Platform Engineering And Internal Developer Platform (IDP) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

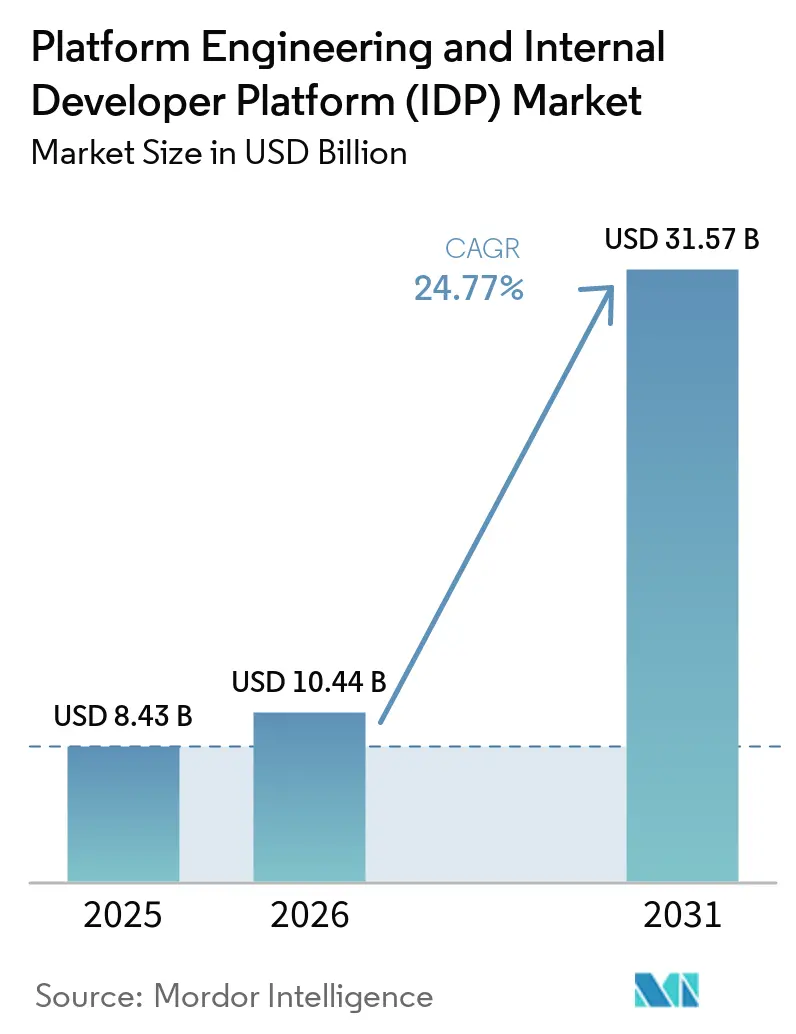

| Market Size (2026) | USD 10.44 Billion |

| Market Size (2031) | USD 31.57 Billion |

| Growth Rate (2026 - 2031) | 24.77% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Platform Engineering And Internal Developer Platform (IDP) Market Analysis by Mordor Intelligence

The platform engineering and internal developer platform (IDP) market size is expected to increase from USD 10.44 billion in 2026 to reach USD 31.57 billion by 2031, growing at a CAGR of 24.77% over 2026-2031. Rising Kubernetes complexity, heightened compliance obligations, and the need to relieve application teams of infrastructure chores are accelerating adoption. Enterprises are moving from scattered DevOps point tools toward unified abstraction layers that cut onboarding time, embed policy-as-code, and automate golden-path templates, helping organizations shrink incident resolution cycles and raise deployment frequency. Momentum is strongest in regulated industries, where self-service portals deliver built-in audit trails for PCI-DSS 4.0 or HIPAA while shielding developers from low-level security tasks. Vendors are bundling observability, CI/CD, and governance into integrated suites, a strategic shift that reduces tool sprawl and positions platforms as product-centric offerings rather than engineering side projects.

Key Report Takeaways

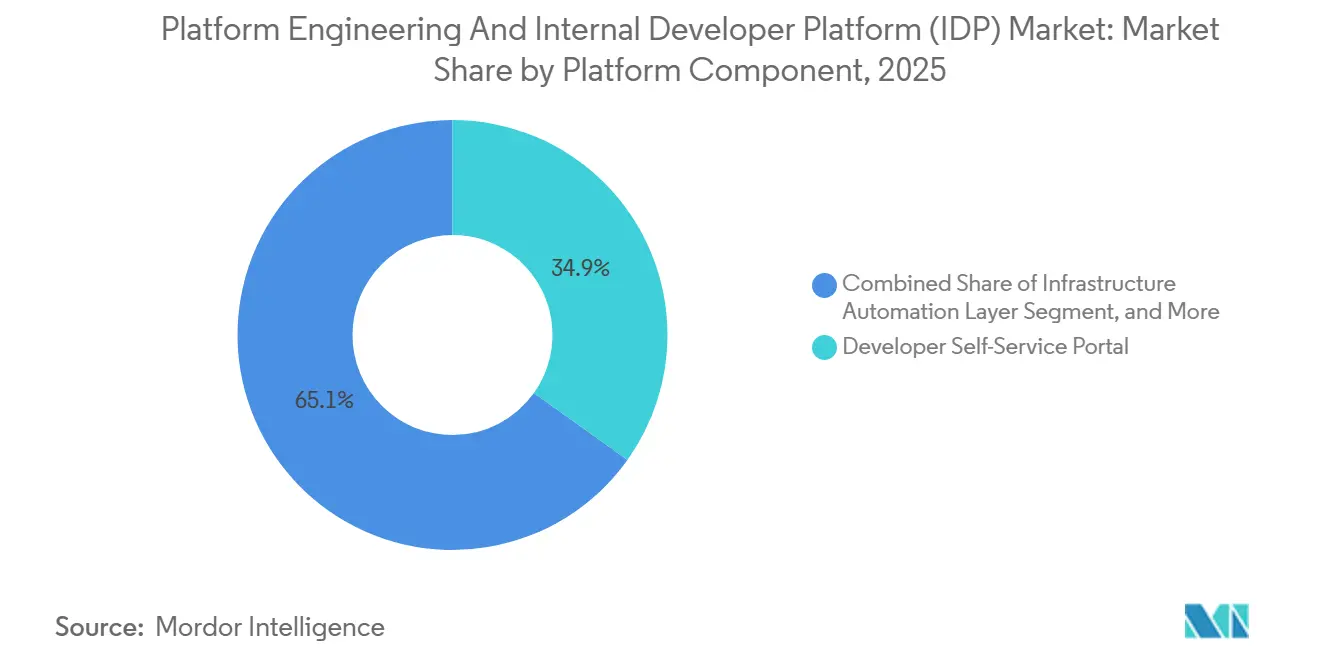

- By platform component, developer self-service portals led with 34.87% revenue share in 2025, while observability and telemetry components are projected to advance at a 25.77% CAGR through 2031.

- By deployment mode, cloud deployment held 46.32% of the platform engineering and internal developer platform market share in 2025, but hybrid architectures are forecast to expand at a 35.37% CAGR to 2031.

- By organization size, large enterprises commanded 61.38% of spending in 2025, while small and medium-sized enterprises are expected to grow at a 25.17% CAGR through 2031.

- By end-user industry, technology and software captured 29.32% of demand in 2025; healthcare and life sciences are poised for the fastest rise at a 26.57% CAGR.

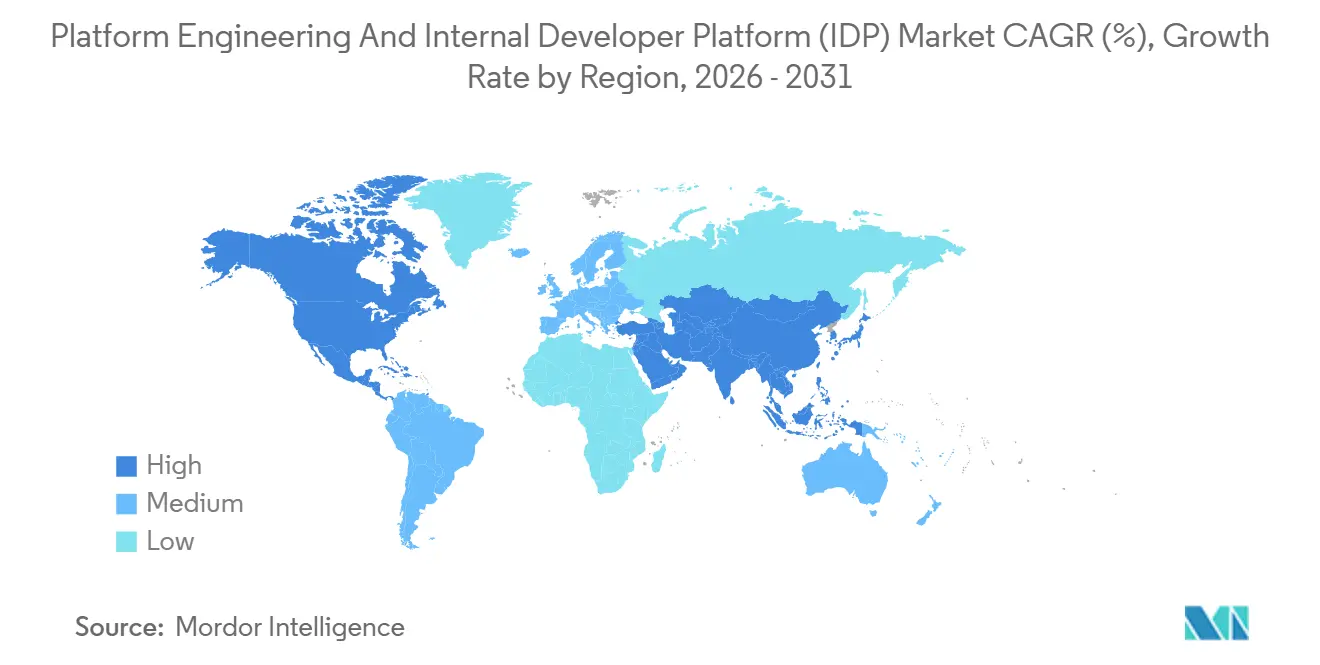

- By geography, North America accounted for 41.68% of 2025 revenue, whereas Asia-Pacific is projected to climb at a 24.89% CAGR during the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Platform Engineering And Internal Developer Platform (IDP) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Shift to Cloud-Native Architectures | +6.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Rising Demand for Developer Productivity Gains | +5.8% | Global, particularly North America and Asia-Pacific | Short term (≤ 2 years) |

| Increasing Kubernetes Complexity Necessitating Abstraction | +4.9% | Global, with early adoption in technology and financial services sectors | Medium term (2-4 years) |

| Expansion of Platform Teams in Large Enterprises | +3.7% | North America and Europe, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Growing Compliance Requirements for Software Supply Chains | +2.4% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Emergence of AI-Augmented DevOps Toolchains | +1.8% | North America and Asia-Pacific technology hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Shift to Cloud-Native Architectures

Cloud-native workloads grew to 82% of production estates in 2025, but the operational burden ballooned as Kubernetes introduced more than 50 core resource types, each carrying dozens of configuration parameters. Internal developer platforms now provision namespaces, ingress, and policy bundles by default, eliminating YAML sprawl and shortening release cycles. Early deployments, such as Nokia’s 5G core, saved hundreds of engineering hours per release by removing manual cluster drift.[1]Nokia, “5G Core Deployment Platform Engineering Case Study,” NOKIA.COM Financial institutions layer Basel III and audit logging policies directly into templates, ensuring regulatory alignment without slowing product delivery. As managed Kubernetes services add edge and multi-networking features, abstraction layers will remain pivotal for keeping the developer experience simple.

Rising Demand for Developer Productivity Gains

Prior to platform adoption, developers devoted roughly 35% of their week to infrastructure tasks, stalling feature velocity. Organizations running mature platforms report near-40% boosts in deployment frequency and around 25% faster mean-time-to-recovery, metrics that translate into sharper competitive positioning. Shopify’s migration to a composable admin interface processed 67 million daily page views across 101 teams, an achievement made possible by platform-driven automation. Regulatory frameworks such as GDPR embed privacy-by-design principles into golden paths so developers never manually handle sensitive data. Affordable SaaS subscriptions, priced near USD 1,000 per month, extend these productivity gains to resource-constrained mid-market firms.

Increasing Kubernetes Complexity Necessitating Abstraction

The Kubernetes 1.32 release expanded edge readiness, but its broader API surface amplified the learning curve, prompting 89% of Backstage adopters to add service catalogs that mask low-level details. Telecommunications providers seeking 99.999% uptime rely on GitOps reconciliation managed by platform teams, not application squads. Google Kubernetes Engine’s multi-networking APIs, launched in March 2026, further complicate native operations but become accessible when surfaced through opinionated platform APIs. Canonical’s 15-year-long-term-support pledge illustrates the maintenance burden that centralized teams absorb so that application developers can focus purely on code.

Expansion of Platform Teams in Large Enterprises

80% of large software organizations are on track to run formal platform teams by 2026, up from 45% in 2023. These units treat developers as internal customers, tracking adoption and satisfaction rather than server uptime. Humanitec’s Platform Orchestrator 2 uses AI to auto-generate pipelines from manifests, slashing manual toil and allowing small platform squads to support hundreds of app teams. Financial-services firms under the Digital Operational Resilience Act centralize third-party dependency reviews within platform layers, sweeping in risk management at code-commit time. The talent war remains fierce, with platform engineer salaries commanding 27% premiums over traditional DevOps roles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Investment in Building Internal Platforms | -3.1% | Global, particularly acute in small and medium-sized enterprises | Short term (≤ 2 years) |

| Talent Shortage of Platform Engineers | -2.6% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Integration Challenges with Legacy Systems | -1.9% | Global, concentrated in financial services and manufacturing | Long term (≥ 4 years) |

| Security Concerns Around Self-Service Portals | -1.4% | Europe and North America, driven by regulatory scrutiny | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Investment in Building Internal Platforms

A production-grade platform often needs three to five full-time engineers for up to 18 months, equating to labor costs between USD 150,000 and USD 650,000 before tooling or cloud fees. This capital hurdle sidelines many small and medium-sized enterprises, which accounted for only 38.62% of 2025 spending despite representing the majority of global businesses. Continuous feature evolution, routine security patching, and user-experience refinement compound lifetime costs, prompting some firms to adopt subscription offerings. Software Defined Automation’s path to ISO 27001 certification in February 2026, following a USD 10 million seed round, highlights how compliance overhead inflates the total price tag.

Talent Shortage of Platform Engineers

Hybrid skills that blend infrastructure automation with product thinking remain scarce. Universities have yet to launch formal curricula, so employers must reskill site-reliability engineers internally. OECD data show that only 14% of SMEs had adopted AI tools by 2024, underscoring the digital-skills gap throttling platform adoption.[2]Organization for Economic Co-operation and Development, “AI Adoption in SMEs 2024,” OECD.ORG North America and Europe host the deepest talent pools, but Asia-Pacific’s surge in sovereign cloud projects is widening regional disparities. Limited headcount forces platform teams to gate self-service expansion, delaying broader organizational rollout.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Component: Portals Lead, Observability Surges

Developer self-service portals captured 34.87% of 2025 revenue, reflecting early enterprise emphasis on workflow automation. This slice of the platform engineering and internal developer platform market size is expected to retain leadership as portals remain the primary touchpoint for developers creating new services. Observability and telemetry pieces, however, are set to grow 25.77% annually, driven by OpenTelemetry adoption that mandates trace-first design across all golden paths. Integrated suites now fold metrics, traces, and logs into the initial scaffolding, so every microservice emits data without extra developer steps, ensuring that performance regressions are caught before they impact users.

A parallel trend favors CI/CD orchestration woven into platform blueprints, with 67% of 2025 respondents citing GitOps as their delivery pattern of choice. Infrastructure automation components, exemplified by Pulumi’s OpenAPI release, abstract diverse cloud REST endpoints behind uniform APIs, easing multi-provider workflows.[3]Pulumi, “OpenAPI Support for Cloud REST APIs,” PULUMI.COM Governance and security layers embed the Open Policy Agent to enforce guardrails at admission controller time. Collectively, these pieces suggest the platform engineering and internal developer platform (IDP) market will shift from discrete modules toward opinionated bundles that minimize configuration debt.

By Deployment Mode: Hybrid Architectures Accelerate

Cloud deployment held 46.32% of the platform engineering and internal developer platform market share in 2025, thanks to mature managed Kubernetes services that lower operational lift. Yet hybrid topologies are projected to compound at 35.37% each year, more than 10 percentage points above the headline CAGR. Driving the swing are regulatory mandates, such as Europe’s Digital Operational Resilience Act, that push banks to maintain on-premises disaster-recovery zones even as they leverage public-cloud elasticity for dev environments. Platform abstraction stitches together these disparate estates, presenting developers with a single API regardless of where workloads eventually land.

Vodafone’s validated OpenShift patterns exemplify how GitOps keeps edge clusters in sync with centralized control planes. On-prem deployments remain mandatory for air-gapped defense workloads, yet the arrival of sovereign cloud options from Oracle and others is eroding the case for purely local installations. As multi-cloud adoption climbs, platform blueprints must mask provider-specific primitives, a design shift that fuels hybrid growth and cements vendor-agnostic orchestration as table stakes.

By Organization Size: SMEs Narrow the Adoption Gap

Large enterprises accounted for 61.38% of 2025 revenue because they can underwrite dedicated teams and absorb six-figure capital outlays. This cohort also captures economies of scale by centralizing tooling across dozens of business units, amplifying return on platform spend. Nevertheless, small and medium-sized enterprises are set to grow at a 25.17% CAGR, closing the gap as SaaS offerings offer budget-friendly pricing. A platform engineering and internal developer platform (IDP) market size subscription of around USD 1,000 per month eliminates the need for headcount-heavy lifting.

The skills deficit remains the primary headwind for SMEs, with fewer than 15% of recent graduates mastering the blend of automation, API design, and product metrics required for platform roles. Vendors are responding by embedding AI-guided pipeline generation, such as Humanitec’s graph-based orchestrator, so that lean teams can bootstrap robust environments without deep Kubernetes fluency. Open-core models like Medplum’s download-first approach let firms validate workflows before committing budget, a pattern accelerating SME penetration.

By End-User Industry: Healthcare Outpaces Technology Incumbents

Technology and software firms retained 29.32% of revenue share in 2025 due to early DevOps maturity, but healthcare and life sciences are projected to outpace all verticals at a 26.57% CAGR. Clinical workloads need airtight audit trails and data residency, making platform abstraction critical for HIPAA compliance without throttling release velocity. Oracle’s Life Sciences AI Data Platform illustrates the thesis by processing 129 million electronic health records inside jurisdictional boundaries while still delivering AI-driven analytics.

Financial-services adoption rides similar compliance currents as Basel III capital rules and vendor-risk scrutiny nudge banks toward centrally governed templates. Telecommunications, targeting five-nines availability, leverage GitOps reconciliation to meet deterministic latency thresholds. Retail and e-commerce are scaling rapidly; Shopify’s platform supports 350 daily pull requests, a throughput impossible under legacy tooling. Manufacturing, energy, and government remain slower due to legacy gear and air-gapped constraints, but milestone certifications such as ISO 27001 and SOC 2 Type 2 earned by Software Defined Automation indicate rising industrial demand.

Geography Analysis

North America held 41.68% of 2025 revenue due to deep Kubernetes penetration and early formation of platform teams. Enterprises in the United States weave PCI-DSS 4.0 and SOC 2 Type 2 controls directly into golden paths, enabling developers to ship code without wrangling compliance minutiae. The region’s salary premium, 27% above DevOps baselines, creates talent gravity but also strains hiring pipelines, prompting firms to automate repetitive platform maintenance tasks. Canada and Mexico follow similar trajectories, modernizing pipelines to manage cross-border data flows governed by GDPR-inspired statutes.

Asia-Pacific is expanding at a 24.89% CAGR, fueled by sovereign-cloud mandates in India and China that make abstraction layers indispensable for multi-region workloads behind unified developer interfaces. The latest Cloud Native Computing Foundation pulse shows that 87% of regional enterprises are either implementing or planning platform programs, an indicator that the platform engineering and internal developer platform markets will post sustained double-digit growth. Japan and South Korea dominate mature adoption, while India’s technology-services giants embed internal platforms to standardize global client delivery. Talent shortages remain acute, so AI-guided platforms fill operational gaps.

Europe maintains a mid-tier share but is accelerating where the Digital Operational Resilience Act, the Network and Information Security Directive 2, and GDPR converge on software supply-chain assurance.[4]European Union, “Digital Operational Resilience Act,” EUROPA.EU The United Kingdom, Germany, and France channel spending into banking and telecom use cases that rely on platform-level policy codification. South America’s penetration is nascent; Brazil and Argentina are modernizing core banking, yet smaller IT ecosystems are curbing uptake. In the Middle East and Africa, the United Arab Emirates and Saudi Arabia anchor sovereign-cloud investments that require platform abstraction, whereas sub-Saharan Africa faces infrastructure gaps.

Competitive Landscape

The platform engineering and internal developer platform (IDP) market remains moderately fragmented, as the top five vendors accounted for less than 40% of 2025 revenue. Enterprises often weigh commercial products against building on open-source foundations such as Backstage, which alone claims 89% share in developer portals and a footprint across 3,400 organizations. Vendors are rapidly converging feature sets, bundling portals, CI/CD, observability, and policy enforcement to reduce integration overhead.

Humanitec’s AI-first Platform Orchestrator, released in September 2025, reduces pipeline authoring time and appeals to firms that lack the team size to curate bespoke platforms. HashiCorp’s pending acquisition by IBM, announced at USD 6.4 billion, signals consolidation as cloud giants seek turnkey platform portfolios. Smaller disruptors like Port and OpsLevel target mid-market buyers with monthly tiers below USD 1,000, while Harness injects AI agents to auto-remediate pipeline failures, trimming platform team toil. Telco-specific solutions, exemplified by Vodafone’s OpenShift deployment, show headroom for vertical platforms unaddressed by horizontal suites.

Pulumi’s March 2026 release of OPA-Rego support and Terraform state backend integration positions it as a bridge between infrastructure-as-code and policy-as-code in multi-cloud estates. Oracle, VMware, and Google Cloud augment core offerings with sovereign-cloud controls, seeking to capture regulated-industry workloads. With white-space still wide in government and energy segments, new entrants can differentiate on air-gapped deployment compatibility and legacy-system integration.

Platform Engineering And Internal Developer Platform (IDP) Industry Leaders

GitLab, Inc.

HashiCorp Inc.

CloudBees, Inc.

Harness, Inc.

Humanitec GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Spree Commerce rolled out version 5.2, featuring AI integrations for Cursor and Claude, a CLI installer, and code generators, embedding AI-assisted scaffolding into e-commerce workflows.

- March 2026: Pulumi released version 1.1.0 with Open Policy Agent and Rego support, plus Terraform state backend integration, streamlining policy-as-code and hybrid IaC governance.

- March 2026: Google Cloud introduced multi-networking APIs and persistent IP allocation in Google Kubernetes Engine, bringing telco-grade capabilities to managed Kubernetes.

- February 2026: Software Defined Automation achieved ISO 27001 certification, validating information-security controls for its industrial DevOps platform.

Global Platform Engineering And Internal Developer Platform (IDP) Market Report Scope

The Platform Engineering and Internal Developer Platform (IDP) Market refers to the ecosystem of tools, frameworks, and services that enable organizations to build, manage, and scale internal developer platforms to streamline software development and operations. These platforms provide standardized, self-service capabilities that abstract underlying infrastructure complexity, enhance developer productivity, and ensure consistency, security, and governance across the software delivery lifecycle.

The Platform Engineering and Internal Developer Platform Market Report is Segmented by Platform Component (Infrastructure Automation Layer, Developer Self-Service Portal, CI/CD Orchestration, Observability and Telemetry, and Governance and Security Controls), Deployment Mode (On-Premise, Cloud, Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-user Industry (Technology and Software, Financial Services, Telecommunications, Healthcare and Life Sciences, Retail and E-Commerce, Manufacturing, Energy and Utilities, Government and Public Sector, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Infrastructure Automation Layer |

| Developer Self-Service Portal |

| CI/CD Orchestration |

| Observability and Telemetry |

| Governance and Security Controls |

| On-Premise |

| Cloud |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises (SMEs) |

| Technology and Software |

| Financial Services |

| Telecommunications |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Manufacturing |

| Energy and Utilities |

| Government and Public Sector |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Platform Component | Infrastructure Automation Layer | ||

| Developer Self-Service Portal | |||

| CI/CD Orchestration | |||

| Observability and Telemetry | |||

| Governance and Security Controls | |||

| By Deployment Mode | On-Premise | ||

| Cloud | |||

| Hybrid | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium-Sized Enterprises (SMEs) | |||

| By End-user Industry | Technology and Software | ||

| Financial Services | |||

| Telecommunications | |||

| Healthcare and Life Sciences | |||

| Retail and E-Commerce | |||

| Manufacturing | |||

| Energy and Utilities | |||

| Government and Public Sector | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the platform engineering and internal developer platform market by 2031?

The market is forecast to reach USD 31.57 billion by 2031.

How fast is the market expected to grow during 2026-2031?

It is projected to register a 24.77% CAGR across the forecast span.

Which platform component currently leads spending?

Developer self-service portals led with 34.87% share in 2025.

Which region is forecast to grow the fastest?

Asia-Pacific is expected to expand at a 24.89% CAGR through 2031.

Why are hybrid deployments gaining momentum?

Data-residency mandates and multi-cloud strategies are driving hybrid architectures, which are projected to grow at 35.37% annually.

What talent challenges affect platform adoption?

A shortage of engineers skilled in infrastructure automation and product thinking is inflating salaries and slowing rollout, particularly for small and mid-sized enterprises.

Page last updated on: