Digital Polymerase Chain Reaction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.93 Billion |

| Market Size (2031) | USD 1.86 Billion |

| Growth Rate (2026 - 2031) | 14.78% CAGR |

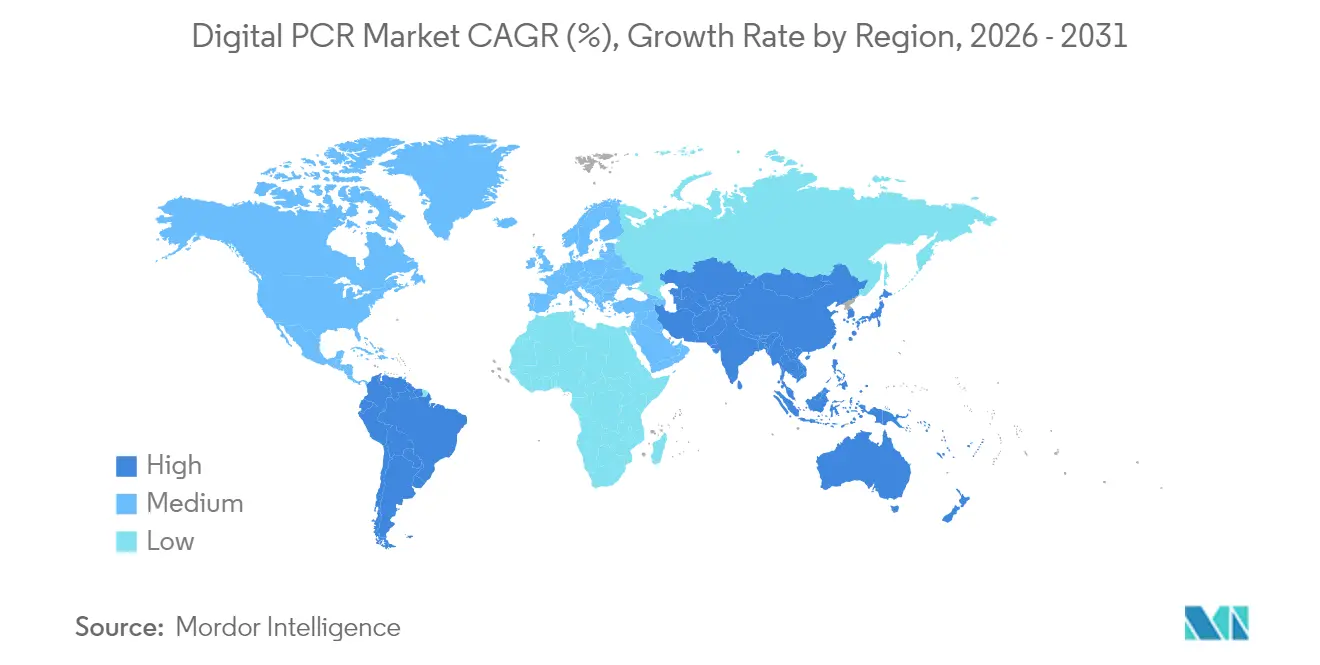

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

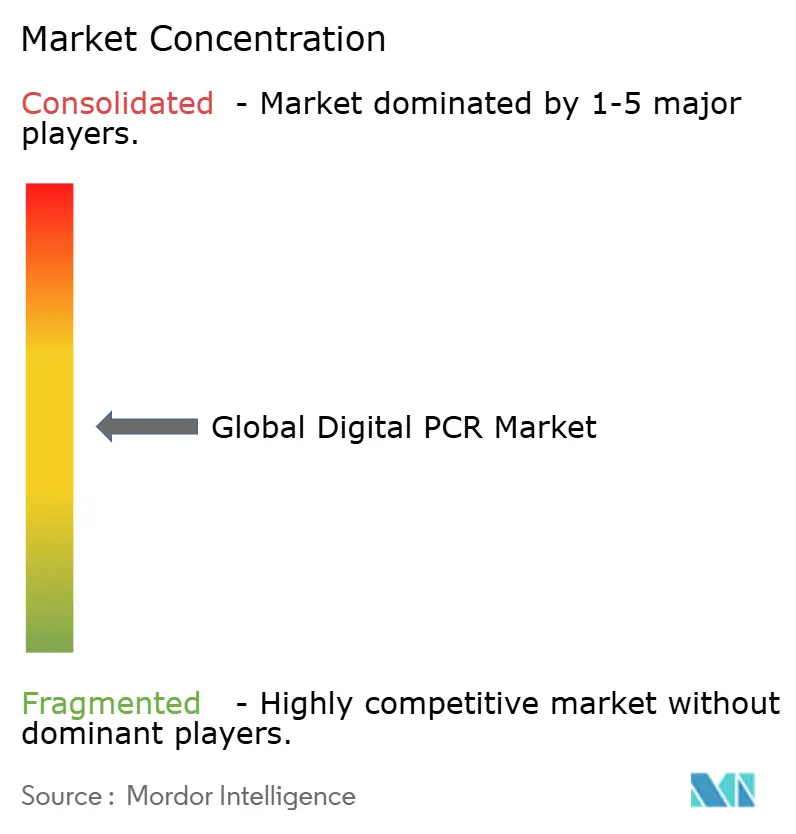

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Polymerase Chain Reaction Market Analysis by Mordor Intelligence

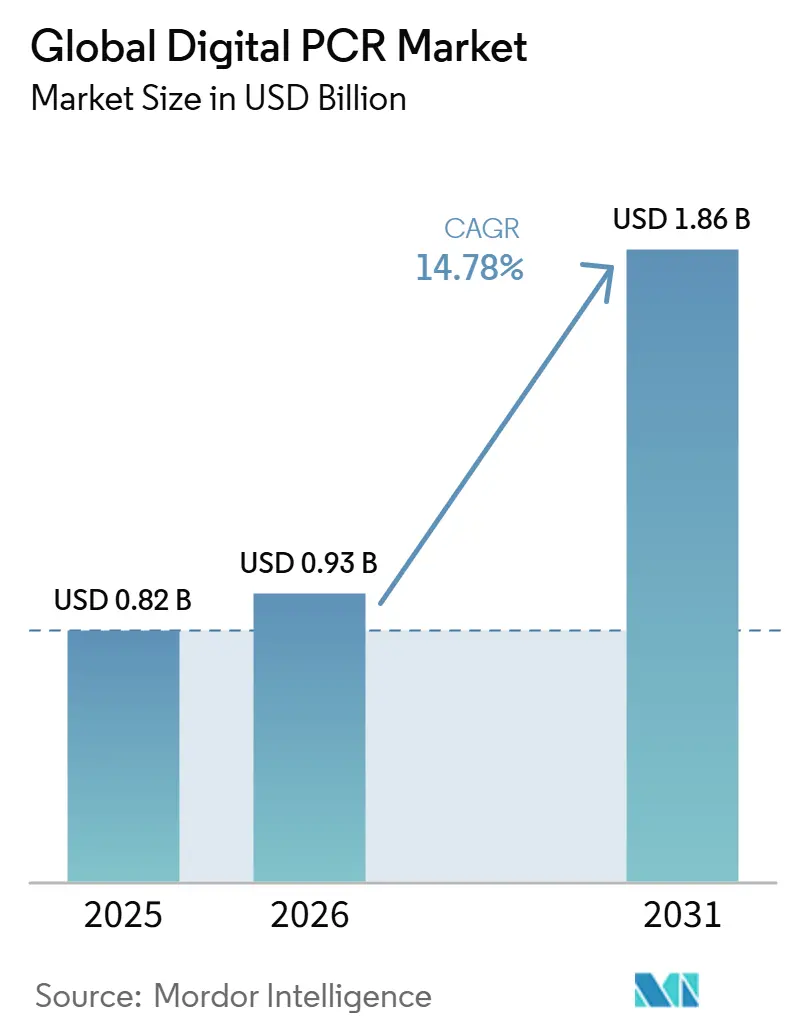

The Global Digital PCR Market size is expected to grow from USD 0.82 billion in 2025 to USD 0.93 billion in 2026 and is forecast to reach USD 1.86 billion by 2031 at 14.78% CAGR over 2026-2031.

A series of macro-level forces underpin this expansion. First, precision‐oncology programs now pair liquid-biopsy strategies with absolute quantification assays, enabling variant-allele detection down to 0.01% and producing clinical evidence that persuades payers to maintain coverage under U.S. MolDX and parallel EU frameworks. Second, antimicrobial-resistance (AMR) surveillance projects in national wastewater networks and hospital infection-control units rely on digital PCR to quantify pathogen load with reaction counts that exceed 5,000 per chip, creating recurring demand for high-throughput reagent kits. Third, Benchtop instruments now achieve ±0.1 °C thermal accuracy with milliliter-level sample requirements, a specification that allows decentralized laboratories to adopt molecular tests previously reserved for core facilities. Lastly, FDA accelerated-approval pathways for companion diagnostics, combined with biopharma investments in cell- and gene-therapy potency testing, create a predictable regulatory and commercial environment that accelerates capital flows into instrument, reagent and software upgrades.

Key Report Takeaways

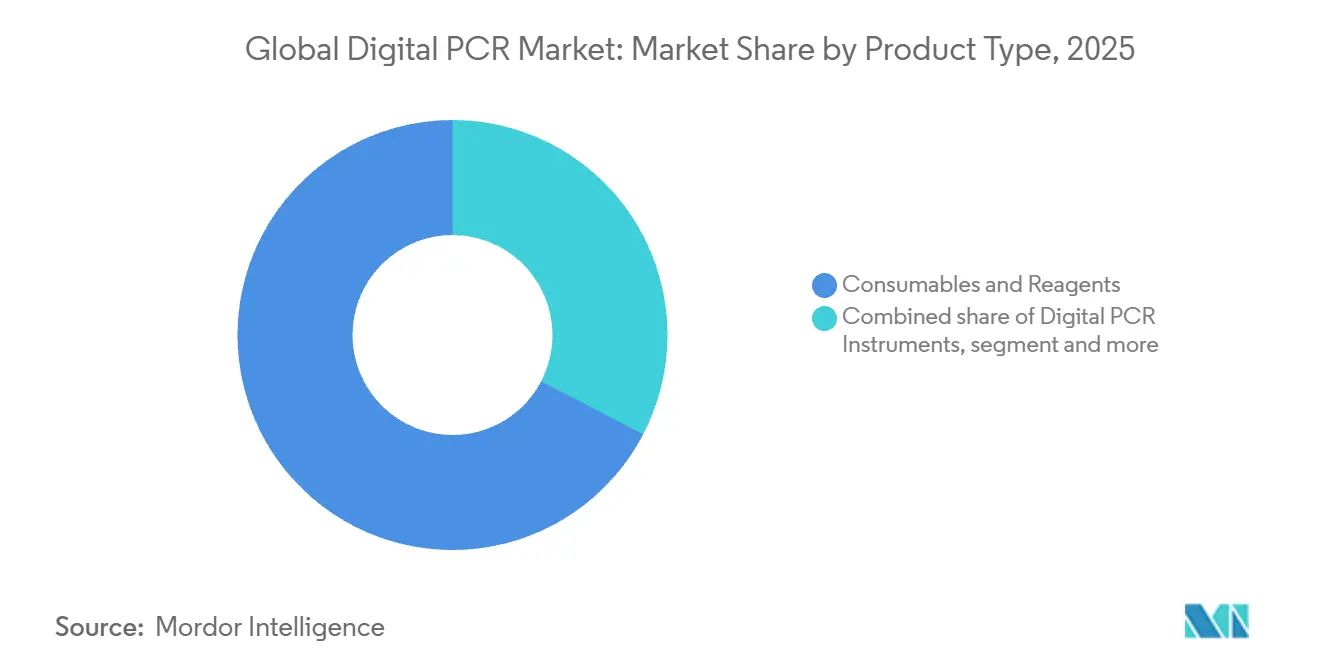

- By component, Consumables & Reagents held 67.35% of the digital PCR market share in 2025, while Software & Services is expanding at a 14.14% CAGR to 2031.

- By technology, droplet systems controlled 64.78% revenue share in 2025; microfluidic platforms are projected to advance at a 15.50% CAGR through 2031.

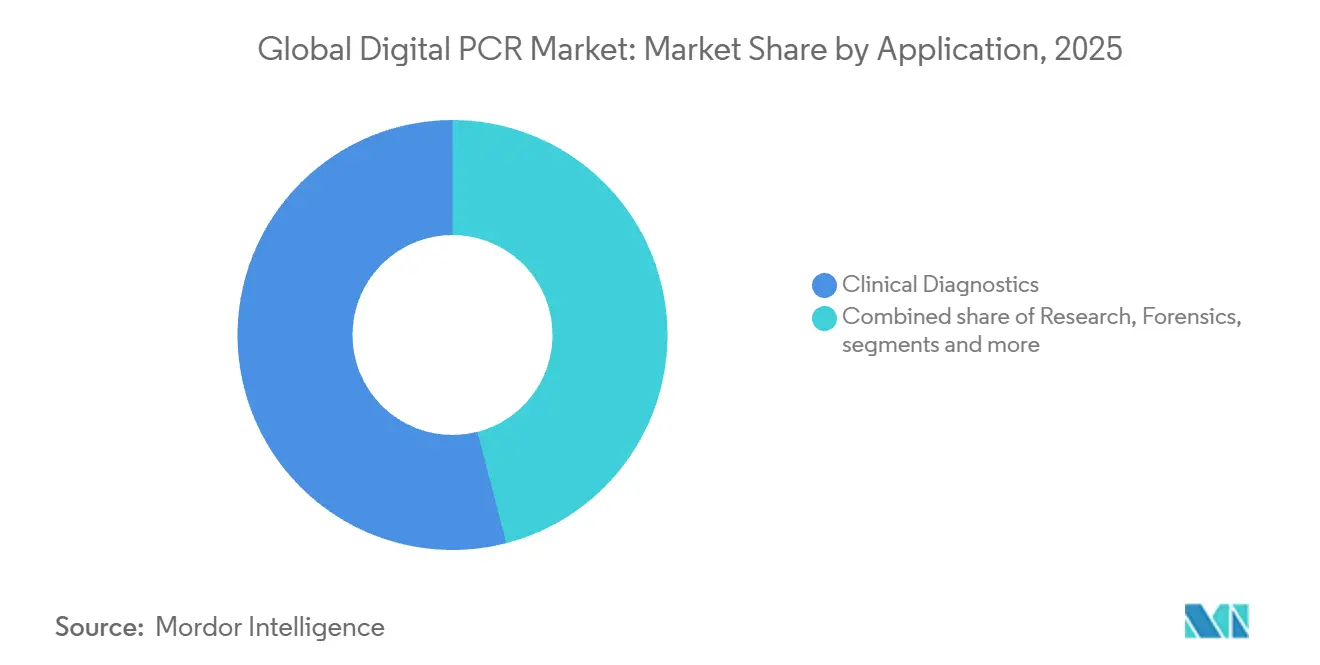

- By application, clinical diagnostics accounted for a 54.02% share of the digital PCR market size in 2025 and continues to grow on the back of liquid-biopsy adoption.

- By end user, hospitals and clinical laboratories commanded 41.69% of the digital PCR market size in 2025, whereas pharma and biotech companies will post an 16.04% CAGR to 2031.

- By geography, North America represented 40.85% of the digital PCR market share in 2025; Asia-Pacific exhibits the highest regional CAGR at 16.18% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Polymerase Chain Reaction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision oncology push for liquid-biopsy-ready assays | +2.1% | Global, early adoption in North America & EU | Medium term (2-4 years) |

| Growing global AMR surveillance programs | +1.8% | Global, strong in APAC & emerging markets | Long term (≥4 years) |

| Decentralization of molecular testing via benchtop dPCR | +1.2% | North America & EU, extending to APAC | Short term (≤2 years) |

| Mainstream reimbursement approvals | +1.5% | Primarily North America & EU | Medium term (2-4 years) |

| Biopharma shift to cell & gene therapy potency tests | +2.3% | Global, concentrated biopharma hubs | Long term (≥4 years) |

| Expansion of wastewater-based epidemiology | +1.4% | Global, focus on large urban centers | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Precision Oncology Push for Liquid Biopsy-Ready Assays

Digital PCR platforms now detect circulating-tumor DNA at clinically actionable levels, enabling oncologists to monitor metastatic disease in real time without invasive tissue sampling. Multicenter European standardization covering 93 institutions confirms that assay protocols are mature enough for routine adoption. Research from MIT indicates that primer-based enrichment can further amplify ctDNA signals by 60-fold, reducing false-negative rates and widening the eligible patient base for liquid biopsy monitoring. Together, these gains shift digital PCR from an exploratory research tool toward a reimbursable frontline diagnostic in precision oncology.

Growing Global AMR Surveillance Programs Using Absolute Quantification

National public-health agencies integrate digital PCR into wastewater-testing grids because the technology quantifies resistant organisms even in heavily diluted environmental matrices. European consortia now require dual testing pipelines that pair digital PCR with whole-genome sequencing, ensuring rapid quantification followed by detailed resistance profiling. Australian and New Zealand laboratories reported higher inter-laboratory comparability once standardized digital PCR protocols replaced lab-developed qPCR methods. As urban wastewater programs expand, demand rises for reagent cartridges that maintain analytical consistency across thousands of daily samples.

Decentralization of Molecular Testing Through Compact Benchtop dPCR

Portable platforms achieve heating rates of 8 °C/s and cooling rates of −9.3 °C/s, supporting 40-cycle assay runs in under 35 minutes. Workflow automation reduces sample-prep time from hours to minutes, enabling general hospitals and even outpatient clinics to operate oncology or infection-control assays that once required central reference labs. Artificial-intelligence optimization adjusts thermal profiles on the fly, eliminating manual parameter tuning and supporting novice users. Manufacturers such as QIAGEN plan to release low-throughput instruments that integrate sample prep, amplification and analysis into a single footprint to broaden market reach.

Mainstream Reimbursement Approvals in US and EU

Medicare’s MolDX framework now lists analytical validation tiers that digital PCR assays meet with less complexity than NGS tests, improving time-to-coverage for new oncology applications. In parallel, the EU IVDR introduced in 2024 harmonizes performance-evaluation requirements, allowing a single dossier to unlock access across 27 member states. Local Coverage Determinations that fund minimal-residual-disease assays in colorectal cancer validate the pay-for-performance model and encourage additional submissions using digital PCR backbones. State biomarker-mandate bills across 15 U.S. jurisdictions compound payer pressure by legally obligating coverage of clinically useful molecular tests.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & per-sample reagent costs | -2.8% | Global, strongest in emerging markets | Short term (≤2 years) |

| Throughput limitations versus qPCR & NGS | -1.5% | Global, large-scale screening programs | Medium term (2-4 years) |

| Scarcity of regulatory-cleared IVD test menus beyond oncology | -1.2% | North America & EU | Long term (≥4 years) |

| IP fragmentation slowing cross-platform kit compatibility | -0.9% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Per-Sample Reagent Costs

Instrument entry prices start around USD 38,000 and escalate when annual maintenance, proprietary consumables and specialized staff training are included. Even though new reagent bundles consolidate up to five assays into one run and cut costs by 43%[1]MilliporeSigma, “Aptegra Genetic Stability Platform Cuts Costs by 43%,” sigmaaldrich.com, the total per-test expense still exceeds high-throughput qPCR by 2-3 times in community hospitals. Start-ups often raise nine-figure venture rounds to cover the long R&D cycle needed to reach cost parity, underlining the capital intensity that limits rapid geographic expansion. Emerging-market budgets therefore prioritize multipurpose hematology or chemistry analyzers unless vendors introduce tiered pricing or reagent-rental schemes.

Throughput Limitations vs. qPCR & NGS for Population-Scale Testing

State-wide newborn-screening programs process tens of thousands of samples each week; current droplet systems plateau at roughly 480 samples per day, leaving room for competing modalities with higher multiplex capacity. Epidemiological demands driven by aging demographics double assay volumes every decade, a trend that favors qPCR arrays or next-generation sequencing in population-health labs. Manufacturers respond with 384-sample microfluidic cartridges yet still collide with physical partition-count ceilings before matching NGS scalability. Consequently, digital PCR retains a niche in low-throughput but ultra-sensitive applications until fundamental architecture innovations appear.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Consumables Drive Revenue, Software Accelerates Growth

Consumables & Reagents dominated revenue in 2025, holding 67.35% of the digital PCR market share as recurring kit purchases underpin vendor profitability. This leadership stems from specialized droplet-stabilizing chemistries that laboratories must replenish daily; no generic substitutes meet validation requirements for regulated assays. Consumable demand rises further as wastewater epidemiology and decentralized oncology centers schedule multi-run workflows, stimulating bulk-purchase agreements that increase order visibility for suppliers. Innovation also surges: the 2025 Vericheck ddPCR Empty-Full Capsid Kit delivers dual-parameter AAV assessments in one assay, streamlining cell-therapy lot release timetables and expanding addressable use cases in advanced therapies.

Software & Services, though beginning from a smaller base, will expand at a 14,14% CAGR through 2031, propelled by laboratories that want end-to-end genomic data management. Cloud platforms that integrate sample tracking, assay parameters and HIPAA-compliant result reporting match new IVDR data-integrity rules without heavy on-premises IT investments. As a result, software subscriptions offer vendors an annuity revenue stream that cushions cyclicality in capital-equipment purchases. In clinical contexts, audit-trail functionality aligns with FDA 21 CFR Part 11 mandates, lowering compliance hurdles and accelerating assay validation cycles. By 2031, cloud analytics bundled with instrument leases could become a default procurement model, fostering tighter customer lock-in while improving lab productivity.

By Technology: Droplet dPCR Leads, Microfluidic Innovation Accelerates

Droplet systems maintained 64.78% revenue share of the digital PCR market in 2025, largely because the format delivers up to 20,000 oil-encapsulated partitions that drive statistical precision without complex microfabrication. Early mover Bio-Rad capitalized on a decade of peer-reviewed validation studies, easing buyer concerns related to analytical performance. Industrial users appreciate the straightforward droplet workflow to quantify vector genomes, residual host-cell DNA and low-copy viral contaminants. Yet the architecture’s dependence on oil-water emulsification introduces consumable overhead and chemical waste that some sustainability programs flag for reduction.

Microfluidic chip platforms will post a 15.50% CAGR by machining microchambers directly into glass or polymer substrates, eliminating oil suspensions and reducing reagent volume per reaction. Nanomaterial coatings improve amplification efficiency and fluidic control, enabling point-of-care cartridges that consolidate sample prep, amplification and readout inside credit-card–sized cassettes. The architecture also lends itself to parallelization; chips with 5,000 to 10,000 microreactors process multiple patient samples simultaneously while preserving single-molecule sensitivity. Capital spending shifts as microfluidic readers cost about 30% less than traditional droplet generators, making entry feasible for first-time purchasers in middle-income economies. Although droplet systems remain entrenched in high-volume oncology labs, microfluidics attracts new users needing portability and lower per-sample cost.

By Application: Clinical Diagnostics Scale, Research Innovation Drives Growth

Clinical diagnostics accounted for 54.02% of the digital PCR market size in 2025, driven by liquid-biopsy oncology panels that now inform therapy selection and residual-disease surveillance. Assays for tuberculosis drug-resistance, CMV viral load in transplant recipients and HIV reservoir detection broaden the clinical menu, embedding digital PCR deeper into hospital pathology budgets. Laboratories praise the technology’s absolute quantification for unpacking subtle viral-load changes that trigger preemptive antiviral therapy. Regulatory agencies also issue companion-diagnostic approvals that mandate digital PCR readouts for emerging targeted therapies, anchoring clinical demand across the forecast period.

Research, while smaller in value terms, will grow at 14.86% CAGR as single-cell workflows and rare-variant discovery rely on digital PCR precision for orthogonal validation of NGS hits. The Shasta Single-Cell platform processes 1,500 cells per run, allowing immunologists to map T-cell receptor diversity with confidence intervals unattainable through qPCR alone. Oncology biomarker consortia apply digital PCR to confirm copy-number alterations in circulating tumor cells before advancing candidates into high-cost clinical studies. In academic centers, grant reviewers increasingly request absolute-quantification data, indirectly accelerating instrument placements in translational labs.

By End-User: Hospitals Lead Adoption, Pharma Drives Innovation

Hospitals and clinical laboratories represented 41.69% of the digital PCR market size in 2025 as they deploy same-day ctDNA or CMV assays that alter oncologist and transplant-surgeon prescriptions. Workflow automation slashes technologist hands-on time, allowing existing staff to operate molecular platforms without adding headcount. After the COVID-19 pandemic, administrators prioritize versatile molecular systems capable of pivoting from viral detection to oncology or antimicrobial-resistance panels, a need that digital PCR addresses through flexible assay menus.

Pharma and biotech entities will record an 16.04% CAGR because cell- and gene-therapy pipelines require validated viral-titer assays and residual-DNA checks for each batch. Contract-development and manufacturing organizations embed droplet platforms into lot-release protocols to comply with global quality guidelines. Biologic-drug sponsors further integrate digital PCR into pharmacokinetic studies that monitor therapeutic cell persistence or viral-vector clearance in vivo. Early adoption in preclinical stages locks the technology into future commercial workflows, multiplying test volumes once products reach market authorization.

Geography Analysis

North America dominated in 2025 by capturing 43.10% of digital PCR market share on the strength of payer reimbursement policies, FDA companion-diagnostic approvals and a USD 2 billion life-sciences capacity expansion by Thermo Fisher through 2028. The region’s academic-medical centers channel NIH precision-medicine grants directly into instrument procurement, while commercial laboratories negotiate reagent standing orders that secure volume discounts. Suppliers consequently prioritize North-American regulatory clearances, releasing oncology and transplant assays in the U.S. market a full year before global rollout. As a result, digital PCR market size in North America is projected to retain lead status throughout the forecast window.

Asia-Pacific will post the highest regional CAGR at 18.92%, reflecting China’s provincial funding for genomics infrastructure and India’s aggressive private-sector investments in NABL-accredited clinical labs. Policy initiatives under China’s Healthy China 2030 blueprint earmark funding for advanced molecular diagnostics, while local manufacturers collaborate with global vendors to localize reagent production and lower costs. Japan and South Korea supplement regional momentum by integrating digital PCR into national cancer screening pilots and rare-disease newborn tests. Government tenders that bundle instruments with multiyear reagent contracts accelerate market accession for first-time buyers. Europe maintains steady expansion as the IVDR standardizes performance-evaluation dossiers for molecular diagnostics across the bloc. Germany, France and the United Kingdom constitute tri-core demand clusters where biopharma hubs and well-funded health systems adopt digital PCR in oncology centers and central laboratories. Emerging EU economies leverage Cohesion-policy funds to modernize diagnostic infrastructure, often selecting microfluidic platforms that minimize reagent consumption. Meanwhile, Middle East & Africa and South America display early-stage adoption curves with pilot projects in tertiary hospitals and public-health institutes that could transition to full procurement cycles once cost barriers ease.

Competitive Landscape

Market concentration is moderate as the top five suppliers collectively command roughly 55% global revenue. Bio-Rad Laboratories secures front-runner status with an extensive droplet digital PCR portfolio and more than 8,000 supporting publications, effectively setting technical benchmarks for assay sensitivity and partition stability. The firm’s binding offer to acquire Stilla Technologies by Q3 2025 broadens its access to microfluidic architectures,[2]Bio-Rad Laboratories, “Bio-Rad to Acquire Stilla Technologies, Expanding Droplet and Microfluidic dPCR Portfolio,” bio-rad.com positioning Bio-Rad to cross-sell chip-based systems within its entrenched customer base and to balance reliance on droplet revenue.

Thermo Fisher Scientific pursues inorganic growth through a USD 40-50 billion M&A pipeline that already encompasses the 2024 acquisition of Combinati, injecting high-resolution counting technology into its instrument suite. QIAGEN draws competitive advantage from a vertically integrated workflow that marries sample preparation, assay chemistry and cloud informatics, offering laboratories a single-vendor solution that satisfies chain-of-custody and regulatory documentation requirements. Sysmex Corporation leverages hematology expertise to differentiate in blood-borne mutation testing, integrating digital PCR modules into its mainstream analyzers to win cross-selling opportunities in existing hospital accounts.

Emerging white-space opportunities include lower-price tiers for middle-income countries and niche environmental-monitoring applications. Standard BioTools partners with Next Gen Diagnostics to shrink per-sample sequencing costs below USD 10, an aggressive price point that forces digital PCR vendors to position their assays as complementary rather than competitive in large-scale surveillance.[3]Standard BioTools, “Standard BioTools and Next Gen Diagnostics Lower Pathogen Sequencing Costs,” standardbio.com Meridian Bioscience competes on specialized gastrointestinal-pathogen panels, illustrating that targeted applications can gain traction even when broader assay menus remain dominated by larger incumbents. As customers increasingly demand integrated hardware-software-reagent ecosystems, suppliers that lack full-stack portfolios are likely to seek partnerships or become acquisition targets.

Digital Polymerase Chain Reaction Industry Leaders

Bio-Rad Laboratories, Inc.

Thermo Fisher Scientific Inc

Sysmex Corporation

QIAGEN N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Bio-Rad Laboratories announced a binding offer to acquire Stilla Technologies to expand next-generation digital PCR capabilities.

- February 2025: Bio-Rad launched the Vericheck ddPCR Empty-Full Capsid Kit for precise AAV vector quality assessment.

- July 2024: Stilla Technologies entered a U.S. distribution partnership with Avantor to extend its Crystal Digital PCR platform.

- February 2024: Stilla Technologies closed a USD 26.5 million Series C round to accelerate commercialization of its microfluidic digital PCR instruments.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the digital PCR market as revenue generated from purpose-built instruments that partition nucleic-acid samples into thousands of micro-reactions for absolute quantification, together with their dedicated consumables, reagents, and bundled analysis software across clinical, research, forensic, and environmental settings in 17 nations.

Scope exclusion: Contract testing services and conventional or real-time PCR platforms fall outside this valuation.

Segmentation Overview

- By Component

- Digital PCR Instruments

- Droplet-based Platforms

- Chip-based Platforms

- Consumables & Reagents

- Software & Services

- Digital PCR Instruments

- By Technology

- Droplet Digital PCR (ddPCR)

- BEAMing Digital PCR

- Microfluidic Digital PCR

- By Application

- Clinical Diagnostics

- Oncology

- Infectious Disease Testing

- Genetic Disorders

- Research

- Gene Expression Analysis

- Copy Number Variation

- Forensics

- Other Applications

- Clinical Diagnostics

- By End-user

- Hospitals & Clinical Laboratories

- Academic & Research Institutes

- Pharmaceutical & Biotechnology Companies

- Contract Research Organizations

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed molecular pathologists, clinical lab managers, procurement heads, and regional distributors in North America, Europe, and Asia-Pacific.

These conversations helped us align average selling prices, replacement cycles, and emerging oncology and wastewater-testing uptake with the secondary evidence.

Desk Research

Publicly available datasets such as U.S. FDA 510(k) clearances, Eurostat HS-code 9027.80 trade flows, NIH RePORTER grant trends, and the WHO Pathogen Surveillance dashboards gave us foundational unit counts.

We then enriched these with insights from bodies such as the Association of Molecular Pathology, peer-reviewed journals, company 10-Ks, and news retrieved through Dow Jones Factiva and D&B Hoovers.

This menu is illustrative; many other sources were used to collect, verify, and clarify data.

Market-Sizing & Forecasting

A top-down reconstruction begins with national production plus import volumes for digital PCR devices, which are then priced using region-specific transfer values before being filtered through laboratory penetration rates.

Supplier installed-base roll-ups and sampled ASP × consumables usage act as bottom-up cross-checks.

Key variables like liquid-biopsy test volumes, infectious-disease funding, reagent-to-instrument attachment ratios, replacement timing, and capacity utilization feed into a multivariate-regression core, while an ARIMA overlay extends trends to 2030.

Data Validation & Update Cycle

Outputs undergo three-layer variance checks, senior-analyst review, and currency normalization.

The dataset refreshes each year, with interim updates triggered by major approvals, acquisitions, or +/-10% price shifts.

Why Mordor's Digital PCR Baseline Commands Reliability

Published figures often diverge because providers mix technology baskets, currency treatments, and forecasting cadences.

Key gap drivers we observed include the inclusion of qPCR or service revenue, single-time currency conversion, and aggressive oncology-testing assumptions that ignore manufacturing capacity constraints.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.84 B (2025) | Mordor Intelligence | - |

| USD 0.86 B (2025) | Global Consultancy A | Bundles multi-year service contracts and extended warranties |

| USD 7.12 B (2024) | Industry Journal B | Combines digital, real-time, and conventional PCR plus outsourced testing revenue |

| USD 0.70 B (2024) | Research Boutique C | Uses pre-COVID import baselines and omits consumables attachment |

These contrasts show that Mordor's tightly scoped hardware plus consumables model, refreshed on a disciplined annual cadence, provides decision-makers with a balanced, transparent baseline traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current digital PCR market size?

The digital PCR market is valued at USD 979.02 million in 2026 and is forecast to reach USD 2.11 billion by 2031, growing at 16.55% CAGR.

Which component segment leads revenue?

Consumables & Reagents lead with 56.74% digital PCR market share in 2025 because recurrent kit purchases dominate laboratory spending.

Why is Asia-Pacific the fastest-growing region?

China’s provincial genomics grants, India’s expanding clinical-lab network and supportive Japanese reimbursement policies drive a 18.92% CAGR across Asia-Pacific.

How do hospitals use digital PCR today?

Hospitals employ digital PCR for same-day liquid-biopsy oncology tests, viral-load monitoring in transplant patients and rapid AMR detection in infection-control units.

Which region has the biggest share in Global Digital PCR Market?

In 2025, the North America accounts for the largest market share in Global Digital PCR Market.

What limits wider adoption of digital PCR?

High capital expenditure, proprietary reagent costs and throughput ceilings relative to qPCR and NGS constrain uptake, particularly in large-scale public-health settings.

Page last updated on: