Triamcinolone Ointment Chlorofluorocarbons Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

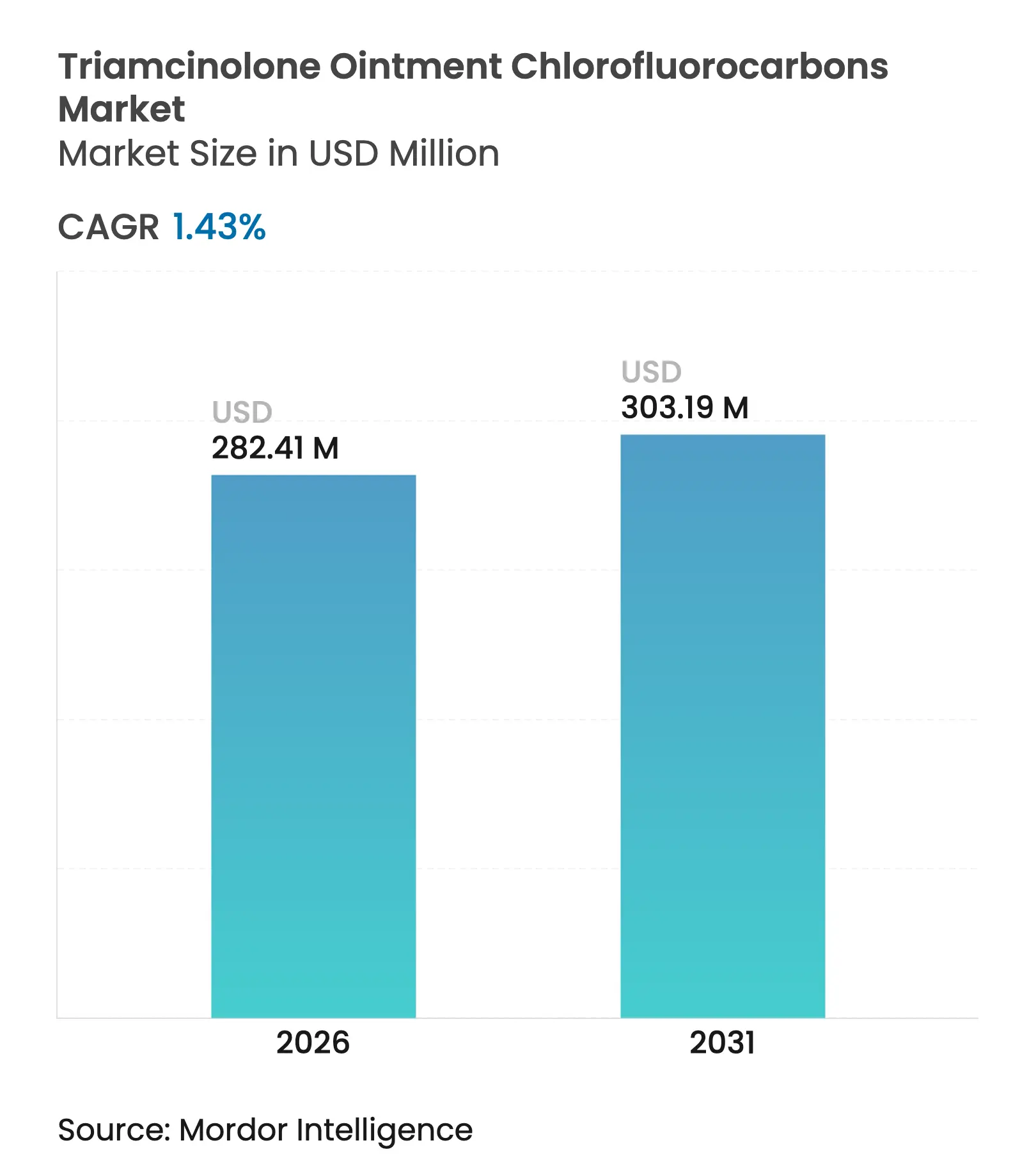

| Market Size (2026) | USD 282.41 Million |

| Market Size (2031) | USD 303.19 Million |

| Growth Rate (2026 - 2031) | 1.43 % CAGR |

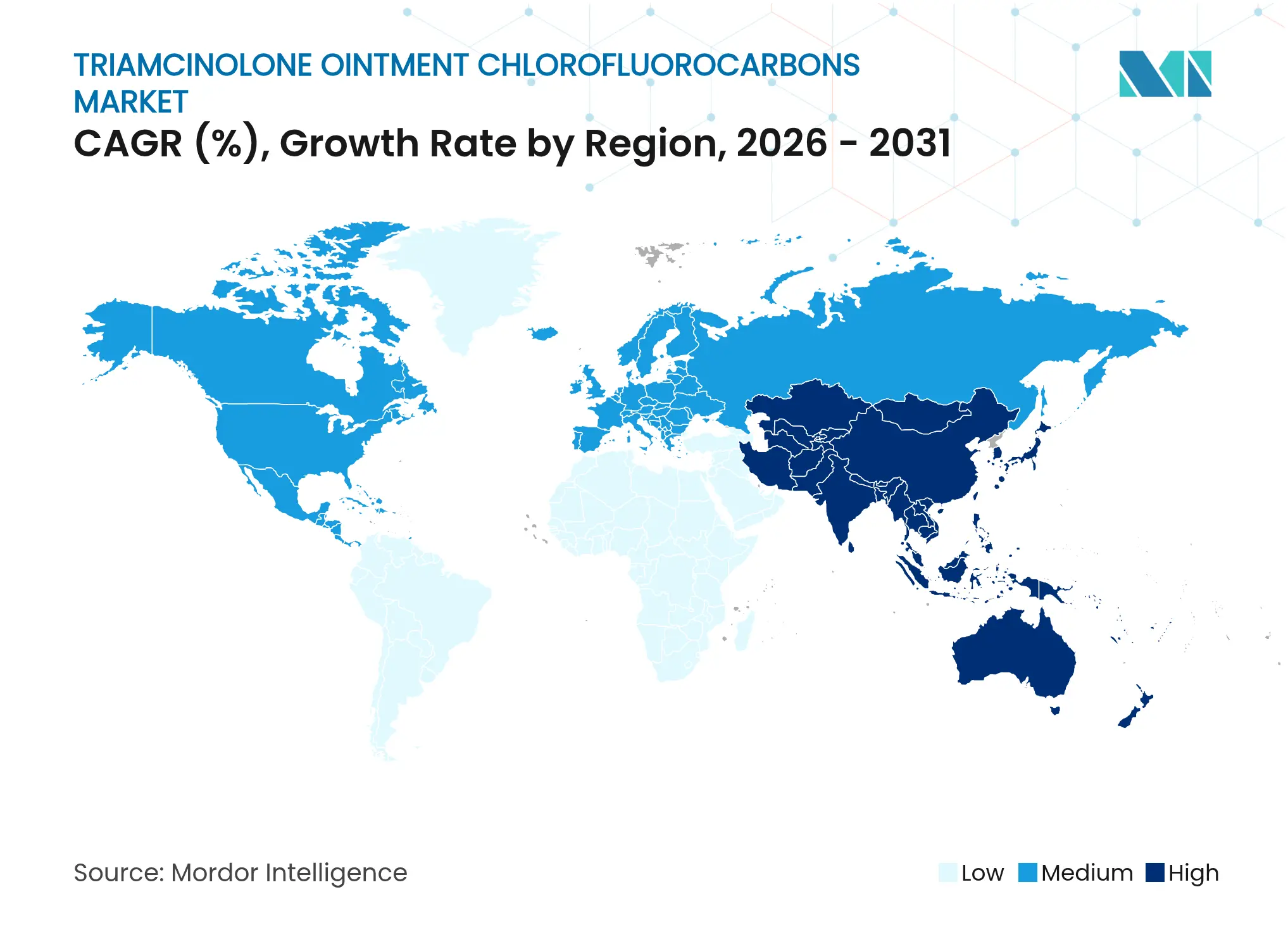

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

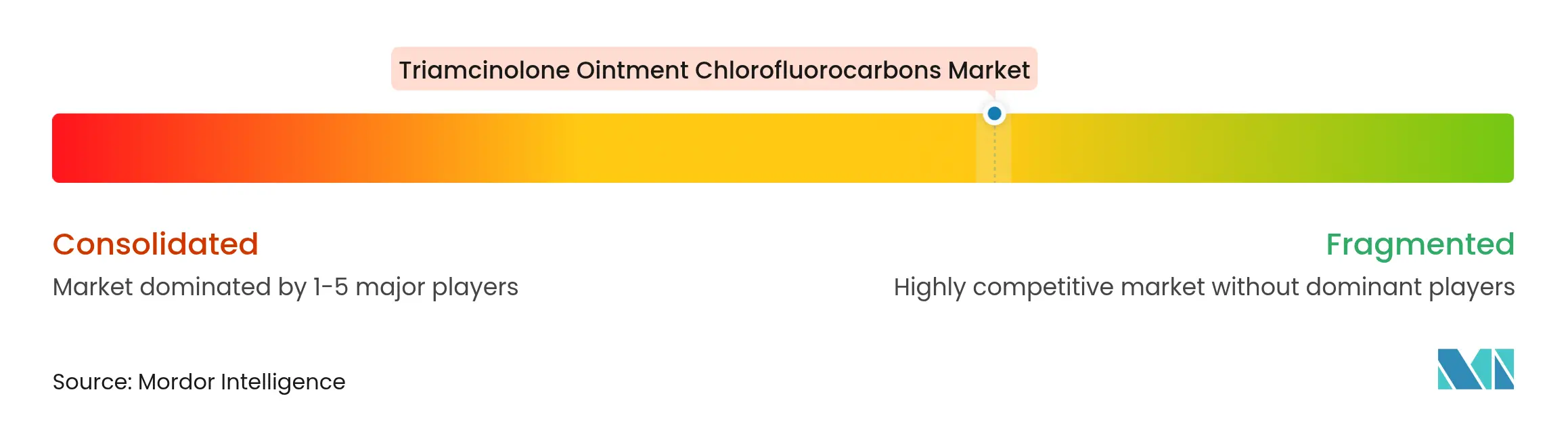

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Triamcinolone Ointment Chlorofluorocarbons Market Analysis by Mordor Intelligence

The triamcinolone ointment chlorofluorocarbons market size was valued at USD 278.43 million in 2025 and estimated to grow from USD 282.41 million in 2026 to reach USD 303.19 million by 2031, at a CAGR of 1.43% during the forecast period (2026-2031). This specialized pharmaceutical segment operates within a unique regulatory framework where chlorofluorocarbons remain permissible under Montreal Protocol exemptions for essential medical uses, creating a niche market insulated from broader environmental phase-out pressures[1]Environmental Protection Agency, "40 CFR 82.66 -- Nonessential Class I products and exceptions," ecfr.gov. The constrained growth trajectory reflects the tension between established therapeutic efficacy and evolving treatment paradigms that favor non-CFC formulations and alternative therapeutic modalities.

Key Report Takeaways

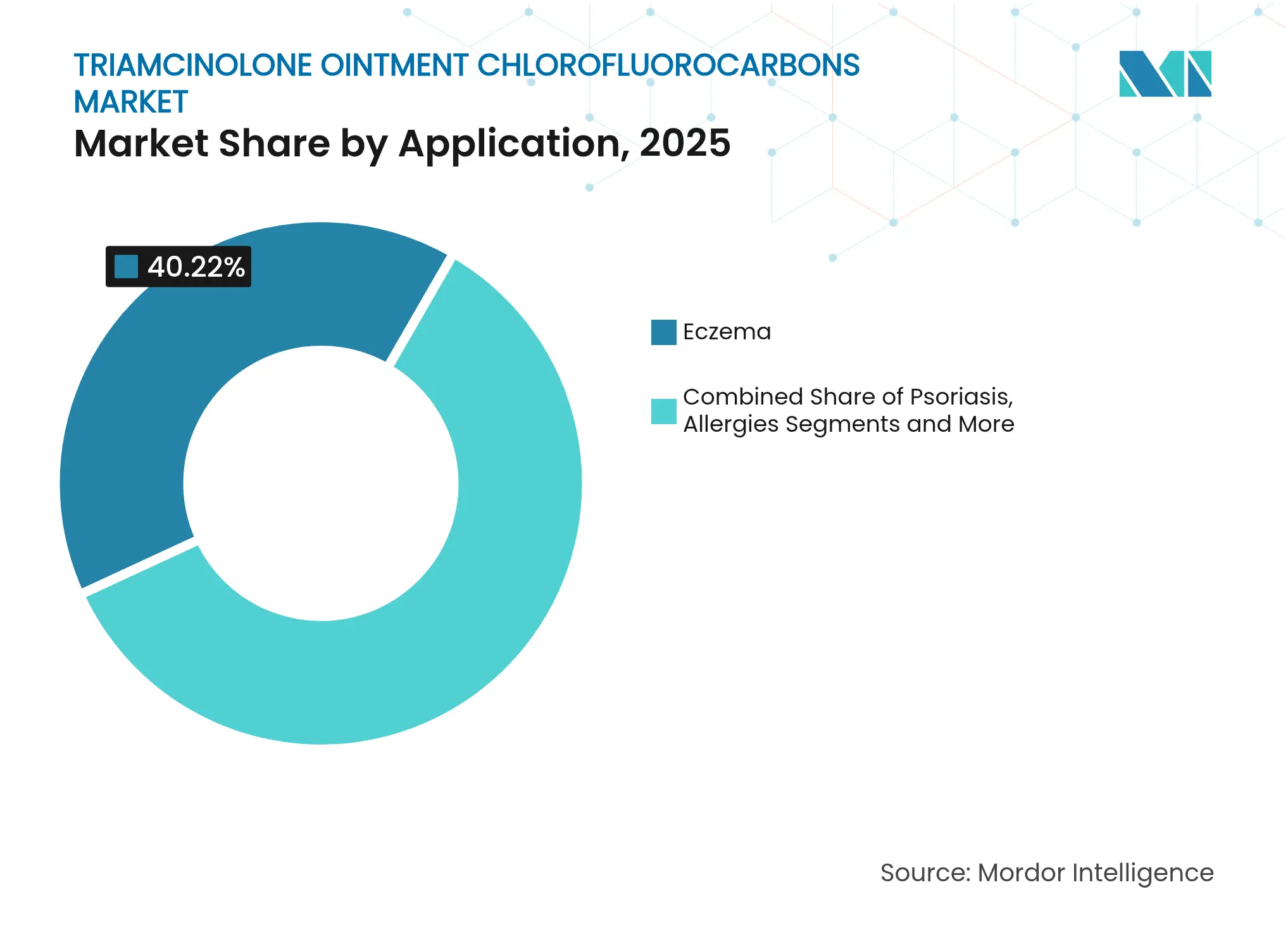

- By application, eczema dominated with 40.22% market share in 2025; psoriasis treatments are forecast to expand at a 6.2% CAGR to 2031.

- By concentration strength, the 0.10% formulation held 45.05% of the triamcinolone ointment chlorofluorocarbons market share in 2025, while higher potency formulations (0.5% and above) recorded the highest projected CAGR at 5.44% through 2031.

- By packaging type, tubes accounted for a 70.10% share of the triamcinolone ointment chlorofluorocarbons market size in 2025 and single-use sachets are advancing at a 7.21% CAGR through 2031.

- By patient age group, adult patients commanded 57.15% share of the triamcinolone ointment chlorofluorocarbons market in 2025, while pediatric applications demonstrated the strongest growth at 7.18% CAGR.

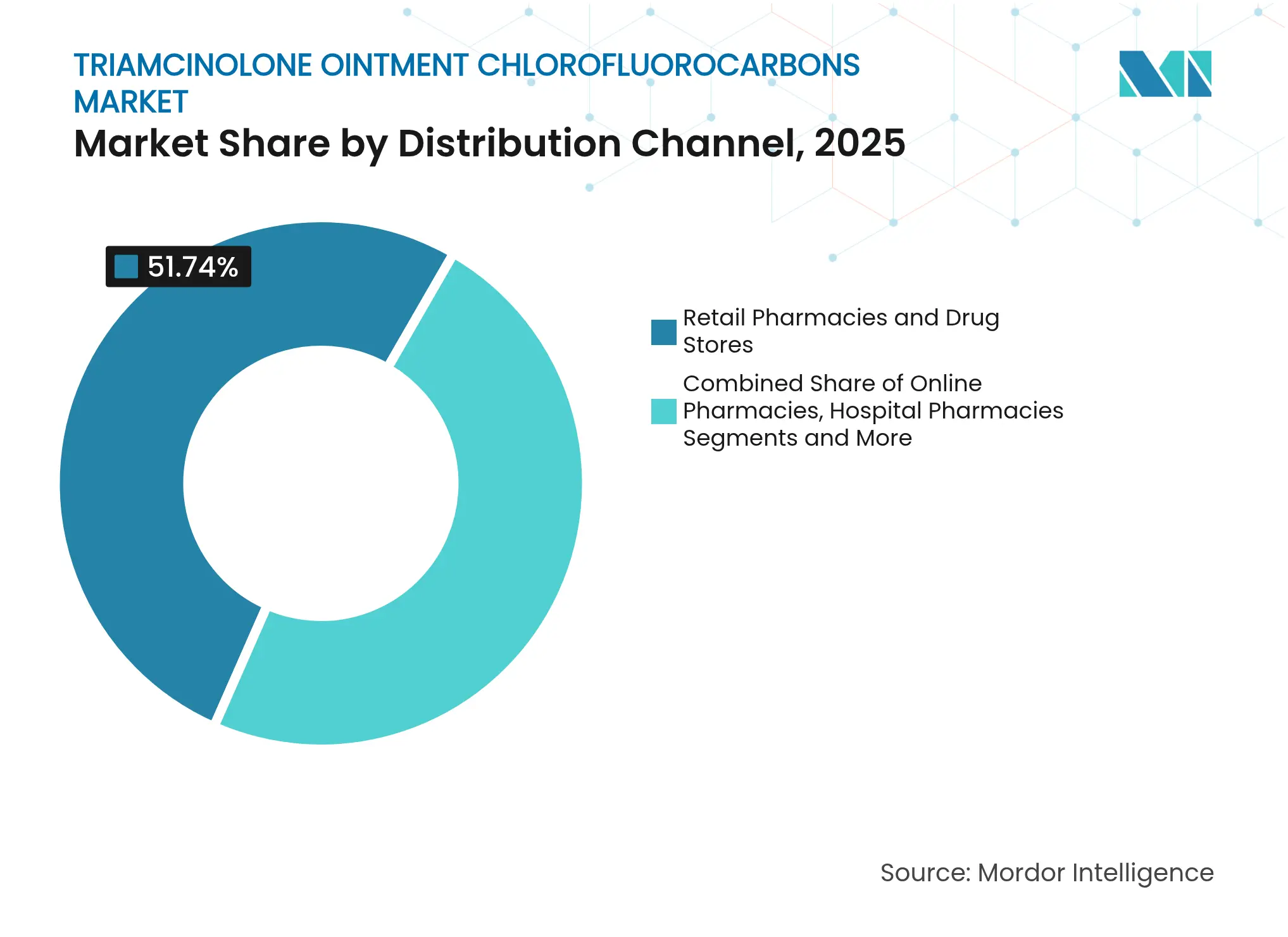

- By distribution channel, retail pharmacies led with 51.74% revenue share in 2025; online pharmacies are forecast to expand at an 7.88% CAGR to 2031.

- By geography, North America maintained 37.35% of the triamcinolone ointment chlorofluorocarbons market size in 2025, while Asia-Pacific exhibited the highest projected CAGR at 6.21% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Triamcinolone Ointment Chlorofluorocarbons Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Prevalence Of Eczema, Dermatitis & Psoriasis

Rising Prevalence Of Eczema, Dermatitis & Psoriasis

| +0.4% | Global, with concentration in North America & Europe | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

+0.4%

| Geographic Relevance:

Global, with concentration in North America & Europe

| Impact Timeline:

Long term (≥ 4 years)

|

Growing Geriatric Population

Growing Geriatric Population

| +0.3% | Global, particularly APAC and North America | Long term (≥ 4 years) | |||

Increasing Awareness Of Early Dermatological Therapy

Increasing Awareness Of Early Dermatological Therapy

| +0.2% | North America & EU, expanding to APAC | Medium term (2-4 years) | |||

Generic Affordability & Price Competitiveness

Generic Affordability & Price Competitiveness

| +0.3% | Global, with emphasis on emerging markets | Short term (≤ 2 years) | |||

Regulatory Exemptions For Essential CFC Uses

Regulatory Exemptions For Essential CFC Uses

| +0.2% | Global, subject to Montreal Protocol compliance | Long term (≥ 4 years) | |||

Expansion Of Online Pharmacy & E-Commerce Channels

Expansion Of Online Pharmacy & E-Commerce Channels

| +0.3% | Global, led by North America and APAC | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Prevalence Of Eczema, Dermatitis & Psoriasis

The escalating burden of inflammatory skin conditions serves as the primary demand catalyst for triamcinolone ointment formulations, with atopic dermatitis representing the highest disability-adjusted life years among dermatological conditions globally. This epidemiological shift reflects urbanization patterns, environmental pollutant exposure, and lifestyle modifications that compromise skin barrier function. The correlation between disease prevalence and Universal Health Coverage indices suggests that improved healthcare access paradoxically increases reported cases, creating sustained demand for established therapeutic options. Dermatological conditions disproportionately affect quality of life metrics, driving patient willingness to utilize specialized formulations despite availability of alternative treatments. The persistence of CFC-containing formulations in treatment protocols reflects their proven clinical efficacy in managing acute inflammatory episodes where rapid symptom resolution takes precedence over environmental considerations.

Growing Geriatric Population

The expanding elderly demographic worldwide creates sustained demand for the triamcinolone ointment chlorofluorocarbons market as aging populations experience higher incidence of dermatological conditions requiring topical corticosteroid interventions. Global burden of atopic dermatitis in elderly populations shows significant upward trends with notable regional disparities. Age-related skin barrier dysfunction increases susceptibility to inflammatory conditions, with reduced epidermal renewal rates and diminished natural moisturizing factors creating favorable conditions for eczema and dermatitis development. Geriatric patients often demonstrate treatment preferences for established pharmaceutical options with proven safety profiles rather than novel therapeutic alternatives with limited long-term safety data. Healthcare provider familiarity with traditional corticosteroid formulations supports continued prescription patterns despite availability of newer treatment modalities. The specialized needs of elderly patients with compromised skin integrity and multiple comorbidities create niche applications where traditional formulations maintain therapeutic relevance.

Increasing Awareness Of Early Dermatological Therapy

Growing recognition of early intervention benefits for inflammatory skin conditions drives expanded utilization of topical corticosteroids as first-line therapeutic options before disease progression necessitates more aggressive treatment modalities. Patient education initiatives emphasize the importance of prompt treatment initiation to prevent chronic inflammation patterns that reduce therapeutic responsiveness. Healthcare provider awareness of disease progression patterns supports prophylactic prescription practices that expand the potential patient population beyond those with severe symptomatic presentations. Digital health platforms facilitate symptom tracking and treatment adherence monitoring, creating opportunities for sustained therapeutic engagement that supports market growth. The triamcinolone ointment chlorofluorocarbons market benefits from established positioning within dermatological treatment algorithms as initial intervention before escalation to immunomodulatory alternatives. Telemedicine expansion enables remote dermatological consultations that increase diagnosis rates and treatment initiation for previously underserved populations with limited specialist access.

Generic Affordability & Price Competitiveness

Generic pharmaceutical pricing dynamics create substantial cost advantages for triamcinolone formulations, particularly in markets where healthcare reimbursement systems favor established therapeutic options over newer biological alternatives. South Korean market analysis demonstrates that increased generic manufacturer participation can reduce pharmaceutical expenditure, though effectiveness depends on pricing scheme structures and market entry sequencing. The tiered pricing model introduced in July 2020 differentiates generic prices based on development efforts and market entry order, creating competitive advantages for established manufacturers with proven bioequivalence profiles. Price variance management becomes critical as the number of generic manufacturers stabilizes, requiring strategic positioning around formulation differentiation rather than pure cost competition. Generic affordability particularly resonates in emerging markets where healthcare budgets prioritize cost-effective treatments with established safety profiles over premium-priced innovative therapies.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Adverse Side-Effects & Steroid-Phobia Among Patients

Adverse Side-Effects & Steroid-Phobia Among Patients

| -0.3% | Global, particularly pronounced in developed markets | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-0.3%

| Geographic Relevance:

Global, particularly pronounced in developed markets

| Impact Timeline:

Medium term (2-4 years)

|

Stringent Potency & Prescription Regulations

Stringent Potency & Prescription Regulations

| -0.2% | Global, with regional variation in enforcement | Long term (≥ 4 years) | |||

Raw-Material Supply-Chain Disruptions (Mineral Oil,

Petrolatum)

Raw-Material Supply-Chain Disruptions (Mineral Oil,

Petrolatum)

| -0.2% | Global, with concentration in Asia-Pacific sourcing | Short term (≤ 2 years) | |||

Uptake Of Steroid-Sparing Biologics & Calcineurin

Inhibitors

Uptake Of Steroid-Sparing Biologics & Calcineurin

Inhibitors

| -0.4% | North America & Europe, expanding globally | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Adverse Side-Effects & Steroid-Phobia Among Patients

Patient apprehension regarding topical corticosteroid use creates significant treatment adherence challenges that constrain market expansion, with steroid phobia particularly pronounced among populations with limited dermatological education. Systemic absorption concerns, including hypothalamic-pituitary-adrenal axis suppression and growth retardation in pediatric populations, drive healthcare provider reluctance to prescribe potent formulations for extended treatment periods. The misuse of topical steroids, particularly in over-the-counter contexts, has created public health concerns that influence regulatory oversight and prescribing patterns. Patient education initiatives emphasizing proper application techniques and treatment duration limitations remain insufficient to overcome deeply rooted safety concerns. The development of selective glucocorticoid receptor agonists represents a strategic response to these concerns, though market penetration remains limited by cost and availability constraints.

Uptake Of Steroid-Sparing Biologics & Calcineurin Inhibitors

Advanced therapeutic alternatives are progressively capturing market share from traditional corticosteroid formulations, with biologics like dupilumab, nemolizumab, and JAK inhibitors demonstrating superior safety profiles for chronic dermatological conditions. Galderma's FDA approval of Nemluvio (nemolizumab) in December 2024 for moderate-to-severe atopic dermatitis, with anticipated peak sales exceeding USD 2 billion by 2027, exemplifies the market shift toward targeted immunomodulatory therapies. These biologics target specific inflammatory pathways, including IL-31 receptor antagonism for itch management, providing mechanistic advantages over broad-spectrum corticosteroid suppression. The European Medicines Agency's recommendations for personalized medicine approaches in atopic dermatitis treatment further accelerate adoption of targeted therapies over traditional formulations. Calcineurin inhibitors offer intermediate positioning between topical steroids and biologics, providing steroid-sparing benefits while maintaining topical application convenience.

Segment Analysis

By Application: Eczema Dominance Drives Therapeutic Positioning

Eczema applications command 40.22% of the triamcinolone ointment chlorofluorocarbons market share in 2025, reflecting the condition's chronic nature and established treatment protocols that favor proven corticosteroid formulations over experimental alternatives. Psoriasis treatments demonstrate the strongest growth trajectory at 6.2% CAGR through 2031, driven by expanding patient populations and improved diagnostic capabilities that identify previously undertreated cases. Dermatitis applications maintain steady demand patterns, while allergic reactions represent episodic usage that creates demand volatility but supports premium pricing for rapid-acting formulations. Other applications, including off-label uses for inflammatory skin conditions, provide market diversification opportunities though regulatory constraints limit promotional activities.

The therapeutic positioning reflects dermatological treatment hierarchies where topical corticosteroids serve as first-line interventions for acute inflammatory episodes, despite availability of newer therapeutic modalities. Eczema's market dominance stems from the condition's requirement for sustained treatment protocols that favor cost-effective, proven formulations over premium-priced alternatives. The aging population's increasing susceptibility to dermatological conditions creates sustained demand for established therapeutic options, particularly in geriatric care settings where treatment simplicity and cost considerations take precedence over innovative delivery mechanisms.

Note: Segment shares of all individual segments available upon report purchase

By Concentration Strength: Mid-Range Potency Balances Efficacy and Safety

The 0.10% concentration strength maintains market leadership with 45.05% of the triamcinolone ointment chlorofluorocarbons market size in 2025, representing the optimal balance between therapeutic efficacy and safety profile considerations that drive prescriber confidence and patient acceptance. Higher potency formulations (0.5% and above) exhibit accelerated growth at 5.44% CAGR, reflecting increasing comfort with potent corticosteroids among specialized dermatological practitioners managing severe inflammatory conditions. Lower concentrations (0.03% and 0.05%) serve pediatric and sensitive-skin populations where safety considerations outweigh maximum efficacy requirements, though growth remains constrained by availability of alternative therapeutic options.

Concentration selection reflects evolving clinical practice patterns where dermatologists increasingly customize potency based on anatomical application sites, patient age demographics, and treatment duration requirements. The FDA's regulatory framework for triamcinolone formulations, including specific concentration approvals for veterinary applications, demonstrates the importance of potency standardization in ensuring therapeutic consistency. Market dynamics favor mid-range concentrations that provide prescriber flexibility while minimizing regulatory complexity and patient safety concerns that constrain higher potency adoption.

By Packaging Type: Traditional Tubes Face Innovation Pressure

Tube packaging dominates with 70.10% of the triamcinolone ointment chlorofluorocarbons market share in 2025, benefiting from established manufacturing infrastructure, cost efficiency, and familiar patient application patterns that support treatment adherence and dosing consistency. Single-use sachets demonstrate the highest growth velocity at 7.21% CAGR, driven by infection control protocols in healthcare settings and precise dosing requirements that minimize waste and contamination risks. Jar packaging serves specialized applications requiring larger volume dispensing, while other packaging innovations focus on tamper-evident features and child-resistant closures that address safety regulatory requirements.

The packaging evolution reflects broader pharmaceutical industry trends toward unit-dose formulations that improve medication safety and reduce cross-contamination risks in clinical environments. Single-use sachets particularly appeal to hospital and long-term care settings where infection control protocols mandate individual patient packaging for topical medications. Manufacturing considerations for CFC-containing formulations require specialized packaging materials that maintain product stability while preventing propellant leakage, creating technical barriers that favor established packaging formats over innovative alternatives. The shift toward sustainable packaging materials creates additional complexity for CFC-containing products where environmental considerations must balance product integrity requirements.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Retail pharmacies and drug stores maintain market leadership with 51.74% of the triamcinolone ointment chlorofluorocarbons market share in 2025, leveraging established patient relationships, insurance processing capabilities, and immediate product availability that support acute treatment needs for dermatological conditions. Online pharmacies exhibit the strongest growth momentum at 7.88% CAGR, reflecting digital transformation trends that prioritize patient convenience, prescription management integration, and direct-to-consumer delivery models. Hospital pharmacies serve specialized patient populations requiring supervised application protocols, while wholesalers and distributors provide bulk supply chain management for institutional customers.

The distribution channel evolution reflects changing patient preferences for pharmaceutical access, with online platforms offering enhanced privacy for dermatological treatments and subscription-based refill management that improves chronic condition adherence. Digital pharmacy platforms provide patient education resources and treatment monitoring capabilities that support sustained therapeutic engagement beyond traditional pharmacy interactions. Regulatory frameworks for online pharmaceutical dispensing continue to evolve, with telemedicine integration creating opportunities for prescription management that bypass traditional healthcare provider visits. The specialized nature of CFC-containing formulations requires distribution partners with appropriate storage and handling capabilities, creating barriers to entry for generic online platforms while favoring established pharmaceutical distributors.

Note: Segment shares of all individual segments available upon report purchase

By Patient Age Group: Adult Dominance Reflects Chronic Disease Patterns

Adult patients represent 57.15% of the triamcinolone ointment chlorofluorocarbons market size in 2025, reflecting the peak incidence of chronic dermatological conditions during working-age years when occupational exposures, stress factors, and lifestyle modifications contribute to inflammatory skin conditions. Pediatric applications demonstrate accelerated growth at 7.18% CAGR, driven by specialized formulation requirements for younger demographics and increasing parental awareness of early dermatological intervention benefits. Geriatric populations require customized treatment approaches that consider comorbidity interactions and medication adherence challenges, though market growth remains constrained by safety concerns regarding systemic absorption in elderly patients.

Age-specific market dynamics reflect dermatological disease patterns where chronic conditions like eczema and dermatitis typically manifest during childhood and persist through adulthood, creating sustained demand for established therapeutic options. Pediatric growth acceleration stems from improved diagnostic capabilities and reduced steroid phobia among healthcare providers who recognize the importance of early intervention in preventing disease progression. The geriatric segment requires specialized consideration of skin barrier function changes, medication absorption patterns, and polypharmacy interactions that influence treatment selection and dosing protocols.

Geography Analysis

North America commands 37.35% of the triamcinolone ointment chlorofluorocarbons market share in 2025, supported by established regulatory frameworks for CFC-containing medical products under Montreal Protocol exemptions and robust dermatological treatment infrastructure that facilitates specialized formulation access. The region's market leadership reflects comprehensive healthcare coverage systems that reimburse proven therapeutic options, extensive generic pharmaceutical manufacturing capabilities, and clinical practice patterns that favor established treatment protocols over experimental alternatives. Regulatory clarity regarding essential use exemptions provides market stability for CFC-containing formulations while maintaining environmental compliance obligations. The United States Environmental Protection Agency's continued oversight of ozone-depleting substances ensures market access for essential medical applications while incentivizing innovation in alternative delivery systems.

Asia-Pacific emerges as the fastest-growing region at 6.21% CAGR through 2031, propelled by expanding healthcare access, rising dermatological disease burden among aging populations, and increasing adoption of Western treatment protocols for inflammatory skin conditions. The region's growth trajectory reflects improving healthcare infrastructure, expanding insurance coverage systems, and growing awareness of dermatological treatment options among previously underserved populations. China's Anti-Espionage Law implementation creates supply chain uncertainties for pharmaceutical raw materials, potentially disrupting active pharmaceutical ingredient sourcing and quality verification processes. Manufacturing localization efforts in India and Southeast Asia provide alternative sourcing options while regulatory harmonization initiatives facilitate market access for established formulations.

Europe maintains steady market positioning through comprehensive regulatory frameworks that balance environmental protection mandates with essential medical use exemptions, creating predictable market conditions for specialized pharmaceutical formulations. The European Union's Regulation 2024/590 addresses ozone-depleting substance production and use while maintaining specific exemptions for essential medical applications, providing regulatory clarity for market participants. Regional healthcare systems prioritize cost-effective treatments with proven safety profiles, supporting continued utilization of established corticosteroid formulations despite availability of newer therapeutic alternatives. The region's emphasis on environmental sustainability creates ongoing pressure for formulation innovation while maintaining treatment access for patients requiring specialized delivery systems.

Competitive Landscape

Market Concentration

The triamcinolone ointment chlorofluorocarbons market exhibits moderate fragmentation with established generic pharmaceutical manufacturers leveraging cost advantages and regulatory compliance expertise to maintain market positioning against specialty pharmaceutical companies pursuing formulation innovations and niche therapeutic applications. Competition intensity remains constrained by regulatory barriers for CFC-containing formulations, specialized manufacturing requirements, and limited market size that discourages new entrant investment in production capabilities. Generic manufacturers focus on bioequivalence demonstration and cost optimization strategies, while branded pharmaceutical companies emphasize clinical differentiation through concentration variations, packaging innovations, and combination formulations that address specific patient populations.

Strategic positioning reflects the dual pressures of environmental sustainability mandates and clinical efficacy requirements, creating opportunities for companies that can navigate both regulatory compliance and therapeutic innovation challenges. White-space opportunities exist in pediatric formulations, geriatric-specific concentrations, and combination therapies that address multiple dermatological conditions simultaneously. Technology adoption focuses on manufacturing process optimization, quality control enhancement, and supply chain diversification rather than breakthrough therapeutic innovations, reflecting the mature nature of corticosteroid pharmacology and regulatory constraints on formulation modifications.

The competitive environment for the triamcinolone ointment chlorofluorocarbons market increasingly emphasizes regulatory expertise and compliance capabilities as differentiating factors, with successful market participants demonstrating proficiency in navigating complex environmental regulations while maintaining product quality standards. Strategic partnerships between generic manufacturers and specialized pharmaceutical companies create synergistic opportunities that combine cost-efficient production capabilities with innovative formulation technologies. Market consolidation remains limited by the specialized nature of CFC-containing pharmaceutical production, creating stability for established manufacturers with proven regulatory compliance records. The competitive landscape evolution reflects the tension between environmental sustainability imperatives and clinical efficacy requirements, with successful companies balancing both considerations in product development and marketing strategies.

Triamcinolone Ointment Chlorofluorocarbons Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: At the Dermatology Education Foundation (DERM) 2025 NP/PA CME Conference, Linda Stein Gold, MD, of the Henry Ford Health System, stated that they use triamcinolone topical for maintenance therapy of psoriasis.

- January 2024: A study published in Journal of Burn Care & Research found that a novel 50/50 mixture of triamcinolone and Polysporin topical ointment is an effective and safe treatment for hypergranulation tissue in burn wounds.

Table of Contents for Triamcinolone Ointment Chlorofluorocarbons Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Prevalence Of Eczema, Dermatitis & Psoriasis

- 4.2.2Growing Geriatric Population

- 4.2.3Increasing Awareness Of Early Dermatological Therapy

- 4.2.4Generic Affordability & Price Competitiveness

- 4.2.5Regulatory Exemptions For Essential CFC Uses

- 4.2.6Expansion Of Online Pharmacy & E-Commerce Channels

- 4.3Market Restraints

- 4.3.1Adverse Side-Effects & Steroid-Phobia Among Patients

- 4.3.2Stringent Potency & Prescription Regulations

- 4.3.3Raw-Material Supply-Chain Disruptions (Mineral Oil, Petrolatum)

- 4.3.4Uptake Of Steroid-Sparing Biologics & Calcineurin Inhibitors

- 4.4Porter's Five Forces

- 4.4.1Threat of New Entrants

- 4.4.2Bargaining Power of Buyers

- 4.4.3Bargaining Power of Suppliers

- 4.4.4Threat of Substitutes

- 4.4.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Application

- 5.1.1Eczema

- 5.1.2Dermatitis

- 5.1.3Allergies

- 5.1.4Psoriasis

- 5.1.5Other Applications

- 5.2By Concentration Strength

- 5.2.10.03%

- 5.2.20.05%

- 5.2.30.10%

- 5.2.40.5 % & Above

- 5.3By Packaging Type

- 5.3.1Tube

- 5.3.2Jar

- 5.3.3Single-use Sachet

- 5.3.4Other Packaging

- 5.4By Distribution Channel

- 5.4.1Hospital Pharmacies

- 5.4.2Retail Pharmacies & Drug Stores

- 5.4.3Online Pharmacies

- 5.4.4Wholesalers & Distributors

- 5.5By Patient Age Group

- 5.5.1Pediatric

- 5.5.2Adult

- 5.5.3Geriatric

- 5.6Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Mexico

- 5.6.2Europe

- 5.6.2.1Germany

- 5.6.2.2United Kingdom

- 5.6.2.3France

- 5.6.2.4Italy

- 5.6.2.5Spain

- 5.6.2.6Rest of Europe

- 5.6.3Asia-Pacific

- 5.6.3.1China

- 5.6.3.2Japan

- 5.6.3.3India

- 5.6.3.4South Korea

- 5.6.3.5Australia

- 5.6.3.6Rest of Asia-Pacific

- 5.6.4Middle East and Africa

- 5.6.4.1GCC

- 5.6.4.2South Africa

- 5.6.4.3Rest of Middle East and Africa

- 5.6.5South America

- 5.6.5.1Brazil

- 5.6.5.2Argentina

- 5.6.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Akorn Inc.

- 6.3.2Bristol Myers Squibb Company

- 6.3.3Cosette Pharmaceuticals Inc.

- 6.3.4Glenmark Pharmaceuticals Ltd.

- 6.3.5Lupin Limited

- 6.3.6Viatris Inc

- 6.3.7Novartis International AG

- 6.3.8Sun Pharmaceutical Industries Limited

- 6.3.9Taro Pharmaceutical Industries Ltd.

- 6.3.10Padagis US LLC

- 6.3.11Sandoz AG

- 6.3.12Teva Pharmaceutical Industries Ltd.

- 6.3.13Astellas Pharma Inc.

- 6.3.14Northstar Rx LLC

- 6.3.15Macleods Pharmaceuticals Ltd.

- 6.3.16Perrigo Company plc

- 6.3.17Glenmark Pharmaceuticals Inc., USA

- 6.3.18Fera Pharmaceuticals, LLC

- 6.3.19Apotex Inc.

- 6.3.20Hikma Pharmaceuticals PLC

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Triamcinolone Ointment Chlorofluorocarbons Market Report Scope

Triamcinolone ointment is used to attenuate the actions of chemicals substances in the body that cause redness, inflammation, and swelling.