Drug Eluting Balloons Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

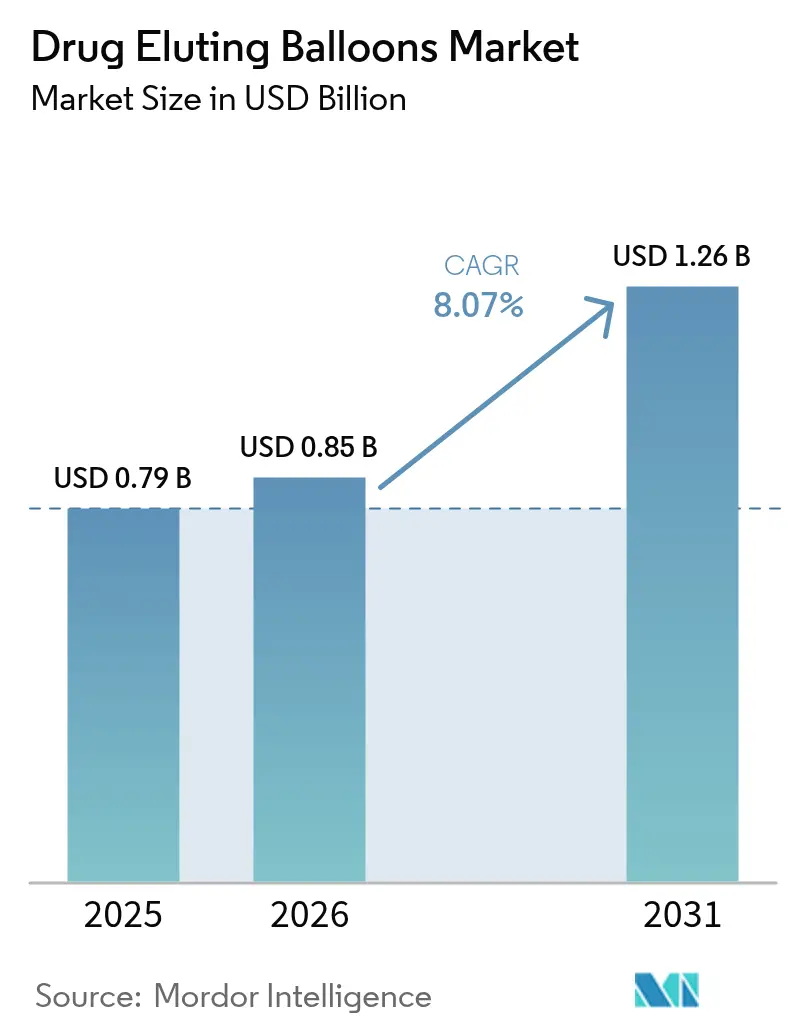

| Market Size (2026) | USD 0.85 Billion |

| Market Size (2031) | USD 1.26 Billion |

| Growth Rate (2026 - 2031) | 8.07% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

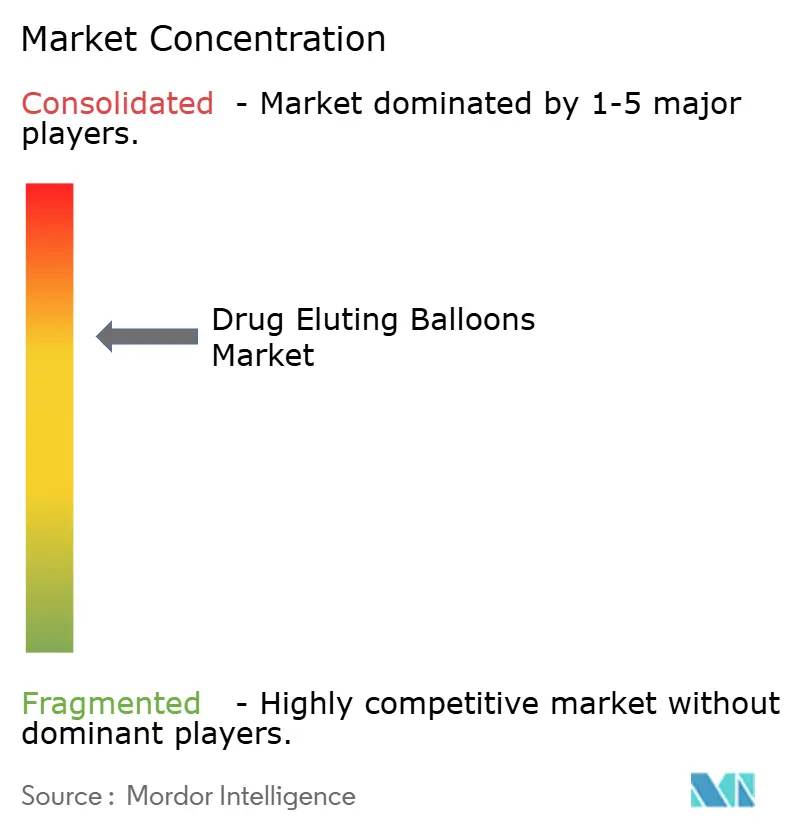

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Drug Eluting Balloons Market Analysis by Mordor Intelligence

Drug Eluting Balloons market size in 2026 is estimated at USD 853.75 million, growing from 2025 value of USD 0.79 billion with 2031 projections showing USD 1.26 billion, growing at 8.07% CAGR over 2026-2031. Accelerated regulatory clearances, expanding reimbursement clarity, and rising cardiovascular procedure volumes continue to shift physician preference from niche in-stent restenosis adjuncts toward mainstream revascularization tools. Paclitaxel formulations still dominate volumes, yet sirolimus platforms gain momentum as long-term safety data accumulate. Ambulatory surgery centers (ASCs) emerge as attractive care settings because drug-eluting balloons (DEBs) allow same-day discharge without permanent implants, aligning with value-based purchasing mandates. The technology’s expanding clinical evidence across coronary, femoropopliteal, and below-the-knee (BTK) territories positions the drug eluting balloon market for steady double-digit revenue upside through the decade.

Key Report Takeaways

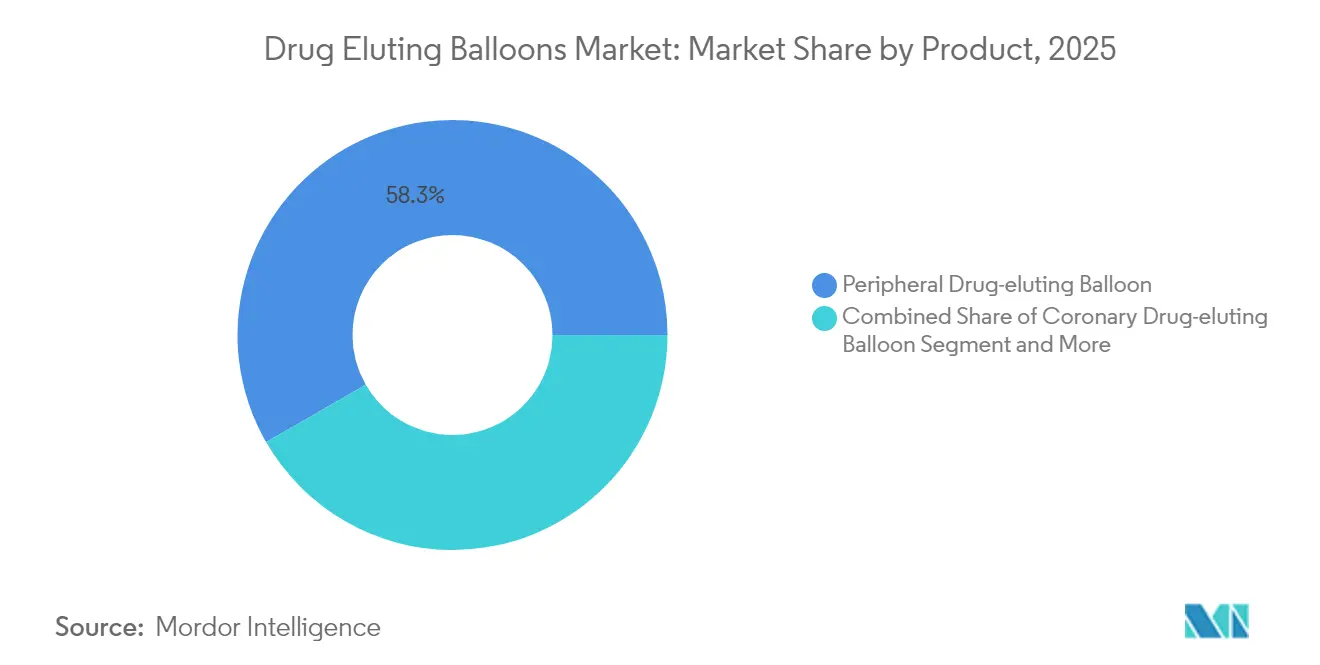

- By product, peripheral balloons held 58.30% of the drug eluting balloon market share in 2025, while coronary balloons are projected to post the quickest expansion at a 9.65% CAGR through 2031.

- By drug type, paclitaxel-based balloons controlled 78.45% of 2025 revenue, whereas sirolimus formulations are expected to advance at a 9.32% CAGR to 2031.

- By coating technology, FreePac claimed 39.70% share in 2025, yet TransPac is forecast to rise at a 9.45% CAGR during the outlook period.

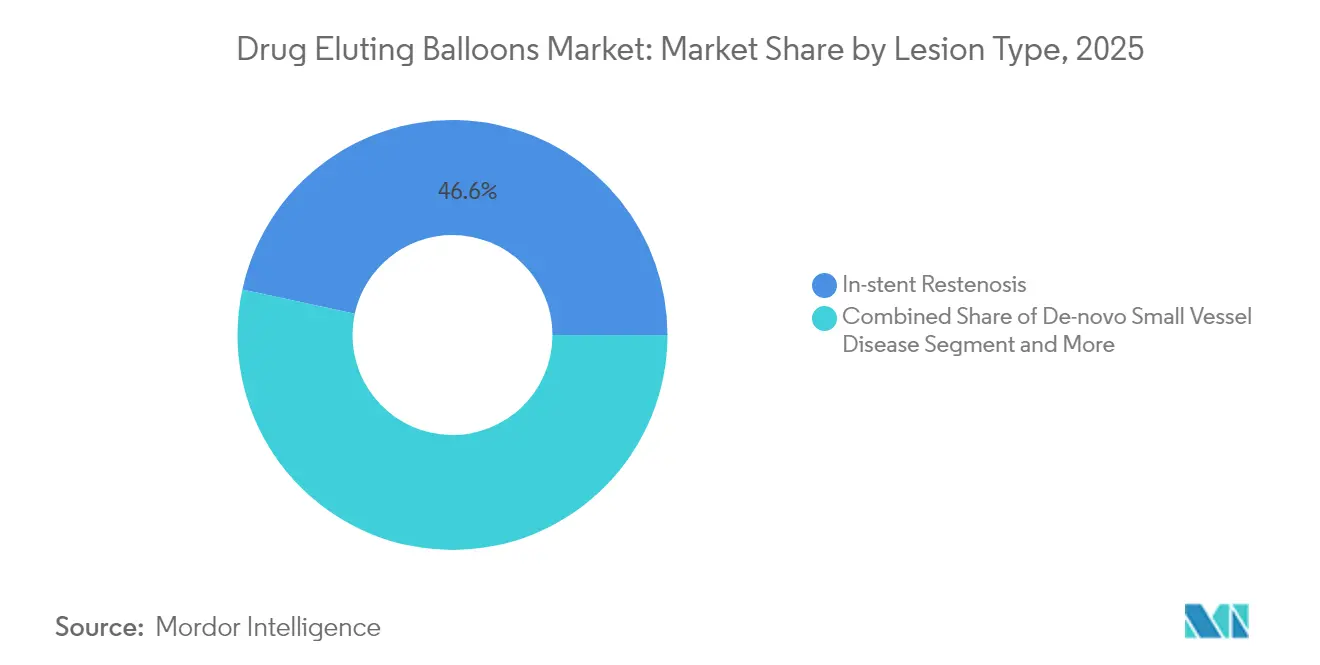

- By lesion type, in-stent restenosis accounted for 46.60% of 2025 cases, while BTK lesions should register the strongest 8.64% CAGR to 2031.

- By end user, hospitals captured 48.75% of 2025 procedures, whereas ASCs are poised to expand at a 9.85% CAGR through 2031.

- By geography, North America contributed 42.10% revenue in 2025, whereas Asia-Pacific is predicted to deliver the highest 10.05% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Drug Eluting Balloons Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Prevalence of Peripheral & Coronary Artery Diseases | +1.8% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Rising Geriatric Population & Cardiovascular Risk | +1.5% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Increasing Adoption of Sirolimus-Coated Balloon Platforms | +1.2% | APAC core, spill-over to North America & Europe | Medium term (2-4 years) |

| Emerging Clinical Data Supporting De-Novo Small-Vessel PCI Use | +1.0% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Regulatory Fast-Tracking of Breakthrough Peripheral DCB Devices | +0.8% | North America & EU regulatory jurisdictions | Short term (≤ 2 years) |

| Shift Toward Day-Case Endovascular Procedures Reducing Hospital Costs | +0.9% | North America & EU, early adoption in urban APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Peripheral & Coronary Artery Diseases

Ischemic heart disease remains the leading source of age-standardized disability worldwide, and absolute case volumes keep rising because population growth offsets mortality gains. As multi-vessel disease burdens older, more-comorbid patients, clinicians require revascularization modalities that minimize vessel trauma and shorten pharmacotherapy. Drug eluting balloon market adoption benefits because DEBs deliver antiproliferative drugs without leaving metal scaffolds, reducing repeat-intervention risk in tortuous or heavily calcified segments. BTK disease, historically underserved, sees particular gains as DEBs demonstrate limb-salvage advantages over plain angioplasty.[1]Source: Amane Kozuki, “SELUTION SFA Japan Trial,” Journal of the American College of Cardiology, jacc.org

Rising Geriatric Population & Cardiovascular Risk

Patients ≥65 years now represent the fastest-growing cohort undergoing percutaneous interventions, yet they carry heightened bleeding risk and intolerance to prolonged dual antiplatelet regimens. DEBs allow local drug delivery without permanent implants, enabling shorter antiplatelet courses that align with geriatric safety priorities. Japan’s 2023 consensus endorsing coronary DEBs illustrates how rapidly ageing regions legitimize stent-free approaches.[2]Source: Japanese Association of Cardiovascular Intervention and Therapeutics, “Clinical Expert Consensus Document on Drug-Coated Balloon,” pmc.nih.gov Because seniors often present calcified and tortuous anatomy, the device’s low-profile crossing ability further drives drug eluting balloon market utilisation in this demographic.

Increasing Adoption of Sirolimus-Coated Balloon Platforms

Sirolimus offers a broader therapeutic window and distinct antiproliferative mechanism compared with paclitaxel. Trials such as SELUTION SFA Japan reported 87.9% primary patency at 12 months in femoropopliteal disease, strengthening clinical confidence. Proprietary MicroReservoir and crystalline drug-layer technologies sustain luminal drug exposure while improving wash-off resistance, giving physicians an alternative when paclitaxel hesitancy persists. Cordis’ USD 1.1 billion acquisition of MedAlliance underscores the commercial potential fueling drug eluting balloon market momentum toward sirolimus platforms.

Emerging Clinical Data Supporting De-Novo Small-Vessel PCI Use

Randomized evidence shows DEBs achieve lower target lesion failure compared with uncoated balloons and comparable late lumen gain to stents in sub-3 mm vessels. Late lumen enlargement observed in 79.1% of de-novo cases points to positive vessel remodeling, fueling guideline discussions around stent-less PCI strategies. The Asia-Pacific Consensus Group's second report on drug-coated balloons emphasizes their role as stent-free alternatives that reduce thrombosis risks and restenosis complications associated with permanent implants. Small vessel disease represents an expanding indication as clinical data demonstrates non-inferiority to drug-eluting stents with potential advantages in specific anatomical and patient subsets

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of R&D And Commercialization | -1.2% | Global, particularly impacting emerging market access | Long term (≥ 4 years) |

| Safety Concerns Over Paclitaxel Mortality Signal | -0.8% | Global, with highest impact in EU regulatory environment | Medium term (2-4 years) |

| Reimbursement Gaps for Below-The-Knee Indications | -0.9% | North America & EU, limited emerging market coverage | Medium term (2-4 years) |

| Supply-Chain Reliance on Specialized Excipients & APIs | -0.6% | Global, concentrated risk in API manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of R&D and Commercialization

Drug-eluting balloon development requires substantial investment in clinical trials, regulatory submissions, and manufacturing infrastructure that creates barriers to market entry and limits competitive intensity. It further requires toxicology work and purpose-built coating facilities that can push development budgets beyond USD 100 million, limiting new entrants. Comparative-effectiveness mandates versus legacy stents add further cost, elevating break-even thresholds and slowing portfolio diversification. Smaller firms often license or sell assets to majors, concentrating intellectual property and tempering price competition within the drug-eluting balloon market. Downstream, premium prices impede penetration in cost-sensitive systems despite clinical need.

Safety Concerns Over Paclitaxel Mortality Signal

Although the FDA concluded in December 2023 that cumulative evidence does not confirm excess mortality, European regulators continue heightened surveillance, and some clinicians remain cautious.[3]Source: Food and Drug Administration, “Update: Paclitaxel-Coated Devices Unlikely to Increase Risk of Mortality,” fda.gov This legacy perception slows adoption in borderline cases or among payers demanding additional justification. The safety signal prompted increased adoption of sirolimus-based alternatives and drug-eluting stents in clinical scenarios where paclitaxel-coated balloons previously represented standard care. The episode underscores how post-market signals can reshape therapeutic algorithms and alter product-mix trajectories inside the drug-eluting balloon market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Peripheral Applications Drive Volume Growth

Peripheral drug-eluting balloons command 58.30% market share in 2025, reflecting their established clinical utility in femoropopliteal and below-the-knee applications where stent placement faces mechanical challenges from vessel movement and external compression. The SELUTION SFA Japan trial's demonstration of 87.9% primary patency at 12 months reinforces peripheral drug-coated balloon efficacy in challenging anatomical territories. Peripheral procedures retain a larger installed base because early paclitaxel devices debuted in femoropopliteal lesions, creating clinician familiarity. Yet the coronary pipeline, supported by expanded de-novo and small-vessel evidence, should narrow the revenue gap as reimbursement hurdles fall.

Coronary drug-eluting balloons show the highest growth trajectory at 9.65% CAGR through 2031, driven by expanding clinical evidence and recent FDA approvals that legitimize their use in coronary in-stent restenosis and small vessel disease. Other products including renal and urology applications represent emerging opportunities, with Abbott's Esprit BTK system approval in April 2024 demonstrating regulatory support for specialized anatomical applications.

By Drug Type: Sirolimus Platforms Challenge Paclitaxel Dominance

The transition toward sirolimus-based formulations accelerates at 9.32% CAGR through 2031, challenging paclitaxel's 78.45% market share in 2025 as clinicians seek alternatives with improved safety profiles and broader therapeutic windows. Cordis's USD 1.1 billion acquisition of MedAlliance brought SELUTION SLR technology, utilizing proprietary MicroReservoir drug delivery for sustained sirolimus release.

Dual-drug and novel agent formulations represent experimental approaches that may address limitations of single-agent platforms, though clinical evidence remains limited. Paclitaxel maintains dominance through established clinical data and manufacturing scale, yet safety concerns following recent mortality signals continue influencing physician preferences despite FDA guidance clearing excess mortality risk.

By Coating Technology: Innovation Drives Competitive Differentiation

FreePac captured 39.70% revenue in 2025 on first-mover adoption, but TransPac’s 9.45% CAGR reflects operator demand for thinner, more uniform drug layers that limit particulate loss. Boston Scientific's AGENT drug-coated balloon utilizes proprietary TransPax coating technology for optimized drug delivery, achieving the lowest drug dose and best acute transfer performance among drug-eluting balloons. EnduraCoat and other technologies compete through differentiated approaches to drug retention, release profiles, and coating durability that address specific clinical challenges. FreePac maintains market leadership through established manufacturing scale and clinical familiarity, yet faces pressure from innovative platforms offering superior performance.

MicroReservoir platforms pursue similar goals through polymer micro-depots and hydrophilic binders. Robust intellectual-property estates around coating science create defensible moats and shape competitive dynamics in the drug eluting balloon market. The evolution toward more sophisticated coating platforms reflects the maturation of drug-coated balloon technology and increasing clinical demands for predictable, reproducible outcomes across varied procedural scenarios.

By Lesion Type: Below-the-Knee Applications Show Strongest Growth

Below-the-knee lesions are set to be the fastest-growing application, projected to expand at a CAGR of 8.64% through 2031. This growth targets chronic limb-threatening ischemia, a condition where traditional therapies often fall short, showing limited durability and necessitating high reintervention rates. In-stent restenosis commands a dominant 46.60% market share in 2025. This underscores the established preference for drug-coated balloons in treating stent failures, especially in scenarios where repeat stenting complicates matters by creating multilayer constructs. As clinical evidence highlights non-inferiority to drug-eluting stents, de-novo small vessel disease is gaining traction, especially with its potential edge in certain anatomical situations. Femoropopliteal lesions, bolstered by robust clinical data and well-established reimbursement pathways, stand out as the largest peripheral application.

The JACC position statement underscores the critical role of below-the-knee endovascular revascularization in staving off limb loss. However, it points out a paradox: while procedural success rates are high, the rates of successful wound healing lag behind. In April 2024, Abbott's Esprit BTK Everolimus Eluting Resorbable Scaffold System received approval, showcasing a notable 75% effectiveness. This starkly contrasts with the 44% effectiveness of treatments that eschewed scaffolds, spotlighting the promise of drug-delivery technologies in navigating challenging anatomical landscapes. The surge in below-the-knee applications is a testament to both the pressing clinical needs and the strides in technology, aiming to serve patient populations that have long been underserved with limited therapeutic avenues.

By End User: Ambulatory Centers Capture Growth

Ambulatory surgical centers (ASCs) demonstrate the highest growth rate at 9.85% CAGR through 2031, driven by healthcare delivery shifts toward cost-effective outpatient models that support same-day discharge protocols. Hospitals retain a dominant 48.75% market share in 2025 due to high procedural volumes and complex case referrals but experience margin pressure from ASC competition and value-based care requirements. Specialty clinics and office-based labs present new market opportunities as drug-coated balloon procedures move to lower-cost settings, reflecting both procedural simplification through technology and healthcare economic pressures.

A 2025 Medicare patient study comparing percutaneous coronary intervention (PCI) outcomes showed similar 30-day adverse event rates between ASCs and hospital outpatient departments. ASCs performed 1.8% of these procedures by 2023, marking substantial growth from prior periods. ASCs achieve better financial margins despite lower reimbursement rates due to reduced operational costs. Drug-coated balloons support ASC adoption by removing permanent implant complications and reducing post-procedure monitoring needs, which simplifies same-day discharge protocols.

Geography Analysis

North America generated 42.10% of 2025 revenue following the FDA’s landmark coronary DEB approval and CMS pass-through payment creation, which together eliminated twin adoption barriers. The presence of leading manufacturers, extensive trial infrastructure, and established ASC networks underpin steady but moderate future growth.

Europe maintains entrenched clinical know-how yet faces stricter paclitaxel surveillance that may temper volumes until sirolimus platforms scale. Germany and Italy remain procedural leaders, while budget-conscious systems in Southern Europe weigh DEB cost-utility versus modern stents.

Asia-Pacific is projected to post the highest 10.05% CAGR as ageing demographics intersect with rapid cath-lab expansion. Japan’s national consensus endorsing broader coronary use, China’s expedited approvals, and India’s rising middle-class demand together create fertile ground for the drug eluting balloon market. Regional manufacturers such as MicroPort bolster domestic supply and stimulate price competition that accelerates penetration. Middle East & Africa and South America together deliver smaller baselines but show selective strength in Gulf Cooperation Council states and Brazil, respectively. Infrastructure upgrades and private-sector cardiovascular centres widen access, yet reimbursement lags and currency volatility moderate the near-term trajectory.

Regulatory Landscape

Drug-eluting/drug-coated balloon catheters are regulated as high-risk device-drug combination products in major markets because the medicinal substance is ancillary to the device primary mode of action. In the United States, drug-eluting peripheral transluminal angioplasty (PTA) catheters are classified as Class III devices, generally requiring Premarket Approval (PMA) under FDA review by the Office of Cardiovascular Devices. This framework drives extensive clinical evidence generation and post-market controls for paclitaxel- and sirolimus-based platforms.

In Europe, Regulation (EU) 2017/745 (MDR) typically places devices incorporating an ancillary medicinal substance into Class III, which increases clinical evaluation and notified body scrutiny. Conformity assessment for certain high-risk devices may involve the Clinical Evaluation Consultation Procedure (CECP), with expert-panel involvement and input associated with EMA processes, which increases the documentation burden for clinical evaluation, risk management, and performance evidence. Across jurisdictions, recognized standards and guidance for vascular device-drug combination products, including ISO 12417-1:2024 and coating-characterization approaches such as ASTM F3320-18, shape expectations for coating integrity, dose consistency, particulate control, and long-term safety follow-up.

Value Chain Analysis

The drug eluting balloon value chain starts with upstream suppliers of medical-grade polymers and tubing for catheter shafts and balloons, radiopaque markers and hypotube components, and pharmaceutical inputs such as paclitaxel or sirolimus API plus biocompatible excipients used to carry and retain drug on the balloon surface. Midstream manufacturers carry out precision balloon forming and assembly, then apply proprietary coating processes (for example, spray-based deposition and drug-polymer/excipient matrices) that determine drug transfer efficiency and particulate performance. These steps are followed by sterilization, packaging, and batch-release testing under ISO 13485 quality systems and combination-product controls.

Downstream, distribution runs through direct sales forces and specialist distributors into cath labs and vascular suites, where purchasing is typically handled by hospital value analysis committees and tender systems. Adoption is closely tied to physician training and clinical evidence packages. Bottlenecks center on single- or limited-source coating materials and process know-how, along with regulatory-linked manufacturing changes that require documented validation. Recent FDA approvals for process or site changes on established drug-coated balloon platforms underscore the operational need to maintain qualified suppliers, validated coating lines, and resilient release-testing capacity. OEM and portfolio strategy also influence channel access, with major branded systems marketed by cardiovascular players such as Boston Scientific (AGENT), Medtronic (IN.PACT/Prevail), B. Braun (SeQuent), and Abbott-linked offerings such as SurVeil (manufactured by Surmodics).

Competitive Landscape

The drug eluting balloon market exhibits moderate consolidation. Medtronic, Boston Scientific, and Koninklijke Philips N.V. leverage integrated cardiovascular portfolios, strong distributor ties, and deep data sets to anchor share. Boston Scientific’s TransPac technology underpins the AGENT coronary balloon, reinforcing its coronary franchise leadership.

Cordis’ USD 1.1 billion buyout of MedAlliance introduces MicroReservoir sirolimus delivery and signals renewed competitive intensity from mid-sized strategic buyers. Teleflex’s 2025 acquisition of BIOTRONIK’s vascular assets expands its peripheral toolkit, highlighting ongoing inorganic expansion as a route to differentiation.

Emerging firms including Concept Medical, Cardionovum, and iVascular focus on next-generation excipient chemistries and dual-drug payloads aimed at restenosis-prone segments. Intellectual-property depth around coating polymers increasingly dictates partnering and licensing negotiations, underscoring R&D’s central role in shaping future drug eluting balloon market share contests.

Drug Eluting Balloons Industry Leaders

Boston Scientific Corporation

Becton, Dickson and Company

Terumo Corporation

Koninklijke Philips N.V.

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Whitespace is opening around sirolimus-coated balloon platforms as clinicians and hospital committees seek alternatives that address lingering paclitaxel perceptions while retaining durable anti-restenotic performance. Evidence flow is increasingly used as a commercial differentiator, and in 2026, peer-reviewed results in JACC on non-inferiority of sirolimus drug-eluting balloons versus usual-care strategies for coronary in-stent restenosis are supported by conference and trial updates (for example, Concept Medical presentations tied to SIRONA and SirPAD). These data points provide concrete inputs for protocol updates, physician education, and payer discussions across both coronary and peripheral indications.

Manufacturing agility and regulatory maintenance work also create a practical opening for scaled incumbents and well-capitalized challengers to improve continuity of supply and geographic reach, particularly as product families expand across lesion subsets and care settings. In 2026, FDA-recorded approvals for manufacturing/process changes for established drug-coated balloon platforms (including Boston Scientific AGENT site-change approval and Medtronic IN.PACT process-change approval) highlight how validated production networks, supplier qualification, and change-control capability support availability and tender competitiveness. The ongoing shift of endovascular procedures toward ambulatory settings further supports opportunities for streamlined inventory models and standardized procedure pathways where drug-eluting balloons align with same-day discharge protocols.

Recent Industry Developments

- April 2026: Cordis announced the launch and availability of the SELUTION SLR PTA drug-eluting balloon in Japan for peripheral artery disease after receiving local approval as a sirolimus-eluting balloon. The launch expands commercial access for sirolimus technology in a major Asia-Pacific market and increases competitive pressure on legacy paclitaxel portfolios in peripheral interventions.

- May 2025: Cordis launched the 10,000-patient SELUTION Global Coronary Registry designed to collect five-year real-world outcomes for its sirolimus balloon platform. The registry broadens the evidence base used in physician adoption and reimbursement discussions, particularly as providers compare stentless approaches against drug-eluting stents across coronary indications.

- March 2024: Boston Scientific received US FDA clearance for the AGENT drug-coated balloon to treat coronary in-stent restenosis. This clearance established a regulated pathway for coronary drug-coated balloons in the United States and raised the competitive bar for subsequent entrants by pairing clinical evidence expectations with a defined reimbursement and procurement reference point.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues generated from drug eluting balloons used in angioplasty procedures, where a coated balloon delivers an antiproliferative drug to the vessel wall during inflation to reduce restenosis.

Scope exclusions: We exclude standard PTA and cutting or scoring balloons without a drug coating, and we also exclude drug eluting stents and other implantable scaffolds.

Segmentation Overview

- By Product

- Coronary Drug-eluting Balloon

- Peripheral Drug-eluting Balloon

- Other Products (Renal/Urology)

- By Drug Type

- Paclitaxel-based Balloons

- Sirolimus-based Balloons

- Dual-drug / Novel Agents

- By Coating Technology

- FreePac

- TransPac

- EnduraCoat

- Other Technologies

- By Lesion Type

- In-stent Restenosis

- De-novo Small Vessel Disease

- Femoropopliteal Lesions

- Below-the-knee Lesions

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting point on procedure volumes, disease burden signals, and regulatory direction for coronary and peripheral interventions. We leaned on public sources such as the US FDA device database and safety communications, CDC cardiovascular statistics, OECD health data, and WHO Global Health Observatory indicators to understand demand-side trends.

To translate these signals into a practical market model, we also reviewed reimbursement and coding references (such as CMS updates), peer reviewed clinical publications on DEB outcomes, and customs or trade statistics where available for catheter type imports. Company annual reports, investor decks, and reputable press helped confirm product launches and geographic presence, and paid company financials and intelligence subscriptions were used selectively to align financial years and standardize product revenue disclosures. These examples are not exhaustive, and many other public sources were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on speaking with interventional cardiology and vascular clinicians, cath lab procurement teams, and device distribution stakeholders, so the model inputs reflected how these balloons are actually purchased and used. We also used these discussions to confirm where coronary versus peripheral use is rising, how sirolimus versus paclitaxel adoption is changing, and what pricing corridors are realistic by region.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 16% | APAC: 45% |

| Mid tier: 49% | Functional/Unit leaders: 26% | EMEA: 31% |

| Smaller Players: 16% | Managers: 58% | Americas: 24% |

Market-Sizing & Forecasting

For the core sizing, we used a top-down build where coronary and peripheral angioplasty procedure pools are reconstructed by region and then filtered through DEB eligibility and adoption. The results were corroborated using selective bottom-up approximations, such as sampled average selling price (ASP) times estimated unit volumes for key geographies, followed by channel checks with distributors and hospital buyers.

The model is guided by inputs that practitioners could verify, including angioplasty and revascularization procedure trends, the share of lesions commonly treated with DEBs (such as in-stent restenosis and femoropopliteal disease), typical balloon usage per case, ASP movement by drug platform, and approval and reimbursement timing that affects uptake. Where country level public data was missing, we filled gaps using nearby country analogs adjusted for healthcare spend, cath lab density, and adoption timing confirmed in interviews.

Forecasts were derived using scenario analysis supported by multivariate regression checks, where procedure growth, penetration shifts, and ASP trends were varied in a controlled way. Assumptions were kept simple so each driver could be traced back to either a public data series or a primary validation point.

Data Validation & Update Cycle

Outputs are validated through triangulation across procedure signals, pricing reality checks, and cross region consistency tests, and then the numbers are reviewed in multiple analyst passes before sign-off. If a variance appears, such as an ASP jump that is not supported by reimbursement updates or product mix changes, we re-check the underlying inputs and reconnect with selected respondents.

Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory actions, a reimbursement change, or a meaningful shift in the drug coating mix. Before delivery, a final review is completed so clients receive the latest updated view based on newly available public data and confirmed market signals.

Mordor Intelligence's Drug Eluting Balloon Market Size Versus Other Published Estimates

Published market sizes for drug eluting balloons often differ because the counted product set and the year of measurement are not always aligned, and that alone can move the total by a wide margin. Differences also come from how procedure demand is translated into units, how pricing is averaged across coronary and peripheral use, and how fast adoption is assumed to expand.

Some estimates appear to include a broader device bucket, such as balloon catheters plus adjacent accessories, and they may also apply aggressive penetration steps from limited country samples. In Mordor Intelligence, only drug coated balloon revenues are counted, and the demand pool is tied back to coronary and peripheral intervention volumes that are checked with clinician feedback and reimbursement timing, which keeps the scope tighter and the pricing logic more consistent.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.85 B (2026) | |

| Global Consultancy A | USD 1.17 B (2024) | Uses an earlier base year and may blend coronary, peripheral, and an 'other' bucket without clearly separating pure drug coated balloon revenue from nearby balloon catheter categories, which can lift the total. |

| Industry Research Desk B | USD 1.53 B (2025) | Positions the scope as drug eluting balloon catheters and applies higher growth and broader material and end use framing, which suggests a wider counted device set and higher average pricing assumptions across regions. |

The comparison shows that the spread mostly comes from scope and year alignment, and then from how penetration and ASP are progressed across coronary and peripheral use cases. By keeping the counted product definition specific and forcing each input to connect back to procedures, adoption, and pricing checks, we get a number that is easier to replicate and update as new evidence emerges.

Key Questions Answered in the Report

What is the projected value of the drug eluting balloon market by 2031?

The market is forecast to reach USD 1.26 billion in 2031, supported by an 8.07% CAGR over 2026-2031.

Which balloon drug type is growing fastest?

Sirolimus-based balloons are expected to expand at a 9.32% CAGR, outpacing paclitaxel alternatives.

Why are ambulatory surgery centers important for drug-eluting balloons?

DEBs enable same-day discharge without implanted metal, aligning with ASC cost models and driving a 9.85% CAGR for this setting.

Which region offers the highest growth potential?

Asia-Pacific is forecast to post a 10.05% CAGR, propelled by ageing populations, regulatory acceleration, and expanding cath-lab capacity.

How did recent FDA approvals impact coronary applications?

The 2024 AGENT clearance validated DEBs for coronary in-stent restenosis, unlocking reimbursement and accelerating US adoption.

What factors restrain BTK drug-coated balloon uptake?

Limited reimbursement clarity and the high cost of specialized devices curb growth despite compelling clinical need.

Page last updated on: