Direct Sourcing Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

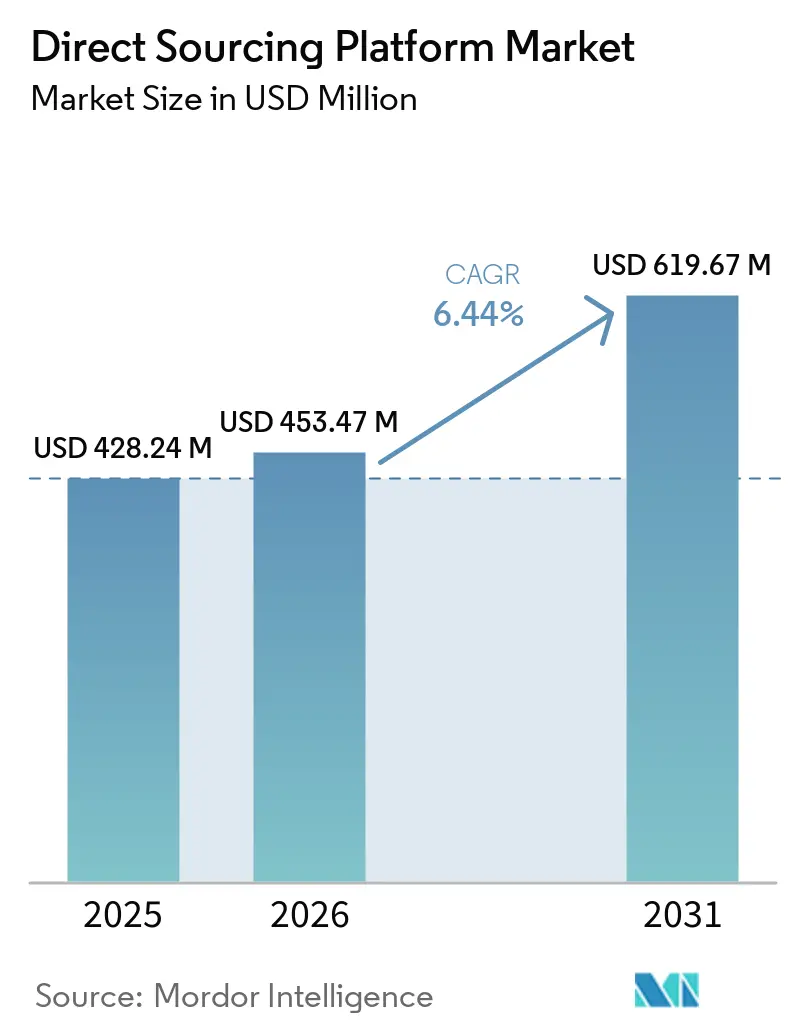

| Market Size (2026) | USD 453.47 Million |

| Market Size (2031) | USD 619.67 Million |

| Growth Rate (2026 - 2031) | 6.44% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Direct Sourcing Platform Market Analysis by Mordor Intelligence

The direct sourcing platform market size is projected to be USD 428.24 million in 2025, USD 453.47 million in 2026, and reach USD 619.67 million by 2031, growing at a CAGR of 6.44% from 2026 to 2031. The direct sourcing platform market is expanding as enterprises move away from reactive, agency-led staffing and toward employer-branded talent communities that support repeat contingent hiring. Cost control and access to specialized skills now shape buying decisions more strongly than risk reduction alone, which is pushing the category deeper into workforce strategy. The direct sourcing platform market is also benefiting from stronger demand for AI-led matching, talent community management, and compliance workflows that can sit across fragmented hiring systems. Opportunity is widening as cloud-native offerings reduce deployment barriers for smaller firms, while large enterprises continue to demand deeper integration and more control. Competitive advantage in the direct sourcing platform market is increasingly concentrated on platforms that combine interoperability, automation, and jurisdiction-aware compliance within a single operating model.

Key Report Takeaways

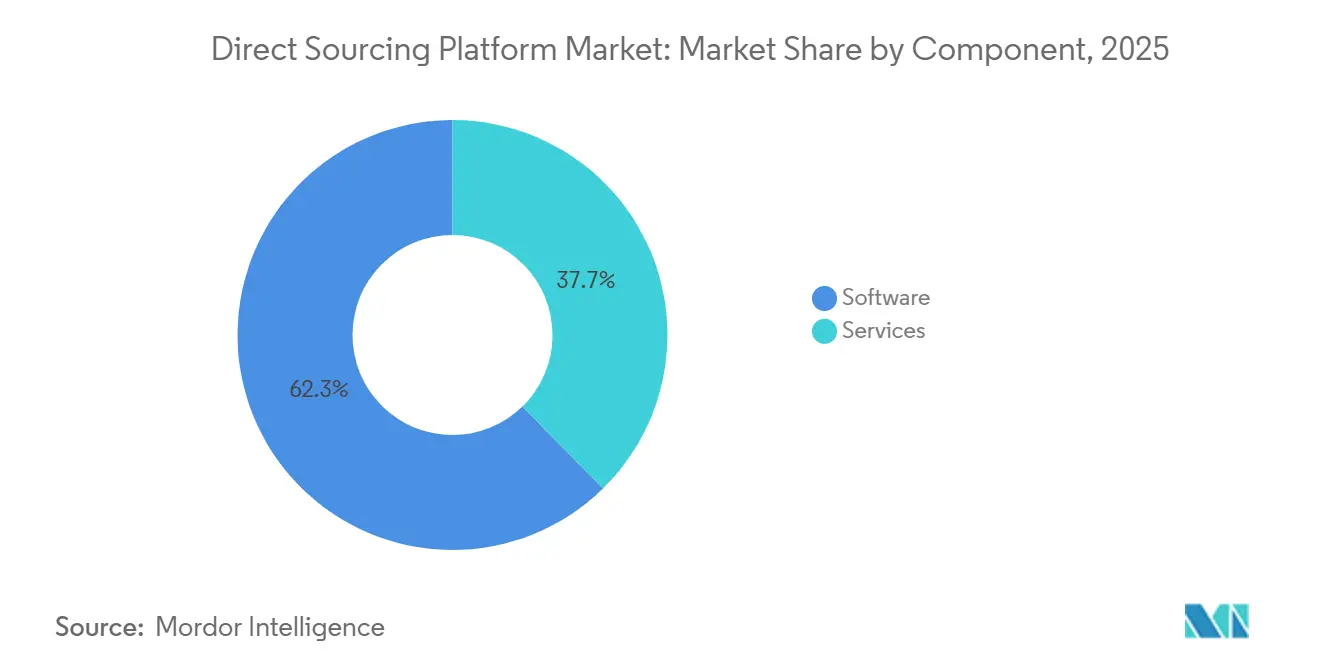

- By component, software held 62.34% share of the direct sourcing platform market in 2025, while services are projected to expand at 9.01% through 2031.

- By functionality, talent community management accounted for 38.41% share in 2025, while AI-driven talent matching and recommendation is forecast to grow at 8.23% through 2031.

- By deployment mode, on-premises deployments represented 68.77% share of the direct sourcing platform market in 2025, while cloud-based solutions are projected to grow at 9.89% through 2031.

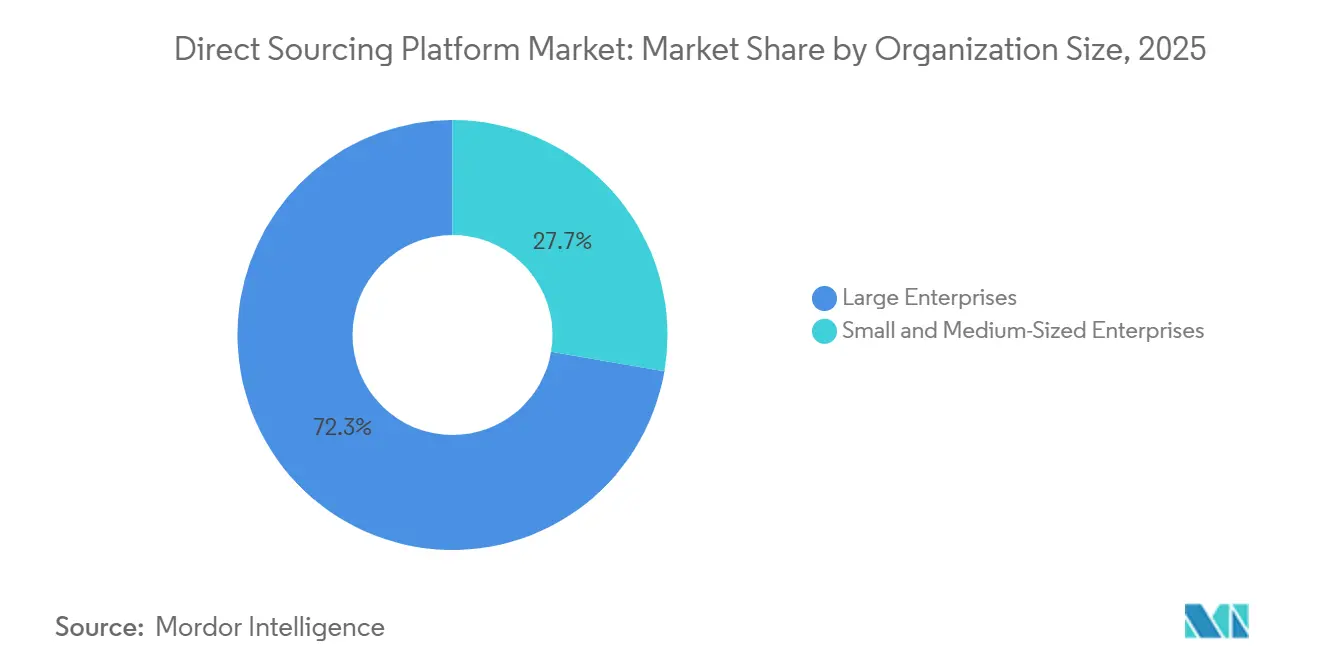

- By organization size, large enterprises held 72.31% share of the direct sourcing platform market in 2025, while small and medium-sized enterprises are expected to advance at 9.43% through 2031.

- By end-user industry, IT and telecommunications captured 35.67% share of the direct sourcing platform market in 2025, while healthcare and life sciences is forecast to expand at 7.78% through 2031.

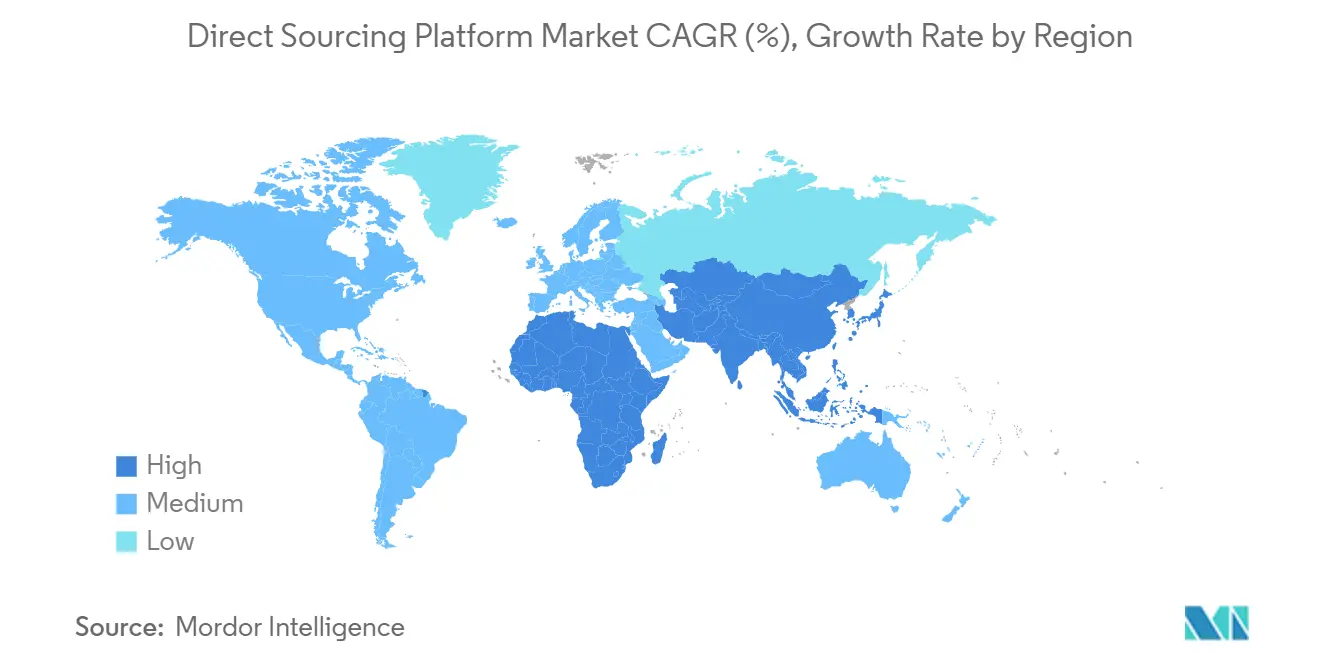

- By geography, North America led with 36.58% share in 2025, while Asia-Pacific is projected to grow at 8.69% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Direct Sourcing Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Enterprise Reliance on Contingent and Project-Based Talent | +1.8% | Global | Short term (≤ 2 years) |

| Branded Private Talent Pools Lower Third-Party Markups | +1.4% | North America and Europe | Medium term (2-4 years) |

| AI-Powered Matching and Talent Community Automation | +1.2% | Global | Medium term (2-4 years) |

| Total Talent Strategies Increase VMS and ATS Integration Demand | +0.8% | North America, Europe, and APAC core | Long term (≥ 4 years) |

| Re-Engagement of Alumni and Silver-Medalist Talent Pools | +0.5% | North America and Europe | Medium term (2-4 years) |

| Regulated Industries Need Pre-Qualified External Talent Communities | +0.4% | North America, Europe, and APAC core | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Enterprise Reliance on Contingent and Project-Based Talent

The direct sourcing platform market is benefiting from a lasting shift toward project-based workforce deployment across enterprises. Korn Ferry reported in August 2025 that contingent workers represented 35% of the U.S. workforce, up from 25% in 2021, and projected that this share could approach 60% by 2032. Vialto Partners found in May 2025 that 94% of organizations use contingent labor, and that 50%-70% of companies in the Asia-Pacific region depend on contingent workers as a standard operating input. Specialized skills in AI, cloud infrastructure, and cybersecurity remain difficult to secure as permanent hires, so many employers now use project-based engagement as a faster route to access these skills. As the contingent share of total headcount rises, the cost of high-margin agency channels spreads across larger procurement budgets, strengthening demand for the direct sourcing platform market for employer-controlled talent channels.

Branded Private Talent Pools Lower Third-Party Markups

The direct sourcing platform market is gaining support from programs that use employer brand to build private, pre-vetted talent pools. Research cited by the Future of Work Exchange in November 2025 showed that organizations with end-to-end direct sourcing programs achieved 58% higher contingent labor cost savings, along with 75% higher reported talent quality and 72% faster fill times. YunoJuno reported in January 2026 that enterprise direct sourcing adoption across its client base grew 30% in 2025, with average savings of 15%-20% per placement versus traditional agency channels.[1]YunoJuno, “YunoJuno Delivers First Profitable Year and 45% Revenue Growth in 2025, Setting the Pace for Contractor Management Globally,” YunoJuno Press Release, yunojuno.com The benefit compounds when workers are re-engaged from an existing community, as it removes not only external markup but also much of the screening, credentialing, and documentation cycle. Platforms that support alums outreach, automated nurture campaigns, and redeployment matching are building a harder-to-replicate position in the direct sourcing platform market.

AI-Powered Matching and Talent Community Automation

The direct sourcing platform market is moving beyond basic keyword matching and toward skills-proximity scoring, agentic sourcing, and automated candidate engagement. Beeline launched Beeline AI into general availability in April 2025, adding agentic AI and a skills-proximity scoring engine that evaluates matched, inferred, and missing skills along with cultural and soft-skill fit. Magnit said in March 2026 that its Maggi AI companion extends intelligence across sourcing, compliance, and analytics within its broader workforce platform. Avature’s AI Impact Report 2026 found that 51% of organizations remained in the exploratory or piloting stage for AI in HR, while only 11% had integrated AI into core workflows. That gap leaves a clear upsell path for vendors that embed AI natively into the direct sourcing platform market rather than offering it as a separate add-on. The EU AI Act will impose full obligations on high-risk recruitment AI systems from August 2, 2026, favoring larger vendors that can support governance, testing, and regulatory documentation at scale.

Total Talent Strategies Increase VMS and ATS Integration Demand

The direct sourcing platform market is being shaped by enterprises that want direct sourcing to operate inside a broader total talent model rather than as a stand-alone tool. The Future of Work Exchange reported in November 2025 that 68% of enterprises running end-to-end direct sourcing programs had strong links to their VMS platforms, with talent communities embedded directly into requisition workflows. DGFP’s 2025 Recruiting Benchmark Study found that 90% of companies already use AI tools for job advertisements, while the applicant management system field remained fragmented, with only 4 providers holding more than 5% share each. That fragmentation creates longer integration paths, but it also increases the value of certified connectors into SAP Fieldglass, Beeline, Workday, and other core platforms. In the direct sourcing platform market, ecosystem architecture is now as important as core functionality because enterprise buyers want a smoother path from the talent community to approved engagements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Worker Classification and Cross-Border Labor Compliance Complexity | -1.2% | Global | Short term (≤ 2 years) |

| Integration Friction across ATS, VMS, HRIS, Payroll, and EOR Stacks | -0.8% | Global | Medium term (2-4 years) |

| Weak Employer Brands Limit Candidate Community Conversion | -0.5% | All regions, particularly SMEs and mid-market | Medium term (2-4 years) |

| Privacy, Consent, and Data Transfer Rules Constrain AI Sourcing | -0.4% | Europe and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Worker Classification and Cross-Border Labor Compliance Complexity

The most immediate restraint on the direct sourcing platform market is the tightening of worker classification rules across several major jurisdictions. G-P noted in May 2026 that the EU Platform Work Directive entered into force in December 2024 and must be transposed into member state law by December 2026, creating a rebuttable presumption of employment for platform-directed workers. In the United Kingdom, IR35 enforcement intensified in early 2026, and new joint and several liability rules for umbrella companies took effect in April 2026, increasing due diligence demands on programs that use umbrella payment structures. In the United States, the Department of Labor proposed a new rule on February 27, 2026, that would rescind the 2024 framework and restore a two-factor test, pushing enterprises to review existing independent contractor arrangements. This uncertainty often causes employers to delay broader rollouts, slowing expansion in the direct sourcing platform market even when platform demand remains clear.

Integration Friction across ATS, VMS, HRIS, Payroll, and EOR Stacks

The direct sourcing platform market also faces a practical barrier at the integration layer, where talent communities must connect cleanly with requisition systems, payroll tools, and employer-of-record partners. Staffing Industry Analysts noted in January 2026 that effective direct sourcing programs usually require candidate engagement technology, curation processes, and a compliance-employer-of-record partner, and those elements rarely come from a single legacy vendor stack. PIXID said its platform processes more than 216,000 contingent and contract workers daily across 222,000 end-client sites, which shows how small handoff failures can scale into material audit and payroll gaps. That friction raises deployment time and cost, which is one reason services are growing faster than software in the direct sourcing platform market. Vendors with pre-certified connectors and dedicated customer success teams are better placed to capture large-enterprise expansions because they reduce the operating burden clients face after purchase.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Reflects a Program Maturity Gap

Software captured 62.34% of the direct sourcing platform market share in 2025, which shows that platform licensing remained the largest discrete budget item as many organizations activated talent community tools for the first time. The direct sourcing platform market still relies heavily on software at the point of purchase because buyers often start with core workflow control before addressing program design gaps. Services are projected to grow at 9.01% from 2026 to 2031, which is materially faster than overall market growth and points to a persistent execution gap after initial deployment. Many organizations still lack the internal operating expertise needed to build automated nurture campaigns, configure VMS workflows, and interpret talent community health metrics.

The Future of Work Exchange reported in November 2025 that 65% of enterprise direct sourcing programs were supported by dedicated platform automation and that 72% were operated through managed service providers. That pattern shows why software alone rarely produces the savings and fill-rate gains buyers expect. In the direct sourcing platform industry, post-sale execution has become a major commercial lever because clients need advisory support to move from first deployment to scaled outcomes. Services revenue in the direct sourcing platform market is therefore likely to stay above the market average as second-generation programs extend beyond their first use case and into broader workforce categories.

By Functionality: Talent Community Management Supports Core Revenue While AI Matching Expands Fast

Talent community management accounted for 38.41% of revenue in 2025, which made it the core functional anchor of the direct sourcing platform market. That position reflects a simple operating reality because organizations cannot match, engage, or redeploy talent effectively without a structured community in place. AI-driven talent matching and recommendation is forecast to grow at 8.23% through 2031 as platforms move from rule-based filters toward skills adjacency and skills-proximity scoring. Candidate relationship management is also gaining weight because conversion depends on sustained engagement through surveys, content, and redeployment prompts rather than on a single sourcing event.

Onboarding and compliance tools continue to address a step that many firms still handle manually, especially when documentation, credential checks, and jurisdiction-specific sign-offs vary by assignment type. Avature’s AI Impact Report 2026 found that 88% of HR professionals expect to increase AI investment, while role matching ranked among the most comfortable AI use cases at 64%. That combination supports continued expansion of AI modules in the direct sourcing platform market, as buyers can justify them on both operational ease and user comfort. The direct sourcing platform industry is, therefore, likely to see AI matching become the most natural upgrade path for clients that already have talent communities in place.

By Deployment Mode: Cloud Growth is Reshaping a Market Still Led by On-Premises Platforms

On-premises deployments accounted for 68.77% of the direct sourcing platform market in 2025, reflecting the data sovereignty, legacy integration, and security audit demands of large, regulated organizations. The direct sourcing platform market has historically favored on-premises setups among banks, healthcare systems, and other compliance-heavy buyers that want closer control over worker data and classification records. Cloud-based deployment is projected to grow at 9.89% through 2031 as mid-market organizations prioritize scalability and lower infrastructure cost. This shift is likely to reduce the relative dominance of on-premises systems over time, but much of that change should come from net-new adoption rather than rapid migration by existing large enterprises.

Large organizations that have already invested in on-premises environments rarely replace those stacks without a contract renewal event or a major merger. PIXID states that it maintains ISO 27001 certification, and Humanforce says it holds both SOC 2 and ISO 27001 certifications, demonstrating how cloud vendors are responding to enterprise procurement standards.[2]“Our Products,” Pixid Group, pixid.com Vendors that cannot demonstrate those controls are often excluded early in regulated buying processes. In the direct sourcing platform market, cloud expansion will continue to accelerate, but trust, certification, and integration depth will determine which vendors actually benefit.

By Organization Size: Large Enterprises Still Dominate, but SME Demand is Rising Faster

Large enterprises held 72.31% of the direct sourcing platform market share in 2025, which reflected both scale economics and the operational burden of running direct sourcing programs across multiple regions and worker categories. The direct sourcing platform market developed first around larger buyers because they had enough hiring volume to justify private talent community investment and enough internal resources to support integration work. Small and medium-sized enterprises are projected to grow at 9.43% through 2031, the fastest rate among organization sizes, because cloud-native architectures lower the cost and complexity of entry. That is widening the addressable market for the direct sourcing platform beyond global procurement teams and into firms with leaner HR operations.

Staffing Industry Analysts noted in January 2026 that direct sourcing adoption has broadly hovered between 30% and 36% since 2016, suggesting that the key difference between large firms and mid-market buyers lies in program depth rather than basic awareness. Mavenside Consulting reported in February 2026 that skills-based hiring reduced average time-to-hire by 25% globally in 2025, which helps explain why smaller employers are now paying more attention to direct sourcing workflows. Vendors that offer faster deployment, simpler configuration, and pre-built integrations for common HR stacks should win a larger share of this next adoption wave. The direct sourcing platform market is therefore shifting from a large-enterprise stronghold toward a broader buyer base, even if enterprise spending still leads.

By End-User Industry: Technology Spending Leads While Healthcare Adds the Fastest Growth

IT and telecommunications accounted for 35.67% of revenue in 2025, which kept the sector at the center of the direct sourcing platform market. That leadership reflects the long-standing use of statement-of-work arrangements and project-based hiring across infrastructure, software development, and managed services. Healthcare and life sciences are forecast to grow at 7.78% through 2031 as providers respond to clinical talent shortages and rising agency markups. The direct sourcing platform industry is also finding a stronger foothold in banking, financial services, and insurance, where skills scarcity and classification risk make pre-qualified talent pools more attractive.

DirectShifts states that its model delivers 95% match accuracy in clinical role filling compared with 60% unqualified submittals from traditional agencies, and that average time-to-fill can fall to 48 hours rather than more than 2 weeks. Fachkraftfreund said in 2026 that it maintained a community of more than 120,000 healthcare professionals, with an 87% placement rate and a 41% higher cost efficiency than that of recruiting agencies. Manufacturing, retail and e-commerce, and energy and utilities also remain important demand pools where shift scheduling and workforce orchestration matter alongside sourcing. Vendors that package those needs into vertical modules should continue to gain ground in the direct sourcing platform market.

Geography Analysis

North America accounted for 36.58% of the direct sourcing platform market in 2025, making it the largest regional base for platform adoption. The direct sourcing platform market remains strongest in North America because the region combines mature VMS adoption, broad familiarity among managed service providers, and employer branding practices that extend to contingent workers. USTech Solutions said in January 2026 that employers in the region are entering an era of total talent intelligence, where permanent and contingent workforce data are brought into a unified analytics environment.[3]Amelie Clancy, “The 2026 North American Contingent Workforce Report: The Era of Total Talent Intelligence,” USTech Solutions, ustechsolutions.com U.S. regulatory changes, including the Department of Labor proposal issued in February 2026 and California classification updates effective January 1, 2026, increased demand for platforms that can document and guide worker classification decisions. South America remains at the forefront of adoption, but Brazil and Argentina are gaining attention as multinational employers standardize contingent hiring through broader regional rollouts.

Europe remains one of the most compliance-sensitive parts of the direct sourcing platform market, and that is shaping both vendor selection and product design. Malt states that it connects more than 850,000 freelancers with enterprise clients, and that 80% of projects start within 6 days of posting, highlighting the speed advantage a scaled network can provide. DGFP’s Recruiting Benchmark Study 2025 found that 90% of companies now use AI tools for job advertisements, while the ATS field remained fragmented, with no single provider holding more than 5% share. Worker classification enforcement in parts of continental Europe and the United Kingdom’s scrutiny of AI recruitment tools have pushed documentation, transparency, and bias controls higher on procurement checklists. The August 2026 compliance deadline under the EU AI Act should strengthen demand for vendors with more mature governance processes and clearer human oversight models.

Asia-Pacific is the fastest-growing geography in the direct sourcing platform market, with a projected 8.69% CAGR through 2031. Vialto Partners reported in May 2025 that 50%-70% of companies in Asia-Pacific already depend on contingent labor, and Kelly OCG found that 50% of senior executives in the region planned to increase contingent talent recruitment within 12 months. India remains the largest regional engine because of its deep IT and engineering contractor base, while Singapore and Southeast Asia are formalizing platform-led hiring structures as digital economies grow and employer-of-record models expand. The Middle East and Africa still represent smaller pools in the direct sourcing platform market, but Saudi Arabia, the United Arab Emirates, South Africa, and Nigeria are drawing more attention as employers formalize cross-border contractor programs.

Competitive Landscape

The direct sourcing platform market is moderately fragmented, with Beeline and Magnit standing out as visible leaders while a broad challenger group keeps switching activity active. Beeline expanded its footprint through the acquisition of MBO Partners, thereby strengthening its ability to manage independent professionals across a broader range of workforce models. Magnit has been positioning its platform around a more unified workforce stack that combines MSP, VMS, employer-of-record, and direct sourcing capabilities with its Maggi AI layer. WorkLLama, Curately, YunoJuno, and High5Hire are using focused vertical depth and geographic expansion to challenge larger incumbents. Curately reported 9 new enterprise direct sourcing and talent pooling contracts within 120 days in 2025, including 1 Fortune 100 and 3 Fortune 500 organizations, which shows that enterprise displacement is already active in the direct sourcing platform market.

AI capability is becoming the most visible point of differentiation in the direct sourcing platform market, as buyers increasingly want more than simple search-and-match tools. Beeline AI introduced skills-proximity scoring that evaluates matched, inferred, and missing skills together with cultural alignment. iCIMS added an AI Sourcing Agent in its fall 2025 release to discover dormant profiles and silver-medalist candidates through more automated workflows. SAP completed its acquisition of SmartRecruiters in September 2025, creating a tighter HCM-to-talent-acquisition pipeline for more than 4,000 organizations and putting more pressure on vendors with weaker ATS integration stories. Vendors that can combine AI governance, human oversight, and deeper connector networks are likely to hold a stronger position as compliance and interoperability become harder procurement filters.

YunoJuno reported its first full-year profit in 2025, with revenue growth of 45% and U.S. revenue growth of 120%, supported in part by a deeper collaboration with Deel that extended employer-of-record capabilities across 150+ countries. Avature’s footprint across more than 110 Fortune 500 clients, 164+ countries, and 32 languages shows how long-standing operating history and deep configuration can create durable switching costs. The most contested white space in 2026 includes healthcare-focused modules, agentic AI sourcing, and Southeast Asian expansion tied to built-in employer-of-record infrastructure. The direct sourcing platform market is, therefore, rewarding vendors that can offer product breadth, deployment support, and regulatory discipline without forcing clients to assemble disconnected point solutions.

Direct Sourcing Platform Industry Leaders

Magnit, LLC

Avature Limited

Worksuite Inc.

Eqip AG

Ceipal Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: High Five officially expanded into Vietnam as a fully incorporated employer-of-record, alongside the launch of end-to-end autonomous AI recruitment agents that perform sourcing, screening, interviewing, and matching 24/7 across Singapore, Indonesia, Vietnam, Malaysia, and the Philippines. Client PayMongo reported reducing recruitment costs by up to 90% and completing 10 senior engineering hires within 3-4 weeks per role.

- March 2026: Magnit Global was named a Market Leader in Ardent Partners' 2026 Digital Staffing and Direct Sourcing Technology Advisor Report, which evaluated 11 providers across solution strength and provider maturity. Magnit also launched Magnit Shift, a per-diem and registry staffing solution for healthcare organizations, with Dental Care Alliance as its first client.

- February 2026: Beeline was named the 2025 Global Market Leader and Elite Performer in 4 categories, direct sourcing, AI innovation, SOW and services procurement, and total talent management, in Ardent Partners' VMS Technology Advisor report, following its acquisition of MBO Partners, which extended Beeline's capability to manage the full independent-professional spectrum.

- February 2026: Catalant Technologies expanded its senior leadership team with 4 appointments including a new chief product officer, accelerating its Consulting 2.0 strategy to build an AI-enabled intelligent consulting platform with curated communities across financial services, healthcare and life sciences, and consumer verticals.

Global Direct Sourcing Platform Market Report Scope

Direct sourcing platforms empower organizations to tap into their talent pools, minimizing reliance on third-party staffing agencies. With features like candidate engagement and AI-driven role matching, these platforms are becoming integral to contingent workforce strategies, aiming to slash hiring costs and expedite the recruitment process. The market's focus is on cultivating proprietary talent ecosystems for sustained workforce benefits.

The Direct Sourcing Platform Market Report is Segmented by Component (Software, and Services [Implementation and Integration Services, and Analytics and Advisory Services]), Functionality (Talent Community Management, Direct Sourcing Campaign Management, Candidate Relationship Management (CRM), Freelancer / Contractor Onboarding and Compliance, AI‑Driven Talent Matching and Recommendation, and Other Functionalities), Deployment Mode (Cloud-Based, and On-Premises), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (IT and Telecommunications, Healthcare and Life Sciences, Banking, Financial Services, and Insurance, Manufacturing, Retail and E-Commerce, Energy and Utilities, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | |

| Services | Implementation and Integration Services |

| Analytics and Advisory Services |

| Talent Community Management |

| Direct Sourcing Campaign Management |

| Candidate Relationship Management (CRM) |

| Freelancer / Contractor Onboarding and Compliance |

| AI-Driven Talent Matching and Recommendation |

| Other Functionalities |

| Cloud-Based |

| On-Premises |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Banking, Financial Services, and Insurance |

| Manufacturing |

| Retail and E-Commerce |

| Energy and Utilities |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software | |

| Services | Implementation and Integration Services | |

| Analytics and Advisory Services | ||

| By Functionality | Talent Community Management | |

| Direct Sourcing Campaign Management | ||

| Candidate Relationship Management (CRM) | ||

| Freelancer / Contractor Onboarding and Compliance | ||

| AI-Driven Talent Matching and Recommendation | ||

| Other Functionalities | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End-User Industry | IT and Telecommunications | |

| Healthcare and Life Sciences | ||

| Banking, Financial Services, and Insurance | ||

| Manufacturing | ||

| Retail and E-Commerce | ||

| Energy and Utilities | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the direct sourcing platform market and how fast is it growing?

The direct sourcing platform market stands at USD 453.47 million in 2026 and is projected to reach USD 619.67 million by 2031, growing at a 6.44% CAGR over 2026-2031.

Which component category leads spending in direct sourcing platforms?

Software led spending with a 62.34% share in 2025, reflecting the priority enterprises place on core platform licensing before deeper service expansion.

Why are enterprises investing more in direct sourcing platforms?

Enterprises are using direct sourcing platforms to reduce third-party staffing markups, improve access to specialized skills, and build reusable private talent communities for repeat contingent hiring.

Which functionality is growing the fastest in this space?

AI-driven talent matching and recommendation is the fastest-growing functionality, with an 8.23% CAGR through 2031, as buyers look for better skills matching and automation.

Which regions are driving expansion?

North America remains the largest region with a 36.6% share in 2025, while Asia-Pacific is the fastest-growing geography with an 8.69% CAGR through 2031.

Which end-user sectors are creating the strongest demand?

IT and telecommunications remains the largest end-user segment at 35.67% share in 2025, while healthcare and life sciences is expanding the fastest at 7.78% through 2031.

Page last updated on: