Intelligent Document Processing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

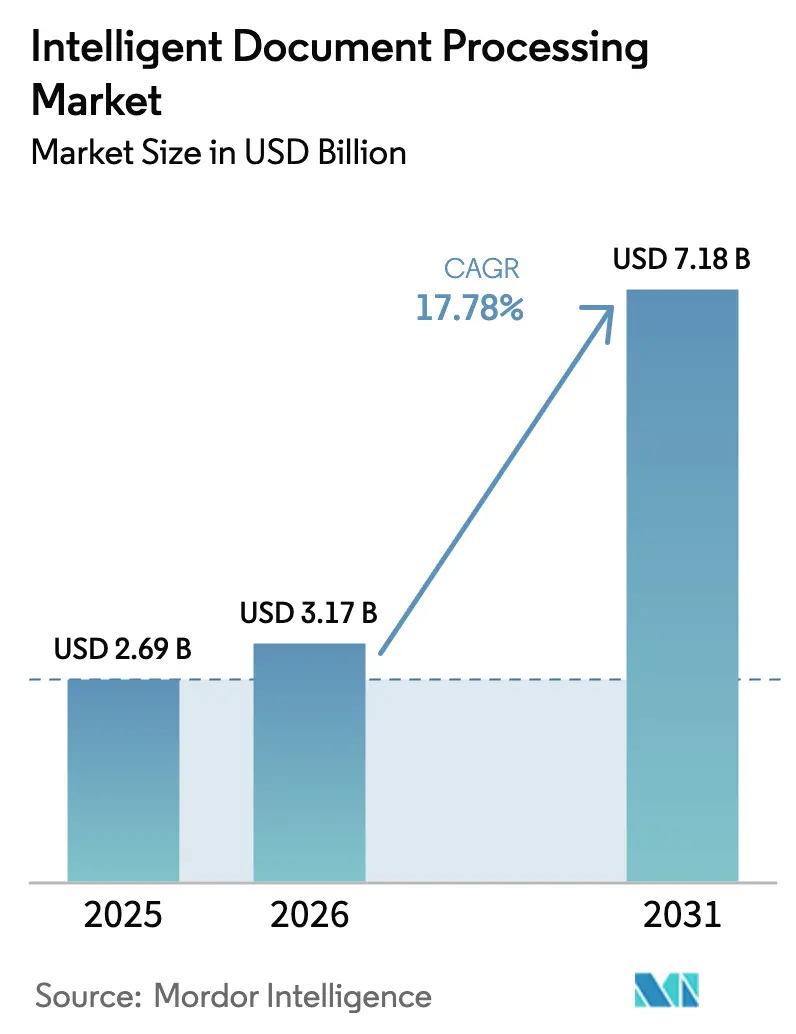

| Market Size (2026) | USD 3.17 Billion |

| Market Size (2031) | USD 7.18 Billion |

| Growth Rate (2026 - 2031) | 17.78% CAGR |

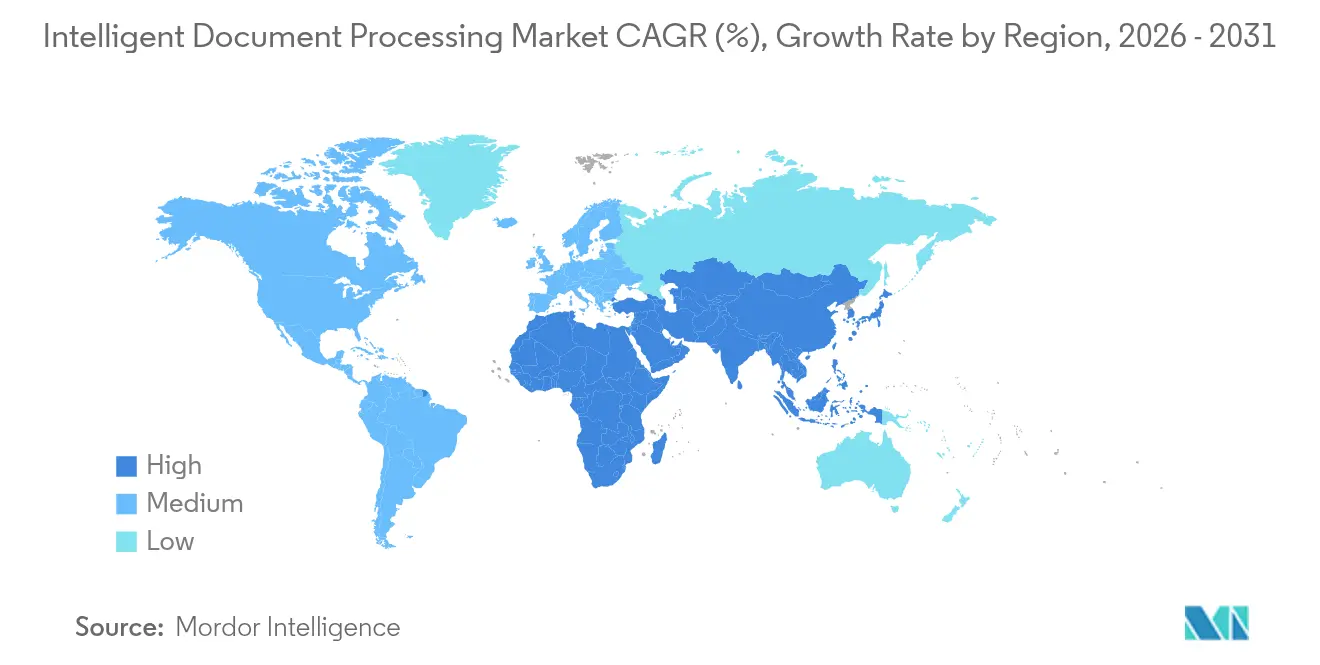

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intelligent Document Processing Market Analysis by Mordor Intelligence

Intelligent document processing market size in 2026 is estimated at USD 3.17 billion, growing from 2025 value of USD 2.69 billion with 2031 projections showing USD 7.18 billion, growing at 17.78% CAGR over 2026-2031. Growth rests on the rapid shift to AI-driven automation, expanding cloud adoption, and mounting regulatory demands for straight-through claims processing in insurance. Enterprises are also reacting to rising volumes of AI-generated documents, which heighten fraud-detection spending, while legacy OCR limitations continue to slow digital initiatives. Providers with vertically tuned models are gaining traction as buyers seek out-of-the-box accuracy and faster time-to-value. Meanwhile, the proliferation of remote work embeds touchless document workflows into core operations, placing extra emphasis on scalable cloud platforms that can be updated in real time.

Key Report Takeaways

- By component, software platforms led with 62.55% of intelligent document processing market share in 2025, whereas services are projected to expand at a 19.15% CAGR to 2031.

- By deployment mode, cloud solutions captured 74.10% revenue share in 2025 and continue to grow the fastest at a 21.85% CAGR through 2031.

- By enterprise size, large enterprises held 64.35% of the intelligent document processing market share in 2025, while small and medium enterprises are advancing at a 19.35% CAGR through 2031.

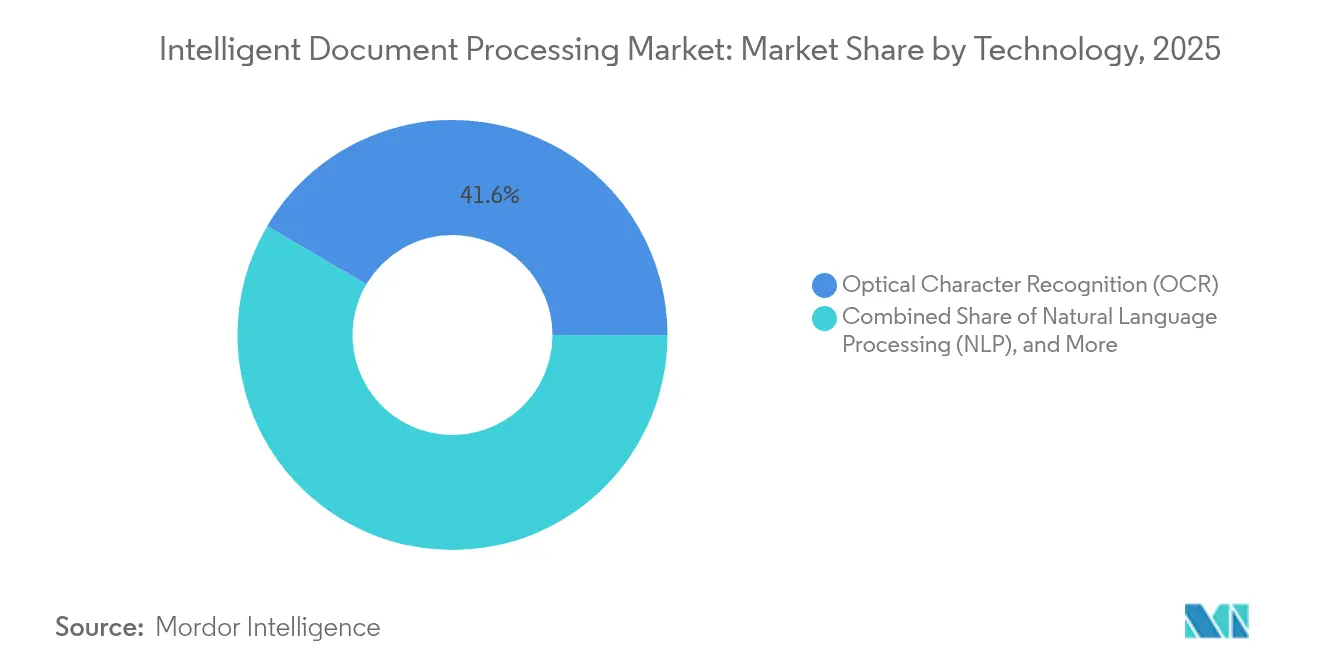

- By technology, Optical Character Recognition commanded 41.55% share of the intelligent document processing market size in 2025, yet natural language processing is pacing the field with a 22.95% CAGR to 2031.

- By end-user industry, banking, financial services, and insurance accounted for a 5.25% share of the intelligent document processing market size in 2025, while healthcare and life sciences are set to rise at a 20.95% CAGR through 2031.

- By geography, North America led with 35.55% revenue share in 2025; Asia-Pacific is the fastest-growing region at a 19.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Intelligent Document Processing Market Trends and Insights

Driver Impact Analyis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing investments in digital transformation | +4.2% | Global; Asia-Pacific leading | Medium term (2-4 years) |

| Shift toward cloud-native IDP platforms | +3.8% | North America and EU core, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Rising demand for remote work automation | +2.9% | Global, accelerated post-COVID | Short term (≤ 2 years) |

| Emergence of industry-specific IDP accelerators | +2.1% | North America and EU first, scaling globally | Medium term (2-4 years) |

| Insurance regulatory push for straight-through claims | +1.8% | North America and EU regulatory zones | Long term (≥ 4 years) |

| AI-generated documents increasing fraud-detection spend | +1.4% | Global, concentrated in financial hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Investments in Digital Transformation

Firms citing workforce constraints in earnings calls are 45% more likely to discuss automation benefits, underscoring how intelligent document processing market adoption now stems from competitive differentiation rather than cost cutting. Early adopters also report that successful projects uncover adjacent workflows ripe for automation, creating a flywheel of data network effects and continuous process optimization. The implication is clear: first movers gain a learning-curve advantage that late entrants struggle to match.

Shift Toward Cloud-Native IDP Platforms

Cloud deployments captured 74.80% share by 2024 and are expanding at 22.20% CAGR because organizations favor elastic scaling and rapid model refreshes over infrastructure control. API-first architectures enable real-time processing in global operations where localized compliance demands quick retraining and redeployment of models. European firms, pressed by GDPR obligations, gravitate toward cloud providers offering dynamic data-residency controls and instant audit trails, turning cloud-native IDP from an IT preference into a prerequisite for cross-border expansion [1]DocuWare, “GDPR Compliance Through Intelligent Document Management,” docuware.com.

Rising Demand for Remote Work Automation

Hybrid work models push enterprises to redesign document-heavy processes for asynchronous handling. Roughly 75% of employees now rely on AI tools that lift customer-service productivity by 14%, reinforcing the intelligent document processing market shift to touchless workflows. In healthcare, automated summarization trims medical-record handling time by 50% UiPath. Public agencies also benefit: the U.S. Department of Homeland Security’s GenAI playbook outlines how remote automation raises service levels even in heavily regulated environments.

Emergence of Industry-Specific IDP Accelerators

Domain-tuned accelerators routinely outperform generic platforms. Specialized healthcare models reach 98% accuracy and reduce deployment cycles from months to weeks. A leading manufacturer achieved 90% touchless processing of delivery notes within 2 weeks, unlocking EUR 5 million (USD 5.5 million) in annual savings thanks to tailored templates and pretrained vocabularies. Vendors cultivating deep vertical expertise can command premium pricing while delivering measurable ROI that CFOs readily validate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex and fragmented data-privacy regulations | -2.1% | EU GDPR core, expanding globally | Long term (≥ 4 years) |

| Scarcity of annotated training data | -1.8% | Global, acute in specialized verticals | Medium term (2-4 years) |

| Rising carbon-accounting scrutiny on large-model inference | -1.2% | EU and North America ESG mandates | Long term (≥ 4 years) |

| Talent poaching inflating total cost of ownership | -0.9% | Global tech hubs, Silicon Valley focus | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Complex and Fragmented Data-Privacy Regulations

GDPR and similar laws force enterprises to juggle divergent consent rules, residency demands, and right-to-be-forgotten requests, extending IDP roll-outs and inflating compliance budgets. Multinationals often maintain separate pipelines for different regions, complicating model governance and driving up maintenance costs. Vendors with proven compliance toolkits thus gain a competitive edge, while newcomers without legal resources face higher barriers to entry.

Scarcity of Annotated Training Data

Vertical-specific annotation requires domain-certified professionals, pushing up labeling costs and lengthening development timelines. Healthcare records, legal contracts, and fraud-detection documents often cannot be pooled across firms due to privacy constraints, compelling each organization to build proprietary datasets [2]BytePlus, “Secure Data-Labeling Solutions for Regulated Industries,” byteplus.com. Those with sizable internal document repositories and secure labeling teams can sustain superior model performance, whereas smaller players may need to outsource to specialized data-labeling services that meet stringent security standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Accelerate Despite Software Dominance

Software retained 62.55% of the intelligent document processing market share in 2025, yet service revenues are climbing at a 19.15% CAGR as enterprises discover that success hinges on process redesign and change management, not just licenses. Post-implementation, many organizations outsource ongoing model tuning and monitoring to managed-service partners, turning operational complexity into a subscription opportunity.

The intelligent document processing market increasingly values outcome-based engagements over traditional seat licenses. Platform vendors now cultivate alliances with systems integrators that can manage compliance mapping, workflow re-engineering, and user training at scale. As more firms adopt mature governance frameworks, services are expected to command a growing slice of total contract value.

By Deployment Mode: Cloud Supremacy Accelerates

Cloud offerings controlled 74.10% of revenue in 2025, with adoption expanding at 21.85% CAGR, cementing a decisive architectural pivot. The intelligent document processing market size linked to cloud subscriptions is forecast to widen further as multinational firms rely on centralized model orchestration coupled with localized inference endpoints.

On-premises systems persist where data-sovereignty rules or air-gapped architectures are mandatory, notably in defense and certain public-sector agencies. Hybrid blueprints are gaining favor: sensitive pre-processing remains in local data centers, while model training and bulk analytics reside in the cloud. Providers that can knit these environments together without latency penalties stand to gain share.

By Enterprise Size: SME Growth Momentum Challenges Enterprise Dominance

Large enterprises still command 64.35% of revenue; however, SMEs are registering 19.35% CAGR, signaling a democratizing trend. Cloud marketplaces now list entry-level intelligent document processing industry packs priced for smaller budgets, letting mid-sized exporters automate invoices, bills of lading, and compliance forms almost overnight.

SMEs often leapfrog incumbents by adopting pre-trained vertical templates and low-code interfaces, cutting deployment cycles from months to days. Conversely, Fortune 1000 firms continue to dominate complex, multi-jurisdictional projects that require layered governance and integration into legacy ERP suites. The coexistence of fast-moving SMEs and compliance-bound conglomerates injects diverse requirements that keep vendors innovating across the price-performance spectrum.

By Technology: NLP Disrupts OCR Hegemony

OCR still holds 41.55% share, but NLP is expanding at 22.95% CAGR as enterprises transition from character recognition to semantic understanding. The intelligent document processing market size attributable to NLP is rising because contextual extraction fuels end-to-end automation without manual validation.

In parallel, computer vision and layout-analysis modules help decode complex forms and mixed-media files, while deep-learning ensembles push standard-document accuracy to 99.56%. Vendors investing in multimodal stacks gain a decisive edge because buyers increasingly demand single-platform coverage for structured, semi-structured, and unstructured inputs.

By End-User Industry: Healthcare Transformation Accelerates

BFSI held a 5.25% share in 2025, reflecting early investments in KYC, claims, and loan-processing use cases. Yet, healthcare and life sciences are forecast to grow at 20.95% CAGR as regulators endorse electronic prior-authorization mandates and value-based care models compel faster documentation cycles.

Retailers and e-commerce platforms leverage IDP for speedy onboarding and supply-chain visibility, while manufacturers drive paperless logistics and quality-control reporting . These sector-specific gains reveal that the intelligent document processing market is no longer confined to paperwork-heavy financial institutions but is diffusing across industries that view unstructured data as a latent efficiency reserve.

Geography Analysis

North America commanded 35.55% of revenue in 2025, giving it the largest intelligent document processing market share. Deep SaaS penetration, abundant AI-skilled talent, and mature regulatory frameworks keep enterprise spending high, especially in financial services, insurance, and healthcare. Cloud hyperscalers shorten deployment cycles and lower ownership costs, while federal stimulus programs channel new funding into public-sector automation projects. Collectively, these factors secure North America’s lead even as faster-growing regions close the gap.

Asia-Pacific is set to post a 19.75% CAGR through 2031, the fastest pace among all regions. China has earmarked USD 2.1 billion for generative-AI investments that underpin large-scale document-automation rollouts. Governments in India, Singapore, and Australia use tax breaks and cloud credits to push businesses toward paperless workflows, and local cloud providers partner with IDP specialists to satisfy strict data-residency rules. Small and medium enterprises adopt mobile-first, API-driven tools to streamline invoices and trade documents, while regional banks deploy IDP for real-time KYC checks as anti-money-laundering rules tighten.

Europe remains influential thanks to GDPR-driven demand for built-in privacy controls, though its growth rate trails Asia-Pacific. Enterprises favor cloud platforms offering configurable data-residency and automated audit trails, yet on-premises systems still prevail in defense and certain public-administration slices. South America and the Middle East and Africa are at earlier stages, but modernization agendas are driving pilot projects that bundle pre-trained language packs with pay-as-you-go pricing. Vendors must therefore balance rapid cloud rollouts in high-growth regions with deep compliance capabilities in mature jurisdictions to capture the full intelligent document processing market size opportunity worldwide.

Competitive Landscape

The intelligent document processing market remains moderately fragmented, with more than 60 active vendors. No single firm holds an overwhelming share, yet tier-one providers—ABBYY, UiPath, and IBM—leverage broad portfolios and extensive partner programs to win global mandates. Cloud hyperscalers such as Microsoft, Google, and Amazon fold document understanding into their larger AI stacks, exerting pricing pressure on specialists while raising customer expectations for seamless integration with existing cloud services.

Strategic focus is drifting from horizontal breadth to vertical depth. Vendors offering healthcare-specific language models or insurance claims accelerators routinely win deals on implementation speed and accuracy, even when their core OCR is comparable to generic alternatives. At the same time, open-source initiatives like IBM’s Docling foster an ecosystem of community-driven add-ons, enabling mid-tier providers to enhance capabilities without starting from scratch.

Start-ups armed with transformer-based architectures and low-code tooling are finding white-space in the SME segment, where ease of use outweighs exhaustive feature lists. Meanwhile, established players shore up positions through joint ventures with systems integrators and industry consortia, aiming to lock in proprietary datasets and compliance certifications that newcomers cannot easily replicate.

Intelligent Document Processing Industry Leaders

IBM Corporation

UiPath Inc.

OpenText Corporation

ABBYY Solutions Ltd.

Automation Anywhere, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: IBM donated three open-source projects—Docling, Data Prep Kit, and BeeAI—to the Linux Foundation, reinforcing community collaboration around document AI.

- February 2025: IBM released Granite 3.2 with multimodal visual-document understanding and a dedicated instruction-tuning dataset, DocFM.

- October 2024: UiPath integrated Anthropic Claude into its Autopilot and Clipboard AI modules, boosting unstructured-data extraction accuracy.

- June 2024: Affinda raised USD 10 million to scale AI document-automation tools aimed at high-volume back-office workflows.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the intelligent document processing (IDP) market as every software platform and managed service that ingests semi-structured or unstructured documents, applies AI techniques such as OCR, natural-language processing, and machine-learning classifiers, and returns clean data to downstream business systems and workflows. According to Mordor Intelligence, it counts vendor revenue from licenses, subscriptions, and implementation support across industries and regions.

Scope Exclusion: Stand-alone hardware scanners, broad document-management suites without embedded AI extraction, and pure manual data-entry services are not covered.

Segmentation Overview

- By Component

- Software (Platform and SDKs)

- Services (Implementation, Managed)

- By Deployment Mode

- Cloud

- On-Premises

- By Enterprise Size

- Large Enterprises

- Small and Mid-sized Enterprises (SMEs)

- By Technology

- Optical Character Recognition (OCR)

- Natural Language Processing (NLP)

- Machine Learning and Deep Learning

- Computer Vision

- By End-user Industry

- Banking, Financial Services and Insurance (BFSI)

- Government and Public Sector

- Healthcare and Life Sciences

- Retail and E-commerce

- Manufacturing and Logistics

- Other Industries (Telecom, Energy, Legal)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with IDP product managers, automation consultants, and IT leaders at banks, insurers, and hospitals across North America, Europe, and Asia-Pacific. Their insights on pricing spreads, cloud adoption pace, and project timelines filled gaps and anchored key assumptions.

Desk Research

We collected spending indicators from the U.S. Bureau of Labor Statistics, Eurostat, and OECD datasets that track office automation investment, and we reviewed papers by NASSCOM, AIIM, and the World Economic Forum quantifying global invoice and claims volumes. Company 10-Ks, SEC filings, Questel patent analytics, and Volza shipment logs helped test vendor revenue splits. Paid sources such as D&B Hoovers and Dow Jones Factiva supplemented competitive intelligence. The sources cited are illustrative, and many others informed data collection, validation, and clarification.

Market-Sizing & Forecasting

Our model combines a top-down and bottom-up approach. Starting with documented global volumes of invoices, bills of lading, and claims, we apply sector-level IDP penetration rates and prevailing subscription prices to size demand. We then corroborate totals with sampled vendor roll-ups and channel checks. Variables such as cloud migration share, GenAI premium uplift, pages per transaction, audit frequency, and large-enterprise automation budgets feed a multivariate-regression and scenario-analysis forecast to 2030. Bottom-up gaps are bridged through expert consensus before finalization.

Data Validation & Update Cycle

Outputs pass anomaly and variance checks against external spend benchmarks and quarterly vendor disclosures. Findings undergo multi-step peer review before sign-off. Reports refresh annually, with interim updates triggered by material events, so clients always receive the latest view.

Why Mordor's Intelligent Document Processing Baseline Earns Trust

Published estimates often diverge because firms choose different inclusion rules, pricing curves, and refresh cadences.

Key gap drivers include whether services revenue is counted, how GenAI premiums are treated, and if adjacent document-management tools are folded into totals. Mordor's scope stays tightly on AI-enabled extraction platforms and applies uniform 2025 currency conversion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.69 B (2025) | Mordor Intelligence | - |

| USD 2.30 B (2024) | Global Consultancy A | Excludes managed-service revenue and counts only core software licenses |

| USD 1.10 B (2022) | Regional Consultancy B | Uses older base year and omits cloud-native platforms launched post-2022 |

| USD 7.89 B (2024) | Industry Association C | Bundles wider document-management and ECM suites, inflating totals |

These differences show how our disciplined scope selection, transparent variable set, and annual refresh cycle give decision-makers a balanced, dependable baseline.

Key Questions Answered in the Report

What is the current size of the intelligent document processing market?

The market is valued at USD 3.17 billion in 2026 and is projected to reach USD 7.18 billion by 2031.

Which deployment mode is growing fastest in intelligent document processing?

Cloud models are expanding at a 21.85% CAGR, reflecting demand for elastic scaling and quick model updates.

Why are small and medium enterprises adopting IDP so rapidly?

Cloud-native platforms with pre-trained templates remove heavy implementation barriers, enabling SMEs to deploy advanced document automation without large IT teams.

Which technology segment is disrupting traditional OCR?

Natural language processing is growing at 22.95% CAGR because it adds contextual understanding to simple text extraction.

How do data-privacy regulations influence IDP projects?

Fragmented rules like GDPR often require separate processing pipelines and localized data storage, increasing both deployment time and ongoing compliance costs.

What regions present the strongest growth opportunities?

Asia-Pacific leads with a 19.75% CAGR as governments and enterprises accelerate digital transformation initiatives.

Page last updated on: