Digital Sustainability Twin Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

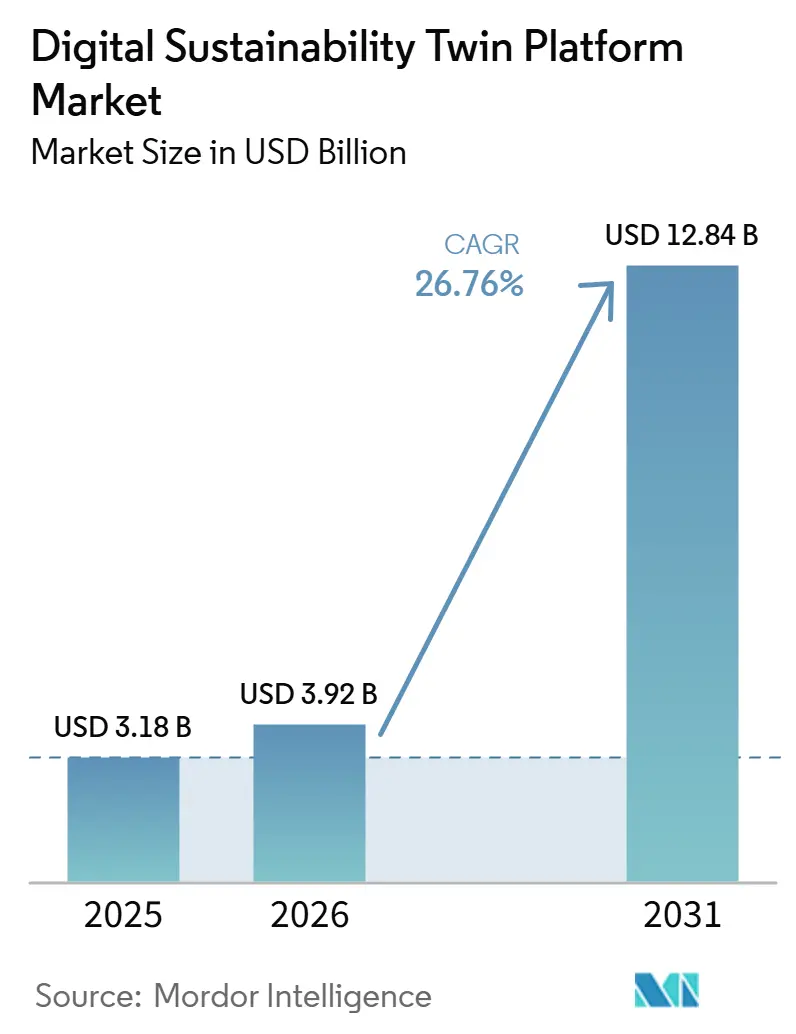

| Market Size (2026) | USD 3.92 Billion |

| Market Size (2031) | USD 12.84 Billion |

| Growth Rate (2026 - 2031) | 26.76% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Sustainability Twin Platform Market Analysis by Mordor Intelligence

The digital sustainability twin platform market size was valued at USD 3.18 billion in 2025 and is expected to reach USD 3.92 billion in 2026 and USD 12.84 billion by 2031, growing at a CAGR of 26.76% from 2026 to 2031. Regulatory pressure is turning these platforms into core operating systems for compliance, especially as companies need more verifiable sustainability data and stronger reporting controls. The move away from spreadsheet-based carbon accounting is also driving adoption, as buyers want live operating views, better audit trails, and faster scenario testing. Competition is getting tighter as industrial software vendors expand proprietary capabilities while cloud providers strengthen the infrastructure layer that many deployments rely on. Demand is also broadening as cloud-native delivery lowers upfront barriers and supply chain disclosure requirements reach more companies across extended vendor networks. Even with this strong outlook, the digital sustainability twin platform market still depends on how quickly buyers can handle system integration challenges and secure enough simulation and sustainability talent.

Key Report Takeaways

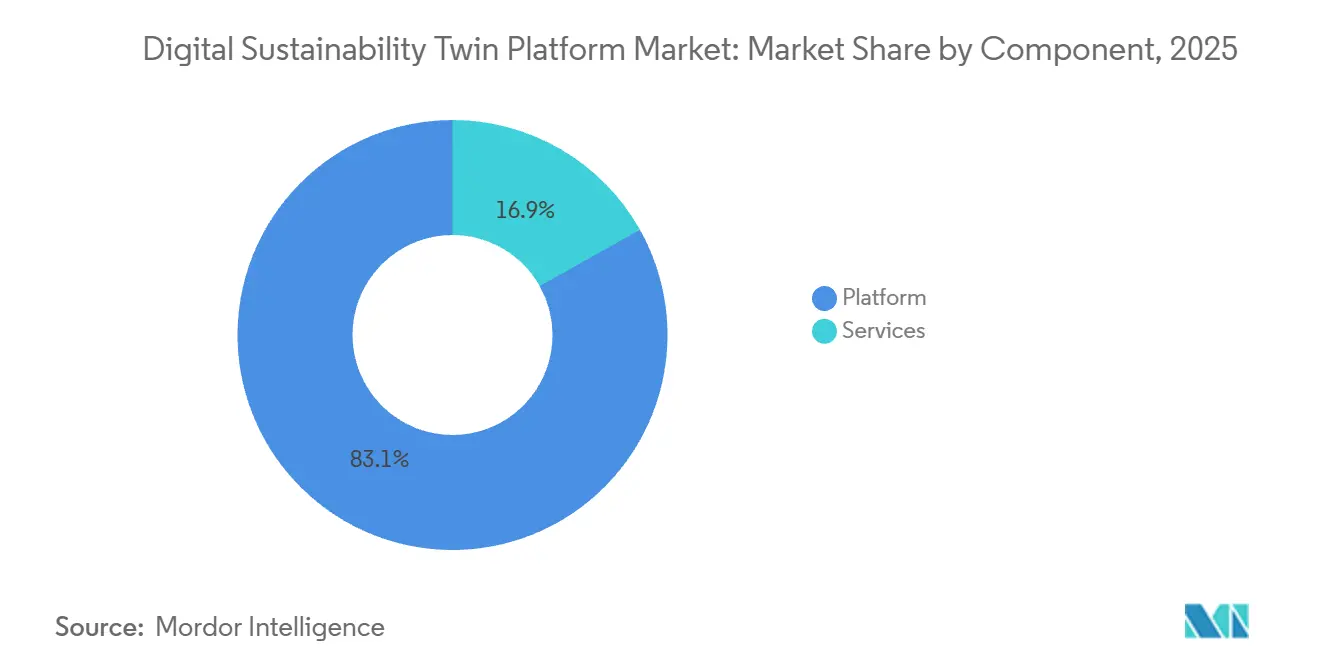

- By component, platform led with 83.14% revenue share in 2025, while services are projected to expand at 30.28% CAGR through 2031.

- By deployment mode, cloud-based architecture held 66.83% of the digital sustainability twin platform market share in 2025, while hybrid deployment is projected to grow at 31.46% CAGR through 2031.

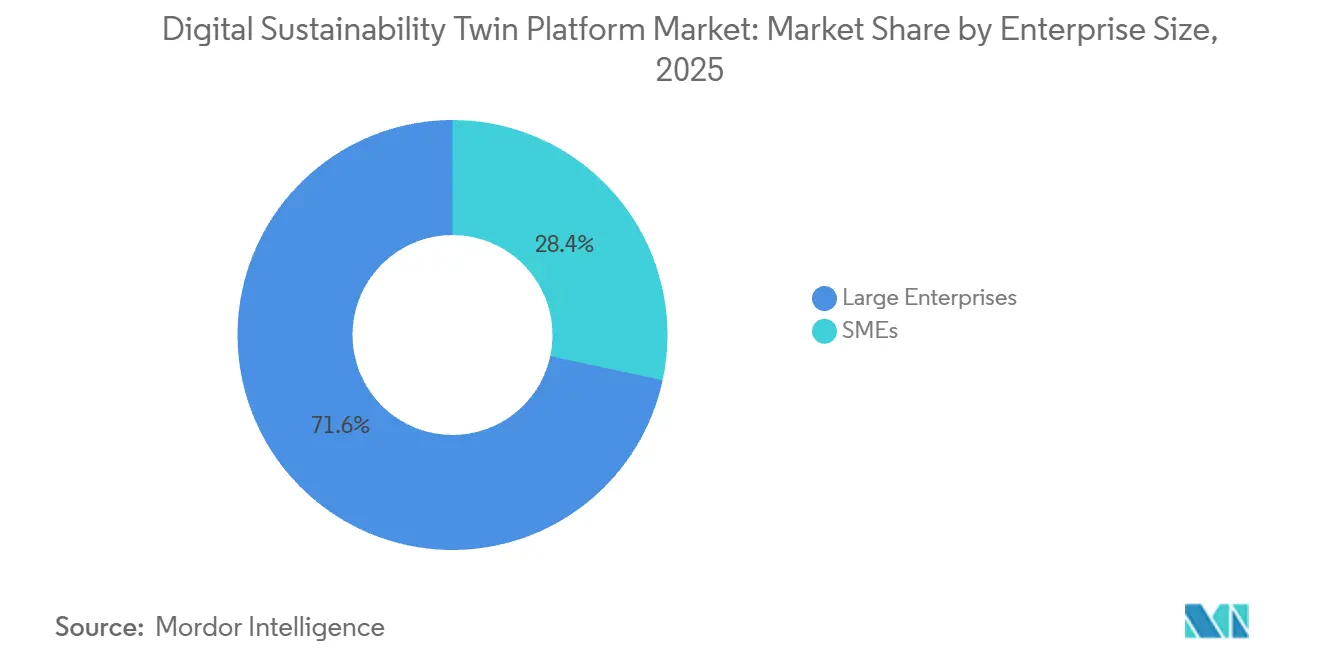

- By enterprise size, large enterprises held 71.62% share in 2025, while SMEs are projected to grow at 28.74% CAGR through 2031.

- By end-user industry, industrial manufacturing accounted for 32.48% share of the digital sustainability twin platform market size in 2025, while government and smart cities are projected to advance at 29.83% CAGR through 2031.

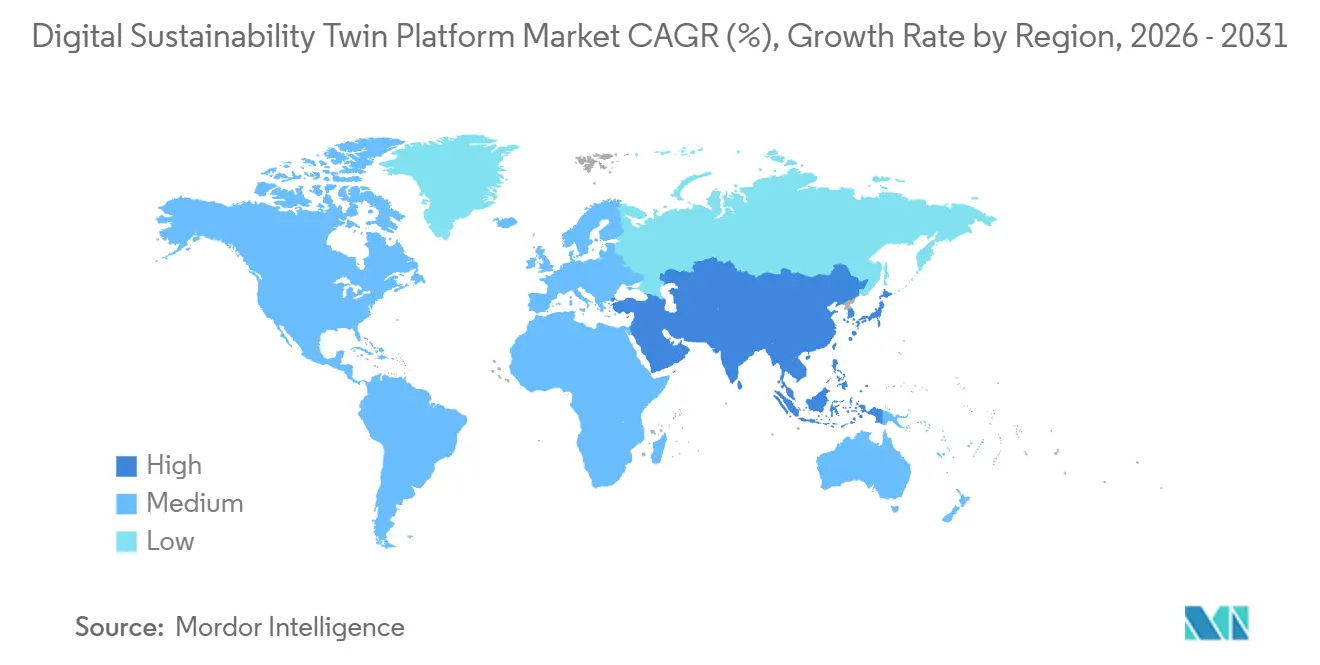

- By geography, North America led with 36.26% share in 2025, while Asia-Pacific is projected to expand at 29.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Digital Sustainability Twin Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability Reporting and Carbon Accounting Pressure | +5.8% | Global, with concentrated early gains in EU, UK, and North America | Short term (≤ 2 years) |

| Real-Time Energy and Emissions Optimization Demand | +5.2% | Global, with Asia-Pacific, North America, and East Asia as core markets | Medium term (2-4 years) |

| Industry 4.0 Expansion Across Asset-Intensive Operations | +4.6% | Global, with spillover to Middle East and Africa and South America through manufacturing FDI | Medium term (2-4 years) |

| Cloud and AI-Enabled Simulation Scalability | +4.1% | North America and EU core, with Asia-Pacific as a fast adopter | Short term (≤ 2 years) |

| Digital Twin Readiness for Smart Buildings and Smart Cities | +3.4% | Asia-Pacific core, EU, and Middle East | Long term (≥ 4 years) |

| Operational Resilience Planning Under Climate and Supply Chain Volatility | +2.8% | Global, with concentrated urgency in coastal and climate-vulnerable economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustainability Reporting and Carbon Accounting Pressure

The compliance case for the digital sustainability twin platform market strengthened sharply as the EU Corporate Sustainability Reporting Directive increased the need for audit-ready sustainability data, and the Carbon Border Adjustment Mechanism tied carbon reporting more directly to financial exposure from 2026 onward.[1]European Commission, “Carbon Border Adjustment Mechanism (CBAM) - Regulation (EU) 2023/956,” Official Journal of the European Union, europa.eu This raised the value of platforms that can track emissions with stronger traceability rather than rely on manual files and fragmented reporting chains. A December 2025 paper in Systems reported that companies using sustainability-focused digital twins had an average ESG score of 0.79, compared with 0.72 for non-adopters. That gap matters because investors, auditors, and regulators increasingly look beyond disclosure volume and focus more on data lineage, model transparency, and repeatability of reported results. Companies that stay with spreadsheet-heavy methods face higher verification effort because static files do not preserve operational context as clearly as live model environments. Vendors that can connect each emissions value to the source asset, process step, and time stamp are therefore better placed to win compliance-led demand in the digital sustainability twin platform market.

Real-Time Energy and Emissions Optimization Demand

Demand in the digital sustainability twin platform market also rose because buyers started to see measurable operating gains, not just cleaner sustainability reporting. A 2026 study in Scientific Reports showed that AI-driven digital twins in power system asset management improved investment ROI by 9.8% while supporting 97% variable renewable energy penetration without reducing grid flexibility. At the facility level, Siemens reported that its AI-enhanced digital twin deployment at the Amberg Smart Factory reduced energy consumption by 25% and cut CO2 emissions by 20%. These results widened the buyer base because they gave operations leaders and finance teams a more direct economic case for adoption. The appeal is especially strong when energy savings and throughput gains can justify investment even before carbon prices or formal reporting requirements become the main trigger. This is why the digital sustainability twin platform market is gaining traction as an operations tool as much as a sustainability tool.

Industry 4.0 Expansion Across Asset-Intensive Operations

The growth of Industry 4.0 created a practical starting point for the digital sustainability twin platform market because many asset-heavy companies have already built sensor, control, and data collection layers. Even so, a 2026 paper in F1000Research found that sustainability outcomes from Industry 4.0 adoption remained uneven because many deployments captured IoT data without linking it to emissions modeling or lifecycle assessment. That finding matters because raw visibility is not enough if companies cannot turn plant data into decisions on energy use, material efficiency, and carbon performance. The firms moving faster are those that integrate production monitoring and sustainability modeling within the same decision process rather than treating them as separate programs. TotalEnergies signaled that direction in September 2025 when it expanded its partnership with Cognite across all operated upstream assets worldwide to support dynamic asset visualization and AI-driven production performance monitoring. The digital sustainability twin platform market benefits most where industrial modernization is already mature enough to support richer sustainability use cases on top of operating data.

Cloud and AI-Enabled Simulation Scalability

The digital sustainability twin platform market is also benefiting from better simulation portability and faster AI-assisted analysis. A January 2026 paper in Energies validated an interoperable user-centered digital twin framework for sustainable energy system management, showing that broader deployment now depends as much on usable design and system interoperability as on computing capacity itself. This suggests that the market is moving beyond the question of whether advanced modeling can run at scale and toward the question of how easily different teams can use it in daily work. SAP reinforced that shift in May 2026 when it said its sustainability AI agents reduced scenario simulation time from 1 day to 20 minutes and cut packaging compliance review hours by more than 50%. Faster analysis matters because it shortens the time between data capture, model output, and management action. As that cycle compresses, the digital sustainability twin platform market becomes easier to justify inside routine planning, compliance review, and operating improvement workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity Across OT and IT Systems | -3.2% | Global, with acute impact in legacy-heavy industrial markets in Europe, South America, and Middle East and Africa | Medium term (2-4 years) |

| Shortage of Simulation, Data Fusion, and Sustainability Modeling Talent | -2.6% | Global, especially pronounced in Asia-Pacific emerging economies and South America | Long term (≥ 4 years) |

| Data Governance, Cybersecurity, and Model Assurance Concerns | -1.8% | Global, within IEC 62443 and ISO 27001 compliance contexts | Medium term (2-4 years) |

| Long Payback Period for Multi-Site Sustainability Twin Deployments | -1.4% | Primarily affecting SMEs and first-time adopters globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity Across OT And IT Systems

The hardest operating challenge in the digital sustainability twin platform market remains the job of bringing plant systems, enterprise software, and sustainability models into one dependable environment. Sustainability twins require time-synchronized data from energy meters, equipment telemetry, process historians, and external carbon factors, and those data streams were not originally designed to work together. This becomes more difficult in older industrial sites where control layers, reporting tools, and security practices were built in separate stages over many years. Standards such as IEC 62443 add a necessary layer of cybersecurity review, but they also extend deployment timelines and increase implementation effort for connected industrial environments. The result is that many projects take longer to move from visibility to decision support than buyers first expect. This keeps integration work near the center of cost, timing, and adoption risk in the digital sustainability twin platform market.

Shortage of Simulation, Data Fusion, and Sustainability Modeling Talent

The digital sustainability twin platform market also faces a labor constraint that technology alone cannot resolve. Effective deployment needs people who can combine simulation knowledge, operational technology context, environmental metrics, and reporting requirements within one operating model. Siemens and IFS pointed to this issue in 2025 when they described the challenge of linking engineering design intent with field performance data from live operations.[2]Siemens AG, “Siemens and IFS Partner,” Siemens News, news.siemens.com That skills gap slows deployment, weakens model maintenance, and raises the risk that users will underuse advanced platform capabilities after purchase. It also favors large enterprises and vendors with managed service capacity because they can spread scarce expertise across broader project portfolios. Smaller adopters may therefore enter the digital sustainability twin platform market later or choose lighter modules until they can support model governance on a more consistent basis.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platform Leadership Supports a Larger Services Opportunity

The platform segment held 83.14% of the market in 2025, which kept it at the center of enterprise buying decisions in the digital sustainability twin platform market. Much of that value sat in core software layers such as simulation engines, data ingestion tools, workflow controls, and carbon modeling frameworks. Buyers often commit most of their initial spend at this stage because the platform determines how operating data, sustainability metrics, and reporting outputs will connect later. Siemens illustrated this approach in January 2026 when it introduced Digital Twin Composer with real-time OT data integration, physics-based AI simulation, and sustainability KPI dashboards in a single environment. Early customer use reported 10-15% capital expenditure reductions through virtual commissioning, which helped support large upfront platform contracts.

Services are projected to grow at 30.28% CAGR through 2031, making them the faster-moving part of the digital sustainability twin platform market size. This pattern reflects what happens after deployment, because model calibration, emissions mapping, scenario design, and reporting alignment become more important once the base system is in place. The services opportunity expands further when companies move from one site to many sites and need to adjust assumptions, thresholds, and governance across each operating context. In that setting, service spending becomes a recurring requirement rather than a one-time implementation step. Springer Nature reported in 2026 that circular economy digital twin frameworks require ongoing expert configuration to turn operational data into actionable sustainability intelligence. That finding supports the view that services growth in the digital sustainability twin platform market is tied to structural maturity needs, not just temporary rollout support.

By Deployment Mode: Hybrid Adoption Reflects Industrial Operating Reality

Cloud-based deployment accounted for 66.83% of the market in 2025, making it the most popular architecture choice across the digital sustainability twin platform market. Its lead came from lower infrastructure overhead, easier scaling across multiple sites, and better support for centralized carbon and operational data aggregation. Cloud environments are especially useful when companies want shared reporting logic across distributed assets and faster access to scenario modeling capacity. Microsoft showed the scale of this model in April 2025 when it said Enerjisa Üretim used Azure Digital Twins to process more than 50,000 signals per second from hydropower, wind, and solar plants while combining real-time monitoring with production forecasting. That example highlights why cloud architecture remains attractive for organizations that need broad asset visibility and consolidated sustainability logic.

Hybrid deployment is projected to grow at 31.46% CAGR through 2031, which shows that many users are choosing a mixed architecture instead of a full move away from local systems. Asset-intensive operations still need strong local control for time-sensitive decisions, especially where latency, process stability, and plant safety remain critical. At the same time, cloud resources are useful for carbon simulation, scenario testing, and cross-site sustainability reporting. This means the fastest-growing model keeps operational control close to the asset while placing heavier analytics and disclosure workloads where shared computing is easier to scale. The digital sustainability twin platform market is therefore adapting to industrial constraints rather than forcing a uniform architecture on every end user. That balance should remain important as adoption expands in sectors with complex operating environments and strict uptime requirements.

By Enterprise Size: Large Enterprises Lead While SME Demand Broadens

Large enterprises held 71.62% of the digital sustainability twin platform market share in 2025, reflecting the budget, data ownership, and cross-functional governance needed for broad deployments. These organizations usually have more mature sustainability programs, larger asset footprints, and stronger internal coordination between operations, IT, finance, and reporting teams. They are also better able to absorb long implementation cycles and build teams that can maintain model quality over time. A December 2025 Systems study found that 56% of high-ESG-maturity firms adopted digital twins, compared with 40% of firms with lower ESG maturity. That result helps explain why the digital sustainability twin platform market has been concentrated first in larger companies with stronger governance readiness.

SMEs are projected to grow at 28.74% CAGR through 2031, which makes them the faster-growing buyer group even though they started from a smaller base. Lower-cost cloud delivery has helped, but regulation and supply chain expectations appear to be the larger force behind this shift. Many smaller suppliers now face requests for more structured emissions and lifecycle data from larger customers that are tightening value chain reporting. This changes sustainability data from a voluntary exercise into a commercial requirement tied to customer retention. Vendors that offer lighter rollout models, clearer templates, and managed reporting support are likely to benefit most from this expanding part of the digital sustainability twin platform market. The shift does not remove SME resource constraints, but it does make delayed adoption harder to sustain over time.

By End-User Industries: Manufacturing Anchors Revenue While Public Use Cases Rise

Industrial manufacturing held 32.48% share in 2025, the largest contribution within the digital sustainability twin platform market size. This position reflected the sector's high energy intensity, complex material flows, and direct scope 1 emissions, which make both operating gains and compliance outcomes easier to measure. Manufacturers can often connect twin deployment to cost, throughput, waste, and emissions in ways that support clearer investment cases. IntechOpen reported that digital twin deployments across manufacturing, energy, and urban infrastructure delivered 15-30% energy savings and emissions reductions of up to 25%, with the strongest returns in high-energy-intensity settings.[3]IntechOpen, “Scenario-Based Analysis on Digital Twin: Toward a Greener Industry 4.0,” IntechOpen, intechopen.com Those conditions keep industrial manufacturing as the clearest commercial anchor for the digital sustainability twin platform market.

Government and smart cities are projected to grow at 29.83% CAGR through 2031, making them the fastest-rising vertical. This growth reflects the need to model climate adaptation, water systems, urban infrastructure, and city-wide emissions in a more dynamic way than static planning tools allow. Public-sector programs can also create wider adoption effects because city projects often involve utilities, transport networks, and building systems at the same time. France reinforced this trajectory in April 2026 when it launched a EUR 25 million (USD 28.6 million) national program to develop digital twins of French territories and target first operational city-scale applications by the end of 2026. That program shows how the digital sustainability twin platform market is broadening from plant-level optimization into public planning and municipal resilience use cases.

Geography Analysis

North America held 36.26% of the digital sustainability twin platform market share in 2025, with the United States accounting for most of the region's demand. Large deployments in energy, industrial manufacturing, and commercial real estate supported this lead. The region also benefited from deep hyperscaler infrastructure, which reduced friction for multi-site cloud-based implementations. AVEVA and Amazon Web Services strengthened that position in May 2026 through a multi-year collaboration focused on industrial intelligence in the cloud, including digital twin capabilities and joint migration programs. Canada and Mexico remained smaller contributors, but supply chain transparency requirements continued to support regional expansion.

Asia-Pacific is projected to grow at 29.24% CAGR through 2031, making it the fastest-expanding geography in the digital sustainability twin platform market. China's dual-carbon policy is creating large-scale deployment opportunities, and Xinhua reported that Haier's Kaoshu COSMOPlat supported zero-carbon industrial parks with energy utilization rates above 80% and annual CO2 reductions of 32,600 tonnes per installation. Japan is also strengthening its position, and Hitachi Energy launched EcoSpace in April 2026 to visualize lifecycle environmental impacts across transmission and distribution grid infrastructure.[4]Hitachi Energy, “Hitachi Energy Launches EcoSpace Digital Platform,” Hitachi Press Release, hitachi.com India, South Korea, Australia, and New Zealand are adding momentum as industrial AI, smart building, and energy transition programs create demand for better sustainability data and asset visibility.

Europe held the second-largest regional share in 2025, and Germany, the United Kingdom, and France remained the main contributor markets. The region's strength came from regulatory density because CSRD, CBAM, the EU Taxonomy, ESPR, and supply chain due diligence rules all increased the value of auditable sustainability data across industrial value chains. France added a public-sector growth layer in April 2026 through its national digital twin program for territories, while broader regional adoption continued to benefit from strong compliance demand. South America, the Middle East, and Africa remained smaller in absolute value, but smart city programs and energy transition spending kept them relevant growth pockets. In these regions, adoption stayed more concentrated in utility, infrastructure, and public investment use cases than in broad private-sector rollouts.

Competitive Landscape

The digital sustainability twin platform market remains moderately fragmented, with large industrial software and technology vendors competing alongside specialist industrial AI firms. Siemens AG, Schneider Electric, AVEVA, Microsoft, SAP SE, and GE Vernova held strong positions in enterprise contracts because they combine software breadth with installed customer relationships. A clear strategic pattern is platform convergence, where vendors combine sustainability modeling, ESG reporting, and real-time optimization inside broader digital architectures instead of selling isolated tools. Siemens deepened this position in early 2026 through its Altair acquisition, and the combined portfolio expanded multiphysics digital twin capabilities and CO2 impact analysis within its broader software stack. This kind of consolidation can raise switching costs for customers who want fewer vendors across simulation, operations, and sustainability workflows.

Another important shift is the spread of shared simulation layers, especially as NVIDIA Omniverse integrations appeared across several industrial software offerings between 2025 and 2026. That trend supports interoperability, but it also reduces room for pure infrastructure differentiation and pushes vendors to compete more on applications, data context, deployment time, and measurable business value. Cognite is a strong example of this pressure because the company reported 465% ROI and payback periods of under 6 months on customer deployments in its Q1 2026 release.[5]Cognite, “Cognite March 2026 Release Accelerates Value Realization Across Industrial Workflows,” Cognite, cognite.com Payback claims of that kind are forcing established vendors to defend longer deployment cycles with broader functionality and deeper integration support. The digital sustainability twin platform market is therefore seeing more pressure from execution speed and value realization than from software features alone.

White space remains strongest in offerings designed for SMEs, regulated supply chains, and municipal users that need faster rollout and less customization. Bentley Systems followed a differentiated path in infrastructure, and its iTwin platform with carbon analysis won the Digital Innovation Award at the 2025 Sustainability Delivery Awards for helping engineers evaluate embodied carbon during design. Schneider Electric, AVEVA, and ETAP also moved early on interoperability in 2025 by joining the Alliance for OpenUSD, which positioned their twin offerings well for more open 3D and data exchange environments. These moves show that competition in the digital sustainability twin platform market is being shaped by standards alignment, sector fit, and delivery outcomes as much as by core software breadth. Vendors that can combine easier deployment, clearer reporting value, and stronger interoperability are likely to defend their position more effectively as adoption broadens.

Digital Sustainability Twin Platform Industry Leaders

Siemens AG

Dassault Systèmes SE

PTC Inc.

Ansys, Inc.

AVEVA Group Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Fervo Energy, NVIDIA, and Pacific Northwest National Laboratory (PNNL) announced the EGS-Twin initiative, a next-generation digital twin platform for Enhanced Geothermal Systems integrating real-time subsurface field data, physics-based modeling, and AI-driven forecasting to optimize power generation and scalability. Implementation is targeted for 2029. The collaboration leverages NVIDIA Omniverse libraries and PNNL's AI training infrastructure to advance 24/7 carbon-free geothermal power capacity.

- May 2026: SAP launched its suite of sustainability AI agents, including the Sustainability Regulatory Readiness Agent, CSRD-aligned reporting automation, and the Footprint Optimization Agent, with general availability by the end of 2026. Demonstrated outcomes include a reduction in scenario simulation time from approximately 1 day to 20 minutes and a greater than 50% decrease in packaging compliance review hours, embedding real-time ESG decision-making directly into enterprise workflows.

- May 2026: AVEVA and Amazon Web Services formalized a multi-year Strategic Collaboration Agreement to deliver industrial intelligence in the cloud, encompassing digital twin capabilities, agentic AI workflows for industrial operations, and joint customer migration programs. AVEVA's products are also listed on the AWS Marketplace under the agreement.

- April 2026: Rockwell Automation's net-zero science-based GHG emissions reduction targets received official validation from the Science Based Targets initiative, targets submitted in December 2025 and approved in April 2026. The validation covers Scope 1, 2, and 3 emissions and reinforces Rockwell's commitment to integrating sustainability into its industrial digital twin and smart manufacturing portfolio.

Global Digital Sustainability Twin Platform Market Report Scope

The digital sustainability twin platform market comprises software platforms that create, integrate, and continuously synchronize digital representations of physical assets, facilities, industrial processes, infrastructure, and enterprise operations to model, simulate, monitor, and optimize sustainability performance throughout their lifecycle. These platforms combine digital twin technology with real-time operational data, IoT connectivity, artificial intelligence (AI), simulation models, and advanced analytics to improve energy efficiency, reduce greenhouse gas (GHG) emissions, optimize resource utilization, enhance asset sustainability, and support enterprise decarbonization initiatives.

The Digital Sustainability Twin Platform Market Report is Segmented by Component (Platform, and Services), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and SMEs), End-User Industry (Industrial Manufacturing, Energy and Utilities, Buildings and Real Estate, Logistics and Transportation, Government and Smart Cities, and Other End-User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Platform |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| SMEs |

| Industrial Manufacturing |

| Energy and Utilities |

| Buildings and Real Estate |

| Logistics and Transportation |

| Government and Smart Cities |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Component | Platform | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Enterprise Size | Large Enterprises | |

| SMEs | ||

| By End-User Industries | Industrial Manufacturing | |

| Energy and Utilities | ||

| Buildings and Real Estate | ||

| Logistics and Transportation | ||

| Government and Smart Cities | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 size of the digital sustainability twin platform space?

It stands at USD 3.92 billion in 2026 and is projected to reach USD 12.84 billion by 2031 at a CAGR of 26.76%.

Which region is growing fastest through 2031?

Asia-Pacific is the fastest-growing region, with a projected CAGR of 29.24% through 2031, supported by policy-driven adoption in China and rising investment across Japan and India.

Which deployment model leads today, and which one is expanding fastest?

Cloud-based deployment led with 66.83% share in 2025, while hybrid deployment is projected to grow fastest at 31.46% CAGR through 2031.

Why are services expanding faster than platforms?

Services are projected to grow at 30.28% CAGR because companies need ongoing model calibration, scenario planning, reporting alignment, and expert support after initial platform deployment.

Which end-user group contributes the most revenue right now?

Industrial manufacturing led with 32.48% share in 2025 because energy, material, and emissions outcomes are easier to measure and tie back to ROI in plant environments.

Why are SMEs becoming more important buyers?

SMEs are projected to grow at 28.74% CAGR as cloud delivery lowers entry barriers and larger customers place more pressure on suppliers to provide structured emissions and sustainability data.

Page last updated on: