3D Reconstruction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

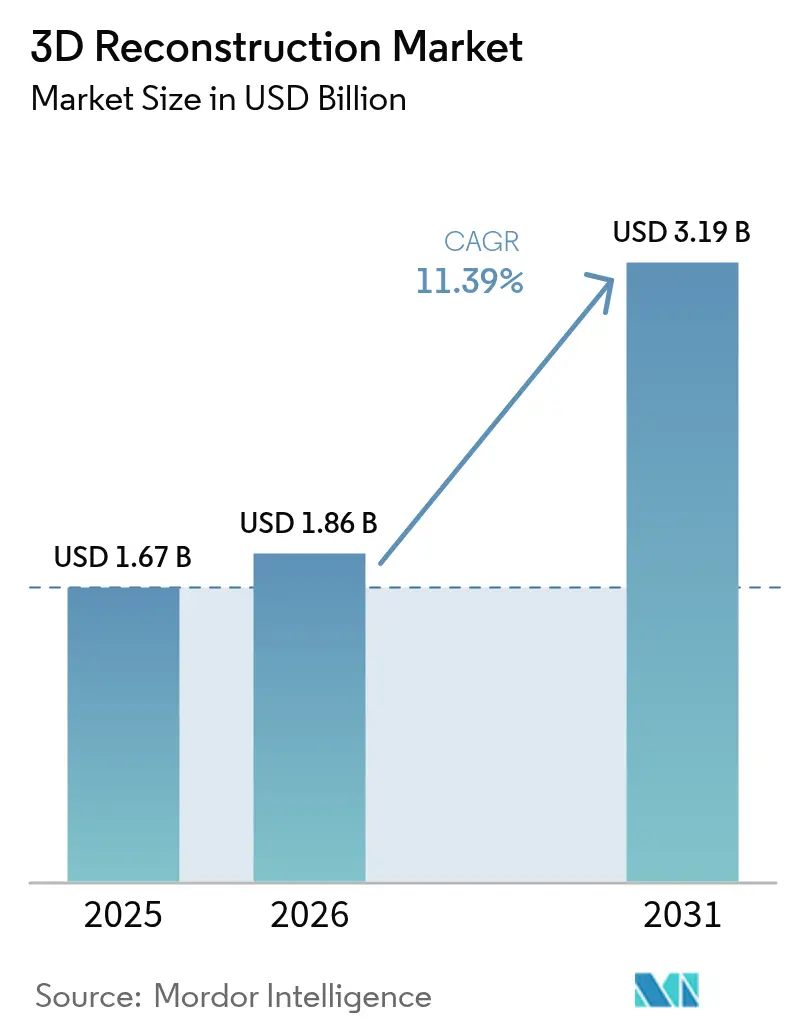

| Market Size (2026) | USD 1.86 Billion |

| Market Size (2031) | USD 3.19 Billion |

| Growth Rate (2026 - 2031) | 11.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

3D Reconstruction Market Analysis by Mordor Intelligence

3D reconstruction market size in 2026 is estimated at USD 1.86 billion, growing from 2025 value of USD 1.67 billion with 2031 projections showing USD 3.19 billion, growing at 11.39% CAGR over 2026-2031. This growth is based on the steady migration from pilot projects to production-scale rollouts in construction, healthcare, media, and advanced manufacturing. Strong demand for digital twins in capital projects, falling LiDAR and imaging sensor prices, wider cloud-GPU availability, and the adoption of autonomous systems in logistics and mining are amplifying market expansion. Suppliers are reorganizing portfolios around vertical solution stacks that collapse capture hardware, cloud processing, and analytics into subscription bundles, a shift that is lowering time-to-value for non-specialist users. At the same time, rising scrutiny of privacy, data-residency, and carbon intensity in cloud workflows is adding compliance overhead that favors vendors with secure, regionally distributed infrastructure. Cost and skills barriers remain, but automated feature extraction, AI-assisted workflow orchestration, and pay-per-use charging models are sharpening the commercial case for enterprise adoption.

Key Report Takeaways

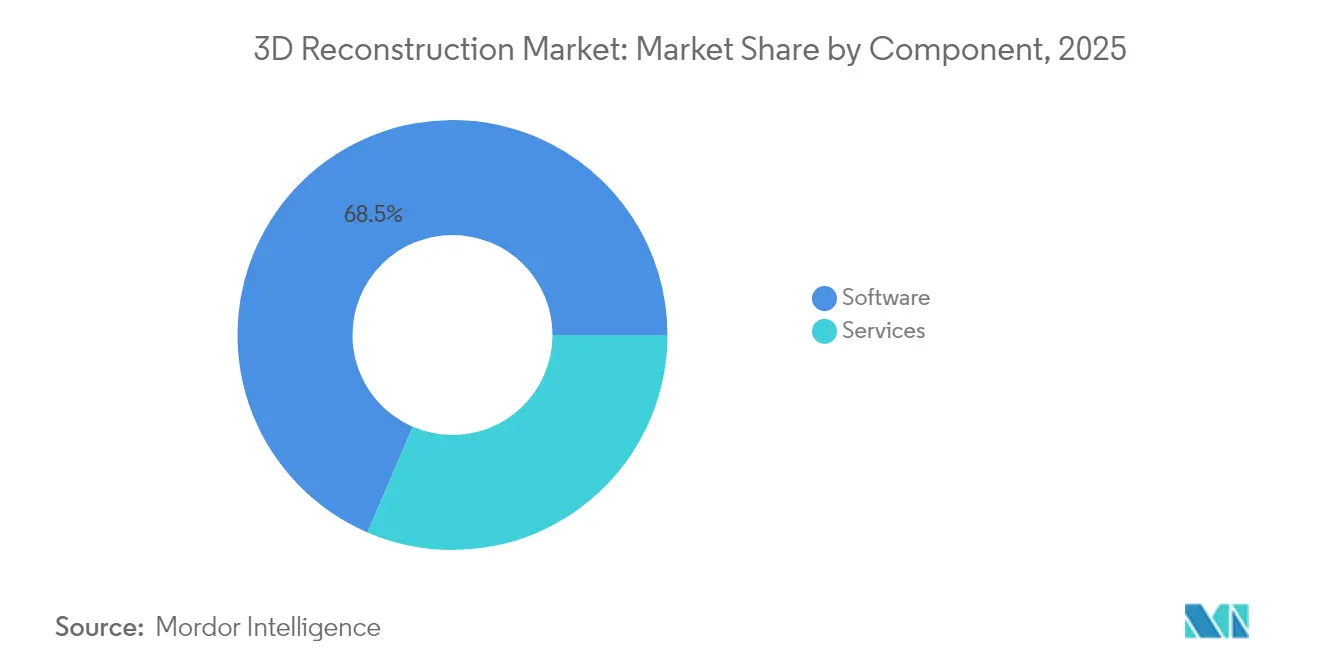

- By component, software led with a 68.52% of the 3D reconstruction market share in 2025, while services are projected to grow at an 11.67% CAGR through 2031.

- By technology type, active 3D reconstruction captured 60.85% of the 3D reconstruction market share in 2025; passive 3D reconstruction is projected to advance at a 11.75% CAGR through 2031.

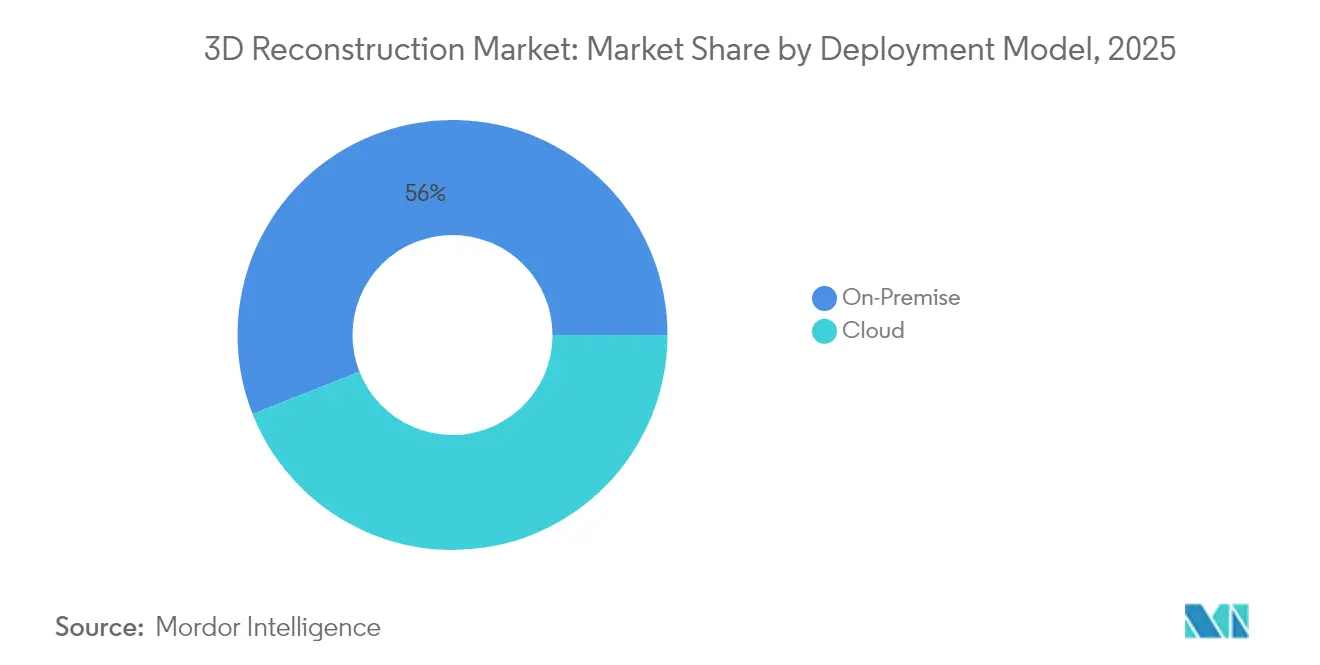

- By deployment model, on-premise installations accounted for 55.98% of the 3D reconstruction market size in 2025; however, cloud processing is projected to expand at a 11.58% CAGR through 2031.

- By application, construction and architecture commanded 40.92% of the 3D reconstruction market share in 2025, whereas robotics and drones are forecast to post a 12.98% CAGR through 2031.

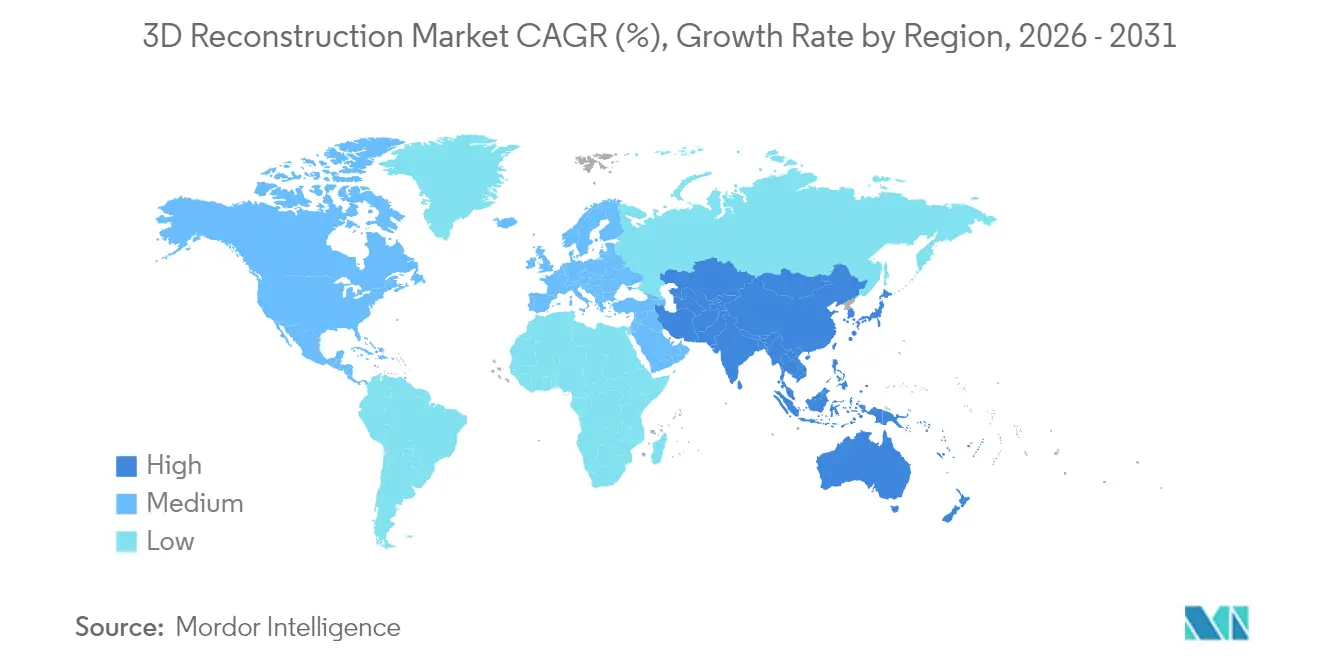

- By geography, North America accounted for 35.25% of the 3D reconstruction market share in 2025, while the Asia-Pacific region is projected to register a 12.44% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global 3D Reconstruction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of BIM-Driven Digital Twins in Construction | +2.8% | Global, with early gains in North America and Europe | Medium term (2-4 years) |

| Falling Sensor and LiDAR Costs Boosting Accessibility | +2.1% | Global, particularly Asia-Pacific and emerging markets | Short term (≤ 2 years) |

| Explosive VR and AR Content Demand Across Media and Entertainment | +1.9% | North America, Europe, and East Asia | Medium term (2-4 years) |

| Drone-Based Data Capture Enabling Large-Area Mapping | +1.7% | Global, with strong uptake in Asia-Pacific and South America | Short term (≤ 2 years) |

| Insurance Sector Shift to 3D Scene Documentation for Rapid Claims | +1.4% | North America and Europe | Medium term (2-4 years) |

| Patient-Specific Surgical Planning Platforms Gaining Traction | +1.7% | North America, Europe, and advanced Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

BIM-Driven Digital Twins in Construction

3D reconstruction is now an always-on feedback loop that keeps BIM models synchronized with on-site reality. Mandates such as the United Kingdom's National Digital Twin Programme and Singapore's Virtual Singapore require public infrastructure contractors to deliver federated digital twins that ingest periodic scans, accelerating demand for automated point cloud capture and mesh alignment. Contractors report that accurate reconstructions reduce field rework and compress handover times, thereby boosting adoption among owners seeking to minimize lifecycle costs. Improved interoperability standards, typified by ISO 19650 extensions, are reducing data conversion friction and encouraging multi-vendor workflows.[1]International Organization for Standardization, “ISO 19650 Information Management,” iso.org As digital-twin programs extend to municipal and utility assets, the 3D reconstruction market is expanding from design teams to facilities managers and maintenance contractors.

Falling Sensor and LiDAR Costs Boosting Accessibility

Solid-state innovation and volume manufacturing have pulled LiDAR price points below USD 500 per automotive-grade unit, widening the accessible customer base beyond tier-one contractors and defense primes.[2]Hesai Technology, “Hesai Announces 50% Price Reduction for AT512 Automotive LiDAR,” hesaitech.com Handheld SLAM scanners, which once cost USD 50,000, now list for under USD 30,000, and drone-mounted LiDAR payloads have dropped below USD 10,000, making corridor mapping accessible to utility cooperatives and mid-sized survey firms. Lower hardware cost is drawing new service entrants in South America, Africa, and South Asia, where earlier projects relied on satellite imagery because terrestrial scanning was uneconomical. The skills gap, however, has shifted to data processing; vendors are responding with cloud-hosted AI toolsets that automatically classify, colorize, and thin-point clouds, thereby shortening training cycles for non-geospatial professionals.

Explosive VR and AR Content Demand Across Media and Entertainment

Film studios, game publishers, and streaming platforms are racing to stock high-fidelity asset libraries as real-time engines such as Unreal 5 deliver cinematic lighting and geometry at interactive frame rates. Photogrammetry offers the fastest route to lifelike replicas, and volume-capture stages equipped with synchronized camera arrays are now standard in major production hubs. European compliance rules requiring labeling of synthetic media have elevated the need for provenance metadata, favoring end-to-end systems that embed capture logs inside the resulting mesh files. Growth will accelerate as edge-rendered AR marketing, virtual showrooms, and immersive sports broadcasts move from pilots to commercial deployment.

Drone-Based Data Capture Enabling Large-Area Mapping

Unmanned aerial systems equipped with RTK positioning and lightweight LiDAR have become essential for infrastructure inspection, agriculture, and disaster response. DJI’s Matrice 350 RTK, equipped with the Zenmuse L2 sensor, captures 240,000 points per second up to 250 meters, effectively replacing manned aircraft for many corridor surveys. Annual drone missions logged by large construction platforms now exceed two million, indicating a shift from periodic surveys to near-continuous monitoring. Regulatory environments are stabilizing as Remote ID in the United States and harmonized BVLOS corridors in Europe establish clearer compliance pathways, enabling asset owners to plan repeatable flight operations at an industrial scale.[3]Federal Aviation Administration, “Remote Identification of Unmanned Aircraft,” faa.gov

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Hardware-Software Investment Outlay | -1.6% | Global, particularly acute in emerging markets | Short term (≤ 2 years) |

| Workflow Complexity Requiring Specialist Skillsets | -1.3% | Global, with skill shortages most severe in Asia-Pacific and Africa | Medium term (2-4 years) |

| Urban-Capture Privacy and Data-Sovereignty Regulations | -0.9% | Europe, North America, and advanced Asia-Pacific markets | Long term (≥ 4 years) |

| Cloud Processing's Rising Carbon-Footprint Scrutiny | -0.7% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Hardware-Software Investment Outlay

A production-grade terrestrial scanner still ranges from USD 40,000 to USD 80,000, and leading photogrammetry software carries annual license and maintenance charges that can exceed USD 4,000 per seat. Cloud GPU time compounds these commitments: dense reconstruction of a 10,000-image survey can consume 200–300 GPU hours and incur USD 1,000 in processing fees. For cultural heritage bodies, small insurers, and municipal planning offices, capital intensity can slow adoption or prompt them to consider outsourcing. Vendor responses include hardware-as-a-service bundles, per-scan pricing, and short-term rentals; however, these alternatives often lock customers into proprietary ecosystems and defer, rather than eliminate, total costs.

Workflow Complexity Requiring Specialist Skillsets

Accurate reconstruction requires knowledge of photogrammetry, camera calibration, ground control, and coordinate systems; yet, globally certified practitioners remain in short supply. University geomatics cohorts are growing slowly, and graduates frequently migrate to higher-paying software roles, leaving field-survey and mapping firms understaffed. Vendors have introduced AI filters for tie-point cleaning, auto-triangulation wizards, and single-click dense-cloud generation; however, edge cases such as low-texture surfaces, reflective materials, and moving elements still require the expertise of experienced operators. Governments in India, Kenya, and Brazil have launched vocational upskilling programs in partnership with industry associations, but tangible workforce expansion is several years away.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain as Integration Complexity Rises

Software captured 68.52% of 2025 revenue through perpetual-license and subscription models, monetizing core photogrammetry and point-cloud platforms. Services revenue, however, is rising at an 11.67% CAGR because enterprises increasingly favor turnkey deliverables over in-house buildouts. Managed-service firms bundle field capture, GPU processing, QA, and data management into monthly fees that better align with project budgets than capital purchases. The American Society of Civil Engineers notes that a rising share of owners demand third-party validation certificates for survey accuracy, expanding opportunity for audit and advisory engagements. Vendors are augmenting product lines with captive service teams. Autodesk, Bentley Systems, and Trimble have each acquired regional survey specialists to offer hands-on workflow configuration and compliance documentation. As regulatory oversight around geolocation precision and personal-data masking tightens, services will remain the fastest-growing component of the 3D reconstruction market.

A second factor elevating services is the episodic nature of several high-value use cases. Insurers, law enforcement units, and emergency response agencies require rapid scene capture after rare events but cannot justify maintaining permanent teams or equipment. Subscription access to pre-shot city twins, on-demand field crews, and pay-per-scan robotics lowers barriers for these intermittent customers. Over the forecast horizon, professional services lines, ranging from change-detection analytics in construction to bespoke AI segmentation models in utilities, are expected to outpace core software revenue and reshape the vendor revenue mix.

By Technology Type: Passive Methods Close the Gap Through AI Advances

Active imaging, dominated by LiDAR, structured light, and time-of-flight sensors, held a 60.85% market share in 3D reconstruction in 2025, owing to its unmatched sub-centimeter fidelity in controlled conditions. Industrial metrology, factory automation, and autonomous vehicles still treat active sensors as mandatory. Yet passive photogrammetry is growing at an 11.75% CAGR as neural radiance fields and Gaussian splatting yield printable accuracy from sparse photographs. Mobile-first apps now transform 30–40 handheld images into textured meshes within minutes, a capability that unlocks ecommerce, residential real estate, and insurance use cases at negligible cost. The cost advantage of passive capture is particularly decisive for outdoor and large-area projects, especially in emerging markets where LiDAR imports face tariffs and supply chain delays.

Hybrid workflows that blend dense LiDAR point clouds with photogrammetric textures occupy a rising middle ground. Cultural heritage conservators and bridge inspectors combine modalities to achieve millimeter-level geometry and photorealistic surface detail in a single model. As the 3D reconstruction market size expands, vendors are shipping integrated toolkits that co-register active and passive inputs, reducing operator effort. Component costs are converging as well: as LiDAR falls below USD 500, price differentials shrink, allowing project managers to choose technology stacks based on the deployment environment rather than solely on budget constraints.

By Deployment Model: Cloud Gains as Processing Demands Exceed On-Premise Capacity

On-premise deployments accounted for 55.98% of installations in 2025, driven by defense, health, and critical infrastructure owners who must segregate sensitive data. National mapping agencies with continuous capture flows also favor local clusters for cost control and deterministic processing queues. However, hyperscalers have built GPU fleets optimized for photogrammetric dense matching, and SaaS platforms now allow users to spin up hundreds of cards for hours rather than purchasing servers outright. As a result, cloud processing is advancing at an 11.58% CAGR and is expected to overtake on-premise workloads before 2031.

Latency-sensitive edge tasks, such as initial imagery QC, blur detection, and coordinate tagging, often remain local, while the heavy lifting shifts to cloud nodes. Vendors have introduced region-locked processing options that keep European customer data inside EU borders, helping clients navigate Schrems II compliance. Carbon accounting dashboards that quantify GPU energy consumption are emerging, enabling sustainability teams to optimize compute allocations. Together, these features reduce buyer anxiety around data sovereignty and climate impact, two issues that historically favored on-premise builds.

By Application: Robotics and Drones Lead Growth as Autonomy Scales

Construction and architecture accounted for 40.92% of 2025 revenue, as contractors validated as-built conditions against BIM designs and facility managers scheduled maintenance based on deformation trends. Healthcare usage is growing as hospitals employ patient-specific anatomical models for pre-surgical rehearsals, reducing operating time and complications. Media and entertainment studios are pushing photorealistic capture for virtual production sets and immersive streaming. Cultural heritage digitization projects continue worldwide, supported by ministries of culture and nonprofits such as CyArk, which preserves at-risk monuments in sub-millimeter detail.

Industrial inspection leverages robotic arms and mobile scanners on automotive and aerospace lines to detect surface defects that camera-only solutions miss. Public safety agencies document crime scenes for courtroom presentation with handheld scanners or LiDAR-equipped drones, while forensic reconstruction tools calculate trajectories and impact zones. Robotics and drones, advancing at a 12.98% CAGR, now combine visual SLAM with dense 3D meshes to localize in GPS-denied environments such as warehouses and underground mines. Universities, museums, and laboratories use 3D reconstruction to virtualize specimens and exhibits, enabling remote collaboration and online learning. Gaming and virtual reality creators utilize photogrammetry libraries, such as Quixel Megascans, to accelerate the process of building environments. Free asset access on major engines lowers the entry barriers for indie developers and educators.

Geography Analysis

North America held 35.25% of 2025 demand, buoyed by early BIM mandates, a robust defense-industrial base, and an insurance sector that widely documents claims in 3D. U.S. federal programs, such as Every Day Counts, promote LiDAR bridge inspections, while Canadian mining and forestry firms deploy drones for environmental monitoring. Data-residency differences among U.S. states and Canadian provinces can complicate cross-border projects; however, local cloud regions help mitigate this issue. Mexico’s rail and airport modernizations have led to corridor-mapping projects, although limited domestic expertise has slowed the field execution.

Europe maintains a strong position through nationwide BIM requirements in the United Kingdom, Germany, and France, as well as through extensive cultural heritage preservation across the Mediterranean. Horizon Europe allocated USD 107.35 billion in research funding toward digital twin and geospatial technologies, stimulating university-industry consortia. Privacy rules under GDPR and the forthcoming AI Act increase compliance costs but also drive demand for automated masking, redaction, and on-shore processing. Russian construction firms, facing import constraints, have turned to domestic software, which has encouraged the growth of the local ecosystem despite capability gaps.

The Asia-Pacific region is the fastest-growing, with a projected 12.44% CAGR. China’s mandate that public projects above CNY 200 million deploy BIM is feeding large-scale scan-to-BIM workflows. Japan’s transport ministry utilizes LiDAR-equipped drones to monitor tunnels and bridges in seismic zones, thereby protecting supply chains and ensuring public safety. India’s Survey of India is mapping cities in 3D to modernize land records and disaster-response planning. South Korea’s shipyards and fabs require sub-millimeter inspection, while Australia’s mining sector leverages aerial LiDAR for pit optimization. Broadband gaps and limited photogrammetry training restrict expansion in Indonesia, the Philippines, and Pacific Island states.

Middle East and Africa sales accelerate as Saudi Arabia’s NEOM and the United Arab Emirates’ Dubai 2040 initiatives demand city-scale digital twins. South Africa’s deep mines scan underground workings for safety, and Egypt’s Ministry of Tourism digitizes antiquities for virtual tourism. Political instability and currency volatility hinder capital acquisitions in several sub-Saharan countries, resulting in uneven market penetration. Gulf Cooperation Council growth, however, drags regional averages upward through mega-project spending.

South America experiences renewed momentum as Brazil’s construction sector rebounds, and Argentina expands its lithium mining operations. Brazilian land-reform programs now mandate drone surveys for land-tenure clarification, spurring demand for cloud photogrammetry. Chile’s public-works ministry relies on LiDAR to map landslide zones on the Pan-American Highway, but import tariffs on laser scanners and GPUs inflate project budgets. A Mercosur digital infrastructure working group is drafting shared technical standards to harmonize cross-border data exchange; yet, tangible adoption remains incremental.

Competitive Landscape

The 3D reconstruction market is moderately concentrated. The top five suppliers, Autodesk, Bentley Systems, Trimble, Hexagon, and Matterport, collectively account for most of revenue. Each is folding reality capture deeper into flagship CAD and PLM suites to cement account control. Autodesk integrated neural-radiance-field reconstruction into ReCap Pro 2025, and Bentley extended its iTwin cloud environment through the USD 1.2 billion Seequent acquisition to seamlessly couple subsurface and surface models. Trimble’s USD 2.124 billion purchase of Transporeon expanded its mapping stack into logistics, signaling a strategy of integrating spatial data with supply-chain execution.

Specialists respond by sharpening vertical focus. Pix4D tailors products for agriculture and mining, Agisoft emphasizes forensic photogrammetry, and GeoSLAM dominates handheld SLAM scanners in mining and underground construction. AI is now a decisive differentiator: Hexagon’s partnership with NVIDIA embeds GPU-accelerated semantic segmentation, halving reconstruction times for large industrial sites. Siemens and Dassault Systèmes link capture engines with manufacturing simulation to shorten design-to-production cycles, defending industrial domains against pure-play entrants.

Price competition is intensifying as the costs of LiDAR and cameras fall and consumer-grade devices achieve sufficient accuracy for many tasks. Turnkey service bureaus must differentiate themselves via domain expertise, rapid turnaround, and integrated analytics, rather than relying solely on equipment access. Compliance credentials, including ISO 19650, SOC 2, and GDPR, as well as national cybersecurity certifications, also influence public-sector tenders, reinforcing the edge held by well-capitalized incumbents with global data center footprints.

3D Reconstruction Industry Leaders

Autodesk Inc.

Pix4D SA

Agisoft LLC

Bentley Systems Incorporated

Matterport Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Hexagon AB introduced HxGN LiveView, a browser-based viewer that streams LiDAR point clouds directly from edge appliances, trimming remote-team data-transfer loads by 70%.

- August 2025: Autodesk unveiled ReCap Pro 2026 Beta with new cloud-GPU orchestration that cuts dense-mesh processing times by 50% on projects exceeding 10,000 images.

- February 2025: Siemens AG embedded RealityCapture photogrammetry into the Xcelerator portfolio, giving manufacturing clients a seamless scan-to-simulation workflow inside a single platform.

- January 2025: Hesai Technology slashed the price of its AT512 automotive-grade LiDAR sensor by 50% to below USD 500, making high-density scanning affordable for drone and mobile-mapping integrators.

Global 3D Reconstruction Market Report Scope

The 3D Reconstruction Market Report is Segmented by Component (Software and Services), Technology Type (Active 3D Reconstruction and Passive 3D Reconstruction), Deployment Model (On-Premise and Cloud), Application (Construction and Architecture, Healthcare and Medical Imaging, Media and Entertainment, Cultural Heritage and Museum, Industrial Manufacturing and Inspection, Public Safety and Forensics, Robotics and Drones, Education and Research, and Gaming and Virtual Reality), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Active 3D Reconstruction |

| Passive 3D Reconstruction |

| On-Premise |

| Cloud |

| Construction and Architecture |

| Healthcare and Medical Imaging |

| Media and Entertainment |

| Cultural Heritage and Museum |

| Industrial Manufacturing and Inspection |

| Public Safety and Forensics |

| Robotics and Drones |

| Education and Research |

| Gaming and Virtual Reality |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Software | ||

| Services | |||

| By Technology Type | Active 3D Reconstruction | ||

| Passive 3D Reconstruction | |||

| By Deployment Model | On-Premise | ||

| Cloud | |||

| By Application | Construction and Architecture | ||

| Healthcare and Medical Imaging | |||

| Media and Entertainment | |||

| Cultural Heritage and Museum | |||

| Industrial Manufacturing and Inspection | |||

| Public Safety and Forensics | |||

| Robotics and Drones | |||

| Education and Research | |||

| Gaming and Virtual Reality | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the 3D reconstruction market in 2031?

The market is forecast to reach USD 3.19 billion by 2031, reflecting an 11.39% CAGR over 2026-2031.

Which component is growing fastest within 3D reconstruction solutions?

Services, including managed capture, cloud processing, and workflow consulting, are expanding at an 11.67% CAGR through 2031.

Why are passive photogrammetry methods gaining ground on active LiDAR solutions?

Neural radiance fields and other AI techniques have narrowed the accuracy gap while keeping hardware costs low, driving an 11.75% CAGR for passive systems.

Which application area is expected to record the highest growth rate?

Robotics and drones lead with a projected 12.98% CAGR as autonomous navigation and warehouse automation demand real-time spatial mapping.

How are privacy regulations affecting urban-scale 3D scanning projects?

GDPR and proposed AI-governance rules require explicit consent and regional data processing, increasing compliance costs but favoring vendors with in-region cloud infrastructure.

Page last updated on: