Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

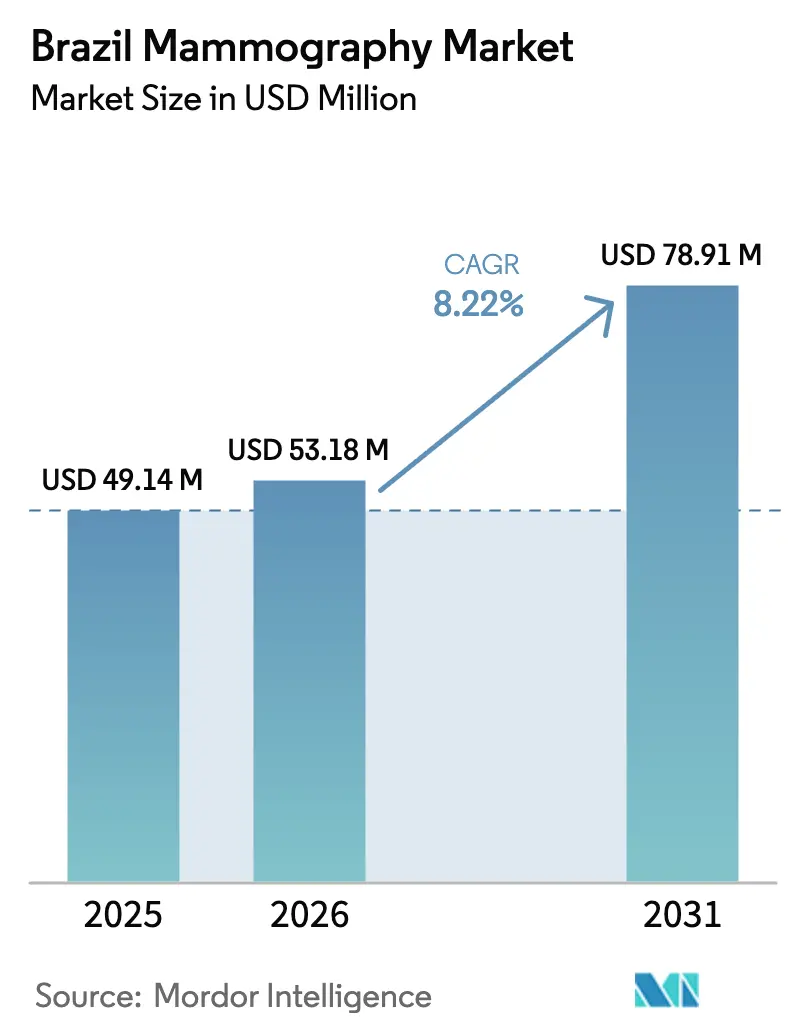

| Base Year Market Size (2025) | USD 49.14 Million |

| Market Size (2026) | USD 53.18 Million |

| Market Size (2031) | USD 78.91 Million |

| Growth Rate (2026 - 2031) | 8.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Mammography Market Analysis by Mordor Intelligence

The Brazil mammography market size is expected to grow from USD 49.14 million in 2025 to USD 53.18 million in 2026 and is forecast to reach USD 78.91 million by 2031 at 8.22% CAGR over 2026-2031. The near-double-digit growth reflects the government’s multi-year investment program in the domestic health industrial complex, the rapid conversion of analog equipment to digital and tomosynthesis platforms, and the steady roll-out of nationwide screening initiatives under the Unified Health System (SUS). Accelerated product approvals under ANVISA’s RDC 751/2022 are shortening time-to-market for imported systems, enabling global vendors to release new models tailored for local clinical workflows. Private-sector reimbursement for 3-D breast tomosynthesis and AI-assisted reporting is catalyzing an upgrade cycle among high-volume diagnostic chains, while mobile screening programs are closing access gaps in remote municipalities. These intertwined factors create a scalable, technology-centered growth trajectory for the Brazil mammography market.

Key Report Takeaways

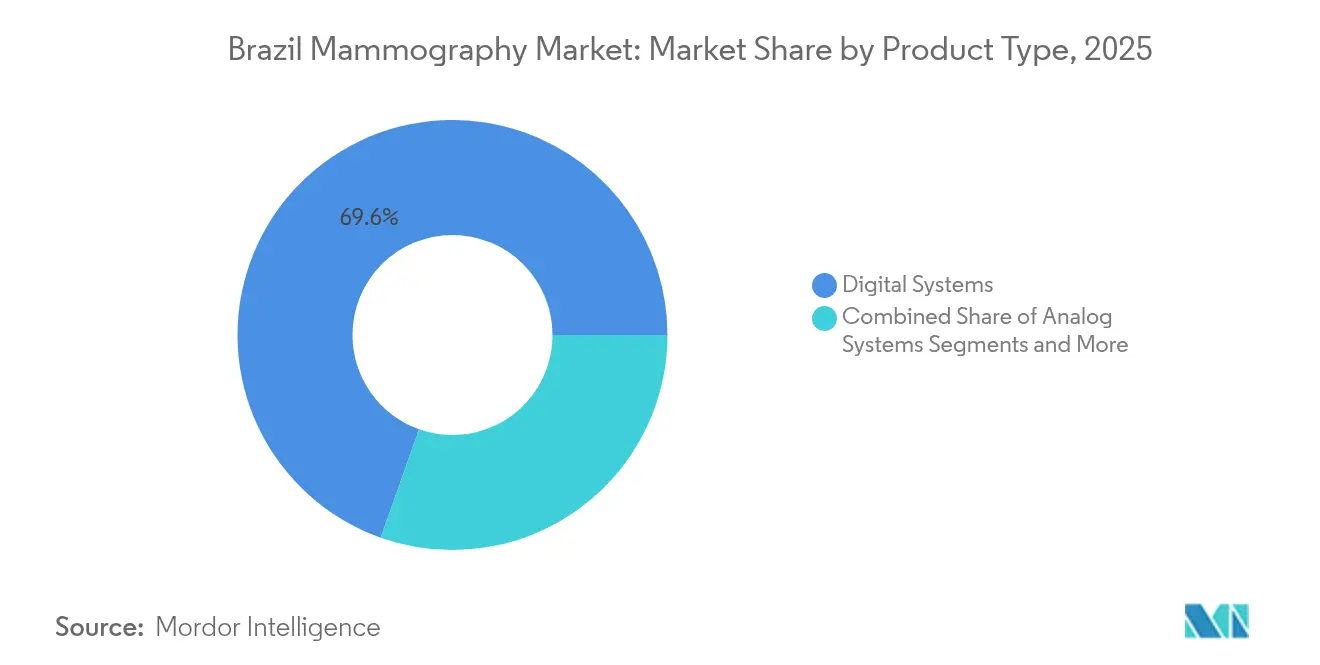

- By product type, digital systems led with a 69.58% Brazil mammography market share in 2025, while breast tomosynthesis is forecast to advance at a 9.31% CAGR through 2031.

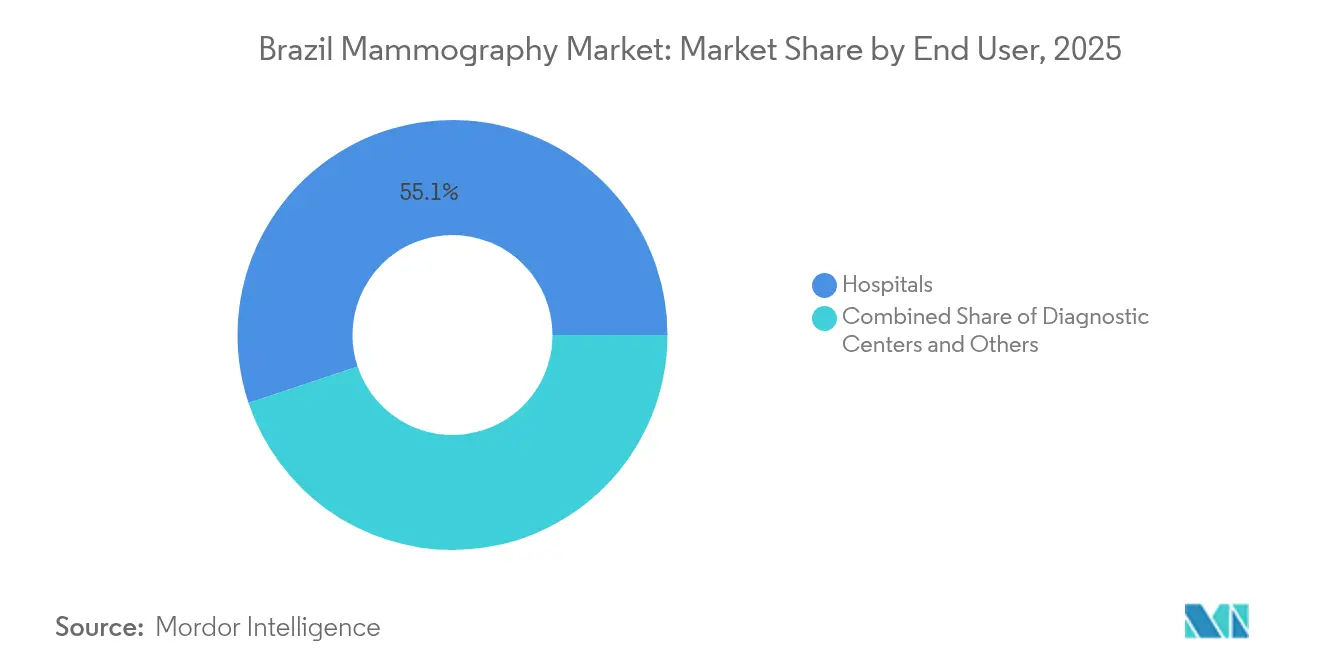

- By end user, hospitals accounted for 55.12% of the Brazil mammography market size in 2025; diagnostic centers are projected to post the fastest 9.58% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Mammography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of breast cancer | +2.1% | National, with higher impact in Southeast and South regions | Long term (≥ 4 years) |

| Roll-out of government-funded nationwide screening programs | +1.8% | National, prioritizing North and Northeast regions | Medium term (2-4 years) |

| Rapid private-sector conversion from analog to digital/tomosynthesis | +2.3% | Southeast and South regions, expanding to Northeast | Short term (≤ 2 years) |

| Reimbursement expansion for 3-D tomosynthesis | +1.2% | National, with early adoption in private healthcare | Medium term (2-4 years) |

| AI-powered CAD tools improving radiologist productivity | +1.4% | Major urban centers, expanding to regional hubs | Short term (≤ 2 years) |

| Mobile screening units reaching underserved regions | +0.5% | North and Northeast regions, rural areas nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing burden of breast cancer

The annual incidence of 73,610 new female breast cancer cases in 2023 and the notification that 1 in 3 diagnoses occurs in women under 50 are expanding the target cohort for routine imaging[1]Instituto Nacional de Câncer, “Estatísticas de câncer,” INCA.GOV.BR. Clinical societies now recommend lowering the SUS screening entry age to 40, potentially enlarging the eligible population by 40%. Higher late-stage detection in SUS-dependent regions is sharpening the political focus on earlier diagnosis, pushing capital spending on imaging infrastructure. Together, these epidemiological and policy forces lift baseline demand across all product classes within the Brazil mammography market.

Roll-out of government-funded nationwide screening programs

PAC Saúde 2025 assigns USD 1.8 billion for 180,000 new health-equipment units, earmarking mammography systems for basic clinics in underserved zones. São Paulo’s “Mulheres de Peito” allows women aged 50-69 to self-schedule exams, and its mobile fleet conducted more than 24,000 screenings across 47 towns in 2023. The new oncology navigation rule (Portaria 6,592/2025) mandates rapid routing from suspicion to treatment, indirectly lifting imaging throughput. These central and state programs institutionalize volume and underpin the future base of the Brazil mammography market.

Rapid private-sector conversion from analog to digital/tomosynthesis

Private chains like Beneficência Portuguesa and Hospital da Baleia spent over USD 1.2 million per site to install digital units, lifting monthly capacity by 177% and raising diagnostic referrals by 16%. With analog systems nearing obsolescence, replacement purchasing is front-loaded into 2025-2027 budgets. Competitive positioning, higher patient throughput, and synergy with AI workflows accelerate capital cycles, sustaining premium equipment demand inside the Brazil mammography market.

Reimbursement expansion for 3-D tomosynthesis

ANS coparticipation rules cap patient out-of-pocket costs at 40%, moderating price sensitivity for advanced imaging. Peer-reviewed economic studies confirm tomosynthesis plus synthetic views is cost-effective under Brazilian practice patterns, strengthening payer acceptance. However, sustained underwriting losses of USD 18 billion at health plans between 2021-2023 necessitate selective benefit expansion, confining early tomosynthesis adoption to higher-tier products. Even so, reimbursement clarity continues to reinforce the upgrade pipeline of the Brazil mammography market.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Radiologist shortage outside Tier-1 metros | -1.1% | North and Northeast regions, interior municipalities | Long term (≥ 4 years) |

| Capital-equipment budget freeze in public hospitals | -0.8% | National, particularly affecting SUS-dependent regions | Medium term (2-4 years) |

| Concerns over cumulative radiation dose in repeat screening | -0.4% | National, affecting screening frequency recommendations | Medium term (2-4 years) |

| Logistical barriers for mobile units in North & Northeast | -0.3% | North and Northeast regions, remote rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Radiologist shortage outside tier-1 metros

Only 15% of board-certified breast imagers practice in the North and Northeast, constraining throughput despite rising equipment availability. Federal incentives totaling USD 86 million under the “Agora Tem Especialistas” program aim to relocate physicians, yet take-up remains slow [2]Governo Federal, “Agora Tem Especialistas,” SECOM.GOV.BR . The mismatch between technology deployment and specialist distribution tempers capacity expansion and slows adoption curves in remote markets within the Brazil mammography market.

Capital-equipment budget freeze in public hospitals

Municipal hospitals faced a 12-month freeze on discretionary purchases in 2024, delaying planned replacements and lengthening analog equipment life cycles. PAC Saúde 2025 reallocates federal funds to bypass local constraints, but procurement cycles remain elongated, creating drag in the public slice of the Brazil mammography market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Transformation Accelerates Tomosynthesis Adoption

Digital systems controlled 69.58% of the Brazil mammography market in 2025 owing to superior image quality, PACS integration, and lower radiation exposure. The Brazil mammography market size for breast tomosynthesis is expected to expand at a 9.31% CAGR, propelled by false-positive reductions of up to 40% and enhanced lesion visibility in dense breasts . Analog units linger mainly in lower-income municipalities but are slated for replacement under federal équipement grants. Contrast-enhanced mammography and molecular breast imaging occupy nascent, high-margin niches in premium private hospitals.

Growing AI adoption multiplies the clinical value of digital platforms. Implementations at Beneficência Portuguesa achieved 97% diagnostic accuracy, illustrating how software upgrades leverage installed hardware to lift clinical performance and reimbursement potential. ANVISA’s RDC 611/2022 quality-assurance mandates favor facilities that invest in compliant digital technology, locking in further share gains for the digital segment within the Brazil mammography market.

By End User: Diagnostic Centers Drive Market Expansion

Hospitals captured 55.12% of the Brazil mammography market share in 2025, anchored by integrated oncology services and established referral pipelines. Yet diagnostic centers are slated to grow at 9.58% CAGR through 2031, buoyed by outpatient convenience, lower procedure costs, and quicker appointment cycles. The Brazil mammography market size attributable to diagnostic centers could double over the forecast period as chains scale nationwide and leverage AI to offset radiologist shortages.

Investments such as dr.consulta’s USD 4.0 million partnership with Canon Medical spotlight the sector’s appetite for cutting-edge imaging. Rede D'Or’s network of 1,000 outpatient units further merges hospital and diagnostic settings, creating hybrid models that sustain volume and diversify payer exposure. Mobile screening vans, aggregated under the “Others” category, extend reach to rural populations and amplify the total addressable base for the Brazil mammography market.

Geography Analysis

Regional contrasts define market opportunity. The Southeast performed 1.86 million SUS screening mammograms in 2022 versus 141,000 in the North, a 13-fold gap illustrating infrastructure concentration. São Paulo routinely pilots new service-delivery models, such as self-scheduled screening and AI-enabled reading, creating demonstration effects adopted by neighboring states. The South boasts the highest per-capita screening, reflecting higher household incomes and dense private-insurance coverage, factors that underpin premium system sales in the Brazil mammography market.

The North and Northeast embody latent growth. PAC Saúde 2025 directs USD 22 million to Amazonas and USD 21 million to Maranhão for equipment roll-outs, laying the hardware foundation where patient travel distances average 448 km for oncology care. FNE development funding of USD 8.7 billion for small businesses in 2024 catalyzes private imaging startups in secondary cities, further diversifying service supply. These policy and financing levers collectively prime the Brazil mammography market for outsized regional catch-up.

Competitive Landscape

The Brazil mammography market exhibits moderate concentration. Global manufacturers—Hologic, GE Healthcare, Siemens Healthineers—collectively hold the lion’s share of installed capacity, leveraging broad portfolios and in-country service networks. ANVISA’s RDC 751/2022 plus IN 290/2024 acceptance of FDA and Health Canada approvals trims lead times and encourages rapid model refreshes, as displayed by GE’s Pristina Via™ and Hologic’s Genius AI Detection PRO launches in 2025.

Competitive intensity is shifting from hardware to integrated AI ecosystems. Lunit’s CAD platform now screens 1 million mammograms annually across more than 200 U.S. sites and is being localized for Portuguese workflows, highlighting software-driven expansion strategies.

Domestic innovators like Huna target non-imaging biomarkers, widening the diagnostic funnel and redefining market boundaries. Service differentiation through turnkey cloud reporting, zero-click acquisition, and mobile workflows is fast becoming the principal battleground in the Brazil mammography market.

Brazil Mammography Industry Leaders

GE Healthcare

Siemens AG

Planmed OY

Hologic Inc.

Fujifilm Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Fujifilm showcased its complete imaging portfolio, highlighting mammography advances, at the Hospitalar 2025 trade fair in São Paulo.

- January 2025: Paige expanded use of its AI diagnostic suite across Oncoclínicas’ nationwide network to improve breast-pathology workflows.

- March 2024: CureMetrix received ANVISA clearance for cmAngio, an AI SaMD that flags breast arterial calcifications on FFDM and tomosynthesis images.

Brazil Mammography Market Report Scope

As per the scope of the report, mammography refers to a standard diagnostic and screening technique that is used to screen breast tissues to check the presence of a malignant tumor. The process involves the usage of low-energy X-rays for the early detection of breast cancer. Brazil Mammography Market is segmented by Product Type (Digital Systems, Analog Systems, Breast Tomosynthesis, and Other Product Types), End Users (Hospitals, Specialty Clinics, and Diagnostic Centers). The report offers the value (in USD million) for the above segments.

By Product Type

| Digital Systems |

| Analog Systems |

| Breast Tomosynthesis |

| Other Product Types |

By End User

| Hospitals |

| Diagnostic Centers |

| Others |

| By Product Type | Digital Systems |

| Analog Systems | |

| Breast Tomosynthesis | |

| Other Product Types | |

| By End User | Hospitals |

| Diagnostic Centers | |

| Others |

Key Questions Answered in the Report

How big is the Brazil Mammography Market?

The Brazil Mammography Market size is expected to reach USD 53.18 million in 2026 and grow at a CAGR of 8.22% to reach USD 78.91 million by 2031.

How fast are mammography equipment revenues expected to expand in Brazil?

Sales are projected to grow at a 8.22% CAGR between 2026 and 2031.

Who are the key players in Brazil Mammography Market?

GE Healthcare, Siemens AG, Planmed OY, Hologic Inc. and Fujifilm Holdings Corporation are the major companies operating in the Brazil Mammography Market.

Where is the fastest end-user growth coming from?

Diagnostic centers are on track for a 9.58% CAGR through 2031.

Page last updated on: