Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

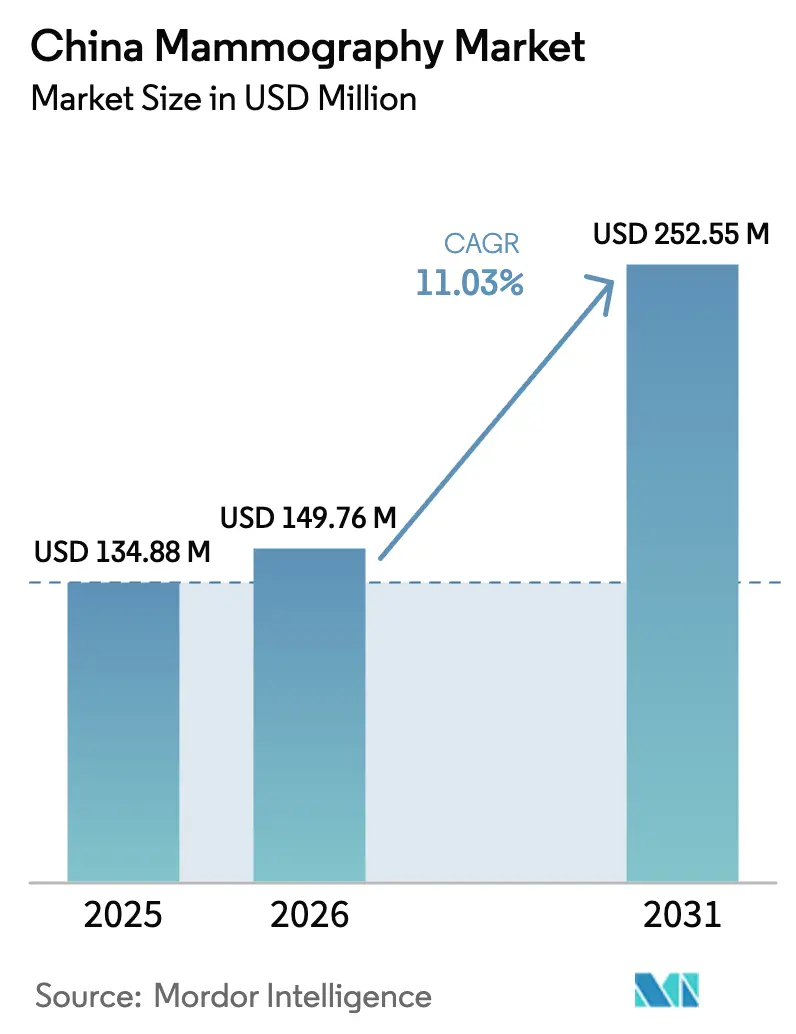

| Base Year Market Size (2025) | USD 134.88 Million |

| Market Size (2026) | USD 149.76 Million |

| Market Size (2031) | USD 252.55 Million |

| Growth Rate (2026 - 2031) | 11.03% CAGR |

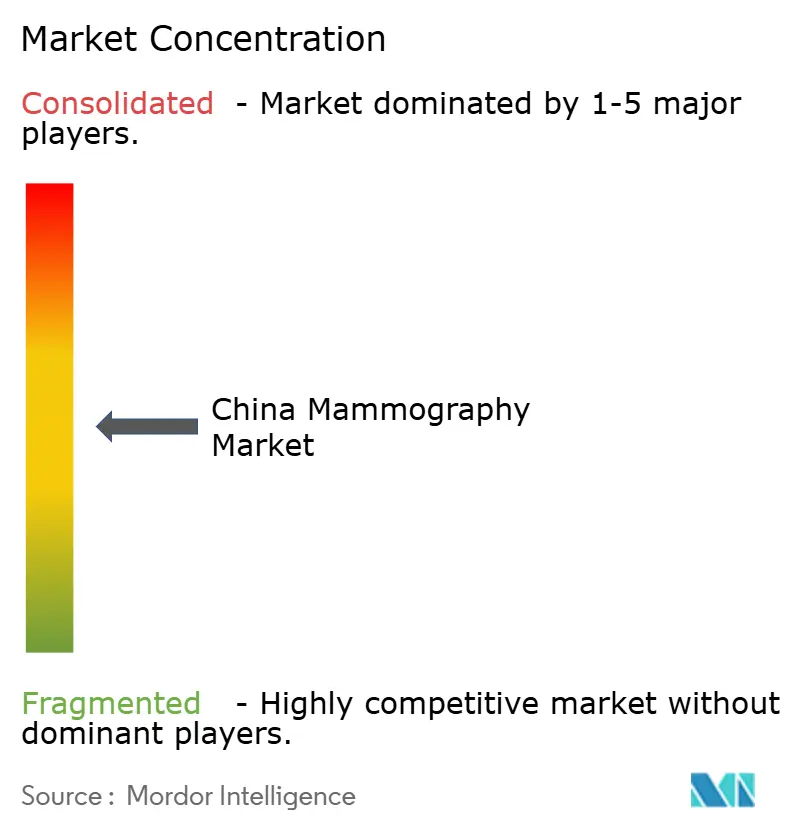

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Mammography Market Analysis by Mordor Intelligence

China Mammography Market size in 2026 is estimated at USD 149.76 million, growing from 2025 value of USD 134.88 million with 2031 projections showing USD 252.55 million, growing at 11.03% CAGR over 2026-2031.

Continued expansion is driven by the government’s “Two-Cancer” screening program, the rising incidence of breast cancer, and accelerated technology upgrades in tertiary hospitals. Hospitals are prioritizing full-field digital and 3-D tomosynthesis systems for sharper images and artificial-intelligence (AI) compatibility, while provincial volume-based procurement (VBP) keeps hardware prices in check, indirectly widening access. Domestic manufacturers leverage cost competitiveness and local procurement preferences to challenge multinational incumbents, yet international vendors retain an edge in high-end AI-enabled modalities. Meanwhile, mobile screening vans and specialty breast clinics extend services into tier 3 and tier 4 counties, closing gaps in rural detection rates. Combined, these forces sustain a balanced growth outlook for the Chinese mammography market through 2030.

Key Report Takeaways

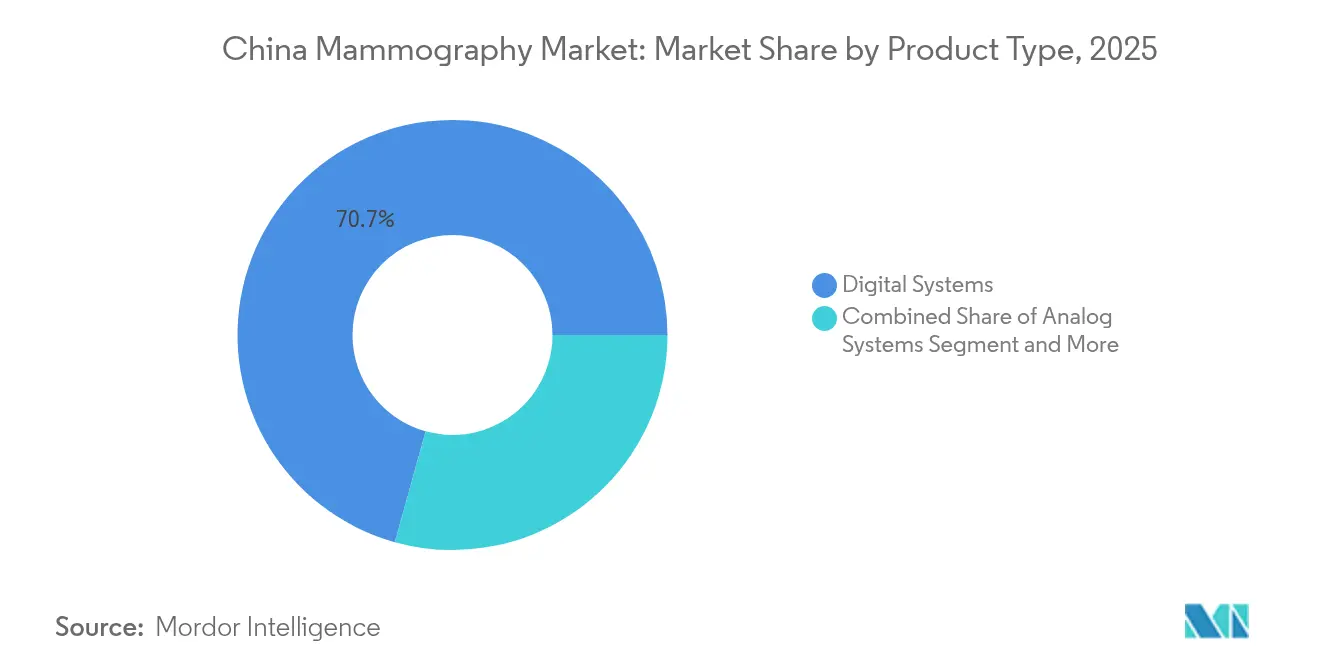

- By product type, digital systems led with 70.68% of the China mammography market share in 2025, while breast tomosynthesis is forecast to expand at an 11.73% CAGR through 2031.

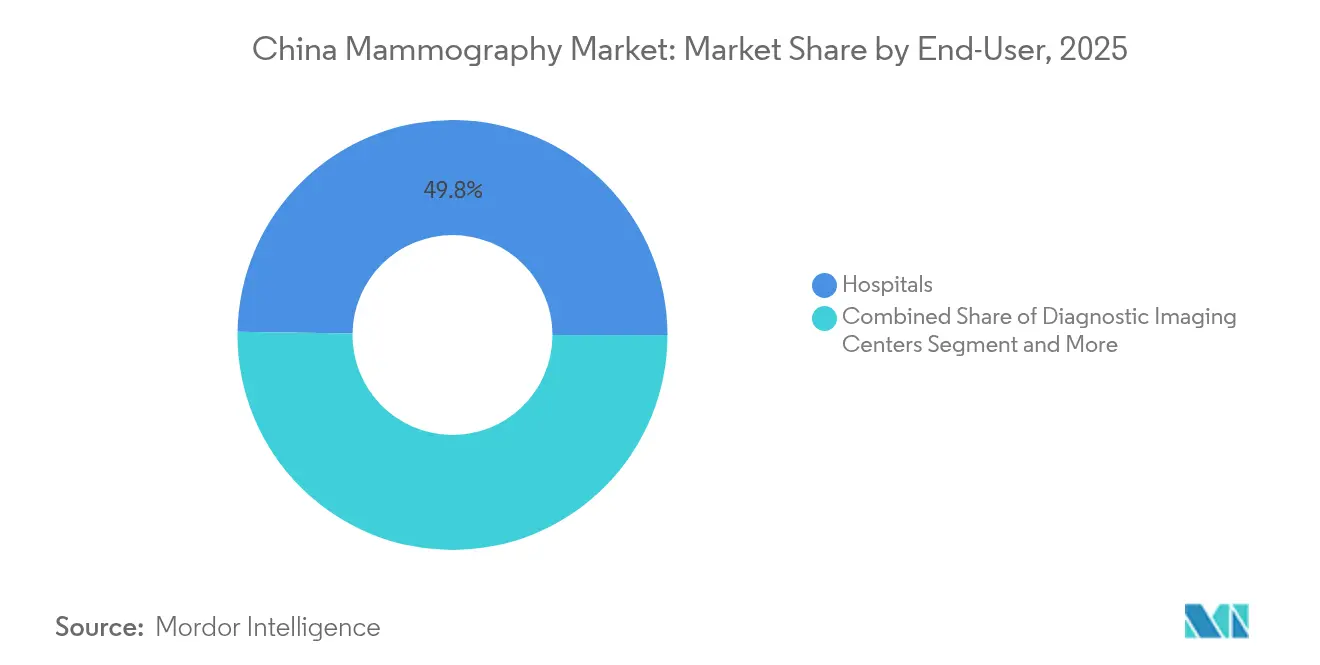

- By end-user, hospitals held 49.76% of the China mammography market size in 2025 and specialty breast clinics are expected to post a 11.99% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Mammography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Burden of Breast Cancer | +2.8% | National, with higher impact in tier-1 cities | Long term (≥ 4 years) |

| Technological Shift to Full-Field Digital & 3-D Tomosynthesis | +2.1% | National, led by Class III hospitals | Medium term (2-4 years) |

| Nation-Wide "Two-Cancer" Screening Expansion | +3.2% | National, with rural focus | Long term (≥ 4 years) |

| AI-Powered CAD Adoption in Class III Hospitals | +1.8% | Tier-1 and tier-2 cities | Short term (≤ 2 years) |

| Provincial Volume-Based Procurement Slashing System Prices | +1.1% | National, provincial variations | Medium term (2-4 years) |

| Mobile Screening Vans Reaching Tier-3/4 Counties | +0.9% | Rural and tier-3/4 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Breast Cancer

China recorded 357,200 new breast-cancer cases and 75,000 deaths in 2022, the highest incidence in Asia, prompting aggressive screening investments. Incidence peaks among women aged 50-54, aligning with global guidelines and underpinning equipment demand across all province tiers. Urban–rural gaps persist, with incidence rates of 35.45 versus 29.38 per 100,000, respectively, motivating resource allocation toward underserved regions. Long-term demographic shifts and lifestyle changes sustain the upward trajectory of breast-cancer burden, reinforcing a durable need for mammography capacity. Consequently, the China mammography market continues to align public-health imperatives with robust commercial opportunities.

Technological Shift to Full-Field Digital & 3-D Tomosynthesis

Digital breast tomosynthesis (DBT) achieves a sensitivity of 86%, compared to 80% for conventional digital systems, resulting in a significant reduction in false-positive callbacks.[1]Xuewen Liu, “Impact of Digital Breast Tomosynthesis on Screening Performance,” PLoS ONE, plos.orgDense breast tissue, present in roughly 70% of Asian women, benefits most, accelerating DBT installations in Class III hospitals. Economic models show incremental cost-effectiveness ratios of USD 5,971.58 per QALY, validating capital outlays. Synthetic 2-D reconstruction further reduces patient radiation exposure without compromising accuracy. AI algorithms integrated into DBT platforms achieve area-under-the-curve scores exceeding 0.93, enhancing lesion detection and positioning high-end systems as the benchmark for the China mammography market.

Nation-Wide “Two-Cancer” Screening Expansion

The “Two-Cancer” program achieved 51.5% coverage of eligible women aged 35-64 in 2024, marking the world’s largest organized breast-cancer screening initiative. Policy makers aim for 70% coverage by 2030, prompting provincial health bureaus to allocate funds for mammography fleets, workforce training, and data infrastructure. Coverage disparities, with urban areas at 65% versus rural areas at 48.2%, drive the procurement of mobile vans and tele-radiology solutions to bridge the gaps. Provinces such as Guangdong are forecasted to have 25,444 new cases in 2023, catalyzing concentrated demand for premium systems in high-burden metropolitan areas. Sustained government funding underpins a stable long-run pipeline for the China mammography market.

AI-Powered CAD Adoption in Class III Hospitals

Clinical studies show AI-assisted CAD achieves 91.5% sensitivity and 96.3% specificity in breast-lesion detection, freeing scarce radiologists for complex reads. Tier-1 hospitals lead the way in deployment because they possess the data-management capacity, PACS integration, and R&D linkages necessary to work with domestic AI vendors. DeepSeek AI now runs in about 100 facilities, demonstrating scalable rollouts that complement existing image-archiving systems. Fast-track NMPA approvals over 60 AI certificates since 2023 shorten commercialization cycles, allowing AI innovators to reach the China mammography market swiftly.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Radiation-Exposure Risk Perception | -1.4% | National, higher in rural areas | Medium term (2-4 years) |

| Inadequate Reimbursement Outside Urban Megacities | -2.1% | Rural and tier-3/4 cities | Long term (≥ 4 years) |

| High Capex Versus Ultrasound Alternatives | -1.8% | Tier-2/3 cities and rural hospitals | Medium term (2-4 years) |

| Stringent NMPA Domestic-Content Localisation Quotas | -1.2% | National, affecting international brands | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Radiation-Exposure Risk Perception

Studies reveal radiation fear remains a leading deterrent to screening participation, especially where health literacy is limited. Misinformation on social media amplifies skepticism, necessitating structured educational campaigns that explain low-dose protocols and highlight cumulative safety records. Manufacturers mitigate concerns by promoting synthetic 2-D imaging that halves radiation relative to legacy systems. Continuous professional training for primary-care providers and collaboration with local women’s organizations help normalize mammography in apprehensive communities, steadily improving uptake within the China mammography market.

Inadequate Reimbursement Outside Urban Megacities

Rural residents often bear higher out-of-pocket costs because public insurance schemes prioritize city centers, hampering equipment utilization in lower-tier hospitals.[2]Yan Zhou, “Knowledge, Attitude, and Practice Toward Breast-Cancer Screening,” Scientific Reports, nature.com Clinics may struggle to meet volume thresholds that justify mammography investments, thereby slowing penetration in provinces with dispersed populations. National Health-Security Administration reforms propose enhanced subsidies, but rollout timelines remain uncertain. Vendors respond by offering leasing models and pay-per-scan contracts that reduce capital barriers. Yet, structural reimbursement gaps continue to temper growth potential in remote segments of the China mammography market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Platforms Consolidate Leadership

Digital systems accounted for 70.68% of the China mammography market share in 2025, underscoring the dominance of full-field digital and DBT technology in tertiary and secondary hospitals. Rapid image acquisition, cloud archiving, and seamless integration with AI-based CAD workflows underpin their appeal. Analog units persist only in budget-constrained rural centers but face declining procurement as VBP narrows price differences. Breast tomosynthesis leads growth, posting an 11.73% CAGR projected through 2031, propelled by superior sensitivity in dense-breast populations and favorable cost-effectiveness profiles.

Beyond screening, stereotactic biopsy attachments and contrast-enhanced modules extend platform utility, offering incremental revenue via procedure-based reimbursements. Manufacturers bundle software upgrades as software-as-a-service, ensuring recurring income while customers maintain updated diagnostic functionality. These trends cement digital systems as the cornerstone of the China mammography market size for the foreseeable future.

By End-User: Hospitals Dominate While Specialty Clinics Surge

Hospitals captured 49.76% of the China mammography market size in 2025, reflecting entrenched referral flows, oncology integrations, and qualified radiology staff levels. Class III institutions deploy multi-vendor fleets to balance capacity, redundancy, and research requirements. Conversely, specialty breast clinics register the fastest growth at a 11.99% CAGR to 2031, fueled by demand for same-day diagnostics, personalized care, and boutique patient experiences.

Diagnostic imaging centers bridge gaps in mid-sized cities, offering accessible yet specialized services without hospital wait times. Mobile units, supported by provincial grants, extend reach into frontier counties, where screening volumes were historically too low to justify fixed installations. Collectively, this heterogenous end-user mix broadens overall penetration, supporting the long-run expansion of the China mammography market.

Geography Analysis

Regional patterns mirror China’s economic geography. Tier-1 clusters, including Beijing-Tianjin-Hebei, Yangtze River Delta, and Pearl River Delta, host the majority of high-end digital and DBT units due to their dense patient volumes, strong purchasing power, and academic-clinical collaboration. Urban facilities routinely integrate AI algorithms and participate in multi-center trials, reinforcing technology leadership and shaping procurement benchmarks nationwide.

Central and western provinces experience faster percentage growth, driven by state-funded infrastructure programs and targeted rural health subsidies.Annual device tenders in these regions increased by 74% during the first half of 2025, indicating a geographic rebalancing of demand. Nonetheless, utilization rates remain lower than coastal hubs, suggesting latent capacity that will mature over the forecast period.

Mobile screening strategies mitigate geographic inequities. Government-backed fleets equipped with low-dose digital detectors and cloud-based AI triage travel to townships on rotating schedules, narrowing participation gaps. Early evidence shows detection rates comparable to fixed centers, validating the model’s clinical efficacy. Taken together, geographic dynamics reinforce both concentration in wealthy metros and dispersion in underserved interiors, sustaining diversified growth across the China mammography market.

Competitive Landscape

Competition centers on technology leadership, VBP resilience, and localization compliance. Hologic, Siemens Healthineers, and GE HealthCare maintain premium positioning through advanced AI integration, ergonomic patient design, and global service footprints. Domestic challengers United Imaging Healthcare, Mindray, and Neusoft capitalize on price agility, NMPA fast-track approvals, and government preference for local content.

Strategic alliances intensify differentiation. Hologic and Siemens share detector technologies to accelerate innovation, while Philips partnered with CHISON to co-develop breast-imaging solutions for mid-tier hospitals. AI software vendors, such as Deepwise and RadNet, embed algorithms into OEM hardware, offering turnkey solutions that combine acquisition and interpretation. VBP favors suppliers capable of scaling nationally, thereby enhancing the bargaining position of large domestic brands.

Localization quotas stipulate rising domestic-content ratios, nudging multinationals to expand in-country manufacturing or joint ventures. Those that comply swiftly protect market access; laggards face procurement exclusion. As AI becomes table stakes, differentiation shifts to workflow orchestration, cloud analytics, and lifetime-service economics, shaping the next phase of rivalry within the China mammography market.

China Mammography Industry Leaders

Carestream Health Inc.

GE Healthcare

Siemens Healthineers AG

Fujifilm Holdings Corporation

Koninklijke Philips NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Clairvo Technologies and Shukun Technology, a Chinese company formed a comprehensive partnership to deploy multi-modality imaging AI, including mammography, across Japan.

- November 2024: GE HealthCare integrated RadNet’s Smartmammo AI workflow into the Senographe Pristina platform for distribution across Chinese breast centers.

- January 2023: Deepwise Technology’s AI mammography-screening software became the first NMPA-approved artificial-intelligence device for breast cancer in China.

China Mammography Market Report Scope

Mammography refers to a standard diagnostic and screening technique that is used to screen breast tissues to check the presence of a malignant tumor. In mammography, low-frequency X-rays are passed through the breast to locate tumors.

The China mammography market is segmented by product type (digital systems, analog systems, breast tomosynthesis, and other product types) and end-user (hospitals, specialty clinics, and diagnostic centers).

The report offers the value (in USD) for the above segments.

By Product Type

| Digital Systems |

| Analog Systems |

| Breast Tomosynthesis (3-D) |

| Others (e.g., stereotactic biopsy units) |

By End-User

| Hospitals |

| Specialty Breast Clinics |

| Diagnostic Imaging Centers |

| Mobile Screening Units |

| By Product Type | Digital Systems |

| Analog Systems | |

| Breast Tomosynthesis (3-D) | |

| Others (e.g., stereotactic biopsy units) | |

| By End-User | Hospitals |

| Specialty Breast Clinics | |

| Diagnostic Imaging Centers | |

| Mobile Screening Units |

Key Questions Answered in the Report

How big is the China Mammography Market?

The China Mammography Market size is expected to reach USD 149.76 million in 2026 and grow at a CAGR of 11.03% to reach USD 252.55 million by 2031.

How fast is breast tomosynthesis adoption growing in China?

Breast tomosynthesis systems are projected to post an 11.73% CAGR between 2026 and 2031, the fastest among product categories.

Who are the key players in China Mammography Market?

Carestream Health Inc., GE Healthcare, Siemens Healthineers AG, Fujifilm Holdings Corporation and Koninklijke Philips NV are the major companies operating in the China Mammography Market.

Which end-user segment contributes most to equipment demand?

Hospitals account for 49.76% of annual revenues, driven by integrated oncology services and high patient throughput.

Page last updated on: