Otoscope Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

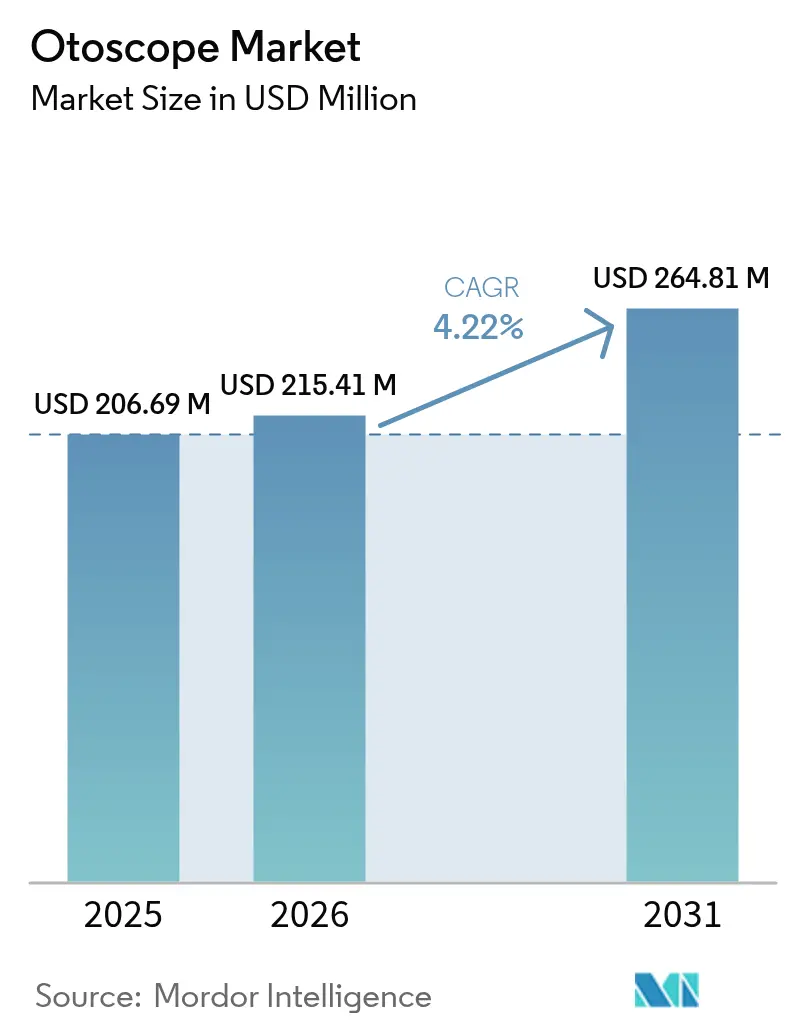

| Market Size (2026) | USD 215.41 Million |

| Market Size (2031) | USD 264.81 Million |

| Growth Rate (2026 - 2031) | 4.22% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Otoscope Market Analysis by Mordor Intelligence

The otoscope market size was valued at USD 206.69 million in 2025 and estimated to grow from USD 215.41 million in 2026 to reach USD 264.81 million by 2031, at a CAGR of 4.22% during the forecast period (2026-2031). Expansion is supported by digital imaging upgrades, smartphone connectivity, and artificial intelligence (AI) algorithms that boost acute otitis media detection sensitivity to 93.8% and specificity to 93.5%. Product innovation remains brisk, as shown by OtoNexus Medical Technologies’ ultrasound otoscope entering the United States Food and Drug Administration (FDA) Safer Technologies Program (STeP) in 2024-2025, a step that validates non-invasive differentiation of bacterial from viral middle-ear infections.[1]OtoNexus Medical Technologies, “Ultrasound Otoscope Receives STeP Selection,” otonexus.com Consumer demand follows suit: the Anykit digital otoscope with a 4.5-inch high-definition screen and gyroscope adds professional-grade imaging to at-home monitoring, reinforcing a shift toward self-managed ear health. Macro fundamentals amplify the opportunity. India’s medical-device sector, valued at USD 11 billion in 2025, is projected to quintuple by the decade’s close, fueled by a USD 400 million production-linked-incentive plan and state-level medical-device parks. Meanwhile, an aging global population increases the prevalence of hearing disorders, placing sustained diagnostic demand on the otoscope market.

Key Report Takeaways

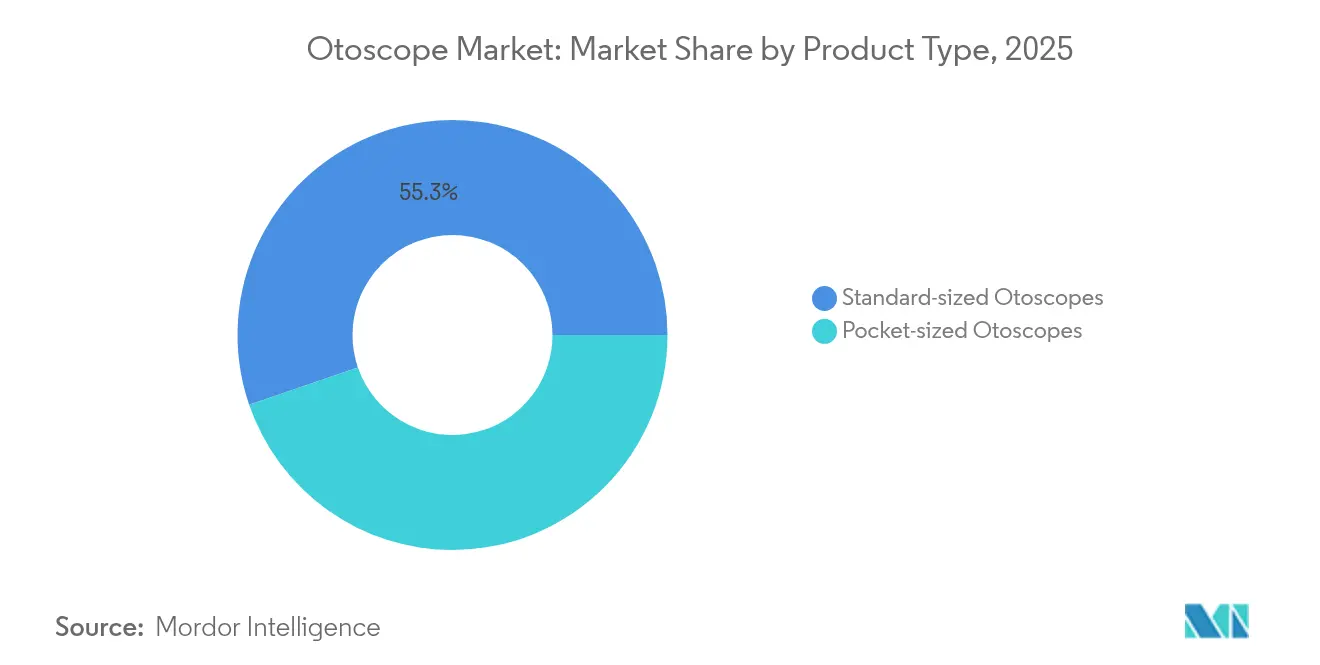

- By product type, standard-sized devices led with a 55.26% otoscope market share in 2025, while pocket variants are projected to expand at a 5.09% CAGR to 2031.

- By portability, portable units controlled 72.12% of the otoscope market size in 2025 and will grow fastest at 5.36% through 2031.

- By power source, mains-powered models held 52.88% of the otoscope market share in 2025; battery units post the quickest 4.98% CAGR over 2026-2031.

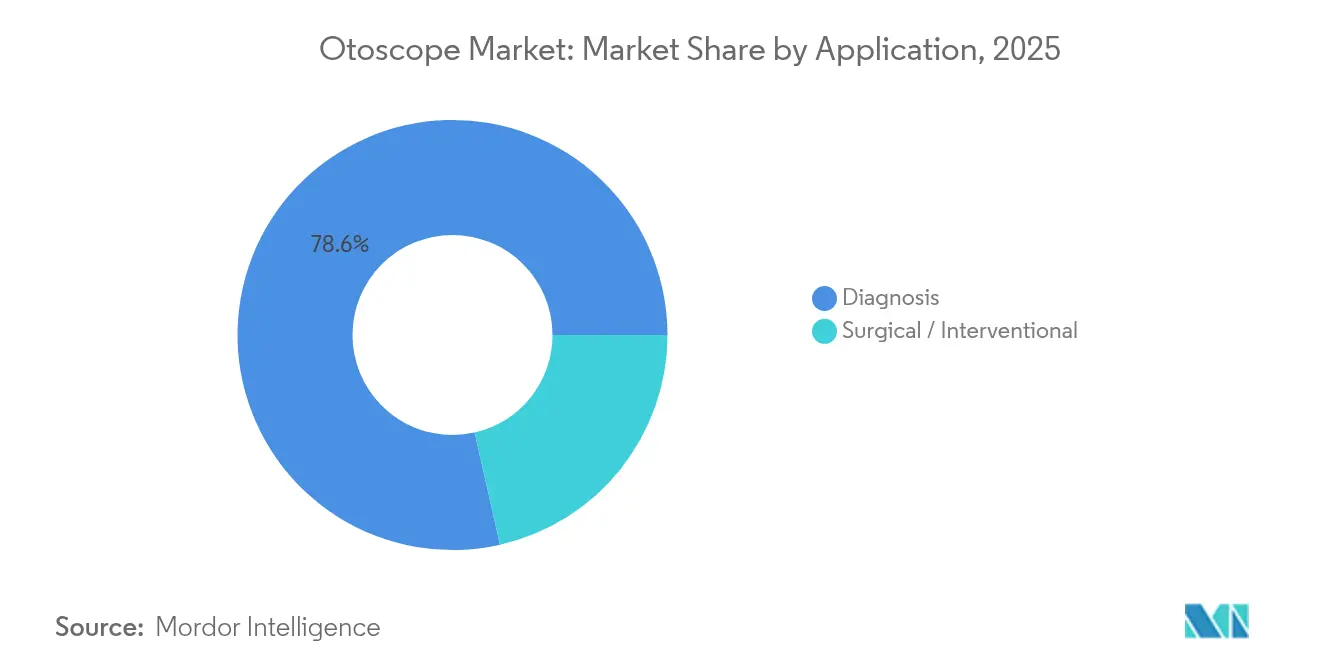

- By application, diagnostic use accounted for 78.55% of the otoscope market size in 2025, whereas the surgical segment will register a 5.49% CAGR to 2031.

- By end user, hospitals captured 62.08% of the otoscope market share in 2025, yet ENT clinics are forecast to advance at 4.72% CAGR.

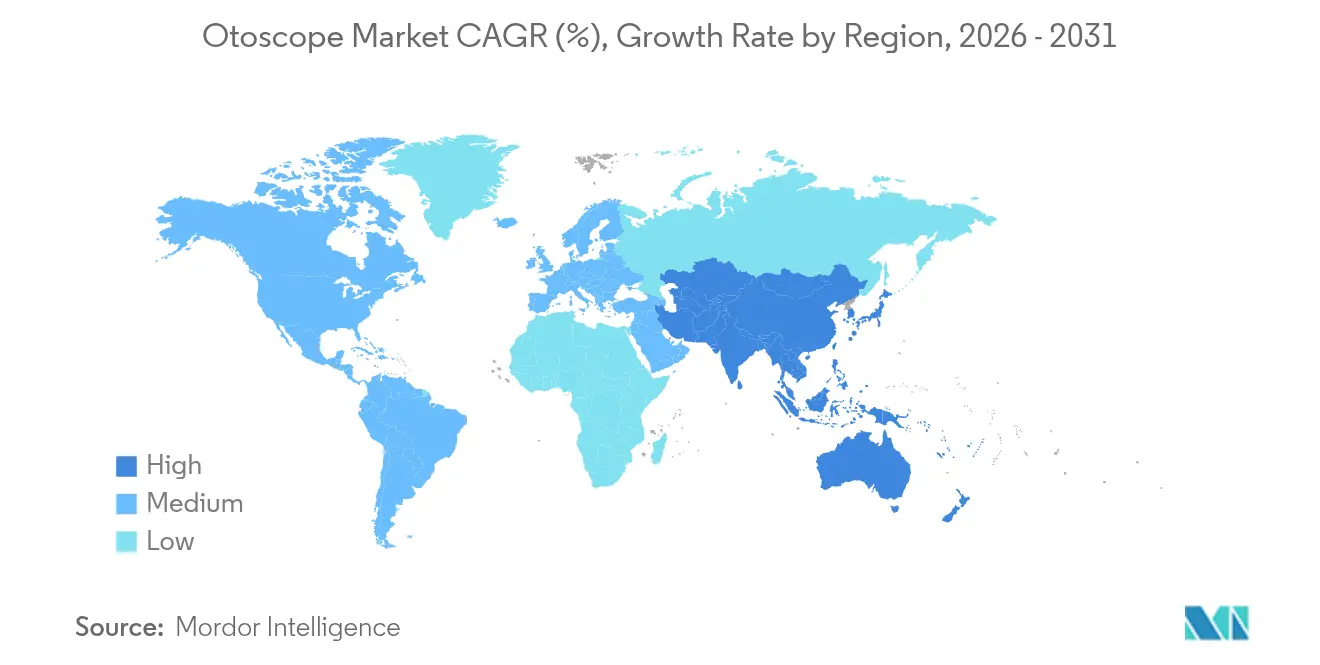

- By geography, North America dominated with 37.15% revenue share in 2025; Asia-Pacific exhibits a 5.92% CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Otoscope Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of ENT-related diseases | +1.2% | Global, higher in Asia-Pacific and Sub-Saharan Africa | Medium term (2-4 years) |

| Technological advancement in digital & video otoscopes | +1.5% | North America and Europe lead; Asia-Pacific rapid adoption | Short term (≤ 2 years) |

| Rising geriatric population-linked hearing disorders | +0.8% | Worldwide, with emphasis on North America, Europe, developed Asia-Pacific | Long term (≥ 4 years) |

| Expanding healthcare expenditure in emerging economies | +1.1% | Core in Asia-Pacific; spill-over to Middle East & Africa and Latin America | Medium term (2-4 years) |

| Tele-otoscopy adoption in primary care & remote triage | +0.9% | North America and Europe, expanding to rural Asia-Pacific | Short term (≤ 2 years) |

| School-based ear-health screening initiatives | +0.6% | Global, strongest in developing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing burden of ENT-related diseases

More precise otologic imaging reduces unnecessary antibiotic use by 50%, as shown with PhotoniCare’s OtoSight platform.[2]PhotoniCare, “OtoSight Middle Ear Imager Clinical Outcomes,” medicaldevicenews.com Despite pneumococcal conjugate vaccines, otitis media prevalence remains stubborn, spotlighting unmet diagnostic needs. High-definition OTO Endoscopes introduced in 2024 deliver superior visuals for chronic otitis media assessment, enhancing diagnostic accuracy at clinics such as Mallige Hospital. Healthcare authorities now link preventable childhood hearing loss to educational performance, strengthening procurement budgets for advanced otoscopes in underserved districts.

Technological advancement in digital & video otoscopes

Optical coherence tomography (OCT) enables cross-sectional tympanic-membrane imaging via the University of Southern California’s handheld device, revealing pathologies such as myringitis previously hidden from traditional scopes. Deep residual-recurrent neural networks achieve clinician-level classification of acute otitis media, underpinning AI-enhanced otoscope market growth. On the research horizon, terahertz endoscopes under development at Waseda University promise non-invasive cochlear visualization, suggesting a future leap in ear-disease management.

Rising geriatric population-linked hearing disorders

Age-related hearing loss already affects 1.5 billion individuals worldwide. Automated classifiers employing bidirectional long-short-term-memory networks reach 99.33% diagnostic accuracy, offsetting shortages of audiology professionals. Over-the-counter hearing-aid rules that took effect in 2022 have democratized assistive-device access, spurring older adults to seek professional confirmation through otoscopy, directly boosting the otoscope market.

Tele-otoscopy adoption in primary care & remote triage

Telehealth visits in the United States jumped from 1% of encounters pre-pandemic to 17% by 2023. Smartphone-based hearing tests attain 94.3% accuracy for normal hearing detection, validating mobile screening in sparsely staffed environments. Remote patient monitoring reimbursements under the U.S. Centers for Medicare & Medicaid Services (CMS) encourage clinics to fold tele-otoscopy into chronic-care programs, positioning the otoscope market for distributed growth.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Social stigma associated with ENT disorders | –0.4% | Global, stronger in parts of Asia-Pacific and Middle East & Africa | Long term (≥ 4 years) |

| Shortage of skilled ENT professionals in low- and middle-income countries | –0.7% | Sub-Saharan Africa, rural Asia-Pacific, Latin America | Long term (≥ 4 years) |

| Regulatory delays for smartphone-connected devices | –0.3% | Worldwide, varies by regulator | Short term (≤ 2 years) |

| Supply-chain dependence on high-precision optics | –0.5% | Global, cost-sensitive economies most affected | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Social stigma associated with ENT disorders

Cosmetic concerns slow adoption of hearing assistance in traditional societies, despite United States regulatory moves to widen over-the-counter access. Innovative designs like Nuance Audio glasses embed hearing aids into stylish frames, but uptake hinges on public‐awareness campaigns and discreet diagnostic options.

Shortage of skilled ENT professionals in LMICs

Uganda’s recent residency analysis confirmed 76% graduate employment yet highlighted urban concentration.[3]PLOS Global Public Health, “ENT Workforce Distribution in Uganda,” journals.plos.org In India, doctor-to-population ratios trail World Health Organization recommendations, forcing rural clinics to rely on AI-assisted otoscopy. Telehealth eases consultant access but requires digital-literacy training and stable internet infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pocket-Sized Innovation Drives Market Evolution

Standard-sized instruments controlled 55.26% of the otoscope market in 2025, reflecting clinical preference for high-end optics and durable construction. Procurement departments favor these units for high-volume environments, particularly where accessory compatibility and long-term service contracts matter. Nonetheless, pocket designs will outpace at a 5.09% CAGR, supported by primary-care mobility and community health outreach. Portable OCT scopes from the University of Southern California bridge premium imaging with handheld convenience. Smart-phone-linked sub-segments integrate AI to deliver 93.8% diagnostic sensitivity, cutting training curves and broadening access. Supply-chain savings during a period when production costs have risen to about 20% of revenue favor compact material-efficient builds, reinforcing pocket uptake.

By Portability: Mobile Healthcare Transformation Accelerates Growth

Portable models contributed 72.12% of the otoscope market size in 2025 and will also log the fastest 5.36% CAGR. Their twin leadership position signals a structural shift toward distributed care rather than early-cycle penetration. Adoption surged when video-enabled scopes such as OtoSpec allowed real-time patient education. Battery advances narrow performance gaps with wall-mounted systems and trim installation overhead, making portable units the default choice for tele-medicine networks and school screenings.

By Power Source: Battery Technology Drives Independence

Mains-powered devices held 52.88% of the otoscope market share in 2025, reflecting established hospital workflows. Battery-operated variants, however, will widen penetration via a 4.98% CAGR through 2031. Design upgrades featuring lithium-ion packs sustain extended use while minimizing weight, critical for rural outreach vans and emergency departments during grid outages. Cybersecurity concerns also ease with self-contained battery designs that limit network exposure.

By Application: Surgical Applications Emerge as Growth Driver

Diagnostic usage comprised 78.55% of the 2025 otoscope market size, owing to routine ear examinations across care levels. The surgical category, though smaller, leads growth at 5.49% CAGR, propelled by minimally invasive procedures and high-resolution imaging. PhotoniCare’s OtoSight platform cut antibiotic scripts in half by improving intra-operative visualization, demonstrating downstream cost savings. OtoNexus’ ultrasound system, recognized by the FDA’s STeP, illustrates how new modalities expand procedural indications.

By End User: ENT Clinics Gain Momentum Through Specialization

Hospitals amassed 62.08% of otoscope market share in 2025 based on sizable capital budgets and comprehensive ENT services. Nonetheless, ENT clinics exhibit a higher 4.72% CAGR through 2031. Specialist centers leverage agility and tele-otoscopy to reach remote patients, while ambulatory surgery centers use cost-controlled settings to attract outpatient procedures. Integra LifeSciences’ USD 1 billion ENT acquisition underscores the commercial value of clinic-based networks.

Geography Analysis

North America accounted for 37.15% of 2025 revenue, buoyed by insurance coverage, standardized ENT protocols, and expedited U.S. FDA approval pathways that now include a clearer De Novo route for novel otoscopes. Canadian universal coverage embeds otoscopy in primary-care check-ups, whereas Mexico expands device import quotas to modernize public hospitals.

Asia-Pacific posts the swiftest 5.92% CAGR during 2026-2031. China is projected to spend USD 210 billion on medical devices by 2025, spurred by healthy-aging priorities and favorable reimbursement rules. India’s National Medical Devices Policy 2023 and its single-window approval system streamline licensing, though delays noted by a 2025 Parliamentary panel have driven some manufacturers to weigh relocation to Vietnam or Malaysia. Japan’s advanced physician networks, Australia’s universal system, and South Korea’s digital-health incentives round out regional momentum.

Europe sustains mid-single-digit growth despite the stricter Medical Device Regulation (MDR) EU 2017/745, which raises clinical-evidence demands and post-market scrutiny. Germany, United Kingdom, and France lead adoption, while Italy and Spain upgrade ENT suites under health-modernization grants. The European Parliament’s 2025 call for MDR revisions seeks to avoid supply shortages by setting binding conformity-assessment timelines.

Competitive Landscape

The otoscope market remains moderately fragmented. Legacy manufacturers such as Heine Optotechnik, Welch Allyn, and Rudolf Riester defend share via service contracts and global distribution. Digital entrants emphasize AI, smartphone compatibility, and cloud analytics. OtoSpec’s iPhone-ready scope illustrates direct-to-provider sales that bypass hospital tenders. Olympus expanded Latin America distribution in 2024 to capture emerging-market growth, while C2Dx’s acquisition of Cook Medical ENT assets signals niche consolidation.

Academic-industry collaboration represents a pipeline accelerant. The University of Southern California’s OCT partnership and Waseda University’s terahertz research portend new visual modalities. AI developers deploy algorithms with 93.5% specificity, democratizing expert-level assessments without specialist oversight.

Supply-chain resilience shapes strategy. Firms with diversified optics suppliers and regional assembly plants mitigate geopolitical disruptions that drove component costs to 20% of revenue in 2024. This environment favors vertically integrated producers or those using modular designs that accept multiple component vendors.

Otoscope Industry Leaders

Wellch Allyn

American Diagnostic Corporation

Heine Optotechnik GmbH

Rudolf Reister GmbH

Sync Vision

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: PhotoniCare’s OtoSight achieved a 50% antibiotic-prescription reduction through precision diagnostics, strengthening antimicrobial-stewardship goals.

- January 2025: OtoNexus advanced its ultrasound otoscope with electronic-health-record integration while retaining FDA STeP designation.

- August 2024: University of Southern California unveiled a portable OCT otoscope that enhances tympanic-membrane visualization in field clinics.

- February 2024: Mallige Hospital reported improved chronic-otitis-media outcomes after deploying high-definition OTO Endoscope technology.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global otoscope market as the aggregated value of stand-alone devices, standard, pocket, and video models, designed for visual examination of the ear canal and tympanic membrane, whether battery-powered or mains-powered, and sold through medical channels to human health end users. The value is expressed in USD at manufacturer invoice level.

Scope exclusion: integrated imaging towers and smartphone clip-on adapters are not included.

Segmentation Overview

- By Product Type

- Standard-sized Otoscopes

- Pocket-sized Otoscopes

- By Portability

- Portable

- Wall-mounted

- By Power Source

- Battery-operated

- Mains-powered

- By Application

- Diagnosis

- Surgical / Interventional

- By End-User

- Hospitals

- ENT Clinics

- Ambulatory Surgery Centers

- Others

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed ENT surgeons, biomedical engineers, and procurement leads in North America, Europe, and Asia-Pacific. These conversations validated average selling prices, battery replacement cycles, and the rising role of video otoscopes in tele-consults, filling gaps that secondary sources could not cover and anchoring assumptions before final modeling.

Desk Research

We began with public datasets that map the clinical need for ear examinations, such as WHO Global Health Observatory procedure counts, CDC outpatient otitis media visit rates, and Eurostat day-case ENT volumes. Trade flows for HS code 901890 across UN Comtrade and national customs portals helped size cross-border supply. Device clearance files on the US FDA 510(k) database, CE-marked product registries, and clinical trial repositories clarified competitive availability and feature adoption. Company 10-Ks, investor decks, and procurement disclosures of hospital groups gave price corridors, while articles in journals like Otolaryngology-Head and Neck Surgery detailed usage frequency. Paid resources, D&B Hoovers for manufacturer revenue splits and Questel for patent velocity, offered additional triangulation. The sources listed here are illustrative; many other documents were reviewed to corroborate and refine the dataset.

Market-Sizing & Forecasting

A top-down construct converts national ENT visit pools into addressable device demand using utilization factors and average unit life. Bottom-up spot checks, supplier shipment tallies and sampled ASP × volume from channel partners, are layered in to cross-verify totals. Key variables include outpatient ENT visit growth, otitis media incidence, hospital bed expansion, shift toward rechargeable power modules, and telemedicine adoption rates. Multivariate regression with these drivers produces the 2025-2030 outlook, while scenario analysis tests sensitivity to reimbursement reforms. Where bottom-up gaps appear, regional proxy ratios are applied and later replaced when fresh evidence arrives.

Data Validation & Update Cycle

Outputs pass variance screens against historical series and adjacent device categories. A senior analyst reviews anomalies, then the model is locked. Reports refresh annually, with interim updates when material events, such as regulatory shifts or major tender wins, occur. A final pre-delivery sweep ensures clients receive the latest view.

Why Mordor's Otoscope Baseline Commands Confidence

Published estimates often diverge because firms choose different product mixes, price definitions, and refresh rhythms. Our disciplined scoping, paired with annual contact-based updates, steadies the baseline that decision-makers need.

Key gap drivers include whether video otoscopes are counted, the use of factory-gate versus end-use values, and the way currency and inflation are normalized. Some publishers also roll adjacent ENT visualization tools into totals or rely heavily on shipment data without demand reconciliation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 206.69 Million (2025) | Mordor Intelligence | - |

| USD 196.30 Million (2025) | Global Consultancy A | Excludes video models and applies shipment-only approach |

| USD 222.50 Million (2024) | Industry Research Firm B | Factory-gate values and constant 2020 currency, no demand checks |

| USD 274.26 Million (2024) | Trade Journal C | Bundles ENT diagnostic sets and handheld lights into scope |

The comparison shows that when scope, price basis, and validation steps vary, totals swing widely. Mordor's balanced blend of verified demand drivers, periodic updates, and transparent assumptions delivers a dependable starting point for strategic planning.

Key Questions Answered in the Report

What is the current size of the otoscope market?

The otoscope market is valued at USD 215.41 million in 2026 and is projected to reach USD 264.81 million by 2031.

Which region holds the largest otoscope market share?

North America leads with 37.15% revenue share in 2025, driven by advanced healthcare infrastructure and early-phase regulatory approvals.

Which segment is growing fastest within the otoscope market?

Portable, battery-operated otoscopes are expanding at a 5.36% CAGR due to telehealth expansion and point-of-care needs.

How are AI tools influencing otoscope diagnostics?

Deep-learning models boost diagnostic sensitivity to 93.8% and specificity to 93.5% for acute otitis media, enabling accurate assessments without specialist oversight.

What regulatory changes are impacting new otoscope launches?

The FDA’s streamlined 510(k) pathway and De Novo classifications shorten approval cycles, while Europe’s MDR has lengthened conformity-assessment timelines for novel devices.

Page last updated on: