Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 29.69 Billion |

| Market Size (2031) | USD 59.91 Billion |

| Growth Rate (2026 - 2031) | 15.07% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

X-by-wire System Market Analysis by Mordor Intelligence

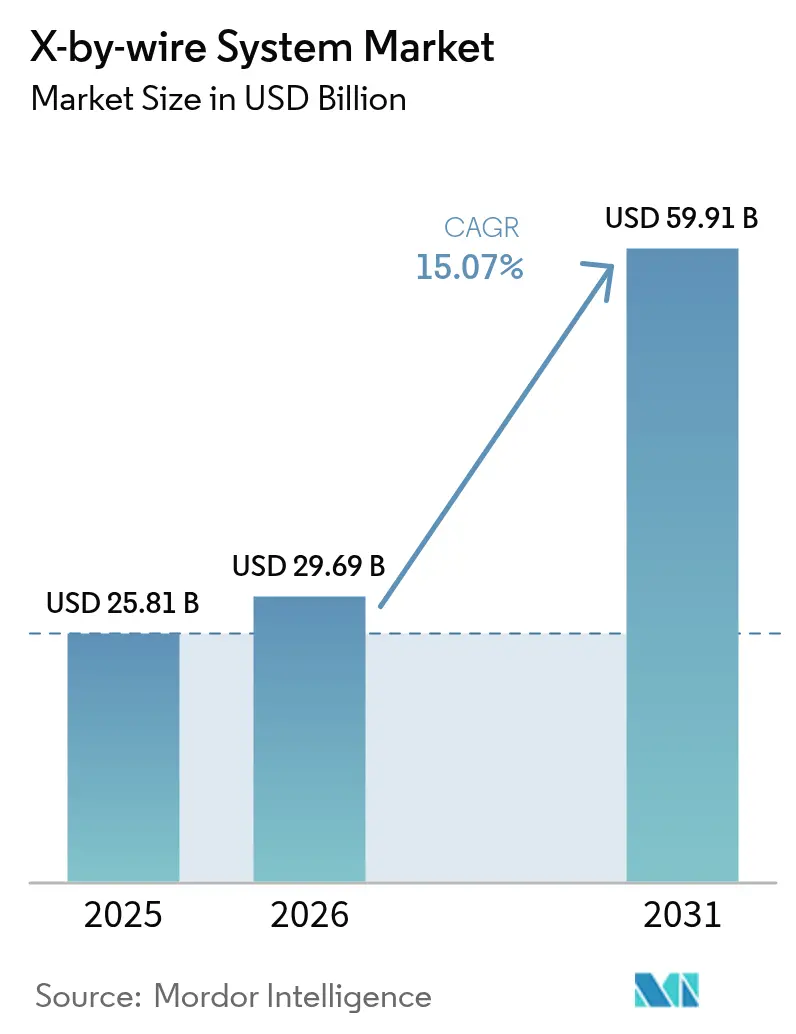

The X-by-wire System Market size is projected to be USD 25.81 billion in 2025, USD 29.69 billion in 2026, and reach USD 59.91 billion by 2031, growing at a CAGR of 15.07% from 2026 to 2031. Growth reflects the automotive shift toward software-defined chassis designs in which electronic control modules replace mechanical linkages, cut wiring mass, and enable over-the-air calibration updates. Battery-electric platforms drive most adoption because flat floors and the absence of engine-bay constraints allow automakers to mount compact actuators at the wheels, recover more energy, and meet stringent fleet-average CO₂ limits set in Europe and China. Brake-by-wire already captures the largest share of revenue because friction-to-regen blending is critical for one-pedal driving. Yet, steer-by-wire is gaining momentum as premium brands launch yoke controllers that eliminate the steering column. Europe currently leads demand on the back of the European Union General Safety Regulation that mandates electronic emergency braking and lane keeping, while Asia Pacific is sprinting ahead due to China’s Level 3 automation subsidies and Japan’s Lexus RZ 450e steer-by-wire debut. Established tier-1 suppliers—Continental, ZF Friedrichshafen, Bosch, and JTEKT—anchor the competitive field. Still, start-ups such as REE Automotive are courting fleet operators with modular corner-module skateboards that simplify body swaps and compress assembly time.

Key Report Takeaways

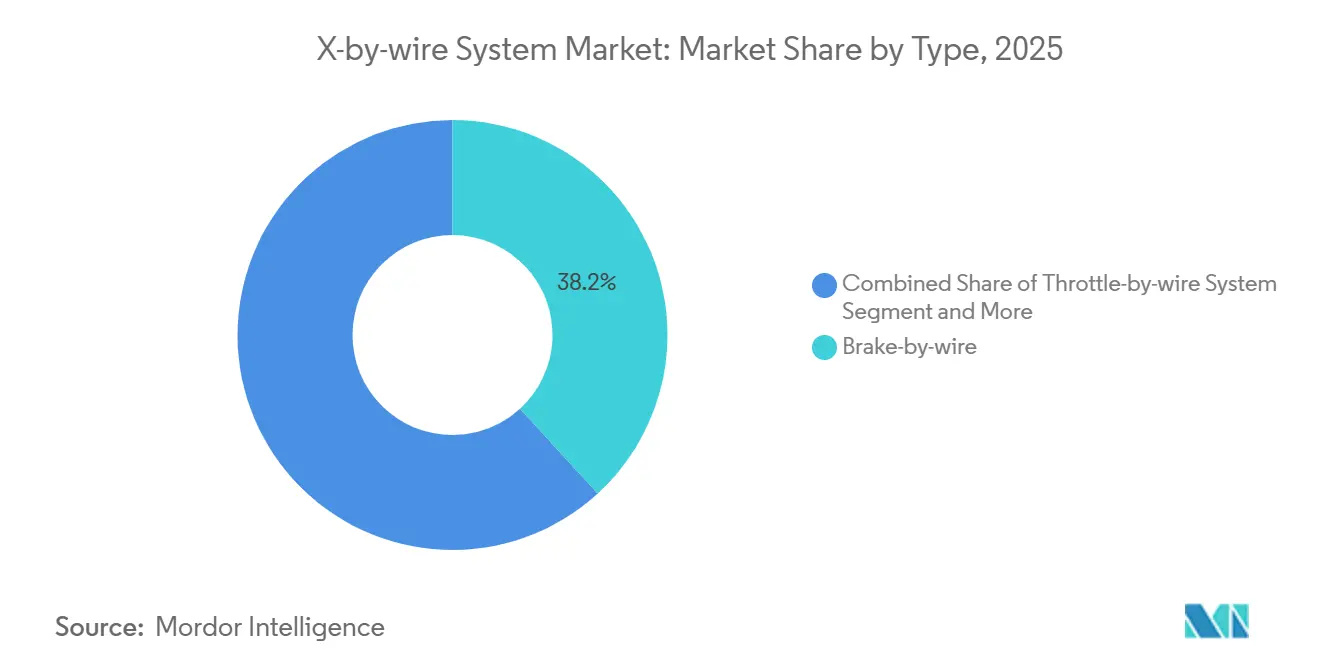

- By type, brake-by-wire led with 38.17% of the X-by-wire systems market share in 2025, while steer-by-wire is advancing at a 15.09% CAGR through 2031.

- By vehicle type, passenger cars accounted for 77.16% of the volume in 2025; medium and heavy commercial vehicles posted the highest projected CAGR of 15.21% to 2031.

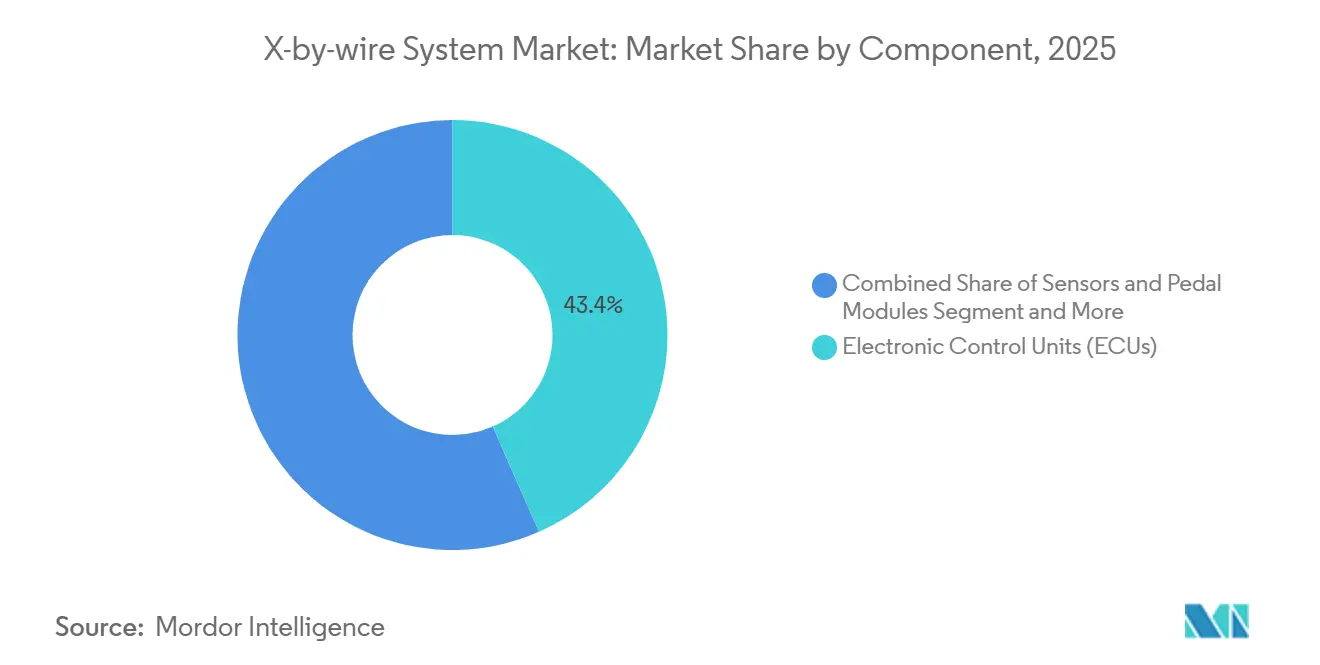

- By component, electronic control units accounted for 43.35% revenue in 2025, yet actuators are forecast to expand at a 15.11% CAGR over 2026-2031.

- By propulsion type, battery-electric vehicles accounted for 61.27% of demand in 2025 and are projected to grow at a 15.13% CAGR through 2031.

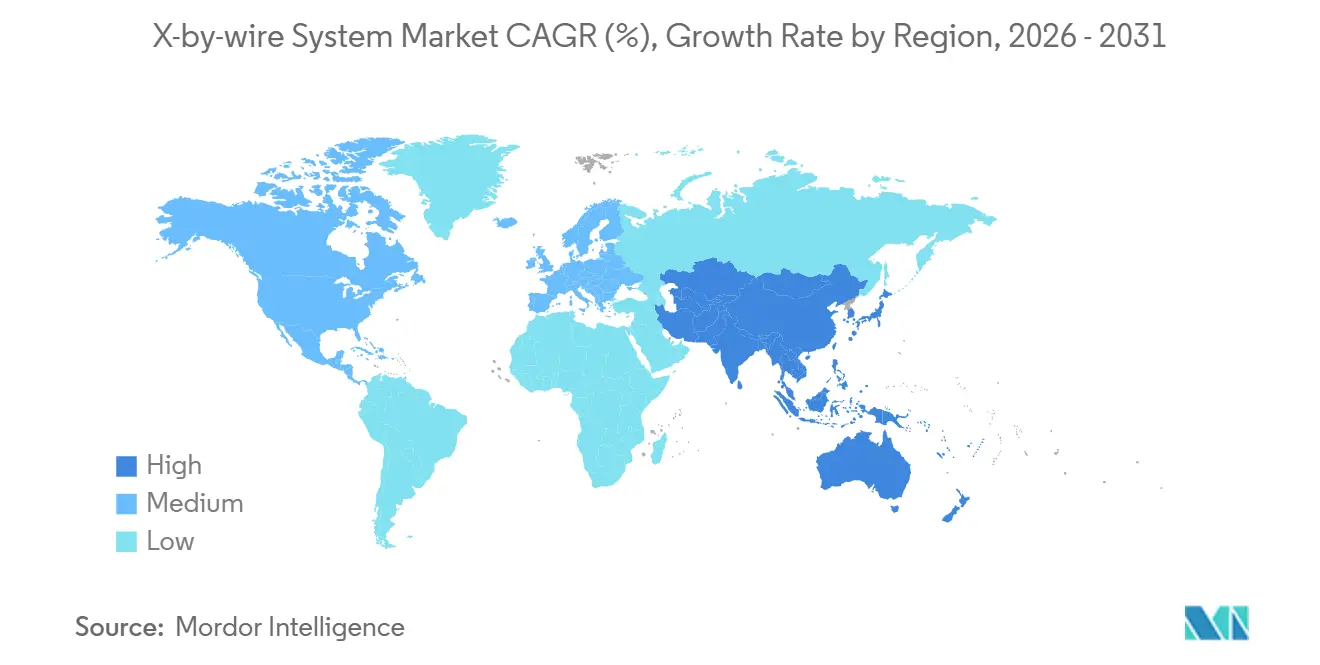

- By geography, Europe captured 36.83% revenue in 2025; Asia Pacific is set for the fastest regional growth at 15.17% annually to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global X-by-wire System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advanced-driver-assistance and Autonomy Push | +3.2% | Global, led by North America & Europe | Medium term (2–4 years) |

| Global Safety and CO₂ Rules Favour Electronics | +2.8% | Europe & China, spill-over to APAC | Short term (≤ 2 years) |

| EV Packaging and Weight-saving Benefits | +2.5% | Global, concentrated in BEV-heavy markets | Medium term (2–4 years) |

| Digital Chassis Cost-saving Platforms | +1.9% | North America & Europe, early adoption in China | Long term (≥ 4 years) |

| OTA-tunable Software-defined Chassis | +1.6% | Global, premium-segment focus | Medium term (2–4 years) |

| Corner-module EV Skateboards for Fleets | +1.4% | North America & Europe, pilot deployments in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advanced-driver-assistance and Autonomy Push

Steer-by-wire and brake-by-wire cut control-loop latency below 50 milliseconds, a threshold that Level 2+ autonomy requires for safe lane-keep and emergency maneuvers [1]“EQS Steering Technology,” Mercedes-Benz, mercedes-benz.com . Mercedes-Benz will ship the first mass-market steer-by-wire system in its EQS sedan during 2026, using ZF dual-pinion actuators that reduce driver effort by 40% in tight parking. Brake-by-wire supports one-pedal driving by merging friction pads with regenerative torque so smoothly that Bosch iBooster 3 recovers up to 0.3 kWh per mile in city cycles [2]“iBooster 3 Technical Sheet,” Bosch Mobility, bosch.com . Autonomous-vehicle developers favor by-wire because direct CAN commands avoid the energy drain of mechanical override motors, trimming redundant power budgets by 25%. Demand also extends to suppliers that embed torque, angle, and temperature telemetry in a single housing, streamlining the bill of materials and accelerating ISO 26262 assessments.

Global Safety and CO₂ Rules Favor Electronics

The EU General Safety Regulation from 2024 mandates intelligent speed assistance, emergency lane keeping, and automatic braking, all of which are easier with precise electronic brake-force and steering actuation [3]“Vehicle Safety Regulation,” Europa, europa.eu . China’s GB 7258 rule extends emergency braking to trucks weighing more than 3.5 tonnes, spurring the fitment of brake-by-wire systems that eliminate 200-millisecond air-brake lag. CO₂ fleet targets dropping to 49.5 g/km by 2030 drive OEMs toward BEVs that benefit from the 8-12 kg mass cut when hydraulics and columns disappear. ISO 26262 and ISO/SAE 21434 set a high bar for certification that favors early movers who already own ASIL D-approved platforms. Net effect is a regulatory ratchet that locks a rising electronics floor into every new vehicle, pushing the X-by-wire systems market deeper into the mainstream.

EV Packaging and Weight-saving Benefits

Battery-electric skateboard frames free up space so engineers can tuck actuation motors directly onto wheel uprights, slicing CAN latency by 30-40% and letting torque-vectoring algorithms react faster on slick roads. REE’s certified P7-C corner module weighs 68 kg per wheel, 15% lighter than conventional struts with separate power steering and hydraulics. Eliminating the column, booster, and fluid lines saves 18-22 kg and extends the range of a 75 kWh pack by 1.5%, enough to meet many subsidy thresholds in Europe and China. Tesla’s Cybertruck uses steer-by-wire, which swings the front wheels 50 degrees, giving it a 13.7 m turning circle despite its long 5.68 m wheelbase. Commercial trucks gain underbody volume for extra battery or hydrogen tanks once bulky air-brake reservoirs are gone.

Digital Chassis Cost-saving Platforms

Consolidating braking, steering, and suspension ECUs into a single domain controller reduces harness mass by 18% and cuts assembly time per vehicle by 25 minutes. Continental’s Integrated Chassis Control goes into production in 2026 with an AURIX TC4x that processes all sensor feeds every 10 milliseconds, while built-in redundancy lets the steering core take over brake calculations if faults occur. Zonal topologies route commands through regional gateways that Bosch says will slash copper by 30% in cars carrying 100+ ECUs. A software-defined chassis also introduces recurring revenue, as OEMs sell mode upgrades that alter steering weight or brake-pedal feel without hardware swaps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Functional-safety Certification Hurdles | -1.2% | Global, acute in North America & Europe | Short term (≤ 2 years) |

| High Integration Cost for Legacy Platforms | -0.9% | North America & Europe, moderate in APAC | Medium term (2–4 years) |

| In-vehicle-network Cyber-security Gaps | -0.7% | Global, regulatory focus in EU & China | Medium term (2–4 years) |

| Supply Crunch of Redundancy-grade Sensors | -0.6% | Global, concentrated in semiconductor supply | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Functional-safety Certification Hurdles

Achieving ASIL D requires the hazardous failure probability to remain below 10 per billion operating hours, which necessitates dual actuators, isolated power, and millions of test kilometers. ZF needed 18 months of hardware-in-the-loop work for the Mercedes EQS steer-by-wire and spent USD 45 million beyond plan, delaying launch. Smaller suppliers pay USD 500-800 per laboratory hour for accelerated tests, a budget many cannot sustain. Brake-by-wire faces even closer scrutiny because loss of pressure poses a higher injury risk, and Bosch cycled its iBooster 3 through 2.4 million duty cycles to gain approval. U.S. homologation lags; NHTSA still grants temporary exemptions capped at 2,500 units, restricting early volume.

High Integration Cost for Legacy Platforms

Retrofitting by-wire into hydraulic frames may cost USD 200 million per car line for tooling and validation. Internal-combustion models still account for 38% of light-duty output in 2025, yet they are near the end of their life cycles, so OEMs avoid large capital outlays. A full steer-by-wire adds USD 800-1,200 to the bill of materials versus USD 150-200 for electric power steering, eroding margins in USD 25,000 compact cars. Hybrid cars keep vacuum boosters for engine-off events, cancelling much of the weight advantage. Commercial trucks must also re-certify their braking systems if they swap out mandated air brakes, which extends project timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Brake-by-wire Leads Electrification Wave

Brake-by-wire generated 38.17% of 2025 revenue, the most significant slice of the X-by-wire systems market share, while steer-by-wire is projected to grow at a 15.09% CAGR to 2031. Demand stems from seamless regen-to-friction blending, which adds 0.3 kWh per urban mile in range and lets OEMs downsize packs. Bosch iBooster 3 began series production in late 2025 without a vacuum pump, illustrating how suppliers strip components and weight. ZF clinched a multi-year order for 5 million brake-by-wire units, signaling a migration from premium to volume segments.

Steer-by-wire is currently lagging but will accelerate as the Mercedes EQS, Lexus RZ, and Tesla Cybertruck popularize column-less designs. Unified chassis controllers mesh throttle, shift, and park functions, further lifting by-wire revenue even though those subsystems already appear in 90% of vehicles. Corner-module suppliers combine steering, braking, and drive motors into a single 68 kg assembly, collapsing historical distinctions among system types. The X-by-wire systems market size for integrated corner units is projected to expand at more than 16% annually once certification bottlenecks ease.

By Vehicle Type: Commercial Fleets Accelerate Adoption

Passenger cars commanded 77.16% volume in 2025, reflecting premium BEV launches that require advanced regen and yoke steering. Yet medium- and heavy-duty commercial vehicles will grow fastest at a 15.21% CAGR to 2031, as fleets pursue predictive maintenance and fuel savings through tighter platooning. Geotab’s 500-van pilot predicts 20% less downtime by tracking current draw anomalies in REE corner modules.

Light commercial vans benefit from brake-by-wire but wrestle with thin margins that make the USD 800-1,200 premium for steer-by-wire hard to absorb. For heavy trucks, China’s GB 7258 braking mandate pushes adoption, while platooning enabled by 40 millisecond electric brake response shrinks inter-vehicle gaps to under 10 m, trimming drag 10%. The X-by-wire systems industry sees strong order pipelines from logistics firms that view autonomous yard parking and remote diagnostics as key to lowering labor costs.

By Component: Actuators Gain as Miniaturization Advances

Electronic control units accounted for 43.35% of revenue in 2025, anchored by dual-core AURIX microcontrollers that crunch sensor data every 10 milliseconds. Actuators are forecast to grow 15.11% per year to 2031 as suppliers switch from custom-wound motors to standard brushless machines at an industrial scale. Continental’s 2026 Integrated Chassis Control folds three legacy ECUs into one, shaving harness mass by 18% and assembly labor by 25 minutes.

Zonal designs reduce discrete ECU counts from 100 to fewer than 10, while loading each remaining unit with higher compute budgets and ASIL D safeguards. Actuator makers now embed inverters and motor drivers inside the housing, which slashes copper by 30% yet requires 150 °C thermal endurance. Sensor backlogs stay acute, but pedal modules evolve into active haptic devices that encourage one-pedal driving, creating a modest but sticky revenue stream.

By Propulsion Type: BEVs Dominate, Hybrids Trail

Battery-electric vehicles captured 61.27% demand in 2025 and head toward a 15.13% CAGR to 2031, cementing their role as the core growth engine for the X-by-wire systems market. Eliminating 12 kg of hydraulics and columns extends the range by 1.5% on a 75 kWh pack, nudging vehicles over subsidy thresholds in many countries. Internal-combustion cars still account for 38% of light-duty builds, facing USD 200 million integration costs per platform, yet delaying by-wire retrofits.

Hybrids gain from regen blending but must keep vacuum boosters for engine-off moments, diluting savings. BEV skateboard layouts shorten signal paths by 40%, enabling tighter torque vectoring. Corner-module frames let fleet operators swap boxes or cabins in 90 minutes, something combustion frames rarely achieve due to driveline packaging. Cybersecurity posture differs: BEVs with zonal networks expose fewer CAN nodes than hybrids that retain legacy sub-nets.

Geography Analysis

Europe led the X-by-wire systems market with 36.83% revenue in 2025 because EU safety rules require electronic lane-keeping and braking, and CO₂ goals reward every kilogram saved. Germany, the United Kingdom, France, and Italy now host multiple steer-by-wire launches from Mercedes, Jaguar Land Rover, and Audi. Suppliers rely on local test tracks and TÜV certification labs that expedite ASIL D validation, reinforcing Europe’s early-adopter status.

Asia Pacific will register the fastest regional expansion at 15.17% CAGR to 2031, buoyed by China’s Level 3 subsidy roadmap and Japan’s luxury steer-by-wire rollouts. China’s GB 7258 emergency-brake rule accelerates medium and heavy truck adoption because electro-mechanical calipers beat a 200-millisecond air-brake delay. South Korea’s Hyundai and Kia have public programs to release steer-by-wire crossovers in 2027, while India restricts fitment to premium SUVs due to price sensitivity.

North America trails slightly; Tesla’s Cybertruck steer-by-wire and REE’s FMVSS-cleared corner modules spur momentum, but NHTSA has yet to issue permanent steer-by-wire rules, capping early volumes at 2,500 units per model. South America, the Middle East, and Africa remain niche markets because BEV penetration is low and hydromechanical platforms persist. Turkey and Saudi Arabia emerge as knock-down kit assembly hubs that may transition to by-wire once regional battery gigafactories scale.

Regulatory Landscape

X-by-wire homologation is anchored by UNECE vehicle regulations and safety standards that specify how electronic steering and braking replace mechanical linkages. For steer-by-wire, UN Regulation No. 79 (steering equipment) is a central type-approval reference, including provisions for Automatically Commanded Steering Functions (ACSF) and Remote-Controlled Parking (RCP), while ISO 26262 functional safety supports the safety-case and development lifecycle for ASIL-rated ECUs and actuators.

Regulatory change management is now a design constraint as WP.29 GRVA advances updates to UN R79, including work toward the 05 series of amendments and defined transition timelines (notably the 1 September 2027 and 1 September 2029 milestones for acceptance of approvals across series). In parallel, national pathways such as the UK Vehicle Certification Agency (VCA) Individual Vehicle Approval (IVA) compliance approach shape evidence expectations for steer-by-wire submissions, reinforcing redundancy, fault handling, and validation traceability alongside cybersecurity practices aligned with ISO/SAE 21434.

Value Chain Analysis

The x-by-wire value chain runs from semiconductor and sensing inputs (MCUs, power devices, position and torque sensors) to actuator and motor subsystems (electromechanical calipers, steering actuators, pedal modules, and backup energy storage), then to Tier-1 integration into safety-certified platforms. Tier-1 suppliers such as Bosch, Continental, ZF Friedrichshafen, and JTEKT typically own system-level validation and ASIL D safety cases, integrating hardware redundancy, software diagnostics, and E/E architecture compatibility (zonal or domain-control) to meet OEM program gates.

Upstream constraints and specialization influence sourcing strategies, with redundancy-grade sensors, safety microcontrollers, and high-temperature electronics affecting both lead times and certification schedules. Partnerships are also used to secure industrialization of electromechanical architectures: in April 2024, BWI Group and thyssenkrupp Steering announced a long-term partnership to develop and manufacture electro-mechanical braking (EMB) systems, with mass production and delivery scheduled for 2026. That sequence shows how braking and steering specialists combine manufacturing scale with chassis-by-wire know-how to move from pilots into series supply.

Competitive Landscape

Continental, ZF Friedrichshafen, Bosch, and JTEKT collectively own most long-term supply deals, reflecting their ASIL D track record and vertically integrated sensor-to-software stacks that help automakers achieve 10 failures per billion hours of reliability. Continental pairs motor control firmware with its own ABS actuators to shave latency, while Bosch stretches across semiconductors, sensors, and actuators to protect margins. ZF partnered with Infineon in 2025 to co-develop safety microcontrollers, blending horizontal collaboration with vertical capability.

Start-ups target gaps the giants overlook. REE Automotive bypasses OEM sourcing by pitching fully certified skateboards directly to fleets and body builders. Schaeffler’s corner-module joint venture embeds hub motors, steer-by-wire, and brake-by-wire into a 68 kg unit that simplifies final assembly. Niche players such as Curtiss-Wright supply aerospace-grade actuators for autonomous shuttles, leveraging mil-spec durability to command premium pricing.

Cybersecurity compliance has become a key differentiator. Bosch, Continental, and ZF maintain in-house penetration testing teams and hardware security modules, enabling them to guarantee ISO/SAE 21434 conformance. In contrast, smaller tier-2 suppliers often outsource testing, thereby slowing time-to-market. Patent filings for dual-redundant torque sensing jumped 22% in 2025, with Infineon, Bosch, and Continental leading the grants. Competition now blends hardware reliability, software upgradability, and provable cyber resilience, reshaping procurement scorecards.

X-by-wire System Industry Leaders

Infineon Technologies

JTEKT Corp.

ZF TRW Automotive Holdings Corporation

Robert Bosch GmBH

Continental AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace is the shift from partial by-wire (brake-by-wire or steer-by-wire alone) to full drive-by-wire chassis integration, where value shifts from discrete components toward safety-certified platforms and software-defined tuning. In 2026, multiple series-production signals reinforced this pathway: Nexteer commenced series production of steer-by-wire for a Chinese NEV positioned as the first passenger vehicle with a full drive-by-wire chassis. Mercedes-Benz also confirmed steer-by-wire introduction for the facelifted EQS in 2026 with ZF as supplier, expanding European reference programs beyond early luxury rollouts.

Another opportunity is scaling electromechanical braking and integrated brake control to support regeneration blending, packaging simplification, and fail-operational architectures needed for higher ADAS capability. Chery launched the Exeed EX7 in China described as a mass-produced passenger car with pure electronic mechanical braking (EMB), and BWI Group launched mass production of its iDBC1 integrated brake control (1-box) system in Europe for a global automaker in May 2026. These series moves create procurement pull for ASIL-ready ECUs, actuators, and redundancy components (including backup power elements and safety microcontrollers), while also increasing the value of validated toolchains and test capacity that shorten ISO 26262 and UNECE R79 evidence cycles.

Recent Industry Developments

- May 2026: JTEKT Corporation introduced the Syncusteer brand for its linkless steer-by-wire system and moved to trademark registration as it broadens proposals to global automotive customers. The branding and commercialization push supports wider OEM sourcing discussions and helps standardize how the company positions safety, redundancy, and packaging benefits across regions.

- December 2025: JTEKT Corporation announced the installation of its Pairdriver steering control technology in the Toyota RAV4 as part of a move toward mass-market software-defined vehicle features. Bringing steering control functions into a high-volume nameplate strengthens the business case for scalable electronic steering architectures that can integrate with by-wire and zonal E/E roadmaps.

- November 2024: Infineon Technologies entered a multi-year collaboration with Stellantis focused on next-generation EV power architectures using AURIX microcontrollers and smart power switches. The agreement strengthens the semiconductor and power-management foundation needed for safety-critical chassis electronics, supporting higher compute and redundancy requirements that x-by-wire programs impose on E/E platforms.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the x-by-wire systems market covers revenue generated from electronic control systems that replace mechanical or hydraulic linkages in vehicle functions. In-scope systems take sensor inputs, route them through controllers, and execute commands via actuators.

Scope exclusions: we exclude non-automotive by-wire uses (such as aerospace or industrial controls) and pure mechanical or hydraulic systems that do not execute commands electronically.

Segmentation Overview

- By Type

- Throttle-by-wire System

- Brake-by-wire System

- Steer-by-wire System

- Park-by-wire System

- Shift-by-wire System

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

- By Component

- Sensors and Pedal Modules

- Actuators

- Electronic Control Units (ECUs)

- By Propulsion Type

- Internal-Combustion Engine Vehicles

- Hybrid Vehicles

- Battery-Electric Vehicles

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary, align terminology, and build an initial set of demand and supply indicators that can be checked later in interviews. We relied on public and official sources, including vehicle production statistics from international automotive bodies, road safety and vehicle regulation publications (such as NHTSA and UNECE), trade and customs datasets for automotive electronics flows, and technical literature in peer-reviewed automotive engineering journals.

To anchor model inputs, we also reviewed company annual reports, filings, and investor presentations for system revenue cues, platform announcements, and regional exposure. We then cross-referenced association websites and reputable press for rollout timelines. Where coverage gaps existed, paid subscriptions for company financials and intelligence were used to standardize entity mapping, and a patent database subscription was used to track activity around steer-by-wire and brake-by-wire architectures. These desk sources are illustrative only, and we consulted additional public references during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating adoption curves and pricing logic for key by-wire functions across passenger and commercial vehicles, then stress-testing regional timing differences for new platforms. We spoke with system suppliers, component specialists, vehicle program stakeholders, and aftermarket-aware experts across APAC, EMEA, and the Americas, which helped close gaps left by public data and made assumptions more realistic.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 13% | APAC: 49% |

| Mid tier: 46% | Functional/Unit leaders: 41% | EMEA: 33% |

| Smaller Players: 16% | Managers: 46% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach. We reconstructed vehicle production by region into an install-base eligible pool, then converted it into demand using penetration rates for brake-by-wire, steer-by-wire, throttle-by-wire, shift-by-wire, and park-by-wire. After shaping the demand pool, we applied average system values with adjustments for propulsion mix (ICE, hybrid, and BEV) and content differences by vehicle class.

To keep totals practical, we corroborated outputs with selective bottom-up approximations, such as sampled system ASP ranges shared in interviews, cross-checks against supplier revenue exposure, and channel checks on ECU, actuator, and sensor content per vehicle. Key inputs included regional light vehicle and commercial vehicle production, BEV share by region, safety and redundancy requirements that can change content levels, typical by-wire adoption timing in new platforms, and observed pricing progression as volumes scale. When bottom-up evidence was incomplete for smaller regions, the gap was handled using calibrated proxy ratios from similar markets, and then corrected after expert review.

Forecasting was carried out using scenario analysis supported by a light multivariate regression layer, where outputs are guided by macro vehicle production outlook, electrification rates, and expected by-wire penetration improvements from platform refresh cycles. Assumptions were kept transparent so the model can be repeated and updated when new production plans and regulation changes become visible.

Data Validation & Update Cycle

Model outputs were validated through multiple checks. First, we compared implied by-wire shipments per vehicle against known platform launch patterns and component content norms. Then we reviewed whether regional totals align with vehicle output and electrification signals. When variances looked unusual, we revisited underlying inputs and re-contacted relevant experts to confirm whether it reflected a real shift (for example, a delayed program) or an assumption error.

A second analyst review is completed before sign-off, so calculation logic, currency treatment, and year alignment remain consistent. Reports are refreshed annually, and interim updates are made when material events occur, such as major regulatory actions or significant platform announcements. Before delivery, a final pass is completed to ensure clients receive the most current view available at the time of release.

Mordor Intelligence's X By Wire Systems Market Size Compared With Other Published Estimates

Published numbers for x-by-wire systems do not always match because teams can define the boundary differently, and they also select different base years, vehicle coverage, and pricing paths. Differences can also come from how quickly adoption is assumed to move from premium platforms into mid-volume vehicles, which can change near-term market size.

By tracking install-rate logic by system type and vehicle output, Mordor Intelligence keeps the model tied to automotive production and propulsion mix, while some estimates fold in broader electronics content or extend pricing assumptions without the same platform-level cross-checks. Currency timing and refresh cadence matter as well, since EV programs can shift regional shares within a year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 29.69 B (2026) | |

| Global Consultancy A | USD 25.88 B (2024) | Uses an earlier base year and frames the market as automotive x-by-wire revenue in 2024, which can understate the run-up from newer brake-by-wire and steer-by-wire platform launches that land closer to 2026. |

| Industry Publisher B | USD 24.80 B (2024) | Applies a long forecast window starting from 2024 and may embed more aggressive price and content expansion across vehicle types, which can lift long-term totals even if near-term penetration is not validated against production mix. |

The table indicates that the spread is mainly explained by year alignment and how adoption and pricing are carried forward from early programs into mass platforms. Our approach stays repeatable because penetration, vehicle output, and content assumptions are written into the model and checked back with experts before totals are finalized.

Key Questions Answered in the Report

How large will the X-by-wire systems market be in 2031?

The X-by-wire systems market size is forecast to hit USD 59.91 billion by 2031 at a 15.07% CAGR from 2026-2031.

Which vehicle category is growing fastest for by-wire adoption?

Medium and heavy commercial trucks show the highest 15.21% CAGR because fleets want predictive maintenance and platooning benefits.

What share do brake-by-wire solutions hold today?

Brake-by-wire captured 38.17% of 2025 revenue, making it the largest segment.

Why do battery-electric architectures favor steer-by-wire?

BEV flat floors free packaging space, and removing columns and boosters cuts 8-12 kg, expanding driving range 1.5%.

Which region will outpace others through 2031?

Asia Pacific posts the fastest 15.17% annual growth due to China’s intelligent-vehicle subsidies and Japan’s early luxury deployments.

What is the main hurdle for new suppliers?

ASIL D functional-safety certification often takes 18-24 months and costs USD 45 million-plus, delaying market entry.

Page last updated on: