Basal Cell Carcinoma Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

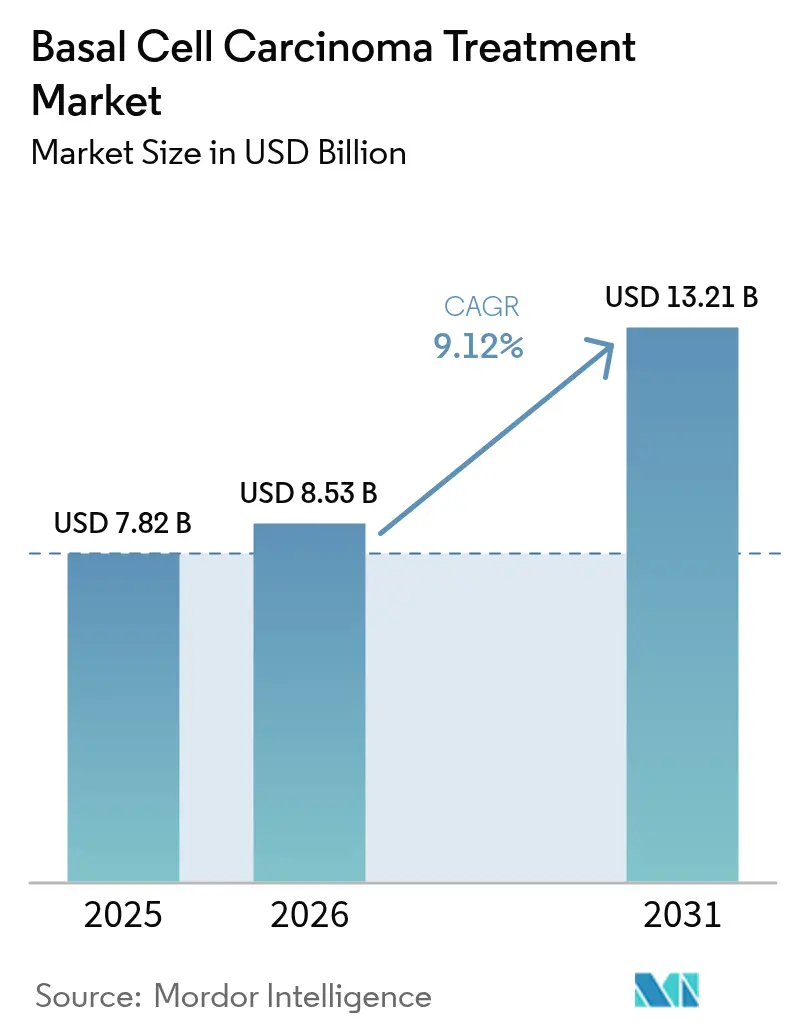

| Market Size (2026) | USD 8.53 Billion |

| Market Size (2031) | USD 13.21 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

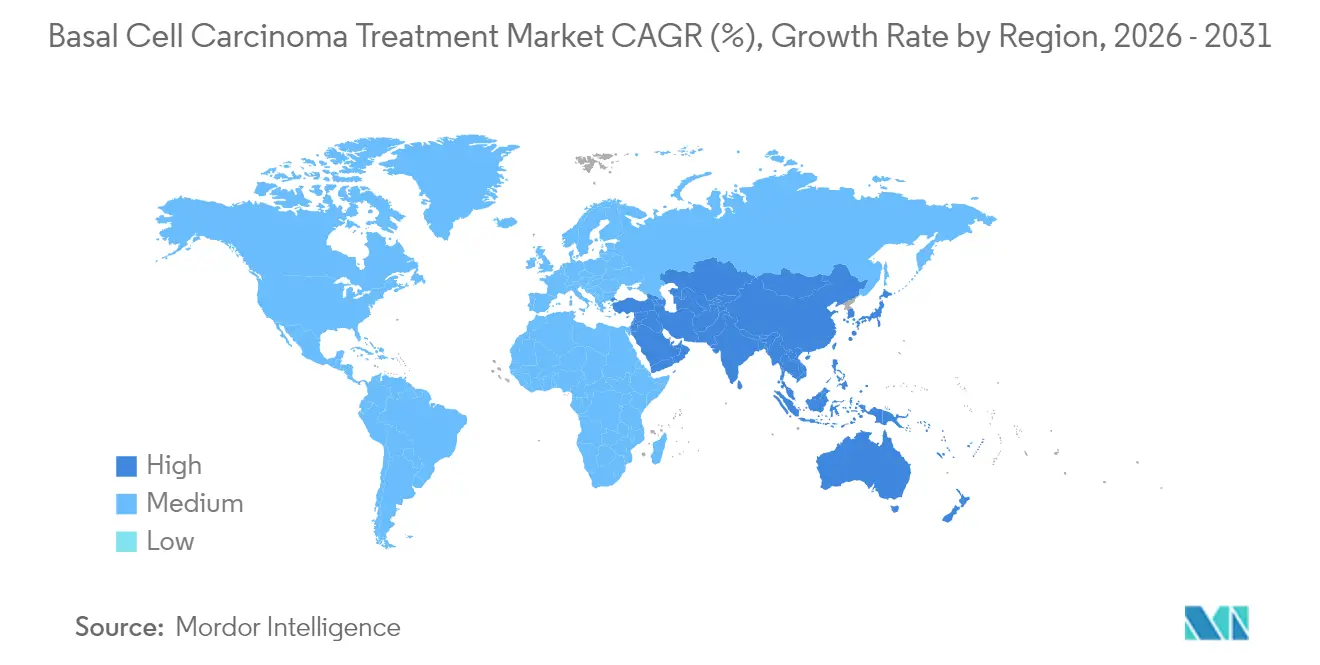

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Basal Cell Carcinoma Treatment Market Analysis by Mordor Intelligence

Basal cell carcinoma treatment market size in 2026 is estimated at USD 8.53 billion, growing from 2025 value of USD 7.82 billion with 2031 projections showing USD 13.21 billion, growing at 9.12% CAGR over 2026-2031. Strong growth reflects the convergence of rising global skin-cancer incidence, the shift toward minimally invasive therapies, and broader access to specialty dermatology services across emerging economies. Momentum is amplified by an aging population that has accumulated decades of ultraviolet exposure and by environmental changes that have intensified average UV radiation. Surgical excision remains the standard of care, yet photodynamic therapy is scaling rapidly as non-invasive devices and topical photosensitizers gain commercial traction. AI-driven dermoscopy and FDA-cleared diagnostic devices are shortening detection-to-treatment intervals, which in turn supports earlier-stage interventions. North America sustains leadership through mature reimbursement systems, while Asia-Pacific posts the fastest growth on the back of surging incidence in Korea and Japan.

Key Report Takeaways

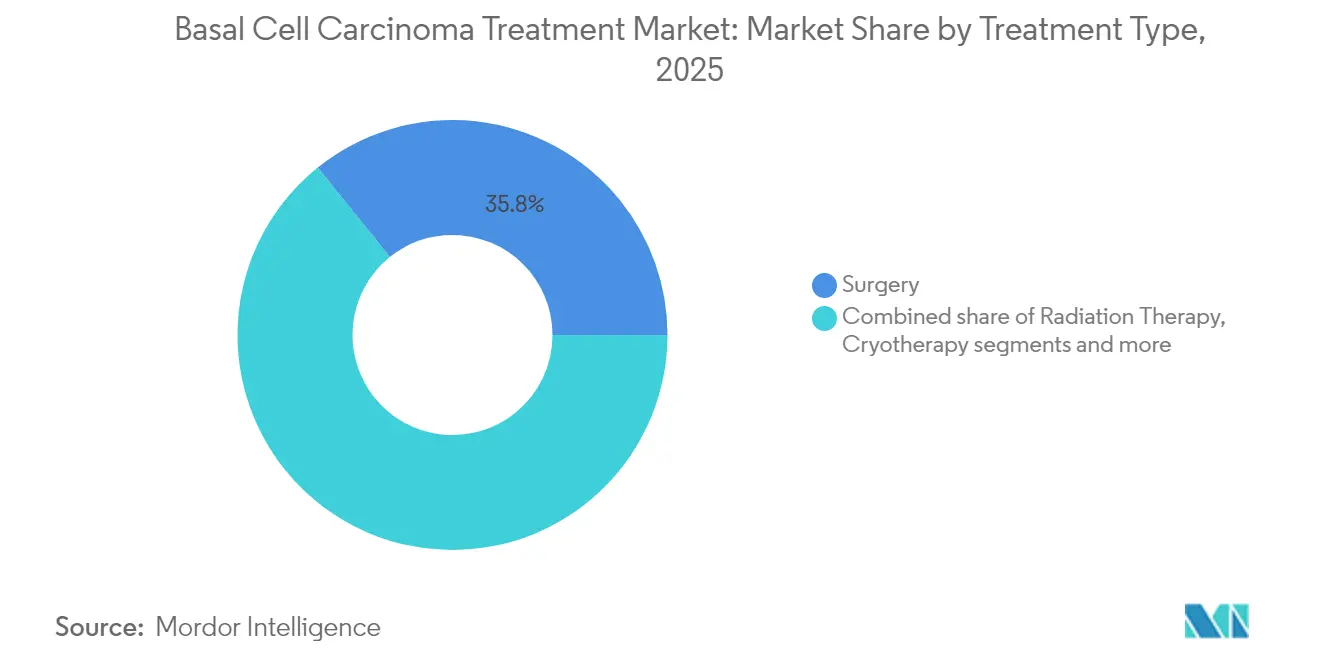

- By treatment type, surgery led with 35.78% of the basal cell carcinoma treatment market share in 2025; photodynamic therapy is projected to expand at an 10.74% CAGR through 2031.

- By disease stage, nodular presentations accounted for 64.41% of diagnosed cases in 2025, whereas metastatic disease is forecast to advance at a 9.88% CAGR to 2031.

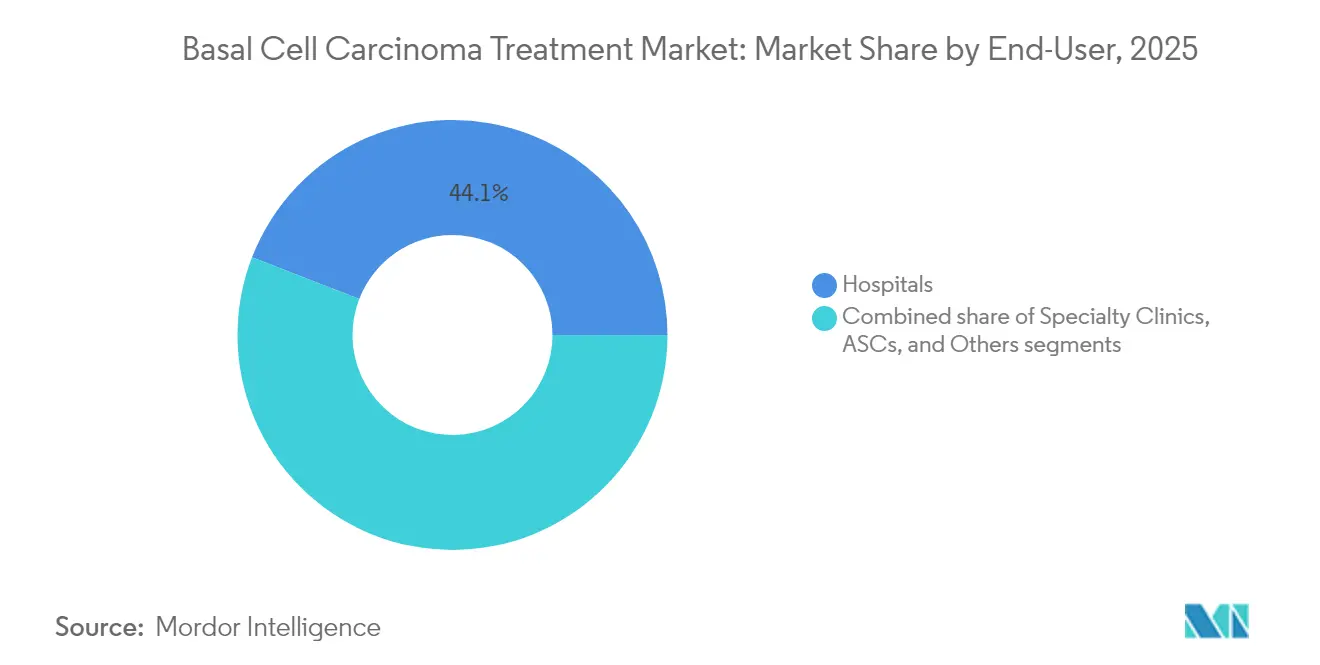

- By end-user, hospitals held 44.12% demand in 2025; specialty clinics are set to grow the fastest at a 9.72% CAGR.

- By geography, North America captured 43.05% revenue share in 2025, while Asia-Pacific is expected to post a 10.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Basal Cell Carcinoma Treatment Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of skin cancers | +2.1% | Global; strongest in APAC and MEA | Long term (≥ 4 years) |

| Aging population with higher cumulative UV | +1.8% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| AI-driven dermoscopy for earlier detection | +1.6% | North America and EU cores, APAC urban centers | Short term (≤ 2 years) |

| Environmental changes raising UV radiation | +1.4% | Global; acute in high-altitude regions | Long term (≥ 4 years) |

| Label expansions of hedgehog-pathway drugs | +1.2% | North America and EU, spillover to APAC | Medium term (2-4 years) |

| Workplace sun-safety legislation | +0.9% | EU and Australia, emerging in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of skin cancers

Global basal cell carcinoma incidence reached 4.4 million new cases in 2021, equal to an age-standardized rate of 51.71 per 100,000. Enhanced dermatology coverage and image-based triage in primary care expose historically hidden caseloads in underserved regions. Climate-model forecasts show that every 1% depletion of ozone could elevate basal cell carcinoma incidence by 2.7%, while a 2 °C temperature rise could add 11% more cases by 2050[1]Bundesamt für Strahlenschutz, “Climate Change and the Risk of UV-Related Diseases,” bfs.de . Japan illustrates demographic acceleration, with individuals aged ≥ 90 now comprising 17% of diagnoses. Occupational exposure remains high among outdoor workers[2]Yoon-Soo Lee, “Occupational Risk Factors for Skin Cancer: A Review,” Journal of Korean Medical Science, jkms.org , prompting employers to invest in UV-protective gear and routine screenings.

Aging population with higher cumulative UV exposure

The share of patients older than 70 increased from 44% to 74% in Japanese cancer registries between 1989 and 2021. DNA damage due to thymine-dimer formation accumulates across decades, making geriatric cohorts especially susceptible. Healthcare systems have responded by adding geriatric dermatology divisions and lowering screening thresholds for senior citizens, which fosters earlier-stage identification and improves cost-effectiveness.

AI-driven dermoscopy enabling earlier detection & treatment

Stanford researchers documented 81.1% sensitivity and 86.1% specificity when clinicians used AI support, versus 75% and 81.5%, respectively, without it. The FDA’s clearance of DermaSensor allows 300,000 US primary-care physicians to conduct quantitative point-of-care scans for all common skin cancers. South Korea approved canofyMD SCAI with 80.9% accuracy, underscoring global regulatory acceptance. Earlier detection funnels more patients into curative resections and short-course topical regimens, easing the economic burden of advanced-stage management.

Environmental changes increasing average UV radiation

Mid-latitude UV-B irradiance has risen since 1980 as stratospheric ozone thinned, despite the partial success of the Montreal Protocol. Germany’s national climate-risk study now classifies heightened UV as a priority health threat, prompting public-awareness campaigns and real-time UV-index dashboards. Alpine zones in Italy report “extreme” UV indices on summer days, reinforcing the need for high-SPF formulations and scheduling guidelines for outdoor work.

Restraints Impact Analysis of Basal Cell Carcinoma Treatment Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced drug therapies | -1.9% | Global; acute in emerging markets | Medium term (2-4 years) |

| Under-diagnosis in primary-care settings | -1.3% | APAC and MEA; rural pockets in North America | Long term (≥ 4 years) |

| Reimbursement hurdles for checkpoint combos | -1.1% | Global; intensity varies by payer model | Medium term (2-4 years) |

| Hedgehog-inhibitor toxicity concerns | -0.8% | North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High cost of advanced drug therapies & surgeries

Vismodegib and cemiplimab list at USD 13,000 and USD 10,000 per month, respectively, placing them out of reach for many self-pay patients. Mohs micrographic surgery costs 120-370% more than standard excision, even though five-year cure rates exceed 98%. Average per-patient spending rose from USD 1,000 in 2006 to USD 1,600 in 2011 and continues to climb. Market entry lags can span up to seven years in lower-income economies, evidencing affordability and regulatory challenges. Patch-based approaches such as SkinJect target a USD 1,000 price point, aiming to close the affordability gap.

Under-diagnosis in primary-care settings

A Thai review found 53 basal cell carcinomas initially mistaken for benign nevi, spotlighting skill gaps outside dermatology. AI triage lifts novice diagnostic sensitivity by roughly 13 points, yet rural sites still contend with bandwidth limits for teledermatology. Insurance authorization layers further delay specialist referrals, contributing to later-stage presentations that require costlier systemic therapy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Basal Cell Carcinoma Treatment Market Segment Analysis

By Treatment Type:

Surgery dominates while non-invasive alternatives accelerateSurgical techniques accounted for 35.78% of the basal cell carcinoma treatment market size in 2025, underscoring clinician confidence in wide excision and Mohs micrographic protocols. Mohs utilization expanded 700% from 1992 to 2009, yet premium costs have triggered payer scrutiny. Radiation therapy records 80-92% local-control rates for patients unsuitable for surgery. Photodynamic therapy is the fastest-growing modality at an 10.74% CAGR, buoyed by short healing times and cosmetic advantages. Combination topical regimens—5-fluorouracil plus calcipotriene—now achieve clearance within seven-to-14 days compared with four-week monotherapy. Hedgehog-pathway inhibitors and checkpoint antibodies extend life in advanced cases: cemiplimab delivers 29% objective responses in locally advanced and 21% in metastatic cohorts. Novel oncolytic peptides such as VP-315 yielded 97% overall response and 51% complete histologic clearance in Phase 2, indicating a disruptive non-surgical future.

Second-generation delivery platforms and AI-guided lesion mapping complement these therapeutic shifts. Optical coherence tomography reaches 95.5% accuracy at lesion centers, allowing surgeons to limit excision margins and preserve healthy tissue. Such precision reduces operative stages, accelerating patient throughput and lessening facility costs. As technology penetrates outpatient centers, the basal cell carcinoma treatment market size for photodynamic and topical agents is projected to expand proportionally.

By Disease Stage:

Nodular drives volume, metastatic fuels value growthNodular disease comprised 64.41% of the basal cell carcinoma treatment market share in 2025, reflecting its common presentation on sun-exposed head and neck areas, where 80% of tumors localize. The segment benefits from high detection rates and straightforward excision protocols, making it the workhorse volume contributor to the basal cell carcinoma treatment market. Superficial variants show unique anatomical clustering, accounting for 25.8% of scalp lesions but only 9.6% on the face. Infiltrative subtypes require wider margins and multifunctional imaging, raising resource intensity.

Metastatic basal cell carcinoma remains rare yet posted the highest growth trajectory at a 9.88% CAGR through 2031, thanks to better imaging and systemic therapy options. The basal cell carcinoma treatment market size for immuno-oncology agents is expanding as cemiplimab secured breakthrough therapy status and avelumab-cetuximab combinations prolong progression-free survival. Preclinical astatine-211-labeled peptides illustrate next-generation tactics for refractory lesions. Early-stage identification and adjuvant applications promise to move some biologics up the treatment ladder, diversifying revenue sources beyond salvage settings.

By End-User:

Hospitals anchor care while specialty clinics surgeHospitals accounted for 44.12% of the basal cell carcinoma treatment market size in 2025, owing to multidisciplinary capacity for complex reconstructions and systemic immunotherapies. Nonetheless, specialty clinics are growing at 9.72% CAGR, capturing patients seeking condensed wait times and dermatology-only expertise. Ambulatory surgical centers leverage lower overhead to offer Mohs and simple excisions at price points 20-30% below hospital charges.

AI tools elevate clinic competitiveness. DermaSensor’s real-time spectroscopy logs a 68% drop in missed cancers by general practitioners, allowing clinics to triage efficiently. Clinics also pioneer photodynamic therapy, achieving 90.9% clearance for actinic keratosis, a common precursor lesion. Teledermatology plus AI platforms such as Helfie extend specialty care into remote districts, broadening the basal cell carcinoma treatment market footprint for outpatient centers.

Geography Analysis

North America Basal Cell Carcinoma Treatment Market

North America controls 43.05% of the basal cell carcinoma treatment market revenue in 2025 and is positioned for an 8.52% CAGR to 2031. Cutting-edge diagnostics such as FDA-approved DermaSensor widen primary-care capabilities, but high-deductible health plans temper therapy uptake as Mohs costs remain 120-370% above standard excision. Regulatory agility benefits innovators, evidenced by breakthrough designations for cemiplimab and cosibelimab, yet supply-chain fragilities surfaced via EFUDEX shortages from December 2024 to July 2025.

APAC Basal Cell Carcinoma Treatment Market

Asia-Pacific is the basal cell carcinoma treatment market’s fastest-growing region at 10.01% CAGR. Korea saw cases climb seven-fold from 1999 to 2019, with basal cell carcinoma soaring from 488 to 3,908 diagnoses. Regulatory bodies green-lit canofyMD SCAI AI software at 80.9% accuracy, underscoring tech-forward adoption. Japan’s registries show patients aged ≥ 90 now represent 17% of cases, spotlighting demographic pressure. Differences in histological subtypes mandate region-specific guidelines, as superficial lesions are less frequent than in Western cohorts.

EMEA and South America Basal Cell Carcinoma Treatment Market

Europe advances at 8.83% CAGR fueled by universal coverage and strict UV-exposure policies. The European Commission approved cemiplimab as the first immunotherapy for advanced basal cell carcinoma, showcasing a receptive regulatory landscape. Photodynamic therapy trials with BF-200 ALA register 90.9% clearance, reinforcing Europe’s lead in cosmetically sensitive treatments. Middle East and Africa progress at 9.56% CAGR, catalyzed by expanding private healthcare and governmental trial approvals. The UAE authorized Medicus Pharma’s SkinJect microneedle patch trials in May 2025, marking a shift toward local clinical research capacity. Yet rural dermatology access remains sparse, pressing teledermatology platforms into service. South America grows at 9.21% but faces reimbursement hurdles for newer biologics, paving the way for cost-effective generics and remote screening pilots.

Competitive Landscape

The basal cell carcinoma treatment market shows moderate fragmentation as legacy drug makers and emerging tech firms vie for share. Regeneron/Sanofi’s cemiplimab anchors the systemic segment, supported by 2025 C-POST data indicating a 68% drop in post-surgical recurrence. Roche, Sun Pharmaceutical, and Viatris leverage deep dermatology portfolios, but smaller actors enable disruptive growth. Verrica’s VP-315 oncolytic peptide achieved 97% overall responses in Phase 2, positioning as a first-line non-surgical contender. Medicus Pharma’s SkinJect patch eyes a USD 1,000 price, undercutting Mohs fees and appealing to self-pay markets.

Capital inflows tilt toward AI diagnostics: DermaSensor secured USD 44.7 million across five rounds, most recently USD 8.93 million in November 2024. M&A activity signals convergence between screening and therapy, exemplified by Longevity Health’s USD 99 million merger with 20/20 BioLabs to bundle AI detection with skincare regimens. Competitive advantage increasingly hinges on integrating AI, real-time imaging, and drug-device combos that shorten care pathways.

Regulatory and reimbursement strategies shape differentiation. Companies widening hedgehog-inhibitor labels or filing for adjuvant positions can tap earlier-stage populations, while those pursuing cost-effective topical or patch formats court emerging-market volumes. Intellectual-property cliffs for first-generation small-molecule inhibitors open doors for biosimilar entrants, raising the prospect of price competition by 2030.

Basal Cell Carcinoma Treatment Industry Leaders

Bausch Health Companies Inc.

F. Hoffmann-La Roche AG

Sanofi S.A.

Sun Pharmaceutical Industries Ltd

Viatris Inc.

- *Disclaimer: Major Players sorted in no particular order

Basal Cell Carcinoma Treatment Market Companies Covered in this Report

- Abbvie

- Bausch Health

- BridgeBio Pharma Inc

- Bristol-Myers Squibb

- Castle Biosciences Inc.

- Eisai

- Roche

- Galderma

- Leo Pharma

- Medicus Pharma Ltd

- Medivir

- Merck

- Novartis

- Perrigo Company

- Pfizer

- Regeneron Pharmaceuticals

- Regeneron Pharmaceuticals

- Sanofi

- Sun Pharmaceuticals Industries

- Taro Pharmaceutical Industries

- Verrica Pharmaceuticals Inc.

- Viatris

Recent Industry Developments in Basal Cell Carcinoma Treatment Market

- May 2025: Medicus Pharma secured UAE Health Department approval to initiate clinical trials of the SkinJect microneedle patch for basal cell carcinoma.

- January 2025: Regeneron reported Phase 3 C-POST data showing cemiplimab cut recurrence risk by 68% in high-risk cutaneous squamous cell carcinoma; FDA filing planned in 2025.

- December 2024: FDA approved cosibelimab (Unloxcyt), a PD-L1 antibody delivering 47% objective responses in advanced cutaneous squamous cell carcinoma.

- January 2024: DermaSensor gained FDA clearance for its real-time spectroscopy device, enabling 300,000 US primary-care physicians to offer point-of-care skin-cancer testing.

Basal Cell Carcinoma Treatment Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the basal cell carcinoma (BCC) treatment market as the value generated when surgical, radiation, topical, photodynamic, cryo-ablation, and systemic pharmacologic therapies are delivered for histologically confirmed BCC across all care settings. We estimate the market at USD 7.82 billion in 2025, covering direct procedure and drug revenues while avoiding any double counting of ancillary dermatology services.

Scope Exclusions: Purely aesthetic skin resurfacing procedures that do not remove or suppress malignant cells are excluded.

Segments Covered in This Report

- By Treatment Type

- Surgery

- Surgical Excision

- Mohs Micrographic Surgery

- Electrodesiccation and Curettage (ED&C)

- Radiation Therapy

- Photodynamic Therapy

- Cryotherapy

- Topical Chemotherapy

- 5-fluorouracil (5-FU)

- Tirbanibulin

- Imiquimod

- Oral Medications

- Intravenous Medications

- Surgery

- By Disease Stage

- Superficial

- Nodular

- Infiltrative

- Metastatic

- By End-User

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Structured interviews with oncologists, dermatologic surgeons, hospital procurement heads, and reimbursement advisors across North America, Europe, Asia-Pacific, and Latin America enabled us to validate treatment mix shifts, ascertain real-world drug pricing, and refine incidence-to-treatment conversion factors. Follow-up surveys with payers clarified reimbursement ceilings and likely adoption timelines for new hedgehog inhibitors, bridging gaps left by desk work.

Desk Research

Mordor analysts first mapped the patient pool through open data from sources such as the National Cancer Institute SEER registry, the World Health Organization cancer factsheets, the American Academy of Dermatology prevalence briefs, and country-level population projections from the UN. Government tariff schedules, Medicare Part B payment files, and peer-reviewed journals on Mohs efficacy then helped us benchmark average procedure costs.

We enriched those baselines with commercial insights drawn from D&B Hoovers company filings, Dow Jones Factiva news flows, Questel patent trends on hedgehog pathway inhibitors, and Volza shipment logs showing topical 5-FU export volumes. Other secondary inputs, such as hospital statistics, clinician society white papers, and reputable press articles, completed the fact base. This list is illustrative; many further references supported data capture and verification.

Market-Sizing & Forecasting

We applied a top-down incidence and treatment penetration model that starts with country-specific BCC case counts and then flows through stage distribution, treatment modality shares, and average service prices. Select bottom-up spot checks, such as provider roll-ups and sampled ASP x volume for key drugs, tested and calibrated totals. Core variables include annual incidence growth, Mohs surgery utilization, radiation session rates, hedgehog inhibitor uptake, and average cost per outpatient excision. A multivariate regression against UV index trends, aging population ratios, and payer reimbursement caps projects demand to 2030, while scenario analysis stresses reimbursement or technology shocks. Any data gaps, such as under-reported outpatient volumes, were bridged using regional analogs validated with expert feedback.

Data Validation & Update Cycle

Outputs run through variance screens versus historical spending, cross-country ratios, and epidemiological norms. Senior reviewers question anomalies, and we re-contact experts when deviations exceed set triggers. Reports refresh each year, with interim revisions issued after major regulatory approvals or coding changes, ensuring clients receive current, quality-checked numbers.

How Mordor Intelligence's Basal Cell Carcinoma Treatment Market Size Compares to Other Published Estimates

Published market values often diverge because firms anchor on different scopes, base years, and price assumptions. Our disciplined inclusion of both procedure and drug spends, coupled with an annual refresh, narrows that gap. Key drivers of variance include geography coverage, treatment catalog breadth, and the method chosen to inflate historical hospital charges to current dollars.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.82 B (2025) | Mordor Intelligence | - |

| USD 3.27 B (2024) | Regional Consultancy A | Counts only product sales, omits surgical fees |

| USD 3.33 B (2024) | Global Consultancy B | Focuses on North America and Europe, excludes Asia incidence |

| USD 5.56 B (2023) | Industry Association C | Uses historical hospital charge data without incidence uplift |

The comparison shows how narrower scopes or outdated incidence multipliers compress totals, whereas Mordor's blended service and drug view, refreshed to the latest epidemiology, delivers a balanced, transparent baseline that decision-makers can replicate with clear variables and repeatable steps.

Key Questions Answered in the Report

What factors are pushing healthcare providers to adopt photodynamic therapy for basal cell carcinoma?

Clinicians favor photodynamic therapy because it leaves minimal scarring, can be delivered in outpatient settings, and pairs well with imaging systems that verify lesion clearance in real time.

Why is the introduction of AI-powered dermoscopy viewed as a game-changer for early detection?

Automated image analysis helps primary-care physicians differentiate malignant from benign lesions more reliably, which reduces unnecessary referrals and speeds patients with suspicious lesions into definitive treatment.

How are environmental changes influencing demand for basal cell carcinoma interventions?

Rising UV radiation in mid-latitude regions and longer outdoor recreation seasons have increased the at-risk population, prompting governments to expand screening campaigns and encourage UV-protective workplace practices.

In what way are geriatric demographics reshaping therapeutic priorities?

As a larger share of diagnoses now occurs in people over 70, health systems are expanding low-impact, non-surgical options and developing guidelines that minimize treatment-related morbidity in elderly patients.

What drives the competitive focus on microneedle patches and topical delivery technologies?

These formats promise shorter recovery times, lower facility costs, and easier access in low-resource settings, making them attractive alternatives to complex surgical or infusion-based regimens.

How are reimbursement policies affecting the uptake of immune checkpoint inhibitors?

Payers often require evidence of failure on earlier therapies before covering newer biologics, leading clinicians to weigh the clinical benefits of early immunotherapy against potential delays from prior-authorization hurdles.

Page last updated on: