Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

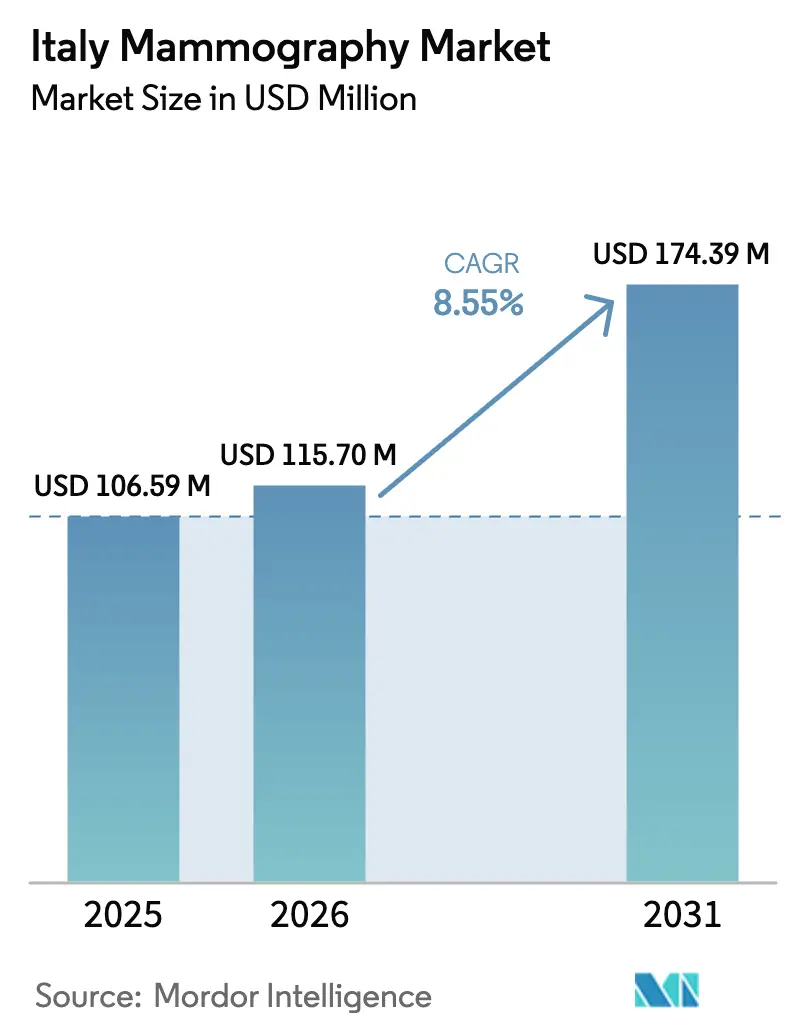

| Base Year Market Size (2025) | USD 106.59 Million |

| Market Size (2026) | USD 115.7 Million |

| Market Size (2031) | USD 174.39 Million |

| Growth Rate (2026 - 2031) | 8.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Mammography Market Analysis by Mordor Intelligence

The Italy Mammography Market size was valued at USD 106.59 million in 2025 and estimated to grow from USD 115.7 million in 2026 to reach USD 174.39 million by 2031, at a CAGR of 8.55% during the forecast period (2026-2031). Growth reflects deepening demand for early-stage breast-cancer detection, accelerated equipment replacement cycles funded by the National Recovery and Resilience Plan (PNRR), and rapid adoption of AI-ready digital platforms. Escalating incidence—55,900 new cases in 2024—sustains screening volumes, while personalized risk-stratified protocols expand the addressable population. Competitive pressure centers on integrated hardware-software offerings, with multinationals and local manufacturers intensifying product differentiation through multimodal imaging, ergonomic designs, and embedded analytics. Decentralized care models and rising private reimbursement spur new opportunities for diagnostic centers, mobile units, and tele-radiology services, collectively reshaping provider economics and patient pathways.

Key Report Takeaways

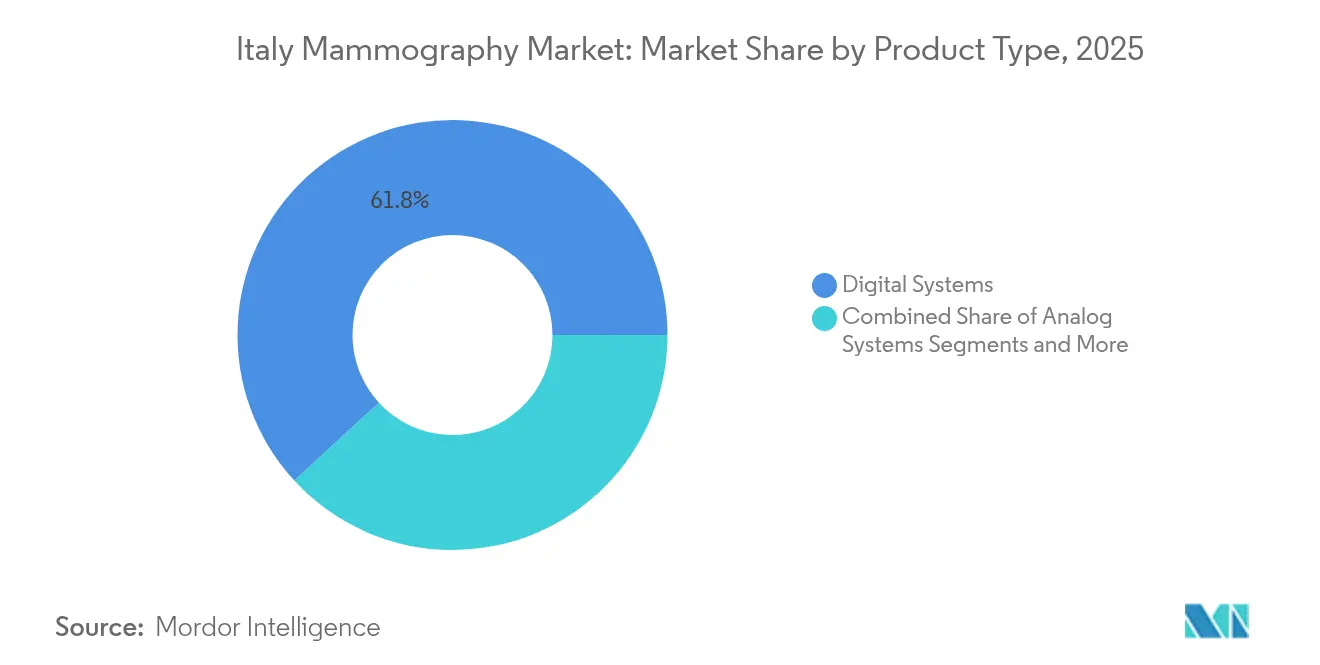

- By product type, Digital Systems led with 61.84% of Italy mammography market share in 2025; Breast Tomosynthesis is set to expand at a 8.98% CAGR to 2031.

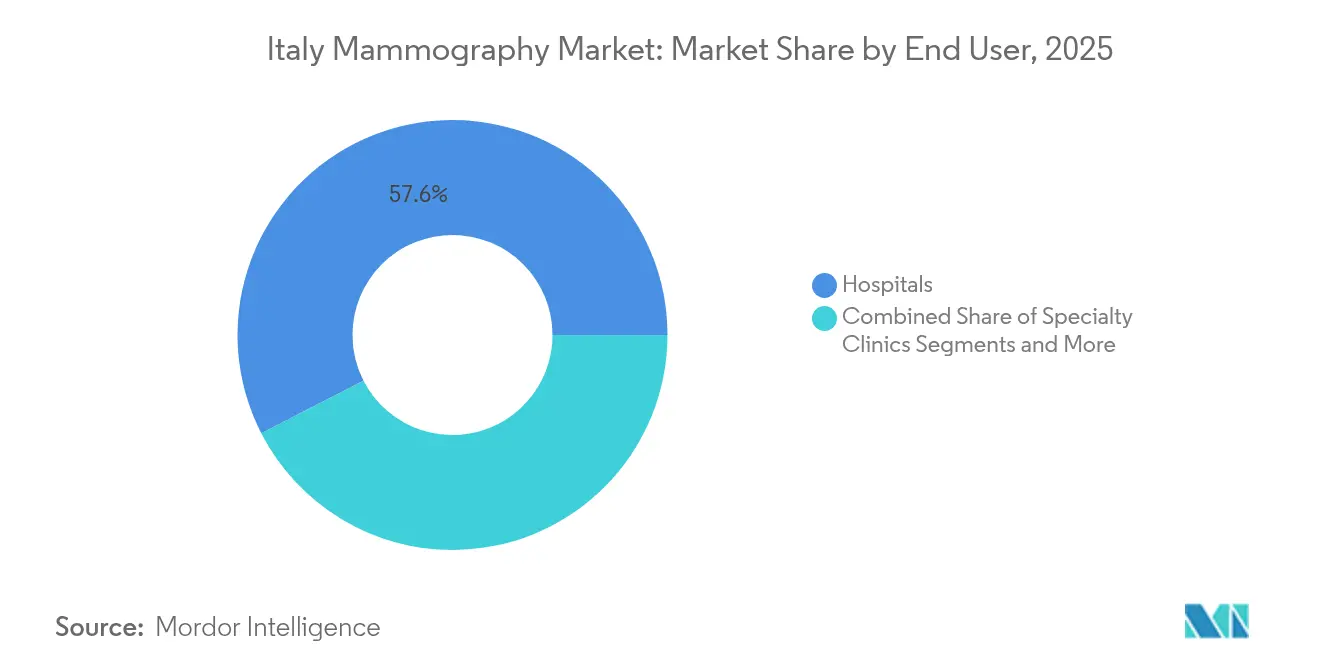

- By end user, hospitals accounted for 57.55% share of the Italy mammography market size in 2025, while diagnostic centers are advancing at a 9.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Mammography Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Burden Of Breast Cancer Cases | +2.1% | National, with higher impact in Northern and Central Italy | Long term (≥ 4 years) |

| Technological Advancements | +1.8% | National, concentrated in major healthcare centers | Medium term (2-4 years) |

| Increasing Funding In Hospitals | +1.5% | National, with PNRR focus on underserved regions | Medium term (2-4 years) |

| Government-Funded National Screening Programs | +1.3% | National, with expansion to age groups 45-49 and 70-74 | Long term (≥ 4 years) |

| Expansion Of Mobile Mammography Units In Rural Italy | +0.9% | Southern Italy and rural areas | Short term (≤ 2 years) |

| Fast-Track Reimbursement For Genomic Screening Tests | +0.7% | National, with early adoption in Northern regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Breast Cancer Cases

Italy records 55,900 new breast-cancer diagnoses each year, and lifetime risk now stands at 1 in 8 women [1]UPMC Italy, “Breast Cancer Prevention: Mammography,” upmc.it. Early-stage detection offers 88% five-year survival, driving sustained utilization of the Italy mammography market. Incidence is higher in the North, yet better screening adherence keeps metastatic presentation at 5.1% versus 7.8% in the South. Ageing demographics intensify demand, as risk rises sharply after 50. Regional cancer registries underscore the urgency of structured screening to curb late presentation and trim treatment costs. The demographic and epidemiological realities translate into predictable equipment replacement cycles and consistent scan volumes across public and private sectors.

Technological Advancements

Digital breast tomosynthesis paired with synthetic 2-D reconstructions doubles detection rates versus conventional 2-D systems—8.1/1,000 versus 4.5/1,000 in the Verona Pilot Study. AI algorithms now surpass 90% sensitivity compared with 70-80% for manual reads. Hologic’s Genius AI Detection and GE HealthCare’s SmartMammo rolled out nationwide during 2024, while Campania’s Synergy-Net couples AI with 3-D tomosynthesis to enhance dense-breast assessment. Equipment vendors embed algorithms on-board, reducing latency and easing compliance with EU Medical Device Regulation (MDR) quality standards. These advances catalyze the transition from analog fleets and underpin the Italy mammography market’s digital premium.

Increasing Funding in Hospitals

The PNRR allocates EUR 15.63 billion to healthcare, including EUR 2.8 billion for hospital digitalization and 2,500 large medical devices. Marche completed full installation of new mammography units under Mission 6 by mid-2025. Overall digital-health spend rose 22% to EUR 2.2 billion in 2023. Upfront capital support accelerates replacement of legacy analog systems and drives bulk procurement of AI-ready platforms. Parallel expansions in private health-fund coverage and tariff revisions improve provider cash flows, reinforcing market momentum.

Government-Funded National Screening Programs

Italy’s organized program covers women aged 50-69 every two years, achieving 57.3% participation and detecting 6,537 invasive cancers in the most recent cycle. Regions now trial extensions to 45-49 and 70-74 age bands; Lombardy already implemented coverage from 45-74. The multicenter 60,000-participant study on optimal intervals will set future evidence-based cadence. Expansion addresses an estimated 2 million currently underserved women, reinforcing scan volumes for the Italy mammography market over the long term.

Expansion of Mobile Mammography Units in Rural Italy

Mobile fleets meet 40% of screening demand in certain southern provinces, bridging infrastructure gaps while cutting patient travel. Tuscany’s model saved EUR 95,000 and 35 tons of CO₂ per 59,000 inhabitants screened. PNRR prioritizes rural rollouts, and the Senologia al Centro initiative offers free prevention via mobile units. Vendors, notably IMS Giotto and Metaltronica, design compact, low-power devices to capture this emerging sub-segment of the Italy mammography market.

Fast-Track Reimbursement for Genomic Screening Tests

2024 reforms sped reimbursement for breast-cancer genomic panels, bolstering demand for comprehensive imaging-plus-biomarker pathways. Northern regions lead early adoption, bundling AI triage with molecular profiling to refine risk stratification. Integrated care models incentivize providers to invest in higher-spec mammography systems that support contrast enhancement and AI analytics, further enlarging the Italy mammography market opportunity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Radiation-Exposure Concerns Limiting Repeat Screening | -1.2% | National, with higher impact among educated populations | Long term (≥ 4 years) |

| Declining Reimbursement Tariffs For Mammography | -1.5% | National, with greater impact on private providers | Medium term (2-4 years) |

| Regional Workforce Shortages In Breast Imaging | -1.8% | Southern Italy and rural areas | Medium term (2-4 years) |

| EU Green-Equipment Mandates Raising Capex | -0.9% | National, concentrated in major healthcare centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Radiation-Exposure Concerns Limiting Repeat Screening

Educated women in Turin show lower adherence due to heightened radiation worries despite superior awareness. Tomosynthesis delivers higher doses than 2-D imaging but remains within EU safety thresholds[2]European Society of Radiology, “Retrospective dose comparison in mammography,” epos.myesr.org . AIRC emphasizes that benefits outweigh risks, yet communication gaps persist. Providers increasingly offer contrast-enhanced or low-dose protocols and deploy decision aids to reassure patients. Mitigating this restraint is pivotal for sustaining participation rates central to Italy mammography market growth.

Regional Workforce Shortages in Breast Imaging

Northern hospitals report 18.4% of staff on work restrictions; 56.1% involve nurses with mobility limits, squeezing mammography throughput. Radiologist scarcity is acute in the South, elongating wait lists and curbing program efficacy. AI support trims reading time by up to 91%, partially easing deficits. Mobile units and tele-radiology add capacity, but only 35% of specialists currently exploit telehealth fully, signaling a lingering operational constraint on the Italy mammography market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Systems Drive Market Transformation

Digital Systems held 61.84% of Italy mammography market share in 2025, benefitting from PNRR-funded upgrades and embedded AI capabilities. Users cite sharper image resolution, lower repeat rates, and seamless integration with RIS/PACS. Analog fleets persist in cash-constrained rural settings but face accelerated obsolescence. EU MDR deadlines intensify digital adoption, shaping procurement preferences through 2031.

Breast Tomosynthesis contributes a 8.98% CAGR, buoyed by compelling evidence of superior detection in dense tissue. Hospitals spearhead uptake to enhance clinical accuracy, while diagnostic centers leverage tomosynthesis for competitive differentiation. Vendors integrate AI to automate lesion characterization, thereby expanding use cases and unlocking premium service tariffs tied to Italy mammography market size for advanced modalities. Multimodal innovations, such as Metaltronica’s Cybele platform that adds ultrasound and densitometry, illustrate convergence trends influencing future demand curves.

By End User: Hospitals Maintain Leadership While Diagnostic Centers Accelerate

Hospitals retained 57.55% share of the Italy mammography market size in 2025 owing to comprehensive oncology pathways and access to PNRR grants covering 2,500 devices. Their multidisciplinary environment facilitates rapid adoption of contrast-enhanced and AI-supported protocols, reinforcing leadership.

Diagnostic centers post the fastest 9.05% CAGR, powered by agile workflows and consumer preference for shorter waits. The December 2024 nomenclatore tariffario harmonized reimbursement, allowing stand-alone centers to price competitively. Partnerships such as Affidea-ScreenPoint enable AI deployment at scale. Mobile screening units complement brick-and-mortar facilities, penetrating rural markets and supporting risk-stratified screening initiatives, thereby broadening the Italy mammography market footprint among infrastructurally underserved populations.

Geography Analysis

Northern regions account for the bulk of Italy mammography market demand, boasting 90% screening adherence and earlier cancer detection. Robust hospital networks and higher disposable income underpin digital-system penetration. Metastatic presentation sits at 5.1% of cases, reflecting program effectiveness. Procurement trends favor AI-ready tomosynthesis, and private insurers aggressively reimburse advanced imaging, strengthening revenue visibility for vendors.

Central Italy shows mid-level uptake but pockets of rural shortfalls. Tuscany’s mobile initiatives trimmed travel expenditure by EUR 95,000 and carbon output by 35 tons, proving scalable for other provinces. Regional authorities integrate tele-radiology to extend subspecialist access, while Auxologico’s cross-regional presence in Lombardy and Piedmont showcases private-sector contribution to consistent service delivery.

Southern regions and islands trail with 60% adherence and 7.8% metastatic rates. PNRR funding prioritizes device deployment and 480 territorial operational centers to bolster primary care interfaces. Mobile fleets and public–private partnerships promise catch-up growth, positioning the South as the fastest-expanding sub-market within the overall Italy mammography market through 2031.

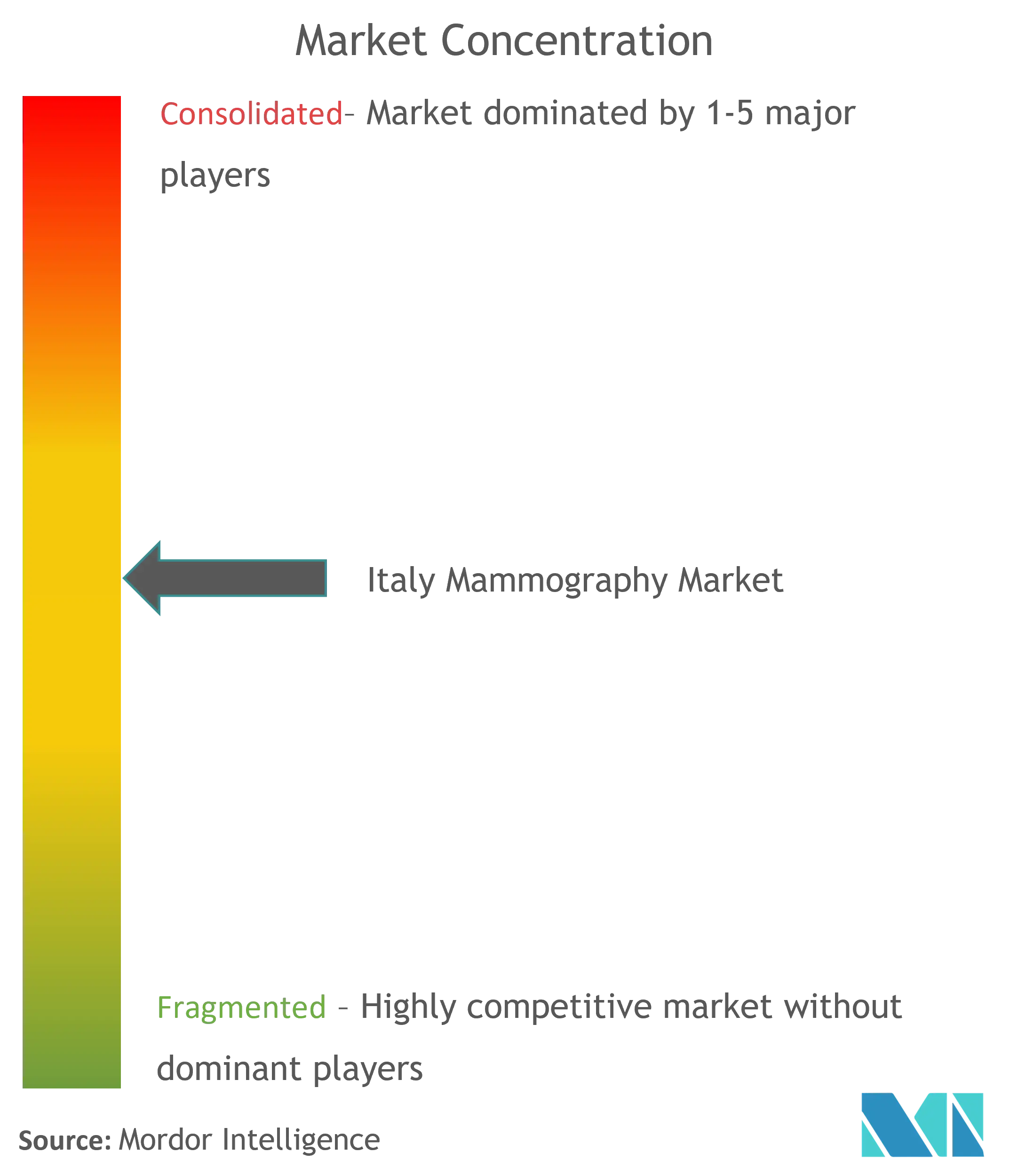

Competitive Landscape

Italy mammography market competition is moderately fragmented. Hologic, GE HealthCare, and Siemens Healthineers anchor share through wide portfolios, service contracts, and MDR-compliant pipelines. AI-centric specialists—ScreenPoint Medical, Lunit, iCAD—win hospital trials via superior algorithm sensitivity, often supplied as vendor-neutral plug-ins. Domestic firms IMS Giotto and Metaltronica leverage localized support and region-specific tenders; the latter’s Cybele multimodal release at ECR 2024 strengthens its niche.

Strategic collaborations dictate differentiation. Hologic’s alliance with Bayer delivers turnkey contrast-enhanced packages aligning imaging and injectable workflows. iCAD partnered with Koios to integrate multimodality AI, bridging mammography and ultrasound. Vendors increasingly bundle cloud analytics, software-as-a-service licenses, and flexible financing to align with PNRR procurement cycles, shaping future dynamics of the Italy mammography market.

Barriers stem from MDR certification costs and EU green-procurement directives that demand energy-efficient equipment, favoring capital-strong incumbents. Nonetheless, AI-software providers with lighter regulatory loads can scale rapidly via OEM integrations, injecting competitive tension across tiers.

Italy Mammography Industry Leaders

Koninklijke Philips NV

Fujifilm Holdings Corporation

Siemens Healthineers AG

Carestream Health Inc.

GE Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Laife Reply and IEO launch AI-agent network to support radiologists in screening workflows.

- February 2024: Fujifilm debuts AMULET SOPHINITY mammography system at ECR 2024, featuring enhanced patient comfort.

- June 2023: MIT’s Mirai model demonstrates five-year risk prediction using digital mammograms.

Italy Mammography Market Report Scope

As per the scope of the report, mammography refers to a standard diagnostic and screening technique that is used to screen breast tissues to check the presence of a malignant tumor. The process involves the usage of low-energy X-rays for the early detection of breast cancer. Italy Mammography Market is Segmented by Product Type (Digital Systems, Analog Systems, Breast Tomosynthesis, and Other Product Types), End User (Hospitals, Specialty Clinics, and Diagnostic Centers). The report offers the value (in USD million) for the above segments.

By Product Type

| Digital Systems |

| Analog Systems |

| Breast Tomosynthesis |

| Other Product Types |

By End User

| Hospitals |

| Specialty Clinics |

| Diagnostic Centers |

| Mobile Screening Units |

| By Product Type | Digital Systems |

| Analog Systems | |

| Breast Tomosynthesis | |

| Other Product Types | |

| By End User | Hospitals |

| Specialty Clinics | |

| Diagnostic Centers | |

| Mobile Screening Units |

Key Questions Answered in the Report

How big is the Italy Mammography Market?

The Italy Mammography Market size is expected to reach USD 115.7 million in 2026 and grow at a CAGR of 8.55% to reach USD 174.39 million by 2031.

Which product segment is growing the quickest?

Breast tomosynthesis is advancing at a 8.98% CAGR due to superior detection in dense breast tissue.

Who are the key players in Italy Mammography Market?

Koninklijke Philips NV, Fujifilm Holdings Corporation, Siemens Healthineers AG, Carestream Health Inc. and GE Healthcare are the major companies operating in the Italy Mammography Market.

Why are diagnostic centers gaining share?

Streamlined workflows, shorter wait times, and harmonized reimbursement encourage patient migration toward specialized centers.

Page last updated on: