Gastric Balloons Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

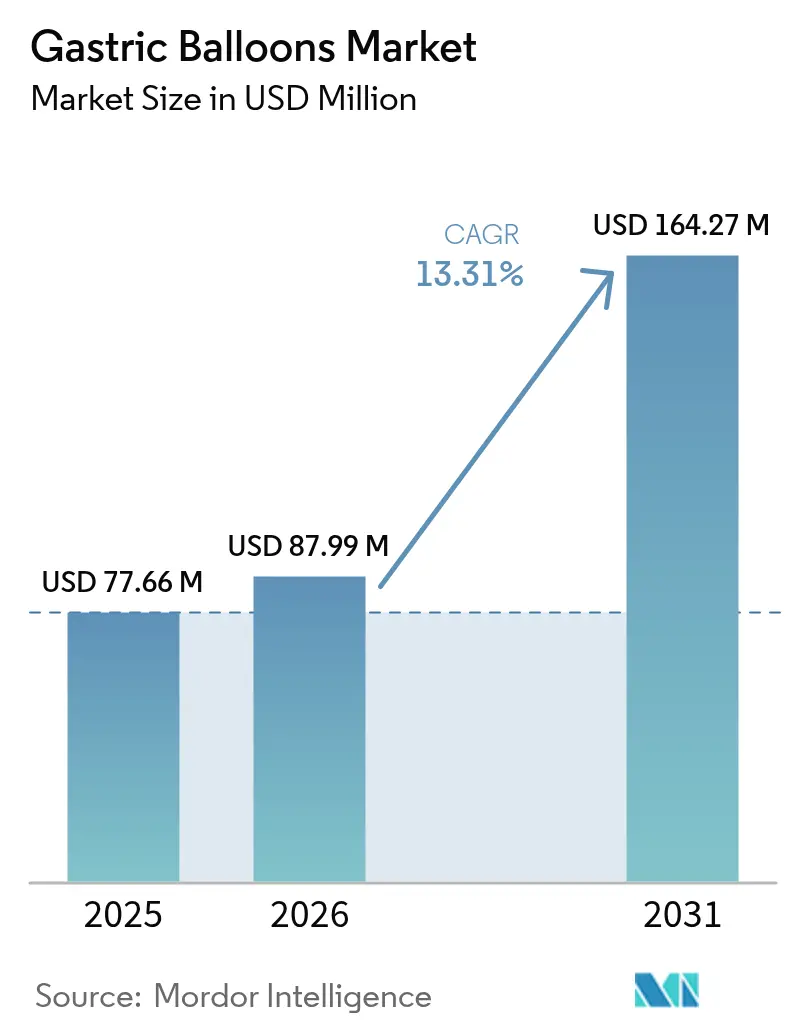

| Market Size (2026) | USD 87.99 Million |

| Market Size (2031) | USD 164.27 Million |

| Growth Rate (2026 - 2031) | 13.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gastric Balloons Market Analysis by Mordor Intelligence

The gastric balloons market size was valued at USD 77.66 million in 2025 and estimated to grow from USD 87.99 million in 2026 to reach USD 164.27 million by 2031, at a CAGR of 13.31% during the forecast period (2026-2031). Accelerating obesity prevalence, procedureless balloon innovations, and rising payer openness to cover reversible therapies fuel this growth. Demand is strongest among individuals with body mass index (BMI) 30–40 kg/m² who reject surgery but seek durable weight control, while clinicians increasingly view balloons as a bridge between lifestyle change and bariatric surgery. Technological advances such as swallowable capsules, soft-robotic pressure adjustment, Internet-of-Things (IoT) telemetry, and concurrent glucagon-like peptide-1 (GLP-1) pharmacotherapy showcase how device makers intend to improve efficacy, comfort, and metabolic impact.

Key Report Takeaways

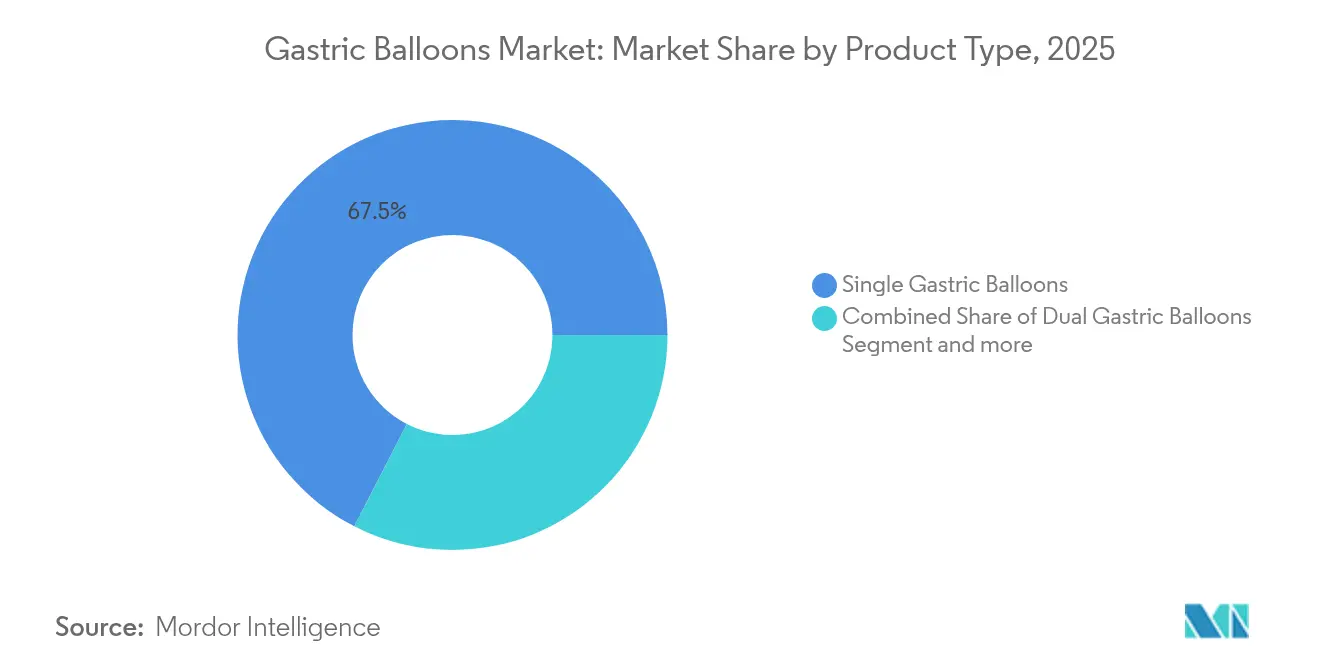

- By product type, single-balloon systems led with 67.45% of gastric balloons market share in 2025; triple balloons record the fastest 13.55% CAGR through 2031.

- By filling material, saline-filled devices held 81.05% of the gastric balloons market size in 2025, while gas-filled balloons expand at a 13.66% CAGR.

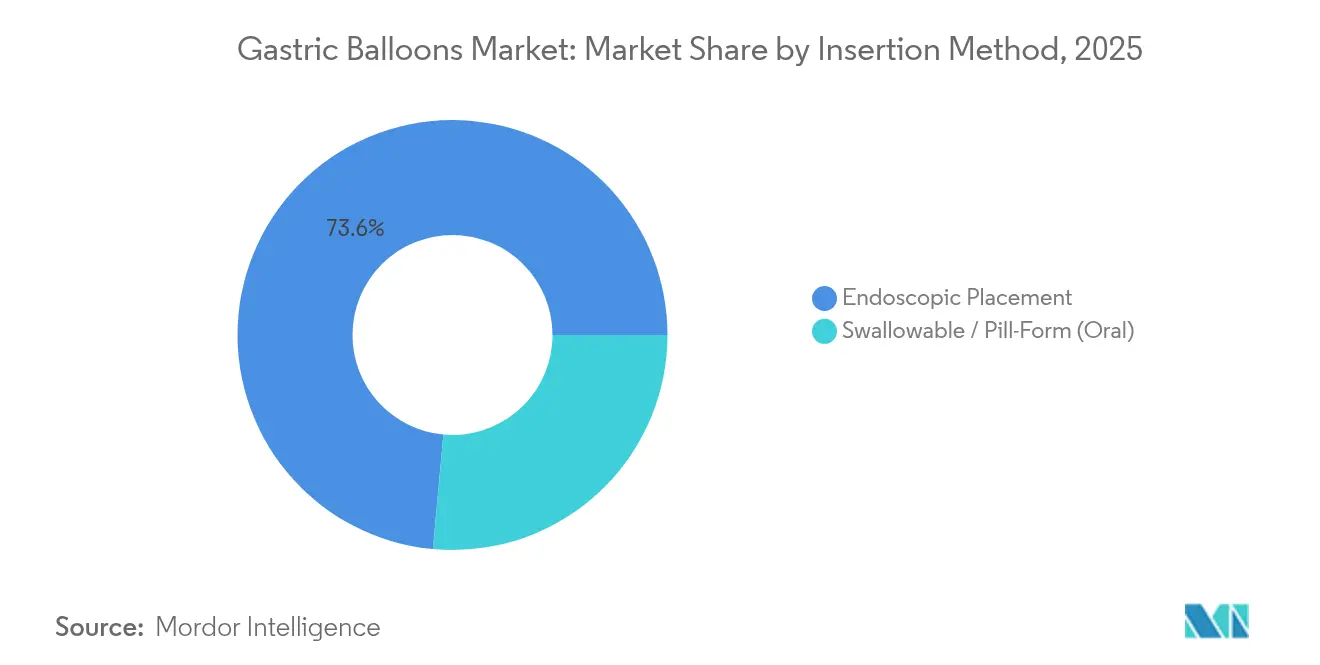

- By insertion method, endoscopic placement retained 73.55% share in 2025; swallowable approaches climb at 13.34% to 2031.

- By end user, hospitals secured 48.05% revenue share in 2025, whereas specialist bariatric clinics post a 13.7% CAGR.

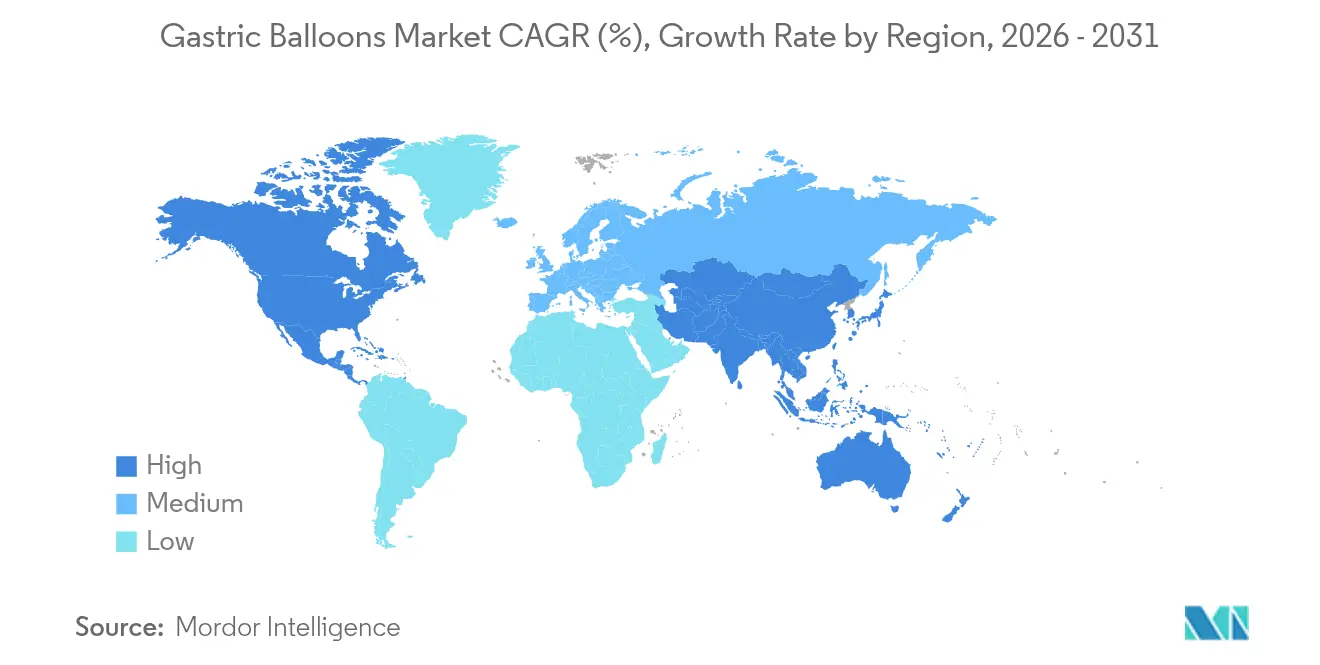

- By geography, North America commanded 39.85% of the gastric balloons market share in 2025; Asia Pacific advances fastest at 13.78% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gastric Balloons Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of obesity | +3.2% | Global; strongest in North America & Europe | Long term (≥ 4 years) |

| Demand for minimally-invasive weight-loss procedures | +2.8% | North America & EU; expanding in Asia Pacific | Medium term (2-4 years) |

| Combination therapy with GLP-1 agonists | +2.4% | Early uptake in North America; global potential | Medium term (2-4 years) |

| Growing clinical evidence & guideline endorsements | +2.1% | Developed markets worldwide | Medium term (2-4 years) |

| Expanding reimbursement coverage | +1.9% | North America & core EU | Short term (≤ 2 years) |

| Smart balloons with soft-robotics & IoT | +1.1% | Initially developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Obesity

Obesity has been reclassified as a chronic disease requiring formal medical intervention. The United States’ 2024 proposal to reimburse anti-obesity drugs under Medicare Part D signals institutional recognition that fuels demand for complementary device-based options[1]Centers for Medicare & Medicaid Services, “Calendar Year 2024 Medicare Part D Redesign,” cms.gov. Health systems see balloons as a cost-effective route to mitigate diabetes, hypertension, and sleep-apnea expenditures. Meta-analyses indicate 55.5% resolution in type 2 diabetes, 58.8% in hypertension, and 57.8% in obstructive sleep apnea within four months of balloon therapy[2]Allurion Technologies, “AUDACITY Pivotal Trial Topline Results,” ir.allurion.com . Rising adolescent obesity opens a younger segment that favours reversible, nonsurgical tools.

Increasing Demand for Minimally-invasive Weight-loss Procedures

Patients increasingly seek interventions that avoid surgery, preserve future options, and permit swift return to routine. Procedureless balloons eliminate sedation, operating theatre time, and the need for gastroenterologist supervision, making therapy accessible in primary-care settings. Swallowable devices show serious adverse events under 3.1%, favourably contrasting with surgical complication profiles. Outpatient-friendly workflows widen provider networks, encouraging rapid adoption despite endoscopy’s current 74% share dominance.

Combination Therapy with GLP-1 Agonists Unlocking New Indications

Early clinical programs combining balloons with semaglutide demonstrate 19% total body weight loss versus 13.7% for balloons alone, pointing to additive metabolic benefits that preserve lean muscle. Such protocols are attractive to payers needing durable outcomes and to physicians managing patients with high cardiometabolic risk. The synergy positions balloons as a platform therapy rather than a stand-alone mechanical solution.

Growing Clinical Evidence Base & Guideline Endorsements

Guidance released in 2024 by the American Society for Gastrointestinal Endoscopy and its European counterpart formally places gastric balloons within endorsed bariatric pathways[3]American Society for Gastrointestinal Endoscopy & European Society of Gastrointestinal Endoscopy, “Guideline on Primary Endoscopic Bariatric Therapies,” asge.org. Meta-analyses now encompass 15-year registries, confirming 25.4% mean excess weight loss and low late complication incidence[4]Korean Journal of Helicobacter and Upper Gastrointestinal Research, “Regional Obesity Trend Review,” kjhugr.org. Such validation accelerates physician confidence, standardizes training, and fosters payer engagement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited long-term efficacy versus bariatric surgery | −2.1% | Global, especially where surgery is entrenched | Long term (≥ 4 years) |

| Patchwork reimbursement in emerging economies | −1.8% | Asia Pacific, Latin America, Middle East & Africa | Medium term (2-4 years) |

| Competition from endoscopic sleeve gastroplasty | −1.6% | North America & Europe; growing worldwide | Medium term (2-4 years) |

| Balloon-related adverse events | −1.3% | Global; higher impact in low-volume centres | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Long-term Efficacy versus Bariatric Surgery

Weight regain after device removal remains a core concern. Evidence shows only 44.7% of balloon patients keep meaningful loss 12 months post-extraction, whereas laparoscopic sleeve gastrectomy delivers better durability ajendoscopicsurg.org. This limitation narrows the eligible cohort to individuals prioritising reversibility over maximal weight reduction. Long-term nutritional counselling and digital coaching add cost and complexity.

Competitive Threat from Next-generation Endoscopic Sleeve Gastroplasty

Endoscopic sleeve gastroplasty (ESG) reports 17.1% total body weight loss at 12 months with similar safety, outpacing 10–15% results typical for balloons endoscopeninternationalopen.com. ESG offers permanent gastric volume reduction without implants, avoiding migration or deflation issues that affect up to 2.9% of balloon recipients obesitysurgery.com. As ESG gathers guideline support, it may displace balloon demand in premium centres.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Single Systems Dominate, Triple Balloons Gain Momentum

In 2025, single devices controlled 67.45% of the gastric balloons market, underwritten by decades of safety data and straightforward placement requirements. Orbera’s lineage illustrates sustained physician confidence, which translates into predictable revenue for hospitals and clinics. Patients often select singles for lower cost and well-documented outcomes. Market incumbents reinforce this position by bundling balloons with nutrition coaching apps that maximise post-procedure support.

Triple-balloon systems record the highest 13.55% CAGR and illustrate how innovation can command premium reimbursement. Spatz’s adjustable platform lets physicians modulate volume to counter weight-loss plateaus, achieving 15% total body weight loss in controlled trials. This adaptability differentiates triple balloons in performance-driven patient segments and signals a route to extend indwell time, potentially mitigating the long-term efficacy gap.

By Filling Material: Saline Tradition Faces Gas-filled Comfort

Saline remains the default fill, occupying 81.05% share in 2025 due to radiographic visibility and long-term safety documentation. Hospitals appreciate the control saline affords during placement and removal, which aligns with standard endoscopy workflow. Moreover, device suppliers maintain mature supply chains for sterile saline kits, supporting cost efficiency.

Gas-filled balloons, led by Obalon, advance at 13.66% CAGR as patients value lighter intragastric load and reduced nausea. Swallowable capsule delivery eliminates sedation and can be completed in under 15 minutes, a major draw for outpatient settings. Despite slightly longer removal duration, improved tolerability supports broader adoption, particularly in primary-care networks seeking scalable interventions.

By Insertion Method: Endoscopy Still Leads, Swallowable Capsules Scale

Endoscopic placement upholds 73.55% share today thanks to ingrained physician training, visual confirmation during deployment, and concurrent diagnostic scope. Hospitals already invested in endoscopy towers realise minimal incremental cost when adding balloons to bariatric programs.

Swallowable capsules post a 13.34% CAGR by removing anaesthesia, facility, and staffing hurdles. The Elipse system documents 14.2% total body weight loss while requiring only a brief clinic visit for ingestion. Such convenience resonates with corporate wellness programs and telemedicine operators that can oversee weight-loss journeys remotely. As regulatory approvals spread, the capsule pathway will increasingly pressure endoscopic volumes, particularly for low-risk patients.

By End User: Hospitals Anchor Volume, Specialist Clinics Accelerate

Hospitals delivered 48.05% of 2025 revenues owing to integrated endoscopy suites, emergency preparedness, and established multidisciplinary care teams. These attributes reassure risk-averse payers and enable bundled payments that include nutritional counselling and follow-up visits.

Bariatric clinics, however, will be the growth engine through 2031 at a 13.7% CAGR. Focused expertise, streamlined pathways, and marketing agility allow clinics to attract self-pay patients swiftly. Procedureless balloons magnify this trend because they require minimal capital equipment, letting clinics scale throughput while keeping overhead low. Ambulatory surgical centres follow a similar trajectory, supported by cost-effective staffing models.

Geography Analysis

North America accounted for 39.85% of the gastric balloons market in 2025, boosted by FDA-cleared device variety and strong clinician awareness. Medicare’s evolving coverage stance and employer wellness initiatives keep demand resilient.

Europe maintains significant weight through broad physician adoption and proactive guideline inclusion. Reimbursement, however, remains patchy, producing a mosaic of regional uptake—Germany’s statutory insurers reimburse balloons selectively, whereas southern Europe often relies on self-pay models.

Asia Pacific exhibits a 13.78% CAGR, the fastest globally. Rising disposable incomes and surging obesity prevalence create favourable demand in China, Japan, and India. Japan’s 15-year registry shows 46.6% mean excess weight loss, instilling confidence among regional gastroenterologists. Yet payer fragmentation and offshore medical tourism mean market development leans toward private-sector hospitals and wellness chains that target affluent urban populations.

Competitive Landscape

A moderately fragmented competitive arena characterises the gastric balloons market. Boston Scientific’s 2023 acquisition of Apollo Endosurgery for USD 615 million bundled Orbera with a global endoscopy portfolio, illustrating the need for scale to navigate multi-region regulation. Allurion Technologies commands procedureless leadership via the Elipse balloon, supported by more than 20 U.S. patents and imminent FDA filing after its pivotal AUDACITY study showed a low 3.1% serious-event rate.

ReShape Lifesciences pursues cost optimisation, shedding 55.4% of operating expense while amassing over 50 patents covering dual-balloon refinements. Cost containment aligns with outpatient clinic needs, positioning ReShape to supply value-tier offerings. Device makers increasingly layer artificial-intelligence coaching apps and GLP-1 medication packages onto hardware sales, seeking subscription revenue and patient-engagement data.

Smart-balloon concepts embedding pressure sensors, micro-pumps, and Bluetooth modules inch closer to market, promising active volume modulation and real-time satiety feedback. Such features may blur lines between implantable devices and digital therapeutics, inviting partnerships with telehealth firms and metabolic-disease drugmakers.

Gastric Balloons Industry Leaders

Allurion Technologies, Inc.

ReShape Lifesciences, Inc.

Helioscope Medical Implants

Boston Scientific Corporation

Spatz FGIA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Allurion Technologies reported positive AUDACITY trial results, with more than 50% of participants hitting significant weight-loss thresholds at 48 weeks and a 3.1% serious-event rate, backing its FDA pre-market approval filing.

- November 2024: Allurion launched AllurionMeds, an AI-native compounded GLP-1 program in the United States, integrating Coach Iris AI for adherence support and aiming at the USD 100 billion GLP-1 addressable market.

- January 2024: Somerset NHS Trust began treating patients with Allurion’s swallowable balloon, marking the first National Health Service deployment of a procedureless device .

- April 2023: Boston Scientific completed its acquisition of Apollo Endosurgery, integrating Orbera into its endoscopy suite and expanding distribution reach.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the gastric balloons market as the revenue generated from single, dual, and triple intragastric balloon systems, whether saline or gas filled, that are temporarily placed in the stomach by endoscopy or swallowable capsule to induce satiety and support medically supervised weight loss.

Scope excludes permanent implantable bands, endoscopic sleeve gastroplasty devices, and all pharmacologic obesity treatments.

Segmentation Overview

- By Product Type

- Single Gastric Balloons

- Dual Gastric Balloons

- Triple Gastric Balloons

- By Filling Material

- Saline-Filled Balloons

- Gas-Filled Balloons

- By Insertion Method

- Endoscopic Placement

- Swallowable / Pill-Form (Oral)

- By End User

- Hospitals

- Bariatric & Metabolic Clinics

- Ambulatory Surgical Centers

- Geography

- North America

- Europe

- Asia-Pacific

- Middle East & Africa

- South America

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interview practicing bariatric surgeons, GI endoscopists, procurement heads at hospital chains, and regional distributors across North America, Europe, Asia-Pacific, and the Gulf. These conversations test secondary assumptions on average selling prices, replacement rates, and patient eligibility criteria, allowing us to refine incidence to procedure funnels.

Desk Research

We begin by mapping publicly available obesity prevalence data and procedure volumes from sources such as the WHO, OECD Health Statistics, and the CDC, and then layer in import-export codes drawn from UN Comtrade that capture finished balloon kits. Company 10-Ks, FDA 510(k) files, and EU CE databases help our team verify product approvals and typical selling prices.

To fill revenue and capacity gaps, Mordor analysts also tap D&B Hoovers for private financials, Dow Jones Factiva for supplier contract values, and Questel to flag new gastric balloon patents that hint at pipeline launches. The sources cited are illustrative; many additional public and proprietary documents were reviewed to validate numbers and narrative.

Market-Sizing & Forecasting

A top-down reconstruction combines national obesity pools with uptake rates by BMI bracket, which are then cross-checked against shipment data and sampled ASP times volume roll-ups for leading suppliers. Key model drivers include adult obesity prevalence, insurer reimbursement coverage, clinic adoption of swallowable capsules, average balloon dwell time, and repeat procedure share. A multivariate regression, anchored on obesity prevalence and disposable income per capita, generates the 2025 to 2030 forecast, while selective bottom-up triangulation ensures no single assumption skews totals.

Data Validation & Update Cycle

Outputs pass three-level analyst reviews, variance checks against new regulatory filings, and follow-up calls where anomalies persist. Models refresh annually, with mid-cycle updates triggered by material events such as FDA approvals or major reimbursement shifts.

Why Mordor's Gastric Balloons Baseline Commands Reliability

Published market values often diverge; definitions, refresh cadence, and inclusion of experimental devices vary across firms.

Prospective buyers deserve clarity.

Mordor reports 2025 market revenue of USD 77.66 million after factoring verified shipments of capsule systems and adjusting ASPs for currency moves.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 77.66 M (2025) | Mordor Intelligence | - |

| USD 57.5 M (2025) | Global Consultancy A | Excludes swallowable balloons and uses list prices without regional ASP discounts |

| USD 68.5 M (2024) | Industry Journal B | Updates every 18 months; relies largely on obesity rates, limited provider interviews |

| USD 88.7 M (2025) | Global Consultancy C | Bundles endoscopic sleeve kits with balloons, inflating revenue base |

Differences stem chiefly from product scope and validation depth. By aligning device-level shipment evidence with real-world pricing and refreshing the model yearly, Mordor Intelligence offers a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current Global Gastric Balloons Market size?

The gastric balloons market size is USD 87.99 million in 2026 and is projected to reach USD 164.27 million by 2031 at a 13.31% CAGR.

Which gastric balloon product type holds the largest share?

Single-balloon systems dominate with 67.45% market share in 2025 due to longstanding clinical familiarity and streamlined placement protocols.

How fast is the Asia Pacific gastric balloons market growing?

Asia Pacific is the fastest-expanding region, advancing at a 13.78% CAGR through 2031 on the back of rising obesity rates and improving healthcare access.

Are swallowable balloons overtaking endoscopic balloons?

While endoscopic placement still carries 73.55% share, swallowable capsules are growing at 13.34% annually, gaining traction where patients value procedureless convenience.

What role do GLP-1 drugs play with gastric balloons?

Combination therapy studies show 19% total body weight loss versus 13.7% with balloons alone, indicating that GLP-1 agonists can enhance balloon efficacy and broaden treatment indications.

Page last updated on: