Document Imaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

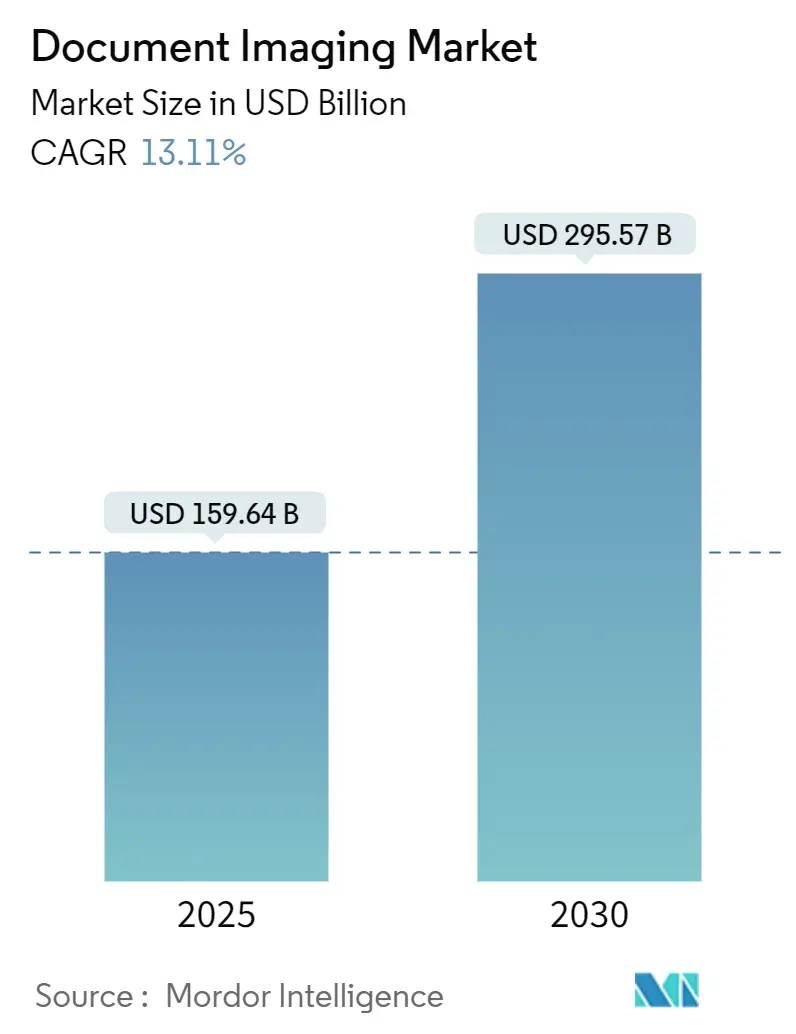

| Market Size (2025) | USD 159.64 Billion |

| Market Size (2030) | USD 295.57 Billion |

| Growth Rate (2025 - 2030) | 13.11% CAGR |

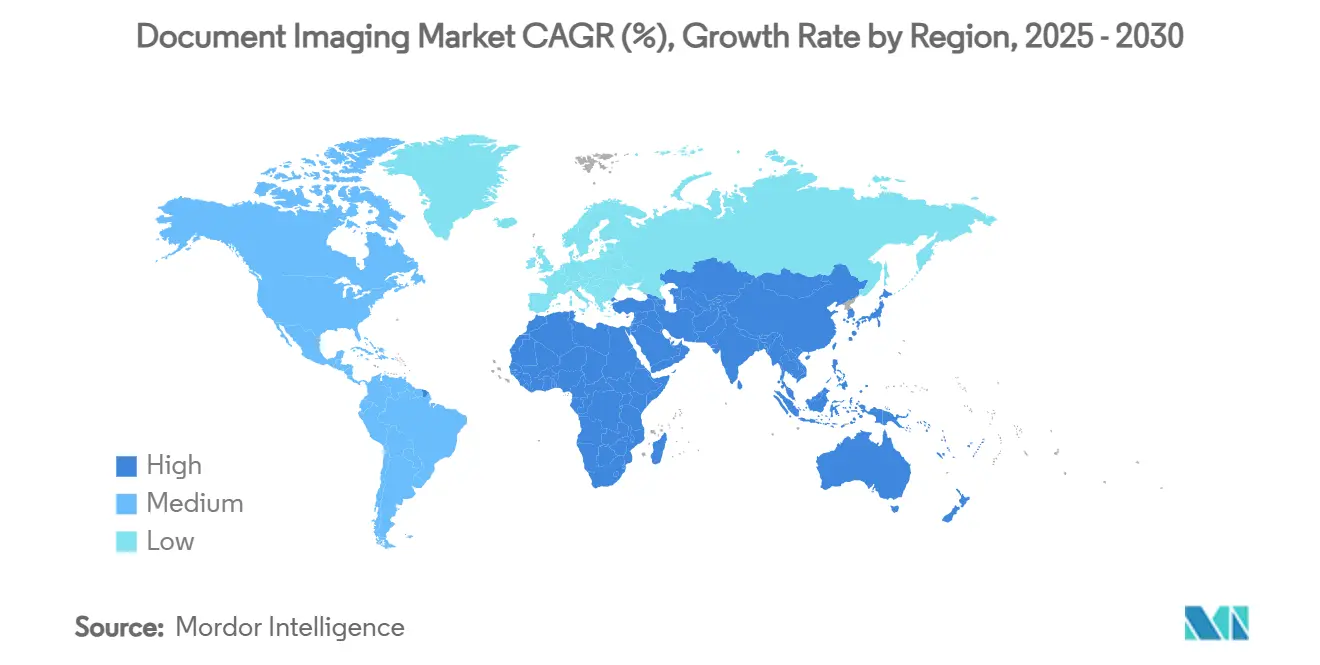

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Document Imaging Market Analysis by Mordor Intelligence

The document imaging market size stands at USD 159.64 billion in 2025 and is projected to reach USD 295.57 billion by 2030, reflecting a 13.11% CAGR. Growth gathers pace from generative-AI document understanding, escalating data-retention rules, and the cost advantages of cloud-native SaaS platforms. Software-centric solutions eclipse hardware as enterprises automate classification and extraction workflows, while rising regulatory fines push healthcare and finance to digitize long-lived records. Cloud subscriptions lower capital barriers, and low-cost mobile capture widens access in emerging economies. Competitive intensity is shifting toward intelligence features rather than scan speed or optical resolution, rewarding vendors that can prove measurable productivity gains.

Key Report Takeaways

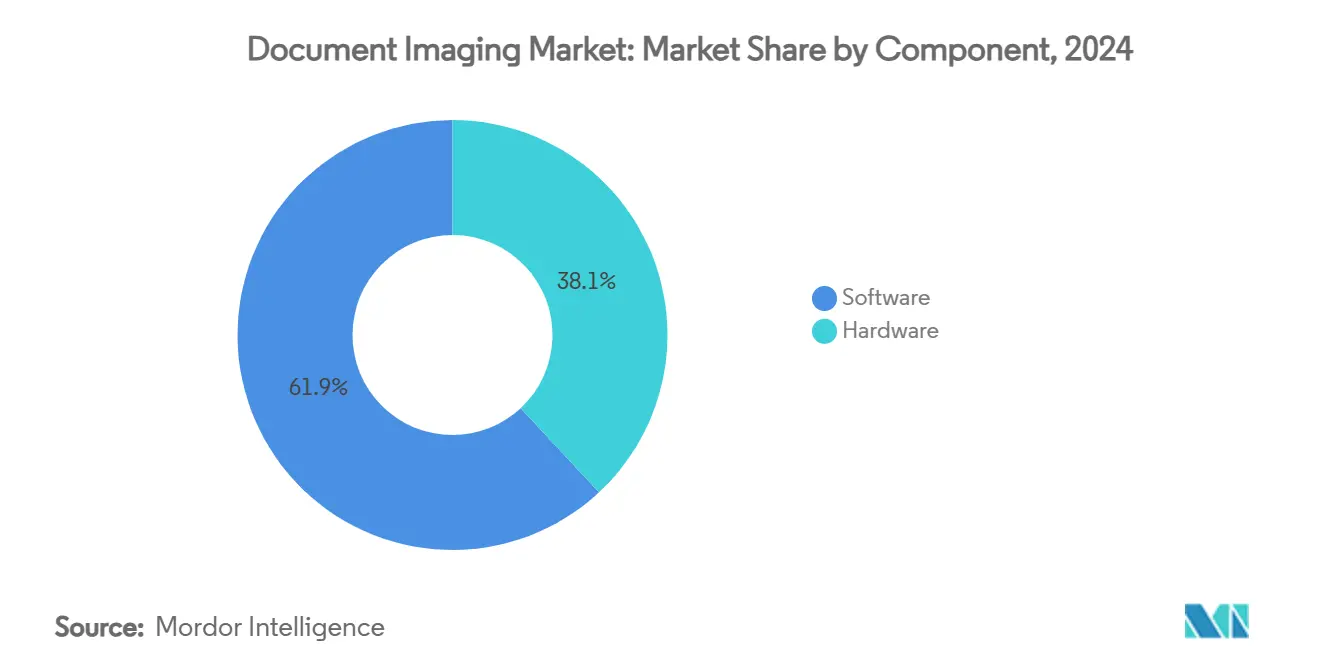

- By component, software commanded 61.94% of the document imaging market share in 2024, while intelligent document-processing software is forecast to expand at 13.19% CAGR through 2030.

- By deployment, on-premise retained 57.24% share of the document imaging market size in 2024; cloud deployments deliver the fastest growth at 13.31% CAGR through 2030.

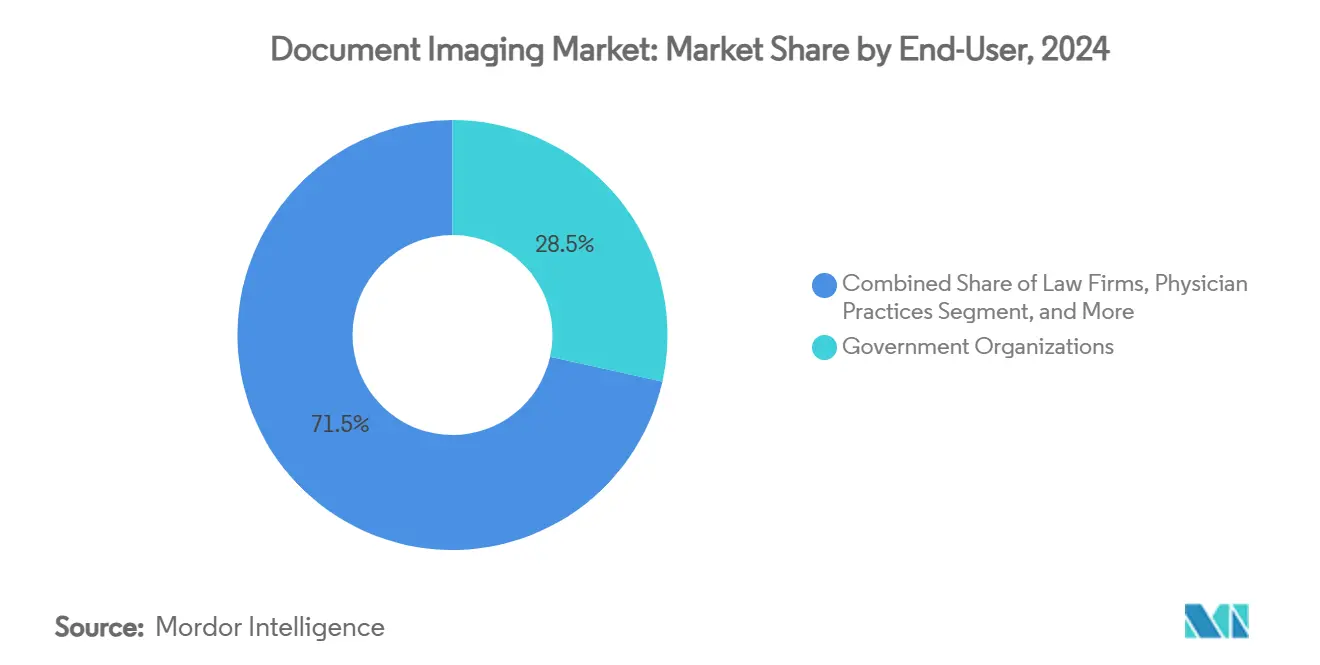

- By end-user, government organizations led with 28.48% share in 2024, whereas physician practices hold the highest growth outlook at 13.56% CAGR through 2030.

- By geography, North America contributed 38.59% revenue in 2024; Asia-Pacific remains the fastest-advancing region at 13.93% CAGR to 2030.

Global Document Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid digital-transformation mandates in public and private sectors | +2.8% | Global, with concentrated impact in North America and EU | Medium term (2-4 years) |

| Stringent data-retention and privacy regulations (HIPAA, GDPR, etc.) | +2.2% | North America and EU primary, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Adoption of cloud-native SaaS imaging platforms that cut CapEx | +2.5% | Global, accelerated adoption in Asia-Pacific emerging markets | Short term (≤ 2 years) |

| Accelerated Electronic Health Record (EHR) rollouts worldwide | +1.9% | Global, with highest impact in North America and Asia-Pacific | Medium term (2-4 years) |

| Generative-AI based intelligent document understanding | +3.1% | Global, led by North America technology adoption | Short term (≤ 2 years) |

| Low-cost mobile capture devices widening emerging-market access | +1.7% | Asia-Pacific core, spill-over to MEA and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Digital-Transformation Mandates Drive Enterprise Modernization

Public agencies and private enterprises now treat paperless workflows as a strategic imperative rather than an IT upgrade. A U.S. city records department cut paper accident-report mail by 75–80% after shifting to web-based submissions, demonstrating quantifiable service gains. [1]Data-Core Systems, “Digital Transformation for City Department of Records,” datacoresystems.com Hybrid work amplifies demand for secure, cloud-accessible repositories that sustain collaboration without physical files. Vendors combining capture devices, intelligent processing, and compliant cloud storage in one stack benefit most from this urgency. The mandate also boosts managed-service uptake as organizations seek turnkey modernization with predictable costs.

Stringent Data-Retention and Privacy Regulations Accelerate Digitization

HIPAA, GDPR, and sector-specific laws drive systematic imaging because fines for non-compliance have escalated. Platforms such as DocuWare carry SOC 2 Type 2 and ISO security certifications that reassure risk-averse buyers. Automated audit trails and lifecycle management outclass manual filing, turning compliance from cost center to efficiency enabler. As regulations tighten in Asia-Pacific, global vendors with built-in governance functions gain ground over niche tools that rely on add-ons.

Cloud-Native Platforms Reshape Capital Expenditure Models

SaaS imaging shifts spending from large, cyclical hardware outlays to pay-as-you-go processing. OpenText recorded USD 455 million in cloud revenue for Q3 FY 2024, an annual rise of 4.4%, underscoring mainstream adoption. Subscription pricing appeals to small and midsize businesses, while automatic updates ease IT burdens. Hybrid deployments also advance, letting enterprises keep some repositories on-premise for sovereignty yet tap elastic cloud processing for burst workloads.

Generative AI Transforms Document Understanding

AI now performs zero-shot classification, contextual search, and summarization. IBM’s open-source Docling project-garnering 30,000 GitHub stars-illustrates developer appetite for pipelines that turn unstructured files into LLM-ready data. [2]IBM, “IBM Adds Open Source Projects Docling, BeeAI, and Data Prep Kit to the Linux Foundation,” ibm.com Healthcare clinics save hours daily by routing incoming faxes to patient charts automatically, freeing staff for higher-value care. Providers lacking AI roadmaps risk displacement by platforms promising rapid productivity wins.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security and privacy concerns in remote/cloud workflows | -1.8% | Global, with heightened sensitivity in EU and healthcare sectors | Short term (≤ 2 years) |

| High upfront cost of production-grade capture hardware | -1.4% | Emerging markets primary, secondary impact in SME segments globally | Medium term (2-4 years) |

| Shortage of Intelligent Document Processing (IDP) specialists | -1.2% | North America and EU primary, expanding globally | Long term (≥ 4 years) |

| Legacy-system integration hurdles in niche vertical apps | -0.9% | Global, concentrated in regulated industries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cyber-security Vulnerabilities Constrain Cloud Migration

Data-breach settlements such as T-Mobile’s USD 31.5 million payment underline the financial stakes. [3]Keepnet Labs, “Top 15 Data Breaches of 2025 and Their Financial Impacts,” keepnetlabs.com Healthcare entities hesitate to move protected health information unless vendors prove end-to-end encryption, granular governance, and third-party attestations. Implementation cycles lengthen as boards demand cyber risk quantification, slowing near-term cloud uptake even though long-run demand remains intact.

Hardware Cost Barriers Limit Emerging-Market Penetration

A 25% tariff on office equipment imported from Mexico and Canada alongside a 10% duty on Chinese devices lifted scanner prices in 2025. Semiconductor shortages further restrict high-speed controller availability, nudging total cost of ownership upward. Cash-constrained buyers pivot to mobile-capture or outsource scanning to service bureaus, restraining hardware revenue but stimulating software-only deployments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Innovation Leads Value Creation

The software segment dominated with 61.94% share in 2024, underscoring how algorithms rather than optics now define competitive edge in the document imaging market. Intelligent document-processing engines are growing at 13.19% CAGR as enterprises adopt machine-learning models that separate, classify, and extract data without exhaustive rulesets. Hardware still matters for high-volume back-file conversion, yet margins face commoditization pressure from generic scanner assemblies. Vendors like Xerox mitigate this by embedding AI agents on-device for instant summarization, effectively blurring hardware-software lines. The pivot to software elevates recurring revenue, encouraging continuous feature releases that lock in customers through productivity gains.

A second trend is the surge of APIs that feed captured content into downstream analytics, turning scanned pages into structured data for RPA and business-intelligence stacks. DocuWare’s takeover of natif.ai adds handwriting recognition and zero-shot separation, proving that acquisitions remain a shortcut to catch up in deep-learning talent. As more endpoints-from printers to smartphones-produce images, centralized AI pipelines will maintain the document imaging market size advantage for platforms designed to ingest diverse inputs.

By Deployment: Cloud Uptake Challenges On-Premise Control

While on-premise still accounts for 57.24% of current revenue, cloud solutions record a 13.31% CAGR thanks to subscription pricing and faster rollout. Early movers in regulated sectors deploy hybrid footprints; sensitive archives stay behind the firewall while burst OCR workloads leverage public cloud GPUs. OpenText booked a 52.6% rise in enterprise cloud orders year over year, signalling accelerating conversion of perpetual licenses to SaaS. The narrative has shifted from if to when cloud becomes the default, with buyer focus turning to data residency, encryption, and audit automation rather than basic functionality.

Cost transparency also tilts decisions. Cloud eliminates forklift upgrades and aligns expenses with volume, an attractive proposition for seasonal industries such as education where scanning peaks in enrollment periods. For multinational firms, unified SaaS deployments avoid duplicative regional hardware, helping compliance teams monitor access centrally. This economics-driven momentum ensures the document imaging market will sustain mixed architectures yet trend inexorably toward cloud-first procurement policies.

By End-User: Healthcare Digitization Spurs Physician Practice Expansion

Government agencies retained 28.48% share in 2024, propelled by mandates to modernize citizen services and meet records-retention statutes. Yet physician practices exhibit the fastest 13.56% CAGR as electronic health record adoption intersects with AI-driven fax routing and chart abstraction. An Image AI Assistant at York Primary Care freed more than 1 hour daily, justifying rapid payback. Hospitals and small clinics alike prioritize HIPAA-aligned imaging pipelines that automatically index, de-identify, and synchronize documents with core EHRs.

Legal firms and educational institutions present steady, compliance-oriented demand, though budget pressures nudge them toward cloud or managed-service models. Financial services fall into the “Others” bucket; here, anti-money-laundering and KYC workflows create niche revenue for platforms capable of parsing IDs and complex forms. Collectively, these verticals illustrate why tailored integrations, not generic scanning, drive wallet share in the document imaging industry.

Geography Analysis

North America contributed 38.59% revenue in 2024 as enterprises invested in AI document processing, healthcare digitization, and mandated data-privacy controls. Federal cloud-first policies, plus mature IT budgets, sustain robust upgrades to intelligent capture suites. Financial-services firms focus on customer-experience gains by embedding e-signatures and instant identity verification into onboarding journeys, deepening platform dependence. Vendors here pilot cutting-edge generative-AI features first, reinforcing regional technology leadership and anchoring the document imaging market.

Asia-Pacific delivers the top 13.93% CAGR through 2030 as government digitization drives large-scale projects under Digital India, Japanese DX strategies, and China’s smart-city blueprints. Low-cost mobile devices let firms bypass expensive scanners, widening adoption among SMEs. International vendors partner with local integrators to navigate data-sovereignty rules, while domestic players adapt SaaS offerings to language and regulatory nuances. The region’s demographic tilt toward young, mobile-centric workforces ensures sustained appetite for cloud capture apps that embed directly into messaging tools.

Europe shows consistent but moderate growth underpinned by GDPR. Enterprises seek granular consent management and immutable audit logs, spurring upgrades even in mature installations. Economic headwinds temper discretionary hardware refresh cycles, yet migration to SaaS offsets the slowdown. Vendors offering in-region data centers and Schrems-II-aligned contractual safeguards gain competitive headway. Overall, tighter privacy regulations reinforce demand for advanced governance features, keeping the document imaging market size resilient across the continent.

Competitive Landscape

The market remains moderately fragmented. Legacy hardware giants—Xerox, Canon, Ricoh—protect installed bases by embedding AI microservices in multi-function devices and bundling managed services. Software-first challengers such as Hyperscience and Tungsten Automation champion zero-shot document classification and low-code AI-agent builders, creating a value proposition rooted in speed to insight rather than scan speed. Tungsten’s TotalAgility 8.1 accelerates agent deployment for non-technical users, reflecting the democratization of intelligent document processing.

Consolidation continues: DocuWare’s natif.ai buyout and Hyland’s AI product line launch illustrate how incumbents fill technology gaps swiftly. Patent filings in automated document search and generation grew, aided by USPTO guidance on AI intellectual-property eligibility, signalling sustained R&D investment. Cloud hyperscalers stay largely out of specialized imaging but provide GPU infrastructure, prompting partnerships rather than direct rivalry.

Strategic differentiation hinges on quantifiable outcomes—hours saved, errors avoided, and compliance tasks automated—over licensing cost. Vendors with vertical-specific templates, such as healthcare fax triage or invoice capture, shorten implementation timelines and lift renewal rates. Managed-service providers aggregate multiple platforms to deliver turnkey compliance and process-outsourcing offerings, especially attractive to SMEs lacking in-house expertise. Overall, technology leadership, rather than price, shapes market power within the document imaging market.

Document Imaging Industry Leaders

Xerox Holdings Corporation

Canon Inc.

Ricoh Company, Ltd.

Konica Minolta, Inc.

HP Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: IBM donated Docling, Data Prep Kit, and BeeAI to the Linux Foundation, with Docling converting unstructured files into AI-ready data.

- February 2025: Hyland opened a Hyderabad office and partnered with Northern Care Alliance NHS to roll out a centralized document system.

- January 2025: Hyland introduced Content Intelligence to transform unstructured content into AI-ready knowledge.

- January 2025: Tungsten Automation launched TotalAgility 8.1 featuring rapid AI-agent creation and advanced OCR.

Global Document Imaging Market Report Scope

| Hardware |

| Software |

| On-premise |

| Cloud |

| Government Organizations |

| Law Firms |

| Physician Practices |

| Educational Institutions |

| Other End-users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| By Deployment | On-premise | ||

| Cloud | |||

| By End-user | Government Organizations | ||

| Law Firms | |||

| Physician Practices | |||

| Educational Institutions | |||

| Other End-users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the document imaging market in 2025?

The document imaging market size is USD 159.64 billion in 2025.

What is the expected growth rate through 2030?

The market is forecast to expand at a 13.11% CAGR, reaching USD 295.57 billion by 2030.

Which component generates the most revenue?

Software leads with 61.94% share, driven by intelligent document processing engines.

Which end-user segment is growing fastest?

Physician practices post the highest 13.56% CAGR thanks to EHR integration and AI fax routing.

Which region shows the strongest growth momentum?

Asia-Pacific records the fastest 13.93% CAGR, propelled by government digitalization mandates and mobile adoption.

What is the main restraint on rapid cloud deployment?

Heightened cyber-security and privacy concerns, especially in EU healthcare, slow immediate migration.

Page last updated on: