Microlearning Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

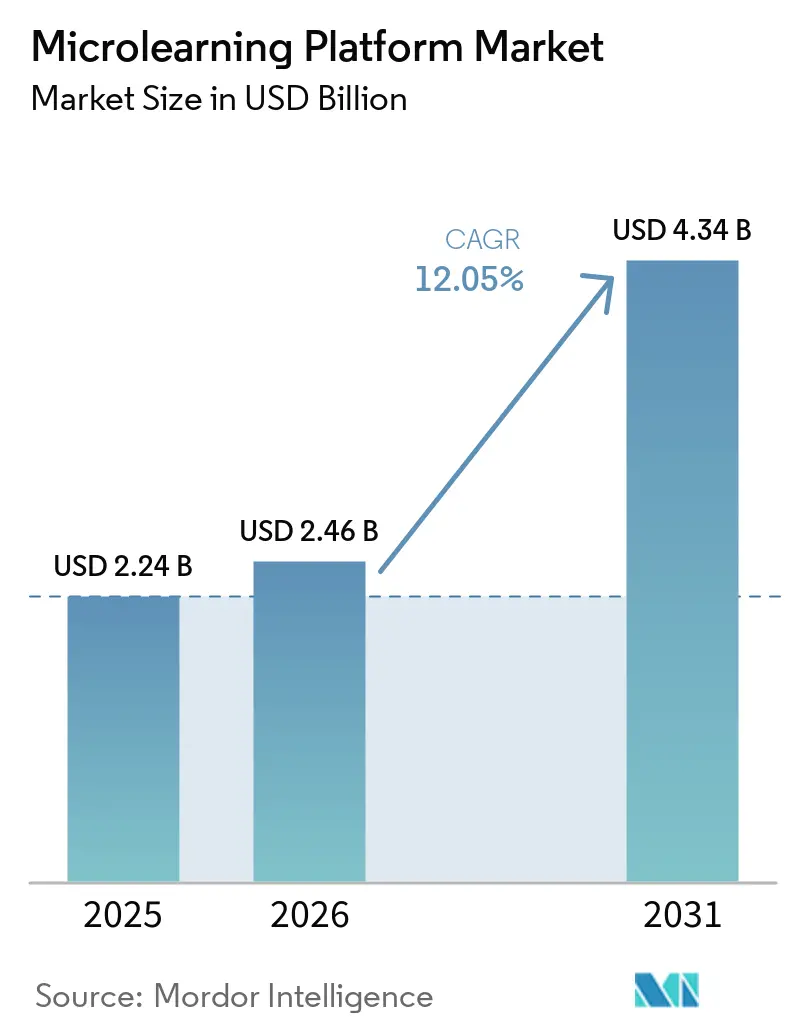

| Market Size (2026) | USD 2.46 Billion |

| Market Size (2031) | USD 4.34 Billion |

| Growth Rate (2026 - 2031) | 12.05% CAGR |

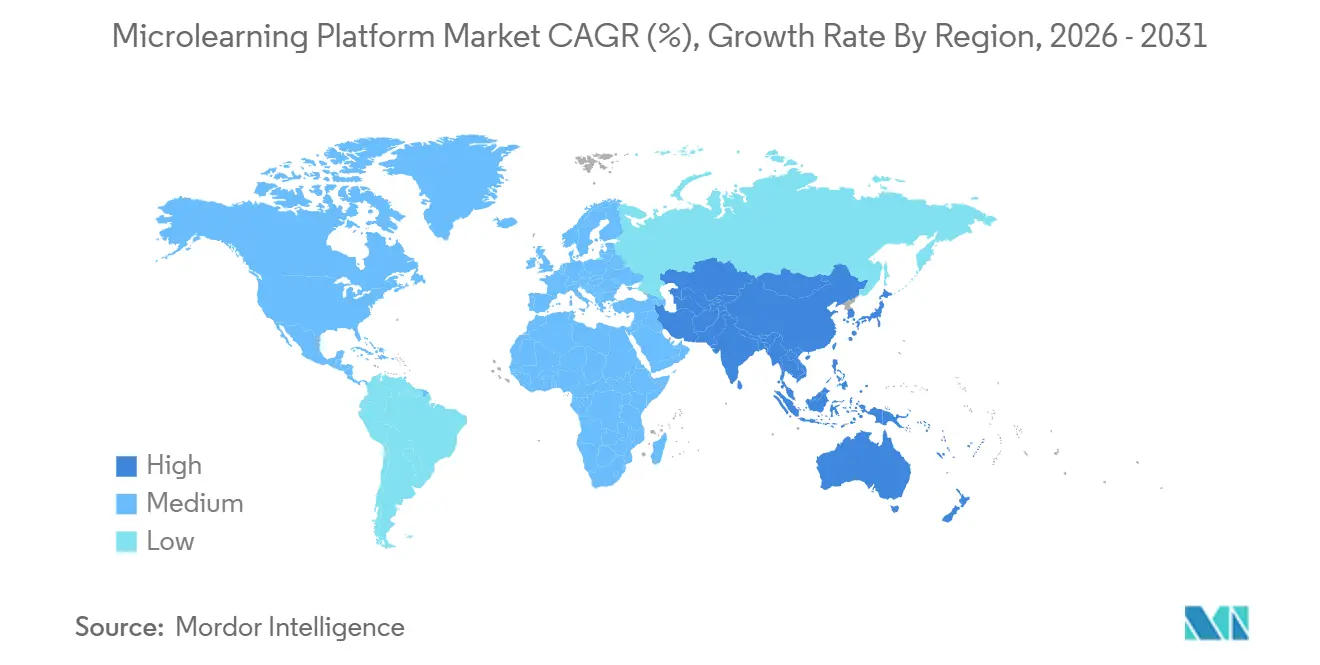

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microlearning Platform Market Analysis by Mordor Intelligence

The Microlearning Platform Market size is projected to expand from USD 2.24 billion in 2025 and USD 2.46 billion in 2026 to USD 4.34 billion by 2031, registering a CAGR of 12.05% between 2026 to 2031. The microlearning platform market is growing faster than broader corporate learning spend because employers are shifting training toward short, repeated modules that fit into daily work instead of isolated classroom sessions. The microlearning platform market is also benefiting from the growing need to refresh worker skills more often, which is raising demand for tools that can update content quickly and distribute it at scale across large workforces. AI-powered personalization, adaptive sequencing, and workflow-based delivery are making the microlearning platform market more central to enterprise productivity systems rather than a secondary add-on within HR technology. Buyer preference remains shaped by integration depth, deployment flexibility, and content governance, as enterprises want stronger links to existing LMS records, manager dashboards, and compliance reporting environments. At the same time, the microlearning platform market is seeing new opportunity in onboarding, regulated training, and mobile-first delivery, while vendors that can balance AI speed with content quality control are positioned more favorably.

Key Report Takeaways

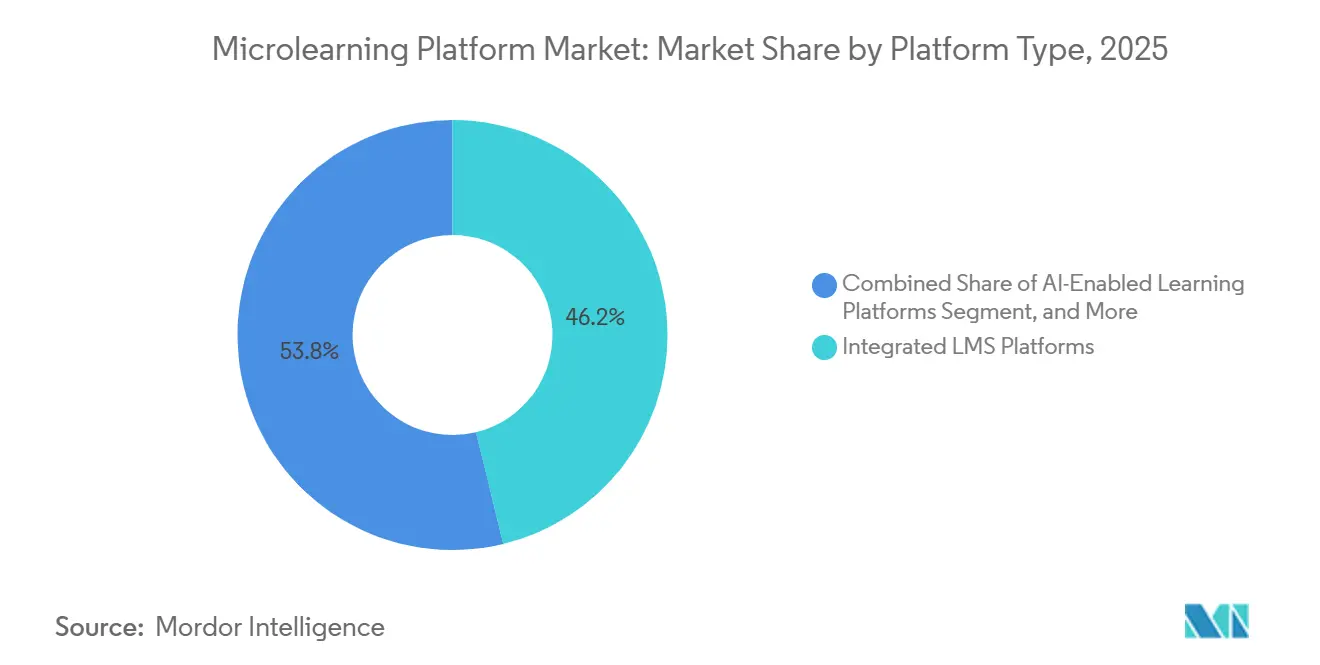

- By platform type, integrated LMS platforms held 46.21% of the market in 2025, while AI-enabled learning platforms are projected to record the fastest growth at a 15.42% CAGR through 2031.

- By deployment model, cloud-based deployment accounted for 68.71% of the market in 2025, while hybrid deployment is forecast to expand at a 14.13% CAGR through 2031.

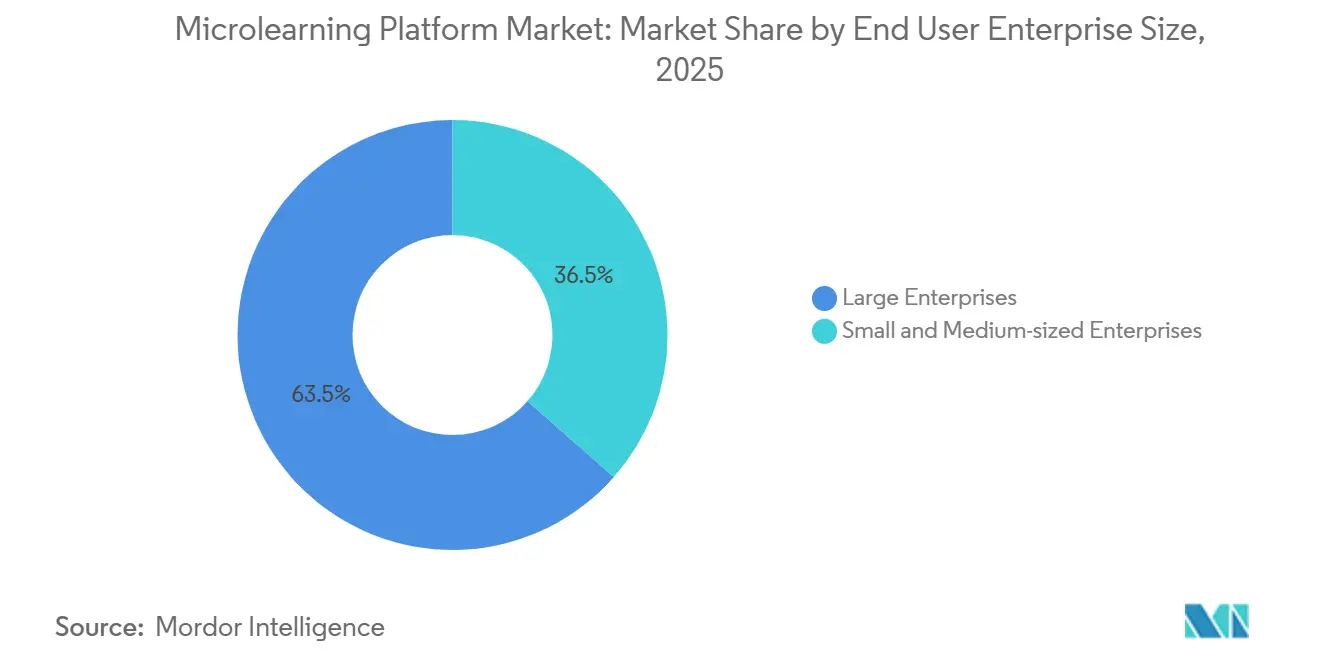

- By end-user enterprise size, large enterprises captured 63.51% of the market in 2025, while small and medium-sized enterprises are expected to grow at a 13.81% CAGR through 2031.

- By application, workforce upskilling and reskilling accounted for 28.92% of the market in 2025, while employee onboarding and new-hire readiness are projected to grow at a 15.42% CAGR through 2031.

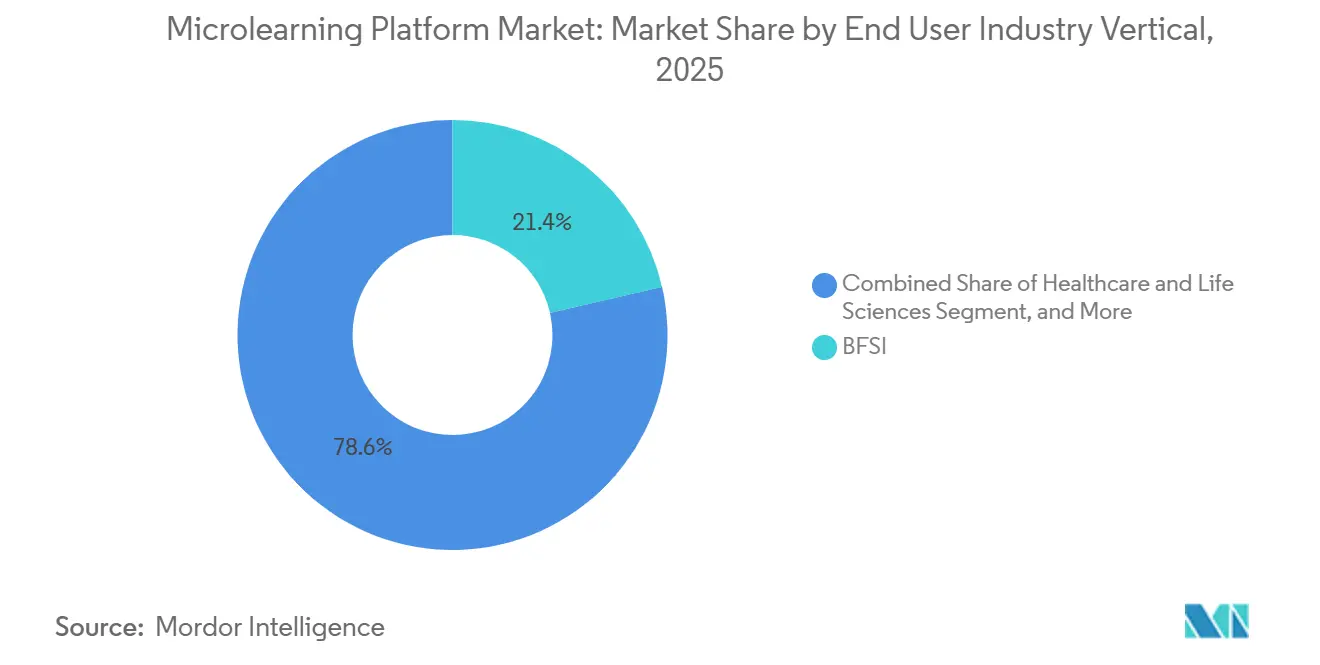

- By end user industry vertical, BFSI accounted for 21.41% of the market in 2025, while healthcare and life sciences are forecast to grow at a 14.83% CAGR through 2031.

- By geography, North America held 38.66% of the market in 2025, while Asia-Pacific is projected to expand at a 16.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Microlearning Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Continuous Workforce Upskilling And Reskilling Need | +3.2% | Global | Medium term (2-4 years) |

| Mobile-First Learning Demand Across Deskless And Distributed Workforces | +2.5% | Global, APAC, South America | Short term (= 2 years) |

| AI-Powered Personalization And Faster Content Authoring | +2.1% | Global, North America and Europe early | Medium term (2-4 years) |

| Rising Use For Compliance And Risk Management | +1.5% | North America and EU, spill-over to APAC | Short term (= 2 years) |

| Flow-Of-Work Delivery Through Collaboration Apps, Text Messaging, And QR Code Triggers | +1.0% | Global, early gains in North America | Short term (= 2 years) |

| AI Translation And Localization For Global Rollouts | +0.7% | APAC, Middle East, and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Need For Continuous Workforce Upskilling And Reskilling

The microlearning platform market is gaining momentum due to a clear mismatch between current workforce skills and the pace of change in digital tools, automation, and job design. The Future of Jobs 2025 report stated that 39% of workers' core skills will need updating within 5 years, which keeps continuous learning high on employer agendas across both private and public organizations.[1]World Economic Forum, “Future of Jobs Report 2025,” World Economic Forum, weforum.org That pressure favors short learning sequences because they can be updated faster and assigned more frequently than longer training formats. It also strengthens the business case for the microlearning platform market, as AI-assisted authoring reduces the time and effort required to create new modules. As reskilling cycles become shorter, vendors that support rapid content refreshes and workflow-based delivery are better placed to serve large organizations with shifting role requirements. This is why the microlearning platform market is moving closer to day-to-day productivity infrastructure rather than remaining limited to periodic training.

Mobile-First Learning Demand Across Deskless And Distributed Workforces

The microlearning platform market is also being supported by learning demand from deskless and distributed employees who do not spend the workday on desktop systems. Mobile-first delivery fits retail, warehousing, field service, food service, and healthcare settings where training has to reach employees during shifts, between tasks, or in low-connectivity environments. Short modules delivered through mobile apps or text-based formats reduce the gap between when a skill is needed and when it is reinforced. Qstream expanded into SMS-based microlearning delivery in January 2026 for pharmaceutical field sales teams working in low-connectivity settings, showing how vendors are adapting the format to operational realities.[2]Qstream, “Company News And Product Information,” Qstream, qstream.com Bites Learning and EZShift announced a partnership in May 2026 to embed training into shift handover workflows, signaling a broader shift toward learning within operational systems rather than outside them. The microlearning platform market is therefore benefiting not only from mobile access but also from the closer alignment between learning moments and work execution.

AI-Powered Personalization And Faster Content Authoring

AI tools are changing both how content is created and how it is delivered, which makes this one of the strongest growth levers in the microlearning platform market. Gnowbe updated its AI-assisted authoring environment in 2025 to support adaptive branching that adjusts lesson difficulty based on learner responses during the session. That kind of capability shifts personalization from after-the-fact reporting into the learning experience itself. It also shortens authoring cycles because teams can work from AI-generated first drafts instead of building each module from scratch. For employers, this lowers the barrier to keeping product knowledge, process changes, and policy content current across large user groups. Even so, the microlearning platform market still faces a content governance challenge, as regulated subject matter in healthcare or finance requires human review before AI-generated content can be trusted for live deployment.

Rising Use Of Microlearning For Compliance And Risk Management

Compliance training continues to support the microlearning platform market, as it represents recurring, non-discretionary demand. Short reinforcement modules align well with how many employers now want to schedule reminders, refreshers, and evidence-based training records throughout the year, rather than relying on a single annual session. This is especially relevant in BFSI, healthcare, energy, and other tightly regulated settings where audit trails and completion records matter as much as the content itself. Vector Solutions launched a dedicated microlearning suite for safety and compliance education in March 2026, which shows that vendors are designing purpose-built offerings for continuing education and regulated environments. Platforms that bundle jurisdiction-specific content libraries, renewal prompts, and reporting tools are better positioned to move from optional feature status to essential operating software. The microlearning platform market benefits from this shift, as compliance budgets tend to remain active even when discretionary learning spend comes under pressure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Suitability For Deep Conceptual Or Procedural Mastery | -1.5% | Global | Long term (= 4 years) |

| Data Privacy And Cybersecurity Concerns In Cloud And Mobile Delivery | -1.1% | EU, North America | Medium term (2-4 years) |

| Weak ROI Attribution Across Embedded Learning Journeys | -0.8% | Global | Medium term (2-4 years) |

| Notification Fatigue And Content Fragmentation | -0.5% | Global, APAC and North America | Short term (= 2 years) |

| Source: Mordor Intelligence | |||

Limited Suitability For Deep Conceptual Or Procedural Mastery

The microlearning platform market still faces a structural ceiling in use cases that require deep conceptual learning or tightly sequenced procedural mastery. Short modules are effective for reinforcement, recall, and habit formation, but they are less effective when learners need long-form explanations, supervised practice, or layered prerequisite knowledge. This matters in areas such as clinical skills, technical certification, advanced software development, and complex equipment maintenance, where learning outcomes depend on depth and context. Vendors that position microlearning as a full replacement for blended or instructor-led programs may face pushback if employer expectations are not met. A more durable role for these platforms is as a reinforcement layer on top of broader learning systems, but that also limits how much of the total training budget they can capture. The microlearning platform market, therefore, expands most effectively when sold as part of a mixed learning architecture rather than as a universal substitute for all training formats.

Data Privacy And Cybersecurity Concerns In Cloud And Mobile Delivery

Cloud and mobile delivery expose the microlearning platform market to growing privacy and cybersecurity scrutiny because these systems process large volumes of learner behavior data. That data can include assessment responses, usage patterns, geolocation details, and AI-driven learner profiles, all of which raise compliance questions in regulated sectors. Epignosis stated in May 2025 that TalentLMS and its broader product suite maintained GDPR compliance under Article 28 standards and supported that position with ISO 27001 certification and SOC 2 Type II attestation.[3]Epignosis, “Company Security And Compliance Information,” Epignosis, epignosishq.com Those capabilities are becoming a baseline requirement in Europe and, increasingly, in North America, as procurement teams place greater weight on security reviews. The EU AI Act also adds new pressure for adaptive learning systems that rely on profiling and algorithmic recommendations, especially where HR deployment touches higher-risk decision environments. Compliance costs are likely to be harder for smaller vendors to absorb, which may support consolidation inside the microlearning platform market over time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: AI Capabilities Reshape Platform Selection

Integrated LMS platforms held 46.21% of the microlearning platform market share in 2025, while AI-enabled learning platforms are projected to grow at a 15.42% CAGR through 2031. That split shows that enterprises still value continuity with their existing learning records, competency histories, and manager dashboards. Many mid-sized and large organizations prefer to extend their current LMS environments rather than add a separate tool that requires new workflows, duplicate reporting, or custom integrations. This explains why integration remains a primary buying criterion for the microlearning platform market, especially among employers with mature learning operations. Standalone vendors still attract interest from teams seeking a simpler deployment path and a more focused user experience, but demand continues to lean toward platforms that integrate with existing enterprise systems.

The rise of AI-enabled platforms is changing that decision process because buyers now assess not only content libraries, but also how quickly a system can produce, personalize, and refresh learning material. Pluralsight launched a new AI sandbox and guided learning environment in April 2026 that added real-time practice feedback within short learning paths, which shows how AI is becoming part of product differentiation rather than a side feature.[4]Pluralsight, “Company News And Product Information,” Pluralsight, pluralsight.com Axonify launched Co-Creator in June 2025, enabling frontline managers to build branded microlearning content without instructional design expertise, further lowering the barrier to frequent content updates. These moves matter because the microlearning platform industry is increasingly judged by how fast it can turn operational changes into usable learning moments. As a result, platform selection is shifting from a simple build-versus-buy choice to a more detailed evaluation of authoring speed, personalization quality, and data continuity.

By Deployment Model: Cloud Dominance Meets Regulated-Industry Pragmatism

Cloud-based deployment accounted for 68.71% of the microlearning platform market size in 2025, while hybrid deployment is forecast to grow at a 14.13% CAGR through 2031. Cloud remains the leading choice because it offers faster implementation, lower infrastructure costs, easier updates, and better support for distributed workers using multiple devices. Those advantages align well with the day-to-day requirements of the microlearning platform market, where content must reach learners quickly and change frequently. Cloud systems also help vendors release new features faster, which matters in a category that is now adding AI tools, reporting layers, and workflow integrations at a steady pace. For many employers, especially those with dispersed frontline teams, cloud deployment remains the most practical way to scale without adding significant IT overhead.

Hybrid deployment is expanding faster because some sectors want cloud flexibility without placing all learner data and performance records outside local control. Banking, defense, healthcare, and public-sector organizations often need to keep sensitive data in specific environments for residency, audit, or internal policy reasons. Docebo introduced configurable data residency controls across AWS, Azure, and Google Cloud regions in April 2026, which directly addressed those procurement concerns. Supporting hybrid architecture is more demanding for vendors because it requires parallel attention to cloud scalability and controlled data management. That challenge creates a technical barrier that can separate larger providers from smaller players, and it gives the microlearning platform market a clearer split between broad-based enterprise vendors and specialists with narrower deployment capabilities.

By End User Enterprise Size: SMEs Accelerate Adoption As Costs Decline

Large enterprises held 63.51% of the market in 2025, while small and medium-sized enterprises are expected to expand at a 13.81% CAGR through 2031. Large organizations still account for most revenue because they have formal learning teams, higher training budgets, broader compliance obligations, and larger employee populations that justify platform investments. They also tend to prefer long-term vendor relationships, which reduces switching costs and supports extending existing systems into microlearning use cases. This has kept large employers at the center of the microlearning platform market even as new entrants target lower-cost segments. In practical terms, large enterprise demand continues to shape product road maps around reporting depth, integrations, governance controls, and multilingual distribution.

At the same time, the fastest momentum is shifting toward smaller businesses because AI-assisted authoring and usage-based pricing are lowering the cost of adoption. Platforms such as 7taps and Gnowbe have focused on low-code content creation and easier deployment, making structured learning more accessible to businesses with limited internal design support. This change is important because SMEs in retail, food service, light manufacturing, and similar sectors face high turnover and frequent onboarding needs. Those conditions make short, repeatable training especially useful, even when formal learning budgets remain limited. As more small employers adopt cloud HR and payroll tools, the same digitalization path is extending into learning systems. That is why the microlearning platform market is broadening beyond enterprise-heavy demand and building a larger base of smaller customers with recurring operational training needs.

By Application: Onboarding And Upskilling Anchor Enterprise Demand

Workforce upskilling and reskilling accounted for 28.92% of the microlearning platform market in 2025, while employee onboarding and new-hire readiness are projected to grow at a 15.42% CAGR through 2031. Upskilling remains the largest application, as employers across sectors seek to keep teams current as AI tools, process redesign, and new digital workflows change job requirements. That use case provides the microlearning platform market with a solid foundation, as it applies to office staff, frontline workers, managers, and technical roles. Onboarding is growing faster because companies are redesigning the first 90 days of employment around spaced learning instead of single-event orientation programs. SHRM stated that structured onboarding programs improve new hire retention by 82% and productivity by more than 70%, which helps explain why this application is gaining budget priority.

Compliance training remains a stable and important application because it keeps learners returning to the platform throughout the year. Sales enablement and product training are also advancing because product cycles now move faster than traditional e-learning revision schedules, which makes shorter modules easier to update and distribute. Leadership and soft skills development are gaining traction as employers use scenario-based lessons to reinforce behavior and decision-making in smaller steps. Customer and partner education is also emerging as a revenue-linked use case, as B2B software providers increasingly seek certified users who adopt products faster and stay engaged longer. These varied applications show that the microlearning platform industry is not tied to a single training budget. Instead, it is spreading across talent development, operations, compliance, and customer success, widening the addressable base without changing the core delivery model.

By End User Industry Vertical: BFSI Anchors Revenue As Healthcare Leads Growth

BFSI accounted for 21.41% of the microlearning platform market share in 2025, while healthcare and life sciences are projected to grow at a 14.83% CAGR through 2031. BFSI remains the largest vertical because compliance obligations in anti-money laundering, know-your-customer checks, cybersecurity awareness, and internal controls create recurring demand for formal training. Those obligations are less sensitive to broader spending cycles, which makes this vertical a dependable source of platform usage and renewal activity. The European Banking Authority strengthened the case for continuous training in its 2025 internal governance guidance, reinforcing the need for documented competency and governance discipline within financial institutions. That environment supports providers that can combine short content delivery with audit trails, credential tracking, and clear reporting.

Healthcare and life sciences are leading growth because protocol changes, staff shortages, and recurring competency requirements create a strong fit with short, repeated modules. Qstream highlighted its work with Cincinnati Children's Hospital in its Q1 2026 review, where spaced reinforcement of clinical protocols improved adherence outcomes, underscoring why proof of practical impact matters in this vertical. Healthcare buyers often expect evidence that content can be updated quickly and remain accurate, especially when the learning topic affects patient care or regulated workflows. Manufacturing is also gaining relevance as robotics, sensors, and quality systems require more frequent operator updates. IT and telecom, retail and e-commerce, and education each generate meaningful demand, but their purchase logic differs depending on whether the emphasis is on speed, turnover reduction, or distributed workforce reach. This spread across sectors gives the microlearning platform market a broader revenue mix, even though regulated industries still carry outsized weight in vendor positioning.

Geography Analysis

North America accounted for 38.66% of the global microlearning platform market in 2025, making it the largest regional revenue contributor. The region benefits from high corporate training spend, a deep enterprise software base, and widespread acceptance of digital learning as a normal part of work. Enterprises in the United States continue to anchor demand because they already operate mature LMS environments and have formal learning and development teams that can scale microlearning across large employee populations. Canada and Mexico are adding to regional growth as training systems become more formal in manufacturing and public-sector settings. This keeps the microlearning platform market well-supported in North America through both installed infrastructure and a broad enterprise customer base.

Asia-Pacific is the fastest-growing region in the microlearning platform market and is projected to advance at a 16.21% CAGR through 2031. Growth is being driven by government-backed upskilling programs, mobile-first learner behavior, and the expansion of formal employment structures that can support structured training. Japan’s Ministry of Economy, Trade, and Industry released Digital Skill Standard version 1.2 in July 2024, which helped define a national benchmark for digital workforce capabilities. India’s National Skill Development Corporation reported by February 2025 that more than 13 million candidates had enrolled through its platform, showing the scale of organized skill development activity in the country. South Korea also supported the expansion of digital learning through KRW 16.9 billion (USD 12.5 million) for AI and digital upskilling in 2025, and KRW 110 billion (USD 80 million) through the AID 30+ workforce reskilling initiative.

Europe remains a mature regional market, with Germany, the United Kingdom, and France accounting for much of the revenue base, and data governance requirements increasingly shape procurement decisions. That makes security credentials, residency controls, and AI compliance more important in vendor selection across the microlearning platform market. The Middle East is emerging as a meaningful growth pocket, especially in Saudi Arabia and the United Arab Emirates, where workforce diversification programs are expanding demand for scalable digital learning. Africa and South America still represent smaller revenue pools, but strong smartphone adoption gives mobile delivery a practical edge in dispersed workforce environments. South Africa, Nigeria, and Kenya in Africa, and Brazil, Argentina, and Colombia in South America, are leading demand in their regions as enterprise digitalization gradually extends into learning technology procurement.

Competitive Landscape

The microlearning platform market remains moderately fragmented, with more than 50 active vendors spanning microlearning specialists and broader learning and talent platforms. Competition centers on AI content generation, reporting depth, workflow integration, and the ability to reduce total ownership costs for enterprise buyers. Vendors are no longer competing only on content libraries or user interface design, but on how well they fit into existing systems, how quickly they can refresh content, and how easily they can demonstrate measurable learning activity. This structure keeps the market open to both focused innovators and large platform vendors with established enterprise relationships.

Several strategic moves highlight how vendors are strengthening their positions. Axonify launched Co-Creator in June 2025 to enable frontline managers to build on-brand content without formal design expertise, addressing a major production bottleneck in large organizations. Pluralsight introduced an AI sandbox and guided learning environment in April 2026 to bring real-time practice feedback into short-form technical learning paths. Docebo added configurable data residency controls in April 2026 to address growing enterprise concerns about sovereignty and privacy requirements. Qstream expanded into SMS-based microlearning in January 2026, extending its reach into field roles that cannot rely on app-heavy delivery. These actions show that product differentiation is increasingly built through specific operating capabilities rather than broad branding claims.

There is still room in the market for workflow systems and learning systems that are not yet tightly linked. Real-time triggers from ERP, CRM, field operations, and shift management tools remain underused opportunities to make training more timely and relevant. Bites Learning’s integration with EZShift in May 2026 directly addressed this potential by embedding microlearning into shift handover activities. Another open area is the SME segment in Asia-Pacific and South America, where affordable, multilingual, mobile-first products could meet demand not well served by enterprise-oriented systems. Bigtincan’s 2024 and 2025 filings showed a continued move toward sales readiness and revenue enablement, with microlearning serving as one part of a broader commercial platform strategy. This boundary shift underscores how the microlearning platform market is increasingly shaped by adjacent software categories moving into learning use cases from nearby positions.

Microlearning Platform Industry Leaders

Axonify Inc.

Qstream, Inc.

eduMe Ltd.

Epignosis LLC

7taps OpCo LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Bites Learning and EZShift announced a partnership integrating microlearning directly into EZShift's shift management platform. The integration enables frontline managers to assign training modules as part of shift handover workflows, embedding learning within operational task execution for deskless workforces.

- April 2026: Pluralsight launched a new AI sandbox, guided learning paths, and enterprise integrations designed to embed microlearning within technology skill development workflows. The release targets IT and DevOps teams and introduces real-time practice environments that convert conceptual microlearning modules into applied skill reinforcement.

- April 2026: Docebo released a significant platform update introducing configurable data residency controls across AWS, Azure, and Google Cloud, enabling enterprises to comply with EU data sovereignty requirements while maintaining cloud scalability. The capability was positioned as a competitive response to GDPR-driven procurement criteria among European enterprise accounts.

- March 2026: Vector Solutions launched a microlearning suite specifically designed for safety and compliance education, targeting industries with continuing education mandates for safety-critical roles. The suite includes pre-built compliance content modules and audit-trail reporting that simplifies regulatory documentation for safety managers.

Global Microlearning Platform Market Report Scope

The microlearning platform market comprises digital learning systems that deliver short, focused training modules for rapid skill acquisition, reinforcement, and continuous workforce development. These platforms emphasize mobile-first access, AI-assisted authoring, compliance tracking, and workflow integration, enabling organizations to update content quickly and align learning with evolving job requirements.

The Global Microlearning Platform Market Report is segmented by Platform Type (Standalone Microlearning Platforms, Integrated LMS Platforms, and AI-Enabled Learning Platforms), Deployment Model (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-sized Enterprises), Application (Employee Onboarding and New Hire Readiness, Compliance Training, Sales Enablement and Product Training, Workforce Upskilling and Reskilling, Leadership and Soft Skills Development, and Customer and Partner Education), Industry Vertical (Banking Financial Services and Insurance, Information Technology and Telecom, Retail and E-commerce, Manufacturing, Healthcare and Life Sciences, Education, Government and Public Sector, and Media and Entertainment), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Standalone Microlearning Platforms |

| Integrated LMS Platforms |

| AI-Enabled Learning Platforms |

| Cloud |

| On-premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Employee Onboarding and New Hire Readiness |

| Compliance Training |

| Sales Enablement and Product Training |

| Workforce Upskilling and Reskilling |

| Leadership and Soft Skills Development |

| Customer and Partner Education |

| BFSI |

| IT and Telecom |

| Retail and E-commerce |

| Manufacturing |

| Healthcare and Life Sciences |

| Education |

| Government and Public Sector |

| Media and Entertainment |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America |

| By Platform Type | Standalone Microlearning Platforms | |

| Integrated LMS Platforms | ||

| AI-Enabled Learning Platforms | ||

| By Deployment Model | Cloud | |

| On-premises | ||

| Hybrid | ||

| By End User Enterprise Size | Large Enterprises | |

| Small and Medium-sized Enterprises | ||

| By Application | Employee Onboarding and New Hire Readiness | |

| Compliance Training | ||

| Sales Enablement and Product Training | ||

| Workforce Upskilling and Reskilling | ||

| Leadership and Soft Skills Development | ||

| Customer and Partner Education | ||

| By End User Industry Vertical | BFSI | |

| IT and Telecom | ||

| Retail and E-commerce | ||

| Manufacturing | ||

| Healthcare and Life Sciences | ||

| Education | ||

| Government and Public Sector | ||

| Media and Entertainment | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the microlearning platform market?

The microlearning platform market stands at USD 2.46 billion in 2026 and is projected to reach USD 4.34 billion by 2031, growing at a 12.05% CAGR over 2026-2031.

Which platform type leads revenue generation in this space?

Integrated LMS platforms led revenue with a 46.21% share in 2025 because many enterprises prefer microlearning functions that connect directly with existing learner records and reporting systems.

Which deployment model is growing the fastest for microlearning platforms?

Hybrid deployment is the fastest-growing model at a 14.13% CAGR through 2031, reflecting stronger demand from regulated sectors that need cloud scale and tighter data control at the same time.

Why are companies using microlearning more often for onboarding?

Employee onboarding and new hire readiness is projected to grow at a 15.42% CAGR through 2031 as employers replace one-time orientation with spaced learning during the first 90 days.

Which end-user vertical has the strongest growth outlook?

Healthcare and life sciences is forecast to grow at a 14.83% CAGR through 2031 because the sector needs recurring competency checks, protocol updates, and documented learning evidence.

Which region is expanding the fastest for microlearning platforms?

Asia-Pacific is expected to grow at a 16.21% CAGR through 2031, supported by government-led skill programs, smartphone-first learners, and the expansion of formal workforce training across major economies.

Page last updated on: