Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Digital Insurance Platform Market Report is Segmented by Deployment (Cloud, On-Premise, Hybrid), Component (Platform/Software, Services), End-User Enterprise Size (Large Enterprises, Small and Medium Enterprises), Application (Automotive and Transportation, Life and Health, Travel, and More), and Geography (North America, Europe, Asia Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

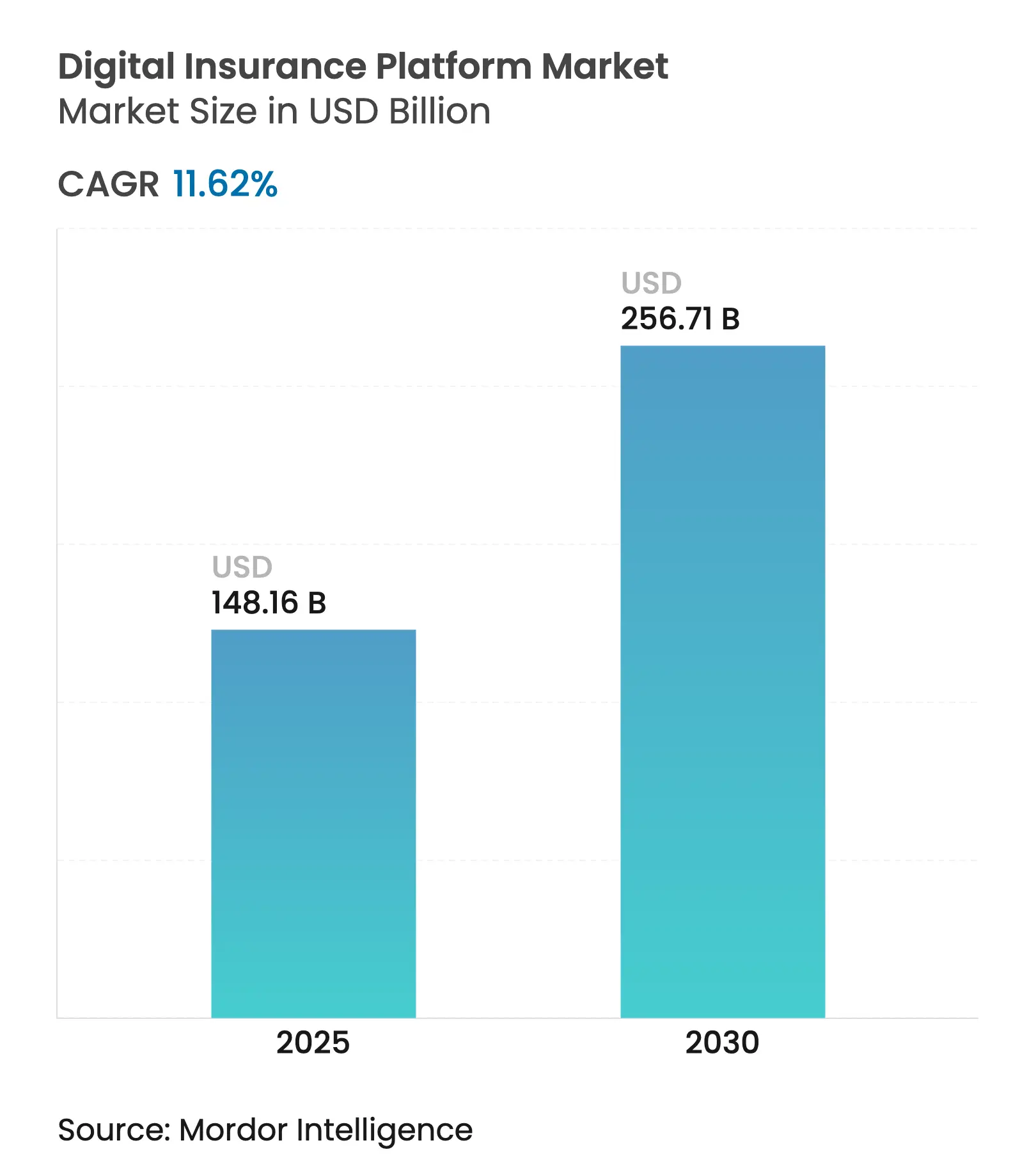

| Market Size (2025) | USD 148.16 Billion |

| Market Size (2030) | USD 256.71 Billion |

| Growth Rate (2025 - 2030) | 11.62 % CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

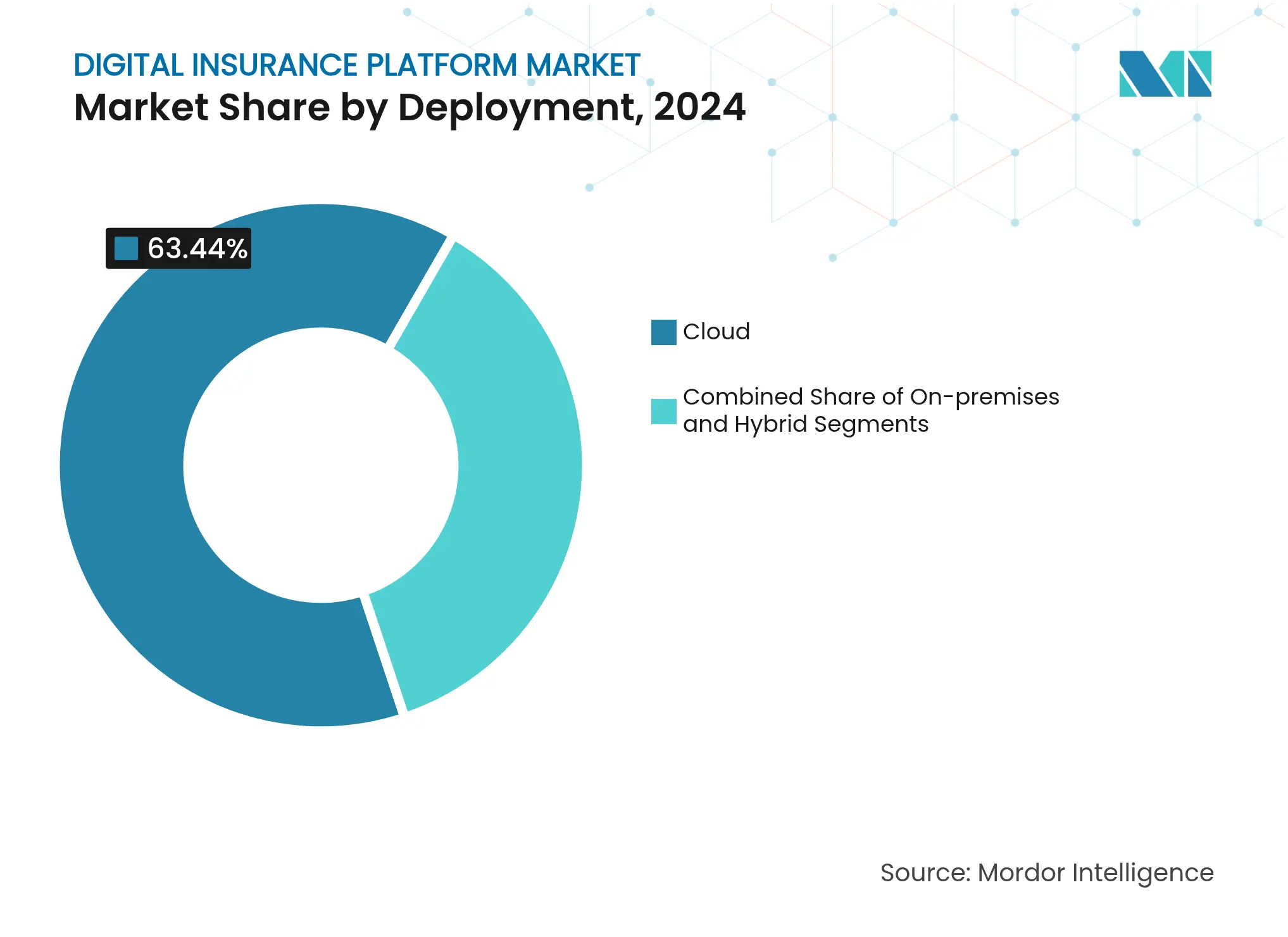

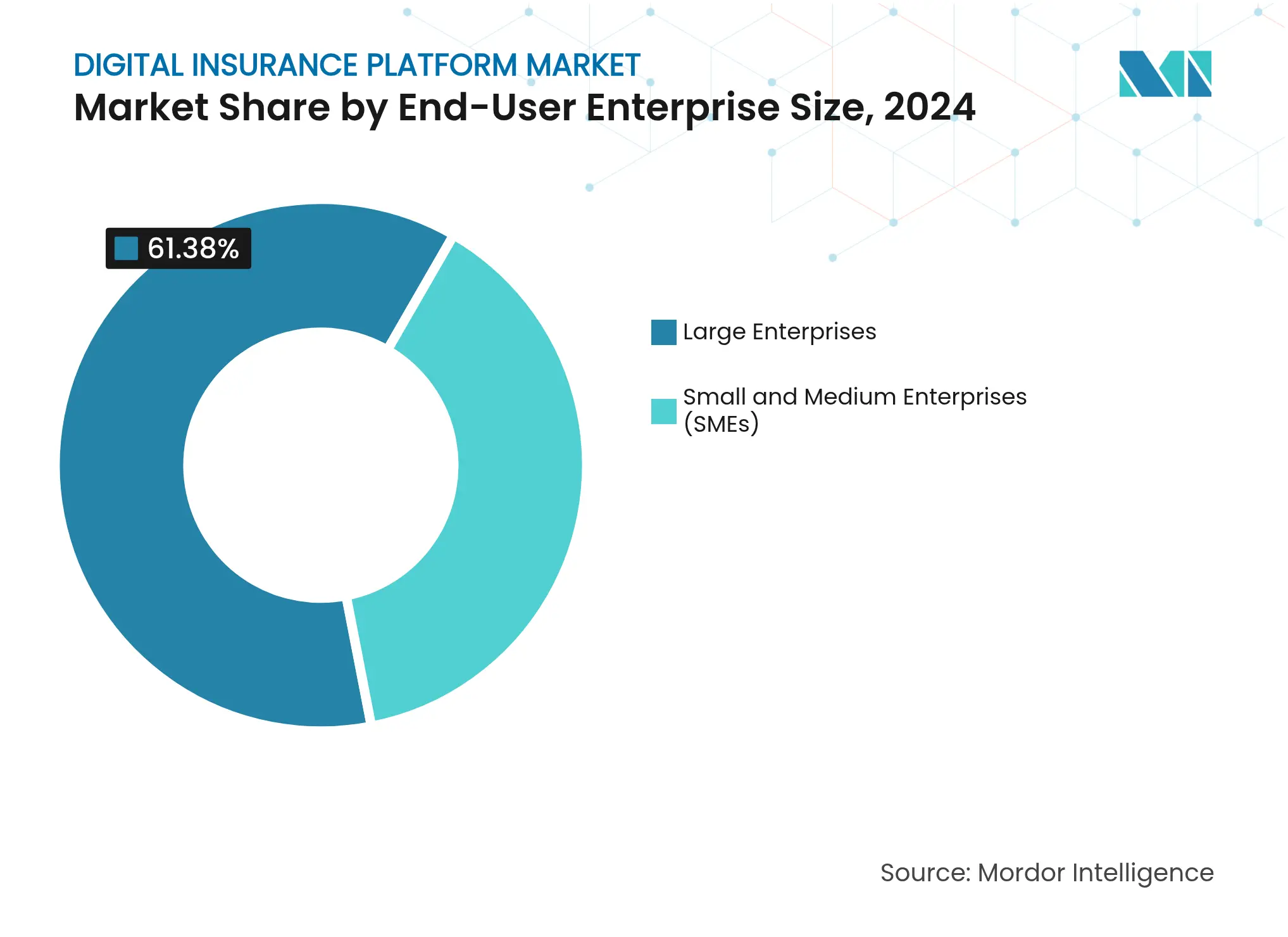

The digital insurance platform market size stands at USD 148.16 billion in 2025 and is forecast to reach USD 256.71 billion by 2030, expanding at an 11.62% CAGR over the period. Cloud deployment’s 63.44% share in 2024, the 72.71% dominance of platform and software components, and a 17.62% CAGR among small and medium enterprises (SMEs) underscore the sector’s migration from isolated tools to fully integrated ecosystems. Insurers’ urgency to modernize legacy systems, monetize data, and respond to regulatory mandates accelerates investment, while embedded insurance partnerships and generative-AI pilots reshape distribution and underwriting economics. Heightened venture funding, epitomized by Munich Re’s USD 2.6 billion purchase of NEXT Insurance, and growing API marketplaces lower time-to-market for new products, magnifying the competitive gap between digital-first carriers and lagging incumbents. At the same time, 22 U.S. states adopting NAIC AI governance frameworks signal rising compliance costs that favor early adopters able to operationalize standardized guardrails.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Customer-centric product shift

Customer-centric product shift

| +2.1% | Global; early adoption in North America and EU | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+2.1%

|

Geographic Relevance

:

Global; early adoption in North America and EU

|

Impact Timeline

:

Medium term (2-4 years)

|

Cloud adoption acceleration

Cloud adoption acceleration

| +1.8% | Global; led by North America, expanding to Asia Pacific | Short term (≤ 2 years) | |||

API-led core modernization

API-led core modernization

| +1.5% | North America and EU core; spill-over to Asia Pacific | Medium term (2-4 years) | |||

Embedded insurance demand

Embedded insurance demand

| +1.2% | Global; concentrated in North America and China | Long term (≥ 4 years) | |||

GenAI in underwriting and claims

GenAI in underwriting and claims

| +0.9% | North America and EU leading; Asia Pacific following | Medium term (2-4 years) | |||

Open-insurance sandboxes

Open-insurance sandboxes

| +0.7% | EU leading with FIDA; selective adoption in Asia Pacific | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Shift from Product-Centric to Customer-Centric Insurance Offerings

Customer-centric architectures gain momentum as 40% of U.K. policyholders switch providers after poor claims experiences, prompting insurers to re-engineer digital touchpoints [1]Nuvei. "Why UK policyholders are losing faith in insurance—and how payments can fix it." March 24, 2025. . Salesforce Customer 360 for Insurance delivered 27% marketing ROI and 32% higher sales revenue by unifying policy and claims data, confirming the payoff from holistic engagement [2]Salesforce. "Insurance Broker Solutions Datasheet." January 1, 2025. . QBE’s generative-AI rollout cut underwriting review time 65%, validating personalization at scale. Real-time preference learning creates data network effects that strengthen competitive moats, while embedded insurance integrations further entwine policies with everyday transactions. Consequently, platform procurement criteria now prioritize experimentation speed over feature checklists.

Growing Cloud Adoption Across Insurers

Cloud migrations have shifted from cost plays to strategic enablers: Guidewire’s quarterly subscription revenue rose 33% on cloud demand[3]Guidewire Software. "Guidewire Announces First Quarter Fiscal Year 2025 Financial Results." December 5, 2024. . NN Group’s two-decade mainframe overhaul cut IT platform costs 80%, illustrating the marathon nature of modernization. Multi-cloud safeguards regulatory risk, as Syntphony Insurance Distribution straddles Azure and AWS for jurisdictional compliance. First-party cloud marketplaces exemplified by Socotra’s Connected Core in AWS Marketplace compress deployment cycles and catalyze usage-based pricing models. Meanwhile, Europe’s Digital Operational Resilience Act (DORA) codifies cloud security baselines, tilting the field toward providers with mature governance.

Rapid API-Led Core Modernization Programmes

API-first designs dismantle monoliths into composable capabilities: AIG cut payment settlement from days to minutes and saved 40% staff effort after adopting OpenLegacy microservices. Bold Penguin’s API link with Salesforce enables real-time data sync and automated underwriting, shortening broker workflows [BOLDPENGUIN.COM]. Insurity’s Spreadsheet API slashed product launch cycles from months to 30 days at 83% lower cost. API ecosystems attract third-party developers, creating positive feedback loops where carriers with richer endpoints gain embedded distribution deals. Yet, legacy integration still constrains velocity, driving demand for hybrid connectors like IBM HATS that salvage multiyear CRM investments while exposing mainframe logic as REST services.

Increasing Demand for Embedded Insurance Partnerships

Embedded insurance has scaled from niche to mainstream, with gross written premiums projected at USD 722 billion by 2030. Forty percent of U.S. SMEs remain underinsured, widening the addressable market for contextual coverage. YAS and QBE’s “Pay-As-You-Sell” product links premiums to real-time e-commerce sales, illustrating dynamic risk-based pricing. Low-code tools are forecast to automate 60% of claims tasks by 2026, shrinking integration hurdles for non-insurance brands. EU FIDA regulations mandate data sharing, cementing open APIs as the backbone of future embedded ecosystems.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Legacy mainframe integration complexity

Legacy mainframe integration complexity

| -1.4% | Global; acute in North America and EU | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

-1.4%

|

Geographic Relevance

:

Global; acute in North America and EU

|

Impact Timeline

:

Medium term (2-4 years)

|

Modern insurance IT talent shortage

Modern insurance IT talent shortage

| -0.8% | Global; acute in developed markets | Long term (≥ 4 years) | |||

Rising data-privacy compliance costs

Rising data-privacy compliance costs

| -0.6% | EU leading with GDPR; expanding globally | Short term (≤ 2 years) | |||

Vendor lock-in fears for cloud-native stacks

Vendor lock-in fears for cloud-native stacks

| -0.4% | Global; higher in regulated markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Integration Complexity with Legacy Mainframes

Mainframe dependence remains the biggest technical drag: modernization programs routinely span decades as COBOL experts retire. mLogica case studies show AI-aided code conversion easing transitions but still requiring specialized skill sets. Hybrid APIs from Software AG permit incremental decoupling, yet dual-run environments inflate operational overhead and security exposure. Carriers unable to bridge legacy and digital cores face delayed product launches, undermining customer experience and regulatory reporting agility. Success stories such as AIG’s phased API layering highlight the payoff for those who tame integration risk early.

Talent Shortage in Modern Insurance IT Skills

Seventy percent of insurers reported IT skill gaps in 2024 versus 40% a decade earlier, with half the workforce nearing retirement. The U.K. alone needs 4,000 tech hires as carriers vie with fintechs for data engineers. Wilbury Stratton found 56% of brokers struggle to recruit professionals versed in both insurance logic and cloud architecture. The deficit pushes 83% of firms toward vendor partnerships or managed services, amplifying demand for turnkey platforms that mask complexity. Larger insurers invest in reskilling academies, yet SME carriers often lack resources, heightening consolidation pressure.

By Deployment: Cloud Dominance Accelerates Digital Transformation

Cloud deployments accounted for the largest slice of digital insurance platform market size, clocking 63.44% share in 2024. The segment is poised to widen its lead with an 18.62% CAGR as carriers equate scalability and AI readiness with competitive survival. Multi-cloud postures mitigate concentration risk and tether compliance to regional data-residency rules, a factor increasingly codified by regulators in Asia and Europe. Hybrid strategies bridge regulatory constraints and sunk infrastructure, yet their share shrinks as mainframe retirement gains momentum. The digital insurance platform market experiences network effects; every workload migrated strengthens provider ecosystems, lowering marginal costs and raising switching barriers.

Second-generation architectures further differentiate vendors as real-time AI model refresh, catastrophe-driven auto-scaling, and marketplace integrations come standard. Korea’s FSC roadmap explicitly permits generative-AI use on cloud infrastructure, signaling broader official acceptance that will unlock deferred migration budgets. The segment’s trajectory also reflects macro conditions: heightened cyber threats amplify the value of cloud-native security stacks, while capital markets reward carriers demonstrating OPEX flexibility and faster product iteration cycles.

Note: Segment shares of all individual segments available upon report purchase

By Component: Platform Integration Drives Market Consolidation

Platform/software holdings constituted 72.71% of digital insurance platform market share in 2024, illustrating the preference for end-to-end suites over point solutions. However, services outpace software with a 22.41% CAGR as implementation complexity and talent shortages push carriers to seek turnkey engagements. The premium commanded by integrators and managed-service providers exemplifies the market’s maturity curve; as core functionality commoditizes, value migrates to configuration, orchestration, and continuous optimization. Platforms like Salesforce Financial Services Cloud back sales pitches with mandatory partner-led implementation, evidencing the inseparability of software and services in achieving ROI.

Mature vendors increasingly embed professional-services capacity, bundling accelerators, migration toolkits, and regulatory packs. This coupling erects barriers to entry for newcomers lacking delivery benches, propelling consolidation as firms acquire specialized consultancies. Conversely, API-first startups focus on narrow but critical layers such as underwriting or billing microservices leveraging ease of integration to bypass full-suite competitions.

By End-User Enterprise Size: SME Adoption Accelerates Through Embedded Solutions

Large enterprises held 61.38% revenue in 2024 yet the SME cohort advances fastest at 17.62% CAGR, propelled by lower entry barriers and embedded partnerships. Platforms package out-of-the-box workflows, subscription pricing, and no-code configurators, enabling SME carriers to launch digital lines without multi-year capex. Walnut Insurance’s USD 3.4 million raise exemplifies capital flowing toward SME-oriented embedded models tailored to retail or gig-economy contexts. Meanwhile, large carriers continue multi-line transformations that incorporate straight-through processing, omnichannel engagement, and advanced analytics to defend market share against digital-native challengers.

The divergence necessitates dual-motion roadmaps from vendors: lightweight launches for SMEs and deep-custom programs for enterprise clients. Over time, SMEs upgrading to richer functionalities become natural expansion pathways, making land-and-expand a prevailing go-to-market tactic among platform providers.

By Application: Travel Insurance Platforms Lead Growth Recovery

Automotive and transportation remained the largest application at 24.21% revenue share in 2024, fueled by connected-vehicle data that underpins usage-based and parametric covers. Yet, travel insurance exhibits the strongest momentum at a 19.77% CAGR as cross-border tourism rebounds and parametric triggers gain consumer trust. AXA’s typhoon parametric policy with MOTOGO underscores how hyper-local risk parameters translate to differentiated products, catalyzing adoption. Life and health lines leverage machine-learning underwriting to compress application times, while B2B supply-chain platforms embed cargo and trade credit covers into procurement flows. Consumer electronics and industrial IoT coverage remain nascent but promising, hinging on sensor proliferation and standardization of real-time data feeds.

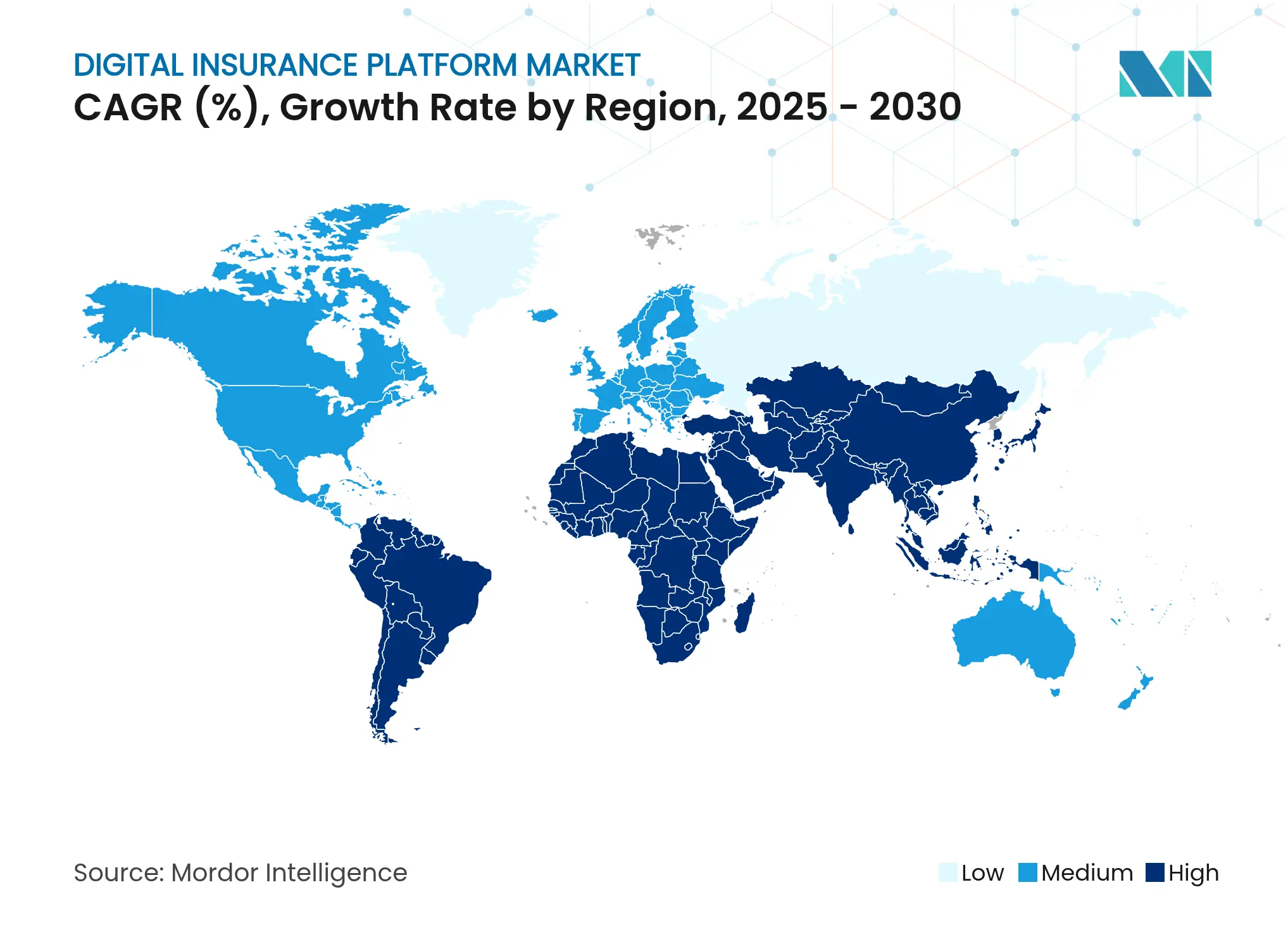

North America sustained a commanding 43.88% share in 2024, buoyed by venture funding depth, cloud incumbency, and regulatory clarity. The NAIC’s AI governance guidelines adopted by 22 states reduce compliance ambiguity and speed platform rollouts, benefitting carriers that operationalize standards early. Strategic investments such as Munich Re’s USD 2.6 billion NEXT Insurance acquisition visibly validate valuations for scale-ready insurtechs. Technology alliances Prudential with Google Cloud, Guidewire with AWS embed advanced analytics and API ecosystems that inspire follower adoption among mid-tier carriers.

Asia Pacific emerges as the fastest mover, forecast at a 16.32% CAGR through 2030 on the back of 58% year-over-year insurtech funding gains. Smartphone penetration and digital-wallet ubiquity enable leapfrog adoption of embedded micro-insurance, while governments in Singapore, China, and Thailand establish sandboxes that de-risk innovation. Korea’s relaxation of network separation underscores regional regulator willingness to balance resilience with innovation. Cross-border MandA, such as Zurich’s USD 670 million stake in Kotak General Insurance, reveals an appetite for inorganic expansion to capture addressable premium pools projected to comprise over 40% of global totals by 2029.

Europe registers steady growth, anchored by forward-leaning policy frameworks like FIDA mandating open-insurance data rails. The EU AI Act requires each member state to launch regulatory sandboxes by August 2026, spurting vendor efforts to pre-qualify models under GDPR-compliant regimes. Carriers in mature markets double-down on customer-experience differentiation as price competition intensifies. South America along with the Middle East and Africa represent longer-horizon plays where low current penetration and digital infrastructure gaps coexist with high mobile adoption, suggesting greenfield upside for cloud-native, mobile-first offerings once regulatory and capital impediments ease.

Market Concentration

Competitive intensity sits at a moderate level, characterized by an axis between broad-suite incumbents Guidewire, Duck Creek, Salesforce, Microsoft and agile disruptors specializing in APIs, underwriting bots, or embedded distribution. Market consolidation accelerates as incumbents buy capability rather than build: Munich Re’s NEXT Insurance deal and Zurich’s Kotak General stake exemplify strategic moves to anchor digital reach. Guidewire’s 27% revenue jump on cloud subscriptions illustrates how incumbents monetize migration waves, while Salesforce claims 95% adoption across surveyed insurers for its front-office stack.

Technology differentiation gravitates to AI acceleration layers: QBE’s generative-AI underwriting cut review time 65%, making operational efficiency the new battleground. Vendor lock-in fears stoke demand for interoperable solutions, pressuring providers to expose extensive APIs and multi-cloud deployment options. White-space opportunities widen around regulatory-as-code modules that auto-configure compliance, cybersecurity baselines, and ESG reporting, attracting venture capital into niche yet critical tooling.

Startups leverage capital efficiency to pursue underserved verticals: Walnut targets SMEs via embedded channels; Boost Insurance offers insurance infrastructure-as-a-service; Zopper scales policy distribution APIs across emerging markets. Although funding has cooled in some quarters, valuations remain resilient for assets exhibiting proven revenue and domain depth, signaling a sustained pipeline of strategic acquisitions among carriers, reinsurers, and cloud hyperscalers.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Digital insurance platforms support insurers by enhancing the efficiency of central-core systems and the differentiation of easy-to-compose customer experience. The digital insurance platform providers' prime responsibility is to ensure the proper deployment and integration of digital insurance solutions as per the specific requirements of clients. By type of deployment, the market is divided into on-premise and cloud. The organization size segments include large enterprise and small and medium enterprises.

The digital insurance platform market is segmented by deployment (on-premise, cloud), by organization size (large enterprise, small & medium enterprise), by application (automotive and transportation, home & commercial buildings, life & health, business & enterprise, consumer electronics & industrial machines, travel), by geography (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Wealth Management Intelligence for the Middle East

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.