Lecture Capture Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 17.44 Billion |

| Market Size (2031) | USD 59.39 Billion |

| Growth Rate (2026 - 2031) | 27.77% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lecture Capture Systems Market Analysis by Mordor Intelligence

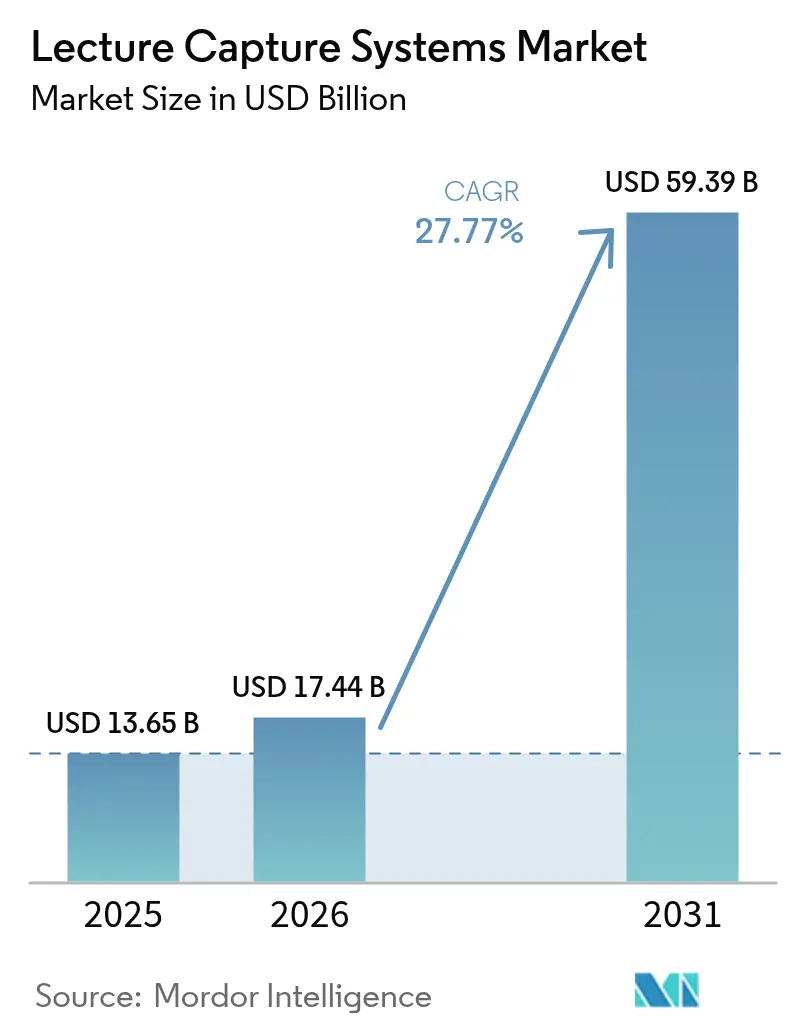

The lecture capture systems market size was valued at USD 13.65 billion in 2025 and estimated to grow from USD 17.44 billion in 2026 to reach USD 59.39 billion by 2031, at a CAGR of 27.77% during the forecast period (2026-2031). Rapid shifts toward hybrid pedagogy, government-funded classroom digitization, and the rise of AI-driven analytics are supporting double-digit expansion. Software-centric deployments are increasingly displacing proprietary hardware as institutions demand cloud-native platforms that incorporate auto-captioning, sentiment analysis, and micro-credential tracking. Compliance mandates under FERPA, GDPR, and similar regulations elevate data-security features from optional extras to purchase prerequisites. Meanwhile, large enterprises intensify spending on asynchronous compliance training, deepening the buyer base beyond traditional higher-education customers.

Key Report Takeaways

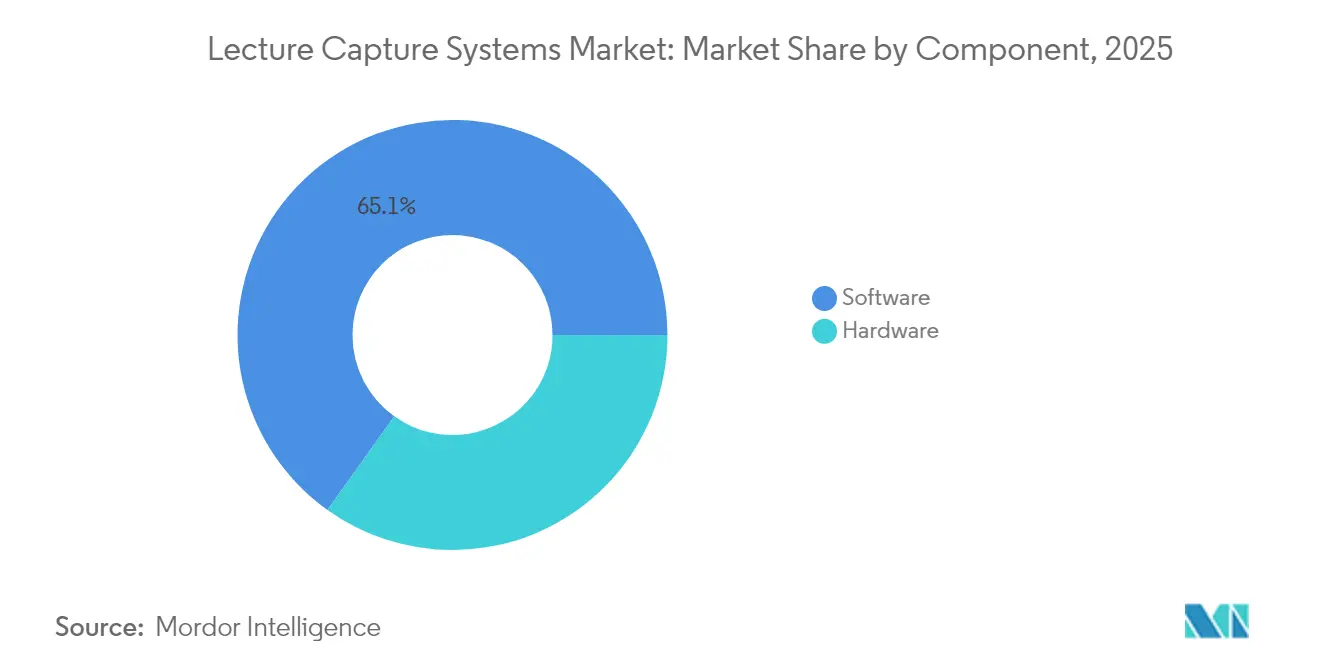

- By component, software captured 65.12% of the lecture capture systems market share in 2025. Cloud delivery is forecast to expand at a 28.67% CAGR through 2031.

- By deployment model, on-premise installations held 53.85% of the lecture capture systems market size in 2025, while cloud-based solutions are projected to advance at 28.95% CAGR to 2031.

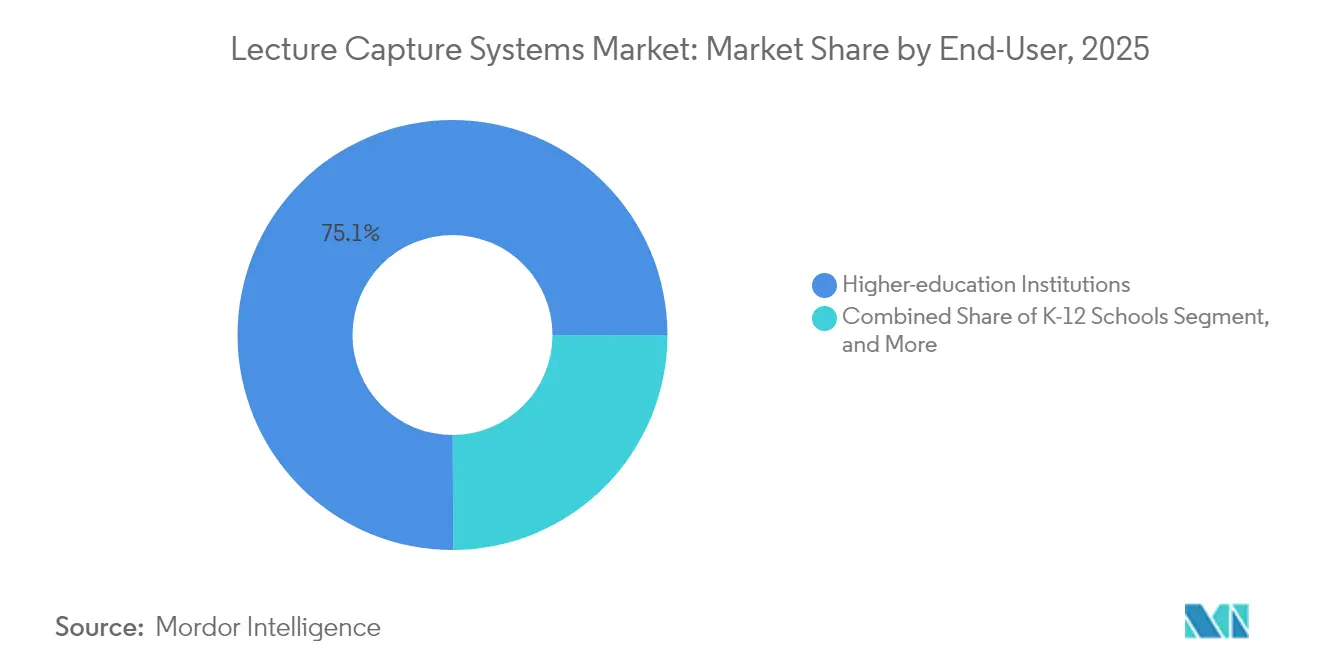

- By end-user, higher-education institutions commanded 75.05% revenue in 2025, and corporate buyers are set to grow at 29.10% CAGR between 2026 and 2031.

- By service type, professional services accounted for 46.20% revenue in 2025, whereas training services will grow fastest at 28.40% CAGR to 2031.

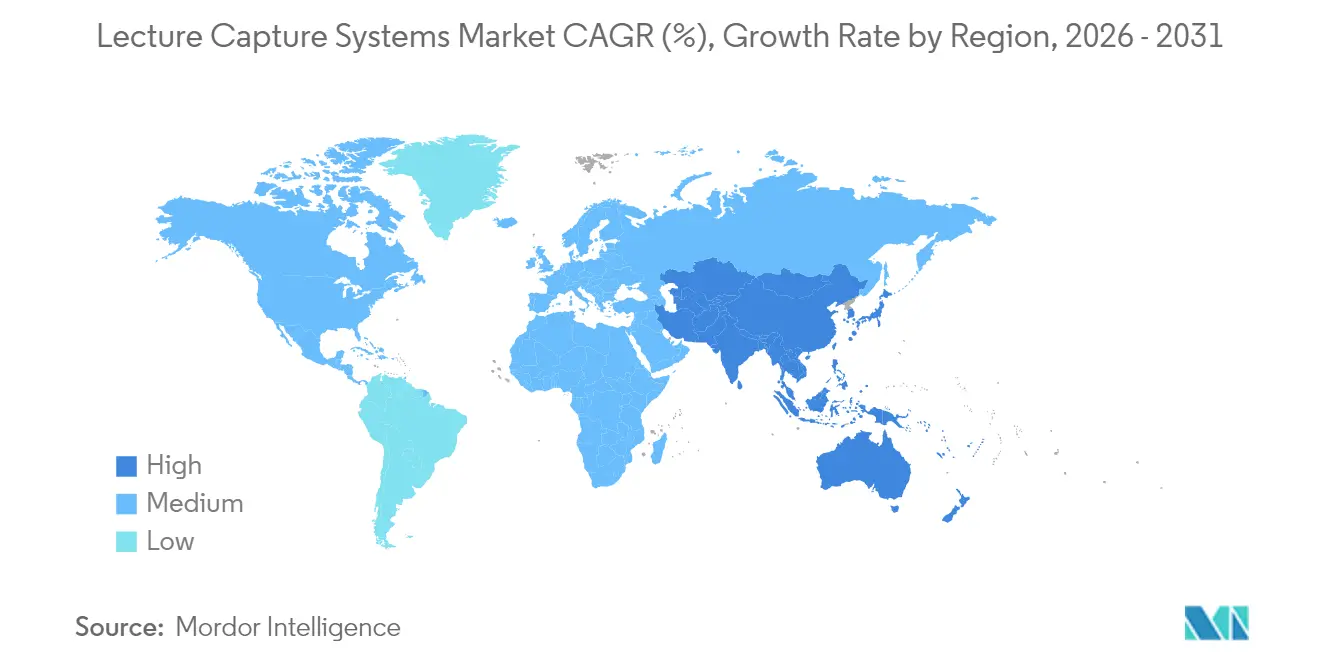

- By geography, North America accounted for 38.10% revenue in 2025, whereas Asia-Pacific will grow fastest at 28.60% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lecture Capture Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for distance and hybrid education | +6.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Government-led digital-learning initiatives | +5.8% | Global, with early gains in South Korea, Germany, Japan, U.S. | Short term (≤ 2 years) |

| Corporate upskilling and compliance training spend | +7.1% | Global, with Asia-pacific core and spill-over to MEA | Medium term (2-4 years) |

| AI-driven micro-credential analytics adoption | +4.3% | North America and EU, expanding to Asia-pacific | Long term (≥ 4 years) |

| Growth of micro-learning and short-form video | +3.9% | Global, mobile-first markets in Asia-pacific and South America | Medium term (2-4 years) |

| LMS–talent-platform integration unlocking ROI | +4.6% | Global, with enterprise concentration in North America | Short term (≤ 2 |

| Source: Mordor Intelligence | |||

Rising Demand for Distance and Hybrid Education

Most of chief online-learning officers report continued student preference for flexible learning pathways, and 52% of online programs generate net revenue, up from 47% in 2020. Learners now expect studio-quality video, interactive transcripts, and mobile-optimized playback as table stakes. Vendors respond by integrating multilingual auto-captioning based on OpenAI Whisper and sentiment-analysis APIs that flag disengagement.[1]Panopto Inc., “Panopto Acquires Elai to Expand AI-Powered Video Creation Capabilities,” panopto.com Hybrid models therefore drive a distinct revenue stream that demands specialized content-production workflows. Institutions that ignore quality thresholds risk erosion of enrollment to competitors that package instruction asynchronously.

Government-Led Digital-Learning Initiatives

The U.S. Digital Equity Act directs USD 811 million toward connectivity, Germany’s Digital Pact 2.0 allocates EUR 2.5 billion, and South Korea designates USD 276 million for classroom digitization.[2]U.S. Department of Commerce, “Digital Equity Act Funding Allocation,” commerce.gov Japan pilots generative-AI content across 52 schools, indicating a shift from device provisioning to algorithm-based instruction.[3]Ministry of Education, Culture, Sports, Science and Technology, Japan, “Generative AI Pilot Program,” mext.go.jp Subsidies lower adoption risk but introduce region-specific compliance mandates such as FERPA or GDPR, forcing vendors to maintain localized SKUs. Such fragmentation increases development costs but expands the addressable demand.

Corporate Upskilling and Compliance Training Spend

Large enterprises intensify their digital learning investments to mitigate regulatory exposure. Accenture logged 13 million training hours in Q3 FY24 as part of its USD 1 billion workforce-development initiative. Organizations that fail to document certifications risk multi-million-dollar penalties, a reality underscored by recent FTC enforcement actions. Compliance needs, therefore, anchor recurring subscriptions even during budget freezes. Platforms that integrate with Workday or SAP SuccessFactors gain preference because they automate re-certification triggers when recorded modules lapse.

AI-Driven Micro-Credential Analytics Adoption

Most academic and corporate learning teams now deploy or pilot AI tools that transform video transcripts into competency maps. Panopto’s October 2024 acquisition of Elai embeds text-to-video generation, letting instructors refresh content without reshooting footage. Micro-credentials demand verifiable engagement metrics, yet opaque algorithms risk over-valuing screen time. Institutions, therefore, scrutinize vendor transparency around model accuracy and bias mitigation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and compliance hurdles | -3.8% | Global, with acute pressure in EU and California | Short term (≤ 2 years) |

| High up-front hardware and integration costs | -4.2% | Global, with concentration in budget-constrained K-12 and emerging markets | Medium term (2-4 years) |

| Faculty push-back over performance scrutiny | -2.7% | North America and Europe, union-dense institutions | Medium term (2-4 years) |

| Fragmented AV standards and interoperability gaps | -3.1% | Global, with legacy infrastructure in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Compliance Hurdles

The FTC levied USD 91.5 million against University of Phoenix in 2024 and USD 5.8 million against Chegg in 2022, demonstrating an appetite for strict enforcement. Most of higher-education institutions suffered breaches in 2024, incurring average costs of USD 3.86 million. The EU AI Act restricts biometric surveillance, compelling vendors to disable facial recognition. These pressures prolong procurement cycles and tilt preference toward suppliers offering indemnification clauses.

High Up-Front Hardware and Integration Costs

Dedicated lecture-capture appliances range from USD 5,000 to USD 50,000 per room, while integration often consumes up to 30% of deployment budgets. Subscription fatigue also looms as institutions allocate a growing share of learning budgets to software, prompting consolidation toward multi-function vendors. Although cloud delivery reduces capex, data-residency requirements force some campuses to retain costly on-premise infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Centric Growth Outpaces Hardware

In 2025, software dominated the lecture capture systems market, holding a 65.12% share. Meanwhile, cloud delivery is projected to grow at a robust 28.67% CAGR, continuing through 2031. This trajectory reflects institutions prioritizing cloud-native video management suites that include AI captioning and engagement analytics. Hardware contributed the remaining USD 4.76 billion and faces pressure from commoditization as inexpensive webcams and mobile devices satisfy entry-level capture needs. Software-driven offerings deliver gross margins of 70% to 80%, supporting aggressive reinvestment in R&D, whereas hardware carries thinner margins, constrained by supply-chain volatility. Vendors therefore champion “software-first” roadmaps that offload encoding and storage to the cloud, anchoring recurring revenue streams that underpin higher valuations.

Moderate hardware demand endures in flagship lecture theaters where multi-camera switching, balanced audio, and redundant recording remain essential. Epiphan’s Pearl Nexus rack-mount encoder, certified with Panopto in January 2024, illustrates hardware’s pivot toward high-density enterprise installations. Yet software’s rapid gains confirm that institutions value agility over appliance ownership, reinforcing the software premium within the lecture capture systems market.

By Deployment Model: Cloud Expansion Amid Residency Constraints

On-premise deployments represented 53.85% of 2025 revenue but now grow in single digits. Cloud-hosted platforms are projected to grow at a 28.95% CAGR to 2031, driven by elastic scaling, lower maintenance costs, and tight LMS integrations that reduce IT workload. Institutions with unpredictable enrollment, especially during periods of MOOC or executive education peaks, leverage usage-based pricing to avoid capital overspending. However, the GDPR and China’s Personal Information Protection Law necessitate localized data centers, which delays wholesale migration. Hybrid models that combine on-premise capture with cloud archiving have therefore gained favor, helping campuses comply with residency mandates while leveraging cloud-based AI services for transcription and analytics.

As vendors bolster zero-trust architectures and secure SOC 2 Type II certifications, cloud apprehension gradually eases. Still, latency-sensitive engagements such as live polling preserve an on-premise niche. The balance of cost, compliance, and user experience will dictate deployment choices as the lecture capture systems market matures.

By End-User: Corporate Segment Accelerates

Higher-education institutions retained a commanding share in 2025, however, enterprise adoption is the fastest-growing segment, with a forecast 29.10% CAGR. Corporations replace fragmented webinar archives with centralized video hubs that integrate with human capital suites, thereby automating compliance renewals.

Accenture’s scale, 13 million training hours logged in one quarter, signals the magnitude of enterprise demand. K-12 districts tapped USD 811 million in Digital Equity Act funds to outfit classrooms with entry-level solutions, but constrained operating budgets temper growth. Government agencies remain cautious, insisting on FedRAMP or equivalent security certifications before migrating sensitive content to cloud-hosted repositories.

By Service Type: Training Services Gain Momentum

Professional services led service revenue in 2025 as institutions contracted consultancies for workflow mapping and API integration. Yet training services will register the highest CAGR at 28.40% through 2031 because faculty acceptance is pivotal.

Platforms now bundle instructor workshops and micro-credential badges that encourage pedagogical adoption. YuJa’s multi-semester onboarding for the Montana University System improved utilization in less than six months. Such programs convert hesitant professors into advocates, ensuring that lecture capture investments yield measurable student engagement outcomes.

Geography Analysis

North America accounted for 38.10% revenue in 2025, supported by USD 811 million from the U.S. Digital Equity Act and Canada’s CAD 39.2 million CanCode investment. Continued hybrid learning demand underpins license renewals; however, many institutions now enter refresh rather than expansion cycles. Budget restrictions, 61% of organizations reported flat or declining L&D allocations, curb upsell opportunities. Meanwhile, heightened data-privacy enforcement following the University of Phoenix settlement compels vendors to embed FERPA-aligned controls at the core of product architectures.

The Asia-Pacific region is projected to grow at a 28.60% CAGR, the fastest worldwide. South Korea’s USD 276 million classroom initiative, Japan’s generative-AI pilots, and India’s National Education Policy 2020 collectively drive volume. Localization challenges abound: China demands onshore data hosting under its personal-information statute, while Japan favors licensed domestic cloud zones. Vendors must therefore field region-specific instances and language packs to capture share, increasing operational complexity across the lecture capture systems market.

Europe shows steady momentum on the back of Germany’s EUR 2.5 billion Digital Pact 2.0 and EU Digital Europe funding. Yet stringent GDPR requirements suppress rapid cloud migration. The EU AI Act bans certain biometric functions in classrooms, forcing feature roll-backs that slow deployment. Emerging regions, including South America and the Middle East, gain traction through World Bank–backed digital-education grants, though inconsistent broadband and power reliability sustain preference for download-first workflow.

Competitive Landscape

The lecture capture systems market remains moderately fragmented, with the top five vendors collectively holding most of share. Panopto, YuJa, Echo360, and Enghouse’s Mediasite assets lead among software specialists, while Zoom, Microsoft Teams, and Cisco Webex offer embedded recording features that undercut standalone pricing. Panopto enhanced its AI capabilities through the October 2024 acquisition of Elai and secured certifications for NewTek CaptureCast and Q-SYS hardware to facilitate seamless multi-camera deployments. Enghouse’s February 2024 purchase of Mediasite removed a distressed rival, but integration delays postponed feature roadmap updates. Kaltura’s valuation slide from USD 10 to USD 1.78, illustrating revenue growth challenges when content storage costs rise faster than subscription expansion.

LMS interoperability and data-governance assurances now trump video fidelity as differentiators. Vendors rush to deliver plug-and-play connectors for Canvas, Google Classroom, and Schoology, while publishing API libraries for Workday and Oracle. YuJa’s AccessNotes.AI auto-generated study guides, boosting time-on-task metrics, and Epiphan’s AV1 codec support for bandwidth-constrained deployments address niche pain points. Unmet opportunities persist in micro-learning personalization and offline mobile synchronization, especially in emerging markets.

Lecture Capture Systems Industry Leaders

Panopto Inc.

YuJa Corporation

TechSmith Corporation

Echo360 Inc.

Cisco Systems Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: YuJa unveiled AutoRedact.AI, an automated privacy tool that blurs faces and removes screen-captured personal data in recorded lectures before institutional release.

- April 2025: Echo360 launched EchoGo Lite, a freemium mobile application that lets instructors clip, caption, and publish short-form videos directly to major LMS platforms without desktop software.

- January 2025: Instructure partnered with Khan Academy to embed Khanmigo AI tutoring into Canvas LMS, adding personalized learning pathways alongside lecture-capture archives.

- January 2025: Panopto announced hardware certification for the Q-SYS plugin, enabling seamless integration with QSC’s audio-visual ecosystem and simplifying multi-room enterprise deployments.

Global Lecture Capture Systems Market Report Scope

The lecture capture systems market report is segmented by Component (Hardware, and Software), Deployment Model (On-premise, and Cloud), End-User (Higher-education Institutions, K-12 Schools, Corporates and Enterprises, Government and Public Agencies), Service Type (Professional Services, Integration and Maintenance, Training Services), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| On-premise |

| Cloud |

| Higher-education Institutions |

| K-12 Schools |

| Corporates and Enterprises |

| Government and Public Agencies |

| Professional Services |

| Integration and Maintenance |

| Training Services |

| North America | United States | |

| Canada | ||

| South America | Brazil | |

| Mexico | ||

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| By Deployment Model | On-premise | ||

| Cloud | |||

| By End-User | Higher-education Institutions | ||

| K-12 Schools | |||

| Corporates and Enterprises | |||

| Government and Public Agencies | |||

| By Service Type | Professional Services | ||

| Integration and Maintenance | |||

| Training Services | |||

| By Geography | North America | United States | |

| Canada | |||

| South America | Brazil | ||

| Mexico | |||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the lecture capture systems market expected to grow through 2031?

The market is projected to expand at a 27.77% CAGR, rising from USD 13.65 billion in 2025 to USD 59.39 billion by 2031.

Which component represents the largest revenue share today?

Software platforms account for 65.12% of 2025 revenue, confirming the shift from hardware to cloud-native solutions.

Why are enterprises adopting lecture-capture platforms?

Corporations need verifiable records of compliance training and favor systems that integrate with HR suites to automate re-certification schedules.

What is the biggest geographic growth opportunity?

Asia-Pacific is forecast to post a 28.60% CAGR through 2031, driven by government digitization programs in South Korea, Japan, and India.

Which regulatory frameworks most affect product design?

FERPA in the U.S., GDPR in Europe, and China’s Personal Information Protection Law shape data-hosting, privacy, and AI-feature roadmaps.

Page last updated on: