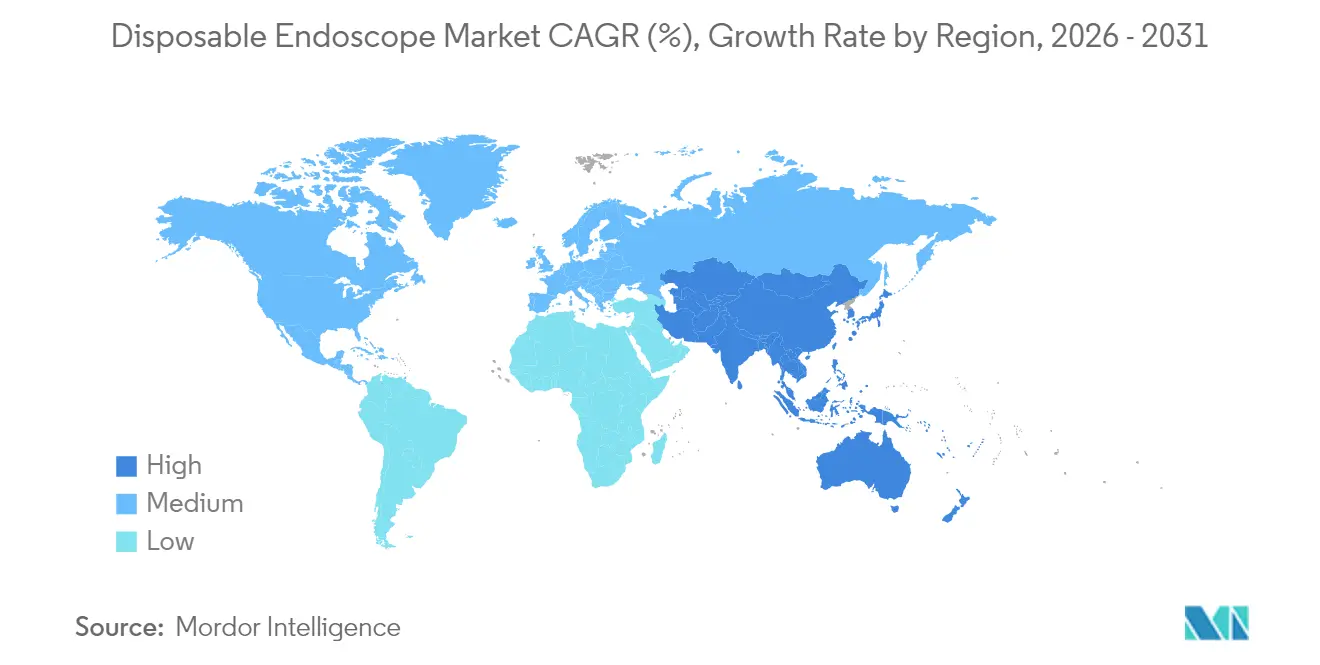

- By geography, North America took 44.92% of the disposable endoscopes market size in 2025, and Asia Pacific is set to grow at an 8.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Disposable Endoscope Market Trends and Insights

Drivers Impact Analysis*

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CMOS imaging sensors at cost parity | +1.4% | Global | Medium term (2-4 years) |

| Joint Commission real-time disinfection tracking | +1.1% | United States, Canada | Short term (≤ 2 years) |

| AMA Category III CPT codes | +1.2% | United States | Short term (≤ 2 years) |

| Sustained ICU bronchoscopy demand | +0.9% | Global | Medium term (2-4 years) |

| Shift toward “Green OR” initiatives driving adoption of fully recyclable polymer scopes | +0.6% | Nordics | Medium term (2-4 years) |

| Chinese volume-based procurement (VBP) policy favoring domestic disposable brands | +0.8% | China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Technological Break-Even of Single-Use CMOS Imaging Sensors

Low-cost CMOS modules now deliver diagnostic-grade resolution at a production cost 35.0% lower than in 2022, enabling community hospitals to replace reusable towers with plug-and-play disposables. Firmware upgrades performed at the factory eliminate console downtime and push procurement teams to evaluate scopes on annual pixel gains, a shift mirroring consumer-electronics replacement cycles. As a result, the disposable endoscopes market is widening beyond tertiary centers, with rural facilities adopting single-use models that remove reprocessing bottlenecks and avoid capital outlays on washers.

Implementation of Accelerated Hospital Accreditation Standards

Revised Joint Commission rules introduced in 2024 mandate real-time tracking of every high-level disinfection cycle, forcing mid-size endoscopy suites to invest over USD 50,000 in compliance hardware[1]Joint Commission, “Device Cleaning and Infection Control Standards 2024,” jointcommission.org. The capital strain has shortened the payback period on single-use scopes to as little as 12 months in high-volume centers, convincing finance committees that disposables solve both infection-control gaps and escalating labor costs. By redeploying sterile-processing staff to patient-facing roles, hospitals align spending with value-based-care objectives and boost clinical availability.

Increased Demand for Bronchoscopy in ICU Settings Post-COVID

Bronchoscopy volumes in ICUs remain elevated because clinicians rely on direct visualization to manage pneumonia and secretion clearance. Immediate availability and zero turnaround time have steered 32% of 2024 disposable endoscopes market revenue toward single-use bronchoscopes. Hospitals purchasing compact, screen-based trolleys instead of traditional towers amplify equipment utilization, supporting higher bed occupancy without scheduling conflicts.

Reimbursement Code Expansion for Category III Single-Use Endoscopes

Dedicated CPT codes for single-use scopes launched in 2023 resolve payment ambiguity and improve outpatient margins by up to 20%[2]American Medical Association, “CPT® Category III Codes for Single-Use Endoscopes,” ama-assn.org. Ambulatory surgery centers quickly adopted the codes, and specialist clinics now include them in patient cost estimators, solidifying a permanent financing pathway. The clear reimbursement picture fuels investment in day-surgery roll-ups that standardize disposable workflows.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High per-case cost in low-volume hospitals | −0.7% | Global | Medium term (2-4 years) |

| Restricted lumen size for advanced therapy | −0.9% | Global | Long term (≥ 4 years) |

| Evolving EU Medical-Device Regulation (MDR) raising time-to-market for new SKUs | −0.6% | European Union | Medium term (2-4 years) |

| Clinical evidence gaps on image quality vs. reusable HD scopes among ENT surgeons | −0.5% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Uncertain Cost-Benefit Equation for Low-Volume Community Hospitals

Facilities performing under 500 procedures per year face 20% higher per-case costs when moving to disposables because their existing reprocessing rooms stand under-utilized. Many adopt hybrid fleets, reserving disposables for high-risk ERCP or ICU bronchoscopy while retaining reusable colonoscopes for routine screenings. The dual-inventory model complicates waste audits and purchasing but allows administrators to reconcile infection-control imperatives with budget realities.

Restricted Lumen Size Limits Advanced Therapeutic Interventions

Most single-use duodenoscopes carry 1.2 mm working channels, too narrow for accessories used in complex stone retrievals. Therapeutic gastroenterologists thus depend on reusable platforms that support 2.0 mm devices. Vendors testing variable-bore designs face higher material costs, putting near-term revenue emphasis on diagnostic disposables and leaving therapeutic-grade launches as a future growth lever.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Bronchoscopes Dominate While Duodenoscopes Accelerate

Bronchoscopes generated 31.62% of the disposable endoscopes market share in 2025, underpinning the segment’s leadership with their slim profiles that navigate distal bronchi without compromising image fidelity. Teaching hospitals favor single-use bronchoscopes as training devices because scheduling conflicts linked to shared equipment vanish, improving educational throughput. Elevated ventilator-associated pneumonia surveillance sustains procedural volume, and combined with predictable per-case costs, cements the disposable endoscopes market size for bronchoscopes on a solid growth path. Suppliers respond by bundling screens, trolleys, and cloud storage, shrinking the operational footprint in crowded ICUs.

Duodenoscopes remain a smaller slice of revenue but are projected to post a >9% CAGR to 2031 as elevator-contamination worries push ERCP suites to adopt premium-priced single-use scopes. Manufacturers now ship disposable elevators that satisfy FDA guidelines, and procurement teams see cost offsets from canceled maintenance contracts. Pilot projects in tertiary centers demonstrate scheduling gains because reprocessing backlogs disappear, encouraging regional hubs to follow once accessory compatibility widens.

By Application Type: Gastroenterology Leads and Pulmonology Races Ahead

Gastroenterology commanded 39.85% of the disposable endoscopes market size in 2025, driven by cross-contamination fears in ERCP and rising single-use adoption for outpatient colonoscopies. GI suites report fewer reprocessing delays, enabling denser scheduling that attracts patients in high-deductible insurance markets. The resulting operational efficiencies, paired with the availability of therapeutic channel expansion roadmaps, keep suppliers focused on developing GI-specific innovations.

Pulmonology shows the fastest growth because sustained bronchoscopy volumes for pneumonia diagnostics and lung-cancer staging fit well with disposable scope attributes. Clinicians cite reduced downtime and lower contamination risk during transbronchial needle aspiration as decisive factors. Hospitals integrate single-use bronchoscopy into quality-improvement metrics, boosting same-day biopsy rates and driving complementary demand for disposable retrieval baskets that match narrow channels.

By Procedure Type: Diagnostics Rule but Therapeutics Offer Upside

Diagnostic procedures are forecast to expand at a 6.92% CAGR from 2026 to 2031. Their straightforward imaging requirements align with the cost-optimized design of disposable scopes, allowing vendors to mass-produce without complex channel architecture. Administrators appreciate simplified tray setups that cut room-turnover time, especially in facilities facing nurse shortages.

Therapeutic procedures remain a smaller revenue contributor yet present a strategic growth pocket. Emerging single-use prototypes accepting 1.8 mm accessories hint at a future shift where reimbursement-rich ERCP, polypectomy, and ureteric stone extraction migrate to disposable platforms. Success would not only lift unit prices but also create aftermarket pull for compatible accessories, increasing lifetime account value.

By End User: Hospitals Remain Core, ASCs Surge

Hospitals held a commanding 69.88% share of the disposable endoscopes market in 2025. Teaching institutions value disposables for standardizing resident training, and hospitals pursuing Magnet or similar designations embed single-use metrics into infection-prevention dashboards. Public reporting of scope-related infections has dropped, reinforcing the perception that disposables are a rapid path to quality gains.

Ambulatory surgical centers (ASCs) post the highest growth outlook. Category III CPT codes remove revenue uncertainty, and ASCs leverage zero-reprocessing footprints to repurpose space into additional procedure bays. Predictable per-case pricing aligns with private-equity roll-up models, encouraging wider adoption and drawing procedures out of inpatient settings—fueling unit-volume gains for manufacturers.

Geography Analysis

North America led the disposable endoscopes market with a 44.92% share in 2025. U.S. integrated delivery networks consolidate purchasing and negotiate volume rebates, while Joint Commission and CMS regulations elevate infection prevention to board-level priorities. Many hospitals defer washer-disinfector replacement once annual service costs exceed lease thresholds, channeling funds into single-use conversion programs. Canada follows a similar clinical rationale but relies on provincial technology grants that lengthen procurement cycles. The FDA’s 510(k) clearance pathway for single-use ureteroscopes like Olympus RenaFlex in 2024 gives clinical teams regulatory confidence.

Asia Pacific posts the highest regional CAGR at 8.61%. China’s provincial tenders include disposable scopes to meet infection-control targets under National Health Commission directives, favoring local manufacturers who avoid import duties. Private hospital chains in India advertise zero reprocessing backlogs as a differentiation lever, and cloud-connected processors streamline tele-mentoring for complex GI cases. Japan applies a selective approach, balancing its domestic reusable manufacturing dominance with the clinical benefits of disposables. South Korean firms such as Hunan Vathin trigger price competition that expands unit volumes despite margin compression, while Australia mandates carbon-accounting disclosures that recognize the lifecycle burden of chemical disinfectants. Europe shows fragmented adoption patterns. Nordic countries top per-capita usage, leveraging “Green OR” directives that prioritize carbon lifecycle metrics; scope recycling logistics now influence tender scores. Germany and France substitute disposables mainly for high-risk ERCP and ICU bronchoscopy, extending reusable fleets elsewhere to protect capital budgets. The UK’s NHS labels single-use scopes a tool for hitting zero-infection targets, yet broader adoption awaits budgetary alignment. Southern and Eastern Europe implement hybrid fleets: disposables for therapeutic ERCP, reusables for mass colonoscopy screenings. EU Medical Device Regulation costs strain small suppliers, potentially narrowing brand diversity and prompting hospital groups to lock multi-year deals with incumbent global vendors.

Competitive Landscape

The disposable endoscopes market is shifting from early fragmentation toward consolidation. Olympus and Boston Scientific leverage their installed imaging platforms, offering single-use scopes bundled with familiar processors to reduce switching friction. Ambu counters with image-enhancement software designed to operate independently of legacy towers, appealing to new buyers and dissatisfied incumbents. As 1080p image parity approaches, competition pivots to channel diameter, ergonomic handles, and integrated data capture.

Therapeutic-grade models with wider working channels represent a hotly contested niche. 3NT Medical focuses on ENT subspecialties, proving that tailored designs can win loyalty in underserved domains. Chinese manufacturers such as Micro-Tech Endoscopy and Hunan Vathin compete on price but trail in premium imaging, creating a two-tier global market. Alliances between scope makers and accessory firms—such as Boston Scientific’s acquisition of optics start-ups—signal that accessory interoperability will determine future procurement, echoing printer-and-toner business models.

Business models evolve as vendors launch subscription packages bundling scopes, transport containers, and recycling logistics into a single monthly fee. The arrangement converts episodic capital purchases into predictable income streams, mirroring software-as-a-service economics. Hospitals benefit from simpler budgeting and integrated end-of-life management, while suppliers lock in long-term loyalty and collect usage data to refine production forecasts. Vendors embedding traceability into electronic health records gain a data-driven edge that transcends hardware.

Disposable Endoscope Industry Leaders

Ambu A/S

Olympus Corp.

Boston Scientific Corp.

Fujifilm Holdings Corp.

Pentax Medical (HOYA)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: MEDNOVA unveiled a single-use bronchoscopy and ureteroscopy portfolio featuring cost-controlled CMOS modules and bundled service contracts to meet per-case budgeting demands.

- May 2024: Olympus introduced a portable monitor tailored for disposable bronchoscopy and ENT scopes, enabling multiple rooms to share a single video platform while maintaining image fidelity.

- April 2024: Olympus received U.S. FDA 510(k) clearance for RenaFlex, its first single-use flexible ureteroscope system, expanding its disposable lineup.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the disposable endoscope market as the global demand, in dollar terms, for factory-sterilized, single-patient flexible or rigid scopes used across diagnostic and therapeutic procedures in gastroenterology, pulmonology, urology, orthopedics, gynecology, and emergency medicine.

Scope exclusion: reusable endoscopes, rental programs, and standalone visualization towers are outside this assessment.

Segmentation Overview

- By Product

- Gastroscopes

- Bronchoscopes

- Duodenoscopes

- Laryngoscopes

- Colonoscopes

- Ureteroscopes

- Other Endoscopes

- By Application Type

- Gastroenterology

- Pulmonology

- Urology

- ENT

- Other Application Types

- By Procedure Type

- Diagnostic

- Therapeutic

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle-East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed procurement managers in high-volume hospitals, pulmonologists using single-use bronchoscopes, and EU market regulators.

Follow-up surveys with distributors in Asia and Latin America clarified price corridors, pre-tax margins, and replacement cycles, which strengthened or corrected initial desk assumptions.

Desk Research

We began with publicly available datasets such as WHO procedure volumes, OECD Health Statistics, and regional infection-control guidelines. Then, we layered in customs shipment codes for HS 901890 and Eurostat export files to gauge unit flows.

Device approval databases from the US FDA and EU MDR helped us track product introductions, while hospital procurement dashboards released by NHS Supply Chain and Vizient informed typical purchase prices.

Paid databases like D&B Hoovers and Dow Jones Factiva supplied hard revenue clues that triangulated company-level performance.

These sources are illustrative, not exhaustive, and many additional references were reviewed during validation.

Market-Sizing & Forecasting

We applied a top-down reconstruction that links national procedure counts to weighted penetration rates for single-use devices, which are then multiplied by verified average selling prices.

Select bottom-up checks, such as supplier revenue roll-ups and channel inventory audits, were used to fine-tune totals.

Key variables inside our model include 1) annual bronchoscopy and ERCP volumes, 2) infection-related readmission penalties, 3) average per-procedure reimbursement under CPT 31622-31624, and 4) CMOS sensor price trends.

Multivariate regression against these drivers produced the 2025-2030 forecast after scenario analysis for policy shifts.

Data gaps, like missing ASPs in smaller economies, were bridged with normalized regional mark-ups validated by distributors.

Data Validation & Update Cycle

Outputs pass two analyst reviews, variance checks against historical ratios, and a senior audit round before release.

Reports refresh every twelve months, with interim updates if recalls, major approvals, or reimbursement code revisions change demand fundamentals.

Why Our Disposable Endoscope Baseline Stands Out

Published figures vary because firms pick different device lists, price types, and update speeds.

We anchor our baseline on clearly disclosed scope, live procedure metrics, and yearly refreshes.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.47 B (2025) | Mordor Intelligence | - |

| USD 1.90 B (2024) | Global Consultancy A | Excludes urology and orthopedic use cases, relies on shipment quantities only |

| USD 2.29 B (2024) | Industry Portal B | Uses list prices without regional discounting; last refresh mid-2024 |

| USD 2.58 B (2025) | Research Firm C | Forecast built solely on company press releases, limited primary validation |

Estimates that omit high-growth specialties or ignore negotiated ASP erosion understate the market, while list-price models inflate value. By blending live hospital interviews with granular trade and reimbursement data, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can trace and replicate with confidence.

Key Questions Answered in the Report

What is the projected value of the disposable endoscopes market by 2031?

The disposable endoscopes market is expected to reach USD 5.37 billion by 2031, reflecting a 7.54% CAGR from 2026.

Which product dominates disposable endoscope sales today?

Single-use bronchoscopes lead with 31.62% of 2025 revenue because their immediate availability suits ICU airflow management.

Why are ambulatory surgical centers adopting single-use scopes rapidly?

Dedicated Category III CPT codes and the absence of reprocessing rooms let centers cut overhead and secure predictable per-case margins.

What is the main restraint on therapeutic-grade disposable scopes?

Current 1.2 mm working-channel limits restrict advanced interventions, keeping many ERCP and stone-retrieval procedures on reusable platforms.

Which region shows the fastest growth outlook?

Asia Pacific posts an 8.61% CAGR through 2031, driven by new hospital builds that embed single-use technology from the ground up.

How are vendors adapting their business models?

Companies increasingly roll out subscription bundles that cover scopes, transport trays, and recycling logistics under one monthly fee, turning capital sales into recurring income.

Page last updated on: