Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

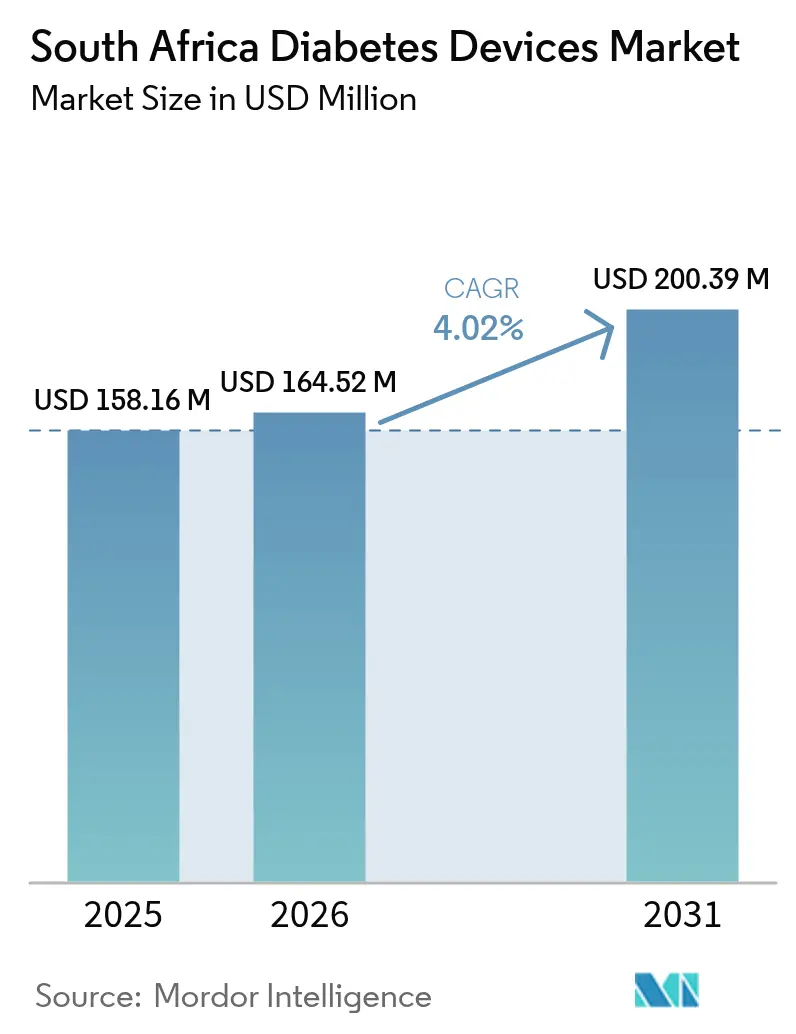

| Base Year Market Size (2025) | USD 158.16 Million |

| Market Size (2026) | USD 164.52 Million |

| Market Size (2031) | USD 200.39 Million |

| Growth Rate (2026 - 2031) | 4.02% CAGR |

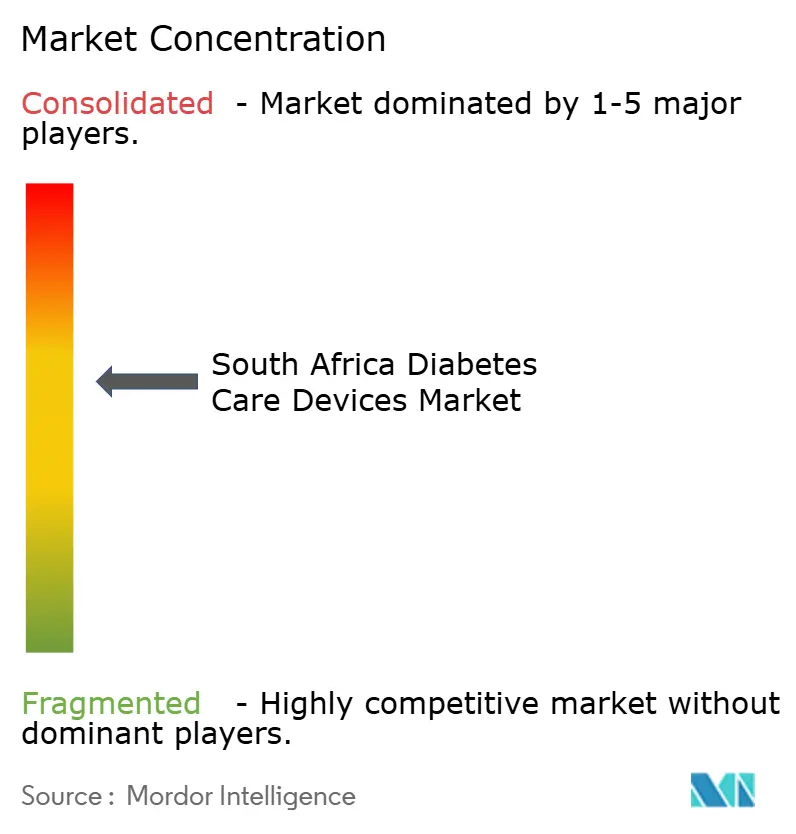

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Diabetes Devices Market Analysis by Mordor Intelligence

South Africa diabetes devices market size in 2026 is estimated at USD 164.52 million, growing from 2025 value of USD 158.16 million with 2031 projections showing USD 200.39 million, growing at 4.02% CAGR over 2026-2031. Growing urban diabetes prevalence, the roll-out of National Health Insurance coverage, and steady technology upgrades in monitoring and delivery devices underpin this expansion. Continuous glucose monitoring (CGM) is taking hold after new 2023 clinical guidance, while e-commerce is broadening access to supplies and widening consumer choice. Local production incentives are beginning to trim costs for test strips and create new jobs. The market also benefits from private medical schemes that now reimburse advanced pumps and sensors, lifting adoption among insured patients and easing long-term complication risks.

Key Report Takeaways

- By device category, Self-Monitoring Blood Glucose held 61.35% of South Africa diabetes devices market share in 2025; Continuous Glucose Monitoring is projected to expand at a 6.24% CAGR through 2031.

- By management device, insulin disposable pens accounted for 44.40% of the South Africa diabetes devices market size in 2025, while insulin pumps are forecast to grow at 4.75% CAGR to 2031.

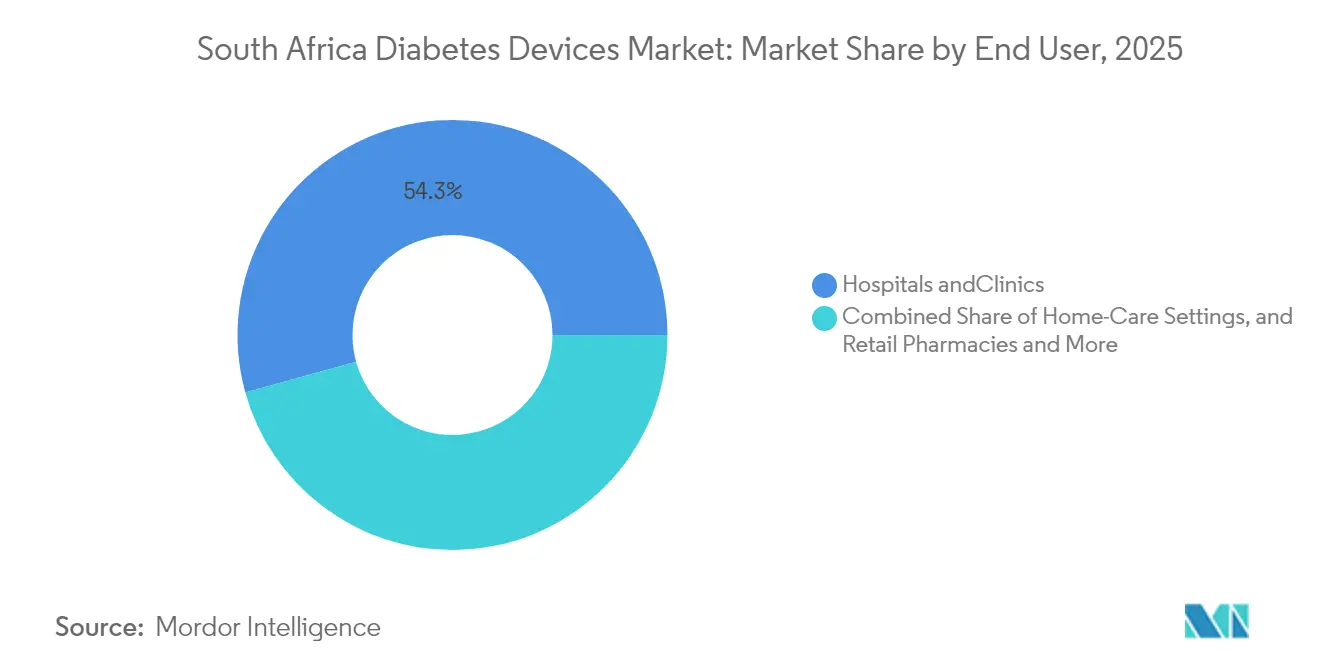

- By end user, hospitals and clinics led with 54.30% revenue share in 2025; home-care settings record the highest projected 4.58% CAGR between 2026-2031.

- By distribution channel, hospital pharmacies commanded 61.20% of 2025 sales, whereas e-commerce platforms are advancing at a 4.96% CAGR to 2031.

- Abbott, Roche, and Medtronic together supplied more than 59.75% of high-end CGM and pump revenues in 2025, reflecting their leadership in advanced technologies.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Diabetes Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of diabetes and obesity in urban South Africa | +1.0% | National urban centers | Long term (≥ 4 years) |

| Expansion of National Health Insurance reimbursement for glucose-testing supplies | +0.8% | Public healthcare facilities | Medium term (2-4 years) |

| Uptake of flash/continuous glucose monitoring after 2023 guidelines | +1.2% | Urban and private sector | Medium term (2-4 years) |

| Private medical schemes improving insulin-pump affordability | +0.6% | Private healthcare | Short term (≤ 2 years) |

| Local manufacture incentives lowering SMBG strip prices | +0.4% | National | Medium term (2-4 years) |

| Smartphone-connected ecosystem driving home-based self-care | +0.6% | High-penetration urban areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Diabetes & Obesity in Urban South Africa

Urban lifestyles are pushing type 2 diabetes incidence to 10.9% of the population, doubling over six years [1]Raylton Chikwati, “Study Shows Type 2 Diabetes Doubled in Sub-Saharan Africa in 6 Years,” Wits University, wits.ac.za. Men and younger adults carry disproportionate risk, opening sizable addressable demand for affordable monitoring devices. Direct medical spending linked to diabetes is set to climb 35% by 2030, making prevention of acute complications through regular testing an economic priority. Device makers focusing on cost-effective meters and connected apps can tap this expanding urban base.

Expansion of National Health Insurance Reimbursement for Glucose-Testing Supplies

The National Health Insurance Bill emphasises chronic disease support, bringing test strips and basic meters onto reimbursement lists for the 84% of citizens served by public clinics [2]Second Presidential Health Compact 2024-2029, Republic of South Africa, stateofthenation.gov.za. As phased coverage rolls out, regular SMBG becomes financially viable for many first-time users. Volume growth is expected first in public facilities before cascading into community pharmacies and mobile clinics.

Rapid Uptake of Flash/Continuous Glucose Monitoring After 2023 DOH Guidelines

Department of Health guidance released in 2023 positions CGM as standard care for intensive insulin therapy. Sensors backed by private medical scheme funding show HbA1c falls of 1.3 percentage points and a 67% drop in diabetes-related hospitalisations [3]Gregory J. Norman et al., “Initiating Continuous Glucose Monitoring Is Associated with Improved Glycemic Control,” Journal of Managed Care & Specialty Pharmacy, jmcp.org. These clinical gains underpin the segment’s 6.5% CAGR outlook and encourage clinicians to move eligible patients from finger-stick routines to sensor-based feedback.

Private Medical Schemes Boosting Insulin-Pump Affordability

Schemes such as Discovery Health spread pump payments across subscription periods, easing upfront expenses while tying coverage to proven clinical benefit. Uptake among the 16.2% privately insured population is steadily rising, narrowing the therapy gap with wealthier countries and stimulating demand for both conventional and hybrid closed-loop systems.

Local Manufacture Incentives Cutting SMBG Strip Prices

The Medical Devices Masterplan seeks to trim the country’s 90% import reliance by fostering domestic strip and meter output [4] “Draft of the South African Medical Devices Masterplan,” TIPS, tips.org.za. Emerging plants already supply public tenders at lower cost, lifting testing adherence and cushioning supply chains against global disruptions witnessed during 2024 insulin pen shortages.

Smartphone-Connected Ecosystem Driving Home-Based Self-Care

Smartphone penetration above 95% among people living with diabetes enables near-real-time sharing of glucose data and teleconsultation. Cloud-linked meters and sensors feed analytics that help clinicians adjust therapy without face-to-face visits, relieving pressure on overstretched clinics and making self-management more convenient.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High out-of-pocket cost of pumps & CGM for uninsured populations | -0.8% | National low-income areas | Medium term (2-4 years) |

| Import duties and logistics bottlenecks on medical devices | -0.6% | National | Short term (≤ 2 years) |

| Shortage of endocrinologists limiting device prescriptions | -0.4% | Rural zones | Long term (≥ 4 years) |

| Grey-market test-strip counterfeiting undermining trust | -0.2% | Urban & border regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Cost of Pumps & CGM for Uninsured Populations

Advanced devices can cost several months of median wages, restricting use to a small slice of the population. Public clinic audits show only 23% of patients reach target glucose levels, underlining the clinical gap. Broader insurance coverage and progressive price cuts remain essential for equitable access.

Shortage of Endocrinologists Limiting Device Prescriptions

South Africa trains few new endocrinologists each year, leaving rural districts without specialist oversight. Primary care clinicians cite limited time for device counselling, slowing pump and CGM penetration despite proven benefits. Tele-endocrinology and decision-support software present interim solutions

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Category: Monitoring Devices – CGM Adoption Accelerates

SMBG systems retained a 61.35% value lead in 2025 thanks to their low unit cost and broad public familiarity. Yet CGM sales are growing fastest at a 6.24% CAGR, reflecting stronger clinical evidence and wider reimbursement. SMBG test strips continue to generate stable recurring revenue, and local strip production is expected to reduce patient spend by double-digit percentages. Research into non-invasive biosensors using carbon nanostructures signals future disruption.

Competitive focus in monitoring is shifting toward data platforms that overlay lifestyle advice onto glucose trends. Device makers offering seamless Bluetooth links to widely used smartphones position themselves to win loyalty as patients demand integrated tracking of diet, exercise, and medication timing.

By Device Category: Management Devices – Pumps Gain Momentum

Insulin disposable pens supplied 44.40% of segment revenue in 2025, underlining their practicality and familiarity. The South Africa diabetes devices market size tied to pen cartridges will expand further once local insulin production from the Novo Nordisk–Aspen partnership comes onstream in 2026. Insulin pump volumes, though smaller, are climbing at 4.75% CAGR as financing schemes improve affordability. Hybrid closed-loop systems integrating CGM feedback cut hypoglycaemic episodes and boost perceived quality of life, supporting steady uptake among type 1 users. Syringes and jet injectors remain critical for price-sensitive and rural segments where refrigeration and training resources are limited.

By End User: Home-Care Settings Expand Through Digital Integration

Hospitals and clinics contributed 54.30% of 2025 revenue, reflecting their role in initiating therapy and handling acute events. Home-care settings, however, show the strongest 4.58% CAGR as connected meters and sensors synchronise with teleconsult platforms. This transition lets overstretched facilities allocate specialist time to complex cases while maintaining oversight of patients remotely. Pharmacies now provide device training and refill reminders, creating a continuum of care outside hospital walls.

Community health workers equipped with mobile apps can guide patients in rural areas, further broadening adoption. Artificial-intelligence tools that predict glucose excursions ahead of time increase patient confidence and adherence, reinforcing growth in home-care demand.

By Distribution Channel: E-Commerce Disrupts Traditional Supply Lines

Hospital pharmacies delivered 61.20% of 2025 turnover by bundling device dispensation with clinic visits. Retail chains such as Clicks and Dis-Chem add reach in peri-urban zones, offering point-of-care HbA1c tests and counselling. E-commerce platforms, rising at a 4.96% CAGR, enable doorstep delivery of sensors and strips, particularly appeals to younger consumers. Transparent pricing and subscription models for consumables improve planning and cut lapsed testing episodes. Regulatory clarity on online pharmacy operations released in 2024 helped resolve concerns on cold-chain and patient verification, paving the way for new entrants.

Geography Analysis

Urban hubs—Johannesburg, Cape Town, and Durban—anchor demand for advanced CGM and pump technologies thanks to higher prevalence, stronger purchasing power, and specialist availability. Private hospitals in these cities serve as early adopters, generating demonstration effects that spur uptake in adjacent municipalities. The South Africa diabetes devices market size tied to Gauteng province alone exceeded USD 46.62 million in 2025.

Rural provinces experience lower device penetration due to lower incomes and sparse endocrinologist coverage. Spatial mapping shows Bojanala District recorded the most screening activity, whereas Dr Ruth Segomotsi Mompati saw the least . Mobile clinics using connected meters help bridge gaps by pushing data to urban specialists for feedback. National Health Insurance aims to level access by standardising device formularies across public facilities, which could lift basic SMBG usage in underserved provinces over the forecast period.

Border regions face heightened counterfeit risk. SAHPRA redoubled surveillance following a 2024 WHO alert on falsified diabetes medicines. Enforcement and patient education are central to rebuilding trust and safeguarding outcomes.

Competitive Landscape

Global majors Abbott, Roche, and Medtronic dominate high-tech segments through established sensor and pump franchises, long-standing clinician relationships, and post-sale support networks. Abbott’s FreeStyle Libre sensors paired with GLP-1 regimens showed encouraging real-world outcomes in South African cohorts, reinforcing the brand within endocrinology circles. Roche leverages its Accu-Chek franchise to cross-sell cloud dashboards that integrate both SMBG and CGM data. Medtronic’s MiniMed pumps appeal to tech-savvy type 1 users seeking automated insulin delivery.

Regional manufacturers concentrate on low-cost SMBG strips and meters to meet public tender specifications. Government incentives for domestic production and preferential procurement help these firms secure volume contracts, eroding import dependence. Digital health start-ups partner with device makers to add predictive analytics that extend specialist reach, a key differentiator in a market constrained by workforce shortages.

Competition is now less about single devices and more about ecosystem breadth. Companies that combine reliable hardware, cloud platforms, and local service centres are best placed to deepen market penetration and maintain user loyalty against low-price entrants.

South Africa Diabetes Devices Industry Leaders

Dexcom Inc.

Abbott Diabetes Care

Novo Nordisk A/S

Roche Diabetes Care

Medtronic PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2023: Novo Nordisk partnered with Aspen SA Operations to produce human insulin in South Africa, setting a ceiling price of USD 3 per vial and planning supply for 4.1 million people across Africa by 2026.

- September 2022: Abbott reported new real-world data showing reduced hospitalisation rates among FreeStyle Libre users with type 2 diabetes on basal insulin therapy.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study sizes the South Africa diabetes devices market as the revenue generated from patient-use glucose-monitoring tools (glucometers, test strips, lancets, CGM sensors and transmitters) plus insulin-delivery hardware (disposable and reusable pens, syringes, pumps and jet injectors) sold through hospitals, pharmacies and direct-to-consumer channels.

Scope exclusion: Pharmaceuticals, software-only diabetes apps, laboratory analyzers and ancillary disposables such as alcohol swabs are left outside this sizing.

Segmentation Overview

- By Device Category

- Monitoring Devices

- Self-Monitoring Blood Glucose (SMBG) Devices

- Glucometers

- Test Strips

- Lancets

- Continuous Glucose Monitoring (CGM) Devices

- Sensors

- Durables (Receivers & Transmitters)

- Self-Monitoring Blood Glucose (SMBG) Devices

- Management Devices

- Insulin Delivery Devices

- Insulin Pump Devices

- Insulin Disposable Pens

- Insulin Cartridges in Re-usable Pens

- Insulin Syringes & Jet Injectors

- Insulin Delivery Devices

- Monitoring Devices

- By End User

- Hospitals & Clinics

- Home-Care Settings

- Retail Pharmacies & Diabetes Centers

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- E-commerce / Online Pharmacies

Detailed Research Methodology and Data Validation

Primary Research

Discussions with endocrinologists, procurement heads at leading private hospitals, diabetes educators and device distributors across Gauteng, Western Cape and KwaZulu-Natal refined strip-per-patient assumptions, CGM adoption curves and pump replacement cycles, enabling the team to close data gaps before triangulation.

Desk Research

Our analysts extracted prevalence and shipment baselines from Statistics South Africa, South African Revenue Service customs data (HS 902780/901890), and the International Diabetes Federation atlas, then corroborated ASPs and launch timing with company 10-Ks, investor decks and Dow Jones Factiva coverage. Peer-reviewed articles in the South African Medical Journal plus National Department of Health device-registration lists clarified usage protocols and public tender volumes. The sources named are illustrative; numerous additional publications informed the analysis.

Market-Sizing & Forecasting

The model begins with a top-down prevalence-to-demand build: adult diabetes population × device-penetration ratio × consumption norms × verified ASPs. Bottom-up roll-ups, supplier revenue splits, sampled hospital purchase records and channel audits validate totals and adjust outliers. Inputs such as private-scheme coverage levels, sensor change frequency, pump uptake, exchange-rate trends and VAT shifts feed a multivariate regression that projects 2025-2030 demand; scenario analysis captures policy shocks like National Health Insurance roll-out.

Data Validation & Update Cycle

Outputs pass variance screens against import series and quoted company performance; anomalies prompt re-interviews and peer review. Reports refresh annually, with interim updates when regulatory or reimbursement shifts breach preset materiality thresholds.

Why Mordor's South Africa Diabetes Devices Baseline Commands Reliability

Published estimates frequently diverge because studies mix therapeutics with hardware, retain outdated base years or layer retail mark-ups on top of factory values. By isolating clearly defined device cohorts, aligning volumes with customs ledgers and refreshing the model every twelve months, Mordor Intelligence delivers a balanced figure users can readily trace.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 158.16 million (2025) | Mordor Intelligence | - |

| USD 960.9 million (2025) | Regional Consultancy A | Bundles drug revenues and distributor mark-ups |

| USD 268.0 million (2023) | Global Consultancy B | Older base year; broader list including point-of-care analyzers |

The comparison shows that scope discipline, current-year anchoring and transparent variables allow Mordor's baseline to remain the dependable starting point for strategic decisions.

Key Questions Answered in the Report

How big is the South Africa Diabetes Devices Market?

The South Africa Diabetes Devices Market size is expected to reach USD 164.52 million in 2026 and grow at a CAGR of 4.02% to reach USD 200.39 million by 2031.

How does National Health Insurance influence device adoption?

NHI reimbursement lowers the cost of basic monitoring supplies for public-sector patients, encouraging regular glucose testing.

Who are the key players in South Africa Diabetes Devices Market?

Dexcom Inc., Abbott Diabetes Care, Novo Nordisk A/S, Roche Diabetes Care and Medtronic PLC are the major companies operating in the South Africa Diabetes Care Devices Market.

Are e-commerce channels significant for device distribution?

Yes, online platforms are the fastest-growing channel with a 4.96% CAGR, offering price transparency and convenient home delivery.

Page last updated on: