Telco-as-a-Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.41 Billion |

| Market Size (2031) | USD 23.76 Billion |

| Growth Rate (2026 - 2031) | 13.87% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Telco-as-a-Platform Market Analysis by Mordor Intelligence

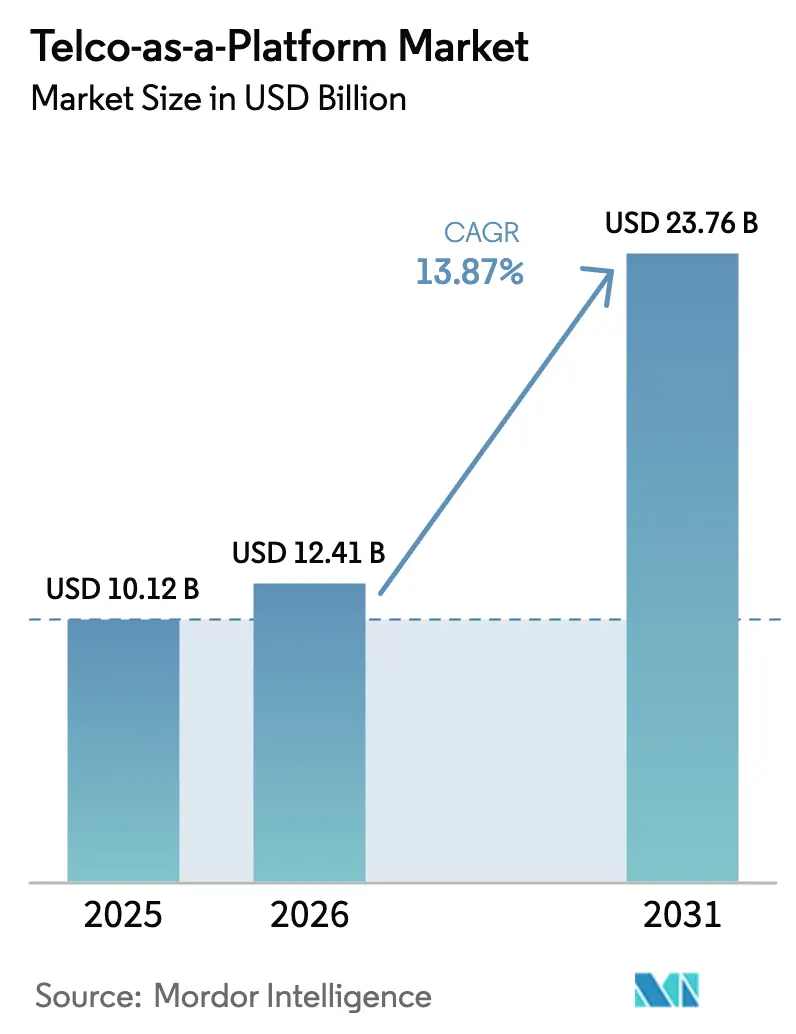

The Telco-as-a-Platform Market size is expected to grow from USD 10.12 billion in 2025 to USD 12.41 billion in 2026 and is forecast to reach USD 23.76 billion by 2031 at 13.87% CAGR over 2026-2031. The growing deployment of 5G standalone cores, the commercialization of multi-access edge computing, and the standardization of network exposure interfaces are accelerating the industry's pivot from pure connectivity to programmable platforms. Operators in North America, Europe, and Asia-Pacific now expose quality-on-demand, device-location, and SIM-swap detection capabilities through unified APIs, reducing integration costs for enterprises and software developers. Partnerships with hyperscalers place cloud compute inside radio sites, positioning telcos as edge-cloud orchestrators rather than bandwidth wholesalers. At the same time, data-sovereignty regulations in Europe, China, India, and the Gulf states require localized processing, creating demand for hybrid platform architectures that balance compliance with scalability. Competitive pressure intensifies as cloud providers, CPaaS specialists, and greenfield operators challenge legacy carriers that still rely on subscription-oriented BSS and OSS stacks.

Key Report Takeaways

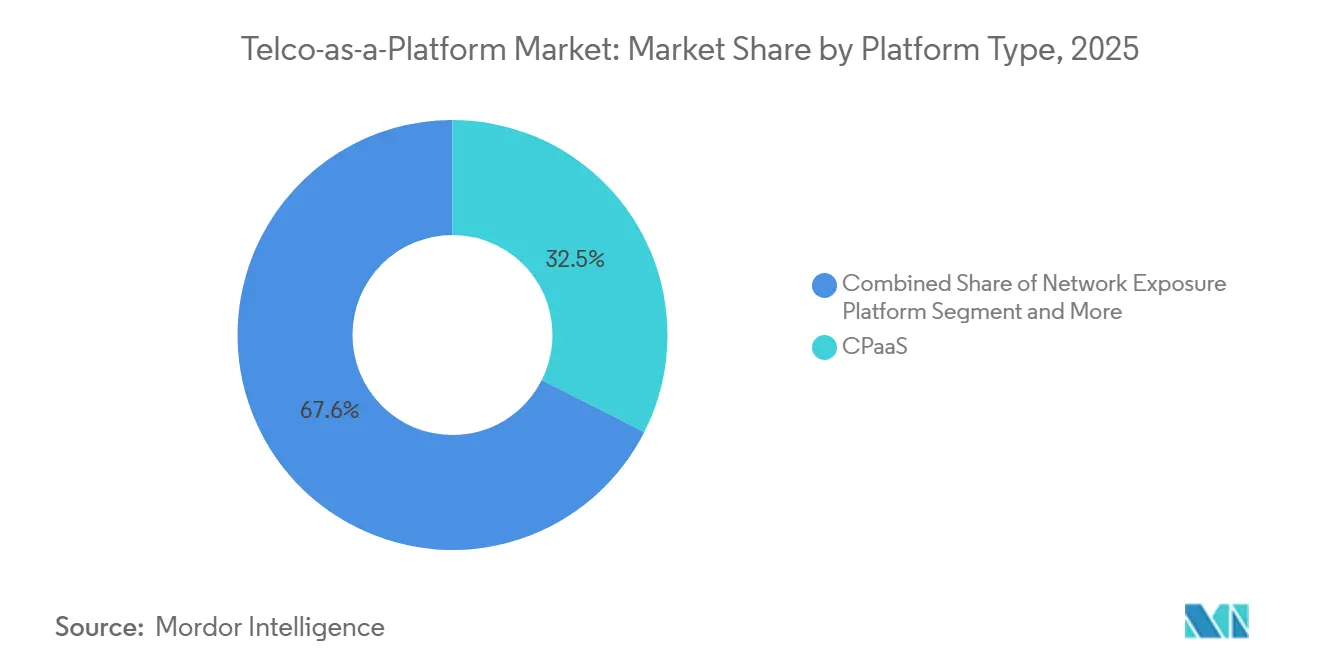

- By platform type, CPaaS commanded 32.45% of the Telco-as-a-Platform market share in 2025, while the edge cloud platform is advancing at a 15.12% CAGR through 2031.

- By deployment model, Public Cloud held 56.43% of the Telco-as-a-Platform market in 2025, and Hybrid Cloud is projected to grow at a 14.03% CAGR through 2031.

- By network technology, 4G/LTE held 34.67% of the Telco-as-a-Platform market in 2025, and NB-IoT and LPWAN are projected to grow at a 14.56% CAGR through 2031.

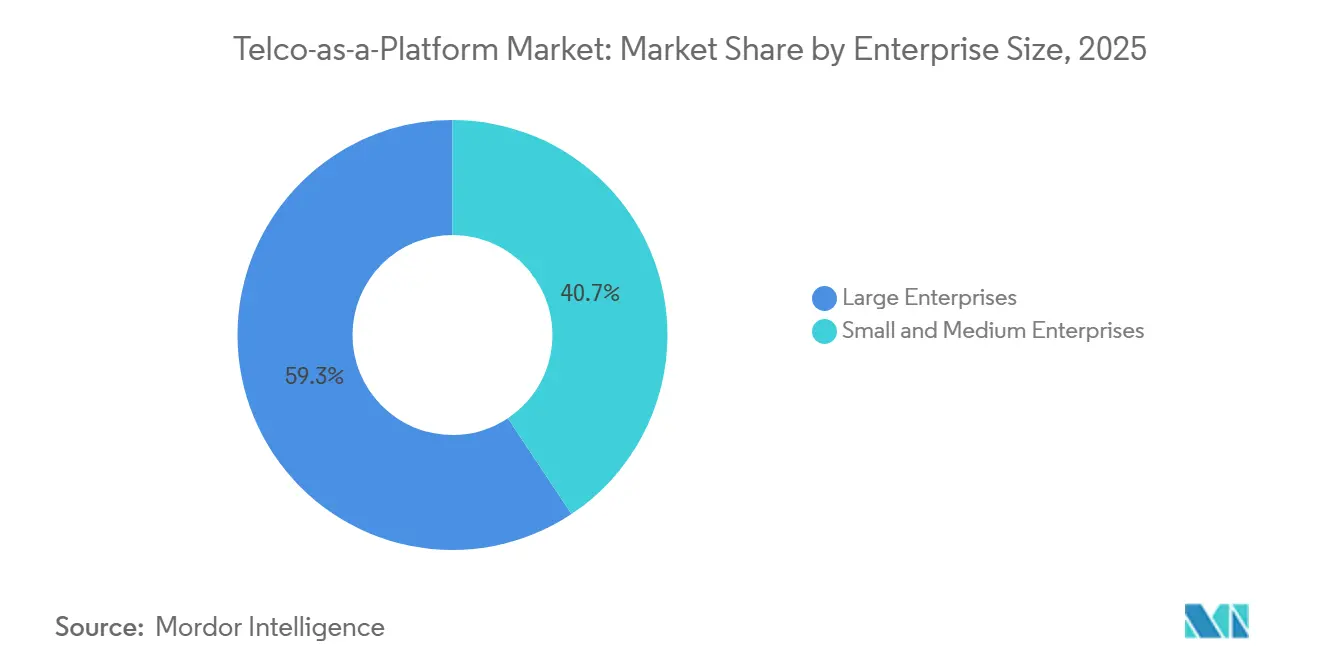

- By enterprise size, large enterprises led with a 59.34% revenue share in 2025, but SMEs recorded the fastest growth at a 13.91% CAGR through 2031.

- By end-user industry, healthcare posted the highest forecast growth, with a 15.06% CAGR to 2031, while BFSI maintained the largest market share at 24.56% in 2025.

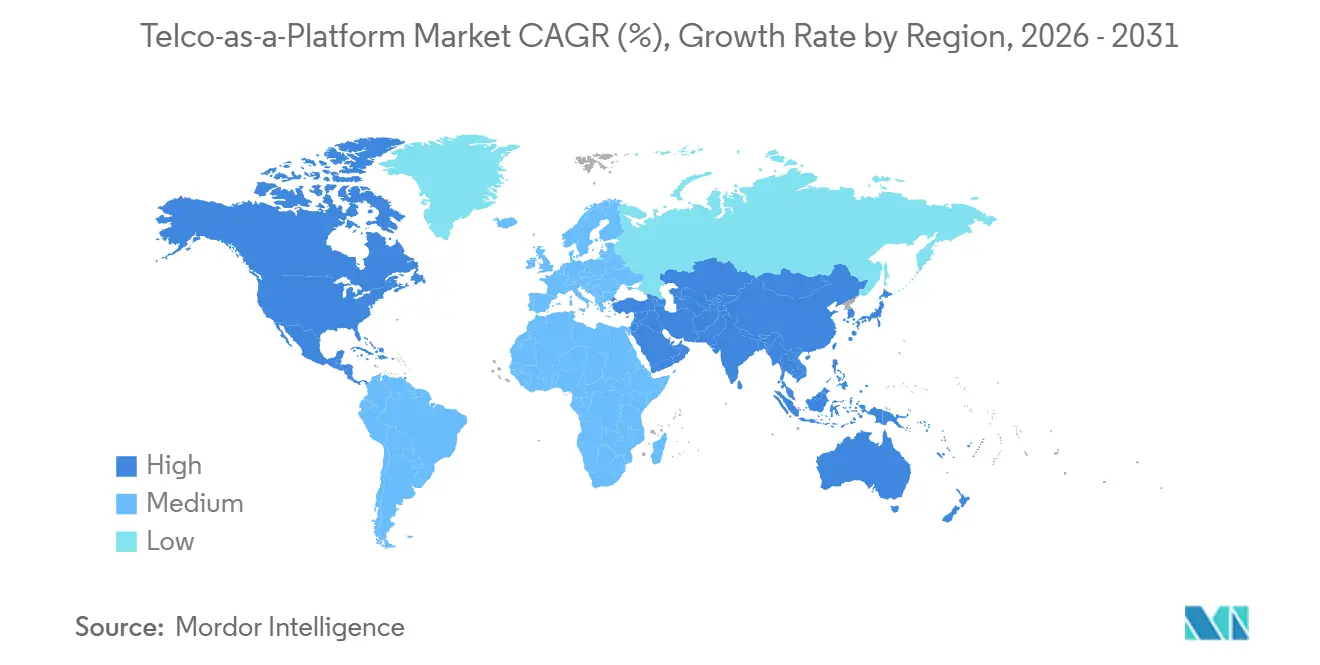

- By geography, North America held 28.54% of the Telco-as-a-Platform market in 2025, and the Asia-Pacific region is projected to grow at a 14.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Telco-as-a-Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of 5G Standalone Core Enabling Network Exposure | +2.8% | Global, led by China, South Korea, United States | Medium term (2-4 years) |

| Rising Enterprise Demand for Embedded Connectivity and API Access | +2.5% | North America and Europe, spreading to APAC and MEA | Short term (≤ 2 years) |

| Shift Toward Revenue Diversification Beyond Connectivity Services | +2.1% | Global in mature mobile markets | Long term (≥ 4 years) |

| MEC Adoption Driving Low-Latency Application Ecosystem | +1.9% | North America, Europe, APAC manufacturing hubs | Medium term (2-4 years) |

| Regulatory Push for Open Networks And Fair Access | +1.6% | Europe, India, select MEA markets | Long term (≥ 4 years) |

| Edge-Native AI Workloads Requiring Telecom-Grade Platforms | +1.8% | Global, concentrated in North America and China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of 5G Standalone Core Enabling Network Exposure

Standalone cores introduce Network Exposure Functions that allow third-party software to invoke quality-of-service tuning, location assurance, and session management through secure northbound APIs. China Mobile surpassed 1 million 5G SA radios by late 2025, and North American operators activated SA cores in major metros, making real-time network slicing commercially viable.[1]China Mobile, “5G Standalone Coverage Milestone,” chinamobileltd.com 3GPP Releases 16 and 17 defined the underlying interfaces, and the GSMA Open Gateway, along with the Linux Foundation CAMARA project, mapped them to a developer-friendly REST API, giving software teams a single call to request deterministic latency across multiple carriers.[2]Linux Foundation, “CAMARA Project Announcement,” linuxfoundation.org Operators now monetize differentiated bandwidth and latency tiers rather than flat connectivity, opening up recurring revenue streams as SA penetration scales toward a majority of global 5G lines before 2028.

Rising Enterprise Demand for Embedded Connectivity and API Access

Banks embed SIM-swap and number-verification calls to stop account-takeover fraud, while hospitals reserve network slices for remote diagnostics that cannot tolerate jitter exceeding 10 milliseconds. Manufacturers orchestrate robotics over private 5G combined with edge compute, using APIs to schedule bandwidth during shift changes. T-Mobile’s 2025 launch of T-Platform offered a self-service marketplace where logistics firms automatically provision slices and IoT connections, removing procurement cycles that once took weeks. Simplified pay-as-you-go models attract SMEs that lack telecom expertise, broadening the revenue pool beyond Fortune 500 multinationals.

Shift Toward Revenue Diversification Beyond Connectivity Services

Carrier average revenue per user continues to flatten in mature markets. Deutsche Telekom disclosed that platform income climbed to 8% of enterprise revenue in 2025 and set a 15% mix target for 2028. Vodafone monetizes device-location APIs across 21 European networks, while Orange collaborates with Microsoft Azure to sell edge analytics bundled with 5G connectivity. Although cultural gaps between software release cycles and telco change control remain, cloud-native billing and open-source developer portals are closing the execution gap.

MEC Adoption Driving Low-Latency Application Ecosystem

Multi-access edge computing moves compute and storage inside central offices or even base-station shelters, keeping round-trip transit under the 10 millisecond threshold required for haptics, machine vision, and real-time digital twins. Verizon 5G Edge integrates AWS Wavelength, and AT&T embeds Microsoft Azure in more than 100 metro rings, giving factories and hospitals the option to keep data on domestic soil while enjoying cloud elasticity. ETSI MEC Phase 4 standardized APIs for application discovery and traffic steering, enabling multinational firms to deploy the same container image on any compliant edge site.[3]ETSI, “MEC Phase 4 Specification,” etsi.org Joint-edge facilities among European operators further reduce capital intensity and accelerate coverage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy IT and BSS/OSS Constraints Hindering API Monetization | -1.4% | North America and Europe incumbents | Short term (≤ 2 years) |

| Fragmented Standards for Network Exposure APIs | -1.1% | Global with regional schema divergence | Medium term (2-4 years) |

| Security and Data Sovereignty Concerns Among Enterprises | -0.9% | Europe, China, India, Gulf markets | Long term (≥ 4 years) |

| Uncertain ROI for Telcos Investing in Platform Capabilities | -1.2% | Operators with high leverage worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy IT and BSS/OSS Constraints Hindering API Monetization

Monthly billing engines cannot meter per-second API calls or support dynamic pricing tied to latency classes. Oracle and Amdocs released cloud-native charging stacks, yet migrating millions of subscribers exposes carriers to churn risk and revenue assurance gaps. TM Forum’s Open Digital Architecture blueprint guides the rebuild, but only a small subset of operators moved beyond the pilot stage by 2025. Without real-time policy control, many carriers offer only blunt bundles, undermining differentiation from hyperscalers.

Fragmented Standards for Network-Exposure APIs

Although 67 operators signed on to GSMA Open Gateway and 40 others joined CAMARA, roll-out schedules differ by region, and national security mandates can force deviations. U.S. carriers converged on CAMARA schemas for number verification in 2025, while European counterparts stayed on an Open Gateway variant. China’s Ministry of Industry and Information Technology mandates separate endpoints for domestic users, increasing engineering overhead for global software vendors.[4]MIIT China, “Data Localization Regulations,” miit.gov.cn Enterprises must still build adapters for each carrier, delaying time-to-market and diluting the aggregated demand that would maximize network economics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform Type: Edge Cloud Platforms Outpace CPaaS as MEC Deployments Scale

CPaaS maintained a 32.45% share in 2025, led by messaging pioneers that abstract protocols into simple REST calls. Edge Cloud Platform now records the highest trajectory, with a 15.12% CAGR, as enterprises deploy microservices within radio sites to avoid backhaul. Verizon 5G Edge provides compute within 10 milliseconds of users across more than 50 U.S. metros, enabling factories to detect anomalies in real time. GSMA Open Gateway’s alignment of eight API families adds network exposure marketplaces that bond communications with compute.

The shift also reshapes revenue models. While CPaaS charges usage fees per message or per minute, edge platforms charge for CPU cycles, storage, and guaranteed bandwidth. The Telco-as-a-Platform market size for the Edge Cloud subsegment is projected to capture a larger share by the end of the forecast window, reflecting demand for in-situ analytics across autonomous vehicles, computer vision, and immersive media. BSS/OSS-as-a-Service solutions attract regional carriers that prefer to outsource charging and catalog functions rather than rebuild on premises, flattening the cost curve for entry.

By Deployment Model: Hybrid Configurations Gain as Data Sovereignty Mandates Tighten

Public cloud still accounted for 56.43% of 2025 revenue, but strict localization rules in the EU, China, and parts of the Middle East are driving hybrid architectures at a 14.03% CAGR. Deutsche Telekom and Google Cloud launched a Sovereign Cloud stack that stores keys and metadata only inside German borders, blending hyperscale innovation with regulatory assurance. Enterprises route latency-critical packets to edge locations while forwarding batch analytics to central regions, optimizing cost and compliance simultaneously.

Private deployments remain a niche confined to heavily regulated BFSI and healthcare domains. Yet even these verticals now rely on federated orchestration layers that unify policy across on-premise clusters and telco edges. The Digital Markets Act obliges dominant cloud providers to support interoperability, strengthening carrier bargaining power. In China and India, cybersecurity laws prohibit cross-border transfer of personal data, fueling domestic edge grids that interconnect with public clouds only through anonymized APIs.

By Network Technology: NB-IoT and LPWAN Surge as Massive IoT Use Cases Proliferate

4G/LTE provided 34.67% of 2025 traffic value, yet low-power wide-area networks will capture outsized future growth. China Mobile manages more than 200 million NB-IoT smart meters and environmental sensors, proving device density at a national scale. Vodafone’s pan-European NB-IoT footprint connects logistics pallets and municipal lighting in 21 countries.

5G SA underpins premium slices with guaranteed jitter and throughput, unlocking monetization of ultra-reliable low-latency telecom services. The Telco-as-a-Platform market share for 5G SA grows in lockstep with cloud-native core roll-outs by Verizon, NTT DOCOMO, and others. LPWAN technologies such as LoRaWAN complement licensed spectrum in rural and indoor locations but remain outside direct carrier control, limiting platform-based upsell opportunities. a

By Enterprise Size: SMEs Accelerate Adoption as API Access Simplifies

Large enterprises accounted for 59.34% of spending in 2025 due to their sizable IT budgets. Automotive and industrial groups procure private 5G networks from AT&T and Deutsche Telekom, pairing them with edge data lakes for machine learning. Yet SME uptake climbs at 13.91% CAGR as self-service portals and usage-based pricing remove integration friction. T-Mobile’s T-Platform lets a start-up provision a 10-megabit slice and an IoT SIM pool in minutes, paying only for usage rather than long-term contracts.

Infobip’s expansion into 70 countries offers localized onboarding for small retailers who want WhatsApp, SMS, and RCS campaigns through a single account. Cost remains a barrier where private cells and dedicated spectrum are required, so shared infrastructure models emerge, allowing multiple SMEs to colocate workloads on the same edge cluster and split fees.

By End-User Industry: Healthcare Leads Growth as Telemedicine and Remote Monitoring Expand

BFSI kept the largest 2025 slice at 24.56% because fraud mitigation delivers an immediate financial return. North American banks report double-digit declines in account-takeover losses after integrating SIM-swap detection APIs via GSMA Open Gateway. Healthcare climbs fastest at 15.06% CAGR as hospitals deploy 5G slices for imaging uploads, VR-assisted surgery, and continuous patient telemetry. Verizon demonstrated sub-10 millisecond round-trip latency for haptic feedback during remote surgical trials in Baltimore.

Manufacturing and Automotive verticals adopt deterministic connectivity for robotic motion control and vehicle-to-everything signaling. Energy utilities use NB-IoT for grid telemetry across remote substations, pushing tens of millions of messages per day through carrier platforms. Retail chains rely on CPaaS for omnichannel order confirmation, and media companies reserve network slices for 8K live streams at sporting venues.

Geography Analysis

North America accounted for 28.54% of 2025 revenue, underpinned by early 5G SA launches and cloud-edge partnerships. Verizon 5G Edge, coupled with AWS Wavelength, spans 75 metro zones, allowing e-commerce firms to run recommendation engines within ten milliseconds of customers, while AT&T Network Edge embeds Azure compute in more than 100 cities. T-Mobile’s marketplace accelerates SME adoption. Although the Federal Communications Commission encourages Open RAN diversity, divergent state privacy laws complicate multi-state deployments.

Asia-Pacific posts the highest forecast growth at 14.97% CAGR through 2031. China Mobile’s extensive SA footprint provides nationwide coverage for industrial parks, while Bharti Airtel’s marketplace makes number-verification and IoT connectivity accessible to India’s start-up ecosystem. NTT DOCOMO commercialized network slicing for autonomous vehicle trials, and Singtel, with AWS, positions Singapore as a hub for cross-border edge services. Regulatory climates vary, from China’s strict localization to Singapore’s open data corridors, shaping platform design and pricing.

Europe benefits from unified policies, such as the Digital Markets Act and the GDPR, that mandate open access and privacy compliance. Deutsche Telekom, Orange, and Telefónica pilot federated edges that share capex while meeting data-residency rules. Vodafone’s API marketplace spans 21 countries and monetizes fraud-prevention and IoT bundles. Middle East carriers leverage sovereign-cloud incentives to host government workloads in Saudi Arabia and the UAE, while African operators focus on smart-agriculture IoT as 4G coverage widens.

Competitive Landscape

Competition blends traditional operators, hyperscalers, and CPaaS vendors. Vodafone, Deutsche Telekom, and Orange extend network assets upstream into developer portals, yet must refactor BSS and OSS to enable real-time billing. AWS, Microsoft Azure, and Google Cloud insert compute inside radio huts without investing in spectrum, capturing edge application revenue through partnership agreements. CPaaS specialists Twilio, Vonage, and Infobip offer channel reach and developer ease but lack deterministic quality of service differentiation.

The GSMA Open Gateway commoditizes baseline APIs, pushing carriers to layer on value-added analytics and security. Linux Foundation CAMARA seeks to align schemas, though timelines vary. Greenfield entrants such as Rakuten Mobile in Japan or Dish Wireless in the United States operate cloud-native cores that skip legacy refits and deploy monetization catalogs within months, yet their smaller subscriber bases limit near-term scale.

Operators increasingly seek vertical specialization to escape horizontal price wars. Deutsche Telekom packages sovereign cloud and 5G for German auto makers. Orange markets medical-grade edge for French hospitals. Verizon and AWS co-develop computer-vision blueprints for logistics clients. Strategic stakes and joint ventures signal continuing convergence between telecom and cloud, with carriers providing local presence and telcos gaining software velocity.

Telco-as-a-Platform Industry Leaders

Vodafone Group Plc

Deutsche Telekom AG

Telefónica, S.A.

AT&T Inc.

Verizon Communications Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Bharti Airtel's digital unit, Xtelify, launched a cloud platform and AI-driven software solutions for businesses and telecom operators, alongside partnerships with Singtel, Globe Telecom, and Airtel Africa. Airtel Cloud offers infrastructure- and platform-as-a-service with secure migration and scalability. The AI-powered software for telecom operators includes a data engine, workforce tools, and customer engagement modules to enhance service and boost ARPU.

- April 2025: Deutsche Telekom and Google Cloud widened their Sovereign Cloud alliance to include edge compute nodes across Germany, France, and Spain.

Global Telco-as-a-Platform Market Report Scope

The Telco-as-a-Platform Market Report is Segmented by Platform Type (CPaaS, Network Exposure Platform, Edge Cloud Platform, BSS/OSS-as-a-Service, and Other Platform Types), Deployment Model (Public Cloud, Private Cloud, and Hybrid Cloud), Network Technology (4G/LTE, 5G Non-Standalone (NSA), 5G Stand-Alone (SA), and NB-IoT and LPWAN), Enterprise Size (Small and Medium Enterprises, Large Enterprises), End-User Industry (Manufacturing, Automotive, Media, Healthcare, Energy and Utilities, BFSI, Retail and E-commerce, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| CPaaS |

| Network Exposure Platform (API Marketplace) |

| Edge Cloud Platform |

| BSS/OSS-as-a-Service |

| Other Platform Types (IoT Connectivity Platform) |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| 4G/LTE |

| 5G Non-Standalone (NSA) |

| 5G Stand-Alone (SA) |

| NB-IoT and LPWAN |

| Small and Medium Enterprises |

| Large Enterprises |

| Manufacturing |

| Automotive and Transportation |

| Media and Entertainment |

| Healthcare |

| Energy and Utilities |

| BFSI |

| Retail and E-Commerce |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Platform Type | CPaaS | ||

| Network Exposure Platform (API Marketplace) | |||

| Edge Cloud Platform | |||

| BSS/OSS-as-a-Service | |||

| Other Platform Types (IoT Connectivity Platform) | |||

| By Deployment Model | Public Cloud | ||

| Private Cloud | |||

| Hybrid Cloud | |||

| By Network Technology | 4G/LTE | ||

| 5G Non-Standalone (NSA) | |||

| 5G Stand-Alone (SA) | |||

| NB-IoT and LPWAN | |||

| By Enterprise Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By End-User Industry | Manufacturing | ||

| Automotive and Transportation | |||

| Media and Entertainment | |||

| Healthcare | |||

| Energy and Utilities | |||

| BFSI | |||

| Retail and E-Commerce | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Telco-as-a-Platform market in 2026?

The Telco-as-a-Platform market size is expected to reach USD 12.41 billion in 2026, up from USD 10.12 billion in 2025.

What CAGR is forecast for Telco-as-a-Platform between 2026 and 2031?

The market is projected to grow at a 13.87% CAGR over the 2026-2031 period.

Which platform type is growing fastest?

Edge Cloud Platform leads growth with a projected 15.12% CAGR as enterprises deploy low-latency workloads at network edges.

Why are SMEs adopting telco platforms more rapidly now?

Self-service API portals and pay-as-you-go pricing lower technical and financial barriers, enabling SMEs to integrate telecom capabilities without specialist teams.

Which region is expected to post the highest growth?

Asia-Pacific is forecast to advance at a 14.97% CAGR through 2031, driven by extensive 5G SA roll-outs and government-backed digital initiatives.

What is the main restraint facing telcos in monetizing APIs?

Legacy BSS and OSS stacks cannot meter real-time API usage effectively, forcing expensive transformation projects that delay monetization.

Page last updated on: