Digital Mammography Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.70 Billion |

| Market Size (2031) | USD 4.30 Billion |

| Growth Rate (2026 - 2031) | 9.75% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Mammography Market Analysis by Mordor Intelligence

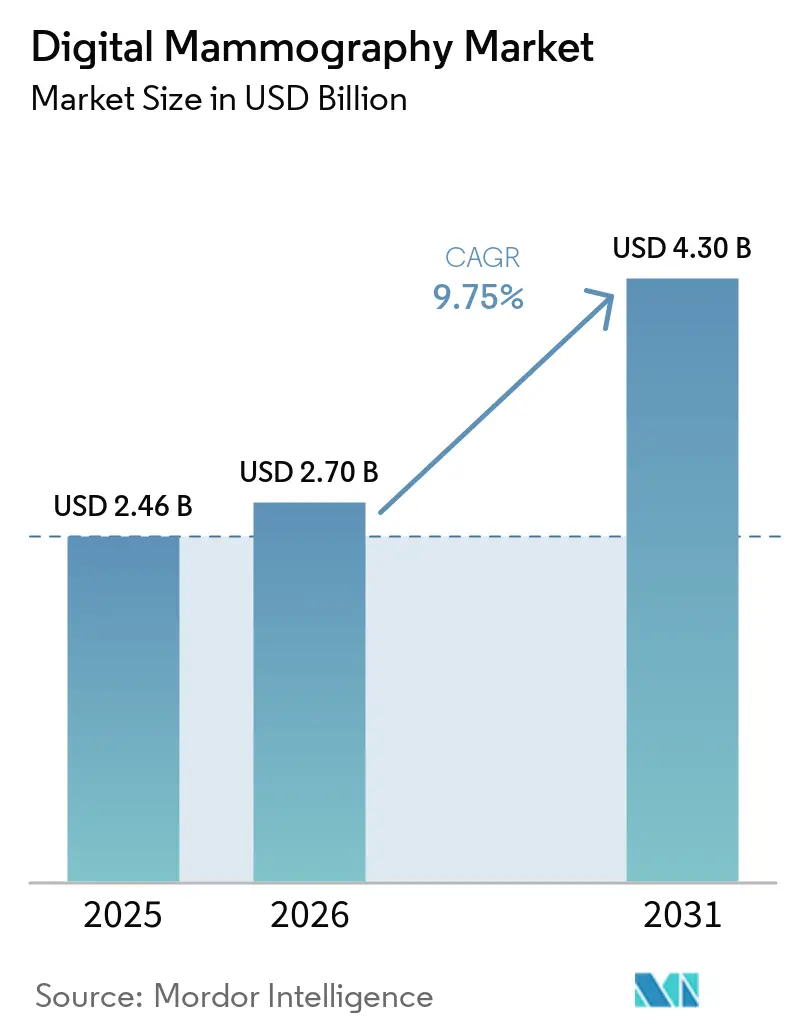

The Digital Mammography Market size is expected to grow from USD 2.46 billion in 2025 to USD 2.70 billion in 2026 and is forecast to reach USD 4.30 billion by 2031 at 9.75% CAGR over 2026-2031.

The digital mammography market is undergoing transformation driven by three key structural changes: broader screening eligibility in the United States, a transition from 2-D systems to 3-D tomosynthesis and AI-enabled platforms, and regulations reducing patient out-of-pocket costs for imaging. These factors are increasing exam volumes and driving demand for advanced systems capable of managing complex breast imaging pathways. Additionally, stronger clinical support for tomosynthesis, greater adoption of dense-breast follow-up protocols, and software tools addressing radiologist staffing challenges are further fueling market growth. Rising demand stems from both statutory screening programs and facilities aiming to lower recall rates, improve workflow efficiency, and centralize diagnostic and biopsy procedures, ensuring steady expansion across hardware, workflow software, and outpatient deployment models.

Key Report Takeaways

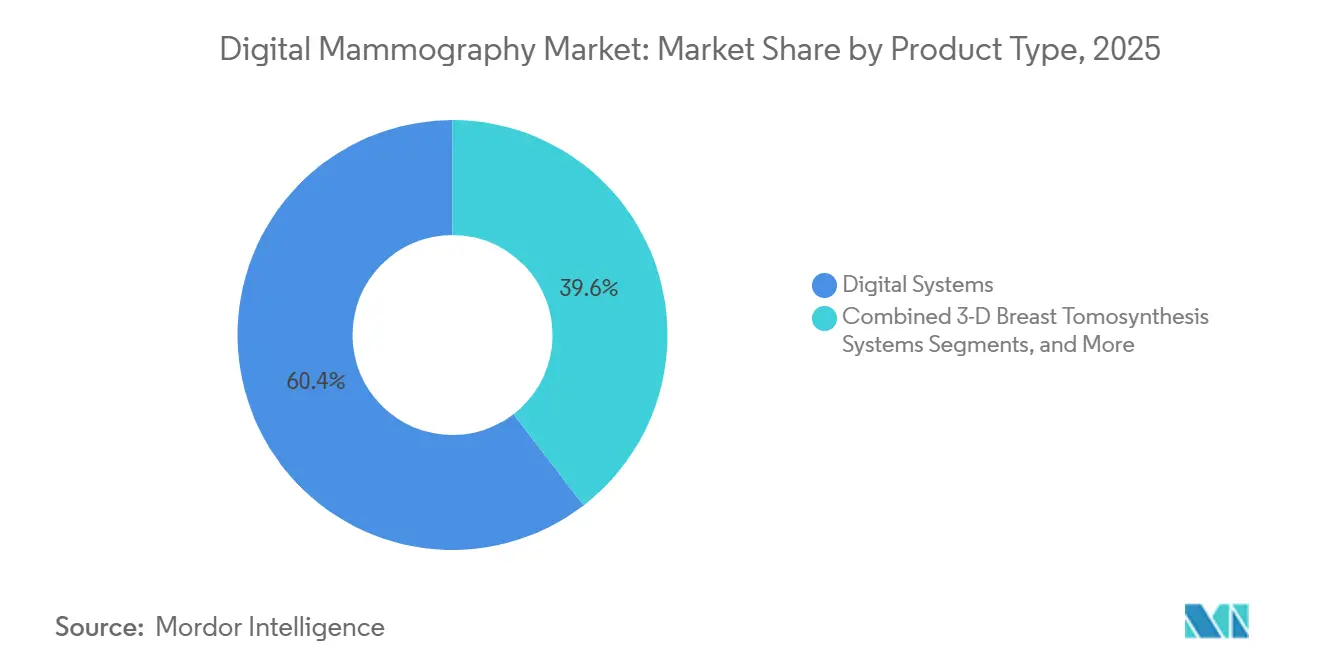

- By product type, digital systems accounted for 60.45% of revenue in 2025, while 3-D breast tomosynthesis systems are projected to expand at an 11.25% CAGR through 2031.

- By technology, 2-D full-field digital mammography held 50.9% of revenue in 2025, while photon-counting digital mammography is expected to grow at a 10.45% CAGR through 2031.

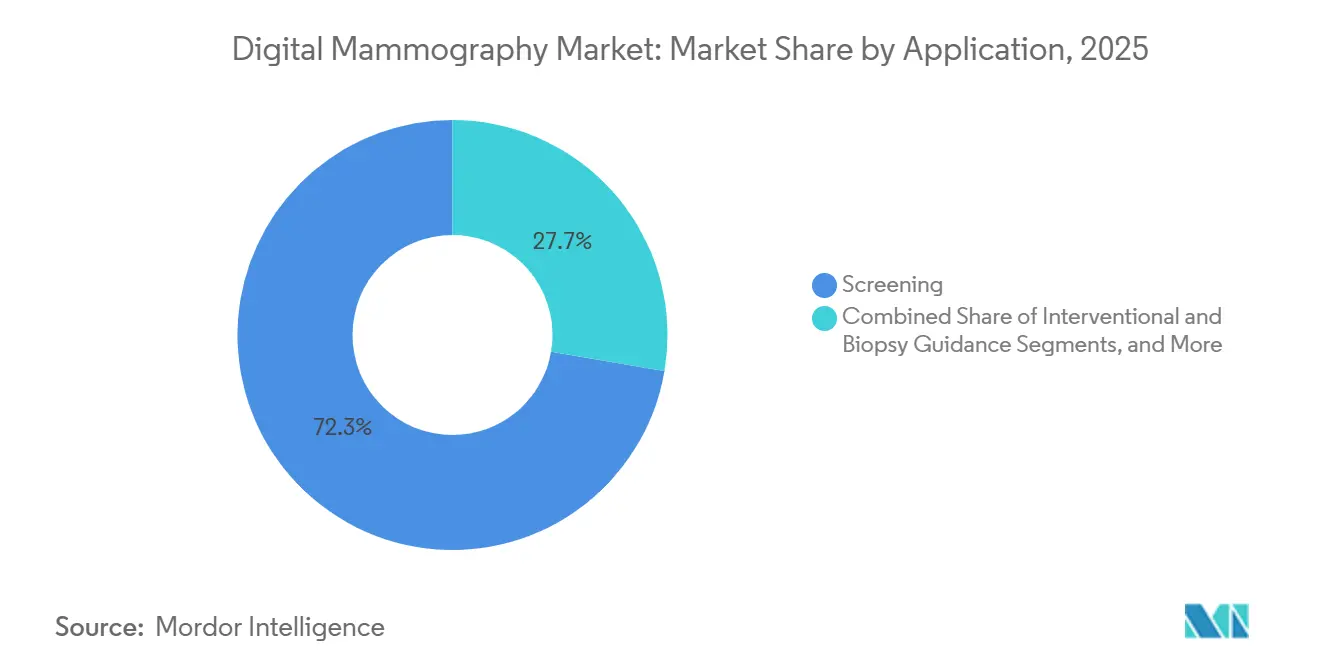

- By application, screening accounted for 72.35% of revenue in 2025, while interventional and biopsy guidance are projected to advance at a 10.78% CAGR through 2031.

- By end user, hospitals held 44.67% of revenue in 2025, while diagnostic imaging centers are projected to expand at an 11.55% CAGR through 2031.

- By geography, North America held 41.47% of revenue in 2025, while Asia Pacific are projected to expand at an 10.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Digital Mammography Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| USPSTF age-40 screening expansion | +1.5% | North America, with spillover to Canada and UK policy review | Short term (≤ 2 years) |

| 2-D to DBT replacement cycle | +1.2% | Global, led by North America and Western Europe | Medium term (2-4 years) |

| Dense-breast notification and follow-up imaging push | +0.8% | North America, with spillover to EU dense-tissue protocols | Short term (≤ 2 years) |

| AI-enabled throughput and recall reduction | +1.0% | Global, with early adoption in North America, Northern Europe, and South Korea | Medium term (2-4 years) |

| 2026 no-cost completion imaging under ACA plans | +0.7% | United States | Short term (≤ 2 years) |

| Rural access and mobile deployment economics | +0.5% | North America, APAC tier-2 and tier-3 cities, and Sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

USPSTF Age-40 Screening Expansion Adds a Structural Volume Floor

In April 2024, the U.S. Preventive Services Task Force (USPSTF) extended biennial screening mammography to women aged 40 to 74, marking a significant shift in demand for the digital mammography market. Starting screenings at age 40 could save 20% more lives compared to the previous starting age of 50, with a larger benefit for Black women, who face a 40% higher mortality rate from breast cancer than White women.[1]U.S. Preventive Services Task Force, “Breast Cancer Screening,” U.S. Preventive Services Task Force, uspreventiveservicestaskforce.org With a Grade B rating, employer health plans must provide first-dollar coverage, encouraging women in their 40s to undergo routine screenings under the Affordable Care Act. Younger screening cohorts, often with dense breast tissue, increase the operational value of Digital Breast Tomosynthesis (DBT) and AI-enhanced workflows, creating a stable volume floor for the market.

2-D to 3-D DBT Replacement Cycle Accelerates Across High-Income Markets

The digital mammography market is driven by an ongoing replacement cycle among 2-D full-field digital mammography systems. As of March 2025, 8,266 of 8,963 certified facilities in the United States had at least one accredited DBT unit, while 13,759 accredited 2-D units still slightly outnumbered 12,780 DBT units, highlighting significant upgrade potential.[2]U.S. Food and Drug Administration, “Important Information, Final Rule to Amend the Mammography Quality Standards Act,” U.S. Food and Drug Administration, fda.gov DBT is increasingly preferred for organized screenings due to its ability to reduce recalls and improve reading efficiency. Vendors offering modular upgrades instead of full replacements are well-positioned, especially in public systems and community hospitals seeking modernization without overhauling capital plans.

Dense-Breast Notification and Follow-Up Imaging Push Drives Incremental Scan Volume

The digital mammography market gained momentum when MQSA-certified facilities in the United States were required from September 10, 2024, to notify patients about breast tissue density and its implications for cancer risk and mammographic sensitivity. Updated preventive services guidance for 2026 mandates coverage for additional imaging and pathology evaluations without cost-sharing when follow-up imaging is needed. This drives more women into advanced imaging pathways, often requiring DBT systems or supplemental imaging. With a significant portion of screening-age women in the United States having dense breasts, the market benefits from sustained demand for both primary screenings and higher-value follow-up exams.

AI-Enabled Throughput and Recall Reduction Redefines Radiologist Capacity

Artificial intelligence is transforming the digital mammography market by addressing throughput challenges amid radiologist shortages. A 2026 study showed AI-primary workflows increased cancer detection by 10.4%, reduced recall rates by 0.8%, and lowered radiologist workload by 37% to 44%. A 2025 study reported a 20.6% increase in breast cancer detection with AI-supported screening, with stable or improved recall rates.[3]M. Posso et al., “Prospective Evaluation of Artificial Intelligence Integration into Breast Cancer Screening in Multiple Workflow Settings, The GEMINI Study,” Nature Cancer, springer.com Staffing shortages remain critical, with 70% of practices reporting insufficient mammography technologists in 2025. AI has become a key growth driver, enabling facilities to manage growing exam volumes while maintaining quality with limited staff.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Capital budget pressure for multi-modality upgrades | -1.2% | Global, especially public health systems in the UK, Europe, and APAC | Medium term (2-4 years) |

| Breast-imaging radiologist and technologist shortage | -1.0% | Global, strongest in North America and Western Europe | Long term (≥ 4 years) |

| MQSA audit and record-transfer compliance burden | -0.6% | United States | Short term (≤ 2 years) |

| Tariff and service-parts volatility | -0.7% | North America and selected APAC markets with import-dependent supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Capital Budget Competition Slows Multi-Modality Upgrade Cycles

Despite favorable demand, the digital mammography market faces capital allocation challenges within health systems. Mammography platforms compete with CT, MRI, and PET/CT for limited budgets, a trend that has intensified since 2024 as providers manage debt, infrastructure upgrades, and service expansions. The high lifecycle costs of DBT platforms make procurement decisions reliant on reimbursement clarity and multi-year budgets rather than clinical preferences. Facilities in rural and emerging areas experience slower upgrades due to additional costs like room shielding, power stability, and PACS connectivity, which often exceed the scanner price. While demand remains strong, these factors extend replacement cycles and push upgrades into long-term planning.

Breast-Imaging Workforce Shortage Creates a Structural Capacity Ceiling

The digital mammography market is constrained by a shortage of radiologists and technologists, limiting its ability to meet rising screening and follow-up volumes. A 2025 Journal of Breast Imaging survey reported that 70% of practices were understaffed for mammography technologists. This staffing gap means improved eligibility and reimbursement do not always translate into increased capacity. Providers are increasingly adopting workflow software, triage tools, and integrated platforms to reduce manual workloads and maintain efficient reporting times. While demand is strong, uneven operating capacity slows the pace at which providers can capitalize on new opportunities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: DBT Systems Take Share in a Digital Replacement Wave

In 2025, Digital Systems dominated the product-type revenue, claiming a substantial 60.45% share. This shift underscores the digital mammography market's decisive pivot away from its analog roots and retrofit-heavy configurations, especially in advanced imaging systems. Despite a significant installed base still featuring 2-D platforms, replacement demand remains robust in mature markets. C

3-D Breast Tomosynthesis Systems are on a rapid ascent, projected to grow at an 11.25% CAGR through 2031. Their momentum is bolstered by clinical validation, policy backing, and sound procurement rationale. As of March 2025, FDA data highlighted 12,780 accredited DBT units in the U.S., still trailing behind the 13,759 accredited 2-D digital units. This gap underscores the ongoing upgrade cycle. Facilities are increasingly drawn to DBT for its promise of fewer recalls and enhanced performance, especially in dense-breast demographics.

By Technology: Photon-Counting Emerges as the Next Platform Shift

In 2025, 2-D Full-Field Digital Mammography accounted for a significant 50.9% of technology revenue, underscoring the continued reliance on legacy digital systems for near-term procedures. This stronghold is bolstered by a widespread installed base in community and rural facilities, coupled with the operational familiarity and reimbursement of 2-D procedures in various markets. Concurrently, AI-driven CAD and image triage are enhancing both 2-D and DBT hardware performance, allowing for improvements without immediate hardware upgrades.

Photon-counting Digital Mammography is set to chart a robust trajectory, with projections indicating a 10.45% CAGR through 2031, marking it as the most rapidly advancing technology segment. Its allure lies in its detector architecture, which champions dose efficiency and spectral imaging. This ensures heightened sensitivity for detecting small invasive cancers and ductal carcinoma in situ, making it particularly relevant for younger screening demographics and sophisticated contrast workflows. Internationally, there's a burgeoning interest, with early installations and clinical applications in several European and Asian markets signaling a shift from mere trial-stage curiosity.

By Application: Screening Dominates, Biopsy Guidance Accelerates

Screening, accounting for a commanding 72.35% of application revenue in 2025, solidified its status as the cornerstone of the digital mammography market. This dominance is anchored in statutory screening initiatives, payer-supported preventive care, and the fundamental role of screening as the gateway to most imaging pathways. The April 2024 USPSTF endorsement expanded the eligible screening demographic to encompass women aged 40 to 74, bolstering the trajectory of routine screening demand.

Interventional and Biopsy Guidance is witnessing the swiftest growth, with projections indicating a 10.78% CAGR through 2031. This surge is attributed to a growing preference among facilities to consolidate detection and tissue confirmation within a single visit. Such a shift aligns with care models aimed at minimizing delays, enhancing patient retention, and maximizing value for outpatient and specialty breast centers.

By End User: Ambulatory Channels Gain Ground on Hospital Anchors

In 2025, hospitals commanded a notable 44.67% of end-user revenue, solidifying their position as the primary procurement channel in the digital mammography landscape. Their dominance is attributed to the necessity of lead-lined rooms, integrated PACS, specialized personnel, and the capability to navigate diagnostic complexities, biopsies, and high-acuity imaging services.

Diagnostic Imaging Centers are emerging as the fastest-growing segment, with an impressive projected growth rate of 11.55% CAGR through 2031. Their ascent in the digital mammography arena is largely due to payer preferences shifting towards more economical outpatient care venues. These centers excel in high-throughput screening, AI-assisted readings, and adaptable scheduling, enabling them to efficiently manage routine demands—often outpacing many hospital departments. Moreover, specialty breast centers and office-based models are gravitating towards same-day service offerings.

Geography Analysis

North America accounted for 61.11% of global revenue in 2025, driven by robust federal funding. North America holds the largest share of the digital mammography market, driven by well‑established breast cancer screening programs, strong reimbursement frameworks, and rapid adoption of advanced technologies like 3D tomosynthesis and AI‑assisted diagnostics. The U.S., in particular, benefits from FDA approvals and insurance coverage that encourage hospitals and imaging centers to upgrade from analog to digital systems. High awareness levels and government initiatives further reinforce market dominance, though equipment costs remain a challenge for smaller clinics.

Europe represents a mature market with widespread adoption supported by national screening programs in countries such as Germany, France, and the UK. The region emphasizes early detection and quality standards, with structured reimbursement policies ensuring accessibility.

The Middle East is an emerging market for digital mammography, with countries like Saudi Arabia and the UAE investing heavily in modern diagnostic infrastructure. Growth is fueled by rising breast cancer incidence, government‑backed awareness campaigns, and partnerships with international healthcare providers.

Competitive Landscape

The digital mammography market remains moderately concentrated at the hardware level, with Hologic, GE HealthCare, and Siemens Healthineers leading through platform breadth, long-term service contracts, and integration with imaging IT systems. Switching costs in mammography extend beyond hardware to include workflow retraining, PACS compatibility, reporting standards, and service continuity. This strengthens the position of incumbent OEMs as facilities replace 2-D systems or add higher-end DBT capacity.

The software segment is creating opportunities for specialized players. GE HealthCare expanded its collaboration with DeepHealth in April 2026 to distribute new AI Breast Suite applications, showcasing how OEMs enhance workflow value through partnerships. Lunit announced FDA clearance for its Version 1.2 algorithm for 3-D mammography AI in April 2026 and reported a presence in over 330 sites across the Americas, emphasizing the role of vendor-neutral AI. ScreenPoint Medical raised USD 16 million in April 2026, with strategic backing from Siemens Healthineers, highlighting the potential for specialized breast AI platforms to scale.

Opportunities exist in photon-counting spectral imaging, long-term risk stratification, and connectivity models for mobile and rural screening programs. As regulatory standards for AI tools rise, better-funded vendors with strong clinical validation, scalable deployment, and regulatory expertise are positioned to succeed, while hardware price competition alone is unlikely to drive market leadership.

Digital Mammography Industry Leaders

GE HealthCare

Siemens Healthineers AG

Canon Medical Systems Corporation

Hologic, Inc.

FUJIFILM Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: GE HealthCare expanded its partnership with DeepHealth to globally distribute AI-powered Breast Suite applications, enhancing cancer detection, density assessment, and workflow prioritization.

- April 2026: Lunit surpassed 330 screening sites and 1 million annual mammograms in the Americas, securing FDA clearance for its Version 1.2 3-D mammography AI algorithm.

- April 2026: ScreenPoint Medical raised USD 16 million, including investment from Siemens Healthineers, to advance its Transpara Breast AI platform, which processed over 12 million mammograms across 30+ countries.

- April 2026: Quibim and Vara partnered to integrate Vara's AI mammography platform into Spain's national screening program, combined with Quibim's QP Breast diagnostic tool.

- April 2026: GE HealthCare acquired Intelerad for USD 2.3 billion to strengthen its cloud-first imaging platform for ambulatory and specialty-center channels.

Global Digital Mammography Market Report Scope

As per the scope of the report, digital mammography (full-field digital mammography or FFDM) is an FDA-approved breast imaging method. It replaces traditional X-ray film with solid-state detectors that convert X-rays into electrical signals. This produces high-resolution computer images that can be enhanced, magnified, or easily stored to aid in early breast cancer detection.

The Digital Mammography Market is segmented by product type, technology, application, end-user, and geography. By product type, the market includes digital systems, 3-D breast tomosynthesis systems, contrast-enhanced mammography systems, and computed-radiography retrofit kits. By technology, the market is segmented into 2-D full-field digital mammography, 3-D digital breast tomosynthesis, AI-enabled CAD and image triage, and photon-counting digital mammography. By application, the market is categorized into screening, diagnostic, and interventional and biopsy guidance. By end-user, the market is segmented into hospitals, diagnostic imaging centers, ambulatory surgical centers, office-based and specialty breast centers, and mobile screening programs. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Digital Systems |

| 3-D Breast Tomosynthesis Systems |

| Contrast-Enhanced Mammography Systems |

| Computed-Radiography Retrofit Kits |

| 2-D Full-Field Digital Mammography |

| 3-D Digital Breast Tomosynthesis |

| AI-enabled CAD and Image Triage |

| Photon-counting Digital Mammography |

| Screening |

| Diagnostic |

| Interventional and Biopsy Guidance |

| Hospitals |

| Diagnostic Imaging Centers |

| Ambulatory Surgical Centers |

| Office-based and Specialty Breast Centers |

| Mobile Screening Programs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Digital Systems | |

| 3-D Breast Tomosynthesis Systems | ||

| Contrast-Enhanced Mammography Systems | ||

| Computed-Radiography Retrofit Kits | ||

| By Technology | 2-D Full-Field Digital Mammography | |

| 3-D Digital Breast Tomosynthesis | ||

| AI-enabled CAD and Image Triage | ||

| Photon-counting Digital Mammography | ||

| By Application | Screening | |

| Diagnostic | ||

| Interventional and Biopsy Guidance | ||

| By End User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Ambulatory Surgical Centers | ||

| Office-based and Specialty Breast Centers | ||

| Mobile Screening Programs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the digital mammography market?

The digital mammography market stands at USD 2.70 billion in 2026 and is forecast to reach USD 4.30 billion by 2031, growing at a 9.75% CAGR over 2026 to 2031.

Why is 3-D breast tomosynthesis growing faster than other product categories?

3-D Breast Tomosynthesis Systems are projected to grow at an 11.25% CAGR through 2031 because facilities continue to replace 2-D systems, and DBT offers stronger clinical performance in dense-breast and high-volume screening workflows.

Which application drives the largest revenue in breast imaging systems?

Screening remained the largest application, accounting for 72.35% of revenue in 2025, because national screening programs and preventive care mandates continue to anchor exam volume.

Which end-user group is expanding the fastest in digital mammography?

Diagnostic Imaging Centers are projected to grow at an 11.55% CAGR through 2031 as payers shift more routine screening toward lower-cost outpatient settings with high-throughput imaging capacity.

Why is North America leading revenue in this space?

North America leads because of its large installed base, favorable reimbursement environment, and policy support from the USPSTF screening expansion and no-cost completion imaging rules.

How is AI changing breast imaging workflows?

AI is helping providers improve detection and manage staffing shortages. The GEMINI study showed a 10.4% increase in cancer detection and a 37% to 44% reduction in projected radiologist workload in AI-primary workflows.

Page last updated on: