Autonomous Procurement And Intelligent Sourcing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

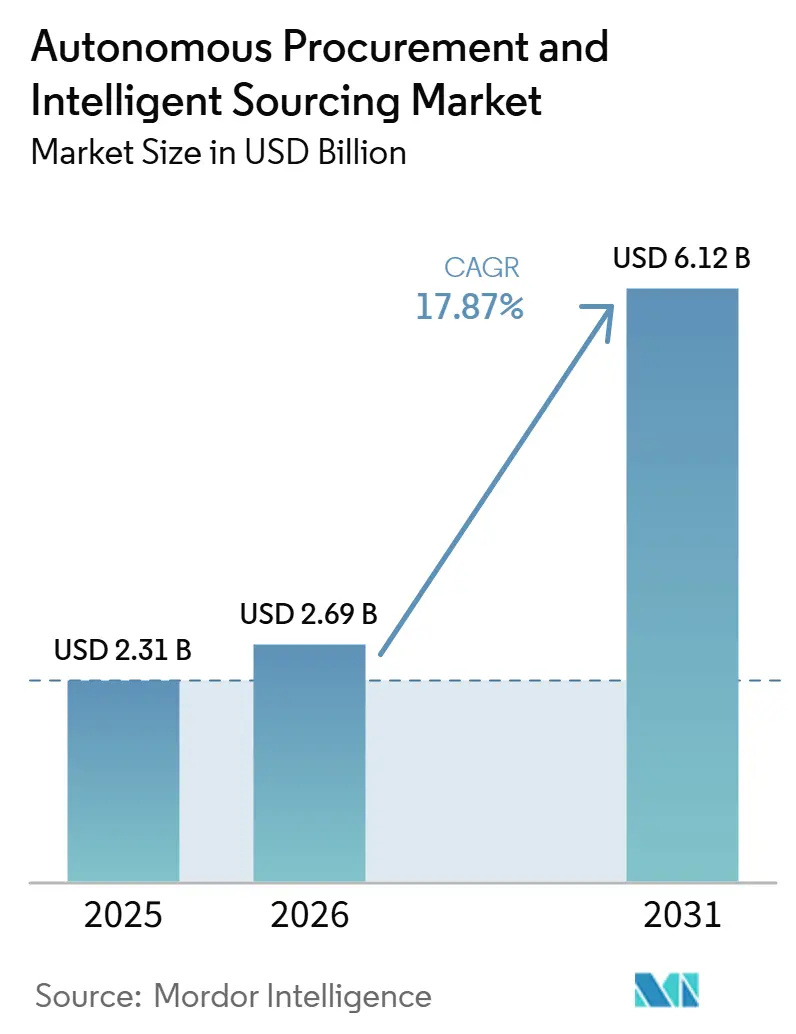

| Market Size (2026) | USD 2.69 Billion |

| Market Size (2031) | USD 6.12 Billion |

| Growth Rate (2026 - 2031) | 17.87% CAGR |

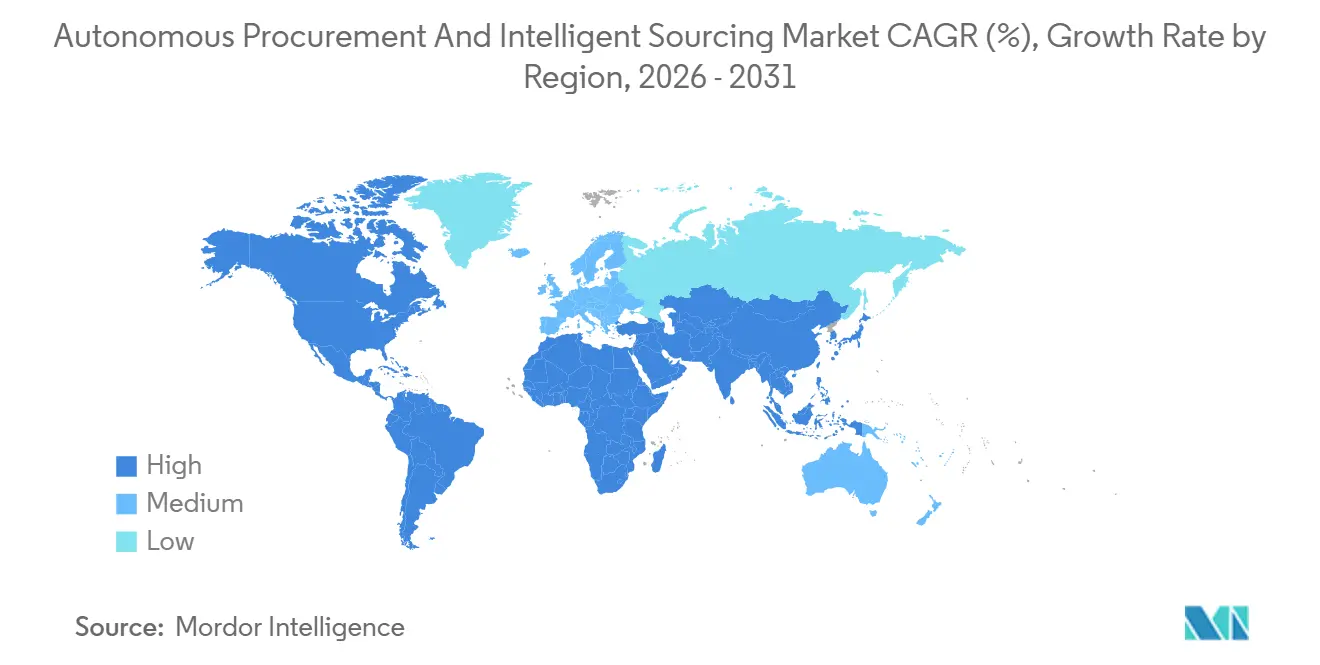

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Autonomous Procurement And Intelligent Sourcing Market Analysis by Mordor Intelligence

The autonomous procurement and intelligent sourcing market size is expected to grow from USD 2.31 billion in 2025 to USD 2.69 billion in 2026 and is forecast to reach USD 6.12 billion by 2031 at 17.87% CAGR over 2026-2031. Rapid migration from rule-based workflow tools to agentic AI engines is unlocking real-time negotiation, predictive risk scoring, and embedded sustainability checks, compressing cycle times and widening savings pools. Cloud deployment continues to dominate, yet hybrid architectures are scaling quickly as highly regulated buyers keep master data on-premise while running analytics in the public cloud. Early adopter industries such as manufacturing enjoy mature supplier ecosystems, while life sciences buyers accelerate spending to meet serialization and audit mandates. Venture funding and product launches indicate a decisive shift toward autonomous decision-making, but persistent ERP data-quality gaps and cybersecurity concerns remain the chief brakes on near-term velocity.

Key Report Takeaways

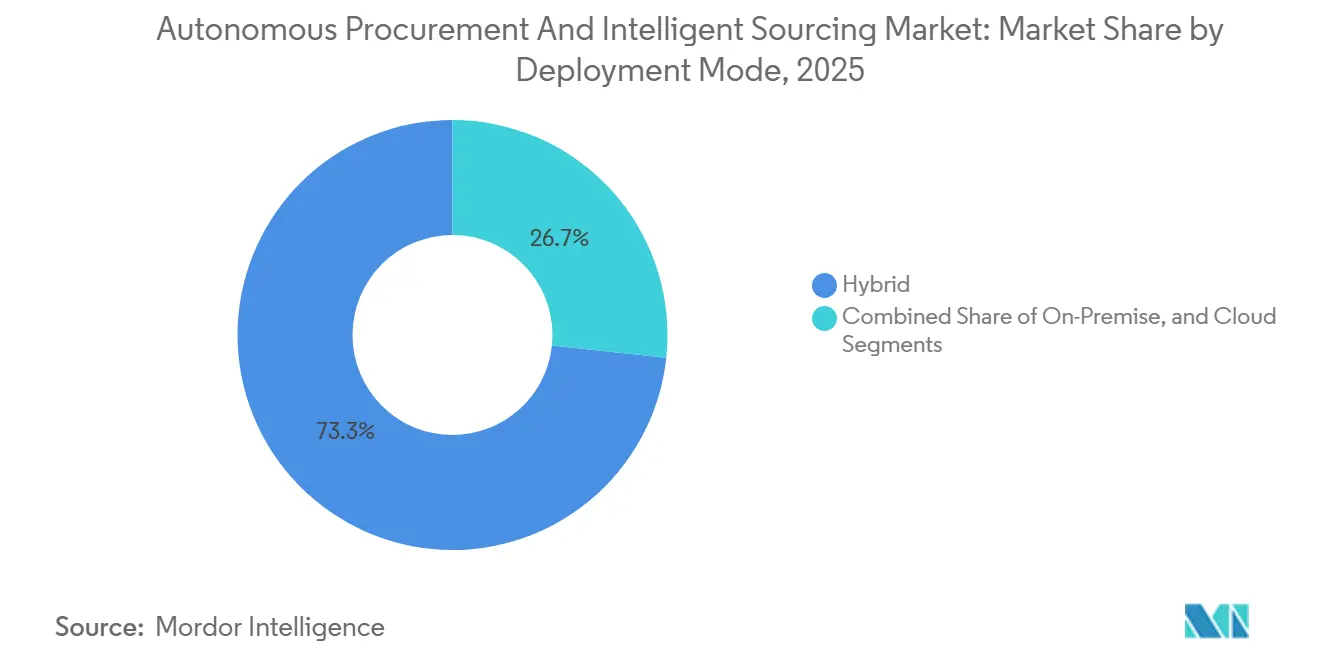

- By deployment, cloud deployment held 73.31% of the autonomous procurement and intelligent sourcing market share in 2025, while hybrid models are projected to expand at an 18.47% CAGR through 2031.

- By component, software accounted for 64.53% of revenue in 2025; services are forecast to grow at a 18.27% CAGR as enterprises seek integration, data cleansing, and continuous model tuning support.

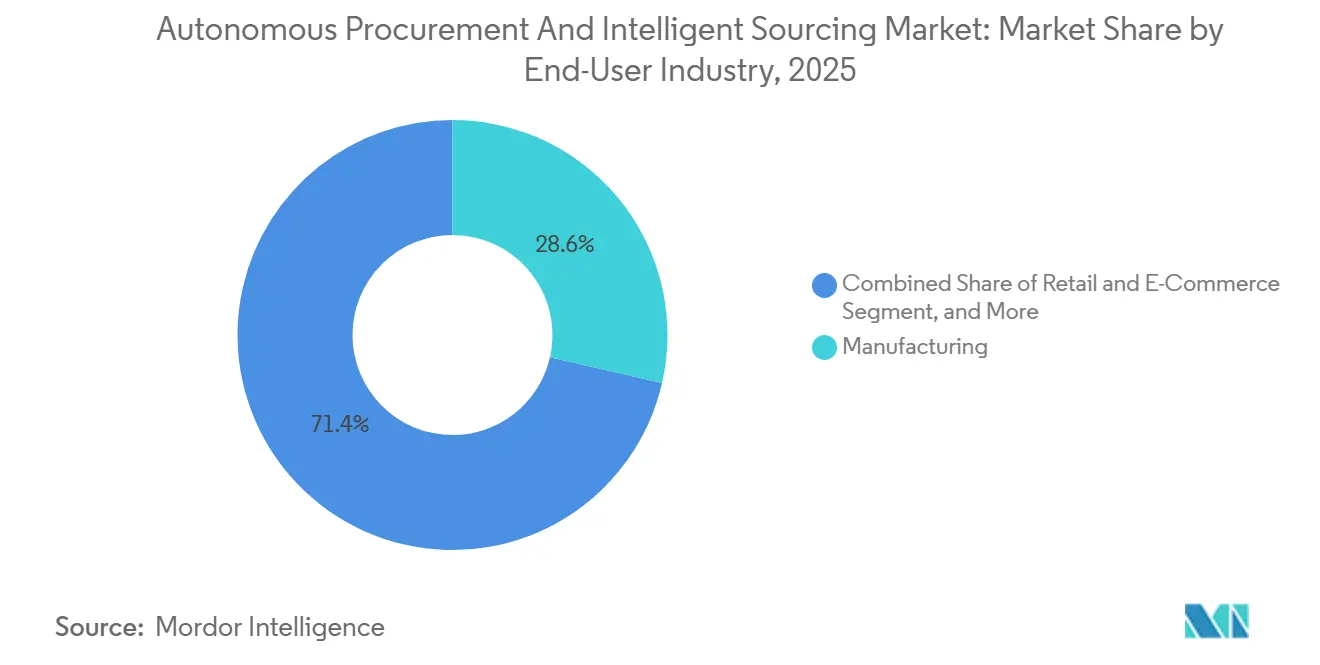

- By end-user industry anufacturing led with 28.59% of 2025 spending, but healthcare and life sciences are set to advance at a 19.07% CAGR through 2031.

- By organization size, large enterprises captured 65.22% of the 2025 value, whereas small and medium enterprises are poised to expand at an 18.67% CAGR as no-code platforms lower entry barriers.

- By geography, North America accounted for 34.81% of global revenue in 2025; Asia-Pacific is the fastest-growing region, with an 18.87% CAGR on the back of government-sponsored digitization drives.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Autonomous Procurement And Intelligent Sourcing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Maturation of Generative AI for Spend Intelligence | +4.2% | Global, with early concentration in North America and Western Europe | Short term (≤ 2 years) |

| Accelerating Shift to Cloud-Native Procurement Suites | +3.8% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Mainstream Adoption of Autonomous Negotiation Bots | +3.1% | North America, Europe, and advanced Asia-Pacific markets | Medium term (2-4 years) |

| ESG-Driven Sourcing Mandates in Regulated Industries | +2.6% | Europe (CSDDD, EUDR), North America (SEC Climate Rule), Asia-Pacific spillover | Long term (≥ 4 years) |

| Expansion of Supplier Risk Data Exchanges | +1.9% | Global, with accelerated adoption in supply-chain-intensive sectors | Medium term (2-4 years) |

| Growing Venture Funding for Procurement Tech Start-ups | +1.5% | North America and Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Maturation of Generative AI for Spend Intelligence

Language-model copilots now parse contracts, emails, and purchase-order histories to uncover tail-spend leakages and recommend category consolidation. Pfizer eliminated 26 manual requisition steps after integrating an agentic workflow engine that automates supplier onboarding. Generative AI also surfaces hidden pricing variances, enabling dynamic budget reallocations that were previously impractical with static dashboards. Enterprises report higher classification accuracy for unstructured spend, which improves supplier rationalization and discount capture. Real-time commodity feeds fine-tune negotiation thresholds, replacing rule-based triggers that lag market volatility.

Accelerating Shift to Cloud-Native Procurement Suites

SAP’s rebuild of Ariba on its Business Technology Platform decouples procurement logic from monolithic databases, allowing microservices to scale AI workloads elastically. Oracle’s Fusion Cloud Procurement 26A embeds 29 pre-built AI agents that draft sourcing events and flag compliance breaches, reducing implementation cycles from months to weeks. Government buyers gain similar agility: the United Arab Emirates compressed catalogue ordering from 60 days to 6 minutes after moving to a cloud-native procurement portal. Hybrid blueprints that host master data on-premise while running analytics in public clouds satisfy sovereignty rules without sacrificing AI performance.

Mainstream Adoption of Autonomous Negotiation Bots

Reinforcement-learning agents in GEP’s SMART platform adjust reserve prices mid-auction, while Zycus’ negotiation bots evaluate multi-attribute bids that balance price, lead time, and sustainability credentials.[1]GEP Worldwide, “SMART Platform Negotiation Engine,” gep.com Keelvar’s combinatorial optimization engine awards bundled lots within seconds, freeing sourcing teams from exhaustive spreadsheet analysis. Autonomous haggling is most valuable in volatile commodity markets and high-velocity retail replenishment, where daily price swings erode the utility of annual contracts. Early deployments show 5%-8% incremental savings on indirect categories that once escaped formal sourcing.

ESG-Driven Sourcing Mandates in Regulated Industries

The European Union’s Corporate Sustainability Due Diligence Directive and Deforestation Regulation oblige buyers to trace emissions and raw-material provenance before awarding contracts. Autonomous procurement suites ingest third-party carbon calculators and conflict-mineral databases, automatically gating non-compliant suppliers. Saudi Arabia’s Vision 2030 embeds sustainability scoring into public procurement, formalized by the Digital Government Authority's 2025 guidelines. Pharmaceutical firms integrate serialization data with AI contract intelligence to ensure ingredient traceability, creating cross-functional demand for real-time compliance automation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Data-Quality Issues in Legacy ERPs | -2.3% | Global, most acute in enterprises with multi-decade ERP installations | Medium term (2-4 years) |

| Cybersecurity Concerns over AI-Led Decision Making | -1.8% | Global, heightened in regulated industries (BFSI, healthcare, defense) | Short term (≤ 2 years) |

| Skill Gaps in Advanced Analytics among Procurement Teams | -1.2% | Global, more pronounced in mid-market and emerging-market enterprises | Long term (≥ 4 years) |

| Fragmented Global Regulatory Standards for E-Invoicing | -0.9% | Europe (ViDA), Asia-Pacific (India GST, Peppol), Latin America (national mandates) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Data-Quality Issues in Legacy ERPs

Decades of inconsistent supplier records, duplicate material codes, and partial invoice data undermine AI model accuracy. Pfizer’s automation rollout required extensive cleansing sprints before workflow orchestration delivered measurable value. Manufacturing firms with sprawling bill-of-materials hierarchies struggle most, often facing 18-24-month remediation timelines. Poor data lineage also hampers autonomous negotiation bots that rely on accurate historical bids to calibrate concession limits.

Cybersecurity Concerns over AI-Led Decision Making

Apono’s 2025 survey found that 98% of enterprises experienced security incidents affecting AI deployments, and widespread fears that agentic bots could be manipulated through adversarial prompts. High-risk classifications under the European Union’s AI Act mandate rigorous conformity assessments for procurement automation.[2]European Commission, “AI Act Regulatory Text,” ec.europa.eu Enterprises deploy zero-trust controls and behavioral monitoring, yet these defenses add cost and extend proof-of-concept timelines, dampening immediate adoption in sensitive sectors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Hybrid Architectures Bridge Sovereignty and Agility

Hybrid models controlled 73.31% of cloud-adjacent workloads in 2025 and are projected to outpace overall growth in the autonomous procurement and intelligent sourcing markets at an 18.47% CAGR. Many defense and public-sector agencies isolate classified data on-premise, while leveraging cloud analytics for supplier collaboration. The autonomous procurement and intelligent sourcing market size for hybrid deployments is expected to grow as confidential-computing enclaves mature, allowing sensitive records to remain encrypted even during processing.

Regulated buyers in the Middle East are showcasing successful proof-of-concept implementations. For instance, the United Arab Emirates securely hosts contract documents within national data centers while simultaneously exposing supplier APIs through the public cloud. This dual approach ensures compliance with regulatory requirements while leveraging the scalability and flexibility of cloud technologies. Similarly, Saudi Arabia’s Etimad portal adopts a comparable framework to efficiently manage its extensive USD 1.3 trillion project pipeline. This hybrid architecture not only addresses the unique needs of highly regulated industries but also serves as a replicable model for other regions. As a result, this approach is expected to drive sustained double-digit growth in adoption and implementation through 2031.

By Component: Services Surge as AI Integration Complexity Escalates

Software accounted for 64.53% of the total revenue in 2025, maintaining its dominant position in the market. However, services such as integration, data cleansing, and model tuning are witnessing significant growth, with a compound annual growth rate (CAGR) of 18.27%. The market share for managed services in the autonomous procurement and intelligent sourcing sector is expected to grow further as enterprises increasingly face challenges related to the complexities of legacy ERP systems and fragmented invoice standards, which require specialized solutions.

JAGGAER’s strategic partnership with Unite integrates consulting services that streamline European catalogues and ensure compliance with VAT regulations, addressing critical operational needs.[3]JAGGAER LLC, “Unite Partnership Announcement,” jaggaer.com Similarly, Oro Labs’ collaboration with Pfizer underscored the labor-intensive process of aligning legacy workflows with AI-driven agents, showcasing the demand for expertise in this area. Additionally, mid-market buyers are increasingly outsourcing tasks such as continuous supplier-risk scoring and ESG (Environmental, Social, and Governance) monitoring to specialized service providers. These providers not only ensure audit readiness but also enable enterprises to shift from capital expenditure (capex) software budgets to operational expenditure (opex) service contracts, offering greater flexibility and efficiency in managing procurement processes.

By End-User Industry: Healthcare Overtakes Manufacturing on Compliance Automation

Manufacturing accounted for the largest share of 2025 spending, contributing 28.59% to the total. However, demand from the life sciences sector is growing rapidly, with a compound annual growth rate (CAGR) of 19.07%. The autonomous procurement and intelligent sourcing market within the healthcare sector is expanding significantly as drug-traceability regulations increasingly mandate real-time verification of active-ingredient provenance. This trend is driven by the need for greater transparency and compliance in the pharmaceutical supply chain to ensure product authenticity and safety.

Serialization rules under the Drug Supply Chain Security Act push pharmaceutical buyers to ingest supplier certificates into AI risk engines, eliminating manual cross-checks. Pfizer’s clinical-trial procurement now routes investigator-site requisitions through automated approvals, trimming onboarding from weeks to days. While automotive and electronics players continue to refine just-in-time replenishment with negotiation bots, healthcare’s stricter audit environment drives faster incremental spend on compliance-ready AI modules.

By Organization Size: SMEs Close the Gap via Pay-per-Transaction Platforms

Large enterprises accounted for 65.22% of the 2025 market value, but small and medium enterprises (SMEs) are expected to grow faster, with a compound annual growth rate (CAGR) of 18.67%. This growth is driven by the increasing adoption of no-code intake portals and subscription-based models, which have empowered firms with annual spending below USD 50 million to access autonomous sourcing solutions without the need for significant IT infrastructure investments. These tools allow SMEs to streamline their operations and reduce costs, making advanced sourcing technologies more accessible to smaller organizations that previously faced barriers due to high upfront costs and technical complexities.

Emerging start-ups such as Lio and Procol have introduced innovative pricing strategies that charge a percentage of realized savings, effectively aligning costs with outcomes and eliminating the need for capital-intensive licensing fees. This approach not only reduces financial risks for SMEs but also ensures that the pricing structure is directly tied to the value delivered. Additionally, public procurement portals in India have implemented SME-preference scoring systems, which prioritize contracts for local businesses and encourage digital adoption among smaller suppliers. As open-source language models continue to democratize access to AI tools, the cost disparity between enterprise and SME deployments is expected to diminish further. This trend will enhance accessibility, foster increased competitiveness across the market, and enable SMEs to leverage advanced technologies on par with larger enterprises.

Geography Analysis

North America accounted for 34.81% of the 2025 revenue, primarily driven by early adoption of cloud-suite technologies and a high concentration of venture capital investments. The region witnessed significant developments, including a USD 100 million Series C funding round for Oro Labs and multiple strategic acquisitions, underscoring investor confidence in AI-driven sourcing solutions. However, the presence of mature ERP estates has led to integration backlogs, tempering incremental growth. As a result, the region's 5-year compound annual growth rate (CAGR) is projected to remain within the range of 18%, lagging behind the faster growth observed in the Asia-Pacific region.

Asia-Pacific is expected to grow at a robust CAGR of 18.87%, fueled by government initiatives mandating e-invoicing and digital procurement practices. For instance, India’s Government e-Marketplace has incorporated machine learning algorithms to enhance fraud detection capabilities, while the United Arab Emirates has significantly reduced ordering lead times to mere minutes by implementing a cloud-native procurement platform. Additionally, large-scale infrastructure projects in Saudi Arabia, coupled with multilateral funding from organizations such as the World Bank and the Asian Development Bank, continue to support the rollout of procurement platforms across South and Southeast Asia, further driving regional growth.

Europe’s market outlook is heavily influenced by regulatory compliance expenditures. The VAT in the Digital Age directive mandates real-time e-invoicing by 2028-2030, while emerging ESG due diligence laws require the integration of sustainability checkpoints into procurement processes. Germany and France are leading the charge in manufacturing automation, while the United Kingdom has seen an increase in hybrid architectures post-Brexit to segregate EU and domestic supplier data. Meanwhile, South America and Africa remain in the early stages of adoption, with growth spikes linked to national e-invoicing mandates. However, macroeconomic challenges and infrastructure limitations continue to moderate the pace of adoption in these regions.

Competitive Landscape

The autonomous procurement and intelligent sourcing market is moderately fragmented, with roughly 666 vendors spanning source-to-pay, supplier risk, and tail-spend niches. Incumbent ERP providers leverage installed bases to upsell AI modules, while best-of-breed specialists innovate faster on negotiation and risk analytics. Oracle embedded 29 AI agents into Fusion Cloud Procurement 26A in March 2026, shrinking implementation lead times and bringing agentic capabilities on-par with innovators.

JAGGAER’s JAI AI Copilot automates intake and compliance workflows, delivering documented savings of EUR 9.4 million (USD 10.6 million) for TRUMPF in manufacturing. Zycus’ Merlin Agentic AI deploys reinforcement learning for real-time bid optimization, while GEP’s SMART platform integrates similar functionality across multi-attribute auctions.[4]Zycus Inc., “Merlin Agentic AI Product Sheet,” zycus.com Keelvar’s combinatorial optimizer addresses bundled freight and logistics sourcing, helping it win share among global shippers.

Venture-backed challengers attack whitespace in SME enablement and niche compliance. Oro Labs’ unified workflow engine focuses on tail-spend visibility, whereas Lio automates indirect negotiations for sub-USD 50 million procurement budgets. Strategic alliances, such as JAGGAER’s integration with Unite’s European marketplace, and Workday’s earlier acquisition of Scout RFP, signal a consolidating trajectory as agentic AI becomes table stakes across the ecosystem.

Autonomous Procurement And Intelligent Sourcing Industry Leaders

SAP SE

Oracle Corporation

Coupa Software Incorporated

GEP Worldwide LLC

Jaggaer LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Oracle released Fusion Cloud Procurement 26A, adding 29 embedded AI agents for category suggestion, autonomous sourcing, and compliance alerts.

- March 2026: JAGGAER launched JAI AI Copilot, an orchestrator that automates supplier intake and risk gating, freeing buyers to focus on strategic tasks.

- January 2026: Zycus was recognized as a Leader for its Merlin Agentic AI platform that unifies intake-to-outcome automation.

- December 2025: JAGGAER version 25.3 introduced automated supplier gating and enhanced risk controls.

Global Autonomous Procurement And Intelligent Sourcing Market Report Scope

The Autonomous Procurement and Intelligent Sourcing Market refers to the global market for advanced software solutions and associated services that leverage artificial intelligence (AI), machine learning (ML), automation, and data analytics to enable organizations to automate, optimize, and enhance procurement and sourcing processes with minimal human intervention.

The Autonomous Procurement and Intelligent Sourcing Market Report is Segmented by Deployment Mode (Cloud, On-Premise, and Hybrid), Component (Software, and Services), End-User Industry (Manufacturing, Retail and E-Commerce, BFSI, Healthcare and Life Sciences, Energy and Utilities, and Government and Public Sector), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-Premise |

| Hybrid |

| Software |

| Services |

| Manufacturing |

| Retail and E-Commerce |

| BFSI |

| Healthcare and Life Sciences |

| Energy and Utilities |

| Government and Public Sector |

| Large Enterprises |

| Small and Medium Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Deployment Mode | Cloud | ||

| On-Premise | |||

| Hybrid | |||

| By Component | Software | ||

| Services | |||

| By End-User Industry | Manufacturing | ||

| Retail and E-Commerce | |||

| BFSI | |||

| Healthcare and Life Sciences | |||

| Energy and Utilities | |||

| Government and Public Sector | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is spending on autonomous procurement platforms growing to 2031?

Market value is projected to reach USD 6.12 billion by 2031, expanding at a 17.87% CAGR from 2026-2031.

Which deployment approach shows the strongest growth momentum?

Hybrid architectures are forecast to rise at an 18.47% CAGR as organizations mix on-premise data control with cloud analytics.

Why are life-sciences buyers accelerating adoption?

Serialization mandates and strict audit trails push healthcare firms to embed AI-driven compliance checks, driving a 19.07% CAGR through 2031.

What is the chief restraint to full autonomy in sourcing?

Poor data quality in legacy ERP systems knocks 2.3 percentage points off forecast CAGR by lowering algorithm accuracy and delaying projects.

Which region will add the most new revenue by 2031?

Asia-Pacific, expanding at an 18.87% CAGR, benefits from government-backed digitization mandates and multilateral funding.

How are small and medium enterprises approaching adoption costs?

No-code portals and pay-per-transaction pricing let SMEs deploy agentic bots without large upfront licenses, supporting an 18.67% CAGR for the segment.

Page last updated on: