Pemphigus Vulgaris Therapeutics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

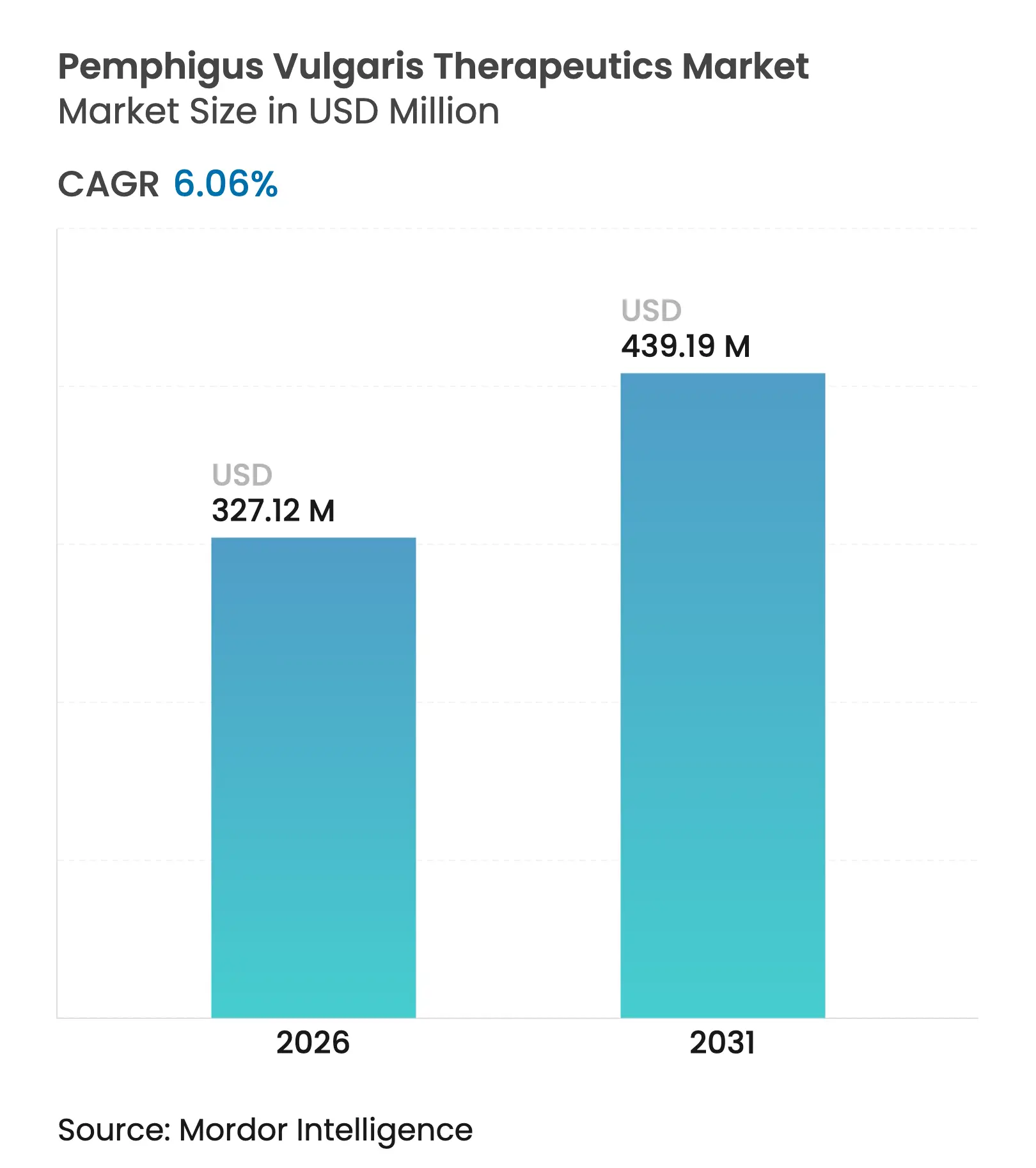

| Market Size (2026) | USD 327.12 Million |

| Market Size (2031) | USD 439.19 Million |

| Growth Rate (2026 - 2031) | 6.06 % CAGR |

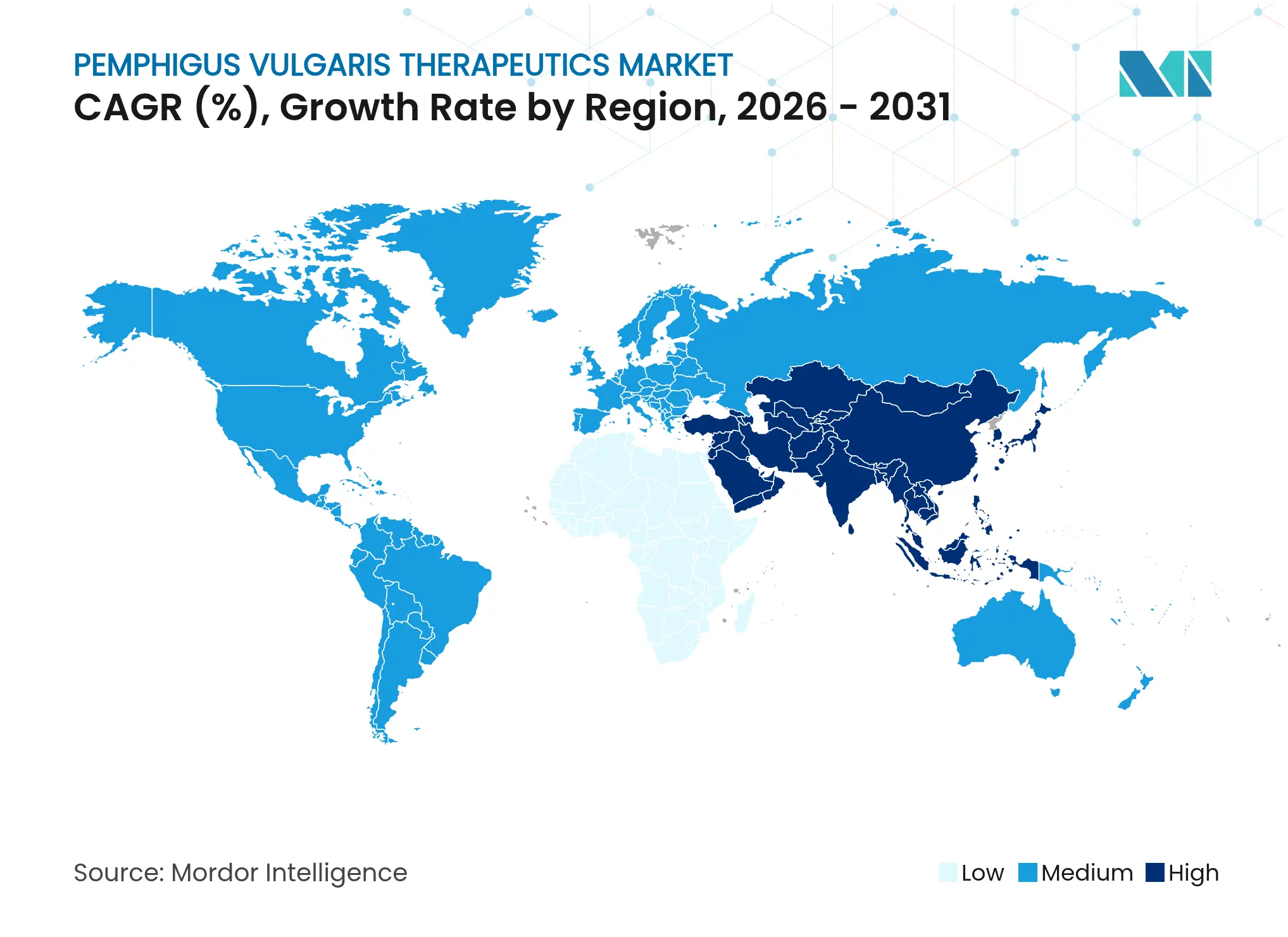

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Pemphigus Vulgaris Therapeutics Market Analysis by Mordor Intelligence

The pemphigus vulgaris therapeutics market size is expected to grow from USD 308.43 million in 2025 to USD 327.12 million in 2026 and is forecast to reach USD 439.19 million by 2031 at 6.06% CAGR over 2026-2031. Robust uptake of targeted biologics after the 2024 approval of rituximab, a maturing pipeline featuring CAR-T, FcRn antagonists and AI-enabled repurposed agents, and widening orphan-drug incentives combine to reinforce an upward revenue trajectory. In clinical use, rituximab has delivered complete remission in 90% of treated patients at the 24-month mark, dwarfing the 28% rate achieved with corticosteroids alone, a shift that has reduced cumulative steroid exposure and long-term toxicity. Demand momentum is also evident in the move toward subcutaneous delivery, which boosts patient autonomy and trims infusion-center overheads; in the rapid expansion of online specialty pharmacies providing home delivery; and in Asia Pacific reimbursement reforms that quicken therapeutic adoption. Still, cold-chain hurdles in tropical markets, the high cost-to-income ratio in low-resource settings, and long regulatory follow-ups temper near-term upside.

Key Report Takeaways

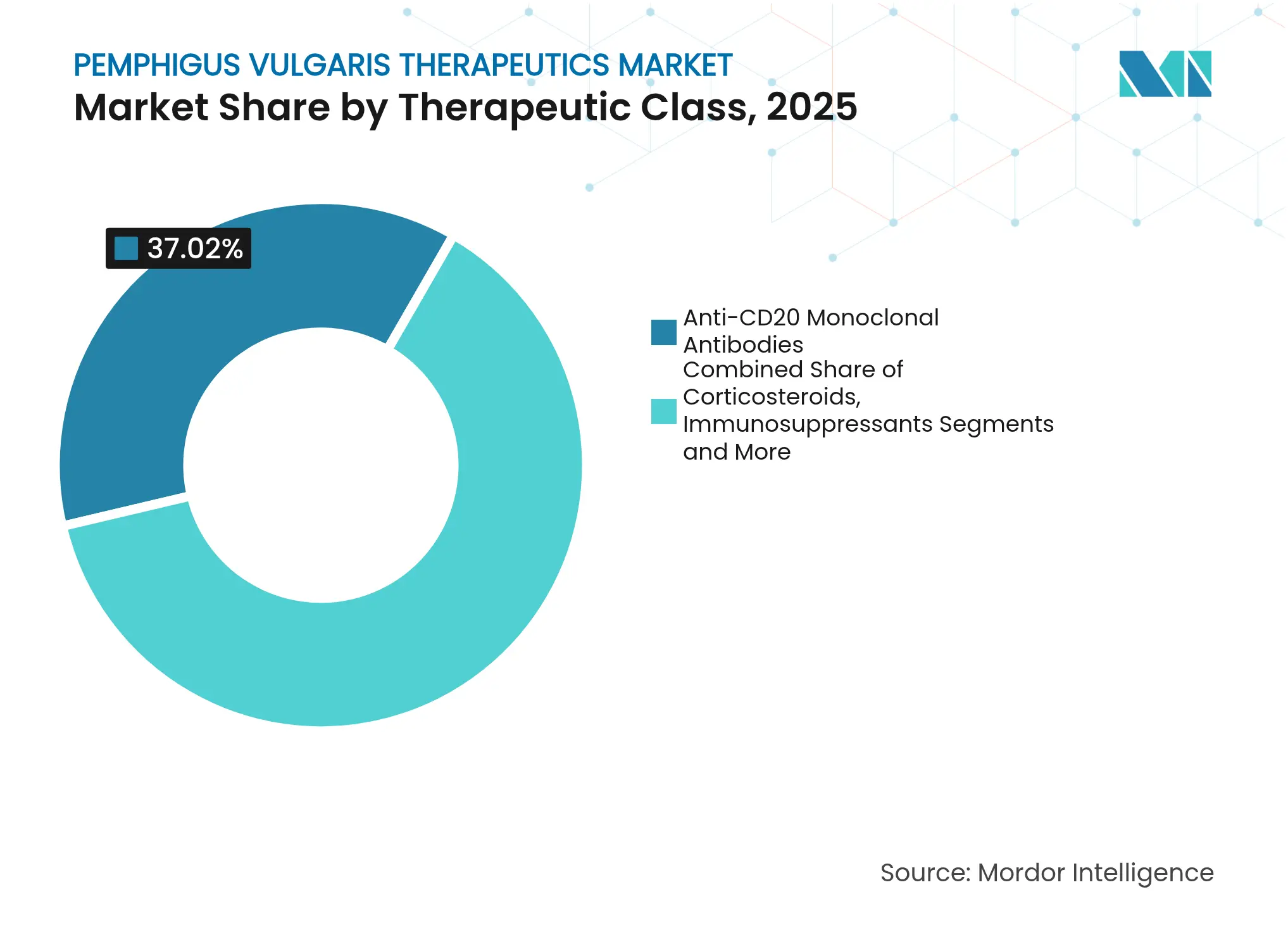

- By therapeutic class, anti-CD20 monoclonal antibodies held 37.02% of pemphigus vulgaris therapeutics market share in 2025, while emerging biologics and small-molecule inhibitors post the fastest 9.32% CAGR to 2031.

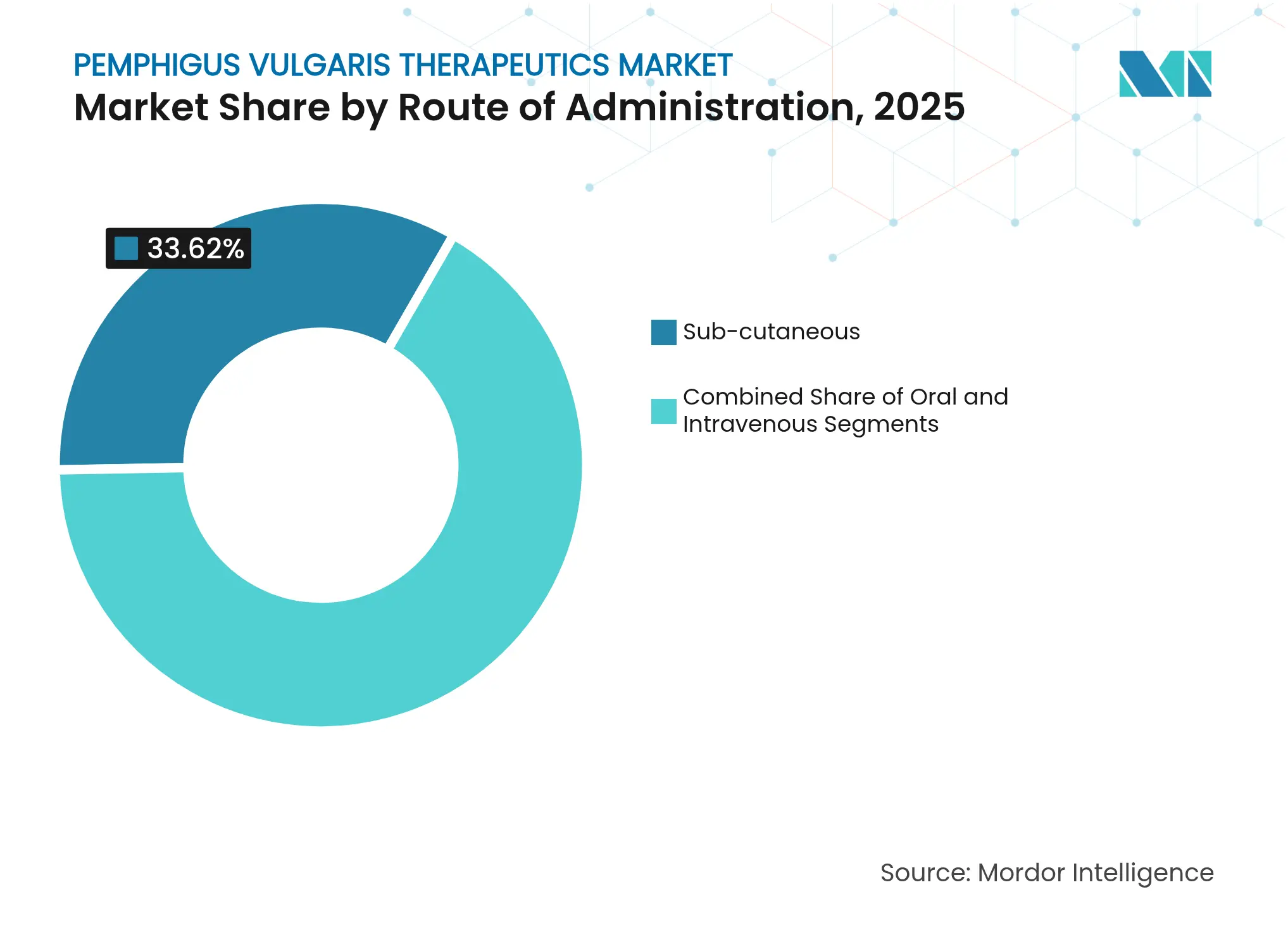

- By route of administration, intravenous drugs dominated with 44.41% revenue share in 2025; subcutaneous formulations lead growth at 8.33% CAGR through 2031.

- By distribution channel, hospital pharmacies retained a 52.94% share in 2025; online pharmacies expanded the quickest at 10.12% CAGR.

- By geography, North America led with 34.15% 2025 share, yet Asia Pacific registers the highest 5.32% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pemphigus Vulgaris Therapeutics Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increasing prevalence of pemphigus

vulgaris

Increasing prevalence of pemphigus

vulgaris

| +0.8% | Global, higher in Mediterranean and Jewish populations | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+0.8%

|

Geographic Relevance

:

Global, higher in Mediterranean and

Jewish populations

|

Impact Timeline

:

Long term (≥ 4 years)

|

Rising adoption of rituximab &

next-generation mAbs

Rising adoption of rituximab &

next-generation mAbs

| +1.2% | North America & EU leading, expanding to APAC | Medium term (2-4 years) | |||

Growing R&D pipeline and

clinical trials

Growing R&D pipeline and

clinical trials

| +0.9% | Global, concentrated in US biotech hubs | Long term (≥ 4 years) | |||

Favorable reimbursement for orphan

drugs

Favorable reimbursement for orphan

drugs

| +0.7% | North America, EU, select APAC markets | Medium term (2-4 years) | |||

Expansion of compassionate-access

programs

Expansion of compassionate-access

programs

| +0.4% | Global, especially emerging markets | Short term (≤ 2 years) | |||

AI-driven repurposing of kinase

inhibitors

AI-driven repurposing of kinase

inhibitors

| +0.6% | North America & EU research centers | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Increasing Prevalence of Pemphigus Vulgaris

Global epidemiology studies place prevalence between 0.38 and 30 per 100,000, a wide span reflecting both genetic predisposition and historical under-diagnosis. As diagnostic immunofluorescence and antibody assays reach community clinics, more cases are identified earlier, especially in populations carrying HLA-DRB1 0402 and DQB1 0503 alleles. Environmental triggers such as thiol- or phenol-based drugs continue to surface, with pharmacovigilance networks flagging new culprits every year. Because onset peaks in the 50-60-year age group, population aging across developed economies further lifts incidence. Collectively these factors enlarge the treated population, reinforcing revenue visibility for manufacturers.[1]Mattie Rosi-Schumacher et al., “Worldwide Epidemiologic Factors in Pemphigus Vulgaris and Bullous Pemphigoid,” Frontiers in Immunology, frontiersin.org

Rising Adoption of Rituximab & Next-Generation mAbs

Rituximab’s 2024 approval as first-line therapy has re-set clinical practice: five-year drug-free survival now reaches 76.7% and persists at 72.1% by year seven, a stark improvement over steroids alone. South Korea’s national insurance listing shortened time-to-therapy initiation and reduced cumulative steroid exposure. Pipeline biologics—from FcRn blockers such as efgartigimod to CD20-targeting bispecifics—seek to replicate or surpass rituximab outcomes, though discontinuation decisions, as seen in bullous pemphigoid, underline the selectivity of autoimmune drug development. Subcutaneous, low-dose iterations further ease outpatient administration and curb infusion costs.[2]Billal Tedbirt et al., “Sustained Remission With Rituximab in Patients With Pemphigus,” JAMA Dermatology, jamanetwork.com

Growing R&D Pipeline and Clinical Trials

Global autoimmune pipelines list 193 active assets, up 47% versus 2020. CAR-T candidate KYV-101 has entered Phase II trials that aim to restore immune tolerance rather than chronically suppress disease. BTK inhibition remains contested after rilzabrutinib’s Phase III miss, yet tirabrutinib continues under orphan-drug protection. Large-pharma deals, exemplified by a USD 1.8 billion BMS–Repertoire pact on tolerizing vaccines, show capital alignment behind durable therapies that could redefine patient journeys.

Favorable Reimbursement for Orphan Drugs

Seven-year exclusivity, federal tax credits, and fee waivers substantially reduce risk-adjusted development cost, while accelerated reviews shorten regulatory cycles by up to 60 days in both FDA and EMA pathways. The US Orphan Products Grants Program disburses above USD 650 million annually, and Japan’s Sakigake system offers parallel incentives, catalyzing multinational submission strategies. Private payers now deploy outcomes-based contracts that tie net prices to remission durability, reinforcing alignment between manufacturers, insurers and patients.[3]U.S. Food and Drug Administration, “Developing Products for Rare Diseases & Conditions,” fda.gov

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stringent regulatory & approval

timelines

Stringent regulatory & approval

timelines

| -0.9% | Global, stricter in EU and Japan | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

-0.9%

|

Geographic Relevance

:

Global, stricter in EU and Japan

|

Impact Timeline

:

Long term (≥ 4 years)

|

High treatment cost in low-income

regions

High treatment cost in low-income

regions

| -0.7% | APAC emerging markets, Latin America, Africa | Medium term (2-4 years) | |||

Limited cold-chain in tropical

markets

Limited cold-chain in tropical

markets

| -0.5% | Southeast Asia, Sub-Saharan Africa, tropical Latin America | Short term (≤ 2 years) | |||

Rural dermatology-specialist

shortage

Rural dermatology-specialist

shortage

| -0.4% | Global rural areas, acute in developing nations | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Stringent Regulatory & Approval Timelines

Autoimmune biologics often require 12-15-year development cycles, several years longer than oncology or metabolic categories. Agencies mandate long safety follow-up because B-cell depletion heightens infection risk, and post-marketing studies extending five years inflate capital needs. Europe further insists on real-world evidence when pivotal trials enroll small cohorts, while Japan’s PMDA tests clinical meaningfulness beyond statistical significance, adding further delay. Endpoint complexity—particularly validation of the Pemphigus Disease Area Index across diverse ethnicities—places statistical and operational strain on sponsors.

High Treatment Cost in Low-Income Regions

Annual biologic therapy can exceed 10-15 times median household income in India or Brazil, effectively rationing care to elite urban centers. Currency volatility, customs duties above 20% on imported proteins, and scarce outcomes-based financing frameworks amplify affordability problems. Public formularies seldom reimburse orphan drugs, leaving families to crowd-fund therapy or forego care altogether, constraining volume uptake despite clinical need.

Segment Analysis

By Therapeutic Class: Biologics Drive Treatment Evolution

Anti-CD20 monoclonal antibodies captured 37.02% of pemphigus vulgaris therapeutics market share in 2025 on the back of rituximab’s landmark approval and well-documented durability. The segment’s leadership is expected to persist as biosimilar entries widen geographical reach and cost competitiveness. Emerging biologics and small-molecule inhibitors record a 9.32% CAGR to 2031, propelled by FcRn blockade, BTK inhibition and CAR-T modalities that aim for immune re-education rather than chronic suppression. In resource-limited settings, corticosteroids and generic immunosuppressants remain front-line options, though the long list of metabolic and infectious side effects keeps the search for safer substitutes active. IVIg, positioned as rescue therapy or adjunct, underpins long-term remission in more than half of monotherapy patients according to two-decade follow-up data. Antibiotics, antivirals and antifungals preserve quality of life by curbing opportunistic infections during immunosuppression.

Continued biological innovation is likely to re-size the therapeutics mix; the pemphigus vulgaris therapeutics market size for emerging biologics is projected to expand at 9.32% CAGR through 2031, narrowing the gap with anti-CD20 incumbents. Yet cost sensitivity, variable reimbursement and heterogeneous physician familiarity suggest a protracted coexistence across the class spectrum. Strategic collaborations, illustrated by Sanofi’s USD 1.9 billion bet on a CD20 bispecific, underscore the premium on differentiated modes of action that can command orphan pricing while promising shorter infusion times and reduced monitoring burden. Payers, facing cumulative budget impact, are expected to press for value-based contracts pegged to relapse-free survival, nudging manufacturers to generate robust real-world evidence early.

Note: Segment shares of all individual segments available upon report purchase

By Route of Administration: Subcutaneous Innovation Accelerates

Intravenous infusions accounted for 44.41% of 2025 sales, sustained by hospital-based rituximab protocols requiring trained staff and acute adverse-event management. Nevertheless, subcutaneous formulations post the quickest 8.33% CAGR and could erode hospital dominance as auto-injectors and on-body pumps migrate therapy to the home. Health-system modeling suggests self-administration lowers overall care cost by 30-40% due to fewer chair-time charges and reduced work-loss days. Oral agents, chiefly immunosuppressants, maintain relevance, yet molecule size and first-pass metabolism limit suitability for monoclonal antibodies. Nanoparticle carriers and transdermal patches under exploration could further diversify the modality spectrum. Clinical guidelines now recommend patient-centric route selection, encouraging shared decision-making that weighs convenience, comorbidity and adherence.

The pemphigus vulgaris therapeutics market size attributable to subcutaneous options is projected to rise rapidly as pipeline drugs adopt this route from the outset, bypassing later reformulation cycles. Hospital pharmacies are responding by integrating training modules and remote supervision software, a model that aligns with payers’ push for site-of-care optimization. Over time, subcutaneous dominance may relax healthcare-facility bottlenecks and shorten treatment queues, particularly in regions with specialist shortages, closing access gaps and enhancing equity.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Digital Transformation Reshapes Access

Hospital pharmacies commanded 52.94% of 2025 distribution owing to the need for infusion oversight, cold-chain facilities and on-site laboratory monitoring. Yet online specialty pharmacies, scaling at 10.12% CAGR, are redefining supply by offering home delivery, nurse hotlines and reimbursement assistance through unified digital portals. Retail pharmacies have lagged because few maintain validated biologics storage, although strategic alliances with third-party cold-chain providers are emerging. Hybrid models, hospital initiation followed by home-delivery maintenance, blend safety with convenience and already account for 18% of biologic volumes in the United States. Payer steering toward designated channels that demonstrate cost-effectiveness and adherence support is likely to accelerate consolidation in favor of high-service platforms.

As e-commerce penetration spreads, the pemphigus vulgaris therapeutics market size transacted via online pharmacies is set to expand briskly, especially in geographies where broadband and mobile payment infrastructure mature rapidly. Compliance analytics derived from connected packaging may enable dynamic copay tiers tied to adherence, aligning economic incentives across stakeholders. For manufacturers, digital distribution enriches pharmacovigilance datasets, informing iterative safety assessments required under post-marketing commitments.

Geography Analysis

North America retained 34.15% of global revenue in 2025, underpinned by FDA breakthrough designations that compress review cycles and by comprehensive payer coverage that absorbs high biologic prices. Academic centers spearhead trial activity, and mature specialty-pharmacy networks facilitate same-day dispensing and remote monitoring. The region also benefits from AI research leadership, evidenced by Penn State’s autoimmune discovery algorithms that guide precision prescribing. Patient-support foundations channel grants and educational resources that speed diagnosis and therapy uptake.

Asia Pacific delivers the fastest trajectory at 5.32% CAGR through 2031. China’s inaugural pemphigus treatment guideline issued in 2024 now standardizes diagnostic work-ups across tertiary and secondary hospitals, priming the market for biologic roll-out as reimbursement lists expand. South Korea’s early inclusion of rituximab illustrates how policy can drive real-world remission gains. Japan’s Sakigake pathway funnels pipeline drugs to market more quickly, while domestic biotech clusters in Shanghai, Seoul and Tokyo nurture local entrants targeting cost-optimized biosimilars and novel agents.

Europe remains pivotal, blending centralized regulatory oversight with country-level reimbursement negotiation. EMA accelerated assessments help orphan drugs reach clinics swiftly, but fiscal pressures in southern and eastern states stretch uptake timelines. Germany’s robust study infrastructure and the UK’s specialist centers act as referral magnets for complex cases, shaping data that informs guideline updates. Biosimilar adoption policies produce price tension that may broaden access yet dilute originator revenue streams.

Middle East and Africa experience structural barriers ranging from specialist scarcity to cold-chain gaps that restrain volume. Nevertheless, centers of excellence in the UAE and South Africa are evolving as regional reference sites, offering manufacturers footholds to extend educational outreach and logistics hubs. Multinational partnerships with local ministries and NGOs are beginning to pilot subsidized access programs that could unlock pent-up demand.

Competitive Landscape

Market Concentration

Competition is moderately fragmented: Roche anchors the anti-CD20 stronghold. The current market concentration score therefore lands at 6, reflecting notable though not overwhelming dominance by leading firms. Large-cap players focus on life-cycle management, including subcutaneous switching and biosimilar defenses, while licensing deals bring in pipeline diversity. AbbVie bolstered its autoimmune portfolio through acquisitions targeting oral small-molecule modulators, and Pfizer advances kinase inhibitors that may complement existing dermatology assets.

White-space opportunities lie in pediatric indications, mucosal-predominant variants and steroid-resistant cohorts where evidence remains sparse. CAR-T developers like Kyverna and Cabaletta Bio propose a one-time curative reset; early data will either validate or temper investor enthusiasm for cell-based modalities in rare autoimmunity. AI-enabled target discovery, exemplified by Autoimmunity Biosolutions, shortens R&D timelines and encourages venture and strategic funding inflows. Cost-containment imperatives spur outcome-based purchasing, favoring companies that can supply digital adherence tools and longitudinal data to corroborate durable remission.

Forward integration into patient-support ecosystems differentiates contenders: Roche’s nurse educator network, Incyte’s holistic assistance platform and Sanofi’s logistics alliances all illustrate how service layers strengthen therapeutic stickiness. With biosimilar entrants expected post-exclusivity, originators prepare defensive plays such as indication-expansion studies, formulation upgrades and value-added service contracts

Pemphigus Vulgaris Therapeutics Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Cabaletta enrolled the first subject in the RESET-PV trial assessing rese-cel without preconditioning for pemphigus vulgaris.

- March 2024: Rilzabrutinib did not meet the primary endpoint in the Phase III PEGASUS study, though subgroup analysis suggested benefit when paired with low-dose steroids.

- February 2024: Seven-year rituximab follow-up published in JAMA Dermatology affirmed 72.1% steroid-free remission durability.

Table of Contents for Pemphigus Vulgaris Therapeutics Industry Report

1. Introduction

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Increasing Prevalence Of Pemphigus Vulgaris

- 4.2.2Rising Adoption Of Rituximab & Next-Gen Mabs

- 4.2.3Growing R&D Pipeline And Clinical Trials

- 4.2.4Favorable Reimbursement For Orphan Drugs

- 4.2.5Expansion Of Compassionate-Access Programs

- 4.2.6AI-Driven Repurposing Of Kinase Inhibitors

- 4.3Market Restraints

- 4.3.1Stringent Regulatory & Approval Timelines

- 4.3.2High Treatment Cost In Low-Income Regions

- 4.3.3Limited Cold-Chain In Tropical Markets

- 4.3.4Rural Dermatology-Specialist Shortage

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technology Outlook

- 4.7Porter’s Five Forces Analysis

- 4.7.1Bargaining Power of Suppliers

- 4.7.2Bargaining Power of Buyers

- 4.7.3Threat of New Entrants

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. Market Size and Growth Forecasts (Value-USD)

- 5.1By Therapeutic Class

- 5.1.1Corticosteroids

- 5.1.2Immunosuppressants

- 5.1.3Anti-CD20 Monoclonal Antibodies

- 5.1.4IV Immunoglobulin (IVIg)

- 5.1.5Antibiotics & Antivirals

- 5.1.6Antifungals

- 5.1.7Emerging Biologics & Small-Molecule Inhibitors

- 5.2By Route of Administration

- 5.2.1Oral

- 5.2.2Intravenous

- 5.2.3Sub-cutaneous

- 5.3By Distribution Channel

- 5.3.1Hospital Pharmacies

- 5.3.2Retail Pharmacies

- 5.3.3Online Pharmacies

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Middle East and Africa

- 5.4.4.1GCC

- 5.4.4.2South Africa

- 5.4.4.3Rest of Middle East and Africa

- 5.4.5South America

- 5.4.5.1Brazil

- 5.4.5.2Argentina

- 5.4.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1F. Hoffmann-La Roche Ltd

- 6.3.2AbbVie Inc.

- 6.3.3Pfizer Inc.

- 6.3.4Novartis AG

- 6.3.5GlaxoSmithKline plc

- 6.3.6AstraZeneca plc

- 6.3.7Grifols Therapeutics LLC

- 6.3.8Prometheus Laboratories

- 6.3.9Gilead Sciences Inc.

- 6.3.10Kyowa Kirin Co. Ltd

- 6.3.11Incyte Corporation

- 6.3.12HanAll Biopharma Co. Ltd

- 6.3.13Argenx SE

- 6.3.14Sanofi

- 6.3.15UCB S.A.

- 6.3.16Immunovant Inc.

- 6.3.17MindImmune Therapeutics

- 6.3.18Daewoong Pharm. Co. Ltd

- 6.3.19Johnson & Johnson

- 6.3.20CSL Behring

- 6.3.21Octapharma AG

7. Market Opportunities & Future Outlook

- 7.1White-Space & Unmet-Need Assessment

Global Pemphigus Vulgaris Therapeutics Market Report Scope

As per the scope of the report, pemphigus vulgaris is a rare autoimmune disorder characterized by painful blisters and erosions on the skin and mucous membranes due to the immune system mistakenly attacking proteins that facilitate cell adhesion. This condition can significantly impact the quality of life and requires ongoing treatment, often involving immunosuppressive medications to manage symptoms and prevent complications. Pemphigus vulgaris therapeutics refers to the medical therapies and interventions designed to manage and alleviate the symptoms of pemphigus vulgaris, an autoimmune disorder characterized by blistering skin and mucous membranes.

The pemphigus vulgaris therapeutics market is segmented by treatment and geography. The market is segmented by treatment into corticosteroids, immunosuppressive, intravenous immunoglobulin, antibiotics and antivirals, antifungals, and other treatments. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across the major regions globally. The report offers the market sizes and forecasts in value (USD) for the above segments.