Insulin Patch Pumps Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

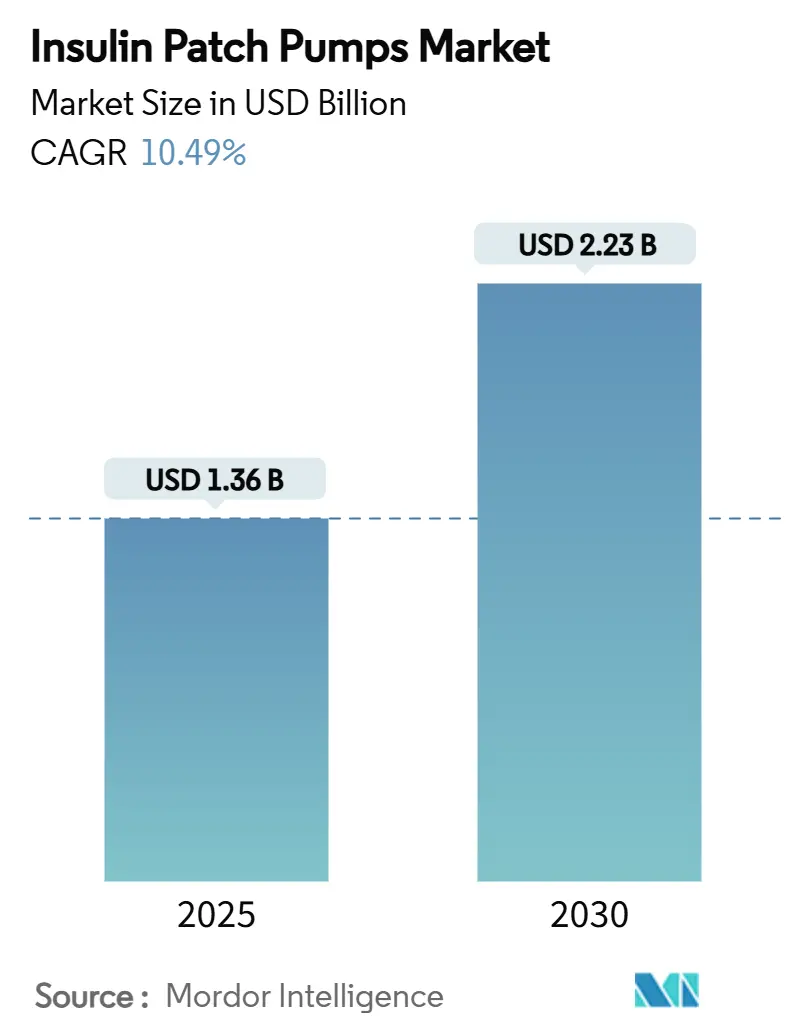

| Market Size (2025) | USD 1.36 Billion |

| Market Size (2030) | USD 2.23 Billion |

| Growth Rate (2025 - 2030) | 10.49% CAGR |

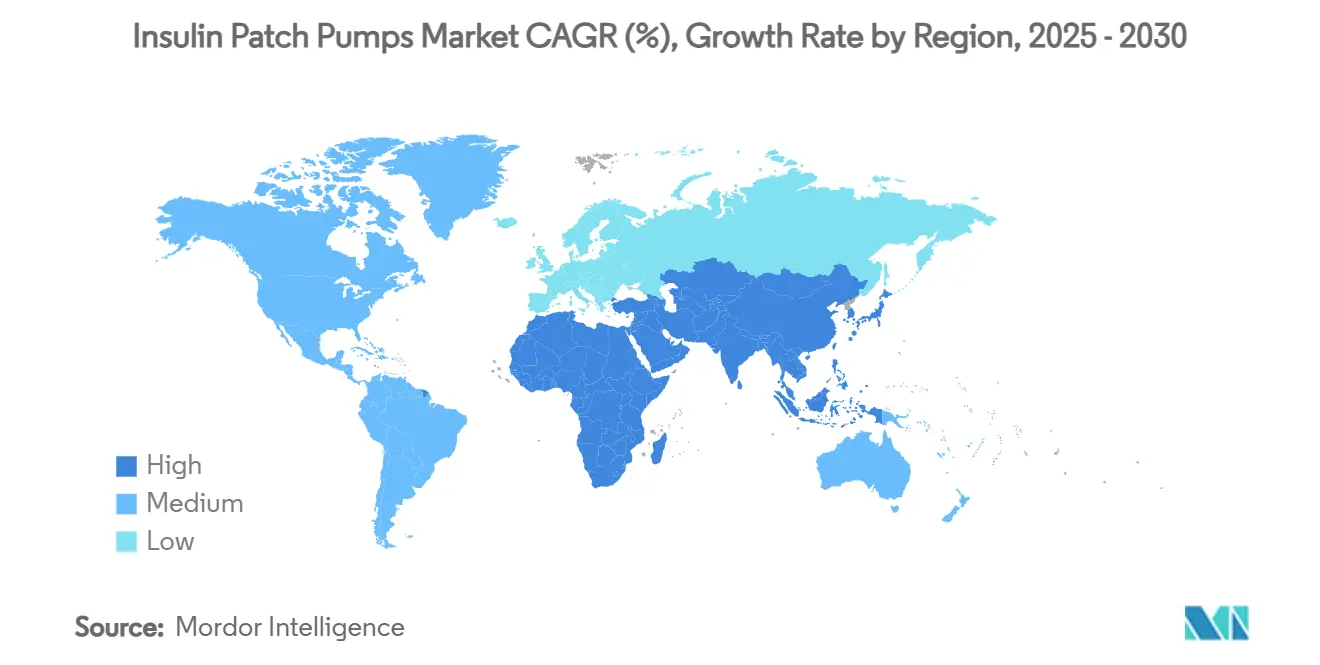

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Insulin Patch Pumps Market Analysis by Mordor Intelligence

The insulin patch pumps market size stood at USD 1.36 billion in 2025 and is slated to reach USD 2.23 billion by 2030, advancing at a 10.49% CAGR. Rising Type 1 diabetes prevalence, fast-spreading use of tubeless automated insulin delivery (AID) systems, and widening reimbursement in Europe and Asia-Pacific create a solid demand base. Disposable pumps dominate revenue because they lower infection risk and simplify daily routines, while reusable designs gain momentum as component durability improves. Integrated continuous glucose monitoring (CGM) options, employer-backed virtual clinics, and piezo-micro-pump miniaturisation collectively strengthen competitive positioning. Meanwhile, cybersecurity requirements, cost pressure versus insulin pens, and scrutiny of single-use plastics add friction but have yet to slow the upward trajectory of the insulin patch pumps market.

Key Report Takeaways

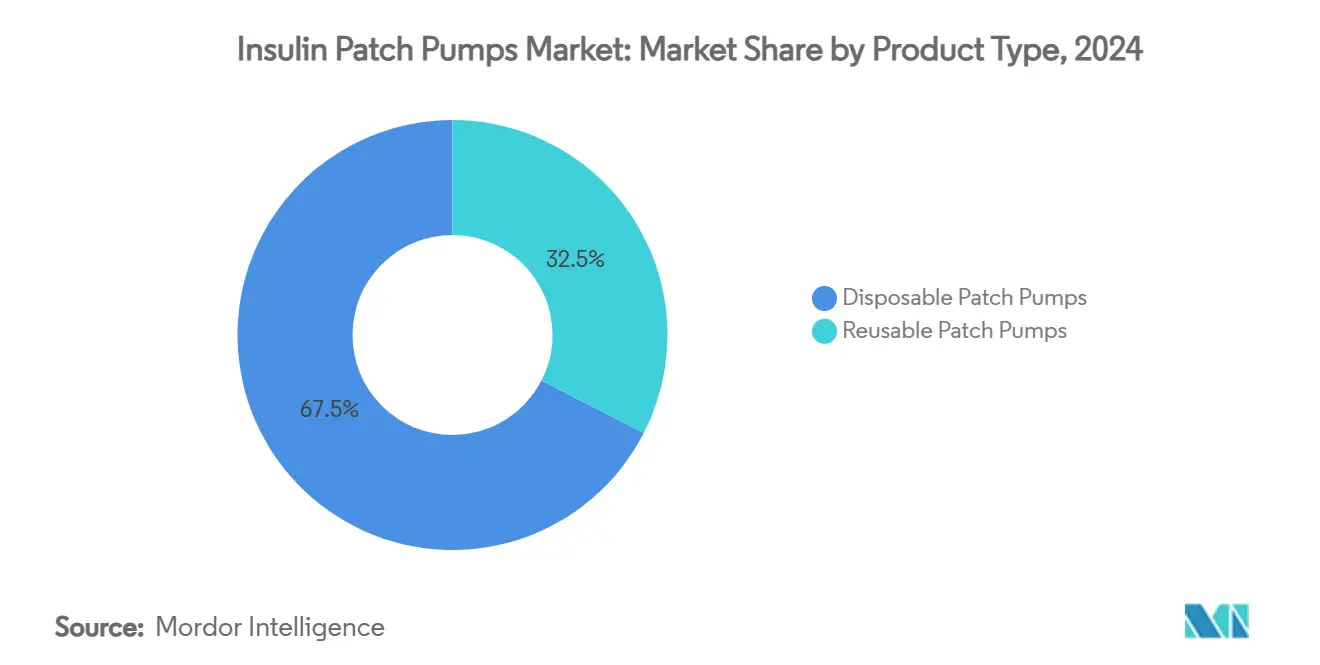

- By product type, disposable patch pumps captured 67.46% of the insulin patch pumps market share in 2024; reusable patch pumps are on track for a 14.26% CAGR through 2030.

- By delivery mode, basal and bolus pumps accounted for 51.34% of the insulin patch pumps market size in 2024 and are expanding at 13.69% CAGR.

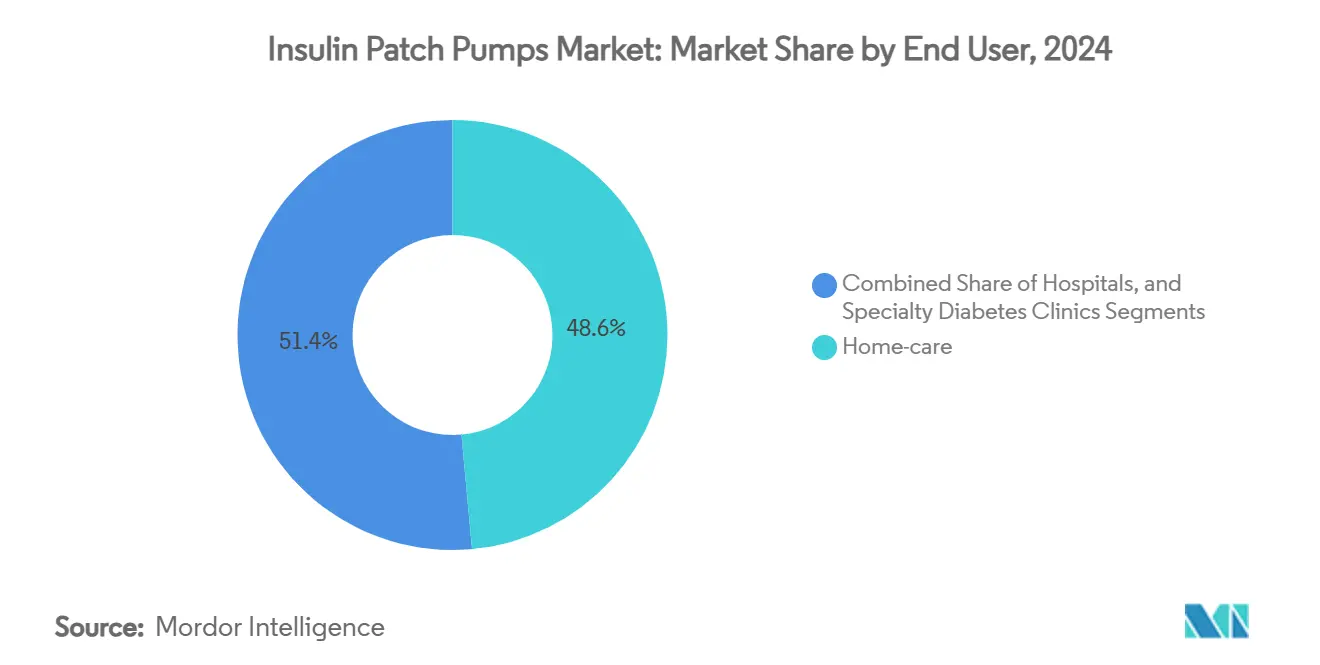

- By end user, home-care settings led with 48.56% share of the insulin patch pumps market size in 2024, climbing at 14.88% CAGR.

- By technology, CGM-integrated pumps held 56.42% of the insulin patch pumps market share in 2024 while growing 14.38% through 2030.

- By geography, North America commanded 37.74% of 2024 revenue; Asia-Pacific delivers the fastest 13.07% CAGR to 2030.

Global Insulin Patch Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Type-1 Diabetes Prevalence In High-Income Nations | +1.8% | North America & Europe | Long term (≥ 4 years) |

| Growing Adoption Of Tubeless AID Systems | +2.1% | Global | Medium term (2-4 years) |

| Reimbursement Expansion For Patch Pumps In Europe & APAC | +1.5% | Europe & Asia-Pacific | Short term (≤ 2 years) |

| Miniaturised Piezo-Micro-Pump Tech Enabling 7-Day Wear | +1.2% | Global | Medium term (2-4 years) |

| GLP-1 + Insulin Combination Regimens Boosting Basal Demand | +0.9% | North America & Europe | Medium term (2-4 years) |

| Employer-Paid Virtual Diabetes Clinics Bundling Patch Pumps | +0.7% | North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Type 1 Diabetes Prevalence In High-Income Nations

Roughly 9.5 million people live with Type 1 diabetes in 2025, and incidence in children and adolescents continues rising across 55 countries.[1]Graham Ogle et al., “Global Type 1 Diabetes Prevalence, Incidence, and Mortality Estimates 2025,” diabres.com Lifelong insulin dependence fuels preference for precise delivery platforms, which positions the insulin patch pumps market for durable growth. High-income healthcare systems support specialised diabetes clinics, certified educators, and remote monitoring hubs, all of which ease pump adoption. Socio-economic factors also influence device uptake as insurance coverage limits out-of-pocket costs. In these economies, physicians routinely recommend advanced AID solutions that maintain tight glycaemic targets while lowering hypo-risk, reinforcing sustained demand for tubeless patch devices.

Growing Adoption Of Tubeless AID Systems

Eliminating catheter lines removes occlusion events and improves user comfort, directly impacting adherence. Real-world data from more than 69,000 Omnipod 5 users indicated median time-in-range of 64.2%, climbing to 68.8% among those aiming for 110 mg/dL targets.[2]Jennifer L. Sherr, “Real-World Evidence of Omnipod 5 Automated Insulin Delivery System,” liebertpub.comUnited States regulatory frameworks that label pumps as “interoperable” foster open architectures linking multiple CGM brands, enabling broader physician choice.[3]FDA, “Interoperability Designation—Creating Options for People With Diabetes and Pump Companies,” pmc.nih.gov The result is a virtuous cycle: better outcomes drive higher prescriptions, while higher volumes help manufacturers scale production. Pediatric endocrinologists especially value the subtle profile and water-resistant build of tubeless platforms that children can keep on during school, sports, and sleep.

Reimbursement Expansion For Patch Pumps In Europe & APAC

France funded Omnipod 5 in 2024, and Spain’s national health service followed quickly, cutting patient pay-outs to virtually zero. Estonia, meanwhile, covers pumps and CGM supplies for people below 19 years, highlighting the region’s collective willingness to invest in technology that prevents costly complications. Asia-Pacific insurers have started pilot programs to subsidise patch devices for high-risk Type 1 cohorts, stimulated by middle-class demand and rising public-private partnerships. As comprehensive coverage lowers economic barriers, device penetration accelerates in both hospital initiation programs and home-care settings, enlarging the insulin patch pumps market.

Miniaturised Piezo-Micro-Pump Technology Enabling 7-Day Wear

Piezoelectric micro-actuators deliver insulin with flow precision down to 0.28 µL, consuming minimal battery power. Seven-day wear removes two site changes each week compared with three-day infusion sets, lightening patient workload and lowering skin-insertion trauma. Small form factors also enable discreet placement under clothing without compromising reservoir capacity, opening opportunities for dual-hormone innovations under investigation. Manufacturers now blend advanced polymers with bio-stable silicones to maintain elasticity and mechanical integrity throughout extended wear intervals, anchoring a new value curve that further differentiates patch systems from traditional pumps.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device & Consumable Cost Versus Pens | -1.4% | Global, particularly emerging markets | Long term (≥ 4 years) |

| Cyber-Security & Data-Privacy Vulnerabilities | -0.8% | Global | Medium term (2-4 years) |

| Environmental Waste Scrutiny For Disposable Pods | -0.6% | Europe & North America | Medium term (2-4 years) |

| Interoperability Lag With Next-Gen CGMs In Emerging Markets | -0.5% | Asia-Pacific & Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device & Consumable Cost Versus Pens

Traditional pens cost far less upfront, and patch pumps add recurring pod expenditure to the total cost of ownership. Embecta halted its newly cleared disposable patch program in late 2024, citing the need for further cost optimisation to match aggressive price benchmarks. In many Asia-Pacific nations, reimbursement either excludes adult Type 2 users or covers only a fraction of consumables, leaving patients to absorb expenses that can exceed average monthly wages. As a result, market penetration remains skewed toward affluent urban populations while rural clinics still rely on vial-and-syringe therapy.

Cyber-Security & Data-Privacy Vulnerabilities

Researchers have successfully reverse-engineered firmware on commercial pumps, exposing pathways for unauthorised dose commands that could trigger hypo- or hyperglycaemia. Although no large-scale attack has materialised, regulators are demanding software bills of materials and post-market patch plans, adding compliance costs. Lightweight cryptography and biometric locks offer protection but complicate user interfaces for elderly segments. Manufacturers must balance safety with ease of emergency access for caregivers, especially in paediatric settings, to sustain confidence in connected devices that anchor the insulin patch pumps market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Disposable Convenience Meets Reusable Momentum

Disposable patch pumps held 67.46% of 2024 revenue because their single-use design eliminates cleaning steps and cuts infection risk. Health professionals favor disposables for paediatric and immune-compromised groups, reinforcing their widespread deployment in outpatient programs. Manufacturers integrate precision control chips and Bluetooth radios without raising pod thickness, keeping wear discreet. Nevertheless, sustainable procurement policies encourage reevaluation of waste streams, and that opens runway for reusable formats.

Reusable variants post the fastest 14.26% CAGR through 2030 as reinforced cannula materials and longer-life adhesives extend wear cycles. Over time, lower pod turnover can trim annual supply costs despite higher device sticker prices, resonating with cost-constrained payers. Hospitals also appreciate reduced inventory volume, given that one rechargeable controller can pair with multiple refill kits. As technology gaps narrow, competition within the insulin patch pumps market shifts toward battery longevity, waterproofing depth, and cloud analytics rather than single-use or multi-use status.

By Delivery Mode: Integrated Basal & Bolus Control Sets the Pace

Basal-and-bolus patch pumps commanded 51.34% of the insulin patch pumps market size in 2024 as clinicians prefer all-in-one delivery to avoid juggling separate devices. Closed-loop algorithms need real-time access to both basal and bolus channels to smooth glucose peaks overnight and around meals, which reinforces integrated formats.

Segment growth at 13.69% CAGR reflects expanded use among newly diagnosed Type 1 youth and off-label adoption by Type 2 patients requiring intensive therapy. Clinical trials demonstrate sharper HbA1c reductions compared with basal-only regimens, strengthening payer justification for higher reimbursement tiers. Device makers now include quick-bolus tactile buttons and smartphone sliders, enabling on-the-go corrections without infusion-set reconnection, an advantage not available on conventional pumps.

By End User: Home-Care Embraces Digital Health Ecosystems

Home-care settings accounted for 48.56% share of 2024 demand as patients transition toward self-management supported by telehealth. Smartphones act as dashboards for real-time glucose trends, pod battery life, and refill reminders, lowering anxiety for first-time users.

Projected 14.88% CAGR stems from virtual coaching programs, same-day pod shipping, and automatic prescription refills that simplify adherence. Hospitals remain essential for initiation and acute stabilisation but discharge patients sooner, freeing beds and cutting costs. Specialty diabetes clinics hold niche roles focusing on algorithm fine-tuning and complex comorbidity cases. In aggregate, the home-centric model underpins a sizeable growth vector for the insulin patch pumps market.

By Technology: CGM Integration Becomes Standard of Care

CGM-integrated systems represented 56.42% of global revenue in 2024, expanding at 14.38% as evidence mounts that real-time data plus automated dosing drives superior outcomes. Open-protocol labeling lets users mix preferred sensors with pumps, though manufacturers still benefit from proprietary pairs that shorten troubleshooting cycles.

Future innovation will likely hinge on dual-analyte sensors that detect both glucose and ketones, enabling early ketoacidosis warnings. Partnerships such as Abbott–Tandem pave the way for firmware over-the-air updates that drop new predictive algorithms without device swaps, tightening upgrade loops. Stand-alone pumps remain relevant in regions where CGM reimbursement lags, but integrated offerings increasingly shape value perceptions in the insulin patch pumps market.

Geography Analysis

North America generated 37.74% of 2024 revenue, anchored by the United States where Insulet surpassed 500,000 active Omnipod users and continues double-digit sales gains. High private-insurance penetration, widespread AID literacy, and physician familiarity accelerate new prescriptions. Canada, aided by provincial reimbursement expansion, shows similar momentum, while Mexico widens pump inclusion in public-sector formularies.

Europe holds the second-largest position thanks to universal healthcare and structured paediatric diabetes programs. France’s 2024 Omnipod 5 listing signals broader cost-effectiveness recognition, and Germany channels value-based procurement to hospitals demonstrating reduced hypoglycaemia admissions. Sustainability mandates stimulate early pilots of recyclable pod shells, injecting new competitive criteria beyond glycaemic metrics.

Asia-Pacific posts the fastest 13.07% CAGR as urban middle classes adopt premium health technologies. China’s tertiary hospitals see fewer than 10 monthly CGM uses in two-thirds of wards, yet policy reforms seek to triple device access by 2030, an opportunity for the insulin patch pumps market. Japan and South Korea leverage domestic electronics expertise to co-develop miniaturised pumps, while India pilots state-funded CGM bundles for low-income youth. Regulatory alignment on sensor-pump interoperability will determine adoption velocity across Indonesia, Philippines, and Vietnam.

Competitive Landscape

The insulin patch pumps market remains moderately consolidated, with Insulet, Medtronic, and Tandem Diabetes Care controlling most global revenue. Insulet leads tubeless AID with multi-sensor compatibility, while Tandem capitalises on a durable pump strategy and Control-IQ+ algorithms for both Type 1 and Type 2 cohorts. Medtronic’s recall of certain MiniMed models in 2024 sharpened industry focus on reliability, yet the firm counters with a pipeline of smaller, fully disposable units.

Strategic alliances define the next phase. Abbott’s linkage of FreeStyle Libre sensors to Medtronic and Tandem platforms illustrates CGM makers’ pivot toward pump-agnostic ecosystems. Patent acquisitions, such as Insulet’s buy-out of Bigfoot Biomedical intellectual property, secure algorithmic know-how and block late-stage entrants. Asian challengers EOFlow and MicroTech Medical scale low-cost variants, targeting national reimbursement rosters that privilege local suppliers.

Product roadmaps now emphasise water-proof depth ratings, integrated bolus calculators, and extended pod life to differentiate. Software upgrades delivered through encrypted cloud portals convert installed bases into subscription revenue, creating annuity-like cash flows. As cybersecurity compliance tightens, established brands leverage broader regulatory teams to outpace smaller rivals on documentation, raising entry barriers.

Insulin Patch Pumps Industry Leaders

Insulet Corporation

Medtronic plc

Tandem Diabetes Care Inc.

CeQur SA

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Tandem Diabetes Care confirmed t:slim X2 compatibility with Abbott FreeStyle Libre 3 Plus in the United States, with phased distribution in H2 2025.

- June 2025: PharmaSens formed a development alliance with SiBionics to launch an all-in-one patch pump based on the Niia Essential platform.

- January 2025: Medtronic previewed a next-generation tubeless pump architecture scheduled for multi-region rollout in 2026.

Global Insulin Patch Pumps Market Report Scope

| Disposable Patch Pumps |

| Reusable Patch Pumps |

| Basal Patch Pumps |

| Bolus Patch Pumps |

| Basal & Bolus Patch Pumps |

| Home-care Settings |

| Hospitals |

| Specialty Diabetes Clinics |

| Stand-alone Patch Pumps |

| CGM-integrated / Automated Patch Pumps |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Disposable Patch Pumps | |

| Reusable Patch Pumps | ||

| By Delivery Mode | Basal Patch Pumps | |

| Bolus Patch Pumps | ||

| Basal & Bolus Patch Pumps | ||

| By End User | Home-care Settings | |

| Hospitals | ||

| Specialty Diabetes Clinics | ||

| By Technology | Stand-alone Patch Pumps | |

| CGM-integrated / Automated Patch Pumps | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current insulin patch pumps market size?

The market generated USD 1.36 billion in 2025 and is forecast to reach USD 2.23 billion by 2030.

2. Which product type leads the insulin patch pumps market?

Disposable patch pumps held 67.46% revenue share in 2024 due to ease of use and low infection risk.

3. How fast is the CGM-integrated segment growing?

CGM-integrated systems are expanding at 14.38% CAGR as automated dosing becomes the standard of care.

4. Why is Asia-Pacific the fastest-growing region?

Rising diabetes prevalence, expanding insurance coverage, and improving healthcare infrastructure lift Asia-Pacific to a 13.07% CAGR.

5. What are key restraints for market growth?

High device costs, cybersecurity risks, environmental concerns over disposables, and limited sensor-pump interoperability in emerging markets.

Page last updated on: