Bioabsorbable Stents Market Size and Share

Market Overview

| Study Period | 2023 - 2031 |

|---|---|

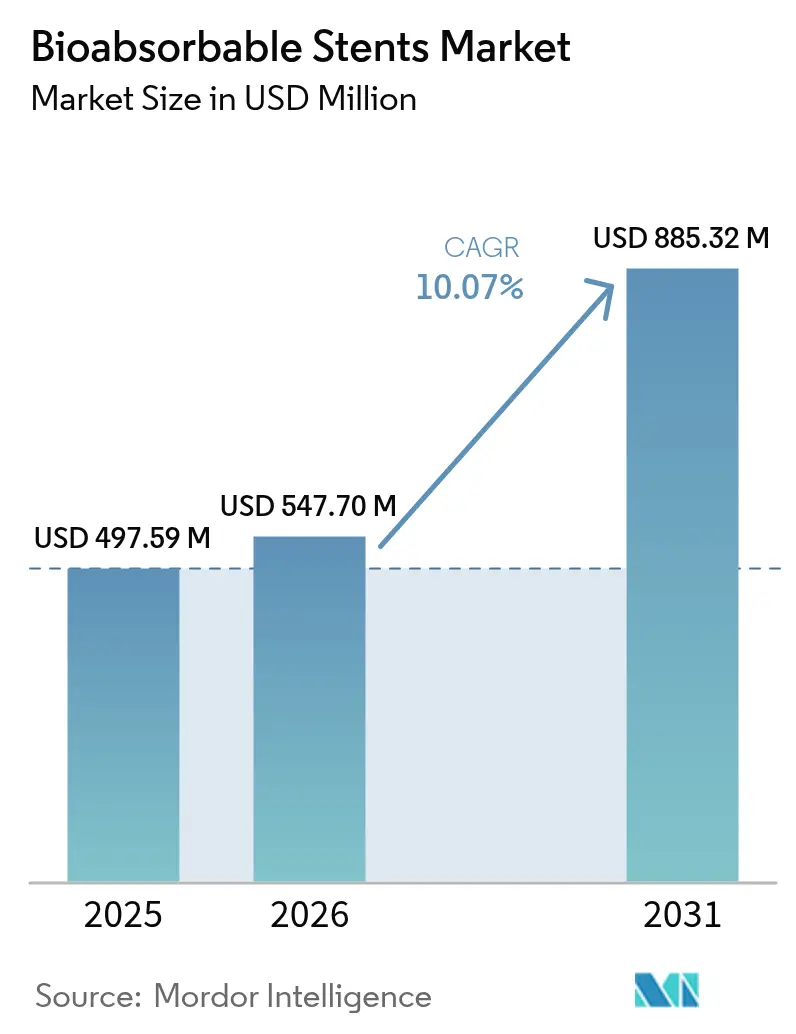

| Market Size (2026) | USD 547.7 Million |

| Market Size (2031) | USD 885.32 Million |

| Growth Rate (2026 - 2031) | 10.07% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bioabsorbable Stents Market Analysis by Mordor Intelligence

The bioabsorbable stents market size is expected to grow from USD 497.59 million in 2025 to USD 547.7 million in 2026 and is forecast to reach USD 885.32 million by 2031 at 10.07% CAGR over 2026-2031. Momentum in the bioabsorbable stents market is shaped by the “leave-nothing-behind” philosophy, a regulatory shift toward expedited approvals for below-the-knee use, and continuous advances in polymer science that allow degradation timelines to mirror vessel healing. Major manufacturers are channeling resources into magnesium-alloy scaffolds that fully dissolve inside 12 months, a milestone that reduces long-term thrombosis risk while supporting vessels during the critical remodeling phase. Hospitals remain the dominant channel, yet high-volume cardiac specialty centers are scaling faster as operators combine AI-guided intravascular imaging with refined deployment techniques. On the supply side, incentives in China and India are lowering average selling prices, broadening access in price-sensitive regions and sharpening global competition.

Key Report Takeaways

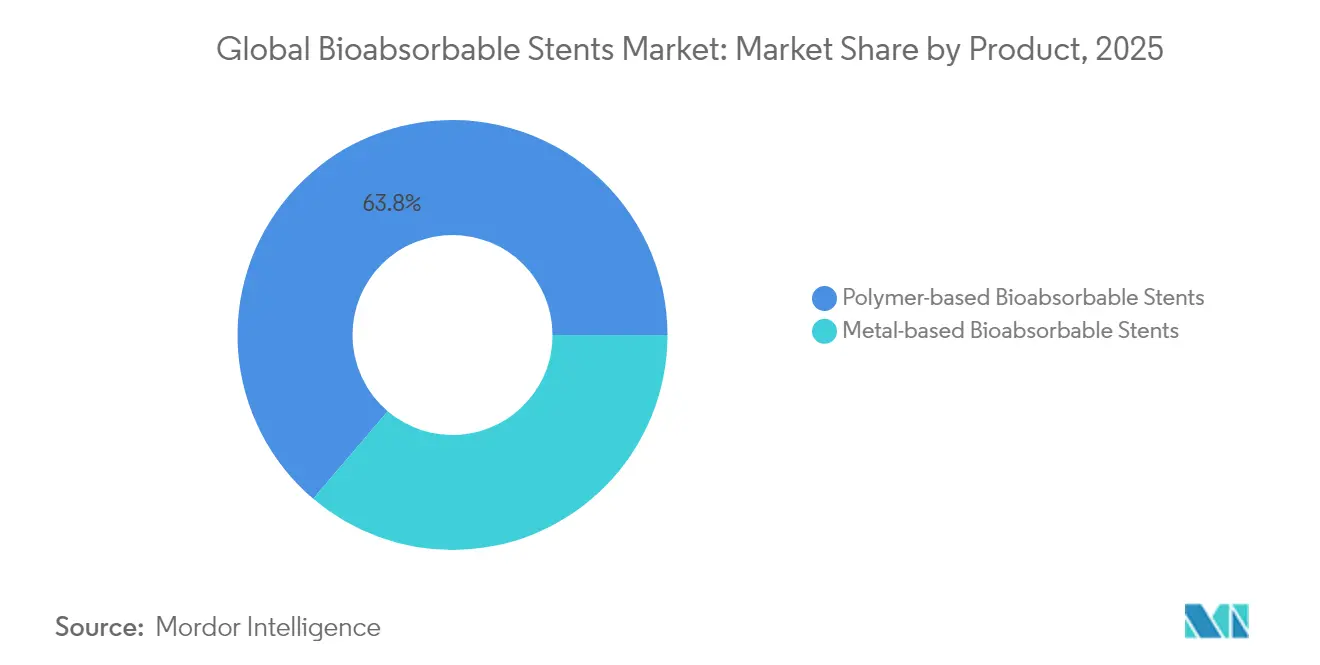

- By product type, polymer-based platforms held 63.78% of bioabsorbable stents market share in 2025 while metal-based systems are forecast to post an 11.18% CAGR through 2031.

- By application, coronary artery disease accounted for 70.62% share of the bioabsorbable stents market size in 2025, whereas peripheral artery disease is expanding at an 11.02% CAGR to 2031.

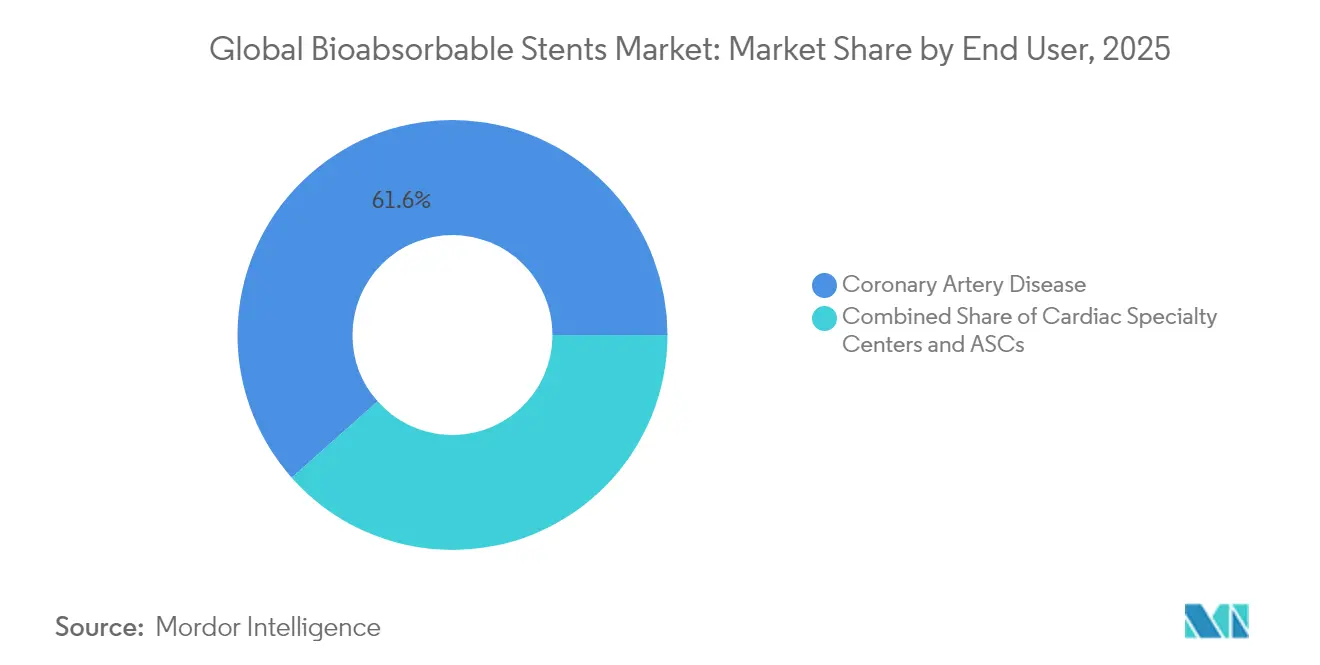

- By end user, hospitals commanded 61.55% of the bioabsorbable stents market size in 2025, while cardiac specialty centers recorded the highest projected CAGR at 11.09% through 2031.

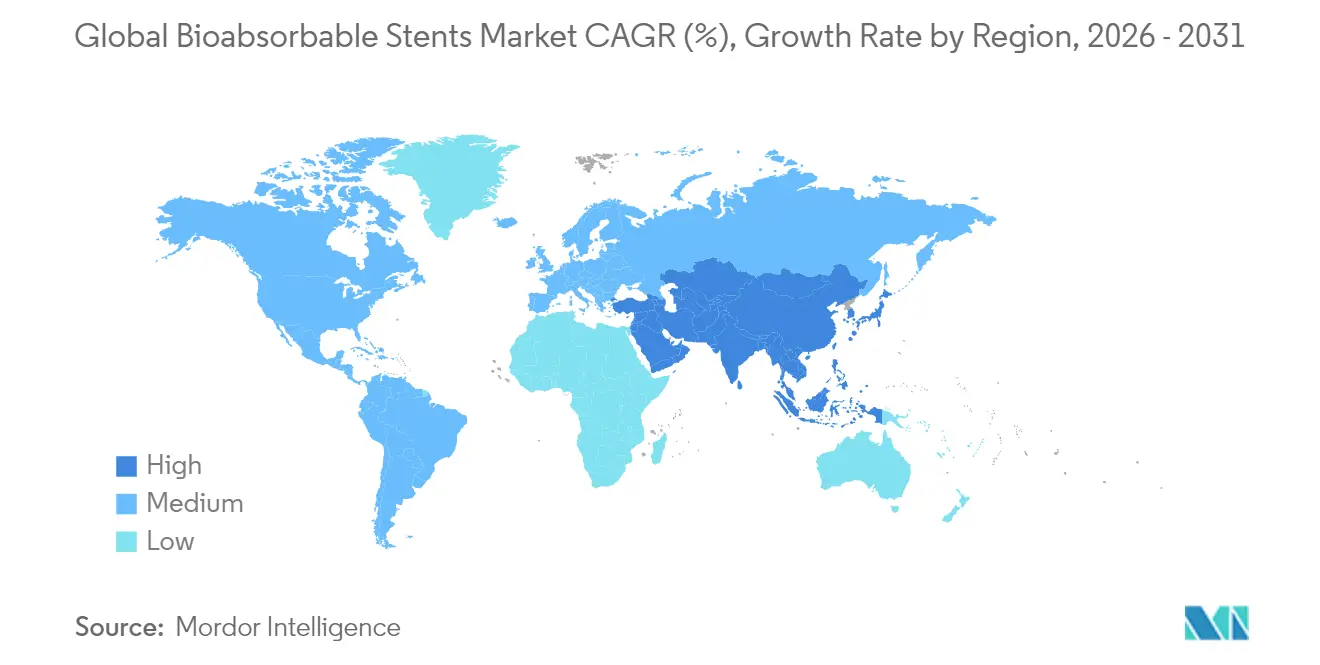

- By geography, North America led with 40.72% of bioabsorbable stents market share in 2025 as Asia-Pacific registers the fastest CAGR of 11.32% to 2031.

- Abbott and Biotronik together captured a double-digit share of the bioabsorbable stents market in 2025, leveraging multi-year outcome datasets to reinforce clinical confidence.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bioabsorbable Stents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid rise in minimally-invasive PCI volumes | +1.8% | Global; peak impact in North America & Europe | Medium term (2-4 years) |

| Shift to “leave-nothing-behind” solutions | +2.1% | Global; led by developed markets | Long term (≥4 years) |

| Fast-tracked below-the-knee BRS approvals | +1.2% | North America & Europe; expanding to Asia-Pacific | Short term (≤2 years) |

| Magnesium-alloy breakthroughs (<12 months) | +1.5% | Global; early adoption in Europe & Asia-Pacific | Medium term (2-4 years) |

| AI-guided intravascular imaging | +0.9% | North America & Europe; gradual uptake in Asia-Pacific | Medium term (2-4 years) |

| Domestic manufacturing incentives | +1.3% | Asia-Pacific core; spillover to Middle East & Latin America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid Rise in Minimally-Invasive PCI Volumes

Surging percutaneous coronary intervention (PCI) volumes stem from aging populations and lifestyle-driven cardiovascular risk. Hospitals worldwide are adopting same-day discharge protocols, making devices that leave no permanent metallic footprint increasingly attractive. As operators emphasize post-procedure vessel physiology, polymer scaffolds that resorb after healing are gaining favor among younger cohorts likely to need future re-interventions. Abbott’s Esprit BTK approval in April 2024 for below-the-knee lesions signaled regulatory acknowledgment of bioabsorbable benefits in complex anatomies[1]Abbott Laboratories, “Esprit BTK Everolimus Eluting Resorbable Scaffold System Clears FDA,” abbott.com. Outpatient migration of PCI further amplifies demand for scaffolds that remove long-term surveillance burdens, reinforcing growth across the bioabsorbable stents market.

Shift from Permanent Metallic DES to “Leave-Nothing-Behind” Solutions

Late stent thrombosis and neoatherosclerosis linked to permanent metallic drug-eluting stents (DES) have intensified interest in fully dissolving alternatives. Clinical studies now document restored vessel compliance and shorter dual-antiplatelet therapy when using bioresorbable technologies. Biotronik’s Freesolve scaffold secured FDA Breakthrough Device Designation in March 2024, underscoring agency support for solutions that eradicate long-term implant risk. Pediatric and young-adult segments, where lifetime device burden matters most, are accelerating the pivot, broadening the addressable base for the bioabsorbable stents market.

Regulators Fast-Tracking Below-the-Knee BRS for CLI Patients

Critical limb ischemia (CLI) carries high morbidity, and metallic stents have struggled in small-caliber tibial arteries. The FDA’s Breakthrough Device pathway grants priority review to bioabsorbable scaffolds targeting CLI, reducing approval timelines by granting direct agency guidance. Abbott’s Esprit BTK victory created a template competitors can follow, rewarding firms with rigorous below-the-knee clinical packages. First-mover advantages are expected to crystallize, carving out specialized revenue pools within the broader bioabsorbable stents market.

Magnesium-Alloy Breakthroughs Enabling Sub-12-Month Scaffold Support

Next-generation magnesium alloys furnish higher radial strength at thin-strut profiles, then resorb completely inside one year. Biotronik’s DREAMS 3G platform reported vessel patency and full scaffold dissolution within 12 months in European trials. Predictable degradation counters the premature recoil seen in first-generation polymer systems, while avoiding the extended presence that once stirred thrombosis fears. The convergence of mechanical integrity and rapid bioresorption sets a new engineering baseline, propelling future adoption.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy of first-generation scaffold thrombosis | -1.4% | Global; highest impact in North America & Europe | Long term (≥4 years) |

| Stringent multi-year clinical-endpoint rules | -0.8% | Global; regulatory stringency varies by region | Medium term (2-4 years) |

| Supply-chain fragility for high-purity PLLA | -0.6% | Global; import-dependent regions most affected | Short term (≤2 years) |

| Reimbursement lag for peripheral BRS | -0.7% | Emerging markets, notably Asia-Pacific & Middle East Africa | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Historical Scaffold Thrombosis Legacy of First-Generation PLLA Devices

After higher thrombosis rates forced withdrawal of Abbott’s Absorb BVS platform, cardiologists demanded stringent post-marketing evidence before adopting newer scaffolds. The ABSORB III five-year data showing late events still echo in risk-benefit discussions[2]L. Redfors et al., “Five-Year Outcomes After Bioresorbable Vascular Scaffold Implantation,” New England Journal of Medicine, nejm.org. Hospitals maintain prolonged dual-antiplatelet therapy to mitigate perceived risk, inflating follow-up costs and dampening uptake. Overcoming this legacy requires consistently favorable trial outcomes and real-world registries that demonstrate parity or superiority to current DES.

Stringent Multi-Year Clinical-Endpoint Requirements

Regulators now insist on target lesion failure and scaffold thrombosis data extending beyond 36 months, extending development timelines and capital requirements. Each material tweak can trigger new pivotal studies, slowing incremental innovation. Smaller firms face financing headwinds, ceding ground to enterprises with the balance sheets necessary to fund multi-region, multi-year trials. While patient safety benefits, the hurdle tempers the entry of new competitors, restraining velocity in the bioabsorbable stents market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Polymer Platforms Drive Innovation

Polymer-based devices accounted for 63.78% of the bioabsorbable stents market size in 2025 and are projected to grow at 10.62% CAGR to 2031. Poly-L-lactic acid scaffolds benefit from matured processing know-how, allowing manufacturers to engineer strut thickness, crystallinity, and drug-elution kinetics to match vessel healing. Over the forecast window, higher molecular weight PLLA grades are expected to lengthen radial support without extending total bioresorption beyond three years, a balance judged optimal for coronary anatomy. Despite entrenched leadership, polymer platforms face intensifying pressure from next-generation metals that promise thinner profiles and shorter resorption.

Metal-based scaffolds, led by magnesium-alloy systems, stand at an earlier part of the adoption curve yet demonstrate robust double-digit expansion prospects. Superior acute hoop strength and fluoroscopic visibility mirror the handling familiarity of metallic DES, easing operator transition. Biotronik’s DREAMS 3G pivotal data showing full scaffold dissolution at 12 months positions this sub-segment as a credible alternative. Commercial momentum will hinge on achieving cost parity with polymer competitors and broadening clinical indications beyond coronary use.

By Application: Peripheral Expansion Accelerates Growth

Coronary artery disease continues to represent 70.62% of bioabsorbable stents market share in 2025, anchored by a voluminous PCI base and established reimbursement frameworks. Five-year follow-ups from large registries underscore acceptable safety, bolstering physician confidence in mainstream lesions. Still, proceduralists often reserve scaffolds for younger patients or bifurcations where permanent metal might complicate future interventions.

Peripheral artery disease delivers the forecast period’s fastest CAGR at 11.02%, catalyzed by April 2024 FDA clearance of Abbott’s Esprit BTK for tibial vessels. Early clinical use shows promising freedom from restenosis in complex below-the-knee anatomy. Physician societies are incorporating bioabsorbable options into CLI management guidelines, a development that will generate sustained volume beyond pilot centers. Expansion into structural and non-vascular uses such as pediatric airway or ureteric strictures remains exploratory but underlines the platform’s versatility.

By End User: Specialty Centers Lead Adoption

Hospitals captured 61.55% of bioabsorbable stents market size in 2025, leveraging integrated catheterization labs and comprehensive postoperative care pathways. Conversion to bioabsorbable technologies is often committee-driven, with formulary inclusion contingent on multi-disciplinary vetting. Adoption levels correlate strongly with availability of adjunct intravascular imaging, a capability more prevalent in tertiary centers.

Cardiac specialty centers are advancing at an 11.09% CAGR through 2031, buoyed by streamlined governance that accelerates device selection and protocol updates. Concentrated procedural volume shortens learning curves, enabling rapid iteration of best practices. AI-augmented software bundled with scaffolds further differentiates specialty providers, enhancing patient acquisition. Ambulatory surgical centers trail but show traction in regions where payors promote same-day PCI to curb inpatient costs.

Geography Analysis

North America led the bioabsorbable stents market with 40.72% share in 2025, a position secured by robust reimbursement and a dense clinical-trial network. FDA’s Breakthrough Device pathway has shortened approval cycles for niche applications, visible in the rapid clearance of Esprit BTK. Even so, payors demand post-market evidence, slowing uptake outside guideline-endorsed coronary lesions. Hospital capital constraints and memories of first-generation scaffold recalls temper aggressive roll-outs, leading to moderate single-digit gains over the forecast window.

Asia-Pacific registers the fastest CAGR at 11.32% through 2031, underpinned by burgeoning cardiovascular disease prevalence and government incentives that cut import tariffs on in-region manufactured scaffolds. Large public tenders in India are shifting procurement to price-volume contracts, expanding device access beyond metropolitan hospitals. Domestic players are forming joint ventures with material science institutes to localize PLLA and magnesium alloy supplies, a move expected to insulate the value chain from geopolitical disruptions. Regulatory agencies in China and Singapore have issued dedicated guidance for fully degradable devices, signaling alignment with international quality benchmarks.

Europe remains a steady growth contributor, drawing on a sophisticated payer framework that ties reimbursement to real-world registry outcomes. Long-term data from German and U.K. investigator-initiated studies are feeding guideline committees, fostering confidence in second-generation devices. Middle East and Africa, while nascent, are allocating funds to cardiovascular center-of-excellence programs that include bioabsorbable platforms in procurement blueprints. Latin America’s private hospital groups are piloting polymer scaffolds in high-income urban populations, setting the stage for broader adoption once insurer coverage widens.

Regulatory Landscape

Bioabsorbable drug-eluting stents are regulated as high-risk implantable combination products in major markets, which keeps approval pathways clinically intensive. In the United States, bioabsorbable drug-eluting coronary stents fall under US FDA Product Code PNY and typically require Premarket Approval (PMA), with sponsors expected to support multi-year clinical endpoint expectations for scaffold thrombosis and target lesion outcomes that shape development timelines and post-market evidence planning.

In Europe, market access is governed by Regulation (EU) 2017/745 (EU MDR), including additional scrutiny for devices incorporating a medicinal substance and related consultation requirements. Across regions, conformity with recognized consensus standards underpins technical files and test strategies, with ISO 25539-2:2020 commonly used to structure performance and safety evaluation of vascular stent systems (including design verification and preclinical testing) before clinical evidence packages are submitted.

Competitive Landscape

The bioabsorbable stents market features moderate consolidation, with the top five suppliers controlling just under 60% of global revenue, resulting in a market concentration score of 6. Abbott, Biotronik, and MicroPort rely on long-view clinical datasets that demonstrate scaffold patency and resorption timelines, differentiating their offerings in tender evaluations. Abbott’s strategy pairs its Esprit platform with Ultreon AI imaging to create a closed procedural loop, driving repeat sales of both hardware and software[4]Abbott Laboratories, “Integrated Imaging and Scaffold Solutions,” abbott.com. Biotronik, by contrast, emphasizes magnesium metallurgy as a proprietary edge, touting the DREAMS series to meet operators’ demand for metal-like handling.

Emerging contenders in Asia-Pacific adopt cost-leadership plays, leveraging government subsidies and local polymer compounding to undercut imported prices. Joint development agreements with university labs are accelerating material iterations without breaching the high capital threshold of multi-region trials. Strategic acquisitions, such as Kaneka’s 2023 purchase of Japan Medical Device Technology, illustrate the scramble for intellectual property that tightens control over next-generation alloys. Competitive intensity is forecast to climb as patent cliffs loom for early polymer formulations, opening white space for challenger brands to remix legacy designs using AI-guided deployment support.

Bioabsorbable Stents Industry Leaders

-

Boston Scientific Corporation

-

Arterius Limited

-

Kyoto Medical Planning Co. Ltd

-

Terumo Corporation

-

Elixir Medical Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Below-the-knee (BTK) peripheral interventions provide a defined commercialization pathway where bioabsorbable scaffolds move from concept to cleared indications. Abbott's April 2024 FDA approval for the Esprit BTK everolimus-eluting resorbable scaffold system is a concrete proof point, since it established a regulator-validated template for CLI-focused clinical packages and creates space for competitors with differentiated degradation profiles or deliverability in small-caliber tibial anatomy.

Asia-Pacific approval activity and local adoption pathways also support opportunity development tied to access and tender dynamics. MicroPort's Firesorb receiving NMPA market approval in July 2024 and Shanghai Bio-Heart Biological Technology reporting NMPA approval for a bioabsorbable drug-eluting stent in July 2026 point to a growing pool of locally approved platforms, which supports price-volume procurement strategies and intensifies regional competition. On technology and clinical practice, wider use of OCT/IVUS and AI-supported PCI workflows aligns with imaging-guided implantation goals to reduce malapposition-linked events, while registry signals of higher short-term thrombosis with off-label use create room for manufacturers to differentiate through indication-specific labeling, standardized sizing protocols, and longer-term real-world evidence generation.

Recent Industry Developments

- May 2026: Elixir Medical announced four-year results from the 445-patient BIOADAPTOR randomized controlled trial for the DynamX Coronary Bioadaptor System, reporting lower target lesion failure versus a comparator drug-eluting stent. The longer follow-up adds to the category narrative on restoring vessel function and provides additional evidence for committees that previously demanded multi-year outcomes after first-generation scaffold concerns.

- October 2025: Elixir Medical reported a prespecified landmark superiority analysis showing a reduction in device-related cardiac events for DynamX versus contemporary drug-eluting stents. The update strengthened differentiation versus permanent metallic DES and supported broader physician engagement around non-permanent, vessel-adaptive implant concepts.

- April 2024: Abbott received FDA approval for the Esprit BTK everolimus-eluting resorbable scaffold system for below-the-knee peripheral artery disease treatment. This milestone expanded regulated use of bioabsorbable scaffolds beyond coronary settings and increased competitive focus on BTK clinical programs and peripheral reimbursement pathways.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from bioabsorbable stents that are implanted to support a narrowed vessel, and then naturally dissolve over time, as counted across the main clinical use settings and geographies.

Scope exclusions: The sizing excludes non-absorbable permanent stents and any stand-alone procedure, imaging, or hospital service fees that are billed separately from the device.

Segmentation Overview

-

By Product

- Polymer-based Bioabsorbable Stents

- Metal-based Bioabsorbable Stents

-

By Application

- Coronary Artery Disease

- Peripheral Artery Disease

- Structural & Non-vascular (e.g., oesophageal, ureteric)

-

By End User

- Hospitals

- Cardiac Specialty Centers

- Ambulatory Surgical Centers

-

By Geography

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- South America

Data Sources, Market Sizing, and Validation

Desk Research

We start by building a demand and supply picture using public sources, and then refine assumptions during fieldwork. For medical devices like stents, the most practical desk inputs are usually procedure volumes and disease burden trends, which help frame the addressable pool before pricing and adoption inputs are applied.

Illustrative sources include CDC and NIH publications for cardiovascular disease indicators, OECD health statistics for utilization patterns, FDA databases for device approvals and safety notices, and WHO and World Bank datasets for population and healthcare spend context. We also review peer-reviewed cardiology journals for shifts in clinical practice, along with investor presentations, annual reports, and reputable press for product pipeline updates and commercialization timelines. In addition, paid subscriptions are used selectively for company financials and intelligence, patent lookups, and shipment-level trade signals where available. These sources are not exhaustive, and additional public documents and datasets were also referenced to collect, cross-check, and clarify the final analysis.

Primary Interviews and Surveys

Next, we validate the model with interviews and structured surveys across the value chain, including clinicians, hospital procurement teams, distributors, and device-side product and regulatory experts. Since adoption differs by region and clinical guidelines, inputs were checked across APAC, EMEA, and the Americas so pricing, approval timing, and utilization assumptions reflect purchase and uptake behavior, not only desk signals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 12% | APAC: 39% |

| Mid tier: 61% | Functional/Unit leaders: 39% | EMEA: 37% |

| Smaller Players: 14% | Managers: 49% | Americas: 24% |

Market-Sizing & Forecasting

Sizing is first constructed using a top-down approach where coronary and peripheral intervention procedure pools are rebuilt from published health statistics, then filtered through the share of cases eligible for absorbable devices. To keep totals realistic, selective bottom-up checks are added using sampled hospital quotes, channel feedback on unit volumes, and implied revenues derived from publicly visible financial commentary, which are then used to adjust outliers.

Key model inputs include interventional cardiology procedure growth, bioabsorbable device penetration rates by setting, average selling price ranges by region, approval and reimbursement timing, and mix shifts between coronary and peripheral use. Because pricing can move with tenders and early-stage adoption, we track discounting patterns and the speed at which new generations replace older designs. Forecasts are produced using scenario analysis, where a base case is informed by expert consensus on adoption constraints and regulatory timing, and then upside and downside cases are stress-tested around procedure recovery and pricing progression. Where bottom-up evidence is thin in smaller countries, gaps are handled by applying region-level adoption curves and then rechecked with local interviews before finalizing.

Data Validation & Update Cycle

Outputs are cross-verified against independent signals such as procedure volumes, regulatory milestones, and observed pricing bands, and then compared with what respondents describe as feasible near-term adoption. Variances are investigated, and if the mismatch is material, assumptions are reopened and the relevant experts are re-contacted for a second pass.

Before sign-off, the model goes through multi-step internal review so unit logic, currency conversions, and year-to-year movements remain consistent. Reports are refreshed annually, and interim updates are made when major approvals, safety actions, or reimbursement shifts change the demand path. Right before delivery, we run a final update check so clients receive the most current view available.

Mordor Intelligence's Bioabsorbable Stent Market Estimate Compared With Other Published Estimates

Published market values for bioabsorbable stents can look far apart because firms do not always use the same base year, they apply different views on how fast adoption expands, and they may count different revenue components.

The biggest drivers are usually what is included as market revenue (device-only versus broader procedure-linked services), how average selling prices are carried forward as volumes scale, and how quickly model inputs are refreshed when approvals or safety notes change demand.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 547.70 M (2026) | |

| Global Research Publisher A | USD 410.00 M (2025) | Uses a manufacturer revenue lens tied to a 2025 base year, which can understate later-year ramp-up when approvals and procurement cycles accelerate, and it may not fully re-rate pricing as mix shifts by region. |

| Industry Research Group B | USD 548.24 M (2024) | Anchors sizing on a 2024 base year and a lower stated growth rate through 2031, which can dampen the effect of procedure growth and penetration gains in faster adopting regions. |

The table shows that part of the spread is timing and what gets treated as market revenue, and in Mordor Intelligence's model the number is device revenue tracked on a 2026 base year with adoption and ASP bands rechecked by region. When those scope and timing choices are held constant, the remaining differences usually come down to penetration speed assumptions and how often they are updated with fresh clinical and procurement feedback.

Key Questions Answered in the Report

What is the projected value of the bioabsorbable stents market by 2031?

The market is forecast to reach USD 885.32 million by 2031, reflecting a 10.07% CAGR from the 2026 base.

Which product type currently leads in unit sales?

Polymer-based platforms held 63.78% share of 2025 revenue, making them the current leader.

Which clinical application is expanding fastest?

Peripheral artery disease applications are advancing at an 11.02% CAGR through 2031, outpacing coronary use.

Why are cardiac specialty centers gaining traction?

High procedural volume, advanced imaging, and streamlined governance enable specialty centers to adopt new scaffold technologies faster than general hospitals.

Which region is expected to show the highest growth?

Asia-Pacific is projected to grow at 11.32% CAGR through 2031 due to manufacturing incentives and increased cardiovascular procedure volumes.

Page last updated on: