3D Sensing And Imaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.98 Billion |

| Market Size (2031) | USD 28.65 Billion |

| Growth Rate (2026 - 2031) | 13.84% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

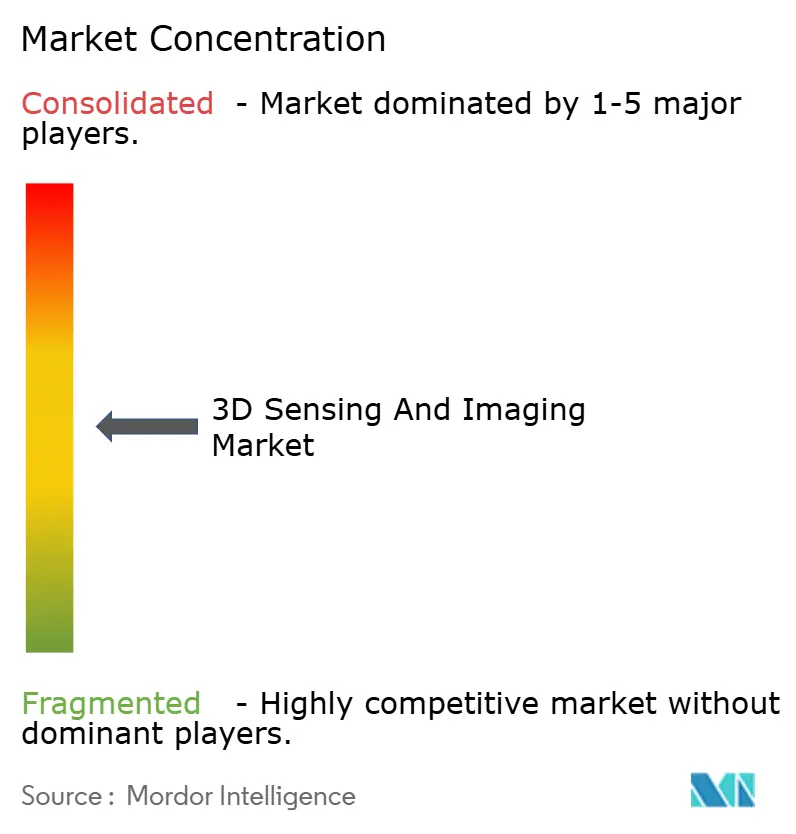

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

3D Sensing And Imaging Market Analysis by Mordor Intelligence

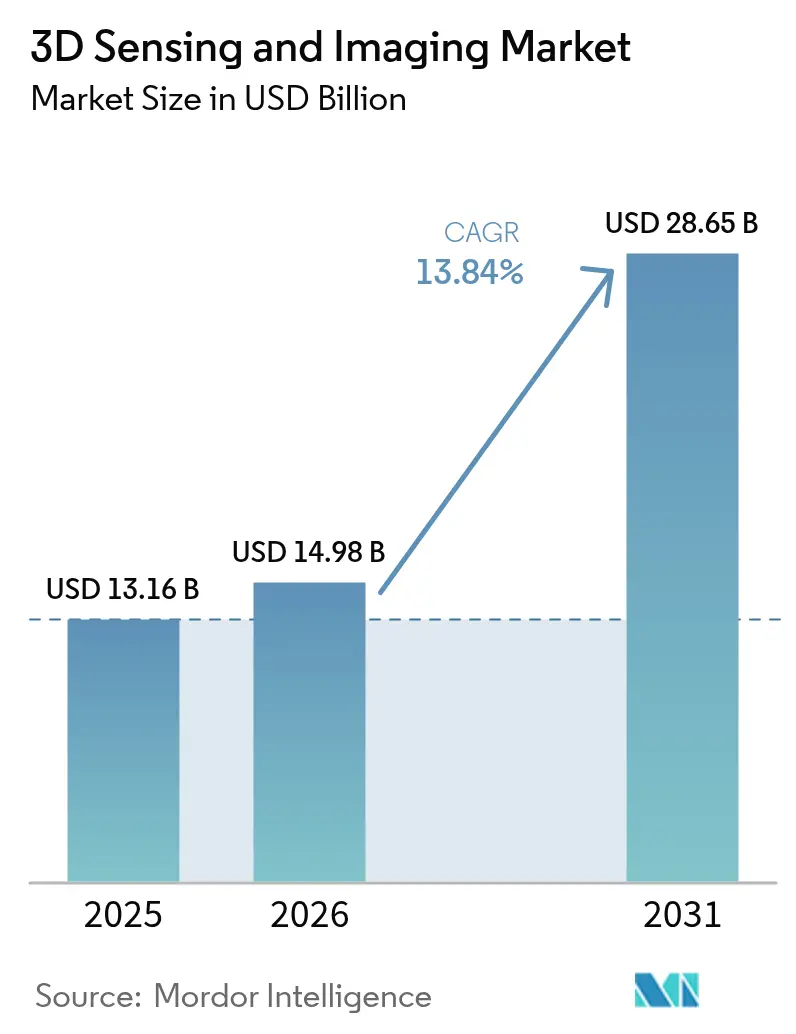

The 3D sensing and imaging market size is expected to grow from USD 13.16 billion in 2025 to USD 14.98 billion in 2026 and is forecast to reach USD 28.65 billion by 2031 at 13.84% CAGR over 2026-2031. Rapid integration of depth sensors in mid-tier smartphones, accelerating deployment of solid-state LiDAR in advanced driver assistance systems, and growing demand for real-time 3D medical imaging anchor this growth trajectory. Advancements in vertical-cavity surface-emitting laser (VCSEL) chiplets, coupled with lower-cost 3D semiconductor stacks, are eroding price barriers and expanding use cases across industrial inspection and climate analytics. Meanwhile, supply-chain exposure to gallium arsenide epi-wafer shortages and evolving biometric privacy regulations temper the near-term outlook but have not derailed investment programs by automotive, healthcare, and consumer-electronics OEMs seeking spatial intelligence at scale. Incumbent semiconductor vendors use portfolio breadth and wafer-level manufacturing control to retain leadership, yet specialized depth-sensing startups are closing the performance-per-dollar gap through AI-optimized algorithms and chiplet architectures.

Key Report Takeaways

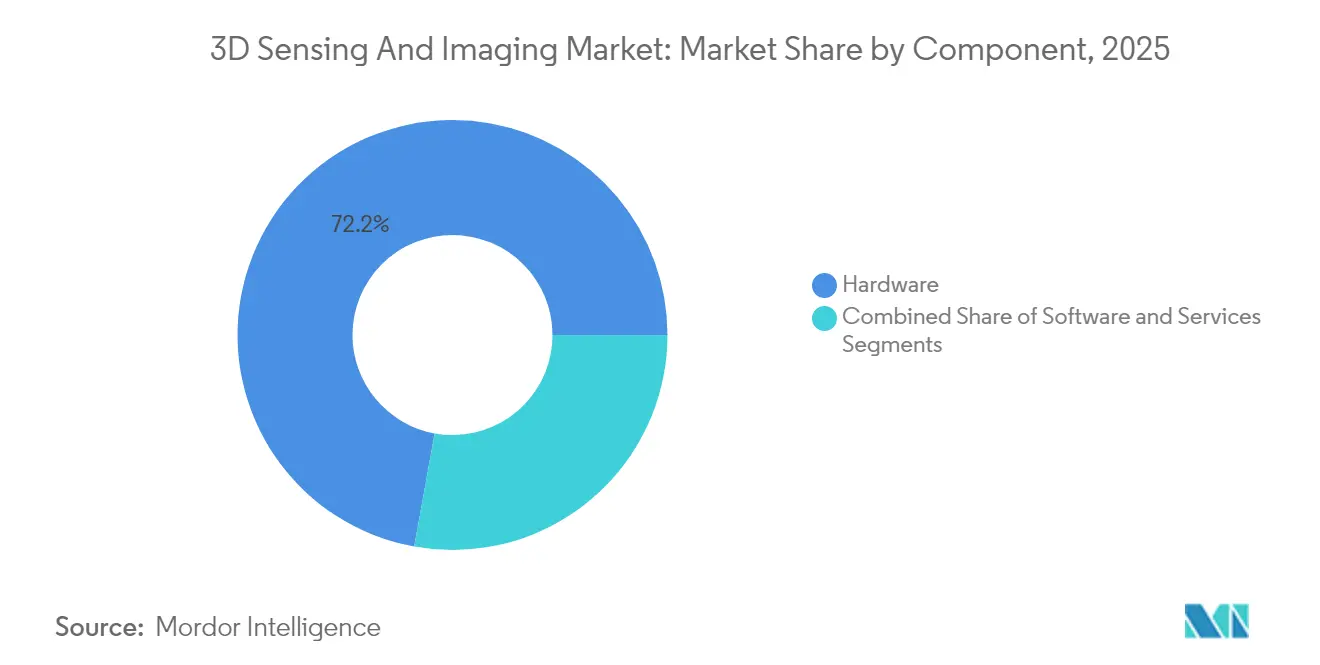

- By component, hardware led with 72.15% of revenue of the 3D sensing and imaging market in 2025, while services are projected to advance at a 14.88% CAGR through 2031.

- By technology, time-of-flight accounted for 43.25% of the 2025 revenue of the 3D sensing and imaging market, whereas ultrasound-based sensing is set to grow at a 15.62% CAGR to 2031.

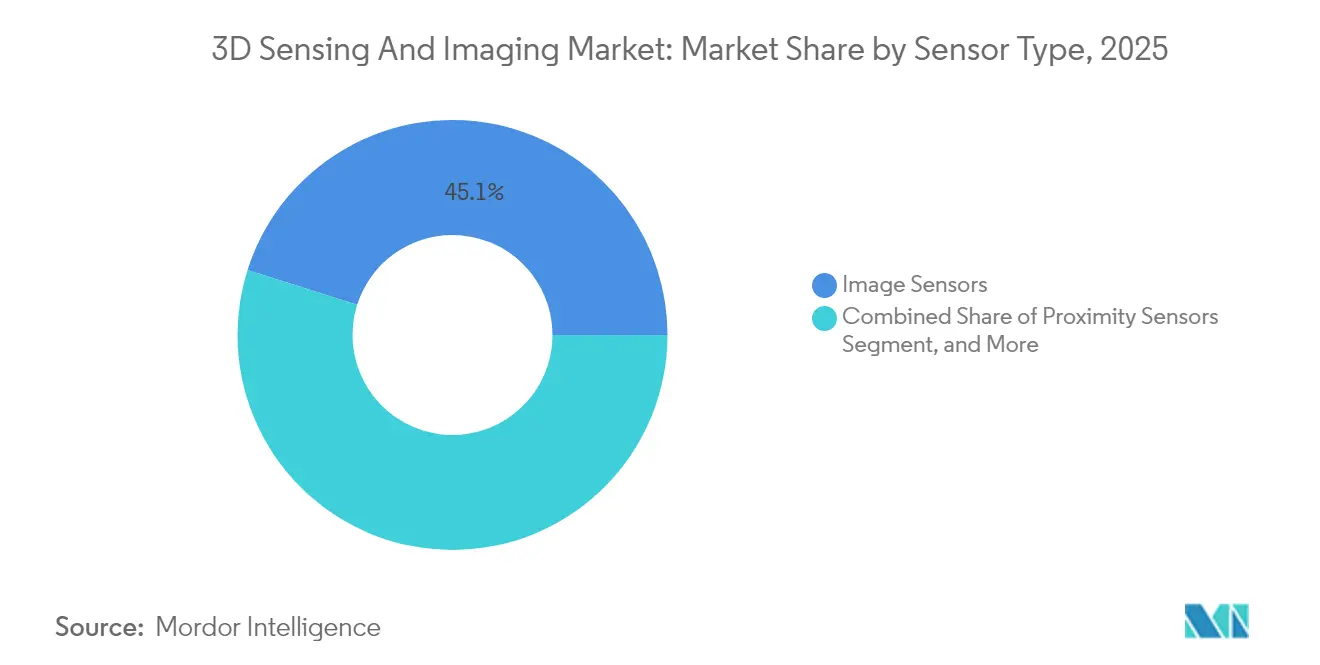

- By sensor type, image sensors captured 45.12% of 2025 sales of the 3D sensing and imaging market, and proximity sensors are forecast to expand at a 16.02% CAGR through 2031.

- By connectivity, wireless networks dominated with a 58.05% share of the 3D sensing and imaging market in 2025 and are also the fastest-growing at a 14.71% CAGR to 2031.

- By end-user industry, consumer electronics held 39.65% of the 2025 revenue of the 3D sensing and imaging market, while healthcare applications are rising at a 16.08% CAGR through 2031.

- By geography, North America led with 37.85% revenue of the 3D sensing and imaging market in 2025, but Asia-Pacific is projected to climb at a 15.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global 3D Sensing And Imaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone roll-out of structured-light depth cameras | +3.2% | Global; Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Automotive ADAS adoption of solid-state LiDAR | +2.8% | North America, Europe, expanding Asia-Pacific | Long term (≥ 4 years) |

| Industry 4.0 3D machine-vision inspection | +2.1% | Global manufacturing centers | Medium term (2-4 years) |

| Healthcare demand for minimally invasive real-time 3D imaging | +1.9% | North America, Europe, emerging markets | Long term (≥ 4 years) |

| VCSEL-on-CMOS chiplets for sub-USD 1 sensors | +1.7% | Global; Asia-Pacific fabrication leadership | Short term (≤ 2 years) |

| Satellite 3D Earth-observation constellations | +1.5% | Global government and research agencies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Widespread Smartphone Integration of Structured-Light 3D Cameras

Structured-light depth modules once reserved for premium flagships are now commonplace in mid-range handsets, lowering entry costs and normalizing user expectations for spatial photography, AR gaming, and secure face authentication. Apple’s iPhone 15 Pro LiDAR module validated consumer appetite for spatial computing, while Android OEMs rapidly released cost-reduced structured-light solutions. OmniVision’s April 2025 unveiling of a 1.5-megapixel global-shutter sensor for driver monitoring illustrates technology spillover from phones to vehicles, deepening economies of scale.[1]EEJournal Staff, “OMNIVISION Launches 1.5-Megapixel Global Shutter Sensor for Automotive Driver Monitoring Systems,” eejournal.com Volume ramp-ups push component pricing toward the sub-USD 1 threshold, unlocking adoption in industrial scanners and handheld medical devices.

Automotive ADAS Demand for Solid-State LiDAR Depth Maps

Vehicle makers are phasing out rotating LiDAR heads in favor of solid-state frequency-modulated continuous-wave (FMCW) units that offer vibration tolerance, velocity measurement, and lower cost. Daimler Truck’s 2024 selection of Aeva FMCW LiDAR underscored industry confidence in chip-scale depth sensors for Level 4 trucking fleets. Although automotive homologation extends timelines, Tier-1 suppliers with zero-defect manufacturing credentials stand to gain recurring design wins as ADAS moves down the vehicle price curve.

Industry 4.0 Adoption of 3D Machine-Vision Inspection Systems

Smart factories prioritize in-line 3D metrology to achieve zero-defect output in increasingly high-mix production. Keyence grew 2024 revenue to USD 7.061 billion with operating margins above 51.9%, attributable in part to instant measurement systems performing 99-dimensional checks in under three seconds.[2]Keyence Corporation, “Our Technology,” keyence.com These systems shave scrap rates and enable rapid line changeovers, ensuring robust demand for AI-assisted depth analysis software that accompanies hardware installs.

Healthcare Shift Toward Minimally Invasive, Real-Time 3D Imaging

Medical-device firms integrate micrometer-class 3D sensors into endoscopes, catheters, and navigation probes to enhance surgical precision and shorten recovery. OmniVision’s OH0TA sensor packs 400×400 RGB pixels at 30 fps inside a tip smaller than a grain of rice, running on just 20 mW. Surgeons gain depth perception that mitigates reliance on mental reconstruction from 2D images, supporting procedure time reductions and better outcomes that justify premium device pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of high-power GaAs epi-wafers | -1.8% | Global; Asia-Pacific fabrication centers | Short term (≤ 2 years) |

| Calibration complexity in multi-sensor camera modules | -1.2% | Global manufacturing regions | Medium term (2-4 years) |

| Cyber-security risks from depth-map spoofing | -0.9% | North America, Europe | Medium term (2-4 years) |

| Uncertain rules on public-space biometric capture | -0.7% | Europe, North America, expanding worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Scarcity of High-Power GaAs Epi-Wafers

Gallium arsenide substrate output remains concentrated among a handful of Asia-Pacific growers, creating price spikes and 20-week lead times for high-power VCSELs used in long-range time-of-flight modules. Sensor makers redesign optics for lower peak current draw and pursue silicon nitride photonics as a hedge, but near-term unit allocations still constrain automotive LiDAR rollout schedules.

Calibration Complexity Across Multi-Sensor Camera Modules

RGB, infrared, and depth elements stitched into single assemblies demand sub-pixel alignment over operating conditions from -40 °C to +85 °C. Automotive safety standards mandate 15-year stability, forcing vendors to adopt self-calibrating architectures and AI-based drift detection. Certification cycles lengthen, elevating engineering costs and raising the barrier to entry for new market entrants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Faces Services Disruption

Hardware retained 72.15% of the 3D sensing and imaging market in 2025, yet services are growing 14.88% CAGR to 2031 as buyers seek turnkey deployments and outcome-based pricing. Faro Technologies now derives 20.9% of quarterly revenue from software and recurring cloud analytics, illustrating how calibration, maintenance, and AI model updates create annuity streams. Vendors package installation and lifetime support to secure multi-year deals, gradually tilting revenue mix toward services.

Demand for edge AI tool-chains that compress depth maps into actionable events further propels software attach rates. This erosion of pure-play hardware margins pressures component suppliers to form alliances with cloud and middleware providers, ensuring ecosystem stickiness and data-driven upsell potential.

By Technology: Time-of-Flight Leadership Challenged by Ultrasound Innovation

Time-of-flight kept a 43.25% share in 2025 because its silicon photodiodes and VCSEL drivers align with smartphone cost envelopes, securing billions of annual units. The 3D sensing and imaging market size for ultrasound-based systems, however, is projected to expand 15.62% annually as acoustic transducers excel in bright-sunlight and translucent-material scenarios. Industrial robotics adopts hybrid optical-ultrasound stacks for defect detection on glossy metals, while hospitals favor ultrasound depth probes for radiation-free fetal and cardiac imaging. Sensor designers leverage 3D-stacked CMOS to co-locate ultrasound receive circuits and optical imagers, yielding sensing clusters that toggle modality based on the environment.

By Sensor Type: Image Sensors Face Proximity Sensor Disruption

Image sensors accounted for 45.12% revenue in 2025, yet proximity sensors will grow 16.02% CAGR, buoyed by touchless interfaces in vehicles and operating rooms. 3D sensing-enabled human-machine interactions rely on short-range ToF or ultrasonic proximity data to wake displays, open doors, or trigger sterile-field commands. Multi-axis accelerometers and gyros embed motion cues that correct for hand jitter in mobile 3D scanning, widening adoption in construction and heritage preservation.

By Connectivity: Wireless Dominance Reflects Mobility Demands

Wireless links captured a 58.05% share in 2025 and will maintain a 14.71% CAGR as 5G release 17 introduces sidelink features ideal for vehicle-to-cloud depth-map uploads. Edge inference reduces bandwidth usage by 80%, transmitting only semantic scene graphs to enterprise servers. Wired Ethernet still rules inside factory cells and avionics cabins where latency determinism and electromagnetic immunity are paramount, prompting hybrid backbones that marry fiber spines with Wi-Fi 7 endpoints.

By End-User Industry: Healthcare Growth Challenges Consumer Electronics Leadership

Consumer electronics contributed 39.65% revenue in 2025 via smartphones, AR headsets, and gaming peripherals. The healthcare segment, expanding 16.08% CAGR, appropriates consumer sensor breakthroughs to power laparoscopic vision, dental scanning, and smart prosthetics. Surgical-robot OEMs demand sub-millimeter 3D accuracy, stimulating partnerships between optical sensor houses and medical-software vendors that navigate FDA 510(k) pathways.

Geography Analysis

North America led with 37.85% revenue in 2025, owing to entrenched automotive and medical-device manufacturers, yet Asia-Pacific is climbing 15.74% CAGR. Chinese handset and contract-manufacturing giants compress bill-of-materials to democratize depth cameras, while Japanese precision-machinery firms elevate quality inspection standards that require micron-level 3D capture. Korean display producers deploy in-line 3D profilometers to validate next-gen OLED stacks. India pilots satellite-based 3D soil-moisture mapping to optimize crop yields, signaling broader smart-agriculture uptake. Europe remains steady, driven by Euro NCAP mandates and industrial automation subsidies that reward machine vision investments.

Competitive Landscape

Market fragmentation is moderate: legacy image-sensor titans Sony, STMicroelectronics, and Onsemi coexist with pure-play depth pioneers such as Aeva, Lumentum, and Airy3D. Semiconductor majors leverage wafer capacity and global sales channels, while startups differentiate with event-based neuromorphic arrays and quantum-dot short-wave-infrared hybrids. Keyence exploits vertical integration from optics through AI analytics, maintaining operating margins above 50%. Meanwhile, OmniVision’s April 2025 presence-detection sensor showcases single-die intelligence that sidesteps costly co-processors.[4]OmniVision Technologies, “OMNIVISION Announces New, Single Intelligent Sensor for Presence Detection, Facial Recognition and Always-On,” ovt.com Strategic directions favor mergers: Zebra bought Photoneo for logistics-automation depth cameras, and Viavi added Inertial Labs for position-aware test gear. Chipmakers pursue chiplet packaging to collapse lasers and photodiodes into CMOS interposers, aiming for sub-USD 1 bill-of-materials.

White-space opportunities span ultra-low-power IoT wake-on-motion modules and radiation-hardened lunar-surface mappers. Competitive advantage increasingly hinges on software ecosystems that transform raw point clouds into semantic maps, enabling vendors with machine-learning stacks to lock in customers through continuous model updates.

3D Sensing And Imaging Industry Leaders

Infineon Technologies AG

Microchip Technology Inc.

OmniVision Technologies Inc.

Qualcomm Inc.

Sick AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: LIPS Corporation partnered with Samsung and Onsemi to push VCSEL-on-CMOS chiplets toward sub-USD 1 cost targets, accelerating smartphone and automotive adoption.

- May 2025: Prophesee and Tobii teamed to blend event-based sensors with eye-tracking algorithms for ultra-low-power AR/VR headsets.

- April 2025: Airy3D and Teledyne e2v introduced the Topaz5D industrial CMOS line, integrating depth capture for sub-millimeter factory inspection.

- March 2025: Zebra Technologies acquired Photoneo, expanding 3D imaging in warehouse automation.

- January 2025: Aeva and Wideye by AGC demonstrated FMCW LiDAR within automotive-grade glass modules, lowering per-unit cost and improving robustness.

Global 3D Sensing And Imaging Market Report Scope

3D sensing is a depth-sensing technology that augments camera capabilities for object and facial recognition in augmented reality, autonomous driving, gaming, and a wide range of other applications. It involves capturing a real-world object's length, width, and height with greater clarity and in-depth detail, which can be achieved using various technologies such as structured light and time of flight.

The 3D sensing market is segmented by component (hardware, software, and services), technology (ultrasound, structured light, time of flight, stereoscopic vision, and other technologies), type (position sensor, image sensor, temperature sensor, accelerometer sensor, proximity sensor, and other types), connectivity (wired network connectivity and wireless network connectivity), end-user industry (consumer electronics, automotive, healthcare, aerospace and defense, security and surveillance, media and entertainment, and other end-user industries), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The report offers the market size and forecasts for all the above segments in value (USD).

| Hardware |

| Software |

| Services |

| Ultrasound |

| Structured Light |

| Time-of-Flight |

| Stereoscopic Vision |

| Other Technologies |

| Position Sensors |

| Image Sensors |

| Temperature Sensors |

| Accelerometer Sensors |

| Proximity Sensors |

| Other Sensor Types |

| Wired Network Connectivity |

| Wireless Network Connectivity |

| Consumer Electronics |

| Automotive |

| Healthcare |

| Aerospace and Defense |

| Security and Surveillance |

| Media and Entertainment |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Singapore | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Technology | Ultrasound | ||

| Structured Light | |||

| Time-of-Flight | |||

| Stereoscopic Vision | |||

| Other Technologies | |||

| By Sensor Type | Position Sensors | ||

| Image Sensors | |||

| Temperature Sensors | |||

| Accelerometer Sensors | |||

| Proximity Sensors | |||

| Other Sensor Types | |||

| By Connectivity | Wired Network Connectivity | ||

| Wireless Network Connectivity | |||

| By End-user Industry | Consumer Electronics | ||

| Automotive | |||

| Healthcare | |||

| Aerospace and Defense | |||

| Security and Surveillance | |||

| Media and Entertainment | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Singapore | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the global 3D sensing and imaging market in 2026?

The market is valued at USD 14.98 billion in 2026.

What compound annual growth rate is projected through 2031?

A 13.84% CAGR is forecast between 2026 and 2031.

Which component category is expanding fastest?

Services are growing at 14.88% CAGR, reflecting demand for turnkey depth-sensing solutions.

Which technology segment leads today?

Time-of-flight holds 43.25% of 2025 revenue and remains the largest technology segment.

Which region is expected to grow most rapidly?

Asia-Pacific is advancing at a 15.74% CAGR, driven by manufacturing scale and smartphone production.

What is restraining near-term supply?

Limited gallium arsenide epi-wafer capacity is delaying VCSEL production and raising component costs.

Page last updated on: