Digital Onboarding Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

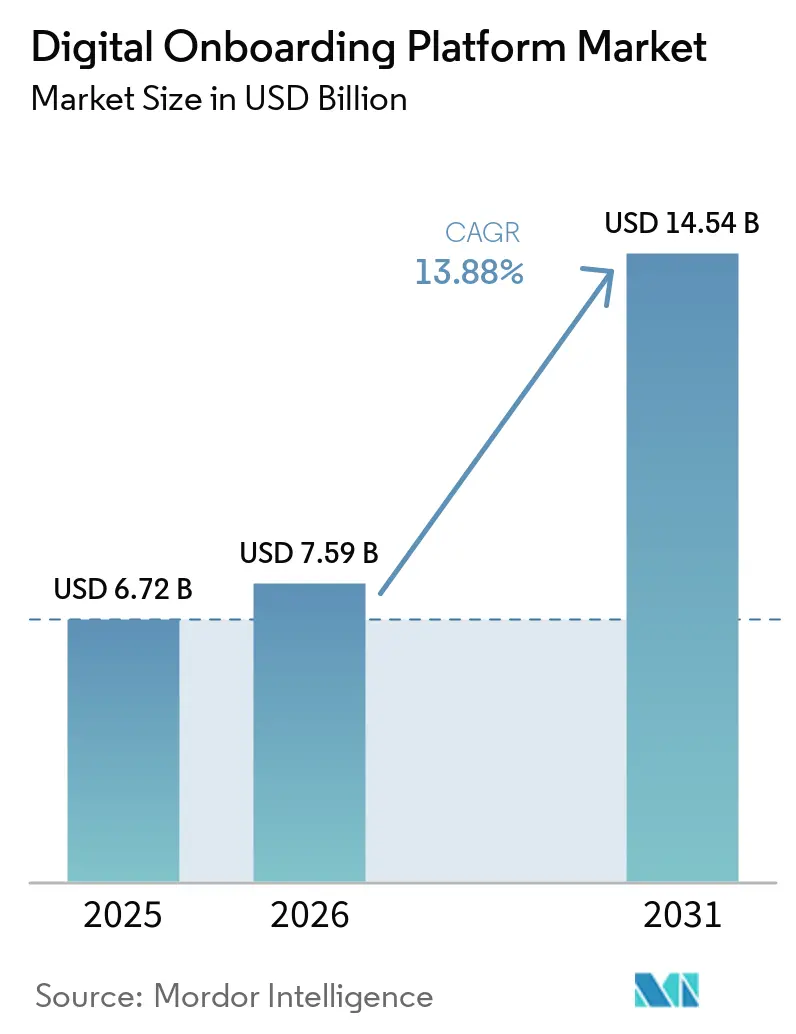

| Market Size (2026) | USD 7.59 Billion |

| Market Size (2031) | USD 14.54 Billion |

| Growth Rate (2026 - 2031) | 13.88% CAGR |

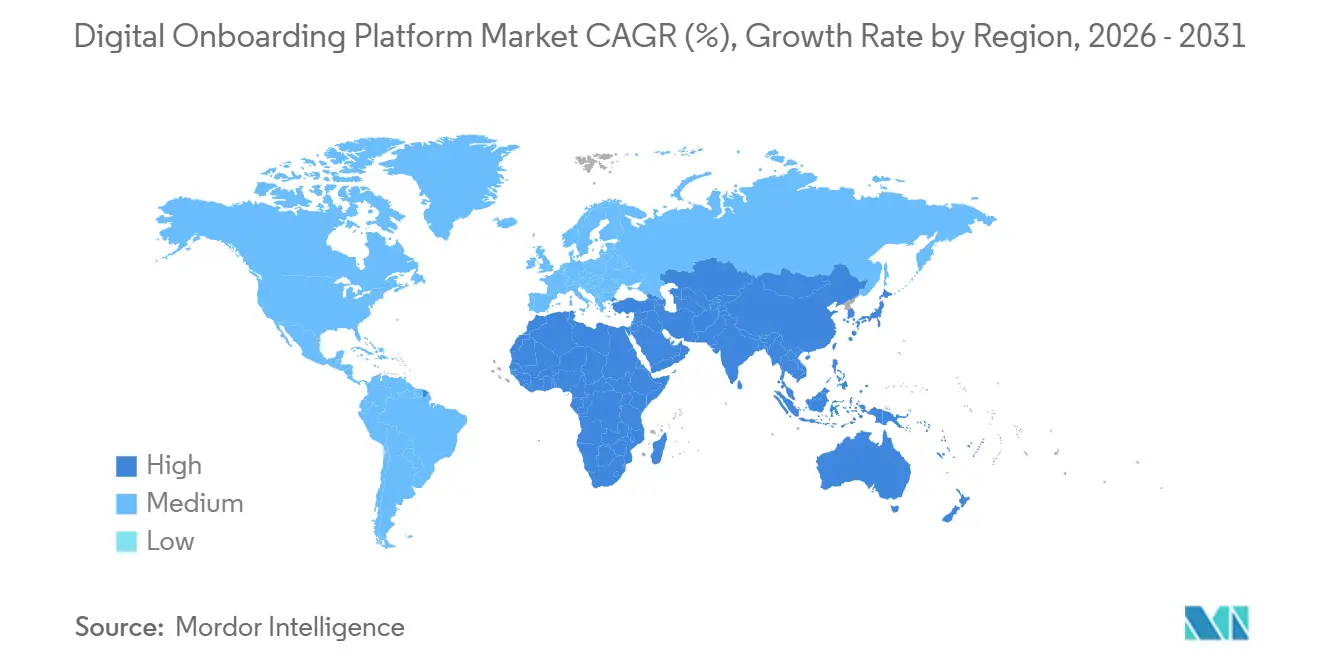

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Onboarding Platform Market Analysis by Mordor Intelligence

The digital onboarding platform market size is projected to be USD 6.72 billion in 2025, USD 7.59 billion in 2026, and reach USD 14.54 billion by 2031, growing at a CAGR of 13.88% from 2026 to 2031. The market is moving forward because identity verification, KYC workflow orchestration, and employee provisioning are now more closely tied to compliance deadlines, fraud control, and a more mobile workforce. Remote account opening and distributed work models pushed digital onboarding into core operating systems, and that shift continues to support demand in 2026. North America remained the largest regional revenue pool because it combined regulated institutions, mature enterprise software buyers, and a dense vendor base in identity and onboarding technologies. Asia-Pacific is set to expand the fastest as digital identity programs, mobile-first user behavior, and formalization across financial services continue to drive onboarding volumes higher. Competition is intense as vendors try to replace fragmented point solutions with broader trust platforms that combine KYC, KYB, AML screening, and fraud analytics, while differing rules across countries still limit easy global standardization.

Key Report Takeaways

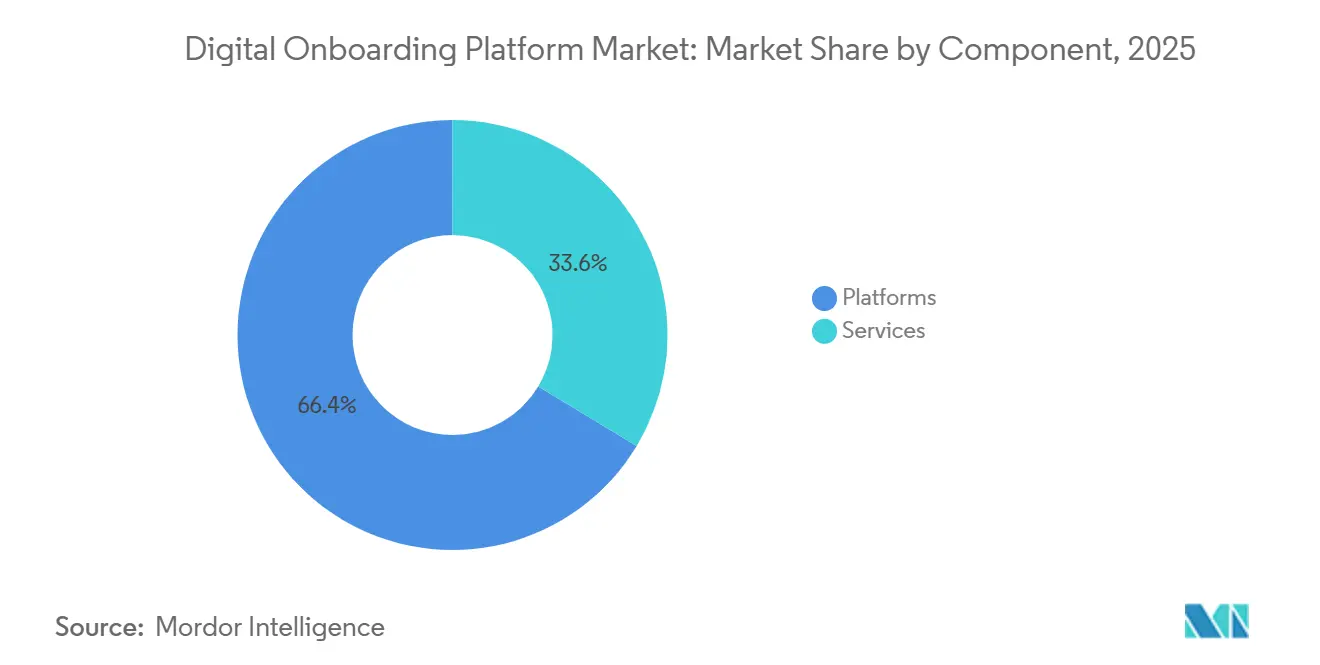

- By component, software platforms accounted for 66.37% of the digital onboarding platform market in 2025, while services are projected to expand at a 13.92% CAGR through 2031.

- By deployment model, cloud-based deployment accounted for 71.29% of the digital onboarding platform share in 2025, while hybrid deployment is projected to grow at a 14.73% CAGR through 2031.

- By enterprise size, large enterprises accounted for 63.41% of the market share in 2025, while SMEs are projected to expand at a 16.87% CAGR through 2031.

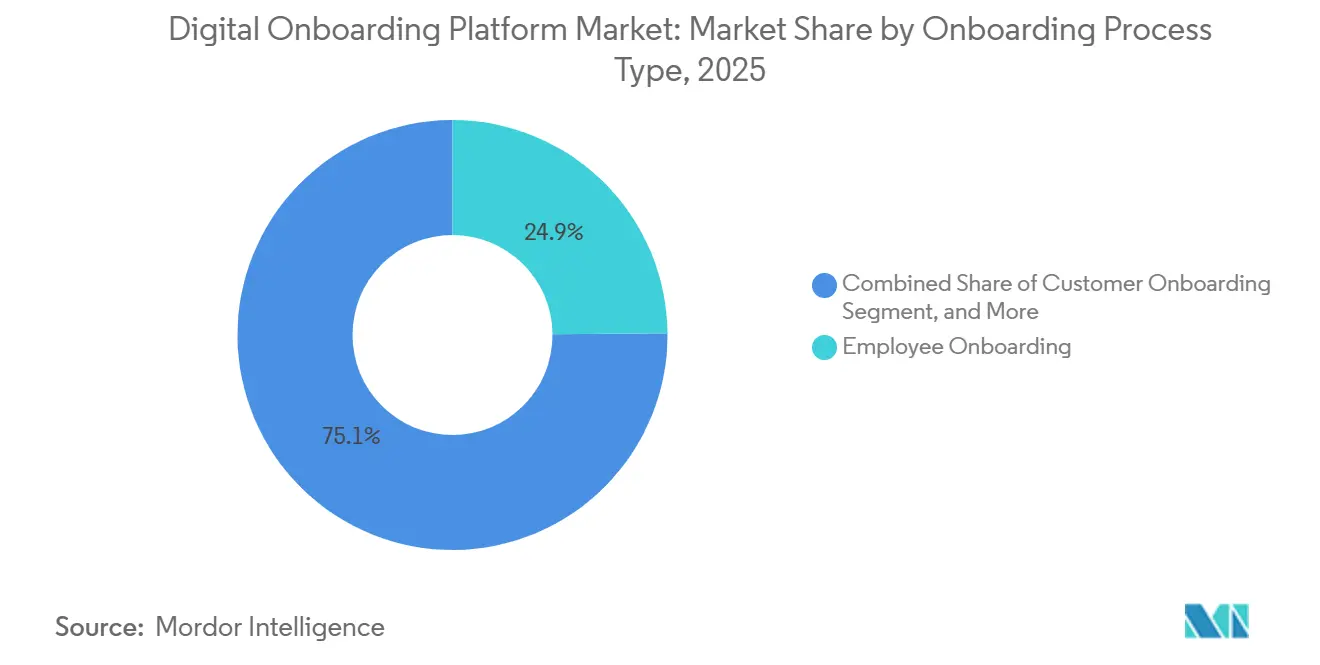

- By onboarding process type, employee onboarding held 24.87% share in 2025, while customer onboarding is projected to grow at a 17.29% CAGR through 2031.

- By end-user industry, information technology and telecom accounted for 29.47% share in 2025, while BFSI is projected to advance at an 18.41% CAGR through 2031.

- By geography, North America held 39.73% of the digital onboarding platform market share in 2025, while Asia-Pacific is projected to expand at a 19.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Digital Onboarding Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening KYC, AML, and Customer Due Diligence Mandates | +3.2% | Global, with concentrated early impact in North America and EU | Short term (≤ 2 years) |

| Acceleration of Remote and Mobile-First Account Opening | +2.8% | Global, led by Asia-Pacific and North America | Short term (≤ 2 years) |

| Rising Synthetic Identity, Deepfake, and Account Opening Fraud | +2.5% | Global | Short term (≤ 2 years) |

| Shift to Cloud-Native and API-First Onboarding Orchestration | +2.0% | Global, accelerating in Asia-Pacific and Europe | Medium term (2-4 years) |

| Emergence of Reusable Digital Identity Wallets and Verifiable Credentials | +0.9% | EU, Asia-Pacific, with spillover to Middle East | Medium term (2-4 years) |

| Embedded Finance and Platform-Led Multi-Party Onboarding Demand | +0.6% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening KYC, AML, and Customer Due Diligence Mandates

Regulatory change remains the clearest near-term trigger for replacement spending in the digital onboarding platform market. In April 2026, FinCEN proposed a risk-based four-pillar AML and CFT framework for financial institutions under the Bank Secrecy Act.[1]FinCEN, “FinCEN Issues Proposed Rule Revising the AML Program Requirements for Financial Institutions,” Federal Register, govinfo.gov The proposal raises attention on material implementation failures, which puts more pressure on firms still using manual reviews or fragmented onboarding controls. In Europe, the European Digital Identity framework and the implementation of eIDAS 2.0 are pushing institutions toward stronger trust services and interoperable digital identity models. That combination keeps compliance from being a one-time upgrade, since each new rule can reset expectations for identity capture, screening logic, audit trails, and consent management. Once a company aligns its workflows with current due diligence rules, moving to a non-compliant platform becomes more difficult, thereby increasing switching costs in the digital onboarding platform market.[2]European Commission, “European Digital Identity Regulation,” European Commission, europa.eu

Acceleration of Remote and Mobile-First Account Opening

Remote onboarding is now judged by completion speed as much as by control strength in the digital onboarding platform market. That shift is spreading beyond banking, as Aetna launched a digital-first benefits onboarding experience for 4 million members in February 2026. Jumio expanded its reusable identity solution to include selfies across South America in April 2026, which shows vendor investment in repeat verification journeys with less friction for returning users. Interac also moved to strengthen national digital onboarding flows in Canada in May 2026 through a collaboration with Incode that adds deepfake and injection-attack defenses. Mobile users are less willing to tolerate long review queues, so providers are redesigning onboarding journeys for fast capture, low friction, and immediate routing. As more enrollment journeys begin on phones, completion rates are increasingly tied to account growth, enrollment volume, and service activation.

Rising Synthetic Identity, Deepfake, and Account Opening Fraud

Fraud pressure is changing product design across the digital onboarding platform market. LexisNexis Risk Solutions reported that synthetic identity fraud increased eightfold globally in 2025 and that more than 1 in 10 frauds involved synthetic identities.[3]LexisNexis Risk Solutions, “Synthetic Identities and Agentic Bots Posing as Human Contribute to 8% Global Rise in Fraud Attacks,” LexisNexis Risk Solutions, risk.lexisnexis.com Entrust stated that deepfakes were linked to 1 in 5 fraud attempts, while injection attacks rose 40% year over year. Jumio said injection attempts rose 700% year over year and responded in April 2026 with continuous identity monitoring that checks risk signals after initial approval. These patterns undermine the value of static document checks, as a single verified event at entry no longer guarantees a stable identity afterward. Vendors that combine document validation, liveness, behavioral signals, and ongoing graph-based monitoring are therefore drawing more attention across the digital onboarding platform market.

Shift to Cloud-Native and API-First Onboarding Orchestration

Cloud-native orchestration is gaining ground because institutions need faster deployment without waiting for full core replacement. Hybrid adoption in the digital onboarding platform market also reflects data residency and control needs that make a full public-cloud move impractical for many regulated buyers. IBM made IBM Sovereign Core generally available in May 2026, demonstrating how infrastructure suppliers are building cloud environments that keep identity data and key management within defined jurisdictions. That model lets institutions modernize the onboarding layer first and connect it to older systems through APIs and governed workflows. It also helps vendors update fraud models, screening rules, and workflow logic without forcing a full replacement of the transaction core. As a result, more buyers now treat orchestration software as a durable operating layer rather than a temporary bridge inside the digital onboarding platform market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Fragmentation and Biometric Privacy Compliance Burden | -1.5% | Global, most acute in multi-jurisdiction operators across EU and US | Short term (≤ 2 years), Medium term (2-4 years) |

| Legacy Core-System Integration Complexity and Implementation Cost | -1.0% | Global, concentrated in North America and EU incumbent banks | Medium term (2-4 years) |

| Gray-Zone Review Queues From AI Spoof Edge Cases and Model Governance | -0.4% | Global | Medium term (2-4 years) |

| Data Localization and Sovereign Cloud Requirements | -0.3% | EU, Asia-Pacific, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Fragmentation and Biometric Privacy Compliance Burden

Regulatory fragmentation remains the clearest brake on scale in the digital onboarding platform market. California's CPRA became effective on January 1, 2026, and treats biometric data as sensitive personal information, adding compliance work from the first point of identity capture.[4]California Privacy Protection Agency, “CCPA Statute Effective January 1, 2026,” California Privacy Protection Agency, cppa.ca.gov In Europe, digital identity rules are moving toward stronger wallet-based trust models, but this does not eliminate local privacy, consent, and processing burdens for operators operating across several countries. Platform providers must therefore maintain separate consent, storage, retention, and review paths rather than rely on a single global workflow. That engineering burden falls hardest on smaller vendors and mid-sized buyers, and it slows launches because privacy design, model documentation, and legal review often need to be repeated by jurisdiction.

Legacy Core-System Integration Complexity and Implementation Cost

The digital onboarding platform market also faces a practical bottleneck in integrating with legacy core systems. Many regulated institutions can digitally approve identities but still struggle to provision accounts, permissions, or downstream records within older systems. That gap stretches implementation cycles, raises testing demands, and delays the operating savings that buyers expect from automation. It also creates a two-speed customer base, with cloud-native challengers moving faster while incumbents absorb long upgrade windows for each major workflow change. For vendors, integration depth is now almost as important as verification accuracy, because buyers want proof that onboarding decisions can flow smoothly into core operations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Keeps The Lead While Hybrid Builds The Next Compliance Path

Cloud-based deployment captured 71.29% of the digital onboarding platform market share in 2025, making it the leading deployment model. Buyers favored cloud because it lowers upfront infrastructure needs and shortens the path to live verification. The cloud model also enables vendors to distribute model updates for liveness checks, fraud detection, and document verification to many customers simultaneously. That matters in environments where attack methods are changing more quickly than traditional software release cycles. It also helps explain why cloud deployment remained attractive even for institutions that still maintain large legacy estates elsewhere.

Hybrid deployment is projected to expand at a 14.73% CAGR through 2031, showing that many buyers are building bridges rather than making full exits from on-premises systems. That pattern is strongest where institutions need cloud speed but must keep sensitive identity data, encryption controls, or approval records within local boundaries. IBM's May 2026 launch of IBM Sovereign Core highlights how suppliers are trying to support that middle path with jurisdiction-bound cloud operations. In the digital onboarding platform market, hybrid is becoming a strategic operating model rather than a temporary compromise. On-premises deployment still holds niche relevance for high-security use cases, but most growth is now centered on architectures that mix cloud orchestration with controlled local data handling.

By End User Enterprise Size: Large Enterprises Still Dominate Spending While SMEs Open A Wider Buyer Base

Large enterprises accounted for 63.41% of the market in 2025, making them the largest spending cohort in the digital onboarding platform market. Their lead came from larger contract values, multi-country compliance requirements, and more complex onboarding volumes across employees, customers, and third parties. Large organizations were also earlier adopters because they had the budget and governance structures needed to justify formal identity orchestration projects. Their deployments often span several workflows, which makes vendor relationships broader and harder to displace. That helps explain why enterprise accounts still account for a large share of revenue, even as newer buyer groups enter the market.

SMEs are projected to grow at a 16.87% CAGR through 2031, showing that identity orchestration is moving downmarket within the digital onboarding platform market. This shift is tied to embedded finance, partner onboarding, and software-led distribution of compliance tasks that smaller firms did not previously handle themselves. Modern Treasury and Persona announced a partnership in April 2026 to strengthen business onboarding and compliance, reflecting the need for easier API-based KYB workflows in payment operations. Veriff's February 2026 acquisition of Vespia also supports this direction by expanding from individual verification into real-time business verification across more than 300 jurisdictions. As regulated services spread through vertical software and platform ecosystems, smaller businesses are becoming meaningful buyers rather than edge cases in the digital onboarding platform market.

By Onboarding Process Type: Employee Flows Lead Today While Customer Journeys Scale Faster

Employee onboarding held 24.87% market share in 2025, making it the largest process segment in the digital onboarding platform market. That position reflects steady demand from enterprises that must verify work eligibility, conduct background checks, and grant access across multiple locations and systems. Employee workflows also benefit from repeatable internal processes, which make them a practical entry point for automation. At the same time, the identity layer used for employee journeys is increasingly overlapping with the layer used for customer and partner onboarding. That shared foundation allows vendors to expand from one workflow into adjacent ones without rebuilding the full identity stack.

Customer onboarding is projected to expand at a 17.29% CAGR through 2031, making it the fastest-growing process type in the digital onboarding platform market. Growth is supported by digital account opening, digital enrollment, and the expansion of identity checks across healthcare, telecom, retail, and financial services. Aetna launched a digital-first benefits onboarding experience for 4 million members in February 2026, demonstrating that customer onboarding demand now extends beyond banking into broader enrollment environments. Merchant, supplier, and partner onboarding also remain strategically important, as payment, platform, and marketplace models now require stronger business verification at the point of entry. That shift is widening the addressable market for onboarding events in the digital onboarding platform market.

By End User Industry: IT And Telecom Generates Scale While BFSI Drives The Fastest Expansion

Information technology and telecom accounted for 29.47% of the market in 2025, placing the segment first in the digital onboarding platform market. The sector supports high onboarding volume on two sides at once, with constant employee intake across distributed teams and customer activation across digital service channels. Telecom operators also face identity-sensitive use cases, such as SIM-related fraud prevention, where delays and friction can both incur direct costs. That makes the sector a strong fit for automated workflows that combine speed, auditability, and biometrics. Its leadership shows how onboarding software is no longer limited to regulated finance and is now tied to broader digital service operations.

BFSI is projected to grow at an 18.41% CAGR through 2031, making it the fastest-expanding vertical in the digital onboarding platform market. FinCEN's April 2026 AML and CFT proposal reinforces why the sector remains highly sensitive to onboarding adequacy and ongoing control effectiveness. Fraud escalation adds further urgency, as synthetic identity and deepfake risks now affect the first step of account opening rather than only later transaction monitoring. Healthcare and life sciences are also gaining relevance through patient onboarding and insurance enrollment, while retail demand is rising amid stronger age-assurance requirements. AU10TIX's April 2026 privacy-first age assurance positioning shows how adjacent compliance categories are creating new demand paths beyond classic banking KYC.

Geography Analysis

North America held 39.73% of the digital onboarding platform market share in 2025, keeping it as the largest regional segment. The United States remained central because it combined regulated financial institutions, enterprise HR software demand, and a deep vendor base in identity verification and fraud detection. FinCEN's April 2026 AML and CFT reform proposal is pushing institutions to review whether legacy onboarding controls can meet a more outcome-focused standard of risk-based effectiveness. In Canada, Interac announced a May 2026 collaboration with Incode to add iBeta Level 3-validated liveness, deepfake detection, and injection-attack defense to Interac Verified solutions, signaling national-level investment in stronger digital onboarding infrastructure.

Asia-Pacific is projected to grow at a 19.13% CAGR through 2031, making it the fastest-growing regional segment in the digital onboarding platform market. Growth is being supported by mobile-first users, expanding fintech ecosystems, and stronger links between digital identity infrastructure and commercial onboarding flows. In Japan, LIQUID eKYC supported Seven Bank's foreign account opening process through IC chip-based identity verification, reducing dependence on manual document capture for some user groups. That combination of mobile use, identity infrastructure, and platform-led service delivery continues to make Asia-Pacific one of the most active regions for the adoption of new onboarding models.

Europe held a significant share of the market in 2025, with Germany and the United Kingdom as major sub-markets. Germany advanced its legal framework for the European Digital Identity Wallet in 2026 through the Digitales-Identitäten-Gesetz, supporting the next phase of national wallet deployment. The broader European Digital Identity framework is also shaping how onboarding platforms prepare for wallet-based identity exchange and interoperable trust services. South America is gaining relevance as reusable identity models spread, with Jumio extending selfie across the region in April 2026. The Middle East and Africa remained smaller in absolute terms, but adoption continued to improve as vendors localized their products and governments expanded digital identity efforts.

Competitive Landscape

The digital onboarding platform market remains highly competitive, with recognized suppliers spread across enterprise trust platforms, focused verification specialists, and workflow orchestration providers. This structure keeps competition active because buyers can choose between broad suites and narrower products based on compliance depth, integration needs, and fraud exposure. It also means no single company appears to dominate the market across all regions and use cases. Buyers are increasingly favoring vendors that can unify KYC, KYB, AML screening, fraud analytics, and reusable identity in one operating environment. That preference is pushing competition away from standalone checks and toward platform depth, governance quality, and long-term workflow ownership.

Strategic expansion through M&A remained a visible pattern in 2025 and 2026. Veriff acquired Vespia in February 2026 to move from individual identity verification toward a broader trust platform with business verification capabilities. Socure acquired Qlarifi in December 2025 to extend its RiskOS platform into buy now, pay later credit infrastructure alongside identity and anti-fraud capabilities. These moves reflect a clear push toward single-vendor trust stacks that reduce vendor sprawl and simplify audit trails.

Product differentiation is also shifting toward continuous monitoring, deepfake defense, and ecosystem reach. Jumio launched Jumio Watch in April 2026 to extend identity intelligence beyond the onboarding event into ongoing post-approval monitoring. Shufti Pro achieved iBeta Level 3 ISO/IEC 30107-3 conformance for passive liveness detection in May 2026, strengthening its position in biometric onboarding. Experian added Incode to its partner ecosystem in August 2025, expanding Incode's access to a broad client base across financial services, healthcare, automotive, and digital marketing.

Digital Onboarding Platform Industry Leaders

Jumio Corporation

Trulioo Information Services Inc.

Signicat AS

Veriff OÜ

Au10tix Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Interac Corp. announced a collaboration with Incode Technologies to add iBeta Level 3-validated liveness and deepfake and injection-attack detection to Interac Verified solutions, with exclusive Canadian rights for document verification using Incode's technology. The phased rollout targets a Q3 2026 launch and aims to accelerate digital onboarding while reducing impersonation risk at the national payments network level.

- May 2026: Shufti Pro achieved iBeta Level 3 ISO/IEC 30107-3 conformance for passive liveness detection on both iOS and Android platforms, becoming the first European company to achieve this standard. The certification validates protection across 2D and 3D presentation attacks and fully synthetic identities, marking a significant competitive differentiator in biometric onboarding.

- April 2026: Jumio launched Jumio Watch, a continuous identity intelligence product that monitors identity risk signals post-onboarding using the Jumio Identity Graph. Early testing showed up to 25% more risk detected after initial onboarding approval, with injection attempt volumes rising 700% year-over-year.

- April 2026: AU10TIX selected Camunda to orchestrate high-volume KYC and KYB identity verification workflows, consolidating document capture, authenticity checks, third-party risk screening, and decision routing into a single governed process for large-scale enterprise deployments.

Global Digital Onboarding Platform Market Report Scope

The Digital Onboarding Platform Market refers to technology solutions and services that automate and optimize onboarding processes for diverse stakeholders, including customers, employees, vendors, suppliers, partners, and merchants. These platforms combine software and services to streamline documentation, compliance, identity verification, workflow management, and integration into organizational systems. Delivered through cloud-based, on-premises, and hybrid deployment models, they cater to both large enterprises and small and medium-sized enterprises across industries such as BFSI, healthcare and life sciences, information technology and telecom, retail and e-commerce, industrial manufacturing, government and public sector, and other end-user industries. The core purpose of this market is to enhance efficiency, reduce administrative overhead, ensure compliance, and improve user experience by leveraging automation, analytics, and digital workflows throughout the onboarding lifecycle.

The Digital Onboarding Platform Market report is segmented by Component (Software Platforms, and Services), Deployment Model (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-sized Enterprises), Onboarding Process Type (Customer Onboarding, Employee Onboarding, Vendor and Supplier Onboarding, and Partner and Merchant Onboarding), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, and Government and Public Sector), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software Platforms |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Customer Onboarding |

| Employee Onboarding |

| Vendor and Supplier Onboarding |

| Partner and Merchant Onboarding |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Software Platforms | |

| Services | ||

| By Deployment Model | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By End User Enterprise Size | Large Enterprises | |

| Small and Medium-sized Enterprises | ||

| By Onboarding Process Type | Customer Onboarding | |

| Employee Onboarding | ||

| Vendor and Supplier Onboarding | ||

| Partner and Merchant Onboarding | ||

| By End User Industry | BFSI | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecom | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the digital onboarding platform market?

The digital employee onboarding platform market reached USD 6.72 billion in 2025 and is estimated at USD 7.59 billion in 2026, with forecasts pointing to USD 14.54 billion by 2031.

How fast is digital onboarding platform expected to grow through 2031?

The market is projected to expand at a CAGR of 13.88% from 2026 to 2031, supported by compliance pressure, fraud defense needs, and broader digital onboarding adoption.

Which region leads global adoption of digital onboarding platform?

North America led with 39.73% share in 2025 because of its large base of regulated institutions, enterprise software buyers, and identity verification vendors.

Which region is growing the fastest in this space?

Asia-Pacific is projected to grow at a 19.13% CAGR through 2031, helped by mobile-first user behavior, digital identity programs, and strong fintech activity.

Which component category generates the most revenue?

Software platforms led the component mix with 66.37% share in 2025 because buyers prefer configurable orchestration layers that can support ongoing compliance and fraud updates.

What is the fastest-growing onboarding process type?

Customer onboarding is projected to grow at a 17.29% CAGR through 2031 as digital enrollment expands across BFSI, healthcare, telecom, retail, and platform-based business models.

Page last updated on: