Drug Eluting Stent Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.46 Billion |

| Market Size (2031) | USD 13.28 Billion |

| Growth Rate (2026 - 2031) | 7.03% CAGR |

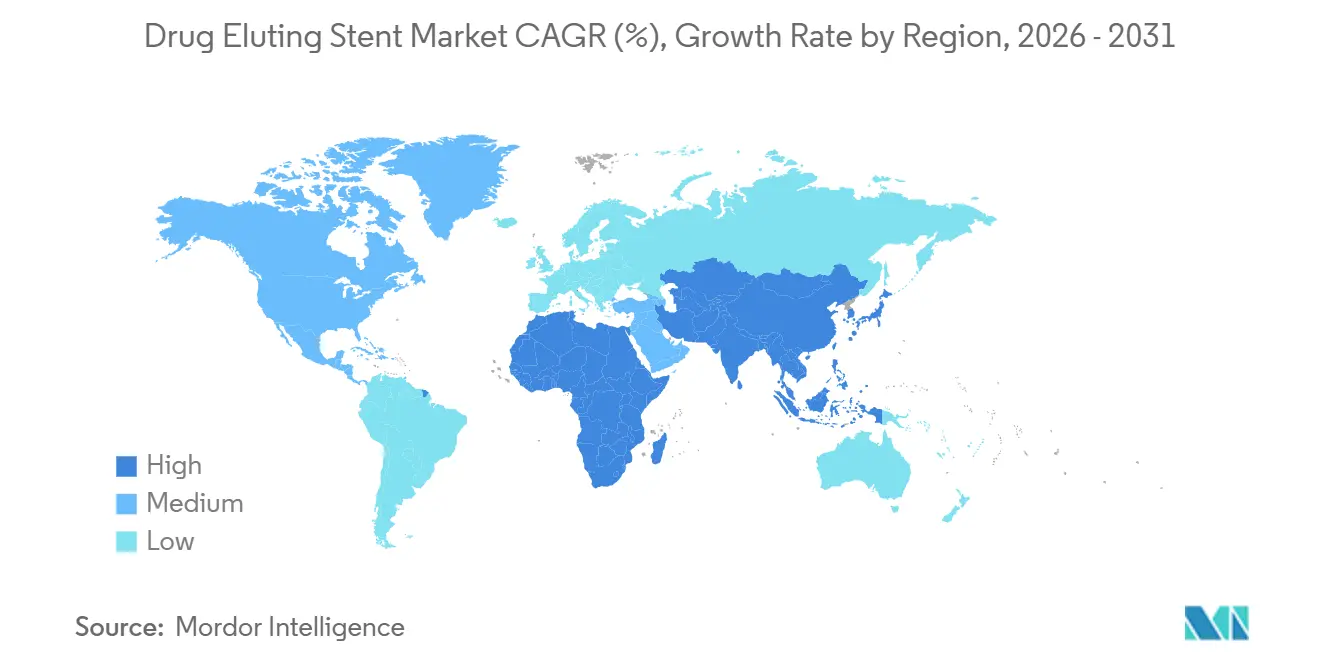

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Drug Eluting Stent Market Analysis by Mordor Intelligence

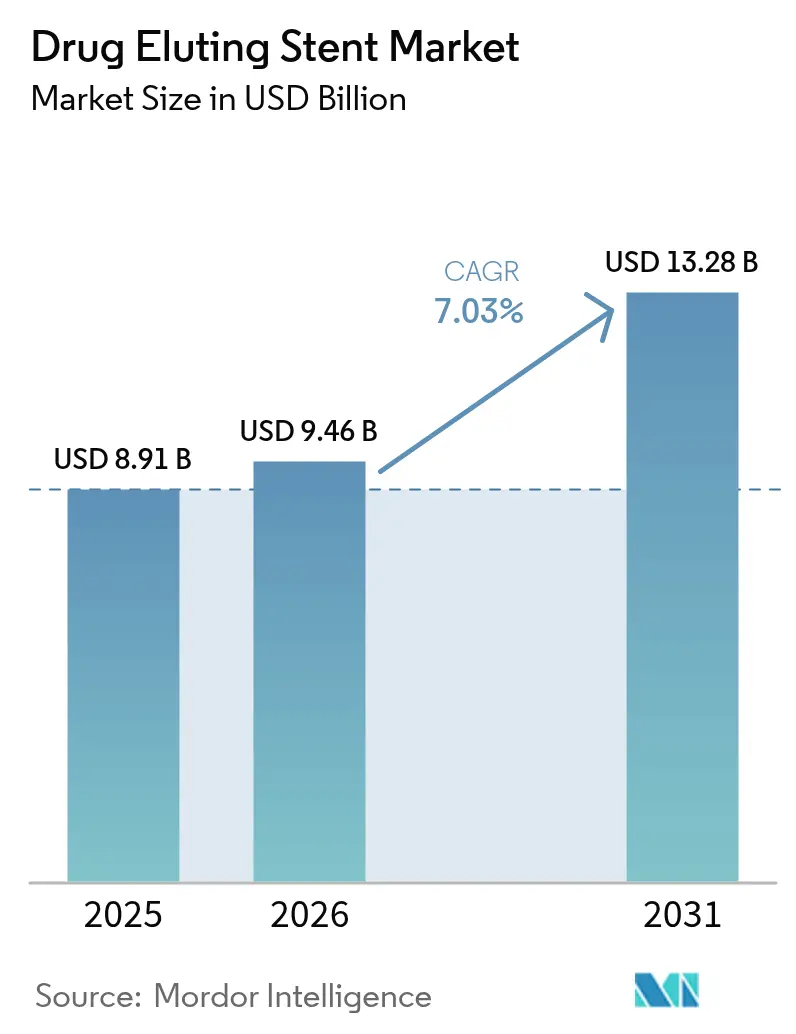

The Drug Eluting Stent Market size is expected to increase from USD 8.91 billion in 2025 to USD 9.46 billion in 2026 and reach USD 13.28 billion by 2031, growing at a CAGR of 7.03% over 2026-2031.

Widening eligibility created by one-month dual-antiplatelet labeling, sustained penetration of ultra-thin strut designs, and the ongoing shift of uncomplicated procedures toward ambulatory surgical centers underpin this trajectory. Bioresorbable polymer platforms, magnesium alloy scaffolds, and AI-guided intravascular imaging are coalescing to lower late-stent thrombosis, reduce repeat revascularization, and cut procedure time, changes that enlarge the addressable population and compress total cost of care. Regional dynamics are evolving just as rapidly: domestic manufacturers in China and India now market cobalt-chromium platforms at price points 40–60% below Western equivalents, while agencies in Japan and South Korea fast-track polymer-free devices that demonstrate superior safety in elderly patients with renal impairment. Simultaneously, hospitals face tightening post-market surveillance obligations that lengthen evidence generation but improve real-world applicability, a regulatory recalibration that favors companies with strong clinical infrastructure.

Key Report Takeaways

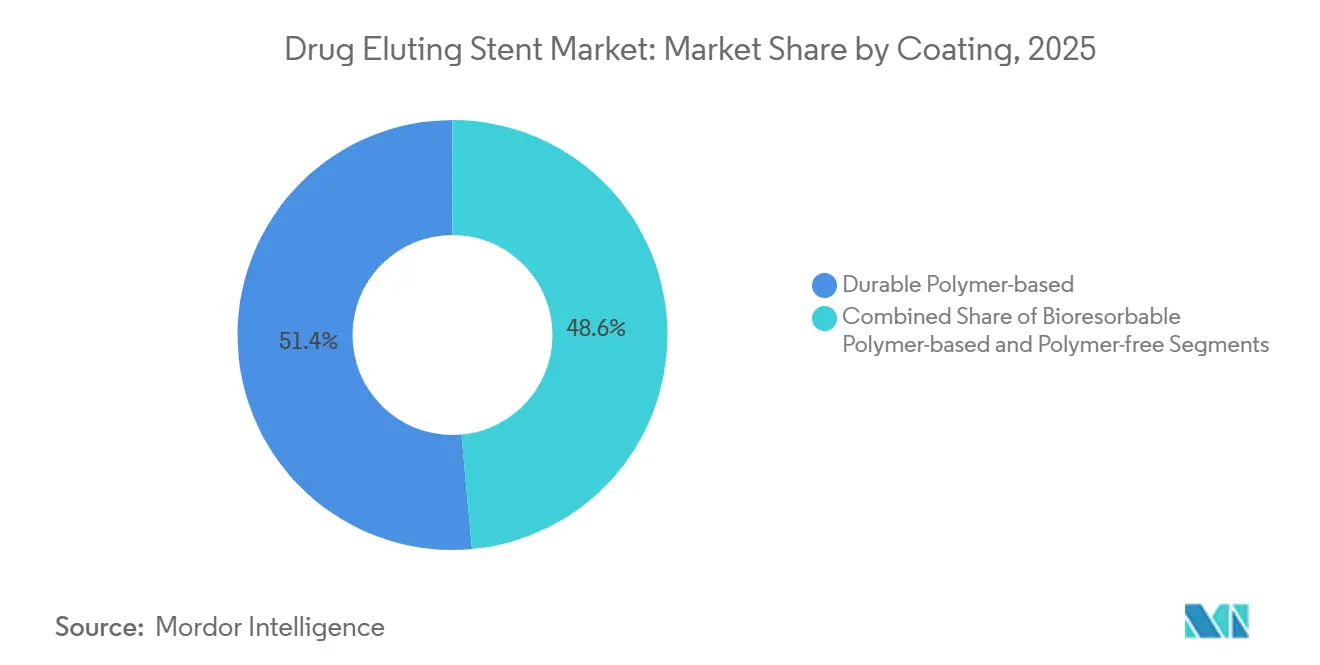

- By coating type, durable polymers led with 51.44% of drug-eluting stent market share in 2025, whereas bioresorbable platforms are projected to advance at a 10.36% CAGR through 2031.

- By material, cobalt-chromium alloys accounted for 37.66% of the drug-eluting stent market size in 2025; magnesium alloy composites are on track to grow at an 11.77% CAGR over 2026-2031.

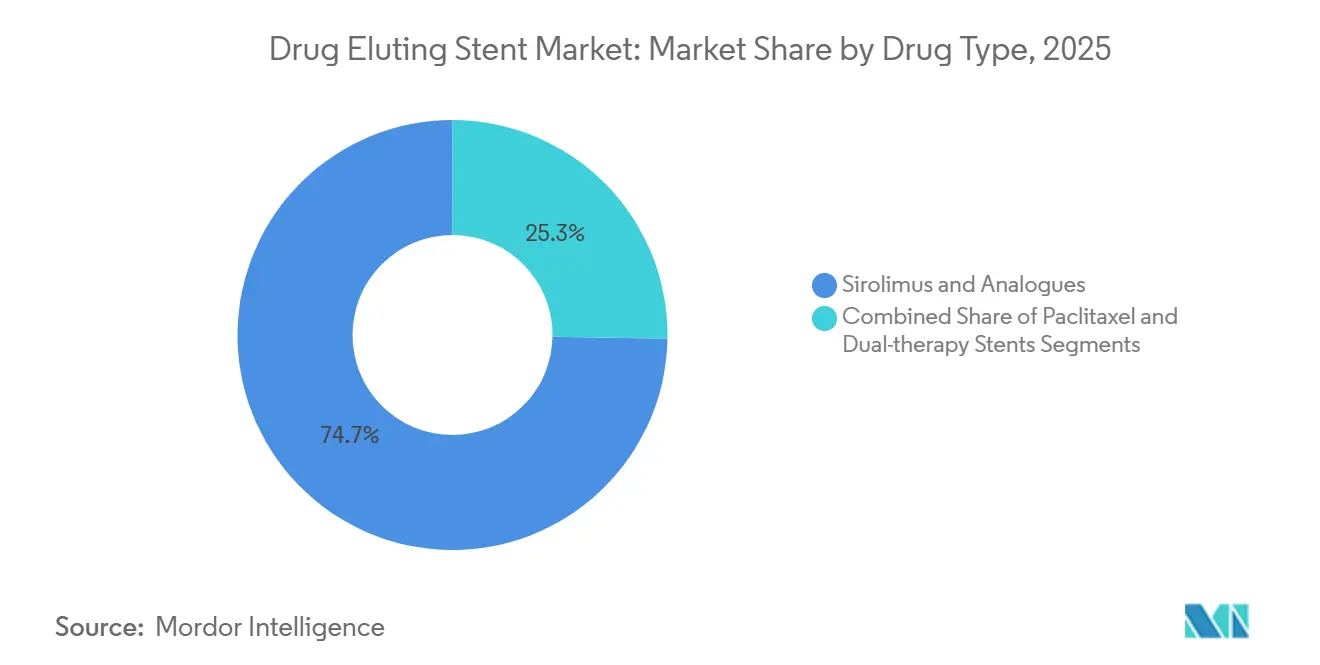

- By drug type, sirolimus and its analogues captured 74.73% share in 2025, while dual-therapy combination stents are forecast to expand at an 11.64% CAGR to 2031.

- By application, coronary artery disease represented 72.42% of the drug-eluting stent market size in 2025; peripheral artery disease is expected to climb at a 10.43% CAGR through 2031.

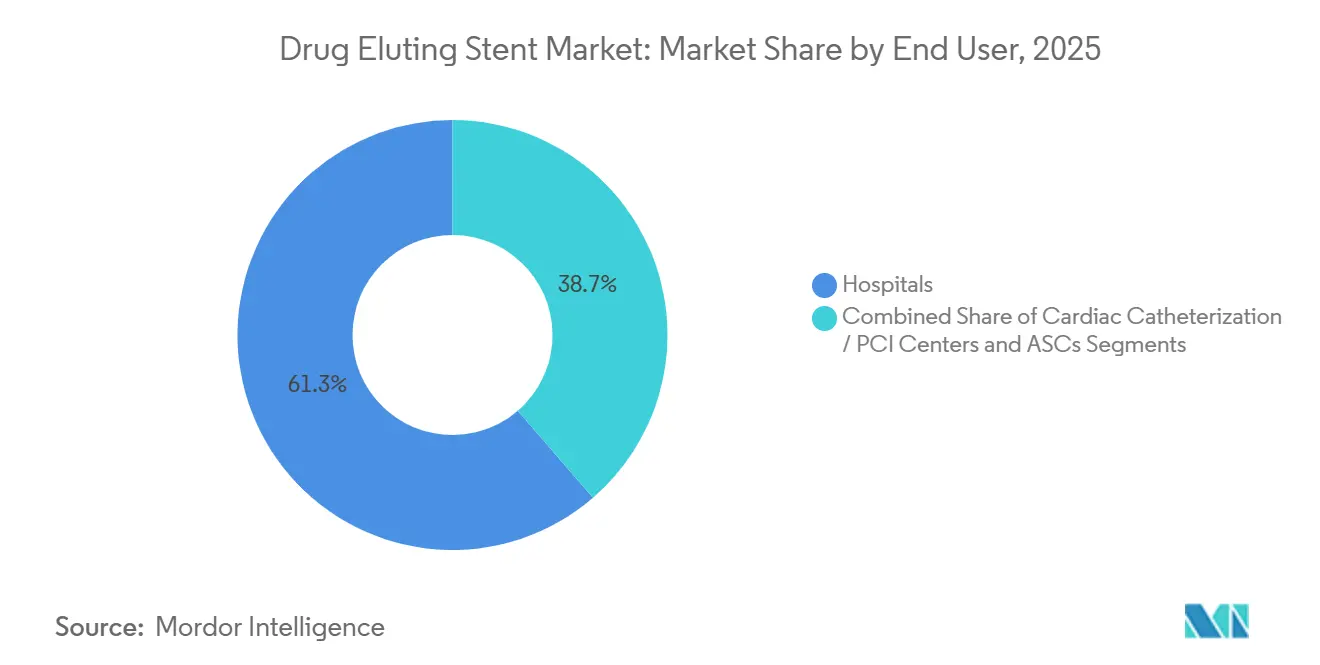

- By end user, hospitals held 61.33% revenue share in 2025, whereas ambulatory surgical centers are poised to register a 9.64% CAGR during 2026-2031.

- By geography, North America led with 39.43% revenue share in 2025, while Asia-Pacific is projected to post the fastest growth at a 9.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Drug Eluting Stent Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Coronary Artery Disease & Aging Population | +1.8% | Global, acute in Europe & North America | Long term (≥ 4 years) |

| Growth in PCI Volumes & Preference for Minimally Invasive Interventions | +1.5% | Asia-Pacific & North America | Medium term (2-4 years) |

| Advances in Polymer Coatings & Ultra-Thin Strut Platforms | +1.2% | North America, Europe, Japan | Medium term (2-4 years) |

| One-Month DAPT Labeling Expanding Eligible Patient Pool | +1.0% | North America, Europe | Short term (≤ 2 years) |

| Domestic Low-Cost DES Production Boosting Adoption in Emerging Asia | +1.1% | Asia-Pacific core, spill-over to MEA & South America | Medium term (2-4 years) |

| AI-Guided Intravascular Imaging Improving Stent Placement Success | +0.4% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Coronary Artery Disease & Aging Population

Global CAD incidence is rising in lock-step with a doubling of the ≥ 65-year demographic, and patients now present with multivessel disease that demands two or more implants per procedure, sustaining device volumes despite preventive cardiology gains.[1]World Health Organization, “Cardiovascular Disease Key Facts,” who.int Age-stratified enrollment, now mandatory in pivotal trials, ensures data relevance for the 40% of interventions performed in Medicare beneficiaries, while chronic kidney disease comorbidity makes bioresorbable polymer stents attractive because they remove long-term foreign material. Geriatric cardiology societies in Europe and Japan endorse ultra-thin strut scaffolds with abbreviated antiplatelet regimens, guidance that converges with evolving ISO-14155 requirements for age-specific analyses.[2]International Organization for Standardization, “ISO 14155:2025 Clinical Investigation,” iso.org

Growth in PCI Volumes & Preference for Minimally Invasive Interventions

U.S. annual PCI volume touched 550,000 in 2024, but the Asia-Pacific surge is more pronounced as China logged 950,000 interventions on the back of rural insurance expansion.[3]National Health Commission of China, “Annual PCI Report 2025,” nhc.gov.cn Radial access and same-day discharge are now commonplace, lowering vascular complications and freeing hospital capacity. Drug-eluting stent market adoption accelerates because target-lesion revascularization remains below 5% at 12 months, a metric embedded in payer scorecards.

Advances in Polymer Coatings & Ultra-Thin Strut Platforms

Sixty-micrometer platinum-chromium scaffolds deliver radial strength above 0.2 MPa yet reduce flow disturbances enough to cut target-lesion failure 18% versus first-generation devices. Predictable 12- to 18-month polymer resorption eliminates chronic inflammation, and FDA-cleared polymer-free designs now serve patients who cannot tolerate extended dual therapy. ISO-10993-13 degradation-product assays add USD 200,000 to validation costs but improve safety transparency.

One-Month DAPT Labeling Expanding Eligible Patient Pool

MASTER-DAPT unlocked one-month regimens for high-bleeding-risk cases and prompted U.S. labeling updates across three leading products. The policy shift immediately freed 150,000 previously deferred U.S. patients for stenting and spurred EMA guidance that any bioresorbable platform with ≤ 1% thrombosis at 12 months can claim similar labeling.

Restraints Impact Analysis of Drug Eluting Stent Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Long-Term Regulatory Evidence Requirements | –0.6% | Global, acute in Europe & North America | Long term (≥ 4 years) |

| High Device & Procedure Cost in Low-Income Regions | –0.5% | Sub-Saharan Africa, South Asia, South America | Medium term (2-4 years) |

| Supply-Chain Vulnerabilities in Medical-Grade Polymers & APIs | –0.3% | Global, peak disruption risk in Europe | Short term (≤ 2 years) |

| Competitive Cannibalization from Drug-Coated Balloons in ISR/Small Vessels | –0.4% | North America, Europe, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Long-Term Regulatory Evidence Requirements

Europe’s MDR obliges five-year follow-up for every bioresorbable scaffold, adding USD 8 million and up to three years to pivotal programs, while the FDA now demands head-to-head non-inferiority against best-in-class comparators, doubling sample size to as many as 3,000 subjects. Post-market registry mandates covering the first 10,000 implants stretch smaller firms yet improve surveillance fidelity.

High Device & Procedure Cost in Low-Income Regions

Unit prices of USD 1,200–3,500 consume up to 60% of annual health spending in some sub-Saharan countries. Only 15% of district hospitals in India and Nigeria operate catheterization labs, forcing 150-km average patient transfers while global donor programs can subsidize barely 30,000 of an estimated 2 million annual unmet interventions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Drug Eluting Stent Market Segment Analysis

By Coating Type:

Bioresorbable Polymers Gain as Inflammation Concerns MountDurable polymer devices held 51.44% drug-eluting stent market share in 2025, sustained by extensive legacy data, yet bioresorbable coatings are pacing a 10.36% CAGR through 2031 because 12-month degradation eliminates chronic foreign-body reactions. Polymer-free alternatives reached 12% share in 2025 and now headline abbreviated antiplatelet strategies. ISO 10993-13 toxicity assays have raised upfront costs yet boosted clinician confidence, helping the drug-eluting stent market size for bioresorbable platforms climb steadily.

Operators continue to select durable polymers for complex diabetes-associated lesions that require extended drug elution, but mainstream use is shifting. The BIOFLOW-VI trial presented at ACC 2025 showed 25% lower late-stent thrombosis with bioresorbable coatings beyond two years, an effect expected to accelerate cannibalization of older platforms and reinforce the drug-eluting stent market trend toward thinner, faster-absorbing polymers.

By Material:

Magnesium Alloys Emerge as Radiolucent Scaffolds That Resorb FullyCobalt-chromium remained the backbone with 37.66% share in 2025, yet magnesium alloy composites are outpacing at an 11.77% CAGR as full resorption within 12 months restores vasomotion. Platinum-chromium alloys deliver the thinnest struts—60 µm—while holding 28% share, retaining a foothold in calcified vessels that demand high radial force. Stainless steel shrank to single digits as surgeons prioritize accelerated endothelialization. Animal-model degradation studies mandated by ISO 10993-15 have lengthened product timelines but cleared toxicity concerns, bolstering clinician acceptance of novel metals and supporting the drug-eluting stent market size outlook for magnesium devices.

Esprit BTK’s 95% resorption at 12 months demonstrated functional restoration in below-the-knee lesions and provides a template for future magnesium platforms, an advance set to divert peripheral applications from permanent nitinol cages and further diversify the drug-eluting stent market.

By Drug Type:

Sirolimus Analogues Dominate as Dual-Therapy Platforms Target Complex LesionsSirolimus family compounds controlled 74.73% revenue in 2025, leveraging four decades of safety evidence. Dual-therapy combinations are the fastest riser at an 11.64% CAGR, layering antiproliferative and anti-inflammatory drugs, especially in bifurcation and CTO cases where inflammation and smooth-muscle migration co-exist. Paclitaxel platforms, at 18% share, face continued attrition on regulatory caution in peripheral arteries, prompting many firms to reformulate with sirolimus analogues, a pivot that reinforces the drug-eluting stent market trend toward mTOR inhibition.

Pipeline projects exploring sirolimus-probucol or sirolimus-tacrolimus combinations must complete dual toxicology workups, extending timelines by as much as 18 months, yet they promise lower late restenosis and could lift the drug-eluting stent market size for complex-lesion devices once safety hurdles are cleared.

By Application:

Peripheral Artery Disease Gains as Below-the-Knee Scaffolds Win ApprovalCoronary indications still dominate with 72.42% of 2025 revenue, but peripheral artery disease is advancing 10.43% annually after FDA clearance of the Esprit BTK scaffold opened a segment long underserved by angioplasty. Femoropopliteal cases continue to rely on nitinol self-expanding designs, yet magnesium resorption and pulsatility restoration are repositioning below-knee therapy and expanding the drug-eluting stent market share for peripheral applications.

CMS assigns a higher ambulatory payment classification to femoropopliteal interventions, improving margins for outpatient centers and driving geographical dispersion of services. Harmonized FDA guidance lets coronary data carry over for peripheral submissions, lopping USD 1 million from each new application and stimulating a wave of pipeline activity that should raise the drug-eluting stent market size devoted to limb-salvage therapy

By End User:

Ambulatory Centers Capture Share as Same-Day Discharge Becomes StandardHospitals retained 61.33% share in 2025 because they remain the hub for multivessel and high-risk acute coronary syndrome cases. Yet ambulatory surgical centers, supported by reimbursement parity, are logging a 9.64% CAGR by capitalizing on radial access protocols that enable same-day discharge. Freestanding catheterization centers hold a 22% share, using streamlined staffing and lower overhead to treat high-throughput urban markets, a dynamic that underlines steady migration and generates new arenas of competition within the drug-eluting stent market.

Hospitals counter by establishing off-campus outpatient departments that still bill under hospital outpatient rates, blunting share erosion. Ambulatory operators are meanwhile adopting AI-guided imaging consoles to speed workflows, a differentiator now factored into payer preferred-provider lists, an evolution that cements site-of-service shifts and keeps the drug-eluting stent market responsive to cost-performance benchmarks.

Geography Analysis

North America Drug Eluting Stent Market

North America generated 39.43% of 2025 revenue, buoyed by premium pricing for bioresorbable platforms and one-month labeling that widened the candidate pool by 150,000 cases. Growth is moderating as drug-coated balloons cannibalize 32% of in-stent restenosis procedures, yet AI-guided imaging adoption offsets some deceleration, keeping the regional drug-eluting stent market sizable.

APAC Drug Eluting Stent Market

Asia-Pacific is the fastest-growing region at a 9.21% CAGR through 2031 as China’s annual PCI volumes approach 1 million and domestic manufacturers offer sub-USD 600 devices that satisfy emerging-market price ceilings. Harmonized dossier pathways now allow a single submission for Japan, South Korea, Taiwan, and ASEAN, streamlining access and accelerating export diffusion, catalysts that elevate the drug-eluting stent market size across developing economies.

EMEA and South America Drug Eluting Stent Market

Europe, wrestles with MDR-instigated evidence burdens that lengthen approvals by two to three years and cost another USD 8 million per scaffold, a deterrent for smaller firms. Nonetheless, rising PCI-to-CABG ratios and one-month dual-therapy endorsements maintain steady demand. Middle East & Africa, at 6%, suffers adoption drag from unit prices equaling half of per-capita health spending, though GCC investment in cath-lab infrastructure is nudging volumes higher. South America holds 8% share, driven largely by Brazil’s 180,000 annual PCIs, while Argentina and Chile post double-digit CAGR as essential-device listings expand reimbursement coverage.

Competitive Landscape

Abbott, Boston Scientific, and Medtronic collectively controlled about large share of 2025 revenue but now confront rapidly scaling Asian players that leverage vertical drug synthesis and local metals sourcing to undercut prices. One-month labeling gives Abbott’s XIENCE, Boston Scientific’s SYNERGY, and Medtronic’s Resolute Onyx defensible moats, yet polymer-free and magnesium platforms from disruptors narrow differentiation. AI-augmented imaging integrations, pioneered by Abbott’s Ultreon and Boston Scientific’s AngioInsight, cut repeat revascularization 14% in registries and permit premium pricing, a margin shield that entrenched leaders will continue to wield.

White-space growth lies in peripheral artery disease after Esprit BTK’s below-knee clearance created an untapped pool of diabetics with critical limb ischemia. Concurrently, FDA-cleared paclitaxel balloons for in-stent restenosis captured nearly one-third of the U.S. indication within 18 months and forced stent makers into hybrid portfolios to hedge share loss. MDR’s five-year safety mandate in Europe increases capital demands, favoring incumbents with robust trial networks and discouraging smaller Asian challengers from immediate EU entry, even as CE marks remain essential for Latin American and Middle-Eastern tenders, amplifying global chessboard complexity.

Drug Eluting Stent Industry Leaders

Abbott Laboratories

Boston Scientific Corporation

Medtronic PLC

Terumo Corporation

Lepu Medical Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Drug Eluting Stent Market Companies Covered in this Report

- Abbott Laboratories

- Alvimedica

- B. Braun

- Balton Sp.z.o.o

- Biosensors International Group, Ltd.

- BIOTRONIK

- Boston Scientific

- Cook Group

- Elixir Medical

- Johnson & Johnson Services LLC

- JW Medical Systems

- Lepu Medical

- Medtronic

- Meril Life Science

- MicroPort

- OrbusNeich Medical

- Sahajanand Medical Technologies Pvt. Ltd.

- Sino Medical Sciences Technology Inc.

- Terumo

- Translumina

Recent Industry Developments in Drug Eluting Stent Market

- January 2026: Boston Scientific won Japanese MHLW approval for its PROMUS Everolimus-Eluting Coronary Stent System, pending imminent reimbursement clearance.

- October 2025: Orchestra BioMed began enrolling the U.S. Virtue SAB trial comparing its sirolimus-infusion balloon with the AGENT paclitaxel-coated comparator for coronary in-stent restenosis.

- June 2025: BIOTRONIK initiated the Leave Nothing Behind study evaluating Pantera Lux drug-coated balloons and Freesolve resorbable magnesium scaffolds versus Orsiro Mission drug-eluting stents in chronic total occlusions.

- May 2025: Boston Scientific received FDA clearance to market TAXUS Liberte Atom Paclitaxel-Eluting Stent for vessels as small as 2.25 mm and announced a full U.S. rollout scheduled for June 2025.

Drug Eluting Stent Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the drug-eluting stent (DES) market as factory-built coronary or peripheral vascular stents that carry an antiproliferative drug on a controlled-release coating and are deployed by catheter to prevent restenosis. According to Mordor Intelligence, this universe generated USD 6.35 billion in revenue during 2025 across five regions and eight product dimensions.

Scope Exclusions: bare-metal stents, fully bioresorbable scaffolds without a drug layer, drug-eluting balloons, and all non-vascular implants are outside this analysis.

Segments Covered in This Report

- By Coating Type

- Durable Polymer-based

- Bioresorbable Polymer-based

- Polymer-free

- By Material

- Cobalt–Chromium Alloy

- Platinum–Chromium Alloy

- Stainless Steel

- Nitinol

- Magnesium Alloy / Composite

- By Drug Type

- Sirolimus & Analogues (Everolimus, Zotarolimus, Biolimus A9)

- Paclitaxel

- Dual-therapy / Combination-drug Stents

- By Application

- Coronary Artery Disease

- Peripheral Artery Disease

- By End User

- Hospitals

- Cardiac Catheterization / PCI Centers

- Ambulatory Surgical Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

We spoke with interventional cardiologists, cath-lab procurement managers, and regulatory officials across North America, Europe, and Asia-Pacific. Their insights on stent mix shifts, polymer adoption, and tender pricing helped us stress-test desk findings and adjust any outlier assumptions before finalizing the baseline.

Desk Research

We began with tier-one public sources such as the US FDA 510(k) database, United States National Inpatient Sample, Eurostat hospital discharges, UN Comtrade shipment data, and peer-reviewed papers from the American Heart Association. To tighten company granularity, our team accessed D&B Hoovers financials and Dow Jones Factiva news transcripts.

Device guidelines from the European Society of Cardiology, statistics from the World Health Organization, and notices from the Indian National Interventional Council aligned nomenclature and current average selling prices. The resources named are illustrative; many other datasets informed screening, validation, and clarification.

Market-Sizing & Forecasting

A top-down model rebuilds global PCI and peripheral angioplasty volumes, then layers stent penetration and weighted average price curves. Selective bottom-up manufacturer revenue roll-ups serve as a reasonableness check. Key variables include procedure growth, stents-per-case ratios, migration to third-generation thin-strut designs, polymer-free uptake, and reimbursement-linked price ceilings. Multivariate regression plus scenario analysis drives the 2026-2030 outlook, while proxy registries fill partial country gaps that are scaled with income-level multipliers validated by experts.

Data Validation & Update Cycle

Outputs pass anomaly filters, independent registry comparisons, and multi-analyst reviews. Mordor analysts refresh models each year and re-open interviews after material approvals, recalls, or policy changes so clients receive an up-to-date view.

How Mordor Intelligence's Drug Eluting Stent Market Size Compares to Other Published Estimates

Published estimates diverge because different firms bundle distinct device types, apply varied price erosion paths, and update on separate calendars. We acknowledge these moving parts up front.

Gaps arise when peripheral DES or drug-eluting balloons are merged into totals, when constant ASPs overstate revenues, or when emerging markets are left unrefreshed for several years. Mordor's disciplined scope, annual refresh, and dual validation through procedure counts and audited revenues minimize such swings and keep our baseline dependable.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.35 B (2025) | Mordor Intelligence | - |

| USD 8.29 B (2025) | Global Consultancy A | Includes drug-eluting balloons and hybrid peripheral stents; relies on static revenue snapshots |

| USD 8.80 B (2024) | Industry Association B | Uses aggregate procedure counts without deducting overlap and applies constant ASPs |

| USD 11.50 B (2025) | Market Publisher C | Bundles all stent types and inflates totals with high inflation-adjusted ASP assumptions |

In summary, our transparent scope selection, recurring primary checks, and balanced top-down plus bottom-up modeling give decision-makers a market view that is traceable, reproducible, and realistically aligned with clinical usage trends.

Key Questions Answered in the Report

How large will the drug-eluting stent market be by 2031?

It is projected to reach USD 13.28 billion by 2031, growing at a 7.03% CAGR from 2027 through 2031.

Which coating type is expanding fastest?

Bioresorbable polymers are pacing a 10.36% CAGR because 12-month degradation curbs late-stent thrombosis.

Why are ambulatory surgical centers gaining share?

CMS reimbursement parity and radial-access protocols enable same-day discharge, lifting ASC volumes at a 9.64% CAGR.

What role does AI play in modern stent deployment?

AI-guided OCT imaging detects malapposition with 92% sensitivity and has reduced repeat revascularization by 14% in early use.

Which region shows the quickest growth?

Asia-Pacific is advancing at a 9.21% CAGR on the back of high procedure volumes and low-cost domestic devices.

Are drug-coated balloons a major threat to stents?

Yes, they now treat 32% of in-stent restenosis cases in the United States after 2024 FDA approval, pressuring repeat-stent placements.

Page last updated on: