Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

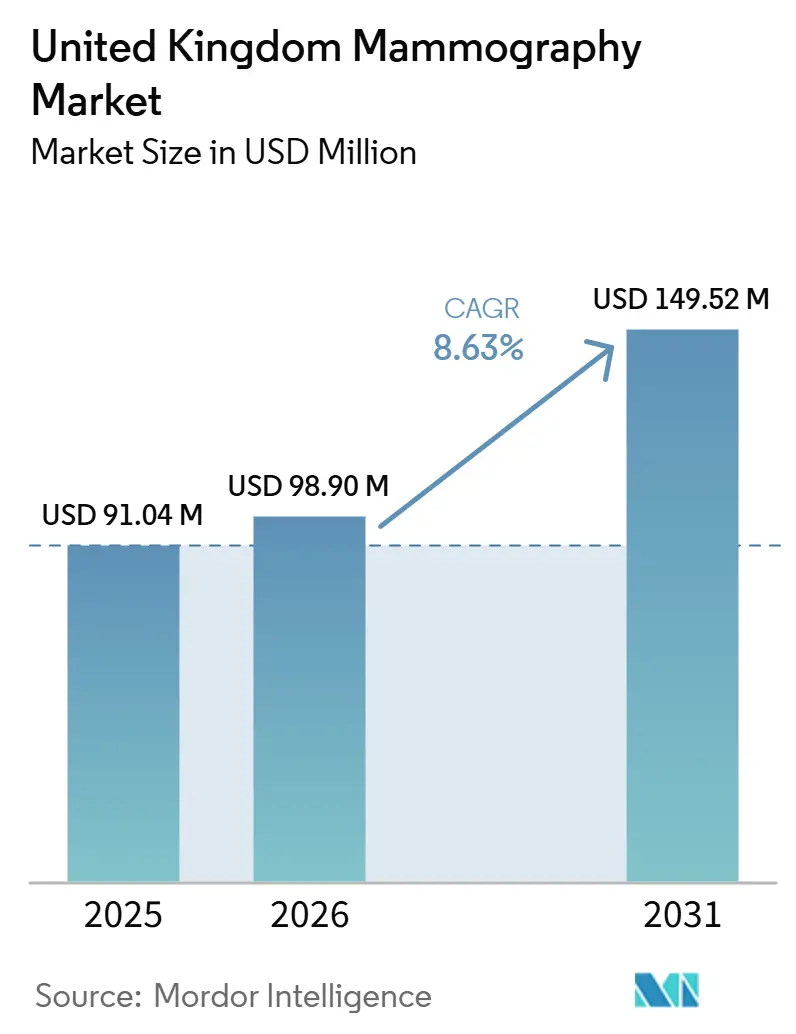

| Base Year Market Size (2025) | USD 91.04 Million |

| Market Size (2026) | USD 98.90 Million |

| Market Size (2031) | USD 149.52 Million |

| Growth Rate (2026 - 2031) | 8.63% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Mammography Market Analysis by Mordor Intelligence

The United Kingdom Mammography Market size is projected to expand from USD 91.04 million in 2025 and USD 98.90 million in 2026 to USD 149.52 million by 2031, registering a CAGR of 8.63% between 2026 to 2031.

Rising breast cancer incidence, continued expansion of the NHS Breast Screening Programme, and rapid technology upgrades combine to accelerate equipment demand. Hospitals and community diagnostic centers are expanding installed bases to maintain service standards amid a nationwide shortage of radiographers. Breakthroughs in 3-D breast tomosynthesis and artificial-intelligence-driven image analysis now form the core differentiation points for manufacturers competing to meet NHS performance specifications. Regulatory certainty from upcoming MHRA reforms and the government’s commitment to faster device approvals further support growth, even as capital-budget pressure pushes trusts toward leasing and managed-service agreements.

Key Report Takeaways

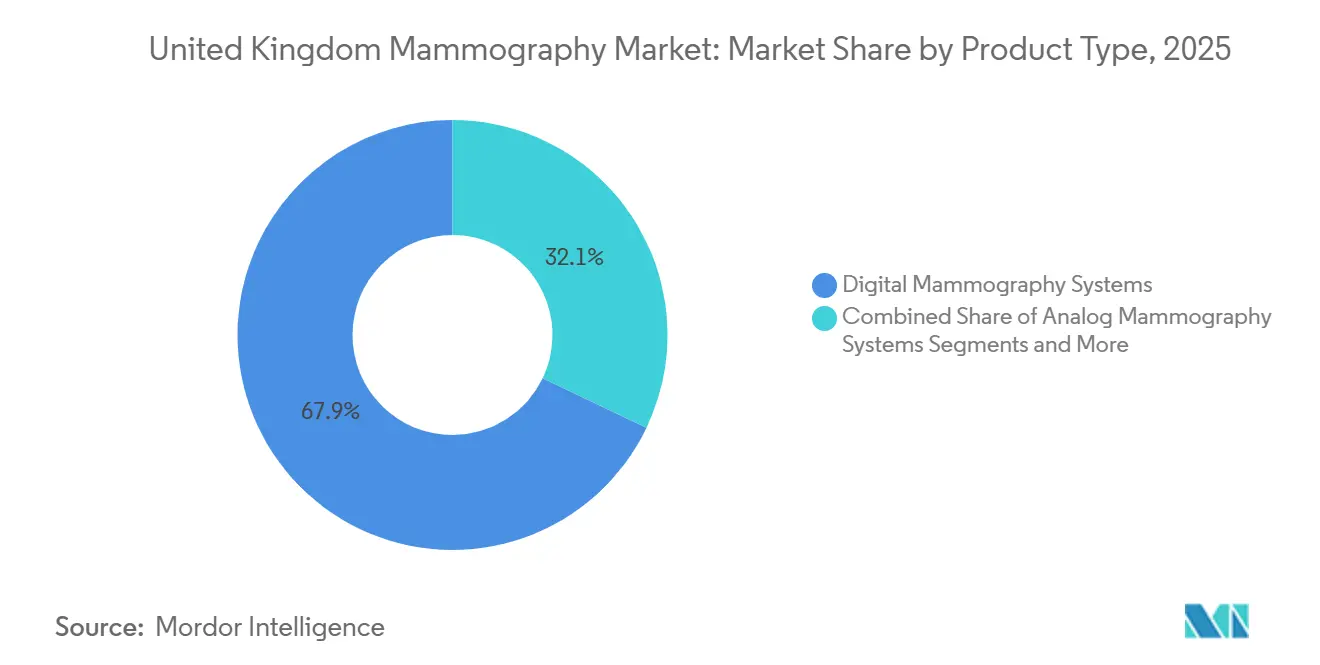

- By product type, digital systems led with 67.90% of United Kingdom mammography market share in 2025, while breast tomosynthesis systems are projected to expand at a 9.29% CAGR through 2031.

- By technology, 3-D mammography commanded 56.70% share of the United Kingdom mammography market size in 2025; 2-D mammography is expected to grow at a 9.03% CAGR over 2026-2031.

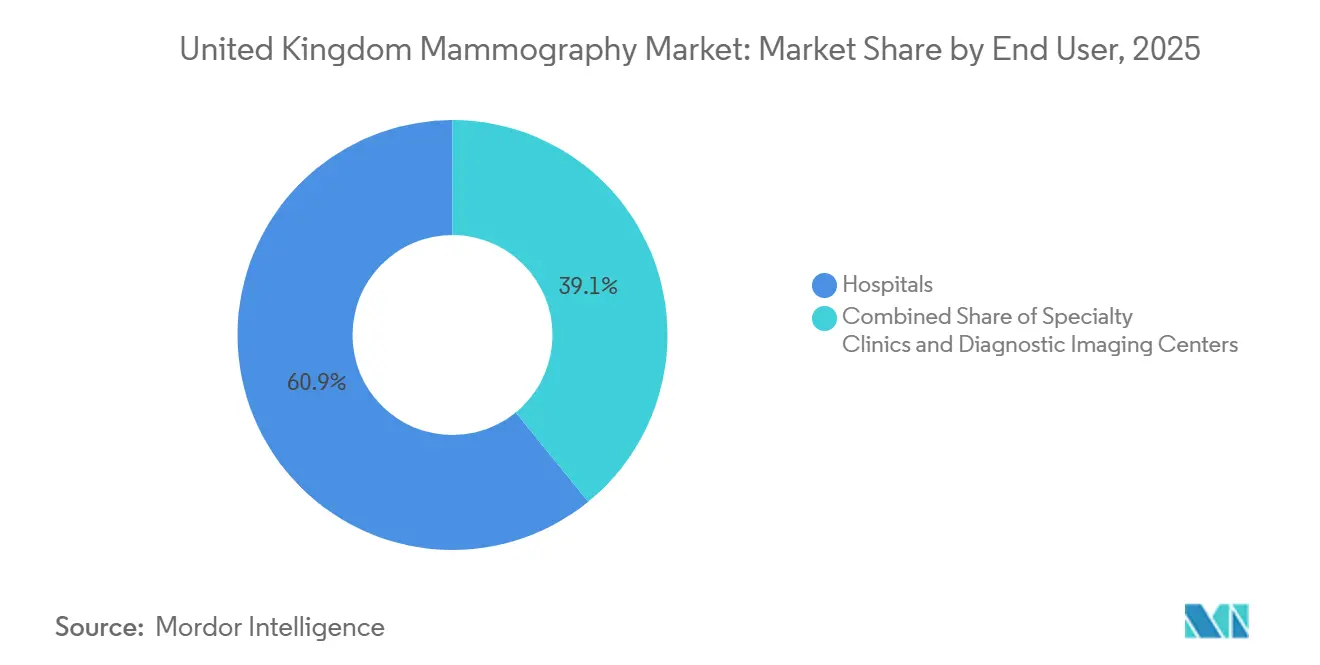

- By end user, hospitals held 60.85% of the United Kingdom mammography market share in 2025; diagnostic imaging centers record the highest anticipated CAGR at 9.58% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Mammography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of NHS Breast Screening Programme coverage and age limits | +2.8% | UK-wide, targeting historically underserved regions | Medium term (2-4 years) |

| Growing incidence of breast cancer and early-onset diagnoses | +2.5% | UK-wide, amplified in densely populated urban clusters | Long term (≥ 4 years) |

| Technological advances and replacement cycles for 3-D breast tomosynthesis | +1.9% | UK-wide, initial uptake in larger NHS Trusts and private clinics | Medium term (2-4 years) |

| Rapid adoption of AI-enabled CAD solutions to mitigate radiologist shortages | +1.4% | UK-wide, accelerating fastest in acute care NHS Trusts | Short to Medium term (1-3 years) |

| Deployment of mobile mammography vans to address rural access inequities | +0.8% | Rural UK specifically (Scottish Highlands, Cornwall, Wales) | Short term (≤ 2 years) |

| ESG-linked capital and NHS Net Zero initiatives driving low-dose system upgrades | +0.6% | UK-wide, tied to NHS Trusts with active green procurement mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Incidence of Breast Cancer in the UK

Incidence continues to rise and is projected to reach one new diagnosis every eight minutes by 2040 [1]Breast Cancer Now, “Breast Cancer in the UK 2024,” breastcancernow.org. The demographic skew toward women older than 50 aligns directly with NHS screening eligibility, creating reliable procedure volumes that refresh the installed base of digital units. Higher cancer risk in women with dense tissue elevates demand for advanced imaging such as molecular breast imaging that complements mammography workflows. Cost estimates show breast cancer management could climb to GBP 3.6 billion by 2034, reinforcing the financial logic of early detection investments. Urban hubs with dense populations require high-throughput systems to manage growing caseloads, which strengthens the purchasing case for premium 3-D equipment that shortens recall cycles and improves detection rates. Clinical researchers at University College London are now trialing prototype dense-breast imaging technologies that will likely feed future procurement requirements.

Expansion of NHS Breast Screening Programme Coverage

The NHS strategy extends screening invitations beyond age 70 and pushes mobile services into underserved regions, instantly increasing annual mammogram demand and straining installed capacity [2]UK Government, “World-Leading AI Trial to Tackle Breast Cancer Launched,” gov.uk . Performance benchmarks set a 70% coverage target, and early results from community diagnostic centers show uptake rising by nearly 50% where mobile units operate. The policy shift obliges trusts to procure additional systems or upgrade existing platforms capable of higher patient throughput. Integration with AI-based risk stratification software is becoming vital as program managers test adaptable recall intervals that tailor screening frequency to individual risk. NHS Digital data-security mandates drive procurement toward platforms offering secure cloud connections and airtight GDPR compliance.

Technological Advances in 3-D Breast Tomosynthesis

Tomosynthesis systems now deliver 92% sensitivity and reduce false-positive recalls by 40%, a performance that quickly converts clinical committees weighing replacement budgets. Reading times nearly double relative to 2-D films, pressing trusts to deploy AI tools that triage images and maintain throughput. Wide-angle tomosynthesis scanners, such as Siemens Healthineers’ 50-degree platform, further sharpen depth resolution, making them attractive for dense-breast protocols. The European Commission’s May 2023 guideline endorsement assures hospital boards that 3-D satisfies international best practice, adding momentum to capital-request approvals.

Rapid Adoption of AI-Enabled CAD Solutions

A national AI trial covering 700,000 women across 30 sites validates CAD algorithms that detect cancers missed by radiologists and slash result times to three days. The MHRA Airlock pilot signals clear regulatory pathways for machine-learning innovations, reducing market-entry friction for vendors. Vendors such as Lunit, now strengthened through its Volpara acquisition, are packaging risk scoring, quality assurance, and workflow analytics in modular subscriptions that fit NHS operating-budget lines. Scalable AI reduces the impact of a 29% shortfall in clinical radiologists, positioning software as a direct workforce multiplier.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patient concerns over radiation exposure | -1.2% | Urban health boards | Short term (≤ 2 years) |

| Cuts to NHS capital budgets | -2.3% | Smaller trusts | Medium term (2-4 years) |

| Shortage of trained radiographers | -1.8% | Rural regions | Long term (≥ 4 years) |

| GDPR limits on cloud AI data sharing | -0.9% | EU data-adequate areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Patient Concerns Over Cumulative Radiation Exposure

Average glandular dose ranges from 1 mGy to 10 mGy per exam, and contrast-enhanced studies can reach 11.84 mGy, prompting safety questions that lower repeat attendance. Surveys show 27% of non-attendees cite fear of pain and radiation as key deterrents. Manufacturers now market automatic exposure control systems that dynamically tailor dose by breast thickness, lowering patient anxiety and improving re-screen rates. Public-facing NHS campaigns emphasize dose transparency, quoting UNSCEAR’s frequency-weighted effective dose of 0.22 mSv for standard screening to build trust.

Cuts to NHS Capital Equipment Budgets

The GBP 37 billion funding gap forces trusts to weigh immediate clinical need against deferred maintenance. Capital guidance for 2025-26 mandates efficiency gains, prolonging replacement cycles for analog or early-generation digital units. To circumvent constraints, vendors offer managed-equipment services that shift expenditure from capital to operating budgets, but longer contract tenures can limit future technology refresh agility. Targeted funds such as the GBP 130 million Radiotherapy Modernisation Fund highlight the potential for ring-fenced grants; mammography suppliers lobby for similar screening allocations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Systems Drive Market Transformation

Digital mammography accounts for 67.90% of United Kingdom mammography market share in 2025 and remains the backbone of NHS screening infrastructure. Conversion from film to digital has improved image clarity and lowered repeat rates, generating total cost savings that help offset acquisition premiums. The United Kingdom mammography market size for digital systems increased in 2026 as trusts replaced aging detectors with models that integrate wireless compression paddles and AI-ready workstations. Vendors are bundling service contracts that guarantee uptime above 99% and include remote diagnostics to reduce site visits.

Breast tomosynthesis systems post the fastest growth at 9.29% CAGR to 2031, fueled by clinical validation and regulatory endorsement. Tomosynthesis improves invasive-cancer detection by up to 65% versus 2-D and lowers recall rates by 40%. The United Kingdom mammography market size for tomosynthesis is expanding as framework agreements under NHS Supply Chain shorten tender cycles and encourage bulk procurement. Analog solutions continue to phase out, yet remain in select rural vans where power constraints and low utilization do not justify 3-D investment. Additional categories such as biopsy-guided tables and contrast-enhanced platforms are gaining niche interest as trusts pursue one-stop breast clinics.

By Technology: 3-D Mammography Reshapes Clinical Practice

3-D platforms held 56.70% of the United Kingdom mammography market in 2025 due to superior lesion conspicuity and fewer recalls. NHS trusts favor systems supporting synthetic 2-D image generation, keeping total dose within legacy parameters while capturing volumetric data for AI post-processing. Facilities planning future purchases cite higher reimbursement tariffs for 3-D as an additional economic rationale.

2-D mammography retains value where throughput needs override the depth advantage of 3-D. Trusts running single-read protocols choose cost-efficient flat-panel units that handle ten patients per hour. The United Kingdom mammography market size for 2-D still increases modestly as community centers prioritize equipment quantity over premium features. Combined 2-D/3-D modes provide configuration flexibility and are expected to dominate replacement cycles past 2028.

By End User: Hospitals Anchor Market While Community Centers Surge

Hospitals captured 60.85% of 2025 demand, reflecting their role as the primary location for symptomatic imaging and multidisciplinary tumor boards. Continuous quality-assurance mandates and on-site engineering teams enable hospitals to adopt the latest 3-D and AI upgrades quickly. The United Kingdom mammography market size in hospitals increases further in 2026 as large trusts consolidate regional screening lists to maximize scanner utilization and secure volume-based discounts from suppliers.

Diagnostic imaging centers are the fastest-growing channel at 9.58% CAGR to 2031, driven by the government’s Community Diagnostic Centre initiative that aims for 9 million additional tests annually. Retail-park locations, high-street clinics, and mobile vans combine to expand geographic reach and cut travel time. These centers leverage cloud PACS solutions that allow off-site radiologists to read exams, supporting service continuity when local staffing is thin. Specialty clinics that focus exclusively on breast care carve out a smaller but stable share by offering same-day ultrasound and biopsy.

Geography Analysis

England accounts for the bulk of installations because of its larger population and denser hospital network. London, Manchester, and Birmingham contribute the highest exam volumes, driving repeat procurement of 3-D scanners. Regional screening units that cover defined post-code clusters support predictable replacement calendars and enable collective bargaining for maintenance contracts. Record participation achieved during the 2025 NHS awareness campaign has intensified machine usage across metropolitan hubs.

Scotland, Wales, and Northern Ireland constitute distinct procurement pools that collectively influence 17.85% of total installations. The NHS boards in these nations face significant rural access challenges and therefore allocate budget for mobile vans equipped with battery-efficient digital detectors. Gloucestershire’s updated mobile cancer unit illustrates how refurbishments can introduce 20 patient visits daily while maintaining image quality standards.

Cross-border initiatives facilitate shared cloud PACS infrastructures that pool radiologist capacity across eight NHS trusts in Greater Manchester, processing up to 4 million exams yearly. Such integration reduces reporting backlogs and informs asset-allocation decisions when neighboring trusts experience scanner downtime. Staffing shortages appear most acute in rural Highlands and coastal Wales, driving local boards to negotiate managed-service contracts that include teleradiology support packages from equipment vendors.

Competitive Landscape

The market exhibits moderate concentration, with five global manufacturers—Hologic, Siemens Healthineers, GE HealthCare, Fujifilm, and Philips—collectively serving a majority of existing contracts. Competition centers on 3-D imaging performance, dose optimization, and the ease of integrating third-party AI software into vendor neutral archives. Strategic moves in 2024-2025 underscore the pivot toward AI ecosystems. Lunit finalized its acquisition of Volpara Health Technologies to deliver an end-to-end breast health platform that addresses risk assessment, image quality assurance, and cancer detection in a single workflow[3]Lunit, “Lunit Completes Acquisition of Volpara,” lunit.io.

Hologic deepened portfolio reach through targeted acquisitions that add cloud-analytics modules capable of automating quality control, while Siemens Healthineers launched MAMMOMAT B.brilliant, the UK’s first unit with a full tomosynthesis scan time below five seconds, improving patient comfort and throughput. GE HealthCare introduced the Pristina Via featuring zero-click acquisition and low-dose exposure for dense breasts, positioning the device as a premium alternative for trusts seeking to upgrade but facing staffing limitations.

Niche entrants such as ScreenPoint Medical and iCAD supply AI solutions that can attach to any DICOM-compatible modality, giving hospitals flexibility without full hardware refresh. Meanwhile, start-ups focused on cone-beam CT and molecular imaging continue pilot studies that may alter competitive hierarchies after 2030 if reimbursement pathways solidify.

United Kingdom Mammography Industry Leaders

Siemens Healthineers AG

Canon Inc. (Canon Medical Systems Corporation)

Koninklijke Philips NV

Fujifilm Holdings Corporation

GE Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: University Hospital Southampton NHS Foundation Trust installed the UK’s first MAMMOMAT B.brilliant tomosynthesis system, reducing scan time below five seconds and enhancing patient comfort.

- February 2025: The NHS launched its inaugural nationwide campaign promoting breast screening, citing that 46.3% of first-time invitees do not attend appointments.

- October 2024: DeepHealth acquired Kheiron Medical Technologies to expand AI mammography capabilities, integrating the Mia algorithm into an enlarged diagnostic platform.

United Kingdom Mammography Market Report Scope

As per the scope of the report, mammography refers to a standard diagnostic and screening technique that is used to screen breast tissues to check the presence of a malignant tumor. The process involves the usage of low-energy X-rays for the early detection of breast cancer. United Kingdom Mammography Market is Segmented by Product Type (Digital Systems, Analog Systems, Breast Tomosynthesis, and Other Product Types), End User (Hospitals, Specialty Clinics, and Diagnostic Centers). The report offers the value (in USD million) for the above segments.

By Product Type

| Digital Mammography Systems |

| Analog Mammography Systems |

| Breast Tomosynthesis Systems |

| Other Product Types |

By Technology

| 2-D Mammography |

| 3-D Mammography |

By End User

| Hospitals |

| Specialty Clinics |

| Diagnostic Imaging Centers |

| By Product Type | Digital Mammography Systems |

| Analog Mammography Systems | |

| Breast Tomosynthesis Systems | |

| Other Product Types | |

| By Technology | 2-D Mammography |

| 3-D Mammography | |

| By End User | Hospitals |

| Specialty Clinics | |

| Diagnostic Imaging Centers |

Key Questions Answered in the Report

How big is the United Kingdom Mammography Market?

The United Kingdom Mammography Market size is expected to reach USD 98.9 million in 2026 and grow at a CAGR of 8.63% to reach USD 149.52 million by 2031.

Which product category holds the biggest share of current installations?

Digital mammography systems account for 67.90% of all units in service.

Who are the key players in United Kingdom Mammography Market?

Siemens Healthineers AG, Canon Inc. (Canon Medical Systems Corporation), Koninklijke Philips NV, Fujifilm Holdings Corporation and GE Healthcare are the major companies operating in the United Kingdom Mammography Market.

Why are community diagnostic centers important for future demand?

They raise screening uptake by up to 50% in underserved areas, driving higher equipment procurement.

Page last updated on: