Diabetes Supplements Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

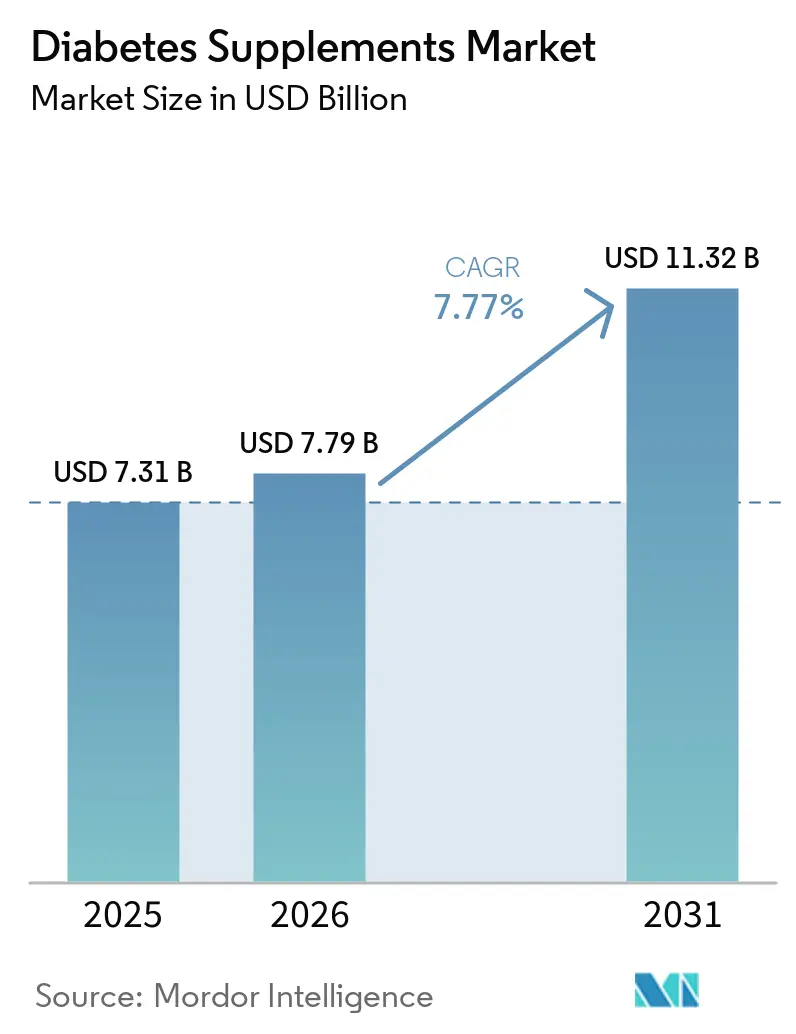

| Market Size (2026) | USD 7.79 Billion |

| Market Size (2031) | USD 11.32 Billion |

| Growth Rate (2026 - 2031) | 7.77% CAGR |

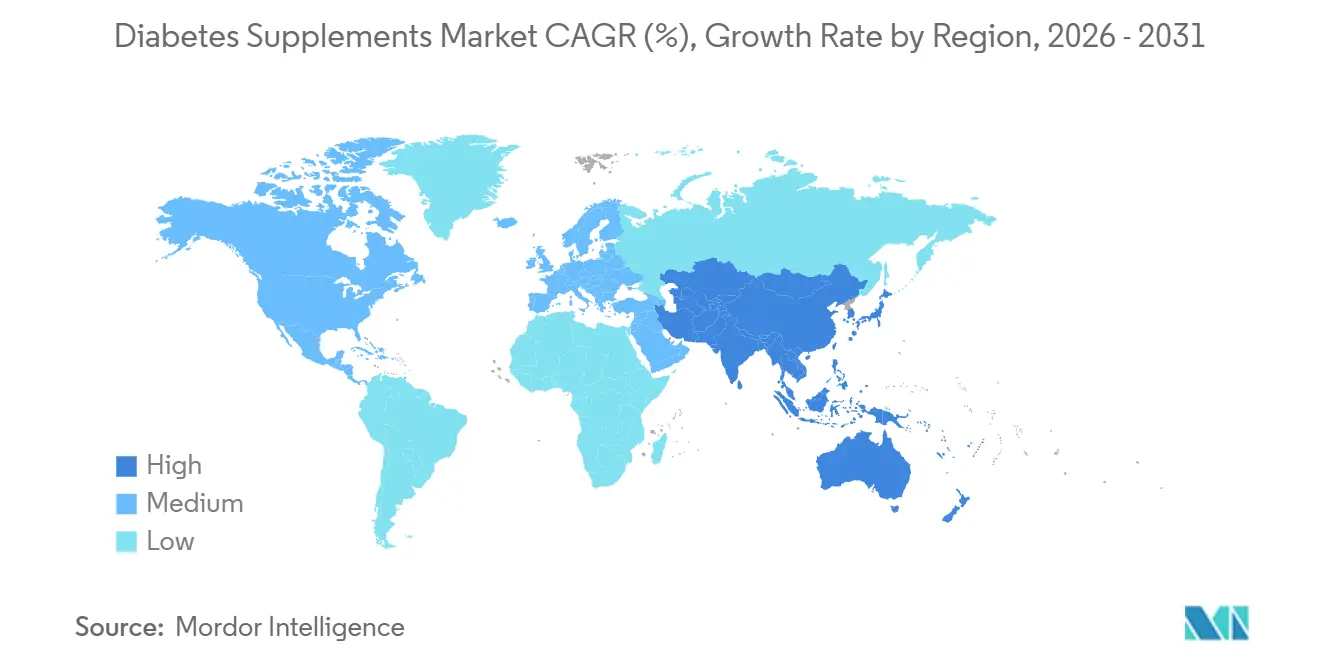

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Diabetes Supplements Market Analysis by Mordor Intelligence

The Diabetes Supplements Market size was valued at USD 7.31 billion in 2025 and is estimated to grow from USD 7.79 billion in 2026 to reach USD 11.32 billion by 2031, at a CAGR of 7.77% during the forecast period (2026-2031).

Preventive nutrition adoption is advancing as prediabetes remains widespread and underdiagnosed, which sustains demand even as prescription GLP-1 and SGLT-2 therapies expand. Consumer use cases cluster around adjunctive support for tolerability and nutrient gaps, especially where access or coverage for weight-loss prescriptions remains limited. North America underpins premium adoption dynamics due to high diabetes spending, while Asia-Pacific scales quickly on demographic burden and digital-first retail models. Ingredient innovation converges on microbiome-targeted approaches such as probiotics, synbiotics, and fibers, complemented by clean-label positioning and format upgrades that raise compliance. Regulatory expectations on claims substantiation and quality control continue to reinforce trust signals, influencing brand selection across both pharmacy-led and online channels.

Key Report Takeaways

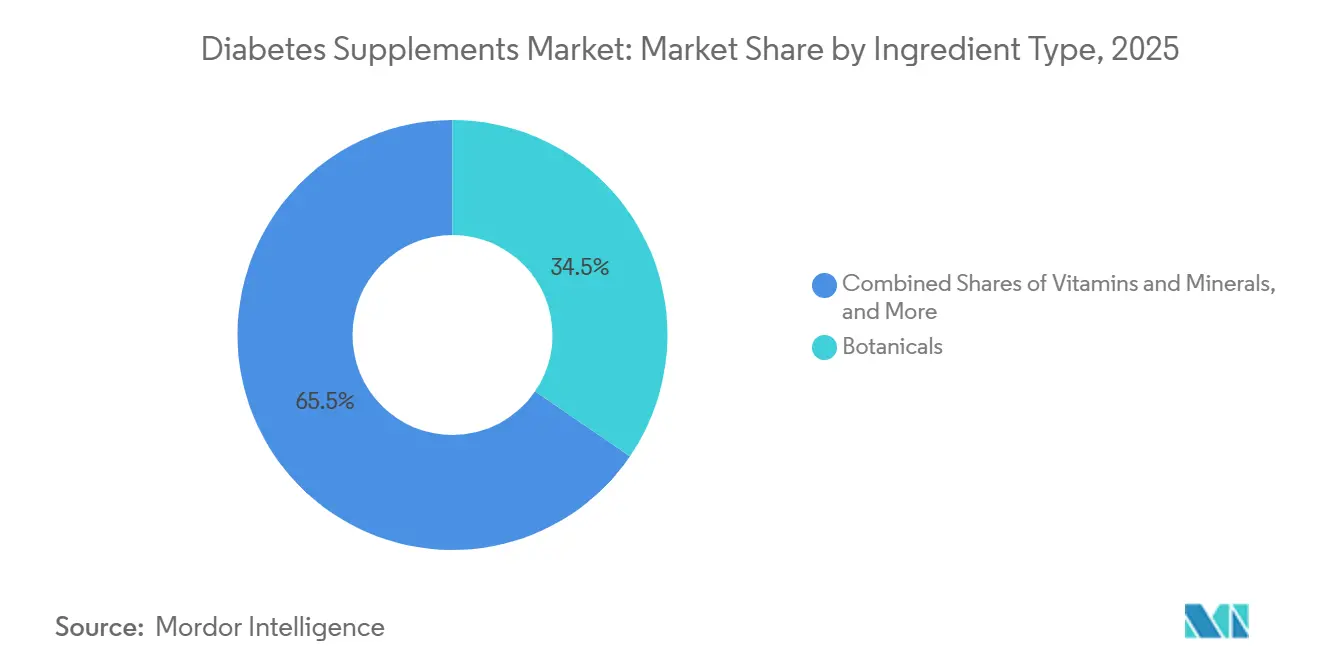

- By ingredient type, botanicals led with 34.53% share in 2025, while probiotics and prebiotics recorded the fastest projected growth at a 9.93% CAGR through 2031.

- By form, capsules held the largest share at 38.42% in 2025, while gummies posted the highest projected growth at a 10.52% CAGR to 2031.

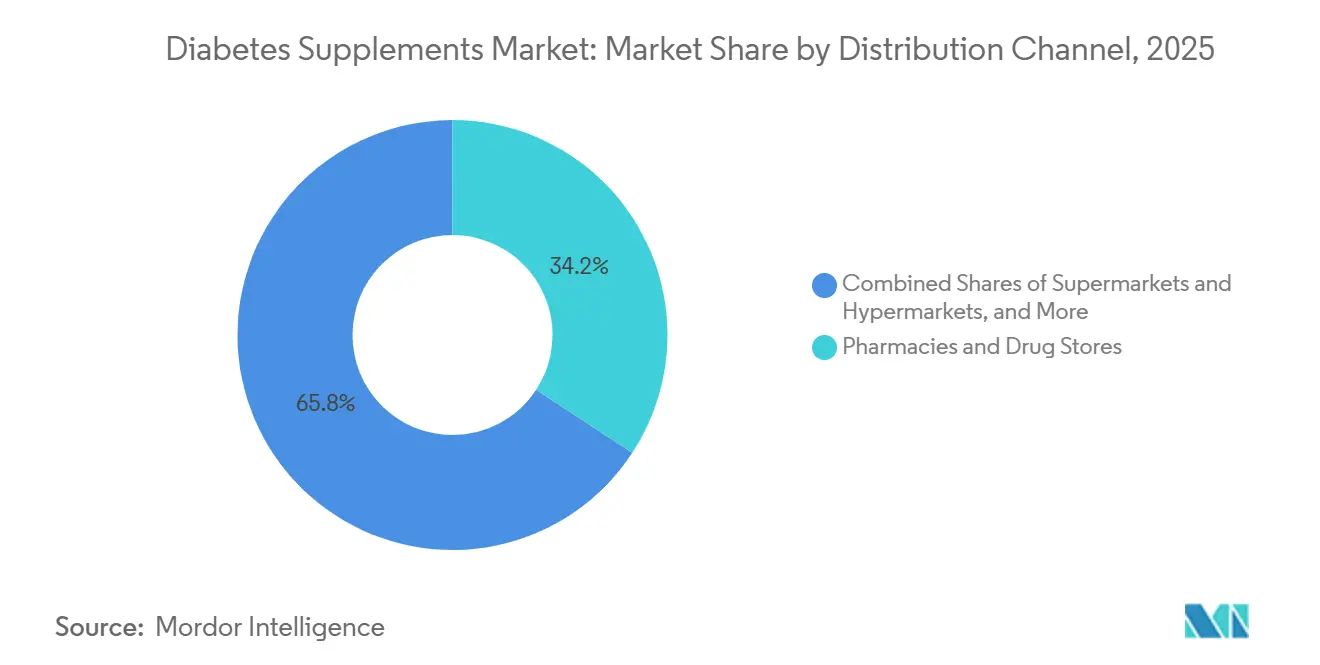

- By distribution channel, pharmacies and drug stores accounted for a 34.23% share in 2025, while online channels were the fastest-growing at an 11.57% CAGR through 2031.

- By geography, North America held the largest share at 34.53% in 2025, while Asia-Pacific is projected to expand at a 10.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Diabetes Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Diabetes And Prediabetes Prevalence | +2.1% | Global, concentrated in Asia-Pacific (India 101M, China 141M diabetics) and North America (38.4M US cases, 97.6M prediabetic) | Medium term (2-4 years) |

| Preventive Nutrition Adoption And Nutraceutical Usage | +1.8% | Global, early gains in US metropolitan areas, Western Europe wellness corridors, urban India | Medium term (2-4 years) |

| E-Commerce And Online Pharmacies Expansion | +1.5% | North America & EU established; APAC core with spillover to MEA emerging markets | Short term (≤ 2 years) |

| EFSA-Eligible Chromium Health Claim Enabling EU Marketing | +0.6% | EU27, UK, Norway, Switzerland regulatory zones | Medium term (2-4 years) |

| CGM Adoption Beyond Diabetics Catalyzing Supplement Experimentation | +0.9% | North America (74% Dexcom share), EU (Germany, UK pharmacy integration) | Medium term (2-4 years) |

| Comorbidity Cross-Sell (Neuropathy, Eye Health) Boosting Adjunct Demand | +0.9% | Global, particularly in aging populations (US 65+: 29.2% diabetes prevalence) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes And Prediabetes Prevalence

Prevalence and awareness dynamics continue to define the demand base for the diabetes supplements market. The IDF Diabetes Atlas 11th edition reports elevated global prevalence and ongoing diagnostic gaps, which shape prevention and adjunctive care choices at scale[1]International Diabetes Federation, “IDF Diabetes Atlas 11th Edition 2025,” International Diabetes Federation, idf.org. In the United States, 97.6 million adults live with prediabetes, yet only 19% are aware of their condition, a gap that sustains interest in lifestyle and supplementation before or alongside medications. Economic burden intensifies prevention incentives, with diabetes costs in the United States reported at USD 412.9 billion, reinforcing the rationale for lower-cost adjuncts that target adherence and tolerability.[2]American Diabetes Association, “Economic Costs of Diabetes in the U.S.,” American Diabetes Association, diabetes.org

Asia-Pacific’s scale, reflected in large national caseloads in India and China, aligns with higher growth expectations for the diabetes supplements market through the forecast period. Emerging clinical evidence on diet and metabolic risk reinforces consumer interest in evidence-backed nutritional support, which dovetails with prevention programs and self-management resources from public health agencies.

Preventive Nutrition Adoption And Nutraceutical Usage

The diabetes supplements market continues to benefit from preventive frameworks that emphasize weight management and physical activity, where programmatic guidance positions diet and lifestyle as front-line measures for people with prediabetes[3]Centers for Disease Control and Prevention, “Public Health Research and Program Strategies for Diabetes Prevention and Management,” Preventing Chronic Disease, cdc.gov. Peer-reviewed findings support microbiome-directed supplementation strategies in diabetes and prediabetes, including multi-strain probiotics and synbiotics, demonstrating modest HbA1c and inflammatory marker improvements in controlled settings. Trials and reviews highlight that daily doses at or above 109 CFU over 8-12 weeks underlie observed effects, with variations by strain composition and baseline gut status that inform product design.

Mechanistic research associates prebiotic fibers with short-chain fatty acid production and improved glycemic homeostasis, which strengthens rationale for synbiotic formulations within the diabetes supplements market. At the same time, evidence remains uneven across botanicals such as cinnamon, where the U.S. government’s complementary health agency advises that current data do not support therapeutic use in diabetes, tempering clinical adoption while leaving room for consumer-led experimentation.

E-Commerce And Online Pharmacies Expansion

Digital channels provide continuous assortment, transparent labeling, and direct-to-consumer education, which increase category access and reinforce brand trust through verified quality and consistent supply pathways. The diabetes supplements market benefits from recurring purchase models and patient self-management patterns that align with subscription replenishment and bundled regimen strategies, particularly in urban corridors with high digital adoption. Pharmacy e-commerce integration and national delivery networks improve reach in markets with fragmented brick-and-mortar access, especially outside tier-1 cities. As shoppers compare formulations, strain specificity, and certificate-backed quality online, differentiation shifts toward clinically characterized ingredients and clear usage protocols that reduce ambiguity. This channel shift complements pharmacist-led guidance in regions where professional recommendations remain decisive, creating a hybrid journey from research to purchase.

EFSA-Eligible Chromium Health Claim Enabling EU Marketing

Chromium’s permitted health claims in the EU for maintenance of normal blood glucose concentration provide a regulatory lever for positioning products that include bioavailable forms of chromium in Europe’s pharmacy-led channels[4]National Institutes of Health Office of Dietary Supplements, “Chromium, Health Professional Fact Sheet,” National Institutes of Health, ods.od.nih.gov. In the United States, FDA allows only qualified claims with explicit uncertainty language, which influences label phrasing and marketing tone for chromium products in the diabetes supplements market. Meta-analyses report modest glycemic effects that often fall below clinical thresholds, guiding most healthcare professionals to avoid broad recommendations while allowing targeted use in select cases with well-specified dosing.

These regulatory asymmetries shape transatlantic product portfolios as companies calibrate evidence summaries, daily values, and co-formulants to fit differing compliance standards. As labels trend toward multi-ingredient designs that address diet quality and micronutrient adequacy, chromium formulations often appear within balanced blends rather than as monotherapies, reinforcing prudent positioning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Scrutiny On Diabetes-Disease Claims For Supplements | -0.9% | Global, acute in U.S. and EU | Medium term (2-4 years) |

| Limited High-Quality Clinical Evidence Reduces HCP Endorsements | -0.7% | Global, with pharmacy-dominant Europe most sensitive | Long term (≥ 4 years) |

| GLP-1/SGLT-2 Uptake Substituting For Glucose-Lowering Supplements | -1.1% | North America and EU core, APAC urban spillover | Short term (≤ 2 years) |

| Botanical Quality Variability Curbing Dosages/Claims | -0.5% | Global, strongest effects in U.S. and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Scrutiny On Diabetes-Disease Claims For Supplements

The regulatory climate places a premium on compliant claims and substantiation, limiting the scope of language that implies treatment or prevention of diabetes and redirecting brands toward structure-function positioning. In the United States, the standard for health claims requires significant scientific agreement, and judicial rulings have enabled qualified claims with disclaimers, which still impose legal and labeling complexity that adds costs and risk controls. EU authorities apply stringent efficacy criteria and close claim definitions, creating distinct EU-U.S. pathways that multinational brands must navigate without confusing consumers. These conditions encourage evidence-first messaging and reinforce the diabetes supplements market’s shift toward transparency on dosing, target populations, and duration of use. As agencies prioritize public protection against delayed medical care, category participants invest more in clinician education materials that clarify adjunctive roles. The net effect is a more cautious promotional environment that rewards brands with robust documentation and disciplined label governance.

Limited High-Quality Clinical Evidence Reduces HCP Endorsements

Healthcare professionals remain selective because multiple systematic reviews and trials report mixed or small effects on glycemic outcomes for several popular ingredients, including cinnamon and chromium, relative to established medication standards. Government-backed fact sheets and academic reviews point to inconsistent evidence or low-certainty findings, which motivates conservative guidance to avoid routine supplementation without individualized rationale. At the same time, probiotic and synbiotic meta-analyses show modest HbA1c and inflammatory marker reductions, but heterogeneity in strain combinations, dosing, and baseline microbiome status complicates universal recommendations.

The resulting evidence gradient tempers uptake in pharmacy-dominant markets, especially where professional recommendations drive shelf placement and consumer selection behaviors. As more RCTs refine strain-specific and dose-specific effects, endorsement thresholds may shift, but for now, many clinicians steer patients toward diet quality, physical activity, and medication adherence as primary levers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Probiotics Lead Innovation Surge

Botanicals held the largest share at 34.53% of the diabetes supplements market in 2025 as brands balanced familiarity and traditional usage with modern quality controls. In parallel, probiotics and prebiotics are the fastest-growing category at a 9.93% CAGR through 2031 as multi-strain and synbiotic designs demonstrate modest yet consistent support for glycemic and inflammatory markers in controlled trials. Research links daily intakes at or above 109 CFU for 8-12 weeks to effect sizes on HbA1c and C-reactive protein that, while small, are relevant to adjunctive regimens in type 2 diabetes and prediabetes. As a result, the diabetes supplements market features strain-forward product labels and co-formulants like inulin to drive SCFA production associated with improved metabolic signaling. Companies are also refining safety and purity practices for botanicals as variability challenges precise dosing and cross-border compliance, which sustains demand for ingredients with standardized actives and transparent sourcing.

Demand patterns across vitamins, minerals, antioxidants, and omega-3s reflect cross-sell into cardiometabolic comorbidities and neuropathy prevention use cases. Chromium remains present but constrained by qualified-claim rules in the United States and modest glycemic effect sizes in meta-analyses, which shapes positioning toward inclusion within broader blends. Alpha-lipoic acid, vitamin D3, magnesium, and B-complex formulations maintain stable roles where practitioners emphasize nerve health and general nutritional adequacy, keeping assortment breadth across channels. As studies refine personalized response patterns, suppliers prioritize clinical documentation that specifies strain, dose, and duration to align expectations and support practitioner guidance. These shifts reinforce product architectures that can be titrated or bundled, which supports repeat purchase behavior and clearer regimen adherence in the diabetes supplements market.

By Form: Gummies Disrupt Capsule Dominance

Capsules held the largest share at 38.42% of 2025 form sales, favored for dose precision and stability in the diabetes supplements market. Gummies are the fastest-growing format at a 10.52% CAGR to 2031 as palatability, ease of intake, and format familiarity improve adherence, especially among consumers who avoid pills. Advances in microencapsulation and moisture control help preserve heat-sensitive ingredients, which expands the range of microbiome-directed gummy formulations with shelf-stable profiles suitable for routine use. Brands improve formulation transparency and sugar-free profiles with sweeteners and fibers that better match metabolic health objectives while managing taste and texture trade-offs. These practical upgrades help gummies compete beyond vitamins, enabling condition-focused products that complement pharmacist and clinician guidance.

The wider diabetes supplements industry has adapted manufacturing to vegan pectin bases, low-sugar systems, and more robust stability profiles, which address historical concerns that limited gummies for complex formulations. Launches featuring multi-ingredient blends that target post-meal glucose response illustrate the role of format innovation in regimen simplification for everyday use. Capsules, tablets, and softgels continue to support omega-3s and other actives that benefit from specific delivery systems, balancing the format mix across retail and e-commerce channels. Liquids and powders retain niche roles for consumers who favor shakes and smoothies within diet-led programs. The net effect is a format portfolio that matches adherence, taste, and price preferences across demographics in the diabetes supplements market.

By Distribution Channel: E-commerce Penetrates Pharmacy Strong holds

Pharmacies and drug stores accounted for a 34.23% share of distribution in 2025, supported by professional counseling and established planograms for condition-focused offerings. Online channels are the fastest-growing at an 11.57% CAGR through 2031 and rising as consumers rely on delivery convenience, subscription replenishment, and transparent quality documentation in the diabetes supplements market. The shift toward digital consideration and purchase broadens market access in suburban and rural areas where physical assortments are narrow. E-commerce also surfaces differentiation through clinically characterized strains, standardized botanicals, and certifications that are easier to verify online than in-store. As brands build digital education and customer service capabilities, conversion and retention improve for multi-month regimens that align with habit formation.

Pharmacy remains essential as a discovery and recommendation channel for older adults and patients with complex medication profiles who value pharmacist input. Cross-channel strategies that use pharmacy for initial guidance and online for replenishment are gaining traction, aligning with the diabetes supplements market’s focus on continuous adherence. Specialty and practitioner channels maintain premium roles for high-potency or condition-specific formulations, while supermarkets and hypermarkets provide convenient access for general wellness bundles. Direct selling contributes parallel access in select geographies, although disease-claim restrictions keep messaging conservative. The channel landscape balances assurance, convenience, and choice, reinforcing steady growth paths.

Geography Analysis

North America held the largest regional position with a 34.53% share in 2025, supported by high care utilization and broad adoption of preventive and adjunctive solutions in the diabetes supplements market. The United States anchors this base with significant diabetes spending, where the reported USD 412.9 billion economic burden elevates consumer and payer interest in affordable adjuncts that can support adherence and comfort alongside standard care. Widespread prediabetes adds to the addressable audience, given that fewer than one in five affected adults are aware of their status, which keeps self-directed prevention and monitoring in focus. Canada and Mexico contribute incremental expansion through pharmacy and online channels as coverage for monitoring technologies evolves and retail assortments broaden. Clinical communication emphasizes realistic expectations for supplements as complements to diet, activity, and medications, which grounds purchasing behavior in safe, long-term use patterns.

Asia-Pacific is the fastest-growing region with a projected 10.02% CAGR through 2031, underpinned by large national caseloads and increasing urban health engagement in the diabetes supplements market. IDF data reflect substantial case volumes in India and China, which steer manufacturers to localized portfolios and language on dosage, format, and diet fit that resonate with younger adults and working-age populations. Digital commerce and health platforms provide route-to-market advantages across cities where pharmacy footprints are fragmented, accelerating access to clinically characterized probiotics, synbiotics, vitamins, and fibers. As product education meets mobile-first content, consumers align choices with lifestyle preferences and feedback from self-monitoring, which encourages repeat purchase patterns. The diabetes supplements market size in these countries will reflect both the scale of metabolic risk and the speed at which transparent labeling and third-party verification practices spread through online marketplaces.

Europe maintains steady growth supported by pharmacy-led distribution, clear claim frameworks, and persistent interest in clinically characterized ingredients. EU-authorized chromium claims shape positioning for glucose-related maintenance, while the United Kingdom’s guideline evolution on medication access informs how consumers choose adjuncts and supportive ingredients to fit personalized care plans. In markets such as Germany, France, Italy, and Spain, the diabetes supplements market share for pharmacy channels remains high due to pharmacist influence on product selection and adherence counseling. Middle East and Africa present a patchwork of opportunities aligned to premium imports in the Gulf states and pharmacy chains in South Africa. South America shows expansion focused on Brazil and Argentina as online retail augments traditional pharmacy distribution.

Competitive Landscape

The diabetes supplements market is moderately fragmented with multinational nutrition and wellness brands, practitioner-focused companies, and regional specialists competing on clinical validation, quality systems, and channel execution. Practitioner-exclusive portfolios maintain pricing power where clinician endorsement is decisive for product choice and adherence guidance. Brands with robust documentation on specific strains, standardized botanicals, and dosage-duration clarity gain trust advantages in pharmacy-dominant markets. Adjacent opportunities continue to emerge around tolerability and nutritional gaps for patients on common medications, which encourages bundled formulations that address glucose, nerve, and cardiovascular support. As evidence syntheses refine use cases, differentiation shifts from broad claims to well-specified benefits within an adjunctive care frame.

Partnerships, certifications, and transparency practices are critical to scale. Companies that publish lot-level testing, highlight GMP compliance, and provide detailed labels on actives, strain IDs, and amounts per serving reduce selection friction for both clinicians and consumers. In parallel, alignment with pharmacy education and patient support programs strengthens conversion for regimen-based products in the diabetes supplements market. Firms invest in formats that remove barriers to adherence, such as palatable gummies with verified stability profiles for microbiome-directed ingredients. Where cross-border sales are material, ISO 22000, country-specific cGMPs, and halal or kosher certifications improve acceptance in health-conscious and culturally diverse populations.

Pharmaceutical companies’ momentum in metabolic therapeutics influences nutraceutical adjacency. Company disclosures underscore the scale of GLP-1 portfolios, which raises consumer awareness of metabolic health and fuels interest in complementary nutrition approaches that support overall wellbeing and adherence. Category participants that clarify supplement roles as supportive, not substitutive, position effectively alongside medical care in the diabetes supplements market. Over time, discipline on claims, evidence, and quality will continue to shape leadership and durability in both pharmacy-led and digital channels.

Diabetes Supplements Industry Leaders

Herbalife Nutrition

Amway Corp.

Nestlé Health Science

Nature's Way Brands, LLC.

NOW Foods

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: A study published in JAMA Network Open revealed that prediabetic adults with specific variations in the vitamin D receptor gene experienced a 19% reduction in diabetes risk when administered a high daily dose of vitamin D.

- November 2025: Abbott launched an advanced new formulation of Ensure Diabetes Care in India. The enhanced product is designed to help people with diabetes manage their nutritional needs more effectively.

Global Diabetes Supplements Market Report Scope

As per the scope of the market, diabetes supplements are nutraceutical and dietary supplement products designed to support blood glucose management, insulin sensitivity, and overall metabolic health in individuals with diabetes or prediabetes.

The diabetes supplements market is segmented by ingredient type, form, distribution channel, and geography. By ingredient type, the market includes botanicals, vitamins and minerals, antioxidants, omega‑3 fatty acids, probiotics and prebiotics, and others, which comprise fibers, specialty carbohydrates, and amino acids. Based on form, the market is categorized into capsules, tablets, softgels, powder, liquid, and gummies. By distribution channel, the diabetes supplements market is segmented into pharmacies and drug stores, supermarkets and hypermarkets, specialty and practitioner channels, direct selling, and online channels (e‑commerce). By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Botanicals |

| Vitamins & Minerals |

| Antioxidants |

| Omega-3 Fatty Acids |

| Probiotics/Prebiotics |

| Others (Fibers & Specialty Carbohydrates, Amino Acids) |

| Capsules |

| Tablets |

| Softgels |

| Powder |

| Liquid |

| Gummies |

| Pharmacies & Drug Stores |

| Supermarkets & Hypermarkets |

| Specialty & Practitioner Channels |

| Direct Selling |

| Online Channels (E-commerce) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Ingredient Type | Botanicals | |

| Vitamins & Minerals | ||

| Antioxidants | ||

| Omega-3 Fatty Acids | ||

| Probiotics/Prebiotics | ||

| Others (Fibers & Specialty Carbohydrates, Amino Acids) | ||

| By Form | Capsules | |

| Tablets | ||

| Softgels | ||

| Powder | ||

| Liquid | ||

| Gummies | ||

| By Distribution Channel | Pharmacies & Drug Stores | |

| Supermarkets & Hypermarkets | ||

| Specialty & Practitioner Channels | ||

| Direct Selling | ||

| Online Channels (E-commerce) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the diabetes supplements market outlook through 2031

The diabetes supplements market size is projected to be USD 7.79 billion in 2026 and reach USD 11.32 billion by 2031 at a 7.77% CAGR, supported by prevention use cases, microbiome-led innovation, and hybrid retail models.

Which regions lead growth for diabetes-focused supplements

Asia-Pacific shows the fastest expansion with a projected 10.02% CAGR through 2031, while North America held the largest 2025 share supported by high diabetes spending and broad adoption of adjunctive support.

Which ingredient groups are gaining the most traction in diabetes supplements

Probiotics and prebiotics lead growth as synbiotic designs demonstrate modest improvements in glycemic and inflammatory markers in controlled studies, while botanicals remain the largest 2025 segment by share.

How are formats evolving for better adherence in diabetes supplements

Gummies are the fastest-growing format due to palatability and convenience, while capsule and softgel formats remain important for dose precision and ingredient stability.

How does regulation affect claims on diabetes supplements

U.S. and EU regimes emphasize substantiation and careful claim language, with the U.S. allowing qualified claims with disclaimers and the EU maintaining strict approved health claims like those covering chromium in glucose maintenance.

What roles do pharmacies and e-commerce play in diabetes supplement access

Pharmacies lead in professional guidance and initial selection, while online channels are the fastest-growing for delivery convenience, transparent quality documentation, and subscription replenishment that supports ongoing adherence.

Page last updated on: