Dermatological Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 54.06 Billion |

| Market Size (2031) | USD 83.59 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

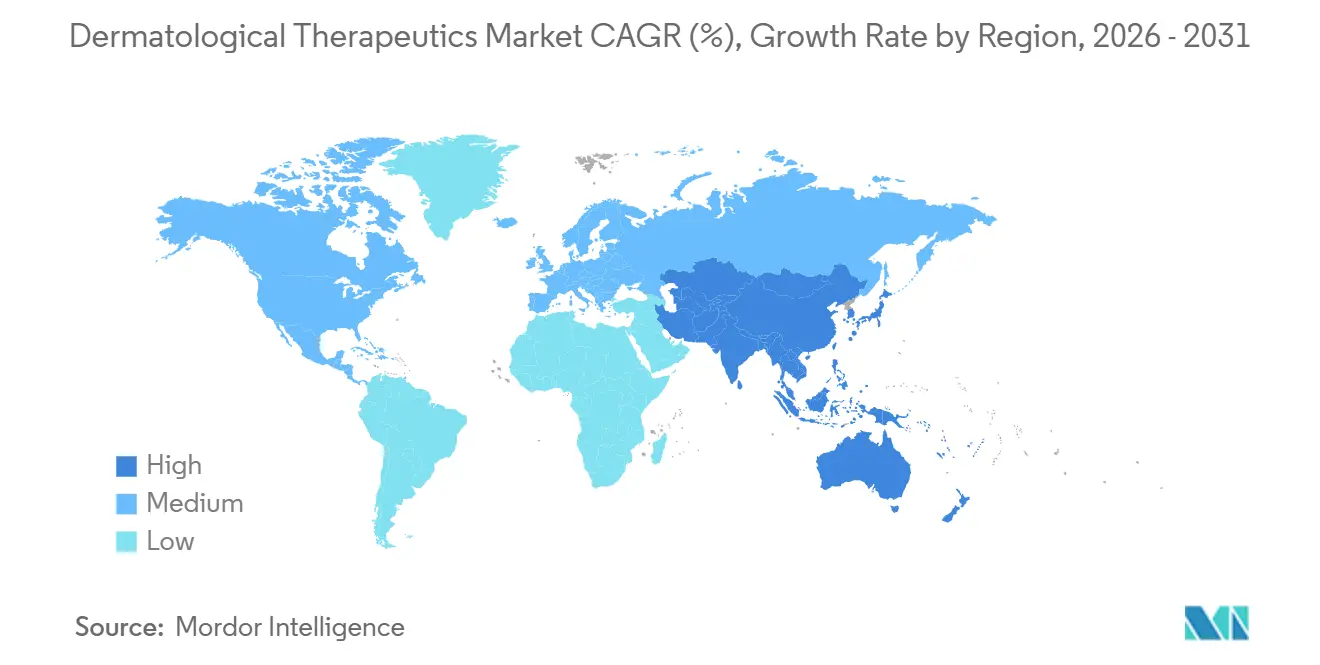

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

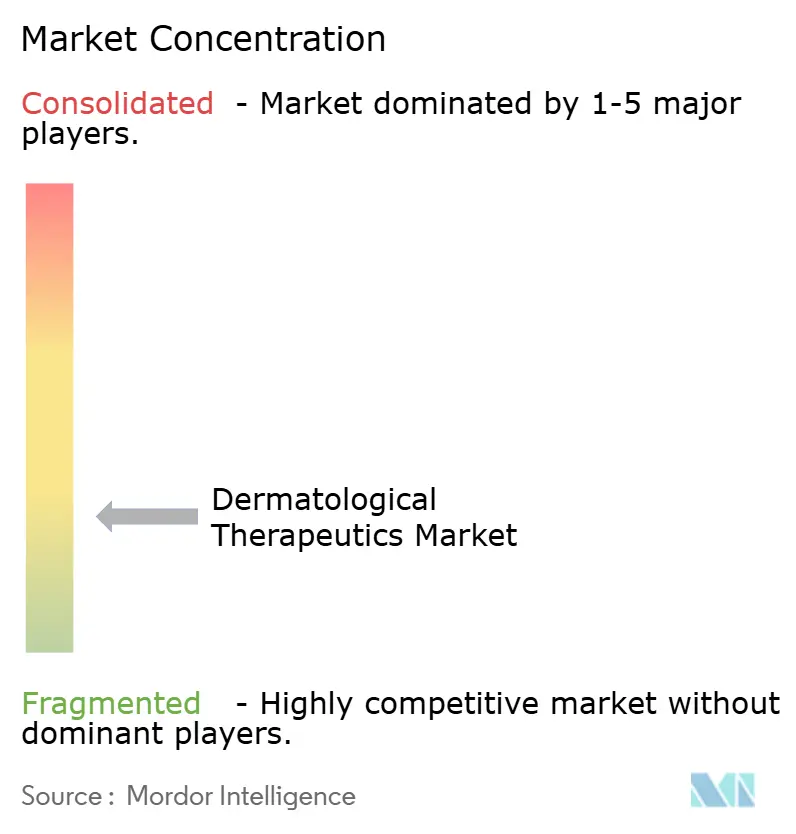

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dermatological Therapeutics Market Analysis by Mordor Intelligence

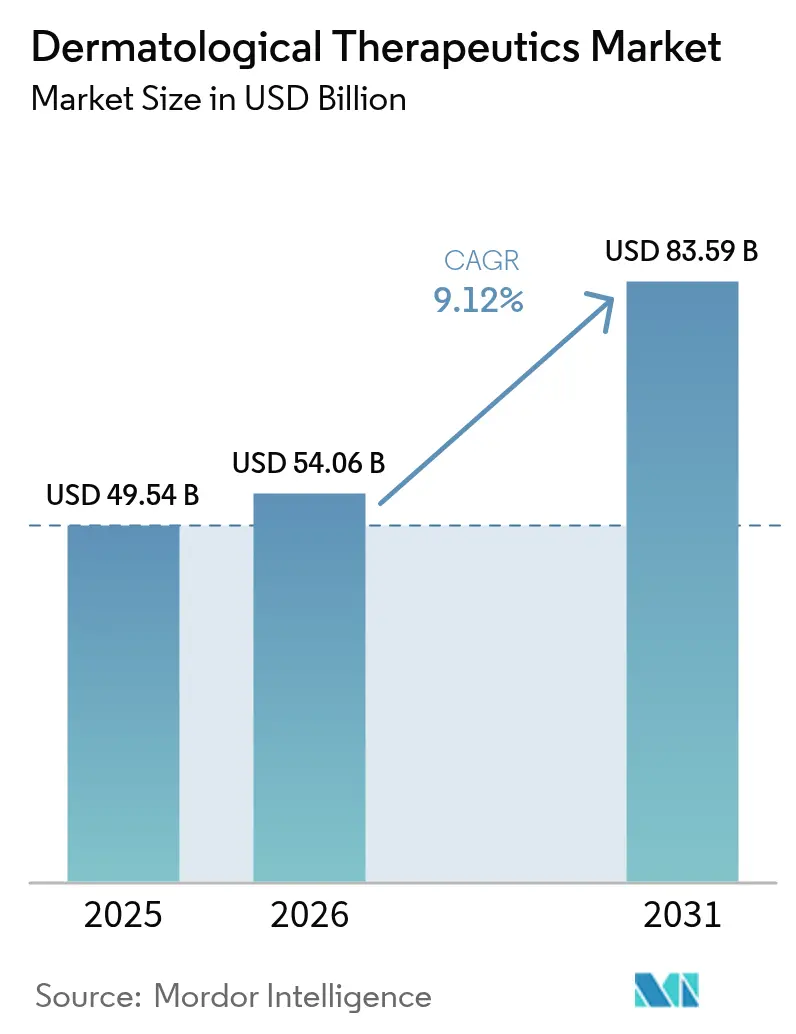

The dermatological therapeutics market size is projected to be USD 49.54 billion in 2025, USD 54.06 billion in 2026, and reach USD 83.59 billion by 2031, growing at a CAGR of 9.12% from 2026 to 2031. Demand is shifting from high-volume topical generics toward precision biologics and oral small-molecule inhibitors that offer measurable adherence advantages and command premium pricing. Eight first-in-class or label-expanded agents won U.S. approval during 2024-2025, reflecting regulatory confidence in mechanism-based dermatology treatments. At the same time, the World Health Organization recorded a 22% rise in chronic inflammatory skin-disease prevalence within high-income nations over 2020-2025. Supply chains are recalibrating after excipient shortages disrupted 12% of U.S. topical-corticosteroid inventories in early 2025. Digital distribution is expanding quickly as online pharmacies use telemedicine overlays to reach rural and millennial populations under extended prescribing flexibilities.

Key Report Takeways

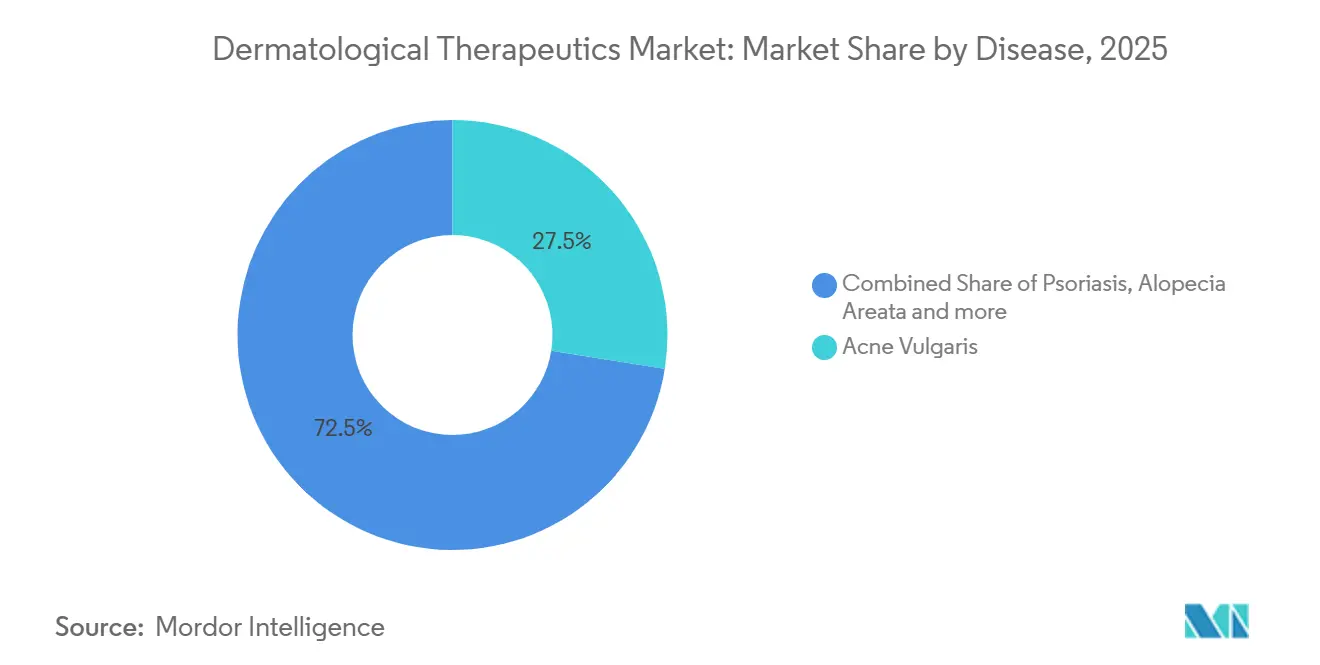

- By disease, acne vulgaris led with 27.55% of 2025 revenue, while hidradenitis suppurativa is advancing at a 14.25% CAGR through 2031.

- By drug class, topical corticosteroids held a 25.53% share of the dermatological therapeutics market size in 2025, and small-molecule inhibitors are projected to expand at a 15.75% CAGR to 2031.

- By route of administration, the topical route accounted for 65.15% in 2025; injectables recorded 11.82% growth, outpacing the 9.12% market average.

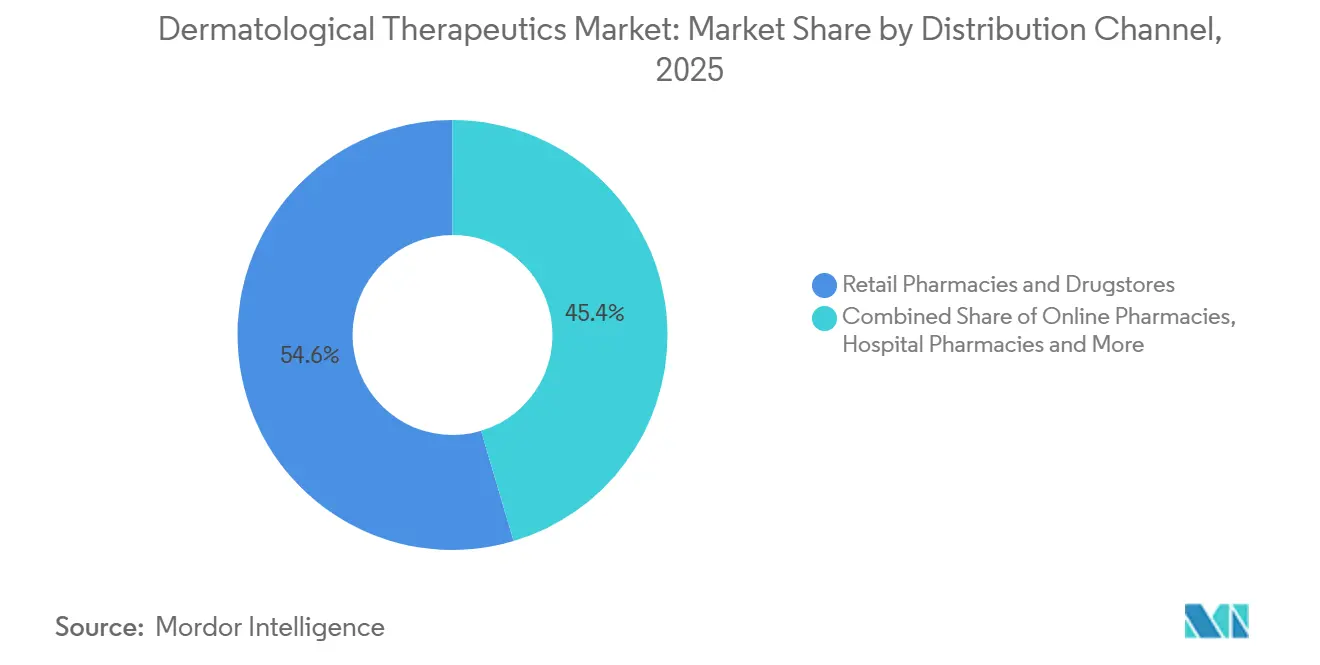

- By distribution channel, retail pharmacies captured 54.65% share in 2025; online pharmacies rose at a 13.32% CAGR, the fastest among all channels.

- By therapy type, prescription drugs accounted for 62.23% in 2025; over-the-counter formulations expanded at an 11.12% CAGR as regulators reclassified low-dose retinoids and mild steroids for self-care.

- By geography, North America accounted for 38.23% revenue in 2025, while Asia-Pacific leads growth at 10.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dermatological Therapeutics Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic dermatological diseases | +2.1% | Global with highest burden in North America and Europe | Long term (≥ 4 years) |

| Rapid uptake of biologics and targeted therapies | +2.8% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Growing aesthetic consciousness and disposable income | +1.4% | Asia-Pacific, Middle East, Latin America | Medium term (2-4 years) |

| AI-driven teledermatology boosting treatment adherence | +0.9% | North America, Western Europe, GCC | Short term (≤ 2 years) |

| Microbiome-modulating topicals gaining regulatory traction | +0.7% | North America, Europe | Long term (≥ 4 years) |

| GLP-1 weight-loss boom creating new skin-repair demand | +0.6% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Dermatological Diseases

Urban air pollution, processed-food consumption, and delayed diagnosis combined to double atopic-dermatitis prevalence in Chinese and Indian cities between 2019 and 2024[1]National Medical Products Administration, “Drug Approval Database,” NMPA.gov.cn. Psoriasis incidence climbed 18% in the United States over 2020-2025, with the Centers for Disease Control and Prevention linking the increase to metabolic-syndrome comorbidities and pandemic-era care gaps. An American Academy of Dermatology campaign trained 12,000 primary-care doctors to detect hidradenitis suppurativa, producing a 40% surge in confirmed cases. Greater diagnostic reach is enlarging the patient pool for both first-line topicals and second-line biologics, especially in regions where specialty capacity is catching up to disease burden.

Rapid Uptake of Biologics & Targeted Therapies

Biologic prescriptions for dermatology rose 31% year over year in 2025, surpassing uptake rates in oncology and rheumatology. FDA approvals of upadacitinib for adolescent atopic dermatitis and for hidradenitis suppurativa broadened access for 2.3 million U.S. patients. The European Medicines Agency cleared baricitinib for alopecia areata, and Germany’s Federal Joint Committee backed reimbursement, creating the first oral pathway in hair-loss care. Payers are abandoning rigid step-therapy sequences and moving toward direct biologic initiation for moderate disease, trimming time to treatment from 18 months to 6 months within many U.S. commercial plans. Biosimilar entry is accelerating adoption by lowering annual adalimumab costs to USD 28,000 from USD 45,000.

Growing Aesthetic Consciousness & Disposable Income

Per-capita outlays on therapeutic-aesthetic hybrids climbed 27% in Asia-Pacific during 2023-2025, led by South Korea, Japan, and urban China. India added 85 million middle-class households over the same period, expanding demand for OTC acne and skin-lightening products under the Drugs and Cosmetics Act. Gulf Cooperation Council countries registered a 34% rise in dermatology tourism during 2024 as the UAE and Saudi Arabia invested USD 1.2 billion in specialized centers. Social-media amplification has driven a 19% increase in first-time dermatologist visits among North American Gen Z and millennial cohorts. This convergence of rising incomes and beauty prioritization is blurring the line between therapeutic and cosmetic offerings, enlarging the dermatological therapeutics market.

AI-Driven Teledermatology Boosting Treatment Adherence

The FDA cleared six AI-supported teledermatology platforms between 2024 and 2025, each posting diagnostic sensitivity above 92%. A 2025 JAMA Dermatology study reported 41% higher adherence among users of AI-guided apps relative to traditional care. Medicare introduced asynchronous visit codes in 2025, reimbursing store-and-forward imaging for 14 skin conditions and opening virtual access for 18 million rural members. Four EU-certified platforms achieved Class IIa status under the Medical Device Regulation, aligning data-privacy and accuracy rules across member states. Commercial insurers now waive copays on virtual visits, cutting acquisition costs for specialty pharmacies by 38%.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost and reimbursement hurdles for biologics | -1.8% | Global, acute in emerging markets | Medium term (2-4 years) |

| Patent cliffs and biosimilar price erosion | -1.3% | North America, Europe | Short term (≤ 2 years) |

| Global dermatologist workforce shortage | -0.9% | Global, severe in rural North America and Sub-Saharan Africa | Long term (≥ 4 years) |

| Critical excipient shortages disrupting topical supply chains | -0.7% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost & Reimbursement Hurdles for Biologics

Annual dermatology biologic regimens cost USD 35,000-65,000, a figure beyond reach for 68% of patients in middle-income economies dominated by out-of-pocket payment. U.S. insurers placed prior-authorization controls on 89% of biologic claims in 2025, generating 14-day average approval lags and 22% first-cycle denials. NICE limited dupilumab coverage to severe eczema cases, excluding about 40% of moderate patients[2]National Institute for Health and Care Excellence, “Technology Appraisal Guidance,” Nice.org.uk. Indian biosimilar adalimumab remains triple the price of oral immunosuppressants, keeping uptake low outside urban tertiary centers. Industry copay-assistance programs assisted only 18% of eligible U.S. patients in 2025 as manufacturers tightened rules in anticipation of biosimilar erosion.

Patent Cliffs & Biosimilar Price Erosion

Humira biosimilars eroded AbbVie’s U.S. dermatology revenue by USD 2.1 billion within 18 months of launch, forcing a 28% originator price decline. Stelara faces U.S. biosimilar launches in 2024 that analysts project will remove 60% of its USD 9.1 billion global sales by 2027. Dupixent’s European patents expire in 2028, and dossiers filed in 2025 suggest rapid competitor entry that may cut combined Regeneron and Sanofi revenue by up to 50% within two years. Innovators are pivoting toward TYK2 inhibitors and long-acting injectables but face 8-10-year development cycles. Fourteen U.S. state Medicaid programs have already mandated automatic biosimilar substitution as of 2025, accelerating share shifts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease: High-Margin Hidradenitis Suppurativa Accelerates Growth

Hidradenitis suppurativa is the fastest-growing indication, advancing at a 14.25% CAGR through 2031, even though acne vulgaris retained 27.55% of 2025 revenue. Cosentyx secured FDA approval for moderate-to-severe cases in 2024, and Humira label expansions opened adolescent access, unlocking reimbursement for 1.8 million U.S. patients. Psoriasis and atopic dermatitis together drive the highest biologic volumes, with dupilumab covering 22% of moderate-to-severe atopic-dermatitis patients in North America by 2025. Alopecia areata diagnoses climbed after baricitinib’s approval, illustrating how therapeutic breakthroughs stimulate diagnostic vigilance.

Market bifurcation is evident: high-volume, low-margin acne competes alongside hidradenitis, a low-volume yet high-margin niche that relies on premium biologics. The dermatological therapeutics market size for hidradenitis is small today but poised for outsized revenue influence as pipeline IL-17 and TNF inhibitors mature. Rosacea and seborrheic dermatitis remain dominated by generics, but microbiome-directed candidates are now in Phase II, hinting at future high-value subsegments. Such heterogeneity sustains innovation incentives while complicating payer forecasting within the dermatological therapeutics market.

By Drug Class: Small-Molecule Inhibitors Reshape Competitive Dynamics

Small-molecule inhibitors across PDE-4, JAK, and TYK2 pathways are on track to grow at a 15.75% CAGR, surpassing biologics and topical corticosteroids. Ritlecitinib gained FDA approval for alopecia areata in 2024 and delivered 40% scalp-hair regrowth in pivotal studies. Ruxolitinib cream expanded into vitiligo, representing the first topical JAK inhibitor to secure a second indication. Deucravacitinib achieved plaque-psoriasis approval and awaits psoriatic-arthritis clearance, which could add USD 2 billion in peak sales.

Topical corticosteroids retained a 25.53% dermatological therapeutics market share in 2025, reflecting entrenched guideline placement and low cost. Yet profit pressure is intensifying because excipient disruptions raise manufacturing risk. Retinoid demand remains steady at 14% of prescriptions, buoyed by new androgen-receptor antagonist clascoterone. Calcineurin inhibitors lose share as JAKs capture moderate-atopic-dermatitis scripts. Biologic revenue faces 2027-2029 patent cliffs, making small molecules central to revenue continuity within the dermatological therapeutics market.

By Route of Administration: Injectables Capture Adherence Premium

Topicals delivered 65.15% of 2025 sales, but injectables are growing at 11.82% CAGR thanks to quarterly and biannual dosing that drives 34% higher adherence versus daily topicals. Three long-acting injectables cleared the FDA between 2024 and 2025, including a six-month dupilumab depot under priority review. Oral JAK inhibitors upadacitinib and abrocitinib expanded indications, yet require safety monitoring that limits first-line use.

The dermatological therapeutics market size for injectables is still smaller than topicals, but payer analyses show 19% lower total cost of care for biologic-treated psoriasis than methotrexate cohorts. Microneedle patches in Phase II aim to localize drug delivery for vitiligo and localized psoriasis. Excipient shortages that hit topical supply chains illustrate why multi-route portfolios hedge manufacturer risk within the dermatological therapeutics market.

By Distribution Channel: Online Pharmacies Extend Virtual Care

Retail pharmacies and drugstores held 54.65% of 2025 revenue, but online pharmacies are expanding at 13.32% CAGR, the swiftest among channels. DEA extensions of pandemic-era telemedicine flexibilities keep Schedule III-V dermatology prescribing online through December 2025. Amazon Pharmacy created a dermatology storefront that couples virtual consults with same-day shipping, underscoring a direct-to-consumer shift.

Hospital pharmacies preserve an 11% share by managing cold-chain injectables and prior-authorization heavy biologics, while dermatology clinics dispense compounded topicals that bypass commercial supply chains. India’s e-pharmacy sector grew 41% during 2024-2025 under CDSCO authorization, proving that regulatory support catalyzes digital uptake. Payers are cutting copays for digital fills, lowering per-prescription costs by 22% versus brick-and-mortar. The dermatological therapeutics market therefore reflects a structural pivot toward omnichannel fulfillment.

By Therapy Type: OTC Reclassifications Accelerate Self-Care

Prescription drugs controlled 62.23% of 2025 sales, yet OTC formulations are expanding at 11.12% CAGR. The EMA shifted hydrocortisone 1% to pharmacy-counter status in 2024, and Japan reclassified three topical antifungals in 2025. The dermatological therapeutics market size for OTC products is rising as regulators shorten switch timelines below five years.

OTC gains boost consumer autonomy but remove reimbursement, restricting adoption among low-income groups. Premium biologics remain insulated because complexity and monitoring needs bar OTC migration. Manufacturers thus weigh early OTC transitions that gain volume at the expense of margins against delayed switches that risk generic cannibalization. Balancing these forces is central to lifecycle strategy in the broader dermatological therapeutics industry.

Geography Analysis

North America generated 38.23% of 2025 revenue, driven by high biologic penetration and favorable reimbursement. Medicare Part D covers 14 dermatology biologics under specialty tiers, offering catastrophic-cost protection after USD 8,000 in out-of-pocket spending. Canada added dupilumab and ustekinumab to provincial plans in 2024, giving 1.2 million additional patients subsidized access. Mexico’s approval of six biosimilars during 2024-2025 cut originator pricing by 35%[3]COFEPRIS, “Regulatory Approvals,” Gob.mx. Workforce shortages persist, and the Association of American Medical Colleges forecasts a deficit of 3,200 dermatologists by 2030. Teledermatology rose 52% over 2023-2025 but reimbursement parity varies by state Medicaid program.

Asia-Pacific is the fastest-growing region at 10.12% CAGR through 2031, propelled by regulatory harmonization and income gains. China approved 14 dermatology biologics in 2024-2025, including local biosimilars priced 60% below originators. Japan granted accelerated clearance to five JAK inhibitors in 2024, leveraging robust post-marketing surveillance. India streamlined biosimilar reviews from 18 months to 10 months in 2025, cementing export ambitions. South Korea and Australia recorded USD 2.1 billion in aesthetic-dermatology sales during 2025, backed by medical-tourism infrastructure. Out-of-pocket expenses still exceed 70% in parts of Southeast Asia, limiting biologic penetration.

Europe presents stringent price controls yet broad access. Germany extended dupilumab reimbursement to adolescents in 2024, covering 340,000 insured lives. NICE evaluated four biologics in 2024-2025, approving three and restricting one to severe cases. France and Italy mandated biosimilar substitution in 2025 and achieved 42% market share within 12 months. The Middle East is emerging, with GCC nations investing USD 1.2 billion in dermatology centers. South America saw Anvisa green-light seven biosimilars over 2024-2025, but public procurement dominates 65% of distribution.

Competitive Landscape

The dermatological therapeutics market is fragmented. The top five players—AbbVie, Eli Lilly, Novartis, Pfizer, and Regeneron—together held a sizable share of 2025 revenue, yet biosimilars and specialty biotechs are fragmenting mature territories. AbbVie’s Skyrizi and Rinvoq delivered USD 9.8 billion in 2025 sales, but Humira erosion trimmed total immunology income by 18%. Arcutis grew roflumilast cream prescriptions 67% year over year, capturing 9% of U.S. plaque-psoriasis topical scripts within two years. Technology alliances are redefining support models: Pfizer, Novartis, LEO Pharma, and Galderma rolled out AI companion apps that knit symptom tracking with refill prompts.

Patent activity underscores shifting priorities. Microbiome-modulating filings jumped 34% during 2024-2025, and twelve candidates entered Phase II trials targeting atopic dermatitis and acne. The FDA granted breakthrough tags to three small-cap dermatology assets in 2024-2025, compressing timelines and priming acquisition interest. Digital-health entrants that bundle teledermatology with fulfillment already capture 6% of U.S. acne sales. Portfolio repositioning ahead of 2027-2029 patent cliffs is intense as companies strive to sustain pricing power within the dermatological therapeutics industry.

Dermatological Therapeutics Industry Leaders

AbbVie Inc.

Eli Lilly and Company

Novartis AG

Pfizer Inc.

Regeneron Pharmaceuticals Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Nektar Therapeutics announced positive 36-week maintenance results for rezpegaldesleukin in moderate-to-severe atopic dermatitis.

- January 2026: Sanofi reported favorable data for amlitelimab in patients aged 12 and older with atopic dermatitis.

Global Dermatological Therapeutics Market Report Scope

As per the scope of the report, dermatological therapeutics are drugs used to treat and prevent various dermatological conditions.

The segmentation of the dermatological therapeutics market is categorized by disease, drug class, route of administration, distribution channel, therapy type, and geography. By disease, the market includes acne vulgaris, psoriasis, atopic dermatitis/eczema, alopecia areata, hidradenitis suppurativa, seborrheic dermatitis, rosacea, and others. By drug class, it is segmented into topical corticosteroids, retinoids, anti-infectives (antibiotics and antifungals), calcineurin inhibitors, biologics and biosimilars, small-molecule inhibitors (PDE-4, JAK, TYK2), and others. By route of administration, the categories include topical, oral, injectable, transdermal patches, and others. By distribution channel, the market is divided into hospital pharmacies, retail pharmacies and drugstores, dermatology and aesthetic clinics, and online pharmacies. By therapy type, it is segmented into prescription drugs and over-the-counter (OTC) drugs. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Acne Vulgaris |

| Psoriasis |

| Atopic Dermatitis / Eczema |

| Alopecia Areata |

| Hidradenitis Suppurativa |

| Seborrheic Dermatitis |

| Rosacea |

| Others |

| Topical Corticosteroids |

| Retinoids |

| Anti-infectives (Antibiotics & Antifungals) |

| Calcineurin Inhibitors |

| Biologics & Biosimilars |

| Small-molecule Inhibitors (PDE-4, JAK, TYK2) |

| Others |

| Topical |

| Oral |

| Injectable |

| Transdermal Patches |

| Others |

| Hospital Pharmacies |

| Retail Pharmacies & Drugstores |

| Dermatology & Aesthetic Clinics |

| Online Pharmacies |

| Prescription Drugs |

| Over-the-Counter (OTC) Drugs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disease | Acne Vulgaris | |

| Psoriasis | ||

| Atopic Dermatitis / Eczema | ||

| Alopecia Areata | ||

| Hidradenitis Suppurativa | ||

| Seborrheic Dermatitis | ||

| Rosacea | ||

| Others | ||

| By Drug Class | Topical Corticosteroids | |

| Retinoids | ||

| Anti-infectives (Antibiotics & Antifungals) | ||

| Calcineurin Inhibitors | ||

| Biologics & Biosimilars | ||

| Small-molecule Inhibitors (PDE-4, JAK, TYK2) | ||

| Others | ||

| By Route of Administration | Topical | |

| Oral | ||

| Injectable | ||

| Transdermal Patches | ||

| Others | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies & Drugstores | ||

| Dermatology & Aesthetic Clinics | ||

| Online Pharmacies | ||

| By Therapy Type | Prescription Drugs | |

| Over-the-Counter (OTC) Drugs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast value of the dermatological therapeutics market in 2031?

It is expected to reach USD 83.59 billion by 2031.

Which disease segment is growing fastest?

Hidradenitis suppurativa is growing at a 14.25% CAGR through 2031.

How quickly are online pharmacies expanding?

Online pharmacy revenue is growing at a 13.32% CAGR.

Which geographic region is the fastest growing?

Asia-Pacific is advancing at a 10.12% CAGR through 2031.

Why are injectables gaining share?

Quarterly or biannual biologic doses drive 34% better adherence and 19% lower total care costs than daily topicals.

Page last updated on: