Ureteral Stent Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

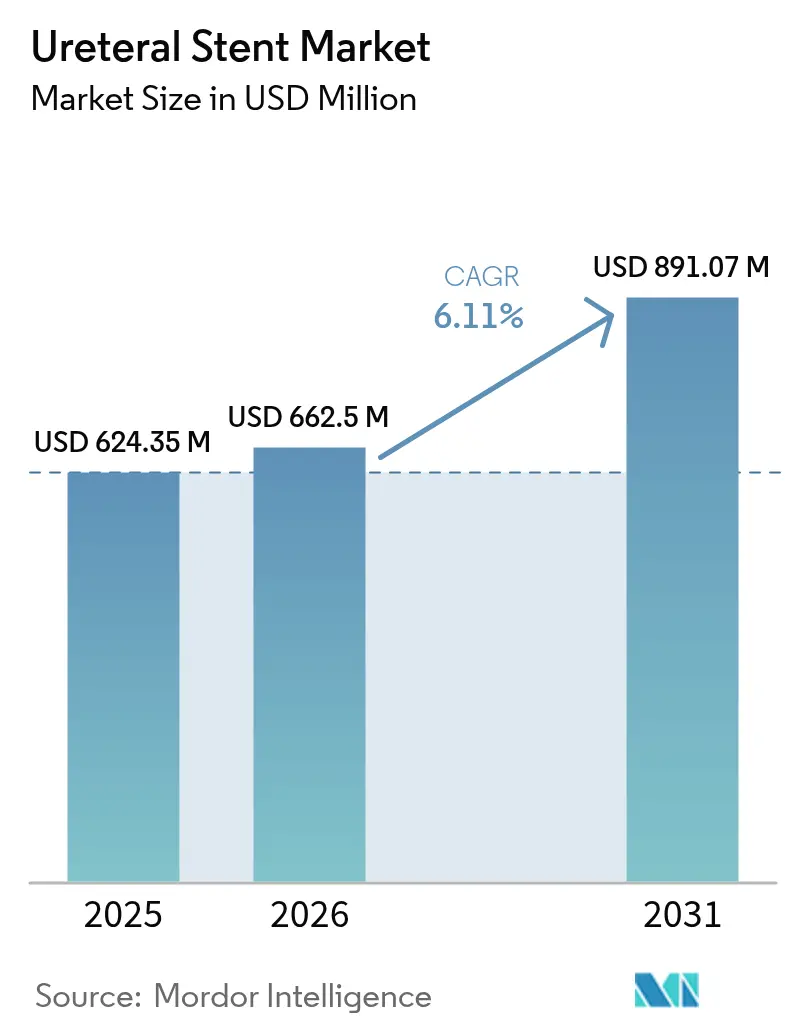

| Market Size (2026) | USD 662.5 Million |

| Market Size (2031) | USD 891.07 Million |

| Growth Rate (2026 - 2031) | 6.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ureteral Stent Market Analysis by Mordor Intelligence

The ureteral stents market size was valued at USD 624.35 million in 2025 and estimated to grow from USD 662.5 million in 2026 to reach USD 891.07 million by 2031, at a CAGR of 6.11% during the forecast period (2026-2031). Biodegradable innovation, accelerated by the FDA’s clearance of the RELIEF stent for vesicoureteral reflux prevention, is reshaping competitive dynamics while simultaneously addressing long-standing concerns around secondary removal procedures. Heightened kidney-stone prevalence—now 9.25% among US adults—expands procedure volumes, especially in women under 60, and pushes manufacturers to refine gender-tailored designs.[1]Hidar Alibrahim, “Kidney Stone Prevalence Among US Population,” JU Open Plus, journals.lww.com Aging demographics intensify demand for less invasive drainage solutions, encouraging healthcare systems to shift complex cases into efficient ambulatory surgical centers. Material science breakthroughs—from anti-encrustation nano-coatings to radiopaque biodegradable polymers—strengthen product differentiation, while AI-guided placement systems improve first-time accuracy and reduce revision rates.[2]U.S. Food and Drug Administration, “2024 Device Approvals,” fda.gov Strategic consolidation continues as large device makers acquire niche innovators, exemplified by Teleflex’s EUR 760 million purchase of BIOTRONIK’s vascular intervention unit to broaden urology cross-selling potential.

Key Report Takeaways

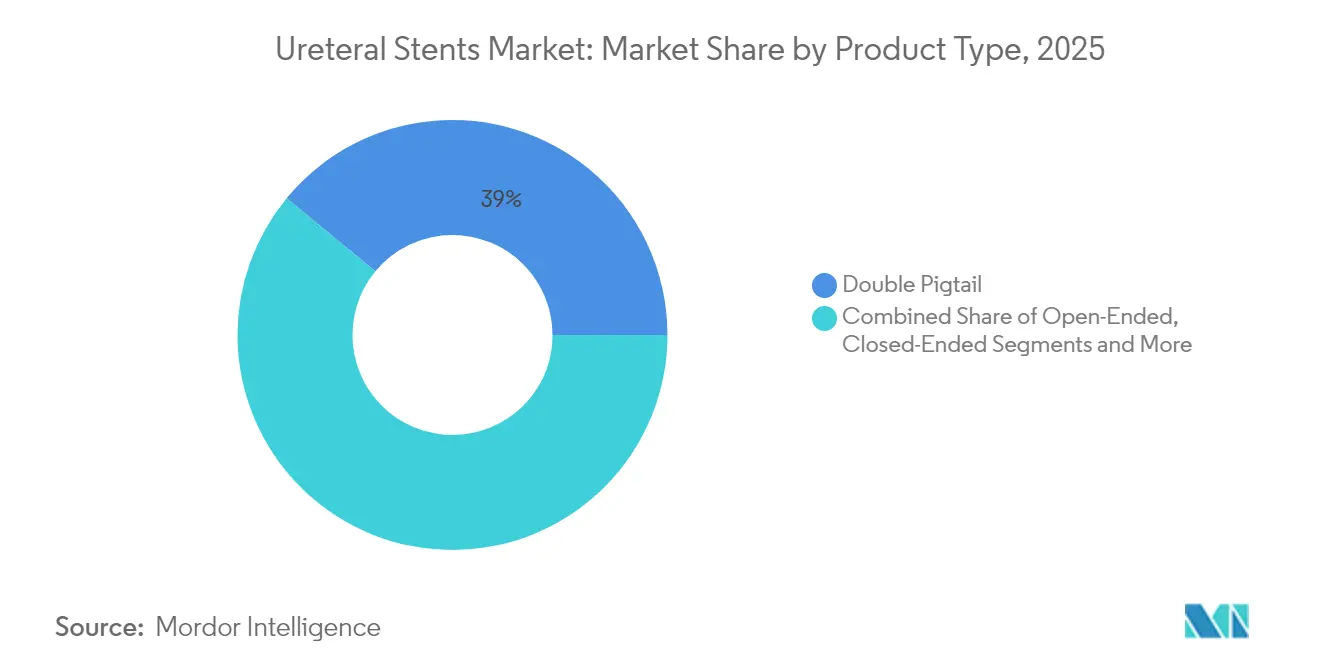

- By product type, double pigtail stents led with 39.02% of ureteral stents market share in 2025, whereas biodegradable designs are advancing at a 10.04% CAGR to 2031.

- By material, polyurethane accounted for 41.85% share of the ureteral stents market size in 2025, while biodegradable polymers are expanding at an 10.48% CAGR through 2031.

- By coating, hydrophilic variants captured 42.78% revenue in 2025; anti-encrustation nano-coated alternatives hold the highest projected CAGR at 7.83% to 2031.

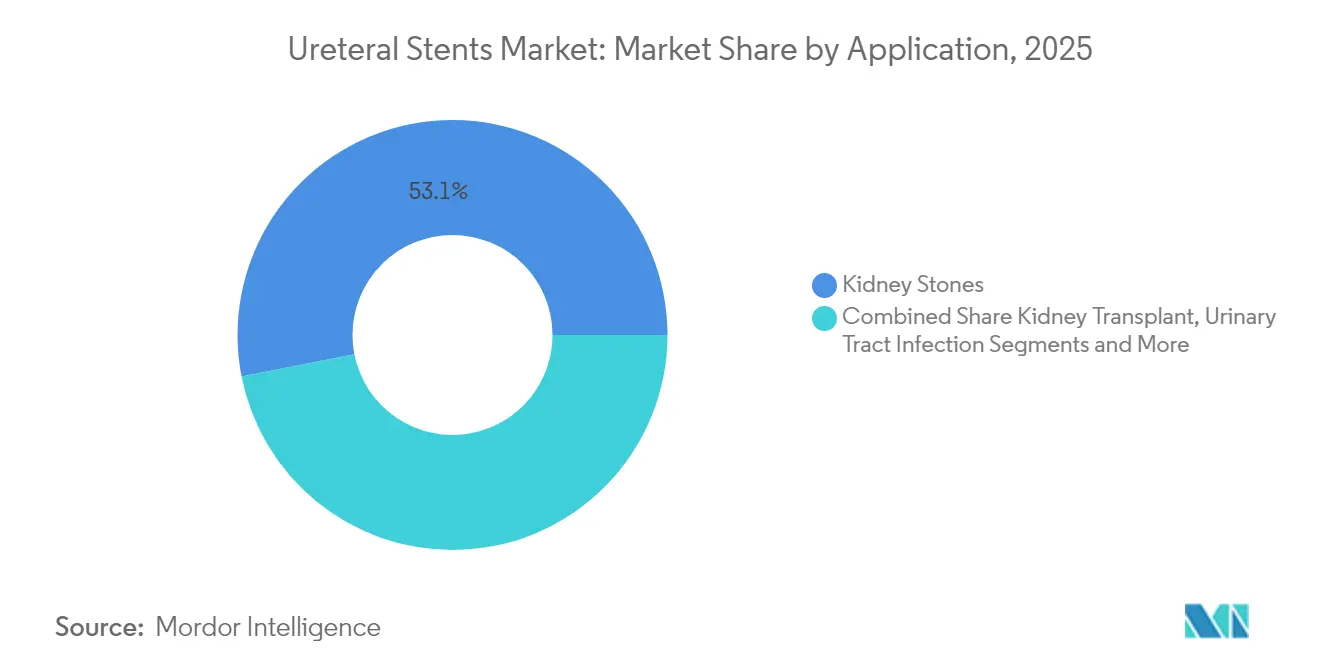

- By application, kidney-stone management represented 53.10% of the ureteral stents market size in 2025; tumor-related procedures are forecast to rise at an 8.35% CAGR.

- By end user, hospitals held 58.92% of ureteral stents market share in 2025, while ambulatory surgical centers are set to grow at 7.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ureteral Stent Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden Of Urological Disorders | +1.2% | Global, with higher impact in North America & Europe | Long term (≥ 4 years) |

| Ageing Population-Linked Urological Surgeries Surge | +1.8% | Global, concentrated in developed regions | Long term (≥ 4 years) |

| Increasing Research and Development for Material & Coating Innovations | +0.9% | North America & EU leading, APAC following | Medium term (2-4 years) |

| Increased Adoption and Launch Of Biodegradable/Bioresorbable Stents | +1.1% | Global, early adoption in North America | Medium term (2-4 years) |

| AI-Guided Sizing & Placement Reducing Revision Rates | +0.7% | North America & EU, gradual APAC adoption | Short term (≤ 2 years) |

| Day-Care Ureteroscopy Growth In ASCs | +0.9% | North America primarily, expanding to EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Urological Disorders

Kidney-stone disease now affects 9.25% of US adults, with the sharpest gains in women under 60—a demographic shift prompting gender-specific stent design refinement.[1]Hidar Alibrahim, “Kidney Stone Prevalence Among US Population,” JU Open Plus, journals.lww.comObesity-linked metabolic changes accelerate stone formation in younger populations, creating a sustained pipeline of preventive stenting procedures. Chronic kidney disease correlates strongly with retained devices; 30.6% of patients with forgotten stents develop CKD versus 8.3% when timely removal occurs, nudging clinicians toward long-dwell, biocompatible options. These epidemiological realities underpin steady procedural growth and motivate manufacturers to deliver designs that maintain drainage while minimizing encrustation over extended durations.

Ageing Population-Linked Urological Surgeries Surge

Roughly 14.53% of older adults now experience renal stones, yet octogenarian treatment outcomes match younger cohorts, validating ureteroscopy coupled with stenting for frail patients. Initial stone-free rates reach 88% and rise to 97% after ancillary therapy, while complications remain near 9%, reinforcing preference for biodegradable stents that negate second interventions. Frailty assessments show a 1.731-fold greater kidney-stone risk, encouraging preventive drainage strategies for vulnerable seniors. Geriatric urology programs are standardizing anesthesia and recovery protocols to accommodate reduced physiological reserves, positioning temporary, dissolvable implants as a default option.

Increasing Research and Development for Material & Coating Innovations

Advanced coatings such as Percushield and pHreeCoat cut calcium and magnesium adherence relative to traditional Hydroplus layers, directly addressing the 80.8% encrustation prevalence in forgotten stents. FDA draft guidance on chemical analysis tightens biocompatibility testing, accelerating the shift toward low-extractable polymers. Nano-engineered anti-encrustation surfaces show 8.12% CAGR, and drug-eluting designs that release antibiofilm agents are moving from bench to bedside. Radiopaque additives integrated into biodegradable matrices enable clinicians to track in-vivo degradation on routine imaging, solving a prior visibility barrier.

Increased Adoption and Launch of Biodegradable/Bioresorbable Stents

Biodegradable models are expanding at a 10.57% CAGR, proving clinically equivalent while sparing patients the discomfort and cost of removal. PLA and PLA/PHB 3-D-printed geometries allow bespoke sizing for complex anatomies, and regulatory clarity arrived when the FDA recognized ASTM F2579-18 for lactide-based resins. Early tracheal-stent data showing 89.7% two-month effectiveness build confidence for urological adaptation. Liquid-injection molding is scaling production without sacrificing sterility, while combined drug-delivery variants promise simultaneous mechanical relief and localized therapy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infection & Encrustation Risks | -0.8% | Global, higher impact in regions with limited follow-up care | Long term (≥ 4 years) |

| Patient Discomfort / Stent-Related Symptoms | -0.6% | Global, particularly affecting quality-conscious markets | Medium term (2-4 years) |

| Supply-Chain Shortage Of Medical-Grade Silicones | -0.9% | Global, concentrated impact in manufacturing hubs | Short term (≤ 2 years) |

| Regulatory Scrutiny On Biodegradable By-Products | -0.4% | North America & EU primarily, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Infection & Encrustation Risks

Encrustation afflicts 80.8% of forgotten stents and drives a 40.2% UTI incidence, while risk escalates from 18.33% at 5 weeks to 75% beyond 12 weeks, underscoring the need for timely exchange or resorbable options. Prolonged pre-operative dwell exceeding two months multiplies post-ureteroscopy infection risk nearly fourfold. Even visually clean devices may harbor internal crystalline blockage, necessitating emergency intervention and prompting R&D toward antimicrobial coatings that disrupt biofilm formation.

Patient Discomfort / Stent-Related Symptoms

Traditional double-J devices cause vesicoureteral reflux in 63% of cases versus none for the RELIEF design, highlighting symptom-relief potential through engineering refinement.[3]Ansley Kelm, “The RELIEF Ureteral Stent Secures FDA Clearance,” University Hospitals News, news.uhhospitals.orgComplete intraureteral placement significantly lowers pain scores for normotensive and diabetic cohorts alike. Quality-of-life impacts extend to sexual function, creating adherence challenges unless next-generation devices minimize irritation. Stent-on-string solutions enable patient self-removal and shorten clinic visits, though small dislodgment risks demand careful selection protocols.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Double Pigtail Dominance Faces Biodegradable Challenge

Double pigtail devices retained 39.02% ureteral stents market share in 2025 because clinicians appreciate their reliable drainage and straightforward placement. Yet biodegradable alternatives are growing 10.04% annually as hospitals focus on single-procedure care pathways that boost throughput and patient satisfaction. Open-ended and closed-ended configurations remain niche, reserved for anatomically complex cases or strictures needing directional flow control. Metallic stents serve malignant obstruction needs, with the Allium system delivering 59.5% functional survival and a 22-month median patency despite notable migration.

Biodegradable innovations address core drawbacks of traditional products. PLA/PGA blends withstand early postoperative forces before dissolving into CO₂ and water, limiting chronic irritation. Hybrid constructs combine self-expanding metal frames with resorbable coverings to unite long-term radial force with eventual lumen restoration. Patient-specific 3-D-printed geometries reduce migration by matching ureteral curvature, aligning with the ureteral stents market trend toward customized therapy at scale.

By Material: Biodegradable Polymers Reshape Traditional Hierarchies

Polyurethane held 41.85% of the ureteral stents market size in 2025 thanks to decades of clinical familiarity and balanced flexibility. However, biodegradable materials exhibit an 10.48% CAGR because payers reward avoidance of second procedures. Silicone continues to dominate extended indwelling cases, valued for smoothness and low encrustation propensity, yet supply-chain shortages of medical-grade grades prompt diversification toward liquid-silicone-rubber variants produced closer to point of care.

Composite designs integrate radiopaque fillers within biodegradable matrices, ensuring visibility without permanent residue. Metal-polymer hybrids exploit nitinol’s elasticity while providing resorbable luminal scaffolding. As ASTM F2579-18 standardization streamlines FDA review, manufacturers accelerate launches, reinforcing a structural change in the ureteral stents market where temporary function replaces permanent implantation.

By Coating/Technology: Anti-Encrustation Innovation Drives Growth

Hydrophilic coatings captured 42.78% revenue in 2025 by easing insertion and lowering friction. Anti-encrustation nano-coatings now expand at 7.83% CAGR, addressing the central pain point of mineral buildup. Early data show Percushield surfaces slashing calcium precipitation, prolonging safe indwelling times without extra systemic antibiotics. Drug-eluting profiles migrate from cardiology, with controlled gentamicin or heparin release targeting infection and thrombosis in situ.

Future-ready designs marry pH-responsive chemistries with intelligent sensors that flag early obstruction signs to cloud-based dashboards. Such convergence mirrors broader ureteral stents market pressures where device makers must pair hardware with data analytics to win procurement contracts emphasizing outcome-based reimbursement.

By Application: Tumor Treatment Emerges as High-Growth Segment

Kidney-stone intervention still delivered 53.10% of ureteral stents market revenue in 2025 because of high prevalence and recurring episodes. Meanwhile, tumor-related drainage shows an 8.35% CAGR as rising cancer survivorship demands durable patency without repeated anesthetic exposure. Post-ureteroscopy recovery benefits from slimline, lubricious stents that reduce hematuria and expedite discharge in ambulatory centers.

In transplant surgery, biodegradable scaffolds protect delicate anastomoses during vascular reperfusion before vanishing to curb infection. AI-guided sizing tools predict optimal diameter based on CT datasets, lowering post-graft obstruction rates. These advances align with payer preference for evidence-based care, solidifying the ureteral stents market’s evolution toward precision-engineered, condition-specific solutions.

By End User: ASC Growth Reshapes Care Delivery Models

Hospitals commanded 58.92% ureteral stents market share in 2025, yet procedure migration to ambulatory surgical centers is advancing 7.18% per year. Urology-focused ASCs execute 95% of cases under 25 CPT codes, achieving predictable scheduling and reduced overhead. Specialty clinics bridge accessibility gaps, especially in rural areas where hospital urologists are scarce but demand for quick stone relief persists.

Patient-led home-care scenarios emerge as stent-on-string models gain traction, offering self-removal and lowering clinic loads. Reimbursement incentives tied to site neutrality may accelerate this trend, underscoring how care-setting flexibility is integral to future ureteral stents market expansion.

Geography Analysis

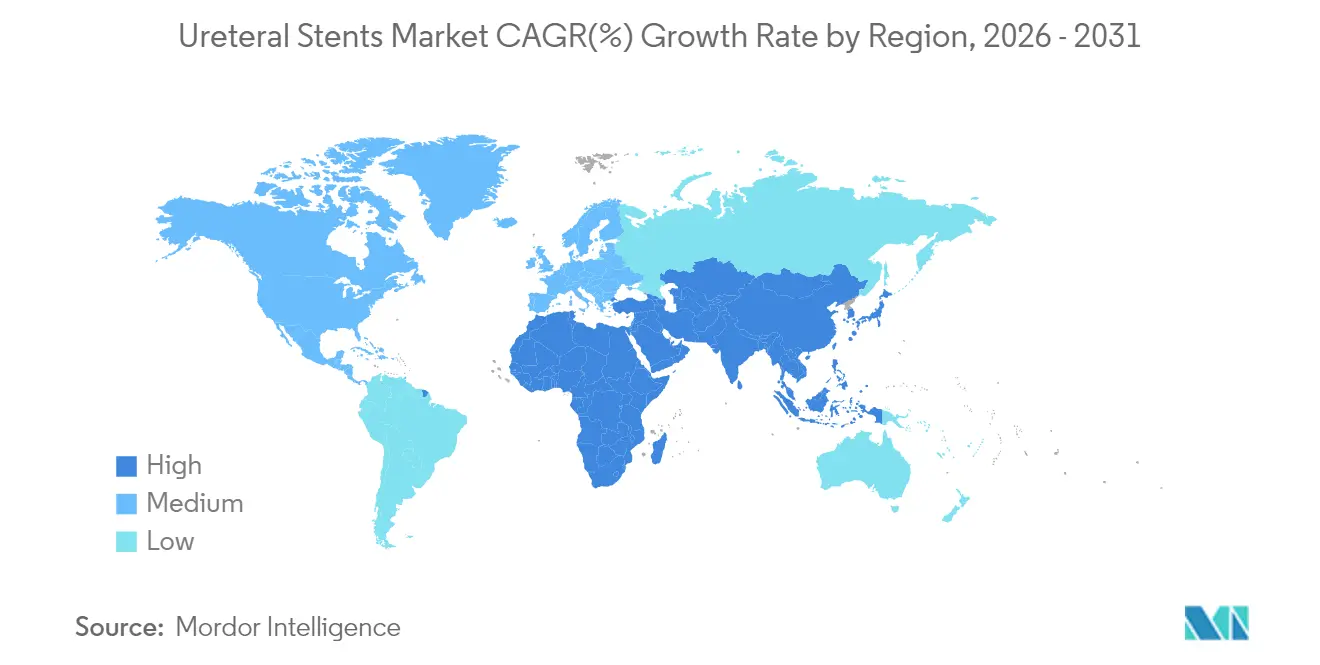

North America held 36.85% ureteral stents market share in 2025, powered by robust reimbursement, established procedural pathways, and early adoption of designs such as the RELIEF stent for reflux prevention. Kidney-stone incidence at 9.25% fuels volume, while ASC penetration improves throughput and patient convenience. Regional supply-chain resilience remains top-of-mind after pandemic-era shortages exposed vulnerabilities in medical-grade silicone sourcing.

Asia-Pacific registers the fastest 7.92% CAGR, reflecting healthcare modernization, aging societies in Japan and South Korea, and expanding insurance coverage throughout China and India. Regulatory harmonization across ASEAN lowers approval barriers, and domestic manufacturing plants shorten lead times, making advanced stents accessible to price-sensitive markets. Telemedicine adoption aids post-procedure follow-up across wide geographies, mitigating rural access gaps.

Europe grows steadily under universal healthcare but navigates a complex regulatory landscape that can slow novel-device rollouts. EMA scrutiny of biodegradable-by-product safety imposes rigorous, expensive trials, though academic-center collaborations support evidence generation. Cost-effectiveness remains pivotal; thus, technologies showing tangible savings—such as eliminating removal procedures—gain faster traction. Brexit-related logistics disruption persists, yet established supplier relationships deliver stability.

Competitive Landscape

The ureteral stents market is moderately fragmented. Boston Scientific notched 23.5% urology-segment growth in Q1 2025, leveraging broad portfolios plus data-backed performance messaging. Its USD 3.7 billion Axonics acquisition augments pelvic-health overlap, fortifying cross-selling channels. Teleflex’s EUR 760 million BIOTRONIK buy and impending corporate split illustrate a push toward focused, innovation-centric business models investors.

Technological differentiation outweighs cost competition: AI-guided placement, anti-encrustation nano-coatings, and biodegradable matrices represent key battlegrounds. FDA’s first-in-class approvals (e.g., RELIEF) offer strong marketing moats, prompting rivals to fast-track comparable innovations. Smaller firms exploit additive manufacturing expertise to supply patient-specific stents, carving niches despite limited scale. Digital-health integration deepens competitive complexity, as outcome-tracking software bundled with hardware can secure value-based contracts.

Supply-chain security shapes procurement decisions after silicone shortages highlighted dependence on narrow supplier bases. Players investing in diversified materials and regional production earn credibility with hospitals optimizing resilience. Overall, heightened R&D spend and merger activity signal sustained transformation of the ureteral stents market.

Ureteral Stent Industry Leaders

Beckton, Dickinson and Company

Boston Scientific Corporation

B. Braun Melsungen AG

Cook Medical LLC

Coloplast A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: University Hospitals secured FDA clearance for the RELIEF ureteral stent, the first device approved to prevent vesicoureteral reflux

- May 2024: Dornier MedTech launched UroGPT, an AI tool that educates kidney-stone patients on treatment options

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the ureteral stents market as the value generated by new, single-use or short-term indwelling tubes designed to maintain urine flow between kidney and bladder after obstruction-relieving or reconstructive procedures. The scope spans polymer, hybrid, and metal devices sold to hospitals and ambulatory surgical centers for kidney-stone, tumor, transplant, and post-lithotripsy care.

Scope exclusion: external drainage catheters, nephrostomy tubes, and vascular stents are not counted.

Segmentation Overview

- By Product Type

- Double Pigtail

- Open-Ended

- Closed-Ended

- Multiloop

- Biodegradable/Bioresorbable

- Metallic

- By Material

- Polyurethane

- Silicone

- Metal (Nitinol/Stainless)

- Biodegradable Polymers (PLA/PGA)

- Hybrid/Composite

- By Coating / Technology

- Hydrophilic-Coated

- Drug-Eluting

- Anti-Encrustation Nano-coated

- Radiopaque / Imaging-Enhanced

- By Application

- Kidney Stones (Urolithiasis)

- Kidney Transplant

- Urinary Tract Infection / Obstruction

- Tumors / Malignancies

- Post-Ureteroscopy / Post-Surgery

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Urology Clinics

- Home-Care Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted interviews with practicing urologists, supply-chain managers, and operating-room buyers across North America, Europe, and key Asia-Pacific economies. Conversations validated procedure-to-stent ratios, confirmed average selling prices, and clarified adoption timelines for biodegradable and coated variants.

Desk Research

We began with structured searches across public datasets such as the US CDC National Health Interview Survey, Eurostat hospital procedure files, WHO Global Health Observatory, and UN Comtrade trade codes for HS 901890. Clinical evidence from PubMed and urology society journals helped map guideline-driven stent placement volumes. Company 10-Ks, FDA 510(k) clearances, and tender portals like Tenders Info added pricing fingerprints, while Questel patent analytics illustrated technology diffusion. These sources, together with other respected references consulted but not exhaustively listed here, provided baseline parameters.

Market-Sizing & Forecasting

A top-down construct starts with kidney-stone, transplant, and stricture procedure counts, which are then multiplied by empirically derived stent usage rates and ASPs. Select bottom-up cross-checks, supplier shipment roll-ups, and sampled hospital purchase orders calibrate country totals before regional aggregation. Core variables include kidney-stone incidence, ureteroscopy penetration, polymer price trends, reimbursement movements, and hospital bed additions. We forecast with multivariate regression blended with scenario analysis to reflect shifts in coating technology uptake and outpatient migration. Where bottom-up evidence is sparse, gap factors are transparently flagged and adjusted during peer review.

Data Validation & Update Cycle

Outputs pass a two-step analyst audit, variance checks against independent indicators (trade volumes, material costs), and senior review. Mordor refreshes every twelve months and issues interim updates when recalls, major approvals, or reimbursement resets materially impact the baseline.

Why Mordor's Ureteral Stents Market Baseline Commands Reliability

Published figures diverge because researchers pick different device mixes, geographic cuts, and refresh cadences. By anchoring volumes to verifiable surgical datasets and cross-testing with supplier evidence, we offer buyers a decision-ready midpoint.

Key gap drivers include: some publishers fold nephrostomy tubes into totals, others exclude emerging biodegradable models; a few inflate demand by applying list rather than transaction prices; cadence differences further widen spreads when fast-growing Asia-Pacific sales are under-sampled.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 624.35 M (2025) | Mordor Intelligence | - |

| USD 575.54 M (2024) | Regional Consultancy A | Earlier base year and narrower material scope |

| USD 611.10 M (2025) | Global Consultancy B | Omits biodegradable stents and relies on trade proxies only |

| USD 693.42 M (2025) | Trade Journal C | Bundles nephrostomy catheters; applies uniform global ASP |

The comparison shows that once scope, price realism, and timely refresh are equalized, Mordor's number sits at the defensible center of industry evidence, giving stakeholders a transparent, reproducible baseline for planning.

Key Questions Answered in the Report

What is the current size of the ureteral stents market?

The ureteral stents market is valued at USD 662.5 million in 2026 and is projected to reach USD 891.07 million by 2031.

Why are biodegradable ureteral stents gaining popularity?

They match traditional devices’ drainage performance while dissolving naturally, sparing patients a second removal procedure and lowering overall treatment costs.

Which region is expanding fastest?

Asia-Pacific leads with an 7.92% CAGR, driven by healthcare modernization and broader insurance coverage.

What segment holds the largest ureteral stents market share?

Double pigtail stents dominate with 39.02% revenue share in 2025.

How are AI technologies influencing stent placement?

AI-guided systems improve sizing accuracy, reduce revision rates, and cut radiation exposure during procedures, enhancing patient safety and procedural efficiency.

What are the chief restraints on market growth?

High infection and encrustation risks, along with patient discomfort from traditional stent designs, moderate overall expansion despite technological advances.

Page last updated on: