Compression Socks Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.32 Billion |

| Market Size (2030) | USD 1.71 Billion |

| Growth Rate (2025 - 2030) | 5.50% CAGR |

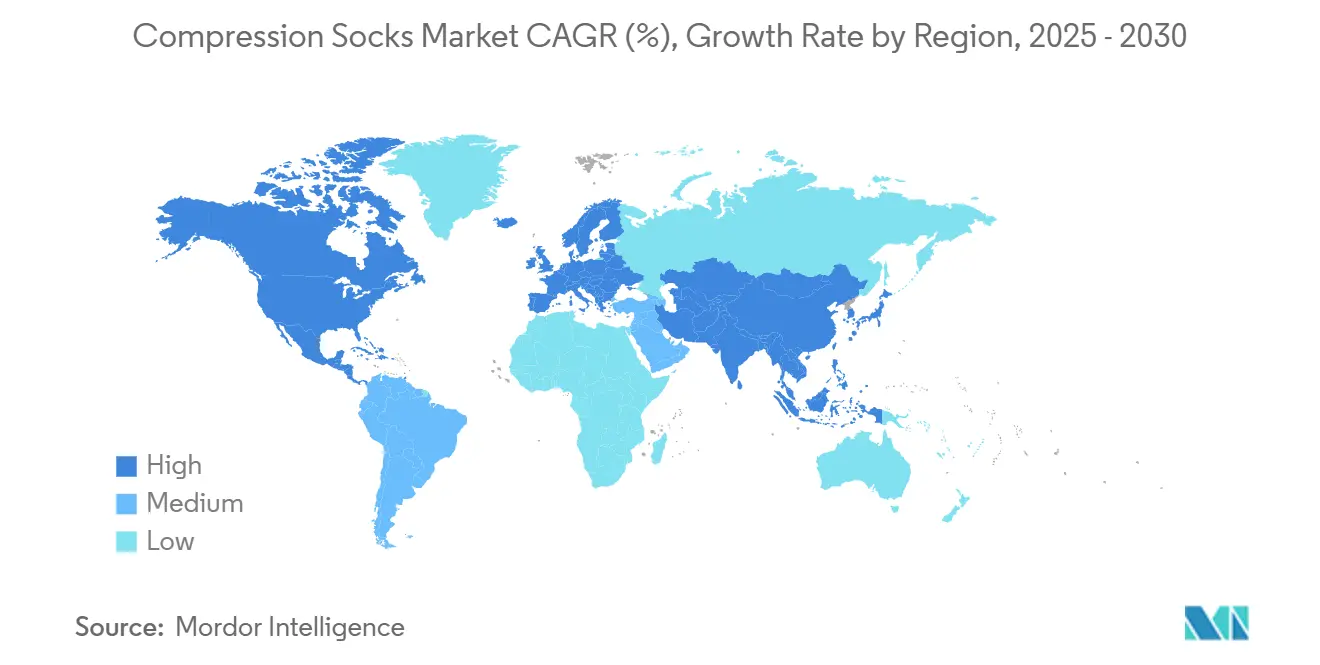

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

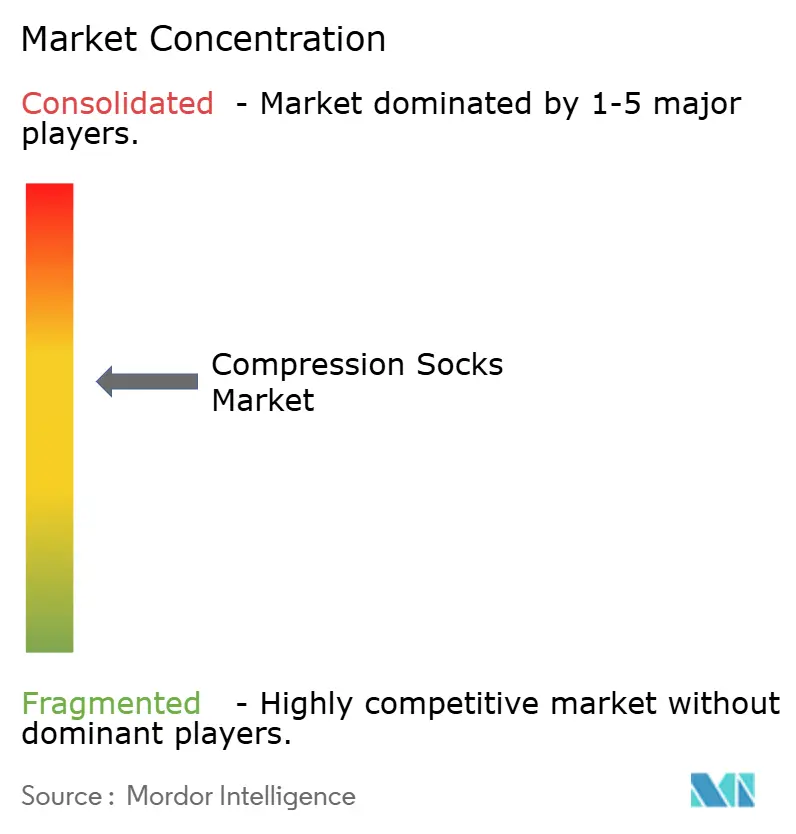

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Compression Socks Market Analysis by Mordor Intelligence

The compression socks market size reached USD 1.32 billion in 2025 and is forecast to climb to USD 1.71 billion by 2030, advancing at a 5.5% CAGR over 2025-2030. Steady demand stems from rising venous disease prevalence, rapid population aging, and broader use of compression garments by athletes and wellness-oriented consumers. Innovation around smart textiles is improving pressure accuracy and comfort. At the same time, favorable policy moves such as the Lymphedema Treatment Act in the United States have lowered reimbursement barriers for medical-grade products. North America leads the compression socks market thanks to robust clinical infrastructure and high patient awareness; Asia-Pacific is the fastest-growing region as healthcare modernization and e-commerce adoption accelerate. Companies are responding with digitally enabled direct-to-consumer models, strategic acquisitions, and product portfolios that balance therapeutic efficacy with style preferences.

Key Report Takeaways

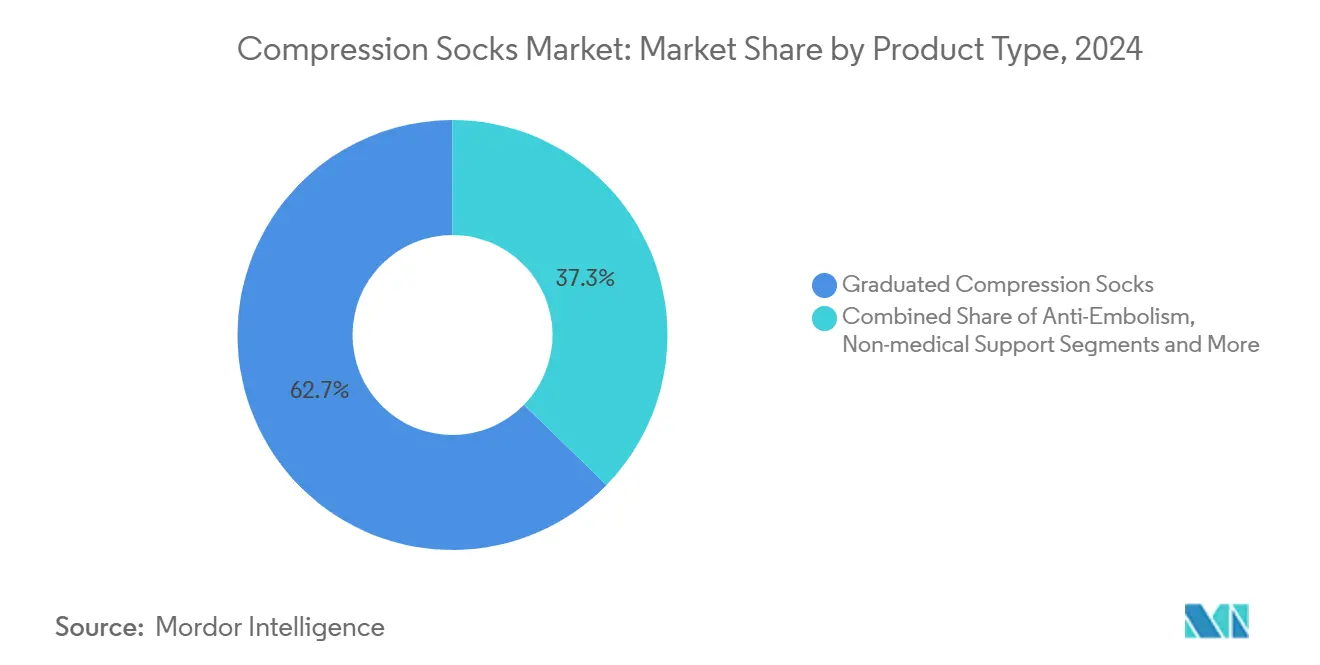

- By product type, graduated compression socks captured 62.7% of the compression socks market share in 2024; bright textile socks are projected to expand at a 13.5% CAGR through 2030.

- By compression level, the 20-30 mmHg category commanded 37.4% share of the compression socks market size in 2024, while 30-40 mmHg is set to post the fastest 8.3% CAGR.

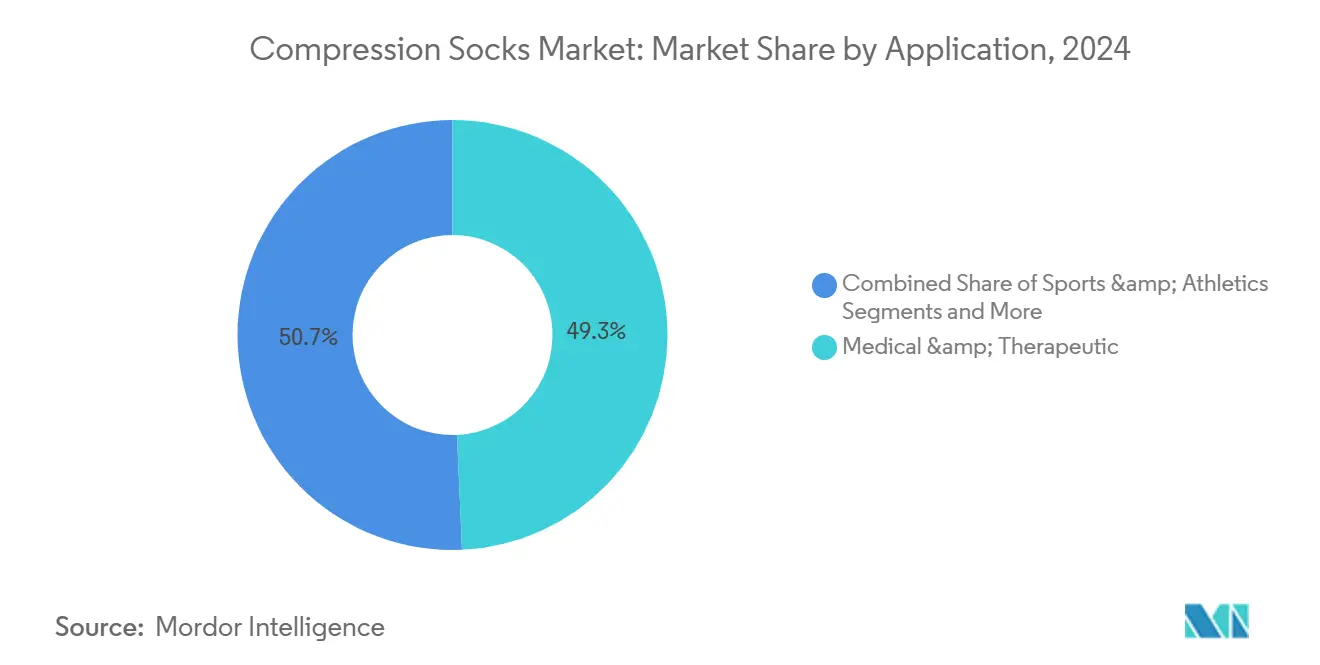

- By application, medical & therapeutic use accounted for 49.3% of the compression socks market size in 2024, and sports & athletics is advancing at a 10.2% CAGR to 2030.

- By distribution channel, offline retail pharmacies led with 46.5% revenue share in 2024; online direct-to-consumer sales are forecast to grow at 11.5% CAGR.

- By geography, North America held 35.8 of % compression socks market share in 2024; Asia-Pacific shows the highest regional CAGR at 8.2%.

Global Compression Socks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Venous Disorders & Lymphedema | +1.20% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Geriatric Population Expansion Raising Chronic Venous Insufficiency Cases | +1.00% | Global, highest impact in Asia Pacific & Europe | Long term (≥ 4 years) |

| Growing Adoption Among Runners & Endurance Athletes | +0.80% | North America, Europe, emerging in Asia Pacific | Short term (≤ 2 years) |

| Rapid E-Commerce Penetration Of Medical Hosiery | +0.70% | Global, led by North America & Asia Pacific | Short term (≤ 2 years) |

| Occupational PPE Adoption By Long-Haul Transport & Airline Crews | +0.50% | Global, concentrated in major aviation hubs | Medium term (2-4 years) |

| Emergence Of Smart-Textile Pressure-Sensing Socks | +0.30% | North America & Europe initially, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Venous Disorders & Lymphedema

Clinical guidelines position compression therapy as first-line care for chronic venous insufficiency and lymphedema. Medicare now covers standard and custom garments under the Lymphedema Treatment Act, permitting three daytime garments every six months and two nighttime garments every two years.[1]Centers for Medicare & Medicaid Services, “Lymphedema Compression Treatment Items,” cms.gov Clear reimbursement pathways are easing cost burdens and expanding physician prescriptions. Clinical studies show that lipedema patients using advanced pneumatic compression devices report significantly improved quality of life compared with traditional methods.[2]Karen L. Herbst et al., “An Advanced Pneumatic Compression Therapy System Improves Leg Volume and Quality of Life in Lipedema,” Life, mdpi.com FDA Class I regulation further assures clinicians of safety and performance, lifting adoption among vascular specialists. Combined, these factors underpin resilient demand in mature healthcare systems and create a benchmark that emerging markets aim to replicate.

Geriatric Population Expansion Raising Chronic Venous Insufficiency Cases

Asia-Pacific is aging faster than any other region; South Korea, for example, will hold the highest elderly-population ratio in Asia by 2045. Older adults face higher incidences of venous reflux, swelling, and ulceration that respond well to compression therapy. National health plans view garments as cost-effective tools that reduce hospitalization and surgical expenses. MedTech revenues in the region are on course to reach USD 190 billion by 2025, signaling strong procurement capacity for compression devices.[3]APACMed, “MedTech in Asia: Committing at Scale,” apacmed.org European markets mirror this demographic pull, sustaining steady baseline demand. Over the long term, broadening insurance coverage and telehealth-based follow-up programs will amplify prescription volumes among seniors.

Growing Adoption Among Runners & Endurance Athletes

Evidence indicates graduated socks enhance calf pump efficiency, shorten recovery intervals, and curb muscle vibration during high-impact sports. Brands historically tied to medical segments are now partnering with professional teams, broadening awareness among recreational runners. Product catalogs emphasize breathability, color options, and inclusive sizing, which resonates with millennials and Gen Z seeking both function and style. Athletic events and marathon expos have become key retail nodes for direct engagement and on-site fitting. As clinical and performance benefits converge, sports retail outlets increasingly stock medical-grade options, blurring lines between healthcare and athletic categories.

Rapid E-Commerce Penetration of Medical Hosiery

Global e-commerce volumes for medical hosiery are climbing as consumers appreciate doorstep delivery and detailed sizing guides. Direct-to-consumer storefronts give manufacturers higher margins and access to anonymized usage data that feeds iterative design. Virtual fitting tools use smartphone cameras to recommend pressure classes, reducing returns and boosting patient compliance. Pandemic-era buying habits entrenched digital pathways, and the trend persists as broadband penetration rises in Southeast Asia and Latin America. Regulatory bodies are also digitizing prescription authentication, allowing pharmacies to verify documentation online and ship insured garments nationwide.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Out-Of-Pocket Cost | -0.80% | Global, highest impact in emerging markets | Medium term (2-4 years) |

| Limited Clinician Awareness In Developing Nations | -0.60% | Asia Pacific, Middle East & Africa, South America | Long term (≥ 4 years) |

| Skin-Microclimate Compliance Drop In Hot-Humid Regions | -0.50% | Southeast Asia, Sub-Saharan Africa, tropical regions | Short term (≤ 2 years) |

| Substitution Threat From Pneumatic Compression Wearables | -0.40% | North America & Europe, expanding to developed APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Out-Of-Pocket Cost

Medical-grade socks cost three to five times more than basic hosiery, limiting access in uninsured populations. Outside the United States, most payers do not reimburse compression garments, forcing users to self-fund treatments. Lower-cost retail versions often lack validated pressure profiles, risking suboptimal outcomes and eroding clinician confidence. Manufacturers have introduced tiered product lines and bundle programs that include donning aids to justify price premiums. Yet sustained growth in the compression socks market depends on broader insurance adoption and value-based pricing models that match clinical benefits with affordability.

Limited Clinician Awareness in Developing Nations

Many physicians in lower-income regions receive little formal training on compression protocols, sizing, and contraindications. Disparate regulatory standards further complicate market entry and lead to inconsistent product quality. Industry associations now fund continuing medical education modules and sponsor residency electives that emphasize conservative venous management. Pilot projects in Malaysia and Kenya reveal prescription rates can double once local champions run workshops and distribute fitting guides. Nevertheless, progress is slow, and the compression socks market in these geographies will expand only when systemic education gaps close.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Smart Textiles Gain Momentum

Graduated socks retained dominance with 62.7% of the compression socks market share in 2024, reflecting decades of clinical trust among vascular surgeons. These garments apply peak pressure at the ankle and taper proximally, promoting venous return and mitigating edema. Smart-textile models, though still niche, are clocking a 13.5% CAGR as embedded sensors log real-time pressure distribution and prompt user adjustments via mobile apps. Clinical trials confirm that low-frequency electrical stimulation delivered through integrated electrodes boosts calf pump action without added discomfort. Anti-embolism socks remain hospital staples for bedridden patients, while open-toe designs serve warmer climates and podiatric conditions. Continuous yarn innovations, such as silver nanowires and advanced nano-coatings, support wash durability and conductivity, enhancing the long-term value proposition.

These advances widen consumer choice and foster cross-selling: athletes, frequent flyers, and post-surgical patients now gravitate toward unified lines that combine therapeutic pressure with breathable, antimicrobial fabrics. As digital health ecosystems mature, bright socks can sync with telehealth dashboards, giving clinicians compliance insight and facilitating remote adjustments. The agile brands that iterate sensor firmware and partner with electronic-component suppliers hold clear competitive advantages in the next development cycle of the compression socks market.

By Compression Level: Moderate Pressure Remains the Workhorse

Products delivering 20-30 mmHg captured the highest share of the compression socks market size at 37.4% in 2024, balancing symptom relief with day-long wear comfort. Physicians reserve 30-40 mmHg for more advanced venous or lymphatic impairment, and that class is posting the quickest 8.3% CAGR as aging cohorts present with severe disease. Lower ranges of 15-20 mmHg cater to wellness buyers who desire light support during prolonged standing or air travel. Conversely, pressures above 40 mmHg serve refractory lymphedema and post-surgical recovery scenarios under close clinical supervision.

Stringent testing and labeling ensure pressure accuracy throughout the product life cycle. Manufacturers increasingly publish digital certificates on product pages, allowing therapists to verify conformity before prescribing. Electrical-stimulation socks now target 1 Hz impulse frequencies, a setting that improves venous hemodynamics with less perceived exertion compared with higher frequencies. Collectively, these developments elevate patient adherence, pointing toward a future where compression class selection also factors in sensor-driven feedback loops to refine therapy on the fly.

By Application: Medical Dominance with Athletic Upside

Medical and therapeutic uses held 49.3% of the compression socks market size in 2024, as guidelines recommend garments for chronic venous insufficiency, deep vein thrombosis prophylaxis, and lymphedema management. Hospitals embed compression therapy in peri-operative protocols, and home-health providers supply replacement pairs under durable-medical-equipment benefits. Sports and athletics, however, are rising fastest at a 10.2% CAGR as runners, cyclists, and basketball players adopt compression socks to shorten recovery intervals and minimize delayed-onset muscle soreness.

Evidence shows no detrimental effect on oxygen consumption or heart rate during extended runs, supporting performance claims. Travel, maternity, and general wellness segments round out demand, each seeking tailored pressures and fabric blends. Hybrids capable of shifting from high-impact workout to casual office wear illustrate how product lines blur traditional application silos, enlarging addressable buyers inside the compression socks market.

By Distribution Channel: Digital Direct Makes Inroads

Offline retail pharmacies still lead at 46.5% share, benefiting from pharmacist counseling, insurance billing, and tactile fitting. Yet online direct-to-consumer avenues are the fastest-growing at 11.5% CAGR, fueled by secure checkout, instructional videos, and subscription replenishment models. Specialist e-commerce platforms partner with tele-clinics to issue electronic prescriptions that auto-populate pressure class and size, streamlining patient journeys.

Hospital and clinic stores maintain relevance for immediate post-procedure garments, while specialty sports retailers stock bright, moisture-wicking lines that double for medical needs. Crucially, omnichannel strategies now integrate inventory between brick-and-mortar and online portals, letting buyers start virtual fittings at home and finish purchases in pharmacies to confirm sizing. This fluid approach broadens reach and supports stable growth in the compression socks market.

By Compression Level: Quantifying Pressure Needs

The mid-pressure 20-30 mmHg band dominated with 37.4% compression socks market share in 2024; use cases include mild edema, orthostatic intolerance, and early venous reflux. Segment growth remains linked to standardized sizing charts and easier donning aids that deter patient dropout. The high-pressure 30-40 mmHg class is tracking an 8.3% CAGR, underpinned by strong physician recommendations for stage II lymphedema and post-ulcer care. Above 40 mmHg products occupy a narrow but critical niche, often custom-made and reimbursed through specialized DMEPOS codes.

Independent laboratories employ advanced systems to confirm pressure decay after multiple wash cycles, ensuring real-world performance aligns with labeled values. Added certifications simplify cross-border commerce inside the compression socks market, as regulators accept mutual recognition agreements and expedite import approvals.

Geography Analysis

North America retained the most significant share at 35.8% in 2024, driven by broad reimbursement, advanced clinical pathways, and widespread physician training. The Lymphedema Treatment Act, effective January 2024, created fresh sales channels for standard and custom garments under Medicare Part B. Hospital purchasing groups quickly updated formularies, while pharmacies launched public-education campaigns that boosted consumer recognition of compression benefits. Canada follows the United States with universal coverage for severe lymphedema patients, and Mexico is piloting state-funded ulcer-prevention programs that include subsidized socks.

Europe ranked second in consistent MDR oversight, established textile-testing infrastructure, and strong patient advocacy communities. National health services in Germany, France, and the Nordic countries reimburse two or more pairs annually, stabilizing baseline volumes. Warmer Mediterranean climates favor open-toe variants, while alpine regions prefer thermal blends, illustrating how micro-climates influence buying patterns.

Asia-Pacific posted the quickest 8.2% CAGR, propelled by demographic aging, e-commerce penetration, and rising disposable income. South Korea’s rapidly aging population has drawn Japanese and European suppliers to open local distribution hubs. China and India present high-volume prospects; both nations now accept electronic import documentation, cutting lead times for foreign brands. Middle East & Africa and South America remain nascent but promising; public-health outreach programs focused on venous-disease prevention are expected to nurture gradual compression socks market adoption.

Competitive Landscape

The compression socks market is moderately fragmented. Medical-device stalwarts—Sigvaris Group, medi GmbH, and Julius Zorn—leverage decades of vascular expertise and strong clinic ties to defend their share. Athletic giants such as Nike and Adidas participate through co-branded recovery lines. Yet, specialized sports labels like CEP (Medi subsidiary) offer broader size ranges and medical-grade pressures, securing loyalty among endurance athletes. Thuasne’s May 2024 acquisition of Corflex consolidated its orthotics and compression portfolio in the United States, streamlining logistics and cross-selling opportunities.

Technology acts as a decisive differentiator. Cardinal Health launched the Kendall SCD SmartFlow system in November 2024; its Vascular Refill Detection feature personalizes inflation patterns, promising better clot prevention for inpatients. Smaller innovators embed printable circuits into yarns, enabling cloud-linked pressure monitoring without altering hand-feel. Patenting activity concentrates on conductive-polymer blends, reflecting a race to integrate diagnostics while maintaining textile comfort.

Distribution strategies mirror product complexity. High-pressure custom garments move predominantly through prescription-based DMEPOS channels, whereas mid-pressure athletic variants flourish online. European producers capitalize on the Made-in-Germany cachet, emphasizing RAL-certified pressure accuracy in marketing. U.S. companies deploy educational webinars for physical therapists, while Asian entrants exploit localized manufacturing to undercut import prices. Collectively, these maneuvers sustain competitive intensity and propel steady innovation across the compression socks market.

Compression Socks Industry Leaders

Sigvaris Group

medi GmbH & Co. KG

Julius Zorn GmbH (Juzo)

Bauerfeind AG

Thuasne Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: French medical-device specialist Thuasne completed its purchase of Knit-Rite and its Therafirm division. This marks Thuasne's fourth and largest U.S. deal in the past decade. The latest acquisition not only bolsters Thuasne’s compression-hosiery manufacturing capabilities but also expands the group's regulatory expertise across the U.S., France, and Germany.

- March 2024: AMERX Health Care’s Extremit-Ease sleeve became the first product approved under the new HCPCS code A6583, following the implementation of the Lymphedema Treatment Act on January 1, 2024. This act allows Medicare beneficiaries with lymphedema to receive up to three garments for each affected limb every six months, creating a clear reimbursement process for both patients and suppliers.

- March 2024: U.S. brand Joocla addressed a common challenge by launching compression socks with a discreet side zipper. This thoughtful design makes it easier for users with limited mobility to put on and take off medical-grade hosiery, combining therapeutic benefits with everyday convenience.

Global Compression Socks Market Report Scope

| Graduated Compression Socks |

| Anti-Embolism Compression Socks |

| Non-medical Support Socks |

| Smart Textile Compression Socks |

| Open-Toe Compression Socks |

| 15-20 mmHg |

| 20-30 mmHg |

| 30-40 mmHg |

| 40-50 mmHg |

| Above 50 mmHg |

| Medical & Therapeutic |

| Sports & Athletics |

| Travel & Aviation |

| Pregnancy & Maternity |

| Wellness & Lifestyle |

| Offline Retail Pharmacies |

| Hospital & Clinic Stores |

| Specialty Stores |

| Online Direct-to-Consumer |

| E-commerce Marketplaces |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Graduated Compression Socks | |

| Anti-Embolism Compression Socks | ||

| Non-medical Support Socks | ||

| Smart Textile Compression Socks | ||

| Open-Toe Compression Socks | ||

| By Compression Level | 15-20 mmHg | |

| 20-30 mmHg | ||

| 30-40 mmHg | ||

| 40-50 mmHg | ||

| Above 50 mmHg | ||

| By Application | Medical & Therapeutic | |

| Sports & Athletics | ||

| Travel & Aviation | ||

| Pregnancy & Maternity | ||

| Wellness & Lifestyle | ||

| By Distribution Channel | Offline Retail Pharmacies | |

| Hospital & Clinic Stores | ||

| Specialty Stores | ||

| Online Direct-to-Consumer | ||

| E-commerce Marketplaces | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the compression socks market in 2030?

The market is forecast to reach USD 1.71 billion by 2030.

Which region will grow fastest through 2030?

Asia-Pacific is expected to post the highest 8.2% CAGR owing to healthcare modernization and e-commerce expansion.

Which compression level currently sells the most units?

The 20-30 mmHg category dominates, holding a 37.4% share in 2024.

Who are the leading medical-grade manufacturers?

Key players include Sigvaris Group, medi GmbH, Julius Zorn, and Thuasne.

How did the Lymphedema Treatment Act affect U.S. demand?

The Act expanded Medicare coverage for garments, driving higher prescription volumes and opening new supplier channels.

Page last updated on: