Nucleic Acid Labeling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.85 Billion |

| Market Size (2031) | USD 4.09 Billion |

| Growth Rate (2026 - 2031) | 7.48 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Nucleic Acid Labeling Market Analysis by Mordor Intelligence

The nucleic acid labeling market size is expected to grow from USD 2.65 billion in 2025 to USD 2.85 billion in 2026 and is forecast to reach USD 4.09 billion by 2031 at 7.48% CAGR over 2026-2031. Momentum is shifting from legacy radioactive workflows toward copper-free click-chemistry and other bioorthogonal platforms that mark DNA and RNA without damaging living cells[1]Robert T. Kennedy, “Bioorthogonal Chemistry for Nucleic Acids,” Nature Chemistry, nature.com. Three intertwined forces underpin growth: record public genomics funding such as the United Kingdom’s USD 190 million program in 2024, attomolar-sensitive CRISPR diagnostics that remove upstream amplification steps, and new commercial bio-orthogonal reagents that bypass copper toxicity. Fluorescent labeling remains the workhorse because of safety and automation readiness, yet better shielding and targeting strategies are igniting a radioactive renaissance for next-generation radiopharmaceuticals. Meanwhile, contract research organizations (CROs) expand fastest as drug makers outsource sophisticated labeling tasks to partners with regulatory-grade infrastructure.

Key Report Takeaways

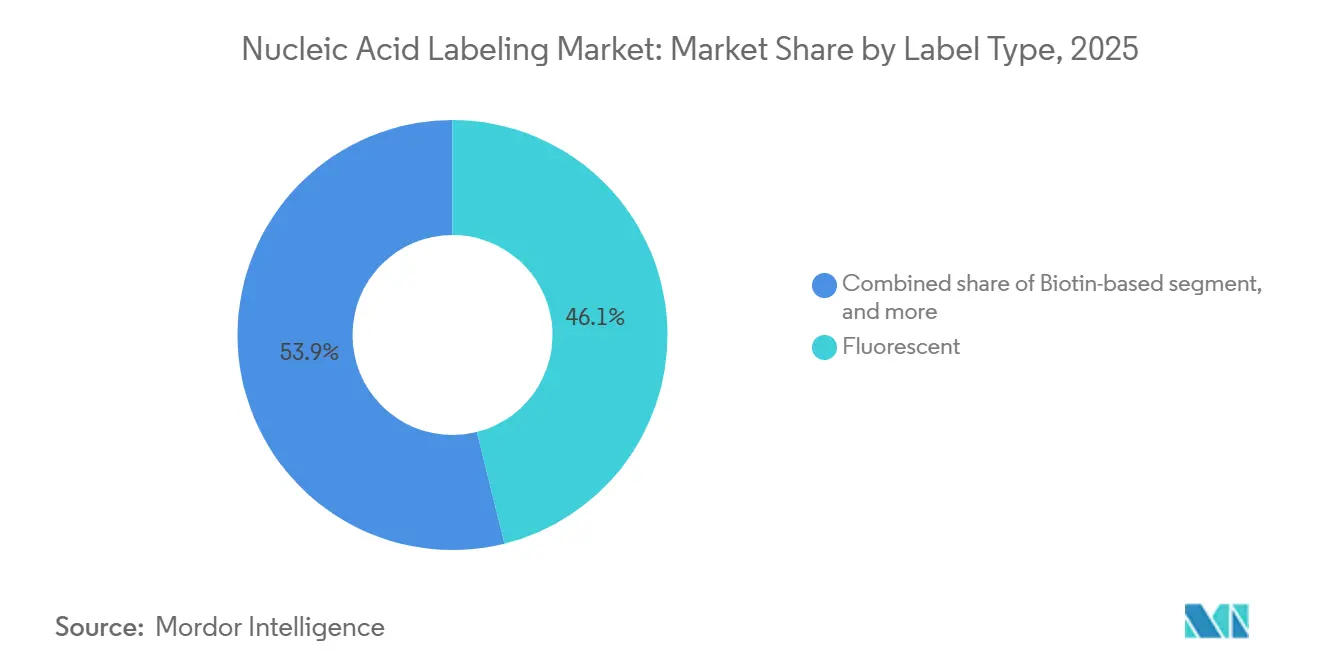

- By label type, fluorescent labeling led with 46.12% of the nucleic acid labeling market share in 2025, while radioactive labeling is projected to expand at a 9.25% CAGR through 2031.

- By product, reagents and kits commanded 55.05% share of the nucleic acid labeling market size in 2025; enzymes and polymerases projected 9.05% CAGR forecast to 2031.

- By method, direct chemical labeling held 43.25% revenue share in 2025, whereas PCR-based is expected to grow at 9.38% CAGR to 2031.

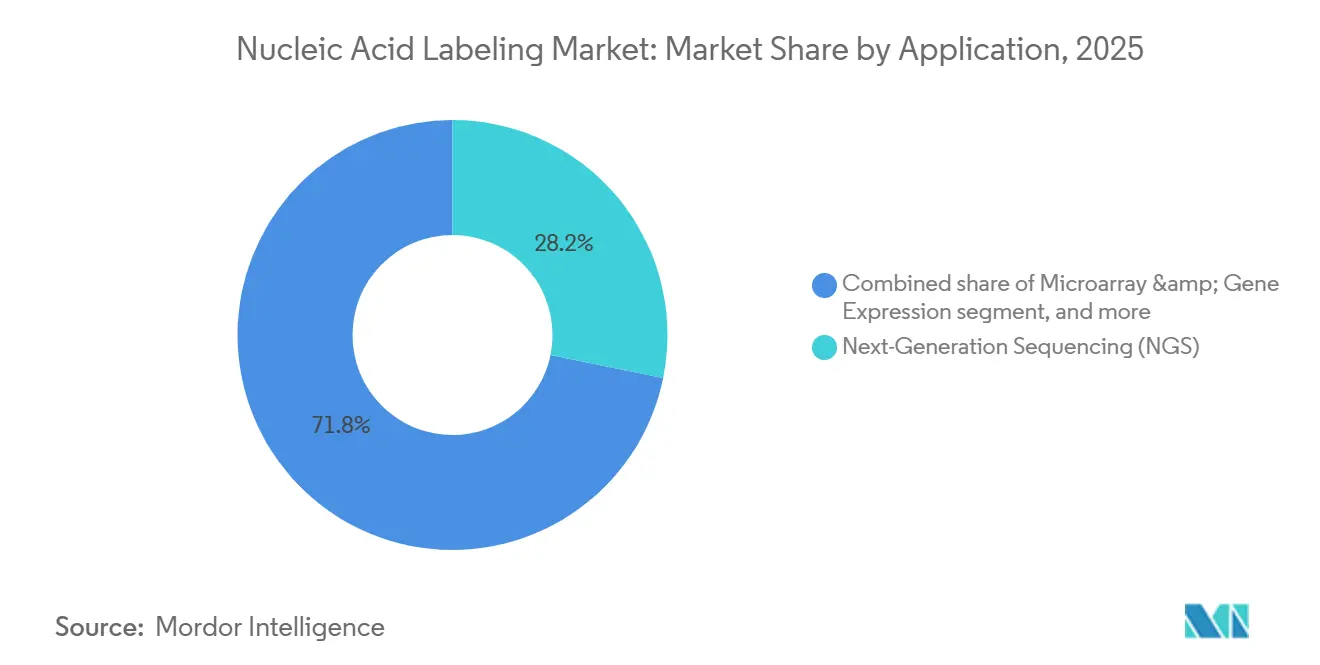

- By application, next-generation sequencing captured 28.20% share in 2025, while CRISPR screening and diagnostics are expected to have the fastest 10.45% CAGR through 2031.

- By end user, academic institutions retained 34.30% share in 2025; CROs record a leading 10.08% CAGR to 2031.

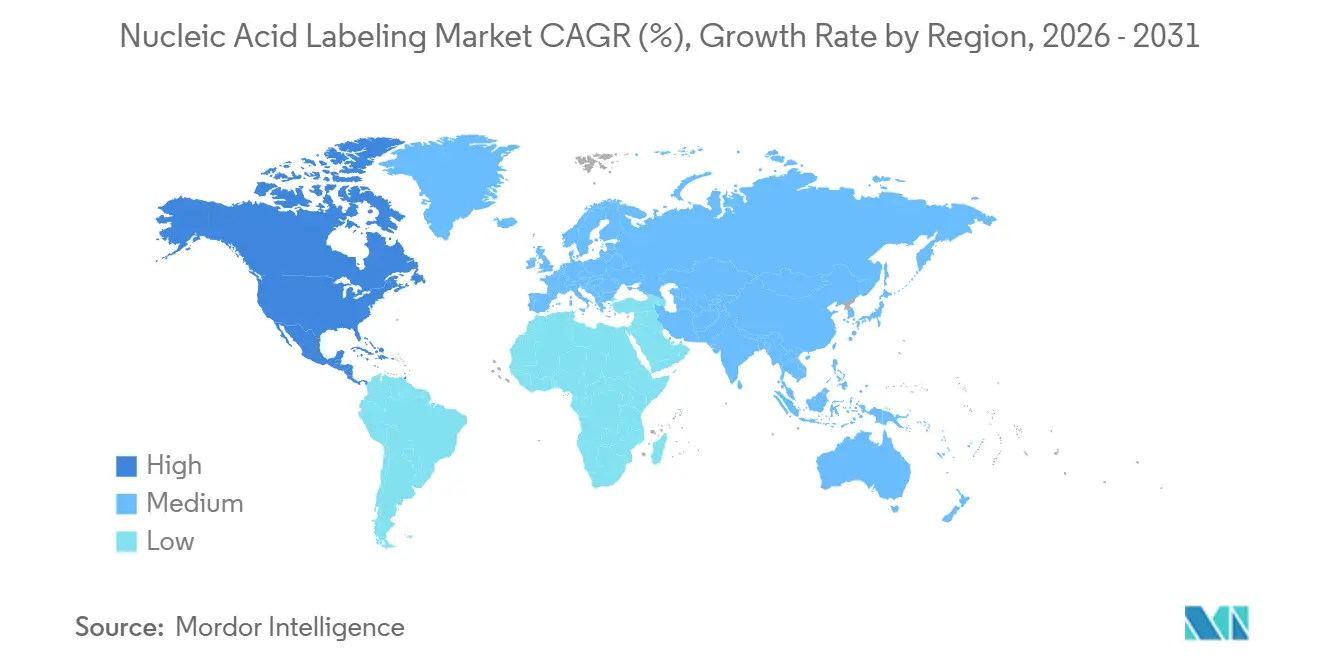

- By geography, North America controlled 43.10% of the nucleic acid labeling market share in 2025, and Asia-Pacific is advancing at an 8.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Nucleic Acid Labeling Market Trends and Insights

Drivers Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Expansion of genomics and proteomics research funding Expansion of genomics and proteomics research funding | +1.8% | Global, with concentration in North America & EU | Medium term (2-4 years) | % Impact on CAGR Forecast:+1.8% | Geographic Relevance:Global, with concentration in North America & EU | Impact Timeline:Medium term (2-4 years) |

Increasing adoption of precision medicine and companion diagnostics Increasing adoption of precision medicine and companion diagnostics | +1.5% | North America & EU core, spill-over to APAC | Long term (≥ 4 years) | |||

Rapid growth of next-generation sequencing workflows Rapid growth of next-generation sequencing workflows | +1.2% | Global | Short term (≤ 2 years) | |||

Rising utilization of fluorescent probes in molecular diagnostics Rising utilization of fluorescent probes in molecular diagnostics | +1.0% | Global | Medium term (2-4 years) | |||

Emergence of click-chemistry and bio-orthogonal labeling technologies Emergence of click-chemistry and bio-orthogonal labeling technologies | +0.9% | North America & EU, expanding to APAC | Long term (≥ 4 years) | |||

Integration of CRISPR-based point-of-care diagnostics Integration of CRISPR-based point-of-care diagnostics | +0.8% | Global, with early gains in North America, EU, China | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Expansion of Genomics and Proteomics Research Funding

Generous public investment fuels an ever-larger experimental footprint. The NIH Centers of Excellence in Genomic Science program is channeling substantial grants into transformative sequencing technologies[2]National Institutes of Health, “Centers of Excellence in Genomic Science,” nih.gov. Parallel efforts such as Human Genome Project II aim to genotype more than 1% of the global population, driving demand for scalable labeling reagents that can handle huge sample volumes while keeping error rates low. Proteomics consortia are pushing multiplexed labeling that distinguishes hundreds of proteins in a single run, raising reagent consumption across academic core facilities. Funding also supports diversity initiatives, meaning reagents must perform consistently across varied ancestries and biosources. In aggregate, better-funded laboratories translate directly into elevated procurement of high-margin labeling kits and enzymes.

Increasing Adoption of Precision Medicine and Companion Diagnostics

Healthcare providers are embedding molecular readouts into routine decision-making. QIAGEN recently broadened its QIAstat-Dx panel to include chronic disease biomarkers, illustrating how multiplex PCR diagnostics rely on robust labeling chemistry for simultaneous detection. Over 30 biopharma partnerships now co-develop companion diagnostics beyond oncology, each demanding standardized, globally accepted labeling workflows. Regulatory agencies push harmonized guidelines, so suppliers able to validate reagents across multiple jurisdictions gain traction. Asia-Pacific uptake is accelerating in step with expanding molecular pathology capacity, creating fresh revenue pools for premium-priced probes. As personalized therapy narrows dosing windows, clinicians need labels that deliver unambiguous signal readouts at very low analyte levels.

Rapid Growth of Next-Generation Sequencing Workflows

Sequencing revenues are projected to leap from USD 14.95 billion in 2024 to USD 106.20 billion by 2034. Library preparation consumes large volumes of labeled adapters, barcode primers, and enzymes, thereby scaling reagent demand almost linearly with data output. Automation is replacing manual pipetting, exemplified by Beckman Coulter’s Biomek Echo One liquid handler that integrates labeling into high-throughput workflows. AI analytics shrink data processing time, but only if upstream labels are applied uniformly to minimize quality control flags. Vendors capable of supplying pre-plated, automation-ready kits are well positioned to capture this spend surge during the forecast horizon.

Rising Utilization of Fluorescent Probes in Molecular Diagnostics

Fluorescent tags are now routine in infectious disease, oncology, and rare genetic testing. Bio-Rad’s newly launched StarBright Red and Violet dye panels improve brightness and spectral separation, enabling 40-colour flow cytometry with fewer compensation artifacts. Advanced probes now rival radioactive sensitivity while eliminating radiation handling protocols, which is pivotal for decentralized test sites. Minimalist benzene- and amino-acid-based probes provide high quantum yield with superior biocompatibility. Better photostability reduces repeat-run costs, reinforcing fluorescent labeling’s status as the default workflow in most clinical laboratories.

Restraints Impact Analysis

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High cost of advanced labeling reagents and instruments High cost of advanced labeling reagents and instruments | -1.2% | Global, particularly impacting emerging markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.2% | Geographic Relevance:Global, particularly impacting emerging markets | Impact Timeline:Short term (≤ 2 years) |

Technical complexity and skill gap in low-resource settings Technical complexity and skill gap in low-resource settings | -0.8% | APAC, MEA, Latin America | Long term (≥ 4 years) | |||

Regulatory restrictions on radioactive labeling methods Regulatory restrictions on radioactive labeling methods | -0.6% | Global, with stricter enforcement in EU & North America | Medium term (2-4 years) | |||

Supply chain vulnerabilities for specialty fluorophores Supply chain vulnerabilities for specialty fluorophores | -0.5% | Global, with acute impact in APAC manufacturing hubs | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

High Cost of Advanced Labeling Reagents and Instruments

Premium fluorophores and specialized instrumentation can price out smaller laboratories. A high-end automated label-incorporation system exceeds USD 100,000, a steep barrier for facilities without large capital budgets. Global supply disruptions, such as recent technetium-99m shortages, expose reliance on single-source isotopes and drive up pricing for alternative kits. Businesses counter by multisourcing raw materials and launching value-tier products, but margin pressure persists, especially where local currencies depreciate against USD.

Technical Complexity and Skill Gap in Low-Resource Settings

Many advanced kits require cold chains, precise thermal cycling, and trained personnel. Automated extraction systems like HiMedia’s Insta NX Mag24 reduce manual steps but remain expensive for regional hospitals. The United States FDA is phasing out enforcement discretion for laboratory-developed tests, compelling labs worldwide to adopt more stringent quality controls[3]United States FDA, “Regulatory Framework for Laboratory-Developed Tests,” federalregister.gov. Smaller institutions struggle to finance compliance, slowing technology penetration outside major centers. Simplified point-of-care platforms such as Dragonfly are promising yet still early in validation.

Segment Analysis

By Label Type: Fluorescent Dominance Faces Radioactive Renaissance

Fluorescent reagents captured 46.12% of the nucleic acid labeling market in 2025, underscoring their status as the default solution for high-throughput microscopy, flow cytometry, and qPCR workflows. This leadership reflects lower biosafety requirements, streamlined disposal, and tight integration with automated optics systems. Radioactive approaches, although regulated, are climbing at 9.25% CAGR as next-generation radiopharmaceuticals leverage isotopic precision for oncological imaging. Copper-free click-labels and tetrazine ligation now let researchers track nucleic acids inside living cells without photo-bleaching or toxicity.

The segment illustrates convergence. Fluorescent platforms increasingly touch attomolar sensitivity once reserved for isotope tracers, while modern isotopes adopt antibody or aptamer targeting to limit off-target radiation. Bio-Rad’s 32-colour StarBright expansion exemplifies how suppliers tailor brightness and emission spectra to specific cytometers. Conversely, VERAXA Biotech’s pre-targeted Affilin radio conjugates rely on click chemistry to attach isotopes only after antibody binding, lowering background uptake. Such cross-pollination blurs traditional label boundaries and sustains innovation momentum across both subsegments.

Note: Segment shares of all individual segments available upon report purchase

By Product: Reagents Leadership Challenged by Enzyme Innovation

Reagents and ready-to-use kits represented 55.05% share of the nucleic acid labeling market in 2025 because consumables are replenished with every batch run. Researchers favor all-inclusive boxes that bundle probes, buffers, and controls, cutting qualification time. Yet engineered enzymes and polymerases show the briskest 9.05% CAGR as thermostable, fidelity-enhanced variants incorporate labels during synthesis rather than after amplification.

Value creation is moving upstream. Merck’s Aptegra CHO genetic stability assay combines whole-genome sequencing with streamlined labeling, trimming 66% off biosafety testing time and 43% off costs. Dual-incorporation polymerases allow orthogonal end labeling that surpasses chemical post-synthesis methods in uniformity and yield. Services supplying custom oligos with embedded click-handles fill specialty gaps for spatial transcriptomics or single-cell multiomics where catalog SKUs fall short.

By Method: Chemical Labeling Leads as PCR Integration Accelerates

Direct chemical conjugation retained 43.25% share in 2025 thanks to versatility across DNA, RNA, and oligonucleotides. Random priming and nick translation remain staples for uniform long-fragment labeling. PCR-based incorporation, however, leads growth at 9.38% CAGR as labs merge amplification and label insertion in one closed tube, halving pipetting steps and minimizing contamination.

Workflow efficiency is the core driver. Modified polymerases tolerate bioorthogonal dNTPs, enabling downstream click-addition of fluorophores or isotopes for precise stoichiometry. Robotics-compatible mastermixes further simplify handoff to next-gen sequencing or digital PCR instruments. Meanwhile, strain-promoted azide-alkyne cycloaddition widens scope to live-cell and in-vivo studies once deemed impossible with classic chemistries. These advances reinforce a gradual pivot toward hybrid protocols that fuse amplification, chemical reactivity, and bioorthogonal specificity into a single workflow.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Application: NGS Dominance Challenged by CRISPR Innovation

Next-generation sequencing held 28.20% share in 2025, supported by massive library preparation volumes that consume labeled adapters, indexes, and capture probes. CRISPR diagnostics and screening tools, however, are accelerating at 10.45% CAGR as SHERLOCK, DETECTR, and Cascade systems achieve lab-quality sensitivity without thermocyclers . Label kits optimized for CRISPR enzymes must function in unpurified matrices such as nasal swabs, shifting design priorities toward low-background fluorescence and rapid readouts.

Digital PCR, FISH, and spatial biology remain solid niches. Multiplexed in-situ hybridization relies on bright labels resistant to RNase-rich environments. Microarray activity is flat but persistent due to established infrastructure in large cohort studies. Ultimately, NGS keeps volume leadership, while CRISPR’s speed and instrument independence position it as the disruptive contender likely to reshape end-user mix by the end of the decade.

Note: Segment shares of all individual segments available upon report purchase

By End User: Academic Institutions Lead as CROs Accelerate

Academic institutes accounted for 34.30% of spending in 2025, reflecting their mandate to pioneer new protocols and their access to grant funding. Flagship initiatives like the NIH genomics centers stockpile every major labeling variant, driving early-stage demand. CROs, however, post the swiftest 10.08% CAGR, fueled by pharma outsourcing of regulatory-grade assays requiring Good Laboratory Practice compliance.

Hospitals and diagnostic laboratories adopt labeling primarily for established assays, such as HPV genotyping or minimal residual disease tracking. As the FDA tightens oversight of laboratory-developed tests, many small facilities may lean on outside expertise, indirectly boosting CRO volumes. Biopharma firms themselves purchase premium kits for companion diagnostic co-development and gene-therapy vector quality control, but much hands-on work migrates to service partners that promise faster turnaround and validated documentation.

Geography Analysis

North America contributed 43.10% of the nucleic acid labeling market size in 2025 on the strength of robust NIH budgets, venture funding, and an FDA framework that clarifies labeling reagent classification. The United States leads with mature sequencing infrastructure, widespread CRISPR diagnostic pilots, and a vibrant biotech supply chain. Canadian centers add depth through specialized stem-cell and epigenetics programs, while Mexico expands biomanufacturing corridors that source labeling consumables regionally.

Asia-Pacific is the fastest-growing arena at 8.35% CAGR to 2031. China alone set aside USD 1.12 billion for nucleic acid drug development, accelerating reagent uptake across research institutes and CDMOs. Japan’s innovation in heat-stable mRNA storage broadens kit durability, critical for tropical deployment. India’s CRO sector scales rapidly, demanding cost-optimized fluorescent and click reagents. South Korea and Australia contribute high-resolution imaging talent and harmonized IVD regulations that shorten approval timelines.

Europe maintains steady, policy-driven expansion. Germany and the United Kingdom anchor R&D with strong pharmaceutical ecosystems, while France, Italy, and Spain invest in regional manufacturing to mitigate post-Brexit logistics hurdles. Sustainability rules encourage moves away from radioactive workflows toward greener fluorophores and copper-free click chemistries. EU-wide initiatives supporting precision oncology ensure continued progression but with heightened scrutiny on waste management and supply transparency.

Competitive Landscape

Market Concentration

The nucleic acid labeling market is moderately consolidated. Thermo Fisher Scientific pursues a USD 40–50 billion acquisition pipeline, most recently buying Solventum’s purification unit to secure upstream raw materials for nucleic-acid-based therapeutics manufacturing. Illumina’s USD 425 million SomaLogic acquisition underscores a pivot toward integrated multiomics that blends proteomic assays with traditional library prep .

Large incumbents defend share via bundled reagent–instrument ecosystems, yet nimble specialists capitalize on click-chemistry and spatial transcriptomics niches. VERAXA Biotech collaborates with Navigo Proteins to co-develop Affilin radio conjugates that improve tumor-to-background ratios. Beckman Coulter partners with Rarity Bioscience to integrate superRCA technology, adding ultra-sensitive mutation detection capabilities to automated liquid handlers. QIAGEN combines QIAstat-Dx with AstraZeneca to embed companion diagnostics into chronic disease management, illustrating a strategy of embedding labeling within treatment workflows.

Competitive intensity rises in point-of-care segments where simplified workflows enable entry of device-first startups. Open-source hardware movements remain nascent but could erode consumables margins if low-cost sequencing gains traction. Conversely, high-complexity radio conjugates and spatial biology assays favor incumbents with GMP isotopic facilities or antibody conjugation lines, preserving higher entry barriers.

Nucleic Acid Labeling Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Illumina completed the acquisition of SomaLogic for up to USD 425 million, integrating the SomaScan Proteomics Assay with NGS platforms.

- February 2025: Thermo Fisher Scientific agreed to acquire Solventum’s Purification & Filtration business for USD 4.1 billion, targeting USD 125 million in year-five synergies.

- February 2025: Bio-Rad launched the Vericheck ddPCR Empty-Full Capsid Kit for precise AAV vector QC.

- January 2025: The FDA proposed reclassifying in-situ hybridization tests from class III to class II devices to streamline clearance pathways.

- December 2024: VERAXA Biotech and Navigo Proteins formed a radio conjugate development pact leveraging click-chemistry pre-targeting.

Table of Contents for Nucleic Acid Labeling Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Expansion of Genomics and Proteomics Research Funding

- 4.2.2Increasing Adoption of Precision Medicine and Companion Diagnostics

- 4.2.3Rapid Growth of Next-Generation Sequencing Workflows

- 4.2.4Rising Utilization of Fluorescent Probes in Molecular Diagnostics

- 4.2.5Emergence of Click-Chemistry and Bio-Orthogonal Labeling Technologies

- 4.2.6Integratioon f CRISPR-Based Point-Of-Care Diagnostics

- 4.3Market Restraints

- 4.3.1High Cost of Advanced Labeling Reagents and Instruments

- 4.3.2Technical Complexity and Skill Gap in Low-Resource Settings

- 4.3.3Regulatory Restrictions on Radioactive Labeling Methods

- 4.3.4Supply Chain Vulnerabilities for Specialty Fluorophores

- 4.4Regulatory Landscape

- 4.5Porter's Five Forces Analysis

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitutes

- 4.5.5Industry Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Label Type

- 5.1.1Biotin-based

- 5.1.2Fluorescent

- 5.1.3Radioactive (32P, 35S, etc.)

- 5.1.4Other Label Types

- 5.2By Product

- 5.2.1Reagents & Kits

- 5.2.2Probes & Primers

- 5.2.3Enzymes & Polymerases

- 5.2.4Custom Labeling Services

- 5.3By Method

- 5.3.1Direct Chemical Labeling

- 5.3.2PCR-based Incorporation

- 5.3.3Nick Translation / Random Priming

- 5.3.4Click-Chemistry Conjugation

- 5.4By Application

- 5.4.1Microarray & Gene Expression

- 5.4.2Next-Generation Sequencing (NGS)

- 5.4.3In-situ Hybridization / FISH

- 5.4.4Polymerase Chain Reaction (PCR/qPCR)

- 5.4.5CRISPR Screening & Diagnostics

- 5.4.6Other Applications

- 5.5By End User

- 5.5.1Academic & Research Institutes

- 5.5.2Hospitals & Clinics

- 5.5.3Diagnostic Laboratories

- 5.5.4Biopharma & Biotechnology Companies

- 5.5.5CROs & Service Providers

- 5.6Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4Australia

- 5.6.3.5South Korea

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East & Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East & Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1Thermo Fisher Scientific, Inc.

- 6.3.2Merck KGaA

- 6.3.3PerkinElmer, Inc.

- 6.3.4GE Healthcare / Cytiva

- 6.3.5Promega Corporation

- 6.3.6Enzo Biochem

- 6.3.7Vector Laboratories

- 6.3.8New England Biolabs

- 6.3.9Agilent Technologies

- 6.3.10Integrated DNA Technologies (IDT)

- 6.3.11LGC Biosearch Technologies

- 6.3.12Takara Bio

- 6.3.13QIAGEN

- 6.3.14Roche Diagnostics

- 6.3.15Bio-Rad Laboratories

- 6.3.16Bioneer Corp.

- 6.3.17Jena Bioscience

- 6.3.18TriLink BioTechnologies

- 6.3.19Lucigen Corporation

- 6.3.20Tocris Bioscience

- 6.3.21Marker Gene Technologies

- 6.3.22Other Emerging Players

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the nucleic acid labeling market as the annual global revenue generated from reagents, kits, and supporting consumables or services that attach detectable tags, fluorophores, chemiluminescent groups, biotin, or radio-isotopes to DNA or RNA for downstream analysis in research, diagnostics, and therapeutic development. Values reflect manufacturer billings, exclusive of bundled sequencing hardware or general extraction kits.

Scope Exclusion: Custom oligo synthesis and bulk unlabeled nucleotides are outside the present scope.

Segmentation Overview

- By Label Type

- Biotin-based

- Fluorescent

- Radioactive (32P, 35S, etc.)

- Other Label Types

- Biotin-based

- By Product

- Reagents & Kits

- Probes & Primers

- Enzymes & Polymerases

- Custom Labeling Services

- Reagents & Kits

- By Method

- Direct Chemical Labeling

- PCR-based Incorporation

- Nick Translation / Random Priming

- Click-Chemistry Conjugation

- Direct Chemical Labeling

- By Application

- Microarray & Gene Expression

- Next-Generation Sequencing (NGS)

- In-situ Hybridization / FISH

- Polymerase Chain Reaction (PCR/qPCR)

- CRISPR Screening & Diagnostics

- Other Applications

- Microarray & Gene Expression

- By End User

- Academic & Research Institutes

- Hospitals & Clinics

- Diagnostic Laboratories

- Biopharma & Biotechnology Companies

- CROs & Service Providers

- Academic & Research Institutes

- Geography

- North America

- United States

- Canada

- Mexico

- United States

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Germany

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- China

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- GCC

- South America

- Brazil

- Argentina

- Rest of South America

- Brazil

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with reagent producers, core facility managers, and molecular pathologists across North America, Europe, and Asia verified price moves, kit throughput, and regional funding shifts. These conversations let us stress-test desk assumptions, adjust for gray-market imports, and refine the split between research and clinical demand.

Desk Research

We began by mapping the universe of addressable spend through open datasets such as the National Center for Biotechnology Information patent portal, U.S. NIH RePORTER grant flows, Eurostat medical technology trade data, and Japanese Customs HS codes for labeled nucleotides. Industry journals like Nucleic Acids Research and association papers from the International Society for Genetic & Genome Technologies helped trace adoption curves, while company 10-K filings clarified segment level revenues. Subscription resources, including D&B Hoovers for company splits and Dow Jones Factiva for shipment-linked news, rounded out baselines. The sources listed illustrate, not exhaust, the literature reviewed.

Market-Sizing & Forecasting

A top-down reconstruction starts with regional production plus net imports of labeled nucleotides and specialty kits, yielding a value pool that is then cross-checked with sampled average selling price multiplied by kit volume data from representative suppliers. Key variables like PCR instrument installed base, NGS run counts, average tags per assay, research grant disbursements, and oncology test penetration feed a multivariate regression model. Forecasts to 2030 apply scenario analysis around grant growth and diagnostic uptake, while gap pockets in bottom-up counts are bridged using channel feedback and Marklines-style shipment proxies where available.

Data Validation & Update Cycle

Mordor analysts run multi-source triangulation and variance checks, compare outputs with import statistics and grant pipelines, and escalate anomalies for senior review. The dataset refreshes yearly, with interim updates triggered by material events such as new reimbursement codes or large-scale funding programs.

Credibility Through Continual Nucleic Acid Labeling Benchmarking

Benchmark comparison

Published estimates often diverge because firms choose different product mixes, price references, and refresh cadences. Our team anchors figures strictly to labeled-reagent revenue and reconciles customs flows with primary pricing insight, which trims double counting and temporal slippage. Key gap drivers we observe include inclusion of adjacent synthesis services, use of catalog prices without real-world discounts, and forecasts built on linear growth instead of grant-linked demand cycles.

Taken together, the comparison shows that Mordor's disciplined scope selection, transparent variable set, and annual review cadence deliver a balanced, reproducible baseline that decision-makers can rely on.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 2.65 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 2.63 B (2025) | Regional Consultancy A | Reports only research use, undercounts diagnostic kits | ||

USD 2.77 B (2025) | Trade Journal B | Uses list prices, ignores customary distributor discounts | ||

USD 2.96 B (2024) | Global Consultancy C | Inflates base by adding custom oligo synthesis revenue |