Surface Vision & Inspection Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

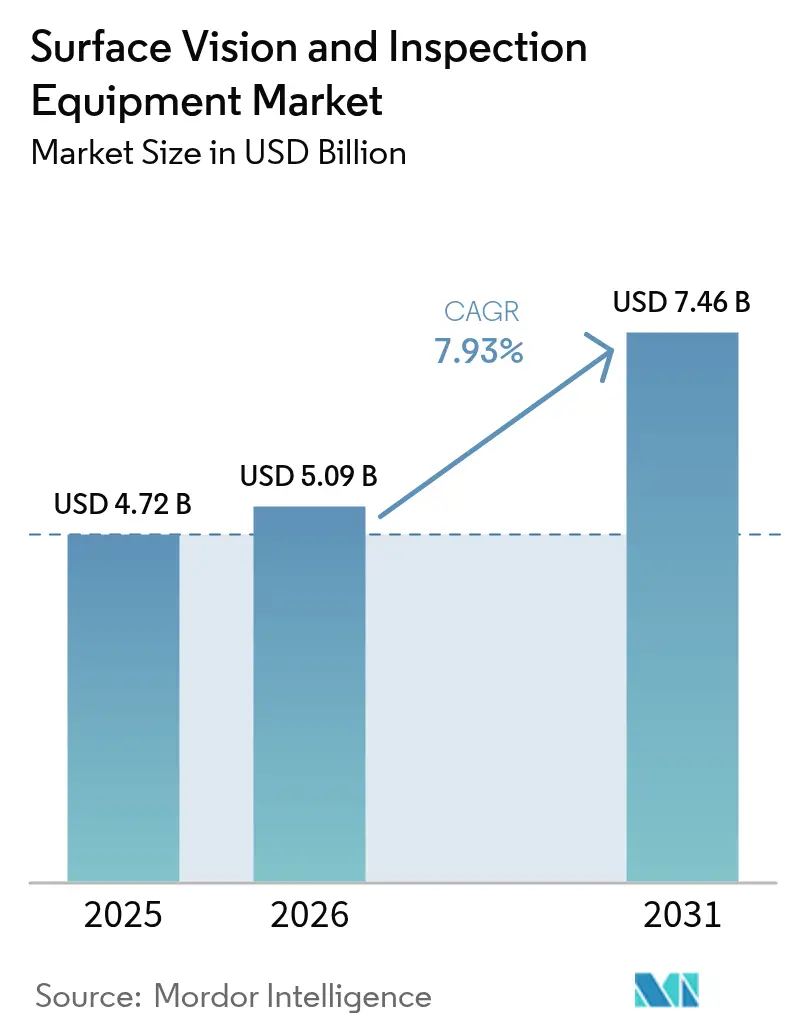

| Market Size (2026) | USD 5.09 Billion |

| Market Size (2031) | USD 7.46 Billion |

| Growth Rate (2026 - 2031) | 7.93% CAGR |

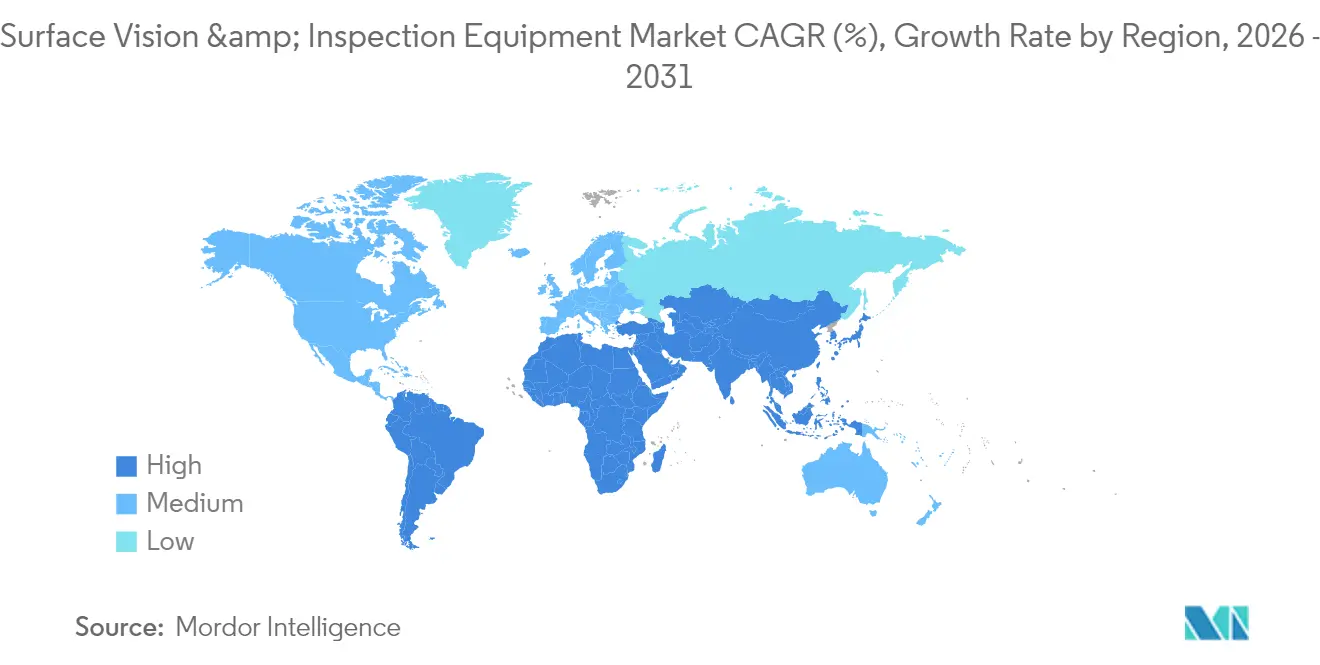

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

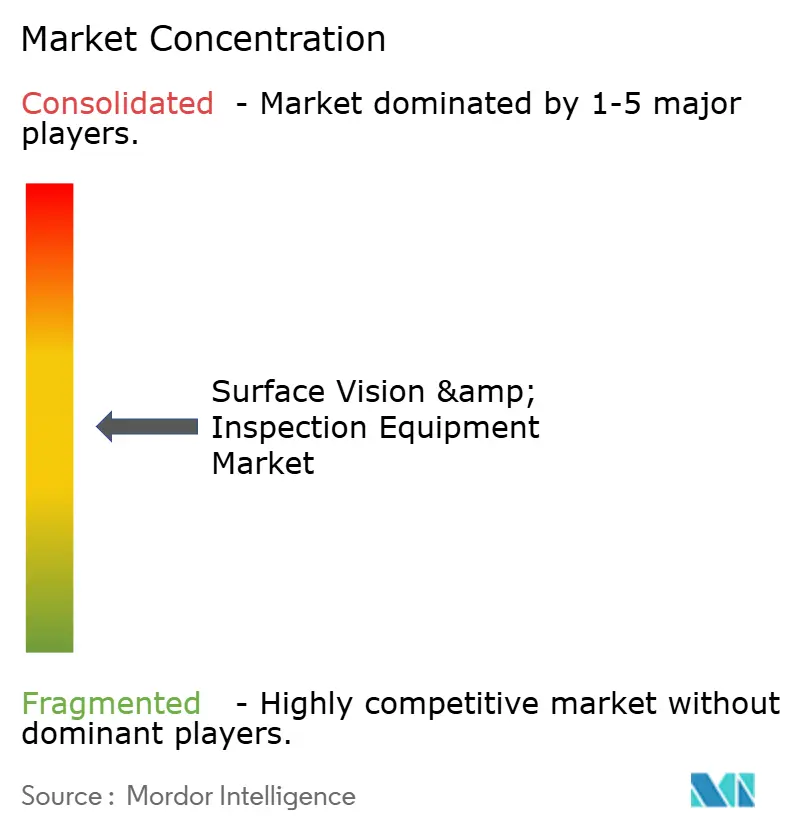

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surface Vision & Inspection Equipment Market Analysis by Mordor Intelligence

The surface vision and inspection equipment market size is expected to grow from USD 4.72 billion in 2025 to USD 5.09 billion in 2026 and is forecast to reach USD 7.46 billion by 2031 at 7.93% CAGR over 2026-2031. Accelerating adoption of hyperspectral imaging, real-time artificial intelligence (AI) inference at the edge, and pay-per-inspection service models are widening access to advanced visual quality assurance. Demand spikes in automotive battery lines, solar cell production, and semiconductor front-end fabrication reinforce the strategic value of near-zero-defect manufacturing. In tandem, the escalation of connected Industry 4.0 architectures is prompting corporations to place cybersecurity and data governance at the center of vision-system roadmaps. Mid-sized manufacturers are responding by favoring portable, low-capex scanners and pay-as-you-use software subscriptions that shorten investment payback cycles.

Key Report Takeaways

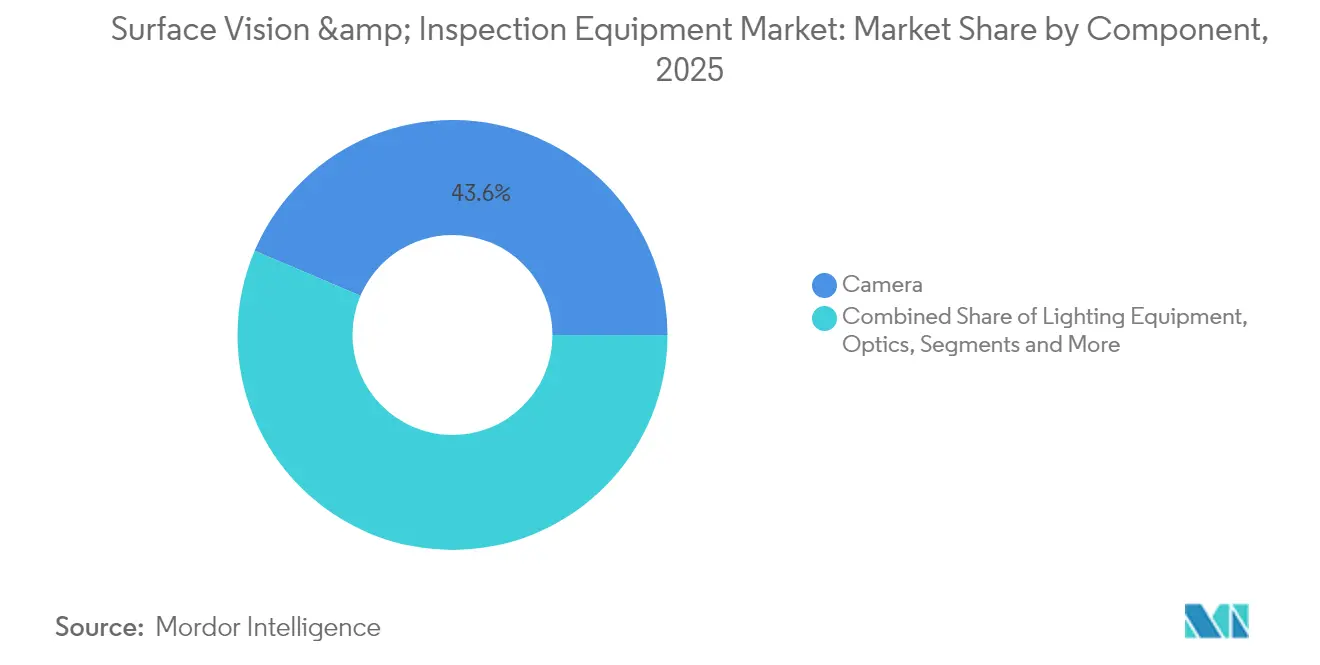

- By component, cameras led with a 43.60% revenue share in 2025, while AI-enabled vision systems are projected to expand at a 9.08% CAGR through 2031.

- By system type, 2D solutions held 62.30% of the surface vision and inspection equipment market share in 2025; AI-enabled systems are set to grow the fastest at an 8.55% CAGR to 2031.

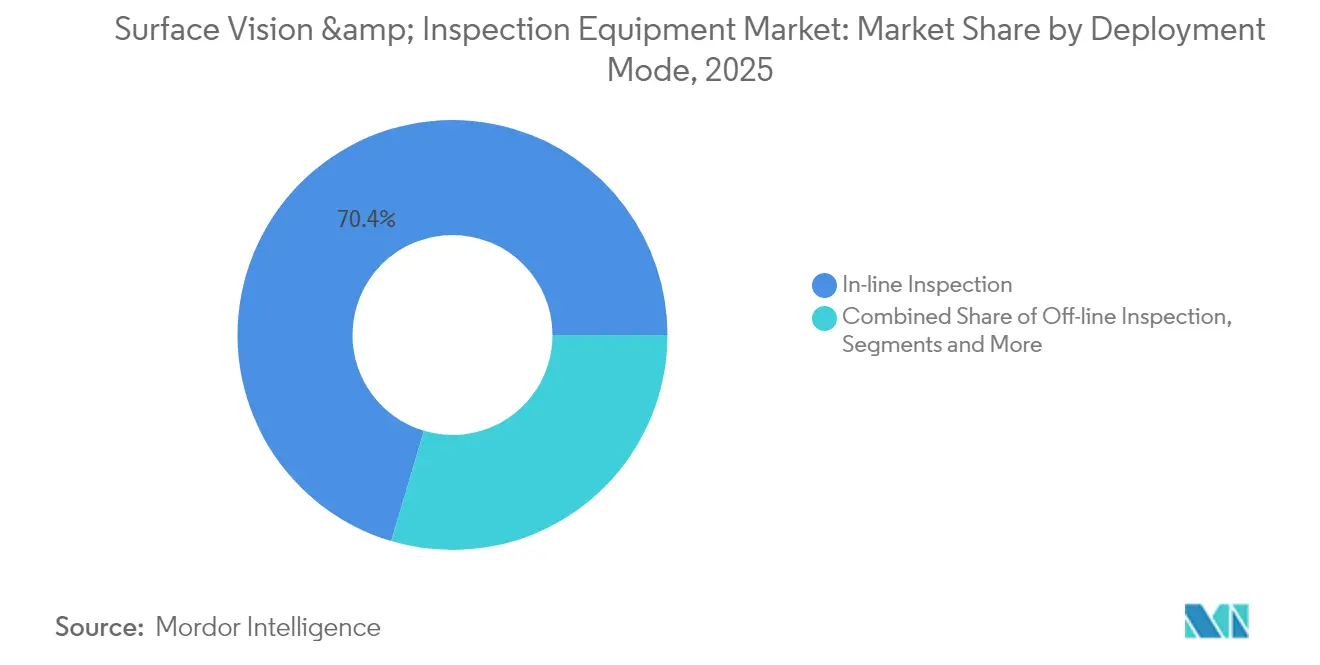

- By deployment mode, in-line inspection accounted for 70.40% of the surface vision and inspection equipment market size in 2025, whereas portable and handheld platforms are advancing at an 7.98% CAGR.

- By application industry, automotive led with 26.40% of the surface vision and inspection equipment market share in 2025, but battery and solar panel lines are positioned for the quickest expansion at a 9.25% CAGR.

- By geography, Asia Pacific dominated with a 38.40% revenue contribution in 2025, while South America is forecast to register the highest regional CAGR of 8.16% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surface Vision & Inspection Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing need for higher manufacturing throughput at lower cost | +2.1% | Global; strongest in APAC hubs | Medium term (2-4 years) |

| Rising demand for zero-defect quality in precision industries | +1.8% | North America & EU automotive, APAC electronics | Long term (≥ 4 years) |

| Adoption of Industry 4.0 and smart-factory automation | +1.6% | Global; led by Germany, China, Japan, South Korea | Medium term (2-4 years) |

| Emergence of hyperspectral imaging for sub-surface defect detection | +1.2% | APAC core; spill-over to North America | Long term (≥ 4 years) |

| Pay-per-inspection service models lowering SME capex barriers | +0.9% | Europe & North America early adopters | Short term (≤ 2 years) |

| ESG-driven mandatory inspection in battery and solar lines | +0.8% | Renewable-energy manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing need for higher manufacturing throughput at lower cost

Vision-enabled automation is enabling processors to compress inspection cycles from minutes to seconds while sustaining ≥99% detection accuracy, as evidenced by cutting-tool systems running four-second cycles assemblymag.com. Electronics factories operating as “dark” facilities in China validate the 24/7 production model and capture energy savings of 15–20%.[1]Antonio Bhardwaj, “China's Dark Factory Revolution,” faf.ae Cost-down pressures therefore reinforce the case for the surface vision and inspection equipment market across discrete and process manufacturing.

Rising demand for zero-defect quality in precision industries

Advanced semiconductor nodes, electric-vehicle battery packs, and implantable medical devices tolerate no latent defects. For example, Onto Innovation reported Q1 2025 revenue growth tied to DRAM and gate-all-around geometries, underscoring inspection’s link to wafer yield. Battery cell producers are similarly adopting round-the-clock visual analytics to prevent downstream safety failures. Consequently, the surface vision and inspection equipment market captures rising capital allocations in high-reliability segments.

Adoption of Industry 4.0 and smart-factory automation

Integration of cameras, illumination, and analytics with manufacturing execution systems supports closed-loop optimization. OMRON’s i-BELT data-service platform demonstrates predictive insight by aggregating line data to pre-empt quality drifts. Government programs, such as South Korea’s USD 2.24 billion robotics master plan, further fuel investments that directly reference machine-vision hardware in sensor roadmaps.[2]International Trade Administration, “South Korea Robotics Industry,” trade.gov

Emergence of hyperspectral imaging for sub-surface defect detection

Hyperspectral sensors capture contiguous wavelength ranges, enabling detection of impurities embedded beneath surfaces in aerospace composites, solar wafers, and additive-manufactured powders. As algorithms mature, manufacturers can segment spectral signatures in real time, unlocking new assurance regimes within the surface vision and inspection equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of skilled vision engineers and integration complexity | -1.4% | Global, particularly acute in North America and Europe | Long term (≥ 4 years) |

| High upfront cost of high-resolution 3D systems | -0.8% | Global, with higher impact on SMEs in emerging markets | Medium term (2-4 years) |

| Cyber-security risks in connected inspection networks | -0.6% | Global, with highest concern in critical infrastructure sectors | Medium term (2-4 years) |

| Rapid product-mix changes outpacing algorithm update cycles | -0.5% | Global, particularly in high-mix low-volume manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Scarcity of skilled vision engineers and integration complexity

Only 19.5% of South Korean SMEs report smart-factory uptake, citing limited technical capability as the top hurdle. [3]Ministry of SMEs and Startups, “Smart Manufacturing Innovation Survey,” venturesquare.net Cognex is countering the talent gap by channeling 17% of revenue into R&D to simplify setup through low-code interfaces. Yet the human-capital constraint continues to temper the near-term expansion rate of the surface vision and inspection equipment market.

High upfront cost of high-resolution 3D systems

Metrology-grade 3D platforms can command six-figure price tags, restricting penetration in cost-sensitive factories. A USD 69 million order for DRAM metrology exemplifies the capital intensity in semiconductor environments. Equipment-as-a-Service models are emerging but remain nascent, leaving many SMEs on the sidelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Dominance of Cameras amid AI Acceleration

Cameras represented 43.60% of 2025 revenue, cementing their status as the foundational element of any inspection stack. Progress in sensor resolution, frame rate, and ultraviolet sensitivity is expanding the attainable defect envelope in semiconductor back-end and micro-LED lines. Lighting and optics integrate tightly with those cameras to expose fine scratches on polished metals and detect voids in transparent substrates. The segment’s scale anchors the surface vision and inspection equipment market and secures volume pricing on complementary optics and frame grabbers.

AI-enabled vision platforms, while a smaller base, are forecast to post a 9.08% CAGR to 2031. Embedding convolutional neural networks directly into smart cameras reduces latencies that previously mandated host-based inference. Cognex’s April 2024 launch of an integrated 3D-with-AI device illustrates how suppliers now collapse multiple sub-systems into a single housing. This convergence is set to reshape the cost stack and expand addressable use cases across the surface vision and inspection equipment market.

By System Type: 2D Established yet AI-Driven Alternatives Scaling

2D vision keeps a 62.30% foothold thanks to barcode decoding, presence checks, and label verification that rarely require depth data. These legacy tasks continue to secure incremental refresh revenue as line speeds accelerate. At the same time, AI-enabled configurations are scaling quickly at an 8.55% CAGR, delivering robustness to variable lighting, shape deformation, and overlapping features that confound rule-based scripts. The surface vision and inspection equipment market size for AI-enabled systems is projected to reach USD 2.26 billion by 2031, supported by declining inference-engine costs.

3D imaging remains a niche for applications like gearbox housing measurement or aerospace fastener depth validation, but the blend of structured light and neural inference is starting to blur historical boundaries. Suppliers that merge 2D, 3D, and spectral content within unified software suites stand to capture cross-selling premiums in the surface vision and inspection equipment industry.

By Deployment Mode: Real-Time In-Line Systems Maintain the Lead

In-line installations delivered 70.40% of 2025 revenue because they intercept defects before value-adding steps. Direct integration with manufacturing execution systems enables instant reject signals and closed-loop process adjustments. Automotive battery-tab welds, for instance, now undergo 100% visual validation within milliseconds to avert downstream thermal-runaway risk. As line tact times shorten, the business case for continuous vision grows stronger, underpinning core demand for the surface vision and inspection equipment market.

Portable and handheld scanners, however, are forecast to post an 7.98% CAGR thanks to wireless operation and no-fixture designs. Hexagon’s 2024 handheld scanner launch demonstrates demand for rapid, point-of-use dimensional checks during rail-carriage repair and aircraft MRO. Off-line laboratories continue to justify investment where deep analytics or regulatory documentation are obligatory, yet they no longer dictate the bulk of spending.

By Application Industry: Automotive Leads; Energy Transition Spurs Growth

Automotive retained a 26.40% contribution in 2025, leveraging machine vision for paint integrity, panel-gap measurement, and power-electronics solder joint verification. Regulatory pushes toward Advanced Driver-Assistance Systems (ADAS) calibration further lift image-sensor demand on final assembly lines. Accordingly, the surface vision and inspection equipment market remains tightly coupled to global light-vehicle output.

Battery and solar manufacturing, by contrast, is expanding at a 9.25% CAGR as ESG mandates demand traceable quality metrics. Thin-film defect mapping and electrode alignment are critical to lifetime performance; vision-guided robotics therefore occupy every process stage from coating to pack assembly.Electronics, medical devices, food packaging, and logistics each contribute incremental diversification, ensuring revenue resilience across economic cycles.

Geography Analysis

Asia Pacific captured 38.40% of global revenue in 2025, powered by large-scale electronics and auto supply chains in China, Japan, and South Korea. Chinese machine-vision vendors benefited from ≥30% sales growth in 2024 as state policies reinforced “smart manufacturing” imperatives. South Korea’s robot density of 1,012 units per 10,000 workers illustrates the region’s appetite for automation hardware that embeds intelligent optics.

Europe and North America retain robust demand lines anchored in aerospace, semiconductor front-end, and regulated medical-device sectors that justify premium pricing. The surface vision and inspection equipment market size for North America is forecast to approach USD 1.92 billion by 2031 as electrification and printed-electronics projects proliferate. Manufacturers also value proximity to high-service vendors to navigate integration complexity.

South America is the fastest-growing territory with an 8.16% CAGR, underpinned by Brazil’s modernization agenda and Argentina’s push into automotive and agricultural-equipment exports. Battery and solar investments in Chile and Brazil offer fresh landing zones for vision suppliers. Although Middle East & Africa remains an emerging prospect, rising pharmaceutical production in Saudi Arabia and UAE is laying foundations for future uptake.

Competitive Landscape

The surface vision and inspection equipment market shows moderate fragmentation. Market leaders—Cognex, Keyence, and Omron—leverage integrated hardware-software ecosystems, creating high switching costs and reinforcing customer lock-in. Their combined installed base enables data network effects that feed algorithm refinement, a critical differentiator as AI surpasses rules-based logic.

Strategic mergers are accelerating. AMETEK’s USD 40 million Virtek buyout broadens its footprint in laser-guided assembly while Zebra Technologies’ planned purchase of Photoneo grants immediate entry to area-scan 3D depth capture. Partnerships between software specialists and sensor manufacturers, such as Visionary.ai and Innoviz, demonstrate that competitive advantage is migrating toward full-stack, perception-plus-compute solutions.

Edge-compute architectures are becoming table stakes, evidenced by Endress+Hauser’s collaboration with Sick to embed analytics inside flow-measurement devices. Suppliers that orchestrate hardware, firmware, and spectral analytics within secure, open APIs can secure double-digit service margins even as component ASPs trend lower.

Surface Vision & Inspection Equipment Industry Leaders

Omron Corporation

Cognex Corporation

Isra Vision AG

Panasonic Corporation

Keyence Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Wabtec Corporation announced its acquisition of Evident's Inspection Technologies division for USD 433 million in projected 2024 revenue, expanding its addressable market from USD 8 billion to USD 16 billion while enhancing capabilities in non-destructive testing and remote visual inspection.

- January 2025: Zebra Technologies announced its intention to acquire Photoneo, a leader in 3D machine vision solutions, to enhance its portfolio in the rapidly growing 3D vision market.

- January 2025: Onto Innovation secured a USD 69 million volume purchase agreement with a leading DRAM manufacturer for its optical metrology ecosystem, including the Iris G2 system designed for ultra-thin multilayer films.

- January 2025: Sick AG and Endress+Hauser formed a strategic partnership creating 'Endress+Hauser Sick GmbH+Co. KG' to enhance process automation and develop solutions for industry decarbonization.

Global Surface Vision & Inspection Equipment Market Report Scope

The global surface vision & inspection equipment market is segmented by component, application, and geography.By component, the market studied is segmented into camera, lighting equipment, optics,frame grabber, and hardware & software. By application, the market studied is segmented intoautomotive, electrical & electronics, medical & pharmaceuticals, food & beverages, postal & logistics, metal, and others. Spare parts offered as a part of maintenance are not considered in the scope of the study. The scope of the report covers detailed information regarding the major factors influencing the surface vision & inspection equipment market suchas drivers and restraints.The study also focuses on various trends in the market, such as the increasing adoption of Industrial 4.0 and IoT, and its effects on the market.

| Camera |

| Lighting Equipment |

| Optics |

| Frame Grabbers and Processors |

| Software |

| Other Components |

| 2D Vision Systems |

| 3D Vision Systems |

| AI-enabled Vision Systems |

| In-line / On-line Inspection |

| Off-line Inspection |

| Portable / Hand-held Systems |

| Automotive |

| Electrical and Electronics |

| Semiconductor and PCB |

| Medical and Pharmaceuticals |

| Food and Beverage and Packaging |

| Metals and Paper |

| Postal and Logistics |

| Other Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | GCC |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Camera | ||

| Lighting Equipment | |||

| Optics | |||

| Frame Grabbers and Processors | |||

| Software | |||

| Other Components | |||

| By System Type | 2D Vision Systems | ||

| 3D Vision Systems | |||

| AI-enabled Vision Systems | |||

| By Deployment Mode | In-line / On-line Inspection | ||

| Off-line Inspection | |||

| Portable / Hand-held Systems | |||

| By Application Industry | Automotive | ||

| Electrical and Electronics | |||

| Semiconductor and PCB | |||

| Medical and Pharmaceuticals | |||

| Food and Beverage and Packaging | |||

| Metals and Paper | |||

| Postal and Logistics | |||

| Other Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | GCC | |

| Turkey | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the surface vision and inspection equipment market?

The market generated USD 5.09 billion in 2026 and is projected to reach USD 7.46 billion by 2031.

Which region holds the largest share of the surface vision and inspection equipment market?

Asia Pacific led with 38.40% of global revenue in 2025, driven by large-scale electronics and automotive manufacturing.

Which component segment is expanding the fastest?

AI-enabled vision systems are forecast to grow at a 9.08% CAGR, outpacing all other components through 2031.

Why are battery and solar production lines important for future demand?

ESG mandates require 100% inspection to minimize waste and guarantee safety, pushing battery and solar factories to adopt advanced vision at a 9.25% CAGR.

What is the main restraint hindering wider adoption?

The shortage of skilled vision engineers and the complexity of integrating AI systems with legacy production lines remain the biggest inhibitors to market growth.

How are vendors responding to high upfront system costs?

Equipment-as-a-Service and pay-per-inspection models are emerging, allowing manufacturers to convert capital expenditure into operating expense and de-risk technology adoption.

Page last updated on: