Drug Discovery Outsourcing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

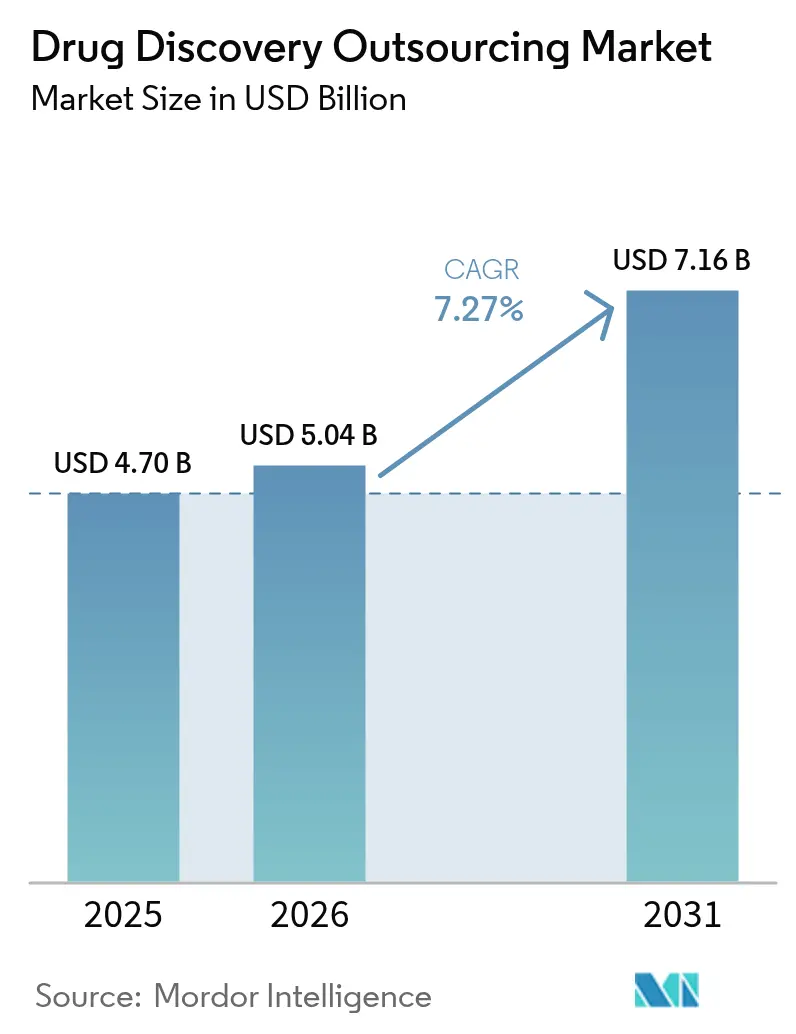

| Market Size (2026) | USD 5.04 Billion |

| Market Size (2031) | USD 7.16 Billion |

| Growth Rate (2026 - 2031) | 7.27% CAGR |

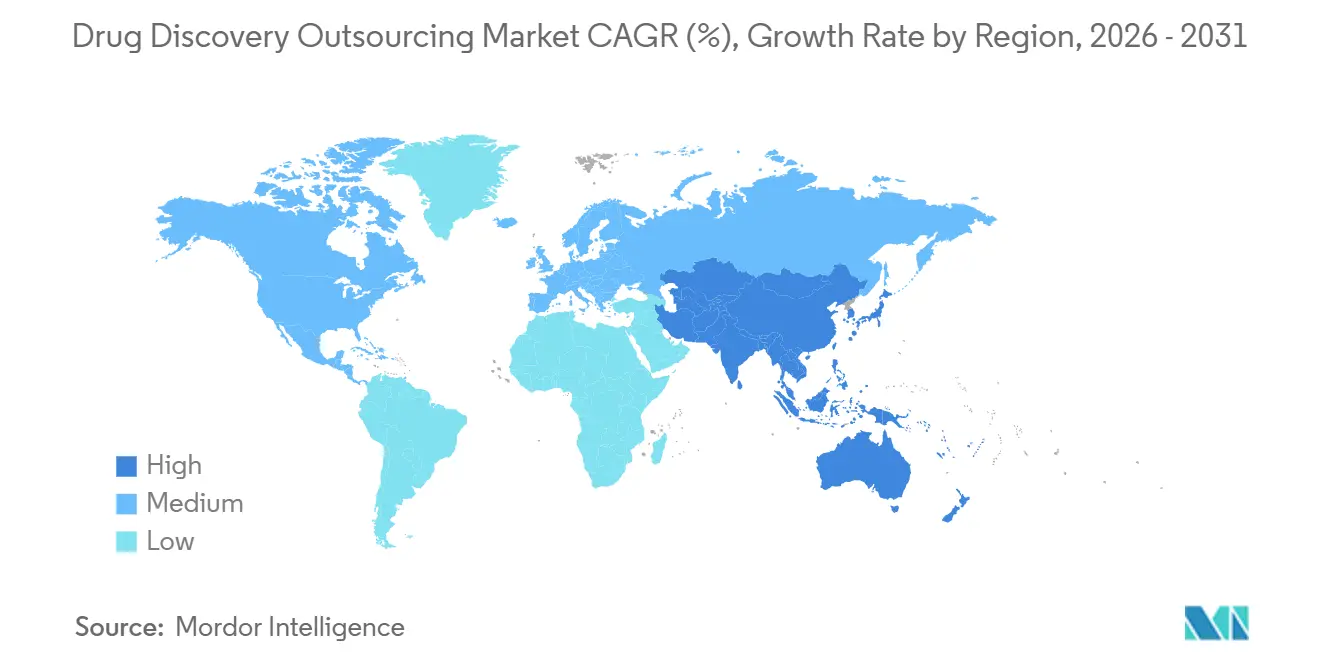

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

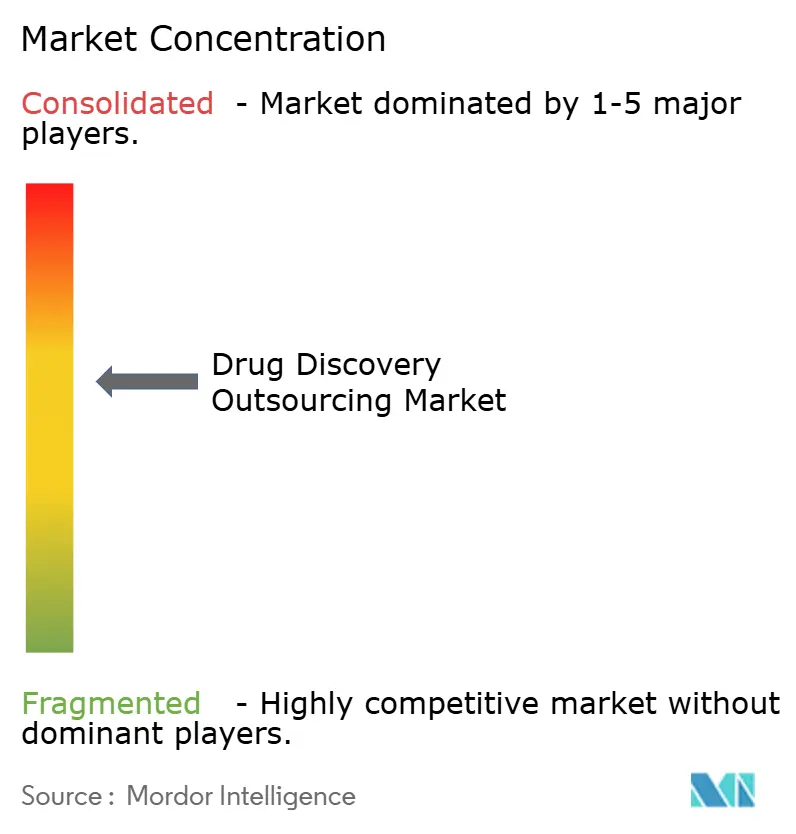

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Drug Discovery Outsourcing Market Analysis by Mordor Intelligence

The Drug Discovery Outsourcing Market size is projected to be USD 4.70 billion in 2025, USD 5.04 billion in 2026, and reach USD 7.16 billion by 2031, growing at a CAGR of 7.27% from 2026 to 2031.

This steady expansion is built on four underlying factors: the pharmaceutical sector’s pivot toward external innovation, the growing scientific complexity of next-generation therapies, digital technology’s acceleration of early discovery workflows, and the need to rebalance internal capital commitments. Sponsors are increasingly shifting to asset-light operating models, enabling them to utilize external AI-driven hit identification, advanced biologics characterization, and CNS-optimized DMPK platforms without incurring the fixed costs of maintaining in-house infrastructure. Although cost differences remain relevant, the strategic priority has moved toward accessing specialized expertise, accelerating development timelines, and distributing risks through milestone-based agreements. The adoption of hybrid service models, which align CRO incentives with clinical outcomes, is on the rise. Additionally, regulatory approval of CRO-generated data packages has eliminated a significant historical obstacle. Automation and AI are being deployed across all service areas, reducing timelines and partially offsetting the impact of rising scientific labor costs.

Key Report Takeaways

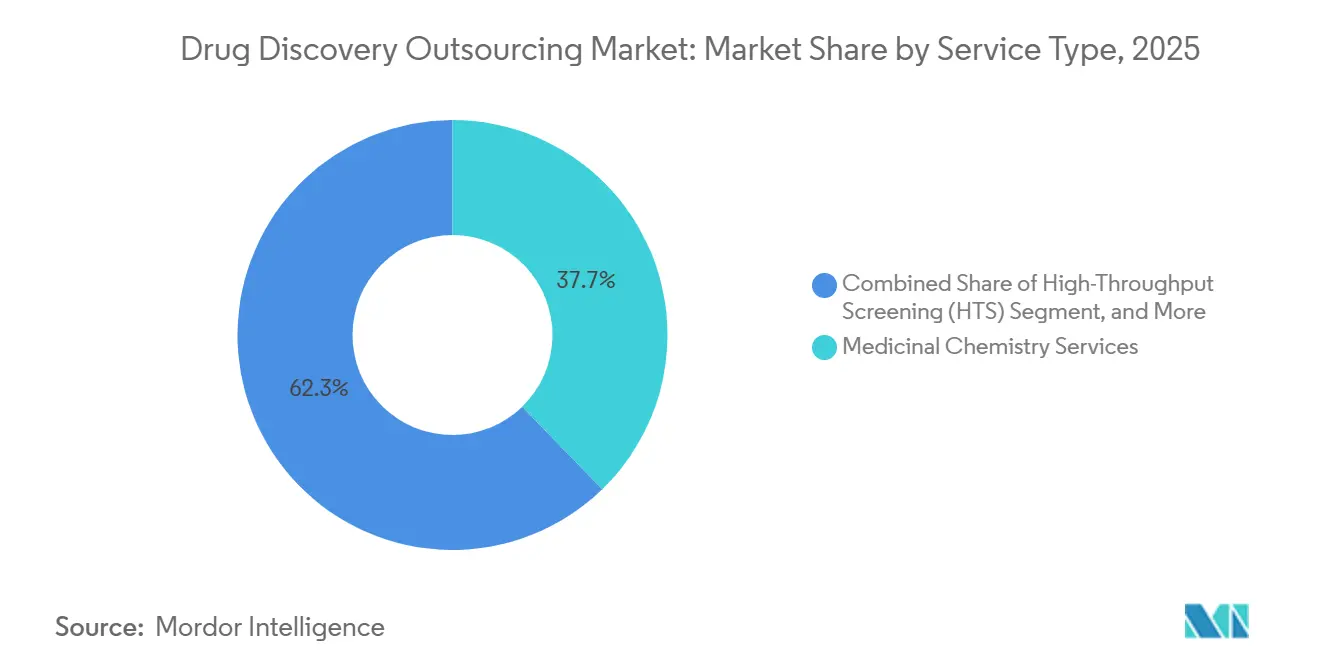

- By service type, medicinal chemistry led with a 37.74% revenue share in 2025; high-throughput screening is projected to grow at a 13.12% CAGR through 2031.

- By drug type, small molecules accounted for 64.70% of the drug discovery outsourcing market in 2025, while cell & gene therapies are expected to expand at a 15.55% CAGR through 2031.

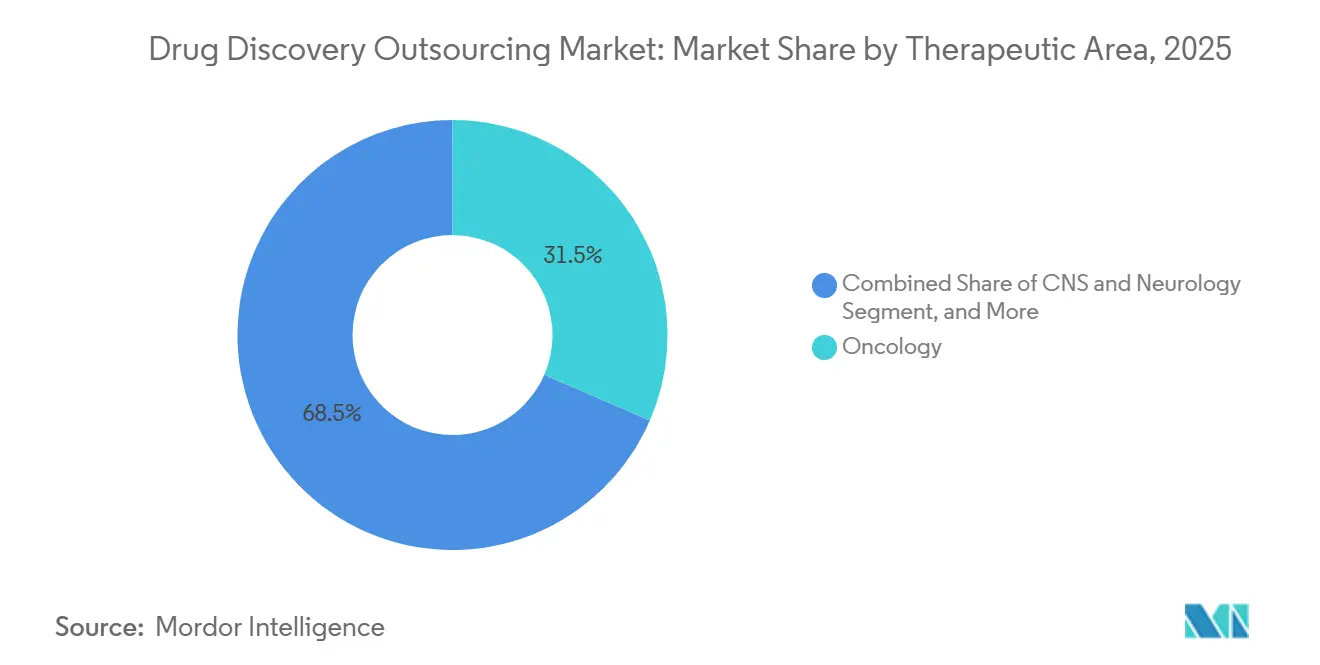

- By therapeutic area, oncology captured 31.50% of the drug discovery outsourcing market share in 2025; the CNS & neurology segment is forecast to grow at a 13.94% CAGR between 2026 and 2031.

- By end user, biotechnology companies accounted for 55.22% of revenue in 2025; academic & research institutes show the fastest growth trajectory, with a 11.32% CAGR to 2031.

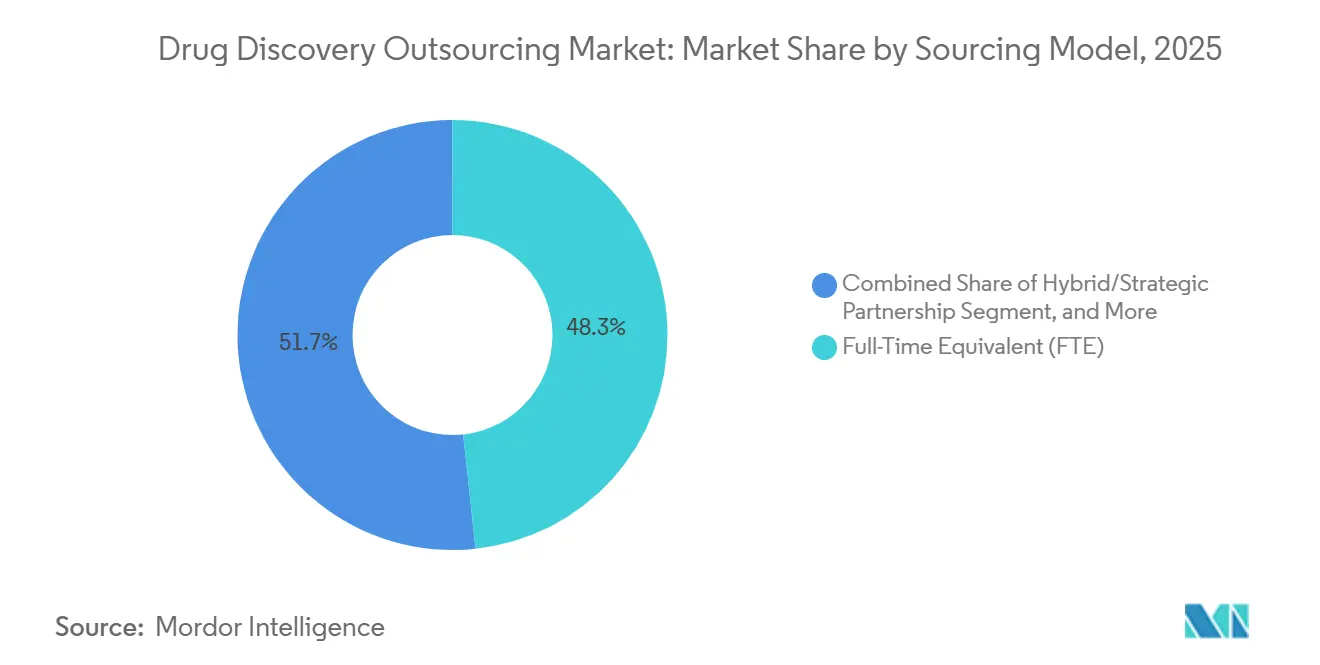

- By sourcing model, full-time equivalent agreements accounted for 48.30% of 2025 revenues, whereas hybrid partnerships are set to grow at a 12.62% CAGR through 2031.

- By geography, North America commanded 40.58% of the market in 2025; Asia-Pacific is forecast to register a 12.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Drug Discovery Outsourcing Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Escalating global R&D spend by pharma & biotech firms | +1.8% | Global with concentration in North America and Europe | Long term (≥ 4 years) |

| Rising burden of chronic and rare diseases is expanding novel therapeutic pipelines | +1.5% | Global, particularly Asia-Pacific | Long term (≥ 4 years) |

| Cost-efficiency & speed-to-market imperatives | +1.2% | Global, stronger pull in North America and Europe | Medium term (2-4 years) |

| Regulatory acceptance of CRO-generated data packages | +0.9% | North America and Europe, gradual Asia-Pacific uptake | Medium term (2-4 years) |

| Proliferation of virtual / asset-light biotech start-ups | +1.1% | North America and Europe biotech hubs | Short term (≤ 2 years) |

| AI-driven de-novo design platforms opening new outsourcing niches | +1.3% | Global, led by North America and China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Global R&D Spend by Pharma & Biotech Firms

The pharmaceuticals represented approximately 18% of all business R&D in the U.K. in 2024, with private-sector spending continuing to grow. External sourcing accounted for 61% of corporate discovery budgets.[1]Office for National Statistics, “Business Enterprise Research and Development, UK: 2024,” ons.gov.uk Virtual biotechs, such as Relation Therapeutics and Latent Labs, operate with lean teams of fewer than 20 employees while outsourcing nearly all discovery tasks to CRO networks. Sponsors are willing to pay premium rates to partners with over 85% IND acceptance, prioritizing CROs that offer integrated services, including chemistry, biology, DMPK, and regulatory documentation. The expansion of pharmaceutical pipelines into multi-modality assets, supported by consistent R&D allocations, drives growth in the drug discovery outsourcing market. Additionally, strong capital-market interest in biotechnology IPOs and venture funding sustains this momentum, even amid macroeconomic volatility. Consequently, CROs benefit from multi-year visibility in their order books and increasing average contract values. AI models such as Stanford’s SyntheMol generated 25,000 antibiotic candidates in under nine hours, illustrating the productivity lift available when algorithmic design meets high-throughput synthesis.[2]Madura Jayatunga et al., “How successful are AI-discovered drugs in clinical trials?,” Drug Discovery Today, sciencedirect.com Such speed gives early movers a chance to secure patent positions before rivals address the same target families.

Rising Burden of Chronic and Rare Diseases Expanding Novel Therapeutic Pipelines

In 2025, the global incidence of cancer exceeded 2 million new cases in the United States, with oncology contributing 31.50% to outsourced discovery spending that year.[3]American Cancer Society, “Cancer Facts & Figures 2025,” cancer.org The demand for CNS candidates capable of overcoming blood-brain-barrier challenges is driving the segment's notable 13.94% CAGR. Rare-disease programs increasingly depend on CROs for phenotypic screening when patient cohorts are limited. These evolving requirements are straining in-house capacities, making external discovery partnerships a strategic necessity rather than an optional approach. In the Asia-Pacific region, the aging population is accelerating the prevalence of chronic diseases, adding a regional dimension to growth. CROs with proven biomarker discovery capabilities and advanced biology suites are gaining stronger negotiation leverage, contributing to higher blended service prices.

Cost-Efficiency & Speed-To-Market Imperatives

Sponsors report 25-50% cycle-time reductions when early-stage work is moved to focused CRO teams that operate purpose-built automation and in silico screening platforms. Digital models reduce false positives, compress hit confirmation runs, and free internal scientists for downstream clinical design. Competitive landscapes in immuno-oncology and metabolic disorders reward first entrants, so financial valuation hinges on shaving months from lead optimization. Outsourcing circulation-dependent tasks such as ADME screening eliminates capital tied up in instrument fleets that rapidly depreciate.

Regulatory Acceptance of CRO-Generated Data Packages

ICH E6(R3) places equal responsibility on sponsors and CROs, provided quality systems comply with ISO 9001 and GLP standards. The FDA's 2024 guidance supports CRO-operated platforms for ADME predictions, provided that algorithm validation is properly documented. In Europe, CTIS streamlines data submission formats across member states, reducing compliance challenges. This development reassures sponsors that outsourcing will not disrupt IND timelines, driving increased reliance on external partnerships. However, the BIOSECURE Act in the United States introduces potential restrictions on the use of Chinese CROs by 2032, compelling sponsors to manage cost, capacity, and geopolitical risks carefully.[4]Reuters Staff, “WuXi AppTec expands despite BIOSECURE uncertainty,” reuters.com

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High capital intensity of cutting-edge discovery platforms limiting cro availability | -0.8% | Global, impacts smaller CROs in Asia-Pacific and Europe | Medium term (2-4 years) |

| Stringent data-integrity & ip-protection requirements complicating cross-border projects | -1.1% | Global, acute for U.S.-China collaborations | Short term (≤ 2 years) |

| Variable quality standards among mid-tier providers undermining sponsor confidence | -0.6% | Global, concentrated in emerging Asia-Pacific and MEA | Medium term (2-4 years) |

| Inflationary pressure on skilled scientific labor eroding outsourcing cost advantage | -0.9% | Global, most acute in China, India, Eastern Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity of Cutting-Edge Discovery Platforms Limiting CRO Availability

With costs ranging from USD 10-50 million, Cryo-EM suites, acoustic liquid handlers, and AI compute clusters remain financially inaccessible for most mid-tier CROs. Lonza's USD 1 billion investment in capsid manufacturing and Thermo Fisher's USD 2 billion expansion in cell therapy highlight the significant scale required to maintain competitiveness. Smaller providers face prolonged payback periods and financing challenges, which concentrate high-end demand among a limited number of global leaders. Sponsors seeking integrated offerings encounter capacity constraints, necessitating project scheduling months in advance, often at premium pricing.

Stringent Data-Integrity & IP-Protection Requirements Complicating Cross-Border Projects

Governments are tightening data-residency rules and auditing electronic lab notebooks, especially for AI-driven discovery programs that rely on large genomic datasets. A single compliance breach averages USD 14.8 million in penalties and remediation, forcing sponsors to vet partners’ cybersecurity postures and blockchain-based traceability solutions. Federated learning and zero-knowledge encryption methods are gaining traction because they allow model training across country borders without centralizing raw patient data. In 2024, regulators issued a dozen warning letters to contract labs for data-integrity violations, such as inadequate audit trails. Concerns over intellectual property protection persist, highlighted by unauthorized Chinese patent filings reported by U.S. sponsors between 2022 and 2024. Consequently, some companies are dividing projects among multiple CROs, creating coordination challenges and reducing efficiency. The BIOSECURE Act has intensified risk perceptions, encouraging sponsors to diversify operations across jurisdictions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Medicinal Chemistry Continues to Anchor, Screening Accelerates

In 2025, medicinal chemistry accounted for 37.74% of the drug discovery outsourcing market, driven by the complexities of scaffold hopping, PROTAC synthesis, and structure-activity relationship optimization. High-throughput screening emerged as the fastest-growing service, with a 13.12% CAGR, supported by acoustic systems that reduce reagent usage by 90% and AI scoring that shortens triage cycles from weeks to days. As the drug discovery outsourcing market grows, biology services such as target validation and cell-based assays maintain steady demand as sponsors increasingly adopt mechanism-agnostic exploration, particularly in oncology and rare diseases. While DMPK and toxicology are becoming commoditized, they remain essential to early kill-fail strategies that help reduce downstream attrition.

The integration of chemistry and biology increasingly shapes contract structures. Sponsors are favoring comprehensive packages that link screening outputs to medicinal chemistry follow-up, fostering long-term partnerships with CROs that offer both capabilities. Meanwhile, niche providers specializing in areas like electrophysiology or translational biomarker services are securing high-value, project-based contracts when sponsors focus on particular endpoints.

By Drug Type: Small Molecules Hold Sway While Modalities Diversify

In 2025, small molecules accounted for 64.70% of revenue, driven by their ease of oral administration and favorable regulatory frameworks. However, cell and gene therapies are driving significant growth with a strong 15.55% CAGR, supported by a USD 3 billion expansion in global CDMO capacity since 2024. These advanced therapies command service premiums of 50-100% over small-molecule counterparts, propelling the overall drug discovery outsourcing market. Furthermore, RNA-based therapeutics are emerging as a key growth area as mRNA and siRNA platforms continue to evolve following their post-COVID-19 success.

Providers are differentiating themselves through specialized CRO suites focused on viral vector engineering, capsid optimization, and lipid nanoparticle formulation. Established small-molecule players are expanding their capabilities in these new modalities through internal development or acquisitions to retain clients. However, the high capital requirements are slowing the pace of portfolio diversification. Meanwhile, sponsors are effectively managing modality risks across their pipelines, maintaining consistent demand for traditional chemotypes while piloting next-generation therapies.

By Therapeutic Area: Oncology Dominates, CNS Surges

In 2025, oncology programs are projected to contribute 31.50% of total revenue, driven by advancements in immuno-oncology, antibody-drug conjugates, and cell-therapy pipelines, which require sophisticated biomarker strategies. Although smaller in scale, CNS and neurology projects are expected to achieve the highest growth, with a 13.94% CAGR. This growth is attributed to innovations such as blood-brain-barrier shuttles and AI-enabled target de-risking, which have significantly reduced historically high failure rates. In contrast, outsourcing for infectious disease projects remains cyclical, increasing during periods of pandemic preparedness and declining when public health budgets are constrained.

The drug discovery outsourcing market benefits from therapeutic diversification, as each therapeutic area demands distinct assay suites and animal models. This dynamic encourages sponsors to engage a mix of providers. Contract Research Organizations (CROs) with extensive expertise across multiple disease areas often secure master service agreements, enabling them to manage a range of assets. Meanwhile, niche specialists excel by focusing on complex indications, such as neurodegeneration and rare metabolic disorders.

By End-User: Biotechnology Companies Drive Current Demand while Academic Institutes Gain Pace

Biotechnology firms accounted for 55.22% of 2025 spending because their lean operating models emphasize external partnerships for wet-lab work, while internal staff focus on scientific vision and investor relations. Access to venture capital has increased, yet investors still scrutinize burn rates; outsourcing offers variable-cost structures and milestone alignment. Academic and research institutes are projected to grow at a 11.32% CAGR, spurred by government grants that encourage translational collaborations and by technology transfer offices that license discoveries into spin-out entities.

Artificial intelligence now bridges bench discoveries with development pipelines, turning raw omics data into druggable hypotheses. CROs supply expertise in assay development and medicinal chemistry to advance these hypotheses toward IND-ready candidates. Successful academic-industry consortia strengthen reputational capital, prompting more universities to embed contract work packages within grant applications, a structural tailwind for the drug discovery outsourcing market.

By Sourcing Model: FTE Contracts Anchor Revenue, Hybrids Gain Momentum

Full-time equivalent arrangements accounted for 48.3% of 2025 revenues by providing sponsors with dedicated scientists, predictable budgeting, and continuity across iterative discovery cycles. Clear governance frameworks and daily communication channels foster shared accountability for scientific milestones. Hybrid partnerships, forecast to grow at a 12.62% CAGR, weave elements of FTE and fee-for-service together, with risk-sharing provisions such as success fees for hitting potency or selectivity thresholds. The model aligns incentives and encourages providers to invest in novel technology platforms because upside participation offsets capital risk.

Sponsors increasingly pilot hybrid contracts in high-uncertainty therapeutic areas like gene editing, where endpoint definitions evolve. CROs willing to shoulder outcome risk gain preferential status lists and early visibility into future pipeline needs. This collaborative stance lifts switching barriers and reinforces market stickiness, securing long-term integration inside the drug discovery outsourcing market.

Geography Analysis

North America generated 40.58% of 2025 revenue attributable to its dense cluster of pharmaceutical headquarters, venture-backed biotechs, and AI start-ups. United States CROs channel venture flows into state-of-the-art automation, layered compound libraries, and curated human data assets. Regulatory openness toward real-world evidence further accelerates project throughput by shrinking non-clinical packages. Canada complements the regional ecosystem with governmental incentives for pre-clinical innovation, bringing fiscal benefits without compromising quality expectations.

Asia-Pacific shows the steepest trajectory at 12.84% CAGR between 2026 and 2031, buoyed by an expanding talent pool, lower operating costs, and national roadmaps that prioritize biopharma self-sufficiency. China leads regional revenue thanks to integrated campus sites that combine chemistry, biology, and GMP suites. India strengthens its position through extensive synthetic chemistry capacity and an English-speaking workforce. South Korea invests in genomic big-data hubs that underpin AI-driven target discovery. Collectively, these dynamics lure global sponsors seeking cost relief without sacrificing scientific sophistication, enhancing the region’s share of the drug discovery outsourcing market.

Europe sustains strong performance on the back of rigorous quality standards, deep academic networks, and domain expertise in complex modalities such as RNA therapeutics. Germany and Switzerland specialize in high-precision analytics and antibody engineering, while the United Kingdom fosters AI-first discovery ventures under supportive data governance frameworks. Although growth rates trail those of Asia-Pacific, Europe’s reputation for compliance excellence secures a steady pipeline of high-value projects. Cross-border initiatives funded by Horizon Europe link small CROs with large pharma sponsors, reinforcing the continent’s role as a strategic partner rather than just a capacity provider.

Competitive Landscape

The competitive arena features moderate fragmentation, with the top 10 vendors accounting for significant revenue. Charles River Laboratories, WuXi AppTec, and Thermo Fisher Scientific drive consolidation by acquiring niche providers in computational chemistry, bioinformatics, and advanced bioanalytics. Their full-service portfolios span target validation through IND-enabling toxicology, reducing transition friction, and offering one-contract simplicity. Smaller specialists differentiate through depth in single modalities, for example, companies focused exclusively on macrocyclic peptide libraries or PROTAC design, and often collaborate with large CROs under preferred-provider frameworks.

Technology integration shapes rivalry. Firms deploying proprietary generative AI engines or quantum-informed docking algorithms can shorten design cycles, justify premium pricing, and attract venture-backed biotech clients that value speed. CROs without digital muscle risk relegation to low-margin commodity work. Intellectual property models evolve accordingly, with shared-ownership clauses and data-residency safeguards becoming standard. Strategic alliances between cloud providers and major CROs surface, combining scalable compute with curated chemical space to reinforce competitive moats.

Geographic expansion also influences market shares. Western incumbents respond by enlarging Singapore and Melbourne labs to serve time-zone-adjacent clients and by building bilingual project-management hubs. The interplay of capability breadth, digital innovation, and regulatory acumen defines competitive posture inside the drug discovery outsourcing market.

Drug Discovery Outsourcing Industry Leaders

Charles River Laboratories International, Inc.

Thermo Fisher Scientific Inc. (PPD)

Laboratory Corporation of America Holdings (Labcorp Drug Development)

Eurofins Scientific SE

WuXi AppTec

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Sygnature Discovery relaunched its brand and website to reinforce positioning as an integrated partner.

- February 2026: Syngene International and Johns Hopkins University began a strategic collaboration delivered through SynVent to accelerate early-stage programs.

- February 2026: Insilico Medicine and China Medical System initiated AI-powered discovery alliances covering CNS and autoimmune projects.

- February 2026: Takeda entered a multi-year partnership with Iambic that could exceed USD 1.7 billion, initially targeting oncology and GI indications.

- January 2026: Insilico Medicine and Qilu Pharmaceutical created a joint program to develop small-molecule cardiometabolic inhibitors via the Pharma.AI platform.

- June 2025: XtalPi and Pfizer expanded their collaboration to co-develop an advanced molecular-modeling platform for discovery.

Global Drug Discovery Outsourcing Market Report Scope

As per the scope of the report, drug discovery outsourcing is a process in which two companies enter into a working agreement in which one company produces the desired drug on behalf of its client. In some cases, the contract manufacturer also handles the client's ordering and shipping.

The drug discovery outsourcing market is segmented by type, drug type, therapeutic area, end-user, sourcing model, and geography. By type, the market is segmented into medical chemistry service and biology service. By drug type, the market is segmented into small molecules and large molecules (biopharmaceuticals). By therapeutic area, the market is segmented into oncology, infectious diseases, respiratory diseases, cardiovascular diseases, gastrointestinal diseases, and others. By end-user, the market is segmented into pharmaceutical companies, biotechnology companies, academic & research institutes, contract manufacturing/development organizations, and others. By sourcing model, the market is segmented into full-time equivalent (FTE), fee-for-service (FFS), functional service partnership, and hybrid/strategic partnership. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers market size and forecasts in value (USD) for the above segments.

| Medicinal Chemistry Services |

| Biology Services |

| DMPK & Toxicology |

| Hit-to-Lead & Lead Optimisation |

| High-Throughput Screening (HTS) |

| Small Molecules |

| Large Molecules |

| Cell & Gene Therapies |

| Peptide/Protein Therapeutics |

| RNA-based Therapeutics |

| Oncology |

| Infectious Disease |

| CNS and Neurology |

| Cardiovascular |

| Respiratory |

| Gastrointestinal |

| Autoimmune & Inflammatory |

| Metabolic Disorders |

| Others |

| Pharmaceutical Companies |

| Biotechnology Companies |

| Academic & Research Institutes |

| Contract Manufacturing / Development Organisations |

| Others |

| Full-Time Equivalent (FTE) |

| Fee-for-Service (FFS) |

| Functional Service Partnership |

| Hybrid / Strategic Partnership |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Medicinal Chemistry Services | |

| Biology Services | ||

| DMPK & Toxicology | ||

| Hit-to-Lead & Lead Optimisation | ||

| High-Throughput Screening (HTS) | ||

| By Drug Type | Small Molecules | |

| Large Molecules | ||

| Cell & Gene Therapies | ||

| Peptide/Protein Therapeutics | ||

| RNA-based Therapeutics | ||

| By Therapeutic Area | Oncology | |

| Infectious Disease | ||

| CNS and Neurology | ||

| Cardiovascular | ||

| Respiratory | ||

| Gastrointestinal | ||

| Autoimmune & Inflammatory | ||

| Metabolic Disorders | ||

| Others | ||

| By End-User | Pharmaceutical Companies | |

| Biotechnology Companies | ||

| Academic & Research Institutes | ||

| Contract Manufacturing / Development Organisations | ||

| Others | ||

| By Sourcing Model | Full-Time Equivalent (FTE) | |

| Fee-for-Service (FFS) | ||

| Functional Service Partnership | ||

| Hybrid / Strategic Partnership | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the drug discovery outsourcing market in 2031?

It is expected to reach USD 7.16 billion on a 7.27% CAGR trajectory.

Which service segment currently generates the highest revenue?

Medicinal chemistry services led with 37.74% share in 2025.

Which region is growing fastest between 2026 and 2031?

Asia-Pacific is forecast to expand at a 12.84% CAGR, outpacing all other regions.

Why are virtual biotech companies important to outsourcing demand?

Their lean structures rely on external partners for lab work, driving steady contract flow toward CROs.

How does AI improve early drug discovery?

Generative engines can create and triage thousands of candidate molecules within hours, compressing hit-to-lead timelines and reducing cost.

Page last updated on: