Digital Twins In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

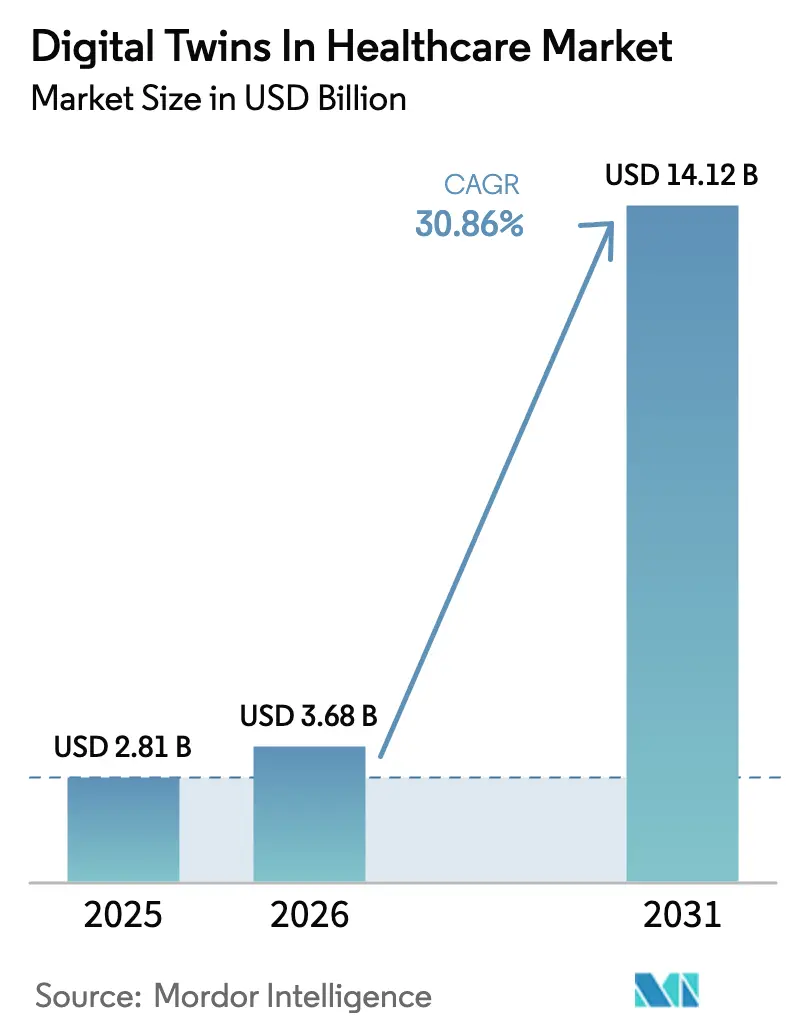

| Market Size (2026) | USD 3.68 Billion |

| Market Size (2031) | USD 14.12 Billion |

| Growth Rate (2026 - 2031) | 30.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Twins In Healthcare Market Analysis by Mordor Intelligence

The Digital Twins In Healthcare Market size was valued at USD 2.81 billion in 2025 and estimated to grow from USD 3.68 billion in 2026 to reach USD 14.12 billion by 2031, at a CAGR of 30.86% during the forecast period (2026-2031).

Continued convergence of AI, real-time analytics, and precision-medicine workflows is pushing hospitals, life-science companies, and technology vendors to accelerate adoption. Rapid venture funding, an evolving regulatory stance from the FDA, and strong demand for workflow optimisation have combined to propel the Digital Twins in Healthcare market toward double-digit annual growth. Meanwhile, cost pressures and workforce shortages in clinical settings are stimulating investments in virtual replicas that improve capacity management and reduce trial timelines. Heightened collaboration between cloud, semiconductor, and med-tech players further underpins the robust outlook for the Digital Twins in Healthcare market.

Key Report Takeaways

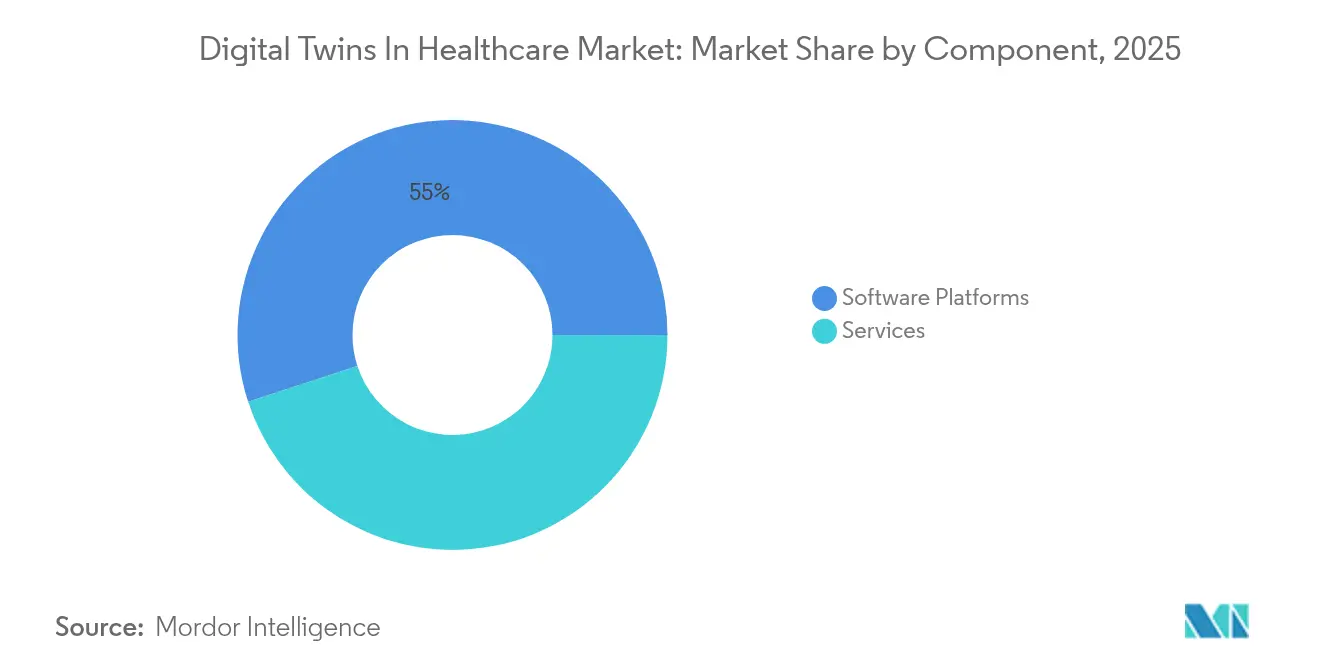

- By component, software platforms captured 55.02% of digital twins in healthcare market share in 2025, whereas patient digital twin analytics is projected to accelerate at a 35.2% CAGR through 2031.

- By application, drug discovery & pre-clinical modelling accounted for 26.58% share of the digital twins in healthcare market size in 2025, while personalized treatment optimisation is forecast to expand at a 37.23% CAGR to 2031.

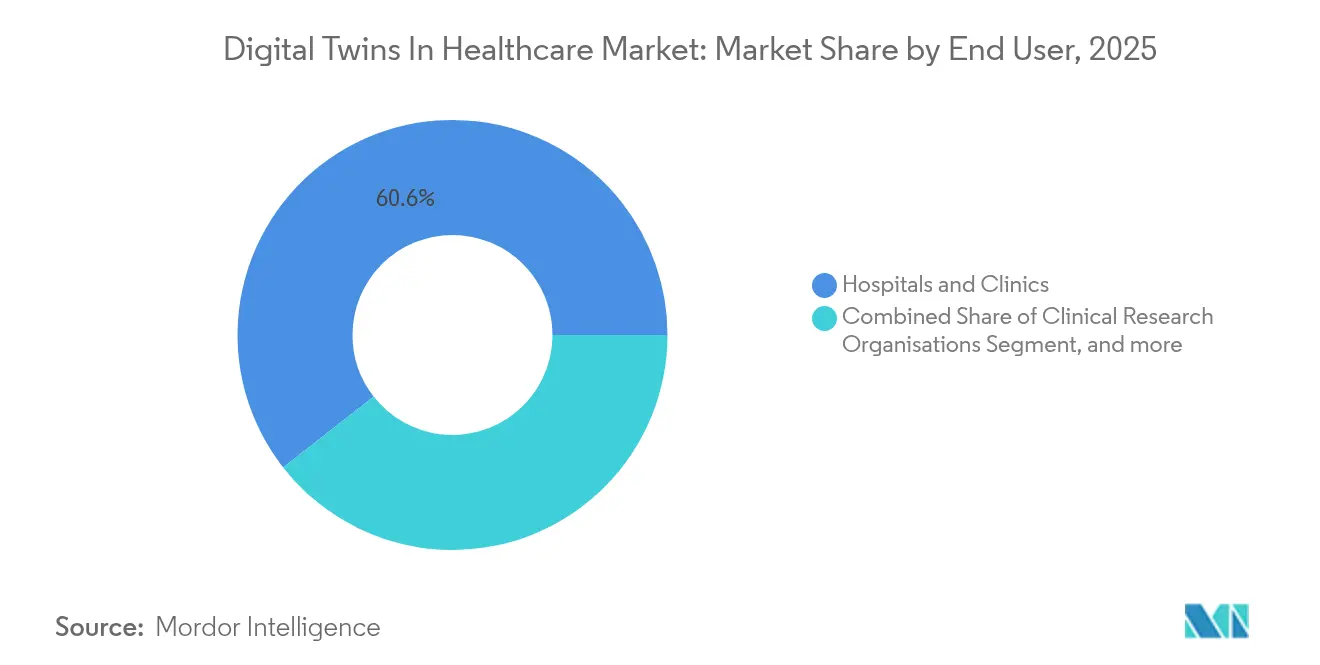

- By end user, hospitals & clinics led with 60.56% share in 2025; pharmaceutical & biotech companies show the fastest growth at 32.82% CAGR through 2031.

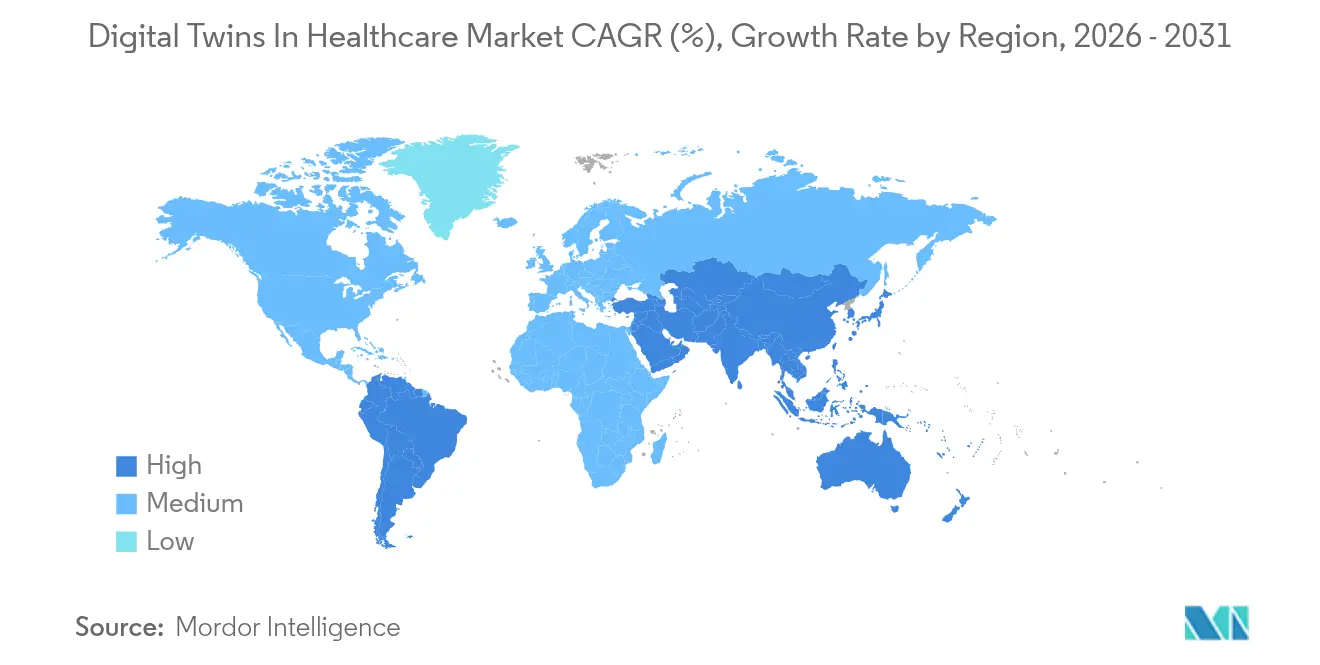

- By geography, North America dominated with 43.42% share in 2025, but Asia-Pacific is advancing at an identical 38.28% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Twins In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating R&D and Venture Funding for Precision-Medicine Twins | +8.5% | North America, EU | Medium term (2–4 years) |

| Advanced AI/ML Integration Elevating Model Fidelity | +7.2% | North America, expanding to APAC | Short term (≤ 2 years) |

| Adoption of Twins to Compress Drug-Discovery Timelines | +6.8% | North America, EU hubs | Medium term (2–4 years) |

| Hospital Demand for Workflow & Capacity Optimisation | +5.1% | Global | Short term (≤ 2 years) |

| Regulatory Pilots Approving Synthetic Control Arms | +3.9% | North America, EU | Long term (≥ 4 years) |

| Multi-Omics Data Unlocking Rare-Disease Patient Twins | +2.8% | Global research centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating R&D and Venture Funding for Precision-Medicine Twins

Global venture investment in digital-twin start-ups surged in 2024, highlighted by Unlearn AI’s USD 50 million Series C round that pushes its total funding above USD 130 million. Parallel momentum came from Twin Health’s USD 50 million infusion to scale its Whole Body Digital Twin platform, reinforcing investor conviction that personalised virtual replicas can cut the USD 100 billion annual clinical-trial bill. Large research programs, such as the Weizmann Institute’s Human Phenotype Project covering 30,000 participants, are enriching multi-omics datasets that improve model granularity. Pharmaceutical majors like Sanofi now simulate virtual patient populations pre-trial, enabling better candidate selection and smaller cohorts.[1]Sanofi, “How Digital Twins Accelerate Drug Discovery,” sanofi.com Collectively, deeper capital pools and pharma partnerships are amplifying development speed and clinical relevance of the Digital Twins in Healthcare market.

Advanced AI/ML Integration Elevating Model Fidelity

Generative AI and foundation models are sharpening prediction accuracy within the Digital Twins in Healthcare market. NVIDIA’s work with Novo Nordisk leverages the Gefion supercomputer to create real-time 3D twins that capture movement and vitals via standard cameras.[2]NVIDIA, “Gefion Supercomputer Powers 3D Digital Twins,” nvidia.com Ansys and NVIDIA Omniverse link numerical solvers to photorealistic renderers, helping surgeons visualise patient-specific anatomies for risk-free rehearsal. Large pathology foundation model Virchow, trained on 1.5 million slide images, posts an AUC of 0.9 across 17 cancer types, underscoring how high-parameter networks raise diagnostic confidence. Multimodal AI now blends genomics, imaging, and wearable feeds into unified representations, widening the scope for predictive dosing and longitudinal disease tracking. Regulatory signals, exemplified by the FDA’s draft guidance on model credibility, are creating safer pathways for AI-rich digital twins in clinical submissions.[3]FDA, “Proposed Framework on Credibility of AI Models,” fda.gov

Adoption of Twins to Compress Drug-Discovery Timelines

Digital twins can slice clinical-trial duration by as much as 50%, trimming burn rates for experimental therapies. CRO tie-ups like Charles River and Aitia use synthetic cohorts to downgrade animal testing and pinpoint promising compounds earlier. Pharmaceutical process twins promise 70% lower cost-of-goods and USD 1.25 billion annual savings per blockbuster by marrying mechanistic process models with machine-learning feedback loops. Qureight’s synthetic control arms lessen ethical hurdles in orphan-disease trials. Endorsements from EMA and FDA further legitimise the Digital Twins in Healthcare market for time-compression use cases.

Hospital Demand for Workflow & Capacity Optimisation

Healthcare systems face budget strain and staff shortages; 66% of executives plan higher digital-twin spending by 2027. At Coventry & Warwickshire NHS Trust, IBM watsonx.ai cut missed appointments to 4% and freed capacity for 700 extra weekly visits. Guthrie Clinic’s virtual-care hub saved USD 7 million in labour and reduced nurse turnover to 13%. Pathology-lab twins reduce label errors 90% and shorten turnaround up to 50%, though implementations cost USD 100,000-200,000. Command-centre solutions at Tampa General and Johns Hopkins removed USD 40 million in excess patient days via predictive bed management. Operating-room twins now optimise workflow while preserving data privacy across institutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation Cost & Complex Data Management | -4.2% | Global, higher in emerging markets | Short term (≤ 2 years) |

| Stringent Privacy & Cyber-Security Requirements | -3.8% | Global, stricter in EU | Medium term (2–4 years) |

| Algorithmic Bias from Limited Physiological Diversity | -2.9% | Under-represented populations | Long term (≥ 4 years) |

| Fragmented Interoperability Standards Across Platforms | -2.1% | Global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Implementation Cost & Complex Data Management

Initial outlays of USD 100,000-200,000 for lab-scale twins deter small providers. Ongoing expenses stem from integrating EHR, imaging, and sensor feeds into cleansed, interoperable lakes many hospitals lack. Although 86% of executives expect lower operating costs from digital health, 70% report delayed ROI because metrics remain hard to track. Standardising vocabularies and governance adds complexity and staffing costs. Limited budgets in emerging markets widen the adoption gap, slowing global scale-up of the Digital Twins in Healthcare market.

Stringent Privacy & Cyber-Security Requirements

IoT endpoints feeding twins create new attack surfaces, increasing exposure of protected health information. Compliance with HIPAA and GDPR forces encryption, redundancy, and audit frameworks that lengthen project timelines. Continuous monitoring and asset-management raise total cost of ownership, especially when legacy clinical systems and modern twins coexist. Bias risk in homogenous datasets necessitates diversity audits and model recalibration. Consent management around streaming wearables poses additional ethical hurdles. These hurdles cap near-term penetration despite technological readiness of the digital twins in healthcare market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Platforms Drive Innovation

Software platforms held 55.02% of digital twins in healthcare market share in 2025, underscoring provider preference for end-to-end suites that slot into electronic medical-record stacks. Rising demand for no-code model authoring, cloud deployment, and embedded analytics guides vendor roadmaps. Managed-service contracts bundle integration and validation, helping mid-size hospitals adopt without deep in-house data-science talent. Patient Digital Twin Analytics is projected to grow at 35.2% CAGR, propelled by value-based-care incentives that reward fine-grained risk prediction.

Growth momentum is now tied to AI-enhanced physics models that forecast individual responses. Twin Health reports a 73% drop in insulin use and 2.2-point A1C reduction among type 2 diabetics enrolled on its metabolic twin program. Cloud providers embed pretrained models so clinicians can configure digital twins via dashboards rather than coding, lowering adoption barriers. Interoperability efforts such as Siemens–Microsoft Digital Twin Definition Language harmonisation promise easier data exchange. As validation cycles shorten, the Digital Twins in Healthcare market envisions continuous-update pipelines where algorithm tweaks roll safely into production.

By Application: Personalized Treatment Leads Growth

Drug discovery & pre-clinical modelling captured 26.58% of digital twins in healthcare market size in 2025, reflecting entrenched usage in virtual screening and synthetic control arms. Nevertheless, Personalized Treatment Optimisation will register a 37.23% CAGR, mirroring the shift toward patient-centric care pathways. Clinical-trial virtualisation also rides regulatory openness; Unlearn AI uses digital twins to cut enrollment by one-third while maintaining statistical power.

Surgical-planning solutions integrate VR with patient-specific hemodynamic twins, boosting stent-placement accuracy. Chronic-disease modules combine wearables and lab panels to predict trajectories for heart failure, COPD, and diabetes, enabling earlier interventions. Hospital workflow twins now deliver 45% shorter documentation cycles and near-real-time bed-assignment insights. Rare-disease researchers leverage multi-omics twins to simulate trial endpoints despite sparse populations. Collectively, therapeutic and operational scenarios are converging, widening the addressable digital twins in healthcare market.

By End User: Pharmaceutical Companies Accelerate Adoption

Hospitals & clinics controlled 60.56% of digital twins in healthcare market share in 2025, reflecting urgent needs to manage throughput and staffing. Yet Pharmaceutical & Biotech Companies will expand at 32.82% CAGR, incentivised by cost-savings from in-silico cohorts and faster regulatory review. CROs embed twin analytics to refine recruitment and retention, reshaping fee models.

Research & diagnostics laboratories deploy slide-scanning twins that reduce mis-label rates by 90%. Med-tech manufacturers use device twins to streamline design-freeze milestones and compile regulatory evidence, a trend McKinsey sees widening across orthopaedics and cardiology. Payers experiment with whole-population twins to stratify premiums and guide benefit design. Ecosystem convergence is reshaping partnership structures, anchoring the digital twins in healthcare market in multi-stakeholder collaboration.

Geography Analysis

North America generated 43.42% of Digital Twins in Healthcare market revenue in 2025 amid ample venture capital, mature cloud penetration, and FDA clarity. High-profile collaborations such as GE HealthCare and NVIDIA’s autonomous imaging pilots—help mainstream the concept.

Asia-Pacific is forecast to deliver 38.28% CAGR through 2031, powered by national AI strategies, hospital-digitalisation grants, and rising chronic-disease burdens. Japan pioneers emotion-aware digital-twin computing via NTT research, while China scales AI hospitals that plug real-world evidence into therapy selection. India’s Ayushman Bharat Digital Mission is laying data rails that favour twin-ready architectures.

Europe benefits from cross-border R&D consortia and supportive data-governance directives. Interoperability initiatives like Siemens–Microsoft strengthen the Digital Twins in Healthcare market by aligning standards. Emerging regions in the Middle East, Africa, and South America invest in diagnostics automation and tele-ICU projects, opening greenfield demand for asset twins that optimise scarce specialist resources.

Competitive Landscape

Competition remains moderate as cloud hyperscalers, industrial-software vendors, life-science majors, and AI start-ups stake positional claims. Incumbents Siemens Healthineers, GE HealthCare, and Philips weave twin modules into imaging scanners and monitoring suites, seeking locked-in upgrade cycles. Meanwhile, pure-plays such as Unlearn AI focus on synthetic control arms and secure validation from both EMA and FDA, positioning for premium SaaS contracts.

Partnership networks constitute the dominant entry strategy. NVIDIA pairs its GPU clusters and Omniverse toolkit with GE HealthCare, Novo Nordisk, and a host of mid-size software firms to widen distribution. Disruptors Qureight, PrediSurge, and Somite target niche therapeutic gaps rare-lung disease, robotic-surgery rehearsal, and tissue-engineering twins respectively where incumbents lack domain depth.

Interoperability, explainability, and cyber-resilience now separate leaders from fast followers. Vendors demonstrating transparent model pipelines gain trust from clinicians and regulators. As funding consolidates around firms with proven ROI, the Digital Twins in Healthcare market is expected to progress toward balanced oligopoly rather than winner-take-all domination.

Digital Twins In Healthcare Industry Leaders

Atos SE

Microsoft

Koninklijke Philips N.V.

Unlearn AI

Twin Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: NVIDIA partnered with Novo Nordisk and DCAI to advance drug discovery through AI technologies, utilizing the Gefion supercomputer to create customized AI models for early research and clinical development, with startup Teton developing AI care companions using real-time 3D digital twins for patient monitoring.

- January 2025: NVIDIA expanded Omniverse platform with generative AI models and blueprints for physical AI applications, including robotic digital twin blueprints adaptable for healthcare applications and industrial AI optimization

- May 2024: Twin Health, a healthcare technology company, launched its whole body digital twin AI platform to reduce reliance on GLP-1s and other costly health interventions for the treatment of type 2 diabetes and obesity.

- May 2024: Ontrak Inc., an AI-powered and technology-enabled healthcare company, reported the launch of its pioneering Mental Health Digital Twin (MHDT) technology. This digital twin technology is used to provide personalized, precise, and effective care for individuals struggling with mental health challenges.

Global Digital Twins In Healthcare Market Report Scope

As per the scope of the report, healthcare digital twins are described as virtual representations of patients that are created from multimodal patient data, population data, and real-time updates on patient and environmental variables.

The digital twins in the healthcare market are segmented into product, component, application, end-user, and geography. By component, the market is segmented into software and services. By application, the market is segmented into personalized medicine, drug discovery, medical education, and workflow optimization. By end-user, the market is segmented into hospitals and clinics, clinical research organizations, research and diagnostics laboratories, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for the above segments.

| Software Platforms | Asset-centric Modelling Suites |

| Patient Digital Twin Analytics | |

| Services | Implementation & Integration |

| Training & Support | |

| Managed Services |

| Drug Discovery & Pre-clinical Modelling |

| Clinical Trial Virtualisation |

| Surgical Planning & Simulation |

| Personalized Treatment Optimisation |

| Chronic Disease Management |

| Hospital & Asset Workflow Optimisation |

| Hospitals & Clinics |

| Clinical Research Organisations |

| Research & Diagnostics Laboratories |

| Pharmaceutical & Biotech Companies |

| Medical-Device Manufacturers |

| Payers & Health-Tech Firms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software Platforms | Asset-centric Modelling Suites |

| Patient Digital Twin Analytics | ||

| Services | Implementation & Integration | |

| Training & Support | ||

| Managed Services | ||

| By Application | Drug Discovery & Pre-clinical Modelling | |

| Clinical Trial Virtualisation | ||

| Surgical Planning & Simulation | ||

| Personalized Treatment Optimisation | ||

| Chronic Disease Management | ||

| Hospital & Asset Workflow Optimisation | ||

| By End User | Hospitals & Clinics | |

| Clinical Research Organisations | ||

| Research & Diagnostics Laboratories | ||

| Pharmaceutical & Biotech Companies | ||

| Medical-Device Manufacturers | ||

| Payers & Health-Tech Firms | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the digital twins in healthcare market?

The market is valued at USD 3.68 billion in 2026, with a forecast to hit USD 14.12 billion by 2031 at a 30.86% CAGR.

Which component leads the digital twins in healthcare market?

Software platforms dominate with 55.02% share as of 2025, reflecting provider demand for turnkey solutions.

Which application segment is growing fastest?

Personalized treatment optimisation is advancing at a 37.23% CAGR, driven by precision-medicine initiatives.

Which region shows the highest growth rate?

Asia-Pacific posts the fastest growth, matching a 38.28% CAGR through 2031 as healthcare digitisation accelerates.

What are the principal restraints hindering adoption?

High upfront costs, complex data integration, and stringent privacy regulations collectively exert downward pressure on near-term uptake.

How are digital twins shortening drug-development timelines?

Synthetic control arms and predictive twins can cut trial enrollment and duration by up to 50%, delivering significant cost savings to pharma sponsors.

Page last updated on: